Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

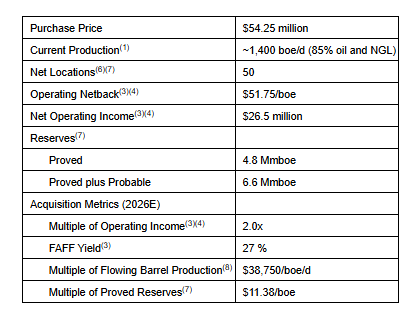

Accretive Strategic Acquisition. InPlay Oil announced the acquisition of a private oil and gas producer for C$54.25 million, adding approximately 1,400 boe/d of oil-weighted production and increasing company-wide production to more than 20,100 boe/d. The acquired assets are contiguous with InPlay’s existing operations, enabling approximately C$2.5 million of annual cost synergies, while adding 50 drilling locations and immediately enhancing adjusted funds flow and free adjusted funds flow on a per-share basis. The transaction is expected to close by the end of August, subject to customary closing conditions. Post-close, InPlay expects to have more than 450 total drilling locations, including approximately 230 Tier-1 locations.

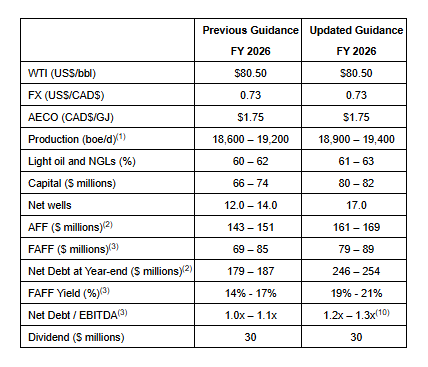

Corporate Guidance. InPlay continues to execute strongly, with recent Cardium wells materially outperforming expectations and being drilled ahead of schedule, allowing InPlay to expand its 2026 drilling program to 17 net wells on a pro forma basis. Reflecting stronger operational performance and the acquisition, management increased 2026 guidance, including adjusted funds flow (AFF) to C$161 million to C$169 million, free adjusted funds flow (FAFF) to C$79 million to C$89 million, and FAFF yield to 19% to 21%, despite higher capital spending of C$80 million to C$82 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

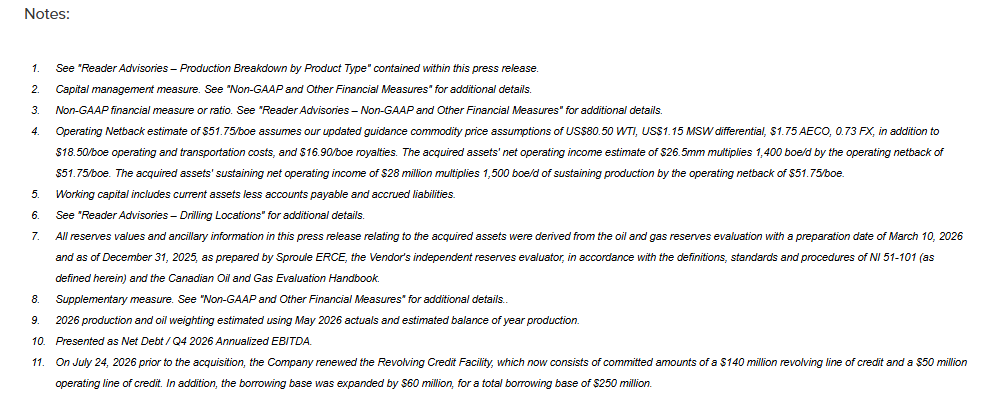

CALGARY, AB, Aug. 5, 2026 /CNW/ — InPlay Oil Corp. (TSX: IPO) (TASE: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) is pleased to announce that it has entered into a definitive agreement today to acquire a private oil and gas producer for cash consideration of $54.25 million, prior to closing adjustments (the “Acquisition“).

