Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q 2026 Financial Results. EuroDry Ltd. reported strong 2Q 2026 financial performance compared to the prior year period, driven primarily by a favorable dry bulk market and higher time charter equivalent (TCE) rates. Total net revenues increased 57% year-over-year to $17.7 million, while average time charter equivalent rates more than doubled to $20,398 per day compared with $10,428 per day during the prior year period. Adjusted net income attributable to controlling shareholders amounted to $6.9 million, or $2.44 per diluted share, compared to a net loss of $3.0 million, or $(1.10) per diluted share, in the prior year period. Adjusted EBITDA increased to $11.7 million compared to $1.9 million during the prior year period, reflecting strong operating leverage as TCE rates increased. We had projected 2Q revenue and adj. EBITDA of $17.4 million and $9.3 million, respectively.

Strong Operational Quarter. Fleet utilization improved to 100.0% compared to 99.3% during the prior year period, with commercial utilization at 100%, reflecting minimal downtime and effective charter execution. Vessel operating expenses declined modestly to $6,608 per day compared to $6,785 per day during the prior year period, while total operating expenses decreased to $7,444 per day compared to $7,539 during the second quarter of 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second Quarter FY 2026 Financial Results. RAIL generated a 2Q FY26 adjusted net loss to common stockholders of $821.0 thousand, or $(0.02) per share, compared to adjusted net income of $3.8 million, or $0.11 per share, during the prior year period. Gross margin as a percentage of revenue amounted to 5.5% compared to 15.0% in 2Q FY 2025. Revenue and rail car deliveries declined to $113.1 million and 927, compared to $118.6 million and 939 during the prior year period. Adj. EBITDA amounted to $1.2 million compared to $9.3 million in 2Q FY 2025.

Updated FY 2026 Guidance. Management updated its FY 2026 guidance. Railcar deliveries are expected to be in the range of 3,500 to 3,900, revenue in the range of $410 to $460 million, and adj. EBITDA in the range of $36 to $44 million. Prior guidance projected railcar deliveries in the range of 4,000 to 4,500, revenue in the range of $500 to $550 million, and adj. EBITDA in the range of $41 to $50 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. CVG delivered year-over-year revenue growth across all three segments, reflecting ongoing efforts to reduce end-market concentration in cyclical North American Class 8 truck exposure through geographic and end-market diversification. While there are still macroeconomic uncertainties to monitor, CVG is hitting its stride as new business wins are ramping coincidentally with a recovery in key end markets.

2Q26 Results. CVG reported 2Q26 revenue of $195.2 million, up from $172 million in the year-ago period, a 13.5% increase, driven by increased customer demand in international markets and the ramp of previously awarded new business wins across all three operating segments. We were at $173 million. Gross margin improved both y-o-y and sequentially to 12.9%. One-time items impacted the reported bottom line. On an adjusted basis, CVG reported a net loss of $0.13/sh, up from a loss of $0.09/sh last year, reflecting increased incentive comp expense in 2Q26 over 2Q25.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, July 31, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the second quarter ended June 30, 2026, on August 6, 2026, before market opens in New York.

On the same day, Thursday, August 6, 2026, at 9:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 800-717-1738 (US Toll-Free Dial In) or +1 646-307-1865 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13762074.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the second quarter ended June 30, 2026, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

AboutEuroDryLtd. EuroDry Ltd. was formed on January 8, 2018, under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 12 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027 and the delivery of the two Kamsarmax vessels in 2028, the Company’s fleet will consist of 15 vessels with a total carrying capacity of 1,050,420 dwt.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

