DODGEVILLE, Wis., July 13, 2026 (GLOBE NEWSWIRE) — Lands’ End, Inc. (Nasdaq: LE) today reported that it made the following inducement grants to Charlie Cole on July 13, 2026, in connection with his commencement of employment and appointment as Chief Executive Officer. The grants were not made under a shareholder approved equity plan and were previously described in a Current Report on Form 8-K filed by Lands’ End with the Securities and Exchange Commission on June 30, 2026.

Mr. Cole’s inducement grants consist of an inducement sign-on grant of 109,361 restricted stock units, payable in the form of shares of Lands’ End, Inc. common stock (“Common Stock”), and an inducement sign-on grant of options to purchase up to 166,018 shares of Common Stock at an exercise price equal to $11.43 per share, which in each case will vest 25%, 25% and 50% per year, on, respectively, the first three anniversaries of Mr. Cole’s July 13, 2026 start date, subject to his satisfaction of vesting conditions.

About Lands’ End, Inc.

Lands’ End, Inc. (NASDAQ:LE) is a leading digital retailer of solution-based apparel, swimwear, outerwear, accessories, footwear, home products and uniforms. Lands’ End offers products online at www.landsend.com, through third-party distribution channels and our own Company Operated stores. Lands’ End also offers products to businesses and schools, for their employees and students, through the Outfitters distribution channel. Lands’ End is a classic American lifestyle brand that creates solutions for life’s every journey.

CONTACTS

Lands’ End, Inc. Bernard McCracken Chief Financial Officer (608) 935-4100

Investor Relations: ICR, Inc. Tom Filandro (646) 277-1235 [email protected]

What was once one of the most high-profile partnerships in technology has turned into one of its most explosive legal battles. Apple filed a federal trade secret lawsuit against OpenAI on July 10 in the Northern District of California, alleging that the AI company orchestrated a systematic campaign to steal confidential hardware designs, supplier information, and product specifications through former Apple employees. The complaint also names io Products, the hardware design firm co-founded by former Apple design chief Jony Ive that OpenAI acquired last year.

The allegations are not subtle. Apple’s filing describes a coordinated effort at every level of OpenAI’s organization to acquire proprietary information about unreleased Apple hardware products. The two former employees at the center of the case are Tang Tan, who served as a vice president at Apple before becoming OpenAI’s Chief Hardware Officer, and engineer Chang Liu, who Apple alleges departed with an unreturned company laptop and exploited a software bug that gave him continued access to Apple’s internal file servers after his departure. Apple further claims that OpenAI interviewers encouraged job candidates to bring Apple prototypes and physical components to interviews as part of the hiring process.

OpenAI has denied the allegations, stating that the company has no interest in other companies’ trade secrets and remains focused on building its own technology.

From Partners to Adversaries

The lawsuit represents a dramatic reversal in the relationship between the two companies. As recently as mid-2025, Apple and OpenAI were working together to integrate ChatGPT into Apple’s software platforms and Siri digital assistant. That partnership has since dissolved entirely. In January 2026, Apple announced it was turning to Google for its Apple Intelligence initiatives, and the companies have been moving in increasingly competitive directions ever since, particularly in the emerging AI hardware device market.

The timing of Apple’s filing is significant for reasons beyond the legal merits. OpenAI confidentially filed for an IPO earlier this summer at a reported valuation of $730 billion to $850 billion, with Goldman Sachs and Morgan Stanley leading the offering. A trade secret lawsuit of this magnitude, filed by the most valuable company in the world, introduces material uncertainty into that process. Discovery alone could force OpenAI to disclose internal communications and hardware development timelines that it would strongly prefer to keep private during a pre-IPO quiet period.

The Three-Way AI Rivalry Deepens

The Apple-OpenAI conflict does not exist in isolation. It is playing out against the backdrop of an intensifying three-way rivalry between Apple, OpenAI, and SpaceX, whose CEO Elon Musk co-founded OpenAI before leaving and eventually launching the competing xAI platform. Musk weighed in immediately after the lawsuit was filed, and the public back-and-forth between Musk and OpenAI CEO Sam Altman escalated over the weekend as both companies simultaneously released competing AI models.

SpaceX completed its record $75 billion IPO in June and is pursuing a $60 billion acquisition of AI coding company Cursor. OpenAI is preparing its own public offering. Apple is navigating a CEO transition as Tim Cook prepares to step down later this year. All three companies are competing aggressively for AI talent, hardware capabilities, and market positioning at the same time.

What It Means for the Broader AI Ecosystem

For investors tracking the AI sector, particularly smaller companies operating in the hardware, semiconductor, and AI infrastructure space, the Apple-OpenAI dispute carries practical implications. If the lawsuit slows or disrupts OpenAI’s hardware ambitions, the competitive landscape for AI device development shifts. Smaller companies building AI edge hardware, consumer AI devices, and specialized components could find themselves operating in a market where one of the most well-funded competitors is legally constrained from executing its product roadmap on the original timeline.

The AI hardware race just became a legal battle. How it resolves will shape competitive dynamics across the sector for years.

NEW YORK, July 06, 2026 (GLOBE NEWSWIRE) — Xcel Brands, Inc. (NASDAQ: XELB), a leading media and consumer products company specializing in influencer-led brands through social commerce and livestream shopping, today announced a licensing agreement with KBL Group for OFF/DUTY by Coco Rocha, the elevated fashion and accessories brand created in collaboration with internationally recognized supermodel, entrepreneur, educator, and fashion icon Coco Rocha.