The Acquisition supports InPlay’s long-term strategy of building a disciplined and sustainable light oil focused growth company. The Acquisition builds on InPlay’s proven track record of executing highly accretive acquisitions, having successfully completed five strategic acquisitions over the past decade that have helped increase production 10x and grow total proved plus probable reserves 13.5x. The acquired assets are currently producing approximately 1,400 boe/d(1) (85% light oil and NGLs) which will increase InPlay’s production to over 20,100 boe/d(1) (62 – 63% light oil and NGLs), with light oil production expected to increase to over 10,500 bbl/d. The high oil weighting of the acquired assets further enhances InPlay’s strong netbacks, providing meaningful accretion to Adjusted Funds Flow (“AFF“)(2) and Free Adjusted Funds Flow (“FAFF“)(3) on a per share basis. The acquired assets generate strong cash flow and free cash flow which will enhance InPlay’s shareholder return strategy. InPlay is forecasted to generate FAFF of approximately $79 – $89 million for 2026 on a pro forma basis, including only four months for the acquired assets, which equates to a FAFF yield(3) of 20%. InPlay pays a dividend of $0.09 per month ($1.08 per year), which equates to a dividend yield of 7.2%. In addition, InPlay recently implemented a Normal Course Issuer Bid, pursuant to which the Company repurchased 0.5% of basic shares outstanding for cancellation during the month of June.

ACQUISITION HIGHLIGHTS

Highly Accretive Acquisition Metrics: Purchase price represents 2.0x net operating income(3) and 27% FAFF yield; per-share accretion of 18% to both AFF and FAFF on an annualized basis; 12% accretion to oil production per share, and 9% accretion to funds flow per barrel netback.

Enhanced Free Adjusted Funds Flow with Growth Potential: InPlay forecasts the acquired assets require sustaining capital of approximately $12 million to reach and maintain production of approximately 1,500 boe/d. Based on an operating netback(3) of approximately $51.75/boe(4), the acquired assets generate sustaining net operating income(3) of $28 million and FAFF of $16 million prior to accounting for synergies.

Acquired Assets are Contiguous with InPlay Assets Providing Significant Synergies: The acquired assets directly offset the Company’s existing operations and are supported by Company owned and operated facilities and infrastructure, creating meaningful operational synergies and enhancing the efficiency of future development. The Company expects to integrate the acquired assets without adding corporate office personnel. As a result of these synergies, the Acquisition is expected to generate approximately $2.5 million in annual cost savings, with the majority captured immediately post closing.

Expands InPlay’s Belly River Position: Pro forma the Acquisition, InPlay will be producing approximately 2,000 boe/d(1) from the Belly River, which at approximately 85% liquids weighting offers strong netbacks and high rate of return development opportunities.

Sustainability and Drilling Inventory: The acquired assets include 50 identified drilling locations, 75% of which are Tier 1 inventory(6) with expected payouts of less than 1.5 years at US $70/bbl WTI pricing.

“This Acquisition represents another important step in advancing InPlay’s strategy of building a disciplined, sustainable light oil company which includes strategic acquisitions” commented Doug Bartole, President and Chief Executive Officer of InPlay. “While modest in size, the Acquisition is a smart and highly accretive transaction that is expected to generate meaningful value relative to the capital invested. The acquired assets are highly complementary to our existing operations, provide meaningful operating and infrastructure synergies, and add a deep inventory of high-return drilling opportunities within our core area. The Acquisition is expected to be immediately accretive to adjusted funds flow and free adjusted funds flow per share, while maintaining conservative leverage and further enhancing our ability to generate sustainable returns for shareholders.”