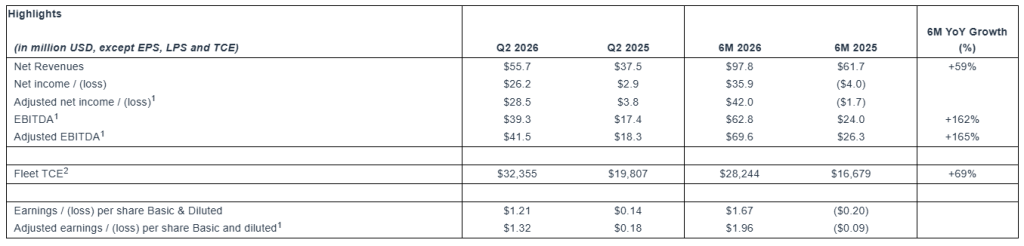

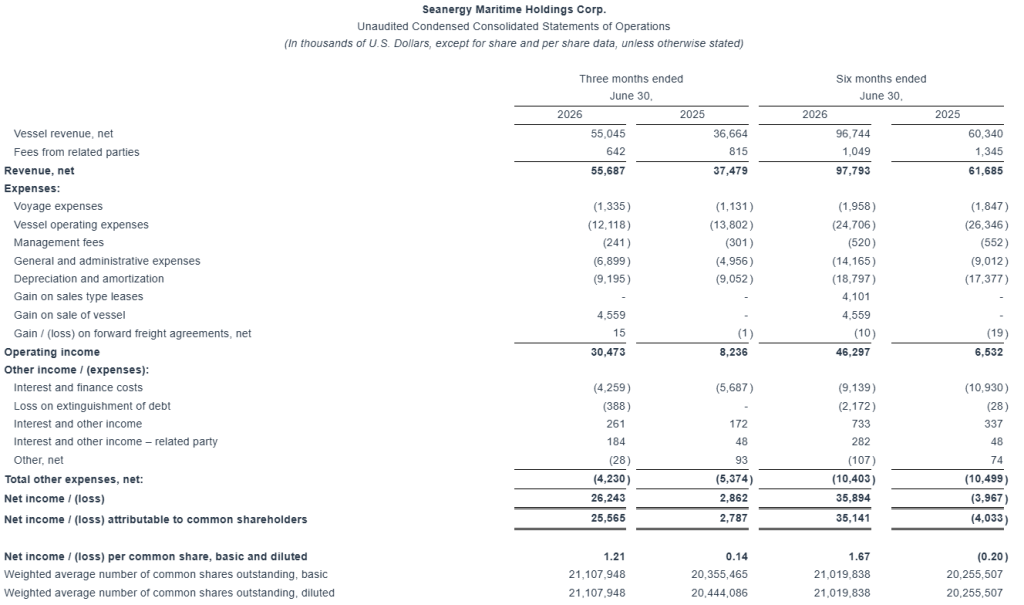

Record Second Quarter 2026 Financial Results. Seanergy reported revenue, adj. EBITDA, and adj. EPS of $55.7 million, $41.5 million, and $1.32, respectively, compared to $37.5 million, $18.3 million, and $0.18 during the prior year period. We had projected revenue, adj. EBITDA, and adj. EPS of $54.9 million, $38.4 million, and $1.15, respectively. Second quarter financial results reflected both materially higher time charter equivalent (TCE) rates compared to the prior year quarter and lower-than-expected interest and finance costs relative to our estimates.

Updating Estimates. We have increased our FY 2026 revenue, adj. EBITDA, and adj. EPS estimates to $205.9 million, $134.2 million, and $3.70, respectively, compared to our prior estimates of $203.2 million, $131.3 million, and $3.50. Our revised estimates reflect higher time charter equivalent (TCE) rates and fewer off-hire days.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Delivers Record Q2 Net Income of $26.2 Million and EPS/ Adjusted EPS of $1.21/ $1.32; Declares Quarterly Dividend of $0.35 Per Share, Representing the Company’s 19th Consecutive Distribution

Expands Fleet Renewal Program to $591 Million Across Eight Modern Capesize & Newcastlemax Vessels; Completes €100 Million Unsecured Bond Offering

______________________________ 1 Adjusted earnings / (loss) per share, Adjusted Net Income / (loss), EBITDA and Adjusted EBITDA are non-GAAP measures. Please see the reconciliation below of Adjusted earnings / (loss) per share, Adjusted Net Income / (loss), EBITDA and Adjusted EBITDA to net income, the most directly comparable U.S. GAAP measure. 2 Time Charter Equivalent (“TCE”) rate is a non-GAAP measure. Please see the reconciliation below of TCE rate to net revenues from vessels, the most directly comparable U.S. GAAP measure.

Highlights and Developments:

Exceptional Financial Performance & Consistent Shareholder Returns — $108.4 Million Returned Since Program Inception

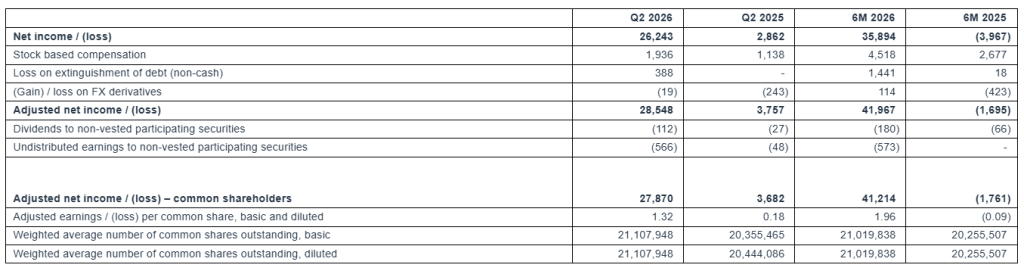

Record Q2 and H1 profit of $26.2 million and $35.9 million, respectively, up from $2.9 million net income and $4.0 million loss in the prior-year periods

Quarterly cash dividend of $0.35 per share, the Company’s 19th consecutive cash dividend; payout of approx. 27% of Q2 Adjusted EPS

$108.4 million of total capital returned to shareholders, comprising $63.2 million of cash dividends ($3.19 per share) and $45.2 million of share, warrant and convertible note repurchases

Disciplined Fleet Growth and Renewal – $591 million Aggregate Investment Plan

Entered into an agreement to acquire two Japanese-built Capesize vessels – a newbuilding and a modern 2022-built vessel – for aggregate consideration of approximately $130 million, both scheduled to join the fleet in early 2029

Expanded fleet renewal and growth program from six to eight modern vessels comprising seven newbuildings and one 2022-built Capesize, for an aggregate investment of approximately $591 million; four vessels to be delivered in 2027

Completed the profitable sale of the 2010-built M/V Squireship, generating approximately $13.8 million of net liquidity and a gain on sale of approximately $4.6 million, while continuing to provide technical and management services to the vessel

Secured long-term time charters with leading counterparties for the three China-built 2027 newbuildings with floor rates covering expected cash breakeven, as well as potentially significant index-linked market upside

Diversified Capital Resources — €100 Million Bond and $296.5 Million of Facilities Secured

Successfully completed a €100 million 5-year unsecured corporate bond offering in Greece, further diversifying the Company’s capital resources and supporting its fleet growth and renewal program