Under the agreement, KBL Group will serve as the production partner for OFF/DUTY by Coco Rocha’s ready to wear collections, leveraging their expertise in sourcing, product development, manufacturing, and supply chain management to bring the brand’s vision to life. The partnership will support the continued growth of OFF/DUTY by Coco Rocha as the brand expands its fashion offerings across multiple retail distribution channels.

OFF/DUTY by Coco Rocha was created to reflect the realities of modern life, offering elevated wardrobe essentials designed for women constantly on the move. Inspired by the pieces Coco has relied on throughout her two-decade career of fashion weeks, international travel, business meetings, and family life. The brand delivers stylish, versatile, and functional pieces that seamlessly transition from day to night.

“KBL Group brings exceptional expertise in product development and manufacturing, making them an ideal partner for OFF/DUTY by Coco Rocha,” said Robert W. D’Loren, Chairman and Chief Executive Officer of Xcel Brands. “As we continue to build the brand, having a best-in-class partner capable of executing Coco’s vision with the highest standards of quality and craftsmanship is critical. We are excited to work together to create collections that resonate with today’s modern consumer.”

David Guisinger, Chief Executive Officer of KBL Group, added, “We are proud to partner with XCEL Brands and OFF/DUTY by Coco Rocha to bring a modern approach to dressing that is both aspirational and accessible. Coco’s authentic point of view and deep understanding of how women dress today have created a powerful foundation for the brand. By combining XCEL’s innovative approach to brand building with KBL’s expertise in product development, sourcing and execution, we are creating a meaningful lifestyle brand that reflects today’s consumer, confident, versatile and effortlessly sophisticated, while developing growth opportunities across multiple channels of distribution.”

About Xcel Brands

Xcel Brands, Inc. (NASDAQ: XELB) is a media and consumer products company engaged in the design, licensing, marketing, live streaming, and social commerce sales of branded apparel, footwear, accessories, fine jewelry, home goods, pet products and other consumer products, and the acquisition of dynamic consumer lifestyle brands. Xcel was founded in 2011 with a vision to reimagine shopping, entertainment, and social media as social commerce. Xcel is an industry leader in developing influencer led brands and owns the Halston and C. Wonder brands, as well as the co-branded influencer led brands Tower Hill by Christie Brinkley, Trust. Respect. Love by Cesar Millan, GemmaMade by Gemma Stafford and OFF/DUTY by Coco Rocha brand and holds a long-term license agreement in Mesa Mia by Jenny Martinez. Xcel also owns and manages the Longaberger by Shannon Doherty brand through its controlling interest in Longaberger Licensing, LLC. Xcel is pioneering a modern consumer products sales strategy which includes the promotion and sale of products under its brands through interactive television, digital live-stream shopping, social commerce, brick-and-mortar retailers, and e-commerce channels to be everywhere its customers’ shop. The company’s previously owned and current brands have generated more than $5 billion in retail sales via livestreaming in interactive television and digital channels alone and has over 20,000 hours of content production time in live-stream and social commerce. The brand portfolio reaches more than 46 million social media followers with broadcast reaching 200 million households. Headquartered in New York City, Xcel Brands is led by an executive team with significant live streaming, production, merchandising, design, marketing, retailing, and licensing experience, and a proven track record of success in elevating branded consumer products companies. For more information, visit www.xcelbrands.com.

KBL Group is a globally-focused fashion brand development and sourcing partner that supports retailers and designers at every stage of the product lifecycle. With a legacy that traces back to 1985, KBL has evolved into a strategic extension of its clients’ teams, blending market insight, creative design and international supply chain execution into comprehensive brand solutions. Today, KBL Group operates with an integrated presence in New York and Hong Kong, aligning it’s global expertise to help fashion and lifestyle brands navigate a competitive, rapidly-changing marketplace.

Coco Rocha is an internationally recognized supermodel, entrepreneur, educator, author, mentor, and advocate. Often referred to as the “Queen of Pose,” she has spent more than two decades at the forefront of the fashion industry, appearing on hundreds of magazine covers, walking for the world’s leading luxury brands, and starring in major global advertising campaigns.

Beyond modeling, Rocha has built a successful business career spanning fashion, education, television, and digital media. She is the founder of Coco Rocha Model Camp, where she has mentored thousands of aspiring and professional models from around the world, and currently serves as mentor and host of Project Runway Canada. Known for combining creativity, entrepreneurship, and education, Rocha continues to shape the future of fashion while inspiring audiences through her work as a businesswoman, mentor, and mother.

The US labor market showed signs of cooling Wednesday morning, and the timing could not be more consequential. Private employers added just 98,000 jobs in June according to ADP’s monthly payroll report, falling well short of the 120,000 economists had anticipated. The miss comes one day before the government’s official employment situation report, which is expected to show a gain of approximately 115,000 positions and is being released Thursday rather than Friday due to the July 4 holiday market closure.

After months of surprisingly strong job gains that helped keep the Federal Reserve locked in a hawkish posture, the June ADP number introduces a new variable into the rate conversation at precisely the moment investors needed clarity most.