ACQUISITION DETAILS

InPlay has entered into an arrangement agreement (the “Arrangement Agreement“) with a privately held arm’s length oil and gas producer (the “Vendor“), to acquire all of the issued and outstanding shares of the Vendor for cash consideration of $54.25 million, prior to closing adjustments. Concurrent with the execution of the Arrangement Agreement, certain shareholders of the Vendor, representing in excess of 72% of the Vendor shares outstanding, have entered into irrevocable written resolutions in support of the Acquisition. The Acquisition is expected to close by the end of August 2026, subject to the satisfaction or waiver of customary closing conditions.

The Acquisition will be funded by a draw on InPlay’s $190 million credit facility, with an expanded borrowing base totalling $250 million(11). Based on pro forma guidance as outlined below, InPlay anticipates Q4-2026 net debt to EBITDA(3) of 1.2x – 1.3x. The Company retains strong financial flexibility including an estimated working capital(5) surplus at June 30, 2026 of approximately $19.4 million and maintains unique access to the Israeli bond and equity markets. InPlay’s series A senior unsecured bonds (which are listed on the Tel Aviv Stock Exchange) are currently trading at a yield to maturity of approximately 6.1% and include a tap feature of approximately $115 million.

The acquired assets are currently producing approximately 1,400 boe/d with the latest well coming on stream in Q1 2026. InPlay plans to drill 2.0 net Belly River wells on the acquired assets post-closing and forecasts the acquired assets will require sustaining capital of approximately $12 million to reach and maintain annual average production of approximately 1,500 boe/d. Based on an operating netback of approximately $51.75/boe, the acquired assets generate sustaining net operating income of $28 million, resulting in sustaining FAFF of $16 million. The acquired assets contain 50 net drilling locations, and subject to supportive commodity prices, the acquired assets are expected to offer strong growth potential in excess of the target sustaining production.

The Acquisition’s purchase price represents approximately 2.0x operating income and is highly accretive to InPlay on both AFF and FAFF per share metrics while maintaining conservative corporate leverage ratios. A summary of the relevant metrics of the Acquisition is as follows:

OPERATIONS UPDATE

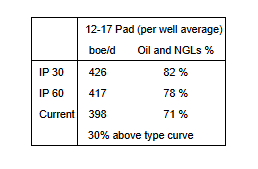

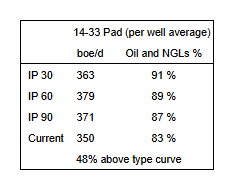

InPlay’s capital program for the second quarter of 2026 consisted of completing and bringing online three gross (3.0 net) Cardium wells in Pembina drilled in the first quarter of 2026, and the drilling and completion of three gross (3.0 net) additional Cardium wells also in Pembina. The most recent three wells were drilled approximately 40 days ahead of schedule, as the Company was able to access the field earlier than is normally anticipated during spring break-up. These wells were brought on production in late May and have materially exceeded internal expectations. Initial production (“IP“) rates for these three wells are as follows:

The three wells drilled in the first quarter continue to deliver strong results ahead of internal expectations. The IP rates for these wells are as follows:

InPlay’s year to date capital program has been completed below budget, resulting in strong capital efficiencies and continuing the “more with less” performance achieved in 2025. Supported by enhanced efficiencies and strong commodity prices, InPlay now plans to drill a total of 15.0 net Cardium wells in 2026, including 7.0 net Cardium wells during the second half of the year, for total capital expenditures of approximately $73 – $74 million, prior to incorporating the expanded pro forma capital program. This compares with InPlay’s original 2026 capital program of $66 million to $74 million, which contemplated the drilling of 12.0 to 14.0 net wells.

Additionally, InPlay plans to drill 2.0 net Belly River wells on the newly acquired assets, bringing the pro forma 2026 drilling program to a total of 17.0 net wells and combined capital expenditures of approximately $80 – $82 million.

In addition, InPlay plans to accelerate its asset retirement closure spend to reduce its decommissioning liability. This increase in asset retirement spending is supported by enhanced FAFF resulting from a more efficient 2026 capital program, stronger commodity prices and an expanded asset base associated with the Acquisition.