Fleet renewal program substantially funded: $72.6 million advanced from own funds and approximately $296.5 million of pre- and post-delivery facilities secured, alongside the €100 million bond

Strong Commercial Performance

Q2 2026 fleet TCE of $32,355 per day, an increase of 63% year over year

Estimated Q3 2026 TCE of approximately $31,0003 per day – increased H2 earnings visibility

ATHENS, Greece, July 30, 2026 (GLOBE NEWSWIRE) — Seanergy Maritime Holdings Corp. (“Seanergy” or the “Company”) (NASDAQ: SHIP), a leading pure-play Capesize owner and operator, today reported its financial results for the second quarter and six months ended June 30, 2026, and declared a quarterly cash dividend of $0.35 per common share. This marks Seanergy’s 19th consecutive quarterly dividend under its capital return policy and reflects the Company’s strong earnings generation and disciplined approach to capital allocation.

For the quarter ended June 30, 2026, the Company generated Net Revenues of $55.7 million, compared to $37.5 million in the second quarter of 2025. Net Income and Adjusted Net Income for the quarter increased to $26.2 million and $28.5 million, respectively, compared to $2.9 million and $3.8 million, respectively, in the prior-year period. EBITDA and Adjusted EBITDA for the quarter reached $39.3 million and $41.5 million, respectively, compared to $17.4 million and $18.3 million, respectively, for the same period of 2025. The fleet achieved a daily TCE of $32,355 for the second quarter of 2026, representing a 63% year-over-year increase.

For the six months ended June 30, 2026, Seanergy generated Net Revenues of $97.8 million, Net Income of $35.9 million and Adjusted Net Income of $42.0 million, compared to Net Revenues of $61.7 million, a Net Loss of $4.0 million and Adjusted Net Loss of $1.7 million in the first half of 2025. Adjusted EBITDA increased by 165% to $69.6 million, while Adjusted EPS reached $1.96, compared to an adjusted loss per share of $0.09 in the prior-year period. Fleet TCE increased by 69% to $28,244 per day.

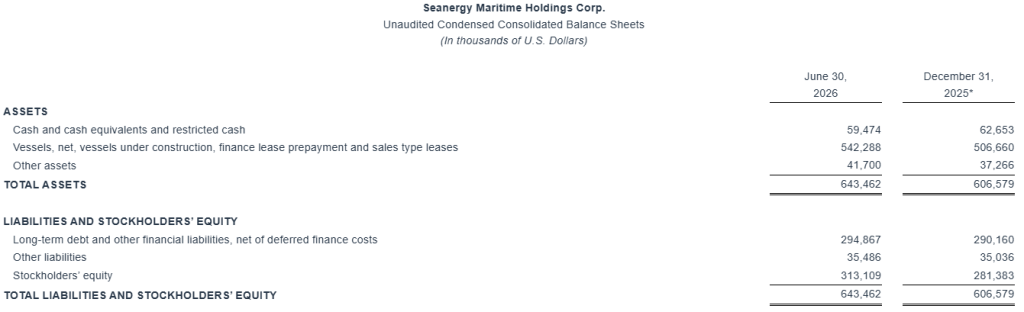

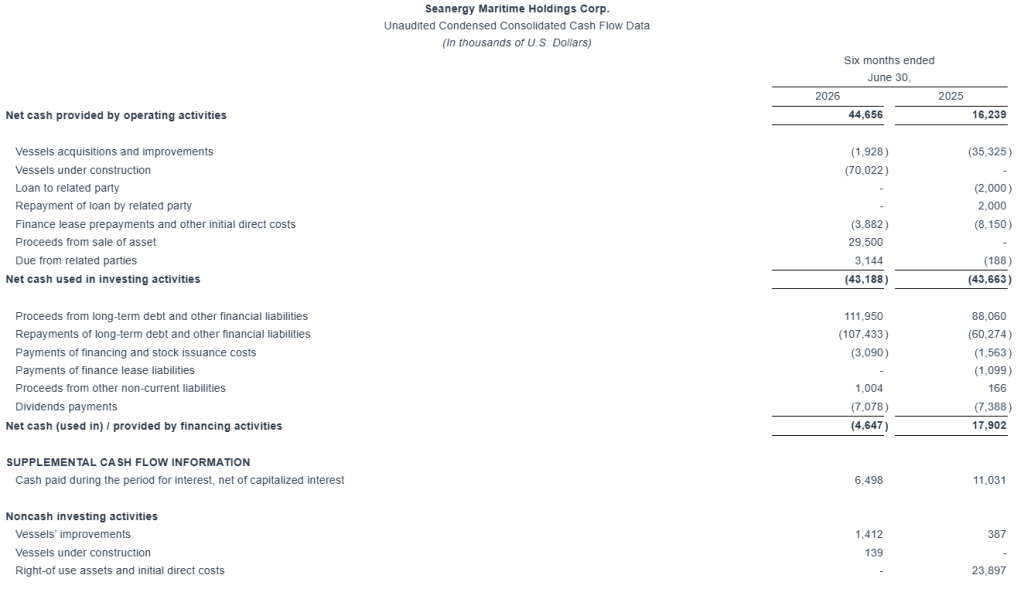

Cash and cash-equivalents and restricted cash, as of June 30, 2026, stood at $59.5 million. Long-term debt (senior loans and other financial liabilities) net of deferred charges amounted to $294.9 million, compared with a fleet book value of $542.3 million, including advances paid for vessels under construction and a vessel under sales-type lease, resulting in a fleet loan-to-book value ratio of approximately 55%. Stockholders’ equity increased by $31.7 million, or 11% to $313.1 million, over the six-month period.