What the Data Actually Shows

The 98,000 figure represents a meaningful deceleration from May’s revised 122,000 and an even sharper slowdown from the blowout 172,000 gain reported in the government’s May payroll data. ADP’s chief economist described the report as reflecting a labor market caught between two forces: workers are taking longer to find new positions, while certain industries are simultaneously running into labor supply constraints. The net effect is a slowdown in job creation that is neither a collapse nor a continuation of the strength that characterized the spring.

Other labor market indicators released this week paint a slightly more constructive picture. Layoff announcements fell in June, and job openings for May came in stronger than economists had predicted at 7.6 million. But hiring activity itself remained weak, reinforcing a pattern the Federal Reserve’s Beige Book described last month as a “low-hire, low-fire environment” in which companies are holding headcount steady rather than expanding.

Why Thursday Matters More

The ADP report is a useful directional signal, but the government’s nonfarm payrolls report is the data point the Fed actually uses in its policy deliberations. Thursday’s number will land less than two weeks after Fed Chair Kevin Warsh’s first FOMC meeting, where the committee dropped its easing bias and signaled through its dot plot that nine of 18 officials expect at least one rate hike before year-end.

A strong Thursday print would reinforce that hawkish posture and keep rate hike probabilities elevated. A miss particularly one that aligns with ADP’s softening signal — would complicate the committee’s case for tightening and could mark the first meaningful crack in the “higher-for-longer” narrative that has dominated rate expectations since March.

The Small Cap Implications

For companies in the sub-$2 billion market cap space, the difference between those two outcomes is material. Small and microcap companies carry disproportionately more variable-rate debt than their large cap counterparts, making them acutely sensitive to shifts in rate expectations. A labor market that is genuinely cooling gives the Fed room to hold rather than hike, which would be a direct and immediate benefit to smaller balance sheets that have been absorbing elevated borrowing costs all year.

At the same time, a slowing labor market carries its own risk for consumer-facing small caps. Fewer jobs means less consumer spending power, and the companies most exposed to discretionary spending: restaurants, specialty retail, travel, and leisure feel that pressure faster than most. The staffing and employment services sector, where several smaller publicly traded companies operate, is also a direct read on hiring trends.

Wednesday’s ADP report is a warning flare, not a verdict. Thursday morning’s number is the one that will actually move the Fed’s thinking, the bond market, and the cost of capital for every small company in America.

For most of 2026, the case for a market broadening beyond a handful of mega cap technology names has been a thesis. As of this week, it is becoming a reality. A global technology selloff intensified Friday, dragging the Nasdaq toward its fourth consecutive session of losses, while the parts of the market that had been overlooked for months quietly moved in the opposite direction. The Dow Jones Industrial Average touched a fresh all-time intraday high this week. And the Russell 2000, the benchmark for small cap stocks, pushed toward the 3,000 level after months of underperformance.

This is the rotation. And the data underneath it suggests it may have staying power.

What’s Driving the Move

The catalyst on the surface is weakness in technology. Apple and Microsoft both fell after announcing price increases on consumer hardware tied to rising memory costs, a reported delay in OpenAI’s IPO rattled sentiment around AI valuations, and a sharp selloff in Asian tech markets — South Korea’s KOSPI triggered a circuit breaker after an 8% intraday drop — spilled into US trading. Investors are reassessing whether the largest technology companies can justify the valuations the market assigned them during the AI rally.

But the more important story is where the money is going, not just what it’s leaving. Underneath the tech weakness, market breadth is expanding meaningfully. By late Thursday, 63% of S&P 500 stocks were trading above their 50-day moving average, up from 50% at the start of June. Advancing stocks have consistently outnumbered decliners even on down days for the index. And the correlation between the cap-weighted and equal-weighted versions of the S&P 500 has fallen to its lowest level since 2003 — a technical signal that the market is no longer moving in lockstep with a few giant names.

The Tailwinds Beneath Small Caps

Several forces are converging to support the move into smaller, more domestically focused companies. The 10-year Treasury yield has dropped below 4.5% as oil prices retreat on the easing Iran conflict, lowering borrowing costs for the smaller companies that carry disproportionately more variable-rate debt. The Russell 2000 has surged roughly 21% in 2026 while the S&P 500 has added less than 10%, and the valuation gap between the two remains near its widest level in over two decades.

The breadth of the rally is visible across exactly the kinds of sectors that had been left behind. Industrials and domestic manufacturers — names ranging from blue-chip Caterpillar down to smaller players like FreightCar America and Titan International — sit directly in the path of the onshoring and infrastructure investment themes driving the broadening. Consumer-facing companies such as ONE Group Hospitality and energy producers including Alliance Resource Partners operate in corners of the market that benefit when capital rotates away from crowded technology positioning and toward businesses with tangible cash flows and reasonable multiples.

What Comes Next

The question now is durability. If Treasury yields continue declining and oil stays contained, the conditions supporting the rotation strengthen. If tech stabilizes and reclaims leadership, the broadening could stall as it did in March and April. But the structural case for small caps — historic valuation discounts, improving earnings growth, and domestic revenue exposure — has been intact all year. What changed this week is that the market finally started pricing it in. For investors who positioned early, the rotation they have been waiting for is no longer a forecast. It is happening in real time.

The inflation data the Federal Reserve cares about most just delivered an unwelcome surprise. The Personal Consumption Expenditures price index — the gauge the FOMC uses to measure progress toward its 2% target — rose to its highest level in three years in May, according to data released Thursday. The reading keeps the prospect of a 2026 interest rate hike firmly in play and complicates the path forward for a central bank already navigating one of the most difficult macro environments in years.