UPDATED 2026 PRO FORMA GUIDANCE

InPlay is also updating its previously announced 2026 guidance as follows:

ADVISORS

Burnet, Duckworth & Palmer LLP is acting as legal counsel to InPlay with respect to the Acquisition.

National Bank Financial Inc. (“NBF”) is acting as Exclusive Financial Advisor to the Vendor with respect to the Acquisition. NBF has provided the Vendor with a fairness opinion that the consideration to be received by the shareholders of the Vendor is fair, from a financial point of view, to the shareholders of the Vendor.

An updated corporate presentation will be available on our website in due course. For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0635

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. We have increased our Q2 FY2026 revenue, adjusted funds flow (AFF), and AFF per share estimates to C$122.0 million, C$49.6 million, and C$1.77, respectively, from C$104.0 million, C$36.2 million, and C$1.29. While we have lowered our production estimate to 18,663 barrels of oil equivalent per day (boe/d) from 18,875 boe/d due to Q2 weather impacts, the increases in our estimates are largely due to higher crude oil prices. For FY 2026, we now project revenue, AFF, and AFF per share of C$425.6 million, C$162.5 million, and C$5.80, respectively, compared to our prior estimates of C$406.2 million, C$148.4 million, and C$5.29. Our FY 2026 average production forecast of 18,900 boe/d is unchanged.

Outlook. InPlay has approximately 190 Tier 1 drilling locations that provide an estimated 10 to 15 years of high-return inventory. The company’s low-decline asset base supports sustainable free cash flow generation while limiting capital requirements needed to maintain production. Conservative leverage provides capacity for future acquisitions while maintaining shareholder returns through the dividend.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

HOUSTON, July 30, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit”, “SMC” or the “Company”) announced today that it will report operating and financial results for the second quarter of 2026 on Monday, August 10, 2026, after the close of trading on the New York Stock Exchange.

Second Quarter 2026 Earnings Call

SMC will host a conference call at 10:00 a.m. Eastern on August 11, 2026, to discuss its quarterly operating and financial results. The call can be accessed via teleconference at: Q2 2026 Summit Midstream Corporation Earnings Conference Call (https://register-conf.media-server.com/register/BI8cebf785fce846a9bb80ae80660d3cbc). Once registration is completed, participants will receive a dial-in number along with a personalized PIN to access the call. While not required, it is recommended that participants join 10 minutes prior to the event start. The conference call, live webcast and archive of the call can be accessed through the Investors section of SMC’s website at www.summitmidstream.com.

About Summit Midstream Corporation

SMC is a value-driven corporation focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in the core producing areas of unconventional resource basins, primarily shale formations, in the continental United States. SMC provides natural gas, crude oil and produced water gathering, processing and transportation services pursuant to primarily long-term, fee-based agreements with customers and counterparties in five unconventional resource basins: (i) the Williston Basin, which includes the Bakken and Three Forks shale formations in North Dakota; (ii) the Denver-Julesburg Basin, which includes the Niobrara and Codell shale formations in Colorado and Wyoming; (iii) the Fort Worth Basin, which includes the Barnett Shale formation in Texas; (iv) the Arkoma Basin, which includes the Woodford and Caney shale formations in Oklahoma; and (v) the Piceance Basin, which includes the Mesaverde formation as well as the Mancos and Niobrara shale formations in Colorado. SMC has an equity method investment in Double E Pipeline, LLC, which provides interstate natural gas transportation service from multiple receipt points in the Delaware Basin to various delivery points in and around the Waha Hub in Texas. SMC is headquartered in Houston, Texas.