______________________________ 3 Blended Q3 TCE estimated on approx. 71% of Q3 available days already fixed and FFA rates as of July 28, 2026.

Stamatis Tsantanis, the Company’s Chairman & Chief Executive Officer, stated:

“Seanergy delivered record results in the second quarter with Net Income of $26.2 million and Adjusted EPS of $1.32, bringing first-half Adjusted EPS to $1.96, and underscoring the strong earnings power and operating leverage of our pure-play Capesize platform.”

“Building on our solid performance, we continued to execute on our disciplined capital return policy. Our board of directors declared a quarterly cash dividend of $0.35 per share, our 19th consecutive distribution, bringing cumulative dividends to $3.19 per share, or approximately $63.2 million in aggregate. In total, we have returned $108.4 million to shareholders since program inception, through dividends and the repurchases of shares, warrants and convertible notes.”

“We further advanced our fleet renewal strategy by agreeing to acquire two additional high-quality Japanese Capesize vessels for an aggregate consideration of approximately $130 million. These transactions consist of a scrubber-fitted newbuilding and a modern 2022-built vessel, both expected to join our fleet in 2029. These acquisitions lock in modern, fuel-efficient tonnage and scarce 2029 delivery slots ahead of an anticipated tightening in Capesize supply.”

“Our fleet renewal and growth program now comprises eight modern vessels, including seven newbuildings and one 2022-built Capesize, and represents an aggregate investment of approximately $591 million. Four of the eight vessels are scheduled to deliver in 2027, accelerating fleet renewal and earnings contribution from 2027 onward. We continue to execute selectively, pairing scarce delivery slots with disposals of older tonnage at firm valuations, while maintaining a disciplined balance sheet.”

“We have also secured multi-year employment for our three Chinese-built 2027 newbuildings with leading global counterparties, at floor rates covering expected cash breakeven plus a premium index-linked formula and profit sharing above an upper threshold. This approach materially de-risks the first phase of the program from day one of delivery while maintaining the upside potential central to our investment thesis.”

“Our successful issuance of a €100 million unsecured corporate bond in Greece diversifies our capital base and complements our existing secured financings. Its five-year non-amortizing structure provides non-dilutive, long-term capital precisely matched to the construction phase of our program, before the new vessels begin generating revenues.”

“The Capesize market continued to perform strongly during the second quarter, supported by record quarterly China iron ore imports and continued growth in bauxite trade against low fleet supply growth. Looking ahead, the market outlook remains constructive: a low orderbook against a rapidly ageing fleet, strong iron ore export growth, and resilient coal and bauxite volumes. In this context, we have fixed about 55% of our ownership days for the second half of the year at a daily rate of $30,800, providing significant earnings visibility while preserving meaningful index-linked exposure in a strong Capesize market. Additionally, based on the current FFA curve, our estimated 3Q 2026 daily TCE of approximately $31,000 further reinforces our positive earnings outlook and our ability to continue generating attractive returns in the quarters ahead.”

“Our strategic direction remains clear: deliver consistent shareholder distributions, invest strategically in modern tonnage, and preserve financial flexibility. We believe this balanced approach positions Seanergy to create meaningful long-term shareholder value.”

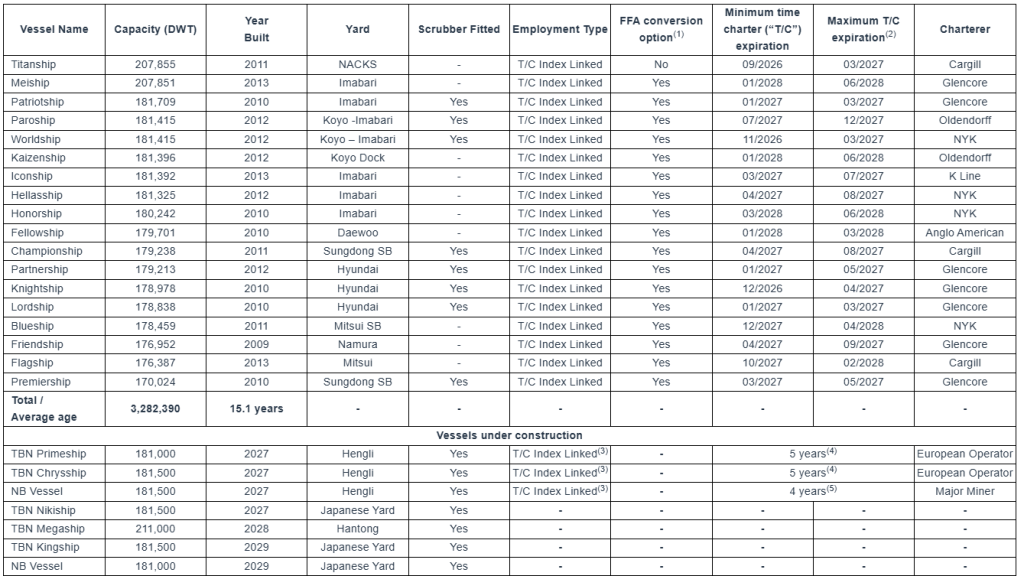

Company Fleet:

