ATHENS, Greece, July 31, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the second quarter ended June 30, 2026, on August 6, 2026, before market opens in New York.

On the same day, Thursday, August 6, 2026, at 9:30 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 800-717-1738 (US Toll-Free Dial In) or +1 646-307-1865 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13762074.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the second quarter ended June 30, 2026, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

AboutEuroDryLtd. EuroDry Ltd. was formed on January 8, 2018, under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters.

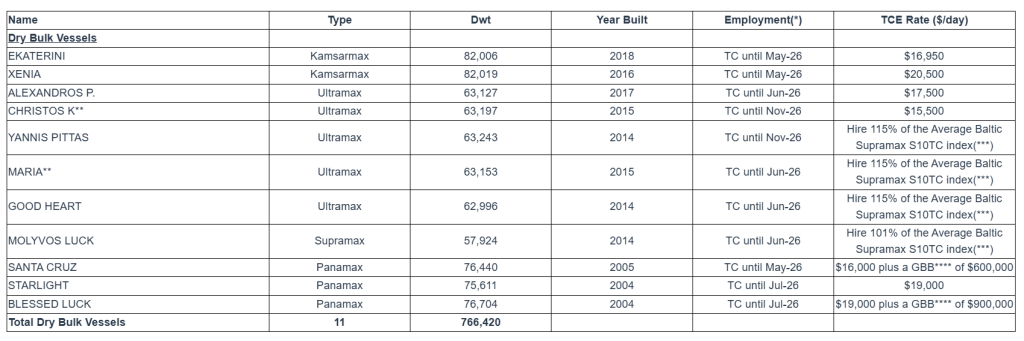

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 12 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027 and the delivery of the two Kamsarmax vessels in 2028, the Company’s fleet will consist of 15 vessels with a total carrying capacity of 1,050,420 dwt.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating Estimates. We have adjusted our second-quarter 2026 revenue, adj. EBITDA, and adj. EPS estimates to $17.4 million, $9.3 million, and $1.44, respectively, from $17.3 million, $8.4 million, and $1.18. Our estimates reflect modestly higher time charter equivalent rates and lower voyage expenses due to lower fuel costs. For FY 2026, we forecast revenue, adj. EBITDA, and adj. EPS of $66.0 million, $31.9 million, and $4.27, respectively, compared to our previous estimates of $65.3 million, $30.5 million, and $3.87.

Intermediate-Term Outlook Remains Constructive. The intermediate-term outlook for the dry bulk shipping industry remains favorable, supported by strengthening charter rates, resilient demand for iron ore, grain, and bauxite, and a highly supportive supply backdrop. A historically low order book, limited shipyard capacity, an aging global fleet, and increasingly stringent environmental regulations are expected to constrain vessel supply growth and support freight rates through 2026. While the 2027 outlook offers less certainty, EuroDry has the flexibility to respond to market conditions by increasing its fixed-rate charter coverage.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

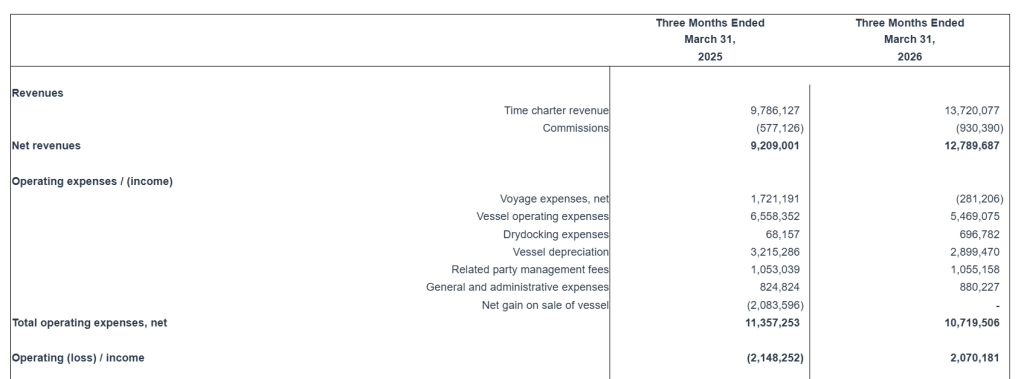

1Q 2026 Financial Results. EuroDry Ltd. reported an improvement in 1Q 2026 financial performance compared to the prior year period, driven primarily by stronger dry bulk charter markets and improved fleet utilization. Total net revenues increased 38.9% year-over-year to $12.8 million, while average time charter equivalent rates more than doubled to $14,416 per day from $7,167 per day during the prior year period. Adjusted net income attributable to controlling shareholders amounted to $330.8 thousand, or $0.12 per share, compared to a net loss of $5.7 million, or $(2.07) per share, in the prior year period. Adjusted EBITDA increased to $4.9 million compared to a loss of $1.0 million during the prior year period, reflecting strong operating leverage as freight rates recovered.