Forward-Looking Statements

This press release includes certain statements concerning expectations for the future that are forward-looking within the meaning of the federal securities laws. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements and may contain the words “expect,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result,” and similar expressions, or future conditional verbs such as “may,” “will,” “should,” “would” and “could.” In addition, any statement concerning future financial performance (including future revenues, earnings or growth rates), payment of dividends on any series of stock, ongoing business strategies and possible actions taken by SMC or its subsidiaries are also forward-looking statements. Forward-looking statements also contain known and unknown risks and uncertainties (many of which are difficult to predict and beyond management’s control) that may cause SMC’s actual results in future periods to differ materially from anticipated or projected results. An extensive list of specific material risks and uncertainties affecting SMC is contained in its 2025 Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 16, 2026, as amended and updated from time to time. Any forward-looking statements in this press release are made as of the date of this press release and SMC undertakes no obligation to update or revise any forward-looking statements to reflect new information or events.

Magnolia Oil and Gas (NYSE: MGY) announced Monday it has entered into a definitive purchase agreement to acquire WildFire Energy for approximately $4.06 billion, marking the largest acquisition in the company’s history and one of the most significant domestic upstream deals of 2026. WildFire, backed by private equity firms Warburg Pincus and Kayne Anderson, operates in the same South Texas basin where Magnolia has built its entire business, making this a pure concentration play rather than a diversification move.

Under the terms of the agreement, WildFire owners will receive 32.2 million shares of Magnolia’s Class A common stock, and Magnolia will assume $600 million in outstanding notes due in 2029. The transaction is expected to close in late Q3 2026. Committed financing has been arranged through JPMorgan Chase and Citigroup.

What Magnolia Is Actually Getting

The deal goes well beyond additional drilling locations. WildFire’s assets are concentrated in the Eagle Ford Shale and Austin Chalk formations in the Giddings area of South Texas, directly adjacent to and overlapping with Magnolia’s existing operations. That geographic overlap is central to the deal thesis because it allows Magnolia to integrate the acquired production into its existing infrastructure with minimal incremental investment.

Two components of the transaction stand out from a typical upstream acquisition. First, the deal includes a sand mine that supplies approximately 80% of Magnolia’s current annual sand consumption, including 100% of WildFire’s sand requirements, with additional third-party sales on top. Controlling your own frac sand supply in a market where sand costs represent a meaningful share of well completion expenses is a structural cost advantage that compounds over every well drilled.

Second, the transaction includes more than 500 miles of gas gathering pipelines in the Giddings area. Owning midstream infrastructure rather than paying third-party gathering and processing fees directly improves operating margins on every barrel produced. For investors who follow midstream economics, companies like Summit Midstream Partners understand exactly how valuable that kind of infrastructure control can be at scale.

The Shareholder Return Story

Magnolia is framing this as a free cash flow accretion story above all else. The confidence in the acquired asset quality translated into an immediate 9% increase in the quarterly dividend to $0.18 per share, payable in Q3 2026. The company also reaffirmed its ongoing commitment to repurchasing at least 1% of outstanding shares per quarter.

On the production side, Magnolia reported Q2 total production averaging 106,100 barrels of oil equivalent per day, with D&C capital of $125 million and $296 million of cash on the balance sheet at quarter end. The company raised its full-year 2026 standalone production growth guidance from 5% to 6% alongside the deal announcement.

The Broader E&P Consolidation Signal

For investors tracking domestic energy producers in the small and microcap space, the Magnolia-WildFire combination reinforces a consolidation pattern that has been accelerating throughout 2026. Private equity-backed E&P companies that built significant acreage positions during the downturn are now exiting to public company buyers at scale. The acquirers with the strongest balance sheets, the lowest cost structures, and the most disciplined capital allocation frameworks are the ones winning the assets.

That dynamic creates a dual opportunity for smaller energy names. Companies like InPlay Oil and Gas and Alliance Resource Partners that operate with similar discipline in their respective basins represent the kind of focused, well-run operators that either benefit from the same elevated pricing environment driving Magnolia’s economics or become attractive consolidation targets themselves as the deal cycle continues.