Fleet Data:

(U.S. Dollars in thousands)

(In thousands of U.S. Dollars, except operating days and TCE rate)

(In thousands of U.S. Dollars, except ownership days and Daily Vessel Operating Expenses)

Net income / (loss) to EBITDA and Adjusted EBITDA Reconciliation:

(In thousands of U.S. Dollars)

Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”) represents the sum of net income / (loss), net interest and finance costs, depreciation and amortization and, if any, income taxes during a period. EBITDA and Adjusted EBITDA are not recognized measurements under U.S. GAAP. Adjusted EBITDA represents EBITDA adjusted to exclude stock-based compensation, (gain) / loss on forward freight agreements, net, loss on extinguishment of debt, and (gain) / loss on FX derivatives. which the Company believes are not indicative of the ongoing performance of its core operations.

EBITDA and adjusted EBITDA are presented as we believe that these measures are useful to investors as a widely used means of evaluating operating profitability from period to period. Management also uses these non-GAAP financial measures in making financial, operating and planning decisions and in evaluating the Company’s performance. EBITDA and adjusted EBITDA as presented here may not be comparable to similarly titled measures presented by other companies. These non-GAAP measures should not be considered in isolation from, as a substitute for, or superior to, financial measures prepared in accordance with U.S. GAAP.

Adjusted Net Income / (Loss) Reconciliation and calculation of Adjusted Earnings / (Loss) Per Share

(In thousands of U.S. Dollars, except for share and per share data)

To derive Adjusted Net Income and Adjusted Earnings / (loss) Per Share, a non-GAAP financial measure, from Net Income / (loss), we adjust for dividends and undistributed earnings to non-vested participating securities and exclude non-cash items, as provided in the table above. We believe that Adjusted Net Income / (loss) and Adjusted Earnings / (loss) Per Share assist our management and investors by increasing the comparability of our performance from period to period since each such measure eliminates the effects of such non-cash items as loss on extinguishment of debt, stock based compensation, (gain) / loss on FX derivatives and other items which may vary from year to year, for reasons unrelated to overall operating performance. In addition, we believe that the presentation of the respective measure provides investors with supplemental data relating to our results of operations, and therefore, with a more complete understanding of factors affecting our business than with GAAP measures alone. Our method of computing Adjusted Net Income / (loss) and Adjusted Earnings / (loss) Per Share may not necessarily be comparable to other similarly titled captions of other companies due to differences in methods of calculation.

Third Quarter 2026 TCE Rate Guidance:

As of the date hereof, approximately 71% of the Company fleet’s expected operating days in the third quarter of 2026 have been fixed at an estimated TCE rate of approximately $30,112. Assuming that for the remaining operating days of our index-linked time charters, the BCI-180 rate will be equal to $33,980 (based on the FFA curve as of July 28, 2026), our estimated TCE rate for the third quarter of 2026 will be approximately $30,9984. The following table provides the breakdown of index-linked charters and fixed-rate charters in the third quarter of 2026:

______________________________ 4 This guidance is based on certain assumptions and the Company cannot provide assurance that these TCE rate estimates, or projected utilization rates will be realized. TCE estimates include certain floating (index) to fixed rate conversions concluded in previous periods. For vessels on index-linked T/Cs, the TCE rate realized will vary with the underlying index, and for the purposes of this guidance, the BCI 5TC 180 rate assumed for the remaining operating days of the quarter for an index-linked T/C is equal to $33,980 (based on the FFA curve as of July 28, 2026). Spot estimates are provided using the load-to-discharge method of accounting. The rates quoted are for days currently contracted. Increased ballast days at the end of the quarter will reduce the additional revenues that can be booked based on the accounting cut-offs and therefore the resulting TCE rate will be reduced accordingly.

Second Quarter and Recent Developments:

Dividend Distribution for Q1 2026 and Declaration of Q2 2026 Dividend

On July 10, 2026, the Company paid a quarterly cash dividend of $0.20 per common share for the first quarter of 2026 to all shareholders of record as of June 29, 2026.

The Company has declared a quarterly cash dividend of $0.35 per common share for the second quarter of 2026 payable on or about October 9, 2026, to all shareholders of record as of September 25, 2026.

The Company is renewing its fleet through the addition of advanced eco-design newbuildings and modern secondhand tonnage, while selectively divesting older vessels. The seven newbuildings under the Company’s fleet renewal and growth program are designed to meet International Maritime Organization requirements for Phase 3 greenhouse gas emissions reduction (“IMO GHG Phase 3”) and Tier III nitrogen oxide emissions (“IMO NOx Tier III”) and are scrubber-fitted.

In parallel, the Company continues to implement the environmental upgrade program across its existing fleet, having invested approximately $37.3 million since 2024 in environmental upgrades, vessel improvements and dry-dockings.

Together, the fleet renewal and environmental upgrade initiatives are expected to improve fuel efficiency and reduce greenhouse gas emissions. Having completed the majority of the scheduled upgrades in prior quarters, the Company expects approximately 50 off-hire days for the remainder of 2026 in connection with scheduled dry-dockings, vessel repairs and environmental upgrades.

Fleet Update

Acquisition of Two Japanese-Built Capesize Vessels for 2029 Delivery

The Company has entered into an agreement with unaffiliated third parties to acquire two Japanese Capesize vessels for aggregate consideration of approximately $130.0 million.