Headline PCE climbed to 3.5% year over year, up from the prior month and the highest since 2023. Core PCE, which strips out volatile food and energy costs and is the measure policymakers watch most closely, also accelerated. The data confirms what last month’s Consumer Price Index reading had already suggested: inflation is not cooling on the timeline markets had hoped for, and the energy-driven spike from the US-Iran conflict has bled into the broader price picture.

Why This Keeps a Hike in Play

The report lands just over a week after new Federal Reserve Chair Kevin Warsh presided over his first FOMC meeting, where the committee held rates steady but dropped its long-standing easing bias and signaled through its updated projections that nine of 18 officials now expect at least one rate hike before year-end. Thursday’s PCE reading strengthens that hawkish case considerably. Markets are now pricing in elevated odds of a rate increase in the second half of 2026 — a dramatic reversal from the rate cuts that were consensus just a few months ago.

For the Fed, the data presents a genuine dilemma. Inflation is accelerating while consumer sentiment recently hit an all-time low and growth signals have been mixed. That combination raises the specter of stagflation — the most difficult environment for any central bank to manage, and one with outsized consequences for smaller, rate-sensitive companies.

Where the Pressure Lands

The companies most exposed to this environment are consumer-facing businesses and those carrying significant variable-rate debt. When inflation erodes real household purchasing power, discretionary spending on dining, travel, apparel, and other non-essentials is typically the first to contract — pressuring the smaller consumer-facing companies that lack the pricing power and balance sheet depth of their large cap peers.

Energy sits on the other side of the equation. As the primary driver of May’s inflation spike, elevated energy prices that squeeze consumers can simultaneously support revenues for oil, gas, and energy infrastructure producers. That divergence is part of what makes the current inflation picture so difficult for the Fed to address with a single policy lever — the same force hurting one part of the economy is helping another.

What Comes Next

The PCE reading sets up a tense second half of the year. If energy prices continue easing as the Iran ceasefire holds and oil retreats below $75, the inflation picture could improve meaningfully in the coming months, giving the Fed room to hold rather than hike. If price pressures prove stickier and spread further into core categories, the case for a hike strengthens with each data release.

For small and microcap investors, the message is to watch the inflation trajectory as closely as the Fed itself. The cost of capital for smaller companies — which carry disproportionately more floating-rate debt than large caps — hinges directly on whether this PCE reading marks a peak or the start of a more troubling trend. Thursday’s number tilted the odds toward caution. The next several data points will determine whether that caution becomes conviction.

Intel (Nasdaq: INTC) stock soared more than 11% Thursday after President Trump posted on Truth Social that Apple has agreed to work with the chipmaker to build its processors. The announcement followed an earlier Wall Street Journal report that the two companies had reached a preliminary agreement under which Intel would manufacture chips for the iPhone maker. Intel declined to comment on the report.

The move caps an extraordinary run for a company that was written off by much of Wall Street barely a year ago. Intel stock has now climbed more than 250% since the start of 2026 and roughly 500% over the past twelve months, making it one of the most dramatic corporate turnarounds in the technology sector.

Why the Apple Report Matters

The significance of a potential Apple partnership is as much symbolic as it is financial. Apple previously relied on Intel chips for its laptops and desktops before abandoning the company in favor of designing its own custom silicon — a high-profile departure that came to symbolize Intel’s competitive decline over the past decade. A renewed manufacturing relationship, even a modest one, would represent a meaningful reversal of that narrative.

Industry analysts have tempered expectations on the initial scope. Early commentary suggests any first agreement would likely involve lower-volume, less critical components rather than Apple’s flagship processors. Intel will need to prove its manufacturing reliability before earning more substantial business. But as analysts noted, the first step is always the hardest — and Intel appears to be taking it.

A Foundry Strategy Finally Paying Off

The Apple report does not exist in isolation. It is the latest in a series of developments validating Intel’s multi-year effort to build out its foundry business — the arm of the company that manufactures chips for third-party customers rather than just for Intel itself. Recent reports indicate Intel will build three million Tensor Processing Units for Google, and that Nvidia is exploring using Intel to fabricate some of its own processors. Earlier this week, Intel announced that its latest 18A-P processor node has entered initial production, a key step toward full-volume manufacturing.

The turnaround effort began under former CEO Pat Gelsinger and has continued under current CEO Lip-Bu Tan, who has focused on aggressive cost-cutting while driving the foundry arm to secure external manufacturing deals. That strategy is now benefiting from favorable industry dynamics. TSMC, the world’s largest chip manufacturer, has been unable to provide enough capacity for all of its customers, forcing fabless chip companies — those without their own manufacturing capabilities — to seek alternative production partners. Intel has emerged as one of the few viable options.

The AI Tailwind Beneath It All

Underpinning the entire Intel story is the AI build-out and a structural shift in chip demand. While graphics processing units remain central to AI data centers, central processing units have become increasingly important as AI firms lean into agentic applications — digital assistants capable of performing tasks on a user’s behalf. As AI agents begin running more operations across networks, they increasingly rely on CPUs to complete requests, a segment where Intel holds genuine strength.

For investors tracking the broader semiconductor ecosystem, Intel’s resurgence carries a wider signal. The capacity constraints pushing major customers toward Intel are the same constraints reshaping the entire chip supply chain. Smaller semiconductor companies, specialty foundry service providers, and advanced packaging firms operating in adjacent parts of that supply chain are positioned within the same demand environment driving Intel’s recovery. When the largest chip customers cannot get enough capacity from the dominant manufacturer, the effects ripple across the entire sector — and the smaller companies serving that demand are worth watching closely.