The brief window of optimism that followed the US-Iran ceasefire is closing fast. Oil shipments through the Strait of Hormuz, which had recovered to roughly 50% of pre-war levels under the June 17 memorandum of understanding, have fallen sharply over the past week as the ceasefire arrangement fell apart and active fighting resumed between US and Iranian military forces. According to Goldman Sachs, flows through the strait have dropped back to an estimated 3 to 5 million barrels per day, down from approximately 10 million barrels per day in early July.

The reversal leaves the global oil market short roughly 13.4 million barrels per day of Gulf supply, a deficit that is already showing up at the pump and in the price of crude. Brent crude has jumped more than 8% over the past five trading sessions to trade back above $84 per barrel. WTI has climbed more than 8% to above $79. Both benchmarks are moving in the wrong direction for an economy that had only just begun pricing in a post-war energy recovery.

What Went Wrong

The MOU signed June 17 was supposed to reopen the strait to pre-war commercial traffic within 30 days and establish a framework for broader negotiations. For roughly four weeks, that framework held. Tanker crossings increased, oil prices declined sharply, and the global economy began adjusting to a lower energy cost environment. Gas prices fell below $4 nationally for the first time in months.

That progress has now reversed. US Central Command announced a new wave of strikes against Iranian military targets Wednesday, the fifth consecutive day of US military action in the region. Iran has continued retaliating with attacks against US installations throughout the Gulf. A second US naval blockade of the strait, which began Tuesday evening, has already redirected commercial vessels attempting to transit the waterway. Energy market analysts at Rystad Energy have stated that expectations for near-term flow normalization have failed to materialize, and the latest escalation has further reduced the probability of a recovery in the weeks ahead.

The Small Cap Squeeze Returns

For investors in the sub-$2 billion market cap space, this reversal hits on two fronts simultaneously. The consumer-facing small caps that had only just begun to benefit from lower fuel costs are now watching that relief evaporate. Companies in transportation, logistics, food service, and retail, including names like ONE Group Hospitality and Travelzoo, are right back in the margin compression environment that characterized the spring. Diesel prices, which had been trending lower, are poised to reverse alongside crude if the strait remains effectively closed.

On the other side of the trade, domestic energy producers are seeing the price environment strengthen again. Independent oil and gas operators, including names like InPlay Oil and Alliance Resource Partners, along with midstream players like Summit Midstream Partners, benefit directly from sustained crude prices above $80. The economics for US producers improve at every dollar WTI moves higher, and the re-escalation removes the near-term risk that a permanent peace deal would collapse prices back toward pre-war levels.

Goldman Sachs strategists have cautioned that recovery this time could be slower than the initial post-ceasefire rebound, given depleted global inventories and continued shipper reluctance to route through the region even via Omani waters. China, the world’s largest crude importer, had reduced its intake by 5 million barrels per day during the first phase of the conflict, but that restraint could shift as Gulf producers adjust pricing and Beijing reassesses its long-term stockpile strategy.

The ceasefire was supposed to be the beginning of the end. Instead, the strait is closing again, and the energy cost pressure that defined the first half of 2026 is threatening to define the second half as well.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating coverage with an Outperform rating. We are initiating coverage on VivoPower International PLC (NASDAQ: VIVO) with an Outperform rating and $10 Price target. The company has recently pivoted toward acquiring and developing power-secured land and powered-shell data center infrastructure, targeting one of the most constrained inputs in the AI value chain: grid-connected power capacity.

Capital-Light Business Model. The company occupies an upstream position within the AI data center value chain. Rather than owning and operating IT infrastructure, it seeks to generate returns through land development, power procurement, and long-term leasing arrangements. In our view, this model provides exposure to AI infrastructure demand while reducing technology and operating risks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent drilling results. Power Metallic Mines reported additional assay results from its Winter 2026 drilling program at the Lion Zone, with the results expected to support the company’s initial NI 43-101 Mineral Resource Estimate (MRE), which is scheduled for completion by the end of July. The MRE for both the Lion Zone and the Nisk deposit will provide the foundation for a Preliminary Economic Assessment (PEA) that is expected to begin immediately afterward.