The acquisitions comprise:

a 181,000 dwt scrubber-fitted Capesize newbuilding, expected to be delivered between the first and second quarters of 2029; and

a 182,162 dwt Capesize vessel built in 2022, with forward delivery expected between the fourth quarter of 2028 and the second quarter of 2029.

The Company has already paid a deposit of 5% of the purchase price for the Capesize newbuilding. The remaining balance of the purchase price shall be payable as follows: 35% in three instalments by November 2028, and the remaining 60% upon delivery of the vessel. Concerning the 2022-built Capesize vessel, the agreement involves a 10% advance payment, while the remaining 90% of the purchase price will be payable upon the vessel’s delivery.

The newbuilding vessel will incorporate advanced eco-design features, intended to enhance fuel efficiency and reduce emissions. Together, the two acquisitions will add modern high-quality tonnage at a delivery point, which is aligned with the next phase of the Company’s fleet renewal strategy and expected requirements.

To date, the Company has already paid $72.6 million for its newbuilding and fleet renewal program while maintaining a strong liquidity position.

Sale of M/V Squireship

In June 2026, the Company delivered to United Maritime Corporation, a related party, the 170,018 dwt M/V Squireship, built in 2010. The gross sale price was approximately $29.5 million, generating net proceeds of about $13.8 million. Seanergy continues to provide technical and management services to the vessel, facilitating the continuation of the vessel’s existing commercial employment.

Commercial Updates

Long-Term Time Charters for Three 2027-Delivery Newbuildings

In July 2026, the Company entered into multi-year time charter agreements for three scrubber-fitted Capesize newbuildings scheduled for delivery between the second and fourth quarters of 2027.

Two of our vessels to be delivered in 2027, to be named M/V Primeship and M/V Chrysship, have each been chartered for a period of five years to a leading European operator, with three optional extension periods of minimum 10 to maximum 14 months each. The third vessel, a 181,000 dwt Capesize vessel scheduled for delivery in the fourth quarter of 2027 has been chartered for four years to a major mining company, with two optional extension periods of about 11 to about 13 months. The charters are expected to commence upon the respective delivery of each vessel.

The agreements provide for average floor rates of approximately $23,100 per day, designed to cover the vessels’ estimated cash breakeven levels. Above the floor, hire is calculated at a significant premium over the BCI-180 up to an average upper threshold of approximately $29,750 per day. Above the upper threshold, incremental earnings based on the same premium over the BCI-180 are shared equally between Seanergy and the respective charterer.

M/V Kaizenship – New Time Charter agreement

In July 2026, the Company entered into a new time charter agreement with Oldendorff Carriers GmbH & Co. KG (“Oldendorff”) for the M/V Kaizenship, for a period of about 18 to about 28 months. The new time charter agreement with Oldendorff is expected to commence in August 2026. The daily hire is based on the 5 T/C routes of the BCI, with an option for the Company to fix the rate for 1 to 16 months based on the prevailing Capesize FFA curve.

M/V Blueship – New Time Charter agreement

In June 2026, the Company entered into a new time charter agreement with Nippon Yusen Kabushiki Kaisha (“NYK”) for the M/V Blueship, for a period of about minimum 14 to about maximum 17 months. The new time charter agreement with NYK is expected to commence in November 2026, in direct continuation of the maximum period of the current charter. The daily hire is based on the 5 T/C routes of the BCI along with a fixed daily premium, with an option for the Company to fix the rate for 2 to 12 months based on the prevailing Capesize FFA curve.

M/V Fellowship – Time Charter Extension

In July 2026, the existing charterer exercised its option to extend the time charter agreement for the M/V Fellowship until a minimum of January 2028 and a maximum of March 2028, with the extension commencing immediately upon the expiration of the current charter period.

M/V Friendship – Time Charter Extension

In June 2026, the existing charterer of the vessel exercised its option to extend the time charter agreement for M/V Friendship by six months beyond the current minimum/maximum charter period, in direct continuation from the previous agreement.

Financing Updates

Successful Completion of €100 Million Five-Year Unsecured Corporate Bond Offering

In July 2026, Seanergy successfully completed a €100 million unsecured bond offering to investors in Greece (ATHEX: SHIPB1). The bonds were admitted to trading on the Fixed Income Securities Segment of Euronext Athens Holding S.A. on July 13, 2026.

The bonds were issued at par, mature in July 2031 and carry a coupon of 4.90% per annum, payable semi-annually. The five-year bullet structure involves no scheduled principal amortization before maturity, preserving liquidity during the construction phase of the Company’s newbuilding program.

Newbuilding Capesize vessel – Sale and Leaseback agreement

The Company has agreed to enter into a $60.0 million sale and leaseback agreement to partially finance the acquisition of the Capesize vessel scheduled for delivery in the fourth quarter of 2027. The agreement also provides pre-delivery financing for certain instalments under the shipbuilding contract. Upon delivery, the vessel will be sold and chartered back for a period of 84 months. The Company will have continuous purchase options at predetermined prices as set forth in the agreement, commencing two years after the charter commencement date. The charterhire principal will amortize in 28 quarterly instalments of $0.7 million along with a purchase option of $40.0 million at the expiry of the bareboat charter. The pre-delivery financing amounts will accrue interest, payable quarterly in arrears.

Conference Call:

The Company’s management will host a conference call to discuss financial results on July 30, 2026, at 10:00 a.m. Eastern Time.