Intel was left for dead a year ago. A 500% move later, the turnaround is no longer a thesis. It is happening.

In one of the more unexpected M&A announcements of the year, Bed Bath & Beyond (NYSE: BBBY) has entered into a definitive agreement to acquire Fathom Holdings (Nasdaq: FTHM), a national technology-driven real estate services platform, in an all-stock transaction. The deal implies an equity value of approximately $53.38 million for Fathom and reflects an exchange ratio of 0.2236 shares of Bed Bath & Beyond common stock for each Fathom share, subject to adjustments at closing. The transaction is expected to close in the second half of 2026, pending Fathom shareholder approval and customary regulatory clearances.

At first glance, a home goods retailer acquiring a real estate brokerage appears to make little sense. The logic becomes considerably clearer once you understand what Bed Bath & Beyond is actually trying to build.

The “Everything Home” Strategy

Bed Bath & Beyond — which operates today as a digital-first brand following its well-documented restructuring and relaunch under the Beyond corporate umbrella — is pursuing a strategy it calls “Everything Home.” The concept is built around three interconnected pillars: Homeownership and Transactions, Omnichannel Commerce, and Home Services. The goal is to own the entire lifecycle of a home, from the moment a consumer buys it, to financing it, to furnishing it, to maintaining it over time.

The Fathom acquisition slots directly into the Homeownership and Transactions pillar. Fathom is not simply a brokerage. It is an integrated platform combining residential real estate brokerage, mortgage origination through Encompass Lending, title services through Verus Title, insurance, and a proprietary cloud-based software platform called intelliAgent. By acquiring Fathom, Bed Bath & Beyond gains an established foothold across the financial and transactional side of homeownership that it could not easily build organically.

The Cross-Selling Thesis

The strategic appeal is the connection point between buying a home and furnishing one. Bed Bath & Beyond’s core business is selling products for the home. Fathom’s business is helping people buy and finance those homes. The combination creates a theoretical funnel: reach a consumer at the moment they purchase a home through Fathom’s brokerage and lending operations, then convert that same consumer into a furnishing and home goods customer through Bed Bath & Beyond’s omnichannel commerce platform.

Fathom, for its part, gains access to Bed Bath & Beyond’s nationally recognized brand, millions of existing customers, and significantly greater capital resources to invest in its technology platform and agent network. For a company with an equity value of roughly $53 million, access to a large consumer brand’s customer base and balance sheet represents a meaningful expansion of reach that would be difficult to achieve independently in the current real estate environment.

Alongside the announcement, Fathom named board member Adam Rothstein as Interim Chief Executive Officer and appointed Daniel Weinmann as Chief Financial Officer, both effective immediately.

The Small Cap Read

For investors tracking the small and microcap space, this deal is worth examining for what it represents rather than just its size. A $53 million all-stock acquisition is small by absolute standards, but it reflects a broader theme: companies are increasingly pursuing platform strategies that combine previously unrelated business lines around a single customer relationship. Real estate technology, in particular, has faced significant headwinds from elevated mortgage rates and suppressed transaction volumes, making smaller players like Fathom attractive targets for acquirers with complementary customer bases and the capital to support a longer-term vision.

Whether the homeownership-to-furnishing funnel ultimately delivers the cross-selling synergies both companies envision will take time to prove. But the strategic logic — owning the customer across the entire arc of homeownership rather than at a single transaction point — reflects exactly the kind of platform thinking that is driving M&A activity across the consumer economy in 2026.

Robinhood announced Tuesday it will cut approximately 10% of its full-time workforce — roughly 290 jobs — as the commission-free trading platform moves to flatten its organizational structure and operate more efficiently. The stock slipped approximately 1.5% in early trading following the news. The reduction is the latest example of a broad corporate trend that has accelerated through 2026: companies across sectors are aggressively scrutinizing headcount and management layers, even when their underlying businesses are performing well.

The Robinhood cuts are notable precisely because the company is not in distress. Its prediction markets business, anchored by the Rothera exchange, accounted for approximately 10% of total revenue in the first quarter of 2026, and the platform has continued to expand its product offering across crypto, retirement accounts, and event-based trading. This is not a retrenchment driven by weakness. It is a deliberate move to reduce organizational layers and improve operating leverage.

The Pattern Across the Market

Robinhood is not operating in isolation. The “efficiency” wave has become one of the defining corporate themes of 2026. Earlier this year, Intuit announced it would cut roughly 17% of its workforce despite beating earnings estimates. Cisco laid off approximately 4,000 employees as part of an AI-focused restructuring. The common thread connecting these decisions is a recognition that artificial intelligence and automation are changing the calculus around how many people a company actually needs to operate at scale.

Executives across industries are increasingly arguing that flatter organizations with fewer management layers move faster, make decisions more efficiently, and deploy capital more effectively. In many cases, AI tools are explicitly cited as the enabler — automating functions that previously required dedicated headcount and allowing companies to maintain or grow output with smaller teams.

What It Means for Smaller Companies

For investors in the small and microcap space, the efficiency wave carries a dual implication worth thinking through carefully.