Strong near-surface copper grades. The latest drilling focused on infill holes designed to improve confidence in resource modeling along the western side of the Lion Zone, particularly within a potential future open-pit area. Results continue to demonstrate strong near-surface mineralization, highlighted by Hole PML-26-115, which returned 13.3 meters grading 3.98% copper equivalent (CuEq) beginning just 25 meters below surface, including a higher-grade interval of 3.77 meters grading 9.36% CuEq. Hole PML-26-105 also delivered a strong intercept of 5.26 meters grading 8.45% CuEq at a depth of approximately 140 meters. Both will be included in the upcoming MRE.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The energy shock that defined the spring of 2026 is unwinding, and American consumers are feeling it at the pump just in time for summer. The national average price of regular gasoline fell to $3.99 per gallon Thursday, dropping below the $4 threshold for the first time in months and delivering meaningful relief to households that watched prices climb above $4.50 per gallon only a month ago at the height of the US-Iran conflict.

For the small and microcap companies that spent the spring absorbing elevated fuel costs with limited ability to pass them through, the decline is more than a consumer story. It is the early stage of a margin recovery that could reshape the second half of the year.

What’s Driving the Decline

The catalyst is diplomatic. Following President Trump’s announcement Sunday that Washington and Tehran had agreed to terms on a 60-day memorandum of understanding aimed at ending the three-month conflict and reopening the Strait of Hormuz to commercial traffic, crude oil prices have fallen sharply. Brent crude, the international benchmark, has dropped roughly 13% over the past five trading sessions to trade firmly below $80 per barrel for the first time since the early days of the war. US benchmark WTI crude has fallen even harder, shedding approximately 15% to trade below $75.

The scale of the recovery reflects the scale of the disruption. The shuttering of the Strait of Hormuz removed more than one billion barrels of oil from the global market over three months, creating one of the most severe supply squeezes in years. Gasoline and other crude derivatives, which carry embedded refining costs and are stored in smaller quantities, experienced even more dramatic price swings than crude itself — which is precisely why they are now falling quickly as the supply picture normalizes.

Industry analysts project the national average could head toward $3.70 per gallon in the near term as the Iran agreement takes hold and movement through the strait resumes, with diesel prices expected to fall below $5 per gallon shortly after.

The Small Cap Margin Story

For consumer-facing companies in the sub-$2 billion market cap range, the decline in fuel costs is a direct and measurable tailwind. Throughout the spring, regional trucking companies, last-mile delivery operators, food service businesses, and logistics providers absorbed surging diesel and gasoline costs that compressed already thin operating margins. Unlike large cap peers with hedging programs and pricing power, smaller operators had few options beyond eating the costs or risking demand destruction by raising prices.

That pressure is now reversing. Lower fuel costs flow almost immediately through to the operating expenses of transportation and logistics-dependent companies. Credit card data throughout the spring showed consumers spending an increasing share of their budgets on gasoline while cutting back elsewhere — a dynamic that squeezed discretionary small cap retailers and restaurant operators. As pump prices fall, that discretionary spending capacity returns, potentially benefiting the consumer-facing companies that had been most pressured.

The Caveats Worth Watching

The recovery is not without risk. Gasoline prices remain elevated above prewar levels, and a well-documented market phenomenon often described as “rockets and feathers” means pump prices tend to rise quickly when crude climbs but fall more slowly on the way back down. The timing of the Strait of Hormuz fully reopening remains uncertain, which means oil prices are unlikely to collapse dramatically as summer driving demand builds.

A more immediate threat comes from the weather. Tropical Storm Arthur is expected to impact the US Gulf Coast, home to the nation’s largest refinery complex. With US refineries already running at 97% of capacity according to federal data, any disruption from flooding could squeeze a system operating at its limit and temporarily reverse some of the relief now reaching consumers.