Audio Webcast and Earnings Presentation:

There will be a live, and then archived, webcast of the conference call and accompanying presentation available through the Company’s website. To access the presentation and listen to the archived audio file, visit our website, following the Webcast & Presentations section under our Investor Relations page. Participants to the live webcast should register on Seanergy’s website approximately 10 minutes prior to the start of the webcast, following this link.

Conference Call Details:

Participants have the option to register for the call using the following link. You can use any number from the list or add your phone number and let the system call you right away.

About Seanergy Maritime Holdings Corp.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company publicly listed in the U.S. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company owns or operates under finance leases 19 vessels (2 Newcastlemax and 17 Capesize) with an average age of approximately 15.1 years and an aggregate cargo carrying capacity of 3,463,843 dwt. Upon the sale of the M/V Dukeship and the delivery of the seven newbuilding vessels and one secondhand Capesize vessel, the Company will own or operates under finance lease 26 vessels (3 Newcastlemax and 23 Capesize), with an aggregate cargo carrying capacity of approximately 4,763,552 dwt.

The Company is incorporated in the Republic of the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events, including with respect to declaration of dividends, market trends and shareholder returns. Words such as “may”, “should”, “expects”, “intends”, “plans”, “believes”, “anticipates”, “hopes”, “estimates” and variations of such words and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks and are based upon a number of assumptions and estimates, which are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to, the Company’s operating or financial results; the Company’s liquidity, including its ability to service its indebtedness; competitive factors in the market in which the Company operates; shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; future, pending or recent acquisitions and dispositions, business strategy, impacts of litigation, areas of possible expansion or contraction, and expected capital spending or operating expenses; risks associated with operations outside the United States; risks arising from trade disputes between the U.S. and China, including the re-imposition of reciprocal port fees; broader market impacts arising from trade disputes or war (or threatened war) or international hostilities, such as between the U.S. and Israel and Iran, the U.S. and Venezuela, China and Taiwan and Russia and Ukraine; risks associated with the length and severity of pandemics; and other factors listed from time to time in the Company’s filings with the SEC, including its most recent annual report on Form 20-F. The Company’s filings can be obtained free of charge on the SEC’s website at www.sec.gov. Except to the extent required by law, the Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating Estimates. We have adjusted our second-quarter 2026 revenue, adj. EBITDA, and adj. EPS estimates to $17.4 million, $9.3 million, and $1.44, respectively, from $17.3 million, $8.4 million, and $1.18. Our estimates reflect modestly higher time charter equivalent rates and lower voyage expenses due to lower fuel costs. For FY 2026, we forecast revenue, adj. EBITDA, and adj. EPS of $66.0 million, $31.9 million, and $4.27, respectively, compared to our previous estimates of $65.3 million, $30.5 million, and $3.87.

Intermediate-Term Outlook Remains Constructive. The intermediate-term outlook for the dry bulk shipping industry remains favorable, supported by strengthening charter rates, resilient demand for iron ore, grain, and bauxite, and a highly supportive supply backdrop. A historically low order book, limited shipyard capacity, an aging global fleet, and increasingly stringent environmental regulations are expected to constrain vessel supply growth and support freight rates through 2026. While the 2027 outlook offers less certainty, EuroDry has the flexibility to respond to market conditions by increasing its fixed-rate charter coverage.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating Estimates. We have increased our 2Q 2026 revenue, adj. EBITDA, and adj. EPS estimates to $54.9 million, $38.4 million, and $1.15, respectively, from $50.0 million, $35.2 million, and $1.00. Our estimates reflect higher time charter equivalent rates than previously estimated. Moreover, we have lowered our estimates for vessel operating expenses in the second quarter and increased our estimate for general and administrative expenses in the second and third quarters. For FY 2026, we forecast revenue, adj. EBITDA, and adj. EPS of $203.2 million, $131.3 million, and $3.50, respectively, compared to our previous estimates of $198.3 million, $130.2 million, and $3.45.

Constructive Outlook. Seanergy’s outlook remains constructive, supported by favorable Capesize market fundamentals, a disciplined capital allocation strategy, and a multi-year fleet modernization program that positions the company to benefit from what we think will be a structurally attractive market through 2029. Following a strong first quarter in which the company reported significantly higher earnings and cash flow, we expect the momentum to continue, with second quarter time charter equivalent (TCE) rates projected to be approximately $31,430 per day.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition of Southern Parts & Equipment, Inc. FreightCar America announced the acquisition of Southern Parts & Equipment, Inc., a Monroe, Georgia-based distributor of reconditioned, new, and used railcar parts and equipment. The transaction, funded with cash, represents the company’s second acquisition in the railcar aftermarket segment within the past year.

A Growing Aftermarket Platform. The acquisition advances RAIL’s strategy of building a larger, more diversified aftermarket business that generates recurring revenue and reduces the cyclicality of new railcar manufacturing. Founded in 1988, SP&E has established a strong reputation serving railcar repair shops and private railcar owners. The transaction expands FreightCar’s customer base, enhances sourcing capabilities, and creates additional cross-selling opportunities across its growing aftermarket platform.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

GLYFADA, Greece, July 08, 2026 (GLOBE NEWSWIRE) — Seanergy Maritime Holdings Corp. (the “Company” or “Seanergy”) (NASDAQ: SHIP) announced today the pricing of the offering of €100 million of unsecured bonds (the “Bonds”) to investors in Greece. The Bonds will be admitted to trading on the Fixed Income Securities Segment of Euronext Athens Holding S.A. (“Euronext Athens”).