On one hand, the trend validates a structural shift that benefits smaller, leaner companies. A startup or small cap company that was always going to operate with a lean team is now competing in an environment where its larger rivals are voluntarily shrinking toward that same operating model. The structural cost advantage that large companies historically held through scale is being partially eroded as AI levels the operational playing field.

On the other hand, the broad-based nature of these workforce reductions is a signal worth monitoring for what it says about the labor market and consumer spending. When profitable companies across multiple sectors simultaneously decide they need fewer workers, it has downstream implications for the consumer-facing small caps whose revenue depends on employed consumers with discretionary income. The May jobs report was strong, but corporate efficiency decisions made today show up in employment data months later.

The efficiency wave is reshaping how companies of every size think about headcount, technology, and operating leverage. For smaller companies, it is simultaneously a competitive opportunity and a macro signal that deserves attention. Robinhood is healthy, growing, and cutting jobs anyway. That combination is the story of corporate America in 2026.

Net Sales Increased 10.5% to $64.0 Million vs. 1Q25

Raises Full Year Fiscal 2026 Guidance

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (Nasdaq: VNCE) (“VNCE” or the “Company”), a global retail platform, today reported its financial results for the first quarter ended May 2, 2026.

Brendan Hoffman, Chief Executive Officer of VNCE said, “We delivered strong first quarter results that demonstrate the powerful momentum we’ve built is not only sustained but accelerating. Net sales grew 10.5%, with direct-to-consumer up 15.6% and wholesale increasing 5.9% demonstrating strength across our entire business. Our strategic investments in customer experience are paying off, fueling double-digit growth in both new and reactivated customers and supporting healthy full-price selling.”

Mr. Hoffman continued, “We’re executing with discipline and precision across our business. The strength we’ve established has carried into the second quarter, reinforcing my confidence in our trajectory. With our strategic foundation firmly in place and a talented team driving product and execution, we are raising our full year guidance and remain focused on driving sustained profitable growth and creating long-term shareholder value.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures.

For the first quarter ended May 2, 2026:

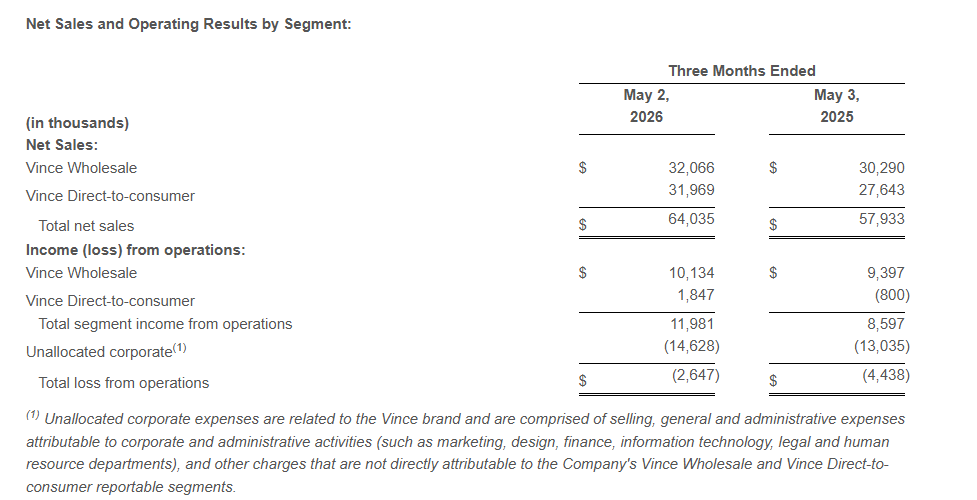

Total Company net sales increased 10.5% to $64.0 million compared to $57.9 million in the first quarter of fiscal 2025. The year-over-year increase was driven by a 15.6% increase in the direct-to-consumer segment and a 5.9% increase in the wholesale segment.

Gross profit was $32.4 million, or 50.6% of net sales, compared to gross profit of $29.2 million, or 50.3% of net sales, in the first quarter of fiscal 2025. The increase in gross margin rate was primarily driven by approximately 130 basis points due to the favorable impact from higher pricing and 100 basis points due to the favorable impact of lower discounting, largely offset by the unfavorable impact of higher tariffs.

Selling, general, and administrative expenses were $35.0 million, or 54.7% of sales, compared to $33.6 million, or 58.0% of sales, in the first quarter of fiscal 2025. The increase in SG&A dollars was primarily driven by higher benefit costs as well as marketing and advertising costs.

Loss from operations was $2.6 million compared to loss from operations of $4.4 million in the same period last year.

Income tax benefit was $0.4 million compared to an income tax expense of $0 in the same period last year. The benefit is due to the impact of applying the Company’s estimated annual effective tax rate to the year-to-date ordinary pre-tax loss.

Net loss was $2.1 million or $(0.16) per share compared to net loss of $4.8 million or $(0.37) per share in the same period last year.

Adjusted EBITDA* was $(1.1) million compared to $(3.0) million in the same period last year.

The Company ended the quarter with 54 company-operated Vince stores, a net decrease of 4 stores since the first quarter of fiscal 2025.

First Quarter Review

Net sales increased 10.5% to $64.0 million as compared to the first quarter of fiscal 2025.

Wholesale segment sales increased 5.9% to $32.1 million compared to the first quarter of fiscal 2025.

Direct-to-consumer segment sales increased 15.6% to $32.0 million compared to the first quarter of fiscal 2025.