Barring significant storm damage or other disruptions, analysts project national average gasoline prices could fall below $3 per gallon by year-end, with diesel below $4. For the small cap companies that endured the spring squeeze, that would represent a full-circle recovery — and a meaningful tailwind heading into 2027.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

LIFE Offering. Power Metallic Mines closed its previously announced brokered Listed Issuer Financing Exemption (LIFE) offering that raised C$28.2 million in gross proceeds. The company issued 22.583 million common shares of the company at a price of C$1.25 per share. The agents received an aggregate cash fee of C$1.4 million. We had already assumed the issuance of equity in our financial model. Prominent mining investor Mr. Eric Sprott invested C$2.0 million through his company, 2176423 Ontario Ltd., with the acquisition of 1.6 million shares.

Use of Proceeds. The proceeds will be used to advance the company’s flagship Nisk Project in Quebec and its Jabul Baudan exploration license in Saudi Arabia, and to fund general working capital and corporate needs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY AB, June 10, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) announced today the voting results for the election of directors at its annual meeting of shareholders held on June 10, 2026 (the “Meeting”). The following eight nominees were elected as directors of InPlay to serve until the next annual meeting of shareholders or until their successors are elected or appointed, with common shares represented at the Meeting voting in favour of individual nominees as follows:

Director

Percentage Approval

Percentage Withheld

Douglas Bartole

99.94 %

0.06 %

Regan Davis

98.66 %

1.34 %

Joan Dunne

99.97 %

0.03 %

Craig Golinowski

99.93 %

0.07 %

Tamir Polikar

99.83 %

0.17 %

Ehud Erez

94.40 %

5.60 %

Stephen Nikiforuk

99.96 %

0.04 %

Dale Shwed

99.84 %

0.16 %

In addition, all other resolutions presented at the Meeting were approved by InPlay’s shareholders, including the appointment of PriceWaterhouseCoopers LLP as auditors. For complete voting results, please see our Report of Voting Results which is available through SEDAR+ at www.sedarplus.ca.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President Corporate & Business Development, InPlay Oil Corp., Telephone: (587) 955-0635

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

George Proost, Research Intern, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Double E Expansion Gains Commercial Traction. Summit Midstream announced additional long-term transportation commitments on its Double E Pipeline, bringing open season commitments to 250 MMcf/d and total contracted capacity to approximately 1.9 Bcf/d. Demand has exceeded available expansion capacity, prompting the company to extend its open season through June 30, 2026, while continuing negotiations with prospective shippers. Management remains on track to reach a final investment decision by the end of summer and has secured key compressor equipment to support a targeted late-2028 in-service date.

Strong Demand Supports Capacity Expansion. The Double E Compression Expansion would increase pipeline capacity by approximately 50%, from 1.6 Bcf/d to 2.4 Bcf/d, further strengthening its role as a key natural gas takeaway system in the Delaware Basin. In addition to the 250 MMcf/d of binding commitments secured, Summit holds a firm option agreement for another 200 MMcf/d and continues discussions with shippers whose interest exceeds available capacity. The strong commercial response reduces project risk and underscores continued demand for Permian Basin natural gas infrastructure.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Stock Repurchase Authorization. Summit Midstream Corporation announced that its Board of Directors has authorized the company’s first stock repurchase program, allowing for the repurchase of up to $35 million of outstanding common stock. As of May 8, shares outstanding were 20.3 million, including 13.8 million common shares and 6.5 million Class B common shares.

Terms of the Program. Summit may repurchase shares through open market transactions, privately negotiated purchases, block trades, or other methods permitted under applicable securities laws. Repurchase activity will depend on market conditions, share price, debt covenant compliance, and other factors. The program has no expiration date, does not require the company to buy back any specific number of shares, and may be suspended or terminated at any time.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.