The Bonds mature in July 2031, were issued at par and carry a coupon of 4.90% per annum, payable semi-annually. Settlement is expected on July 10, 2026 and trading is expected to commence on July 13, 2026.

The proceeds are expected to be used to finance part of the cost of newbuilding vessels and/or second-hand vessel acquisitions, as well as for general corporate and working capital purposes. Offering expenses are estimated at approximately €4.4 million.

Stamatis Tsantanis, the Company’s Chairman & Chief Executive Officer, stated:

“We are very pleased with the successful completion of this offering, which represents an important milestone for Seanergy in the Hellenic capital markets.

“We sincerely thank the Hellenic investment community for its strong confidence in our strategy and long-term prospects.

“The Bonds provide meaningful non-dilutive capital, diversifying further our capital structure, while supporting the disciplined execution of our fleet growth strategy.”

The Bonds have not been and will not be registered under the Securities Act of 1933, as amended or the securities laws of any state of the United States, and, subject to certain exceptions, may not be offered or sold within the United States. The offering of Bonds is not directed to, and may not be accessed by, any person located in the United States. This press release does not constitute an offer to sell or the solicitation of an offer to buy the Bonds, nor shall it constitute an offer, solicitation or sale in any jurisdiction in which such offer, solicitation or sale would be unlawful.

AboutSeanergyMaritimeHoldingsCorp.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company publicly listed in the U.S. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company owns or finance leases 19 vessels (2 Newcastlemax and 17 Capesize) with an average age of approximately 15.0 years and an aggregate cargo carrying capacity of approximately 3,463,843 dwt. Upon completion of the sale of the M/V Dukeship and the delivery of the newbuilding vessels, the Company is expected to own or finance lease 24 vessels (3 Newcastlemax and 21 Capesize), with an aggregate cargo carrying capacity of approximately 4,400,390 dwt.

The Company is incorporated in the Republic of the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events, including with respect to the consummation of and use of proceeds of the offering of Bonds. Words such as “may”, “should”, “expects”, “intends”, “plans”, “believes”, “anticipates”, “hopes”, “estimates” and variations of such words and similar expressions are intended to identify forward-looking statements. These statements involve known and unknown risks and are based upon a number of assumptions and estimates, which are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to, the Company’s operating or financial results; the Company’s liquidity, including its ability to service its indebtedness; competitive factors in the market in which the Company operates; shipping industry trends, including charter rates, vessel values and factors affecting vessel supply and demand; future, pending or recent acquisitions and dispositions, business strategy, impacts of litigation, areas of possible expansion or contraction, and expected capital spending or operating expenses; risks associated with operations outside the United States; risks arising from trade disputes between the U.S. and China, including the re-imposition of reciprocal port fees; broader market impacts arising from trade disputes or war (or threatened war) or international hostilities, such as between the U.S. and Israel and Iran, the U.S. and Venezuela, China and Taiwan and Russia and Ukraine; risks associated with the length and severity of pandemics; and other factors listed from time to time in the Company’s filings with the SEC, including its most recent annual report on Form 20-F. The Company’s filings can be obtained free of charge on the SEC’s website at www.sec.gov. Except to the extent required by law, the Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

For further information please contact: Seanergy Investor Relations Tel: +30 213 0181 522 E-mail: [email protected]

Capital Link, Inc. Paul Lampoutis 230 Park Avenue Suite 1540 New York, NY 10169 Tel: (212) 661-7566 E-mail: [email protected]

Anna Wichmann Capital Link Athens Tel: +30 210 6109 800 E-mail: [email protected]

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First Raise. Commercial Vehicle Group reported that it has made the first raise under the recently announced $25 million Capital on Demand agreement. As of June 29, 2026, the Company had sold 2.6 million shares of common stock in the ATM Program, generating net proceeds of approximately $11.6 million.

Use of Proceeds. As required by the Company’s secured term loan facility, all net proceeds were used by the Company to pay down outstanding indebtedness and the associated prepayment premium under the facility. As we noted previously, as of June 17, 2026, outstanding indebtedness under the Term Loan was $80 million. The Term Loan matures in June 2030 with a current interest rate of 13.47%. Any reduction in the outstanding loan balance is a positive for the Company, in our view, not only reducing high-cost debt but also eventually providing additional financial flexibility.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Commercial momentum. FreightCar America secured a multi-year order for 1,900 railcars from a key customer, with deliveries scheduled through 2028. Combined with approximately 3,000 railcars ordered during the second quarter valued at roughly $300 million, the multi-year order highlights strong commercial demand and improves long-term backlog visibility.

Broad Customer Demand. Second quarter orders were received across all core market segments and included both new and existing customers, demonstrating the company’s expanding commercial reach and diversified product portfolio. The order activity reflects growing confidence in RAIL’s engineering expertise, manufacturing flexibility, and ability to execute reliably.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Transportation exit complete. Conduent announced the sale of its Tolling business for $70 million, completing its planned exit from the Transportation segment and substantially finishing management’s portfolio rationalization strategy.

Higher-quality business emerges. The Transportation divestitures simplify Conduent’s operating structure, reduce capital intensity, and sharpen management’s focus on its core Government and Commercial businesses, which we believe should improve long-term earnings quality and free cash flow generation.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.