Income from operations excluding unallocated corporate expenses was $12.0 million compared to income from operations of $8.6 million in the same period last year.

Balance Sheet

At the end of the first quarter of fiscal 2026, total borrowings under the Company’s debt agreements totaled $29.1 million and the Company had $31.2 million of excess availability under its revolving credit facility.

Net inventory at the end of the first quarter of fiscal 2026 was $70.8 million compared to $62.3 million at the end of the first quarter of fiscal 2025. The year-over-year increase in inventory includes approximately $4.5 million of higher inventory carrying value due to tariffs.

During the quarter ended May 2, 2026, the Company did not make any offerings or sales of shares of common stock under the Virtu At-the-Market Offering. At May 2, 2026, $0.9 million was available under the Virtu At-the-Market Offering.

Outlook

For the second quarter of fiscal 2026 the Company expects the following:

Net sales to increase approximately 10% to 12% compared to the prior year period.

Adjusted operating income as a percentage of net sales to be approximately 6.5% to 7.0%.

Adjusted EBITDA as a percentage of net sales to be approximately 8.0% to 8.5%.

For fiscal 2026 the Company expects the following:

Net sales to increase approximately 7% to 8% compared to the prior year.

Adjusted operating income as a percentage of net sales to be approximately 4% to 4.5%.

Adjusted EBITDA as a percentage of net sales to be approximately 5.5% to 6.0%.

Following the Supreme Court’s decision striking down certain tariffs imposed under the International Emergency Economic Powers Act, (“IEEPA”), the Company’s outlook assumes a 10 percent rate for applicable inventory receipts under Section 122 of the Trade Act of 1974. The Company’s outlook does not consider potential tariff refunds resulting from the Supreme Court’s decision on the IEEPA tariffs.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three months ended May 2, 2026 and May 3, 2025, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, and capitalized cloud computing amortization.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 to this press release.

Conference Call

A conference call to discuss the first quarter results will be held today, June 16, 2026, at 8:30 a.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (833) 461-5787, conference ID 639507707. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail platform that operates the Vince brand women’s and men’s ready-to-wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for everyday effortless style. Vince Holding Corp. operates 41 full-price retail stores, 12 outlet stores, and its e-commerce site, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; general economic conditions; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement relating to the Vince brand with ABG Vince; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

NEW YORK, June 11, 2026 (GLOBE NEWSWIRE) — Xcel Brands (NASDAQ: XELB), an industry-leading media and consumer products company specializing in building influencer led brands through social commerce and livestream shopping, is pleased to announce a new licensing partnership for Trust. Respect. Love by Cesar Millan with licensing partner EcoStrong for product categories that include cleaning products, odor management, shampoo and conditioners.

The partnership will introduce a collection of innovative pet care, pet shampoo, and home cleaning products inspired by Cesar Millan’s philosophy that trust, respect, and love are the foundation of every meaningful relationship between pets and their owners. The collection includes environmentally safe cleaning, grooming, and odor control solutions designed to support healthier homes and happier pets.

“We are excited to partner with EcoStrong as our licensing partner for the Trust. Respect. Love by Cesar Millan. Cesar Millan is one of the most recognized and trusted names in the pet space, and this partnership allows us to expand his philosophy into thoughtfully designed pet care products that align with today’s consumer demand for effective and environmentally safe solutions. EcoStrong’s expertise and innovation in pet safe products make them an ideal partner for this category launch,” said Robert D’Loren, Chairman and Chief Executive Officer of Xcel Brands.

“Cesar Millan has spent his career helping people build stronger relationships with their pets, and his mission aligns perfectly with EcoStrong’s commitment to creating safer, healthier environments for pets and their families,” said Bryan Sims, Chief Executive Officer and President of EcoStrong.

The Trust. Respect. Love by Cesar Millan collection will combine practical everyday functionality with products designed to help pet owners maintain clean and comfortable living environments while also supporting the health and wellness of their pets through premium grooming essentials, including pet shampoos and other pet care products.

“For me, trust, respect, and love are not just words — they are the foundation of every relationship with a dog,” said Cesar Millan. He further stated, “I’m excited to work with EcoStrong Pet Products and Xcel Brands to create products that support healthier homes and happier pets.”

About Cesar Millan Cesar Millan is a world-renowned dog behaviorist with over 25 years of experience transforming relationships between humans and their dogs. As the original host of the hit TV series, the Dog Whisperer, to his most recent Better Human, Better Dog, to his best-selling books and iconic workshops, Cesar has become a trusted guide for millions of dog lovers worldwide. With social media following over 21 million people and a legacy that spans two decades on television around the world, Cesar’s influence extends far and wide. Trusted by celebrities, world leaders, and first-time pet owners alike, Cesar is committed to helping you achieve lasting harmony with your dog. Cesar moves forward in his journey with purpose, and you can follow this journey at www.cesarmillan.com.

About Xcel Brands Xcel Brands, Inc. (NASDAQ: XELB) is a media and consumer products company engaged in the design, licensing, marketing, live streaming, and social commerce sales of branded apparel, footwear, accessories, fine jewelry, home goods, pet products and other consumer products, and the acquisition of dynamic consumer lifestyle brands. Xcel was founded in 2011 with a vision to reimagine shopping, entertainment, and social media as social commerce. Xcel is an industry leader in developing influencer led brands and owns the Halston and C. Wonder brands, as well as the co-branded influencer led brands Tower Hill by Christie Brinkley, Trust. Respect. Love by Cesar Millan, GemmaMade by Gemma Stafford and Off/Duty by Coco Rocha brand and holds noncontrolling interests or long-term license agreement in Mesa Mia by Jenny Martinez. Xcel also owns and manages the Longaberger by Shannon Doherty brand through its controlling interest in Longaberger Licensing, LLC. Xcel is pioneering a modern consumer products sales strategy which includes the promotion and sale of products under its brands through interactive television, digital live-stream shopping, social commerce, brick-and-mortar retailers, and e-commerce channels to be everywhere its customers’ shop. The company’s previously owned and current brands have generated more than $5 billion in retail sales via livestreaming in interactive television and digital channels alone and has over 20,000 hours of content production time in live-stream and social commerce. The brand portfolio reaches more than 46 million social media followers with broadcast reaching 200 million households. Headquartered in New York City, Xcel Brands is led by an executive team with significant live streaming, production, merchandising, design, marketing, retailing, and licensing experience, and a proven track record of success in elevating branded consumer products companies. For more information, visit www.xcelbrands.com.

EcoStrong is one of the fastest-growing consumer brands in the pet care category, known for developing high-performance household and pet care solutions powered by the latest advancements in natural, plant-based, and bio-enzymatic technologies. Its portfolio includes innovative cleaning products, odor eliminators, stain removers, laundry care products, and pet grooming solutions that deliver professional-grade results while maintaining a strong commitment to safety and sustainability. By combining scientific innovation with environmentally responsible product development, EcoStrong helps consumers care for their homes, their pets, and the planet without sacrificing effectiveness.

The 2026 FIFA World Cup officially begins today, June 11, and runs through July 19 across 16 cities in the United States, Canada, and Mexico. It is the largest tournament in the competition’s history — 48 teams, 104 matches, a projected global audience of more than 5 billion viewers, and commercial revenues estimated between $11 billion and $13 billion, up roughly 50% from the 2022 edition in Qatar. The United States is hosting 78 of the 104 matches across 11 cities including New York, Los Angeles, Miami, Dallas, Atlanta, Boston, Houston, and Seattle. The last time the US hosted was 1994 — a generation ago, before smartphones, before streaming, and before legal sports betting existed in virtually any American state.

The scale of what has changed in those 32 years is precisely what makes 2026 different from every prior World Cup as an investment event.

For investors, the question is not whether the World Cup generates economic activity. It clearly does. The question is where that activity concentrates — and which publicly traded companies are positioned to capture a meaningful share of it across a six-week window that begins today.

The Sports Betting Opportunity Is Real and Measurable

The single clearest financial beneficiary of a US-hosted World Cup in 2026 is the domestic sports betting industry — and the timing could not be more favorable. Legal sports betting is now available in 38 US states, compared to just three states when the tournament was last held on American soil. Global betting volumes during the tournament are projected to exceed $50 billion, averaging approximately $500 million per match, up sharply from $35 billion recorded during the 2022 World Cup. In-play wagering and parlay products tied to individual match events are expected to drive the majority of that volume growth.

For smaller publicly traded gaming and sports betting companies, a six-week window of record betting activity on 104 matches is a direct near-term revenue catalyst. Rush Street Interactive, one of the smaller publicly traded sportsbook operators, runs BetRivers across multiple US states and stands to benefit directly from elevated match-day wagering volumes. Regional casino operators with integrated sportsbook offerings in host cities are similarly positioned.

Prediction markets represent a newer layer of exposure. Robinhood’s recently launched Rothera exchange already accounted for approximately 10% of the company’s revenue in Q1 2026, making it one of the more direct plays on the prediction market boom that major sporting events historically accelerate.

The Hospitality Picture Is More Complicated

The economic impact projections for hotel and tourism spending are significant on paper — FIFA and the World Trade Organization project $6.4 billion in tourist spending in the US alone, with the accommodation and food sector identified as the primary beneficiary. However, the American Hotel and Lodging Association reported as recently as May that 80% of US host city hotels say bookings are tracking below those projections, citing visa processing barriers and geopolitical headwinds from the ongoing Iran conflict dampening international travel demand.

That gap between projection and reality is a meaningful qualifier for smaller regional hospitality operators in host cities who may have priced in demand that has not fully materialized. The domestic fan spending story remains more reliable than the international tourism story for this particular tournament, and investors tracking consumer-facing companies in host cities should weigh both sides of that equation carefully.

The Longer Arc

Beyond the six-week tournament window, the structural story is more compelling. Multiple research firms have characterized 2026 as soccer’s cultural inflection point in the United States — the moment the sport transitions from niche followership to mainstream commercial relevance in the largest sports economy in the world. Broadcast rights, digital engagement, merchandise, and youth participation spending all have multi-year trajectories that a successful US-hosted World Cup accelerates in ways that outlast the final whistle on July 19.

For companies in sports media, digital fan engagement, sports data and analytics, and gaming technology, that longer arc may ultimately matter more than the tournament itself. The 32-year wait is over. The commercial machine behind it has never been larger.

SSS. Improving Same Store Sales remains a key focus of management. In the first quarter of 2026, all brands saw sequential SSS growth, with STK reporting positive SSS and Benihana flat SSS. Even the Grill concepts have experienced a significant improvement in SSS over the past three quarters. ONE Group’s focus on providing value, the vibe experience, execution, and targeted marketing is paying dividends in a tough operating environment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.