Strong Operational Quarter. Fleet utilization improved to 99.7%, with commercial utilization at 100%, reflecting minimal downtime and effective charter execution. Vessel operating expenses declined year-over-year due to a smaller average fleet size, while daily operating costs remained stable despite inflation. Meanwhile, dry bulk market conditions strengthened in April and May 2026, with one-year Ultramax and Kamsarmax charter rates nearing or surpassing $20,000 per day, supporting improved earnings prospects for the coming quarters.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, May 20, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today its results for the three-month period ended March 31, 2026.

First Quarter 2026 Highlights:

Total net revenues of $12.8 million.

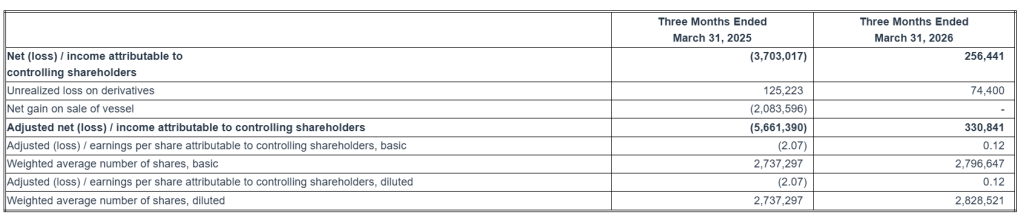

Net income attributable to controlling shareholders, of $0.26 million or $0.09 earnings per share attributable to controlling shareholders basic and diluted.

Adjusted net income1 attributable to controlling shareholders for the quarter of $0.33 million or $0.12 earnings per share attributable to controlling shareholders basic and diluted, which represents the net income attributable to controlling shareholders excluding the unrealized loss on derivatives.

Adjusted EBITDA1 was $4.9 million.

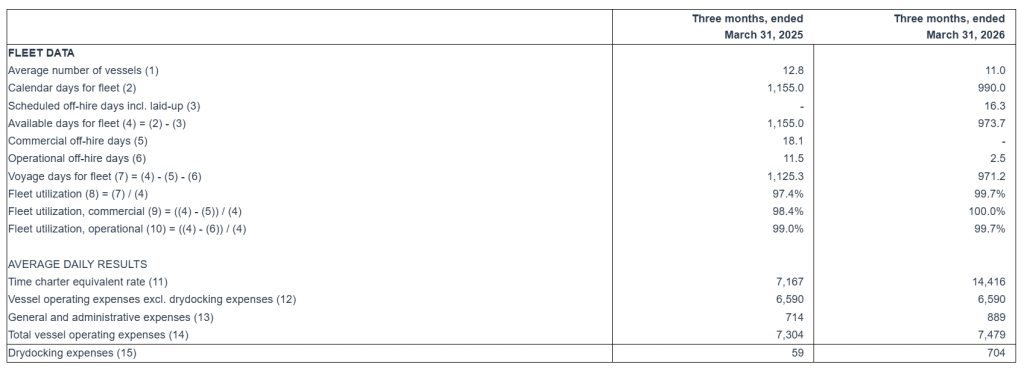

An average of 11.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $14,416 per day. Refer to a subsequent section of the Press Release for the definition and method of calculation of the time charter equivalent rate.

To date, about $5.6 million has been used to repurchase 349,330 shares of the Company, under our share repurchase plan of up to $10 million, announced in August 2022. The Board approved the continuation of the share repurchase plan for a further year in August 2025 and will review it again after a period of twelve months.

____________________________ 1Adjusted EBITDA, Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders are not recognized measurements under US GAAP (GAAP) and should not be used in isolation or as a substitute for EuroDry’s financial results presented in accordance with GAAP. Refer to a subsequent section of the Press Release for the definitions and reconciliation of these measurements to the most directly comparable financial measures calculated and presented in accordance with GAAP.

Recent developments

The Company has signed two contracts with Hengli Shipbuilding (Dalian) for the construction of two 82,000 DWT Kamsarmax bulk carriers. Both vessels are eco and are built to EEDI phase 3 design standard; they are scheduled to be delivered during the first and second quarters of 2028. The total consideration for the two newbuilding contracts is approximately $74.0 million and will be financed with a combination of debt and equity. The contracts are conditional upon receiving a refund guarantee from a bank acceptable to the Company.

Aristides Pittas, Chairman and CEO of EuroDry commented: “During the first quarter of 2026, a seasonally slow quarter, the drybulk market gave up very little ground as compared to the last quarter of last year. Additionally in April and May 2026, the market has firmed across the board with one-year time charter rates and trip earnings flirting and reaching $20,000 per day for both Ultramaxes and Kamsarmaxes.

“Our profitability during the first quarter fully reflected the market conditions with our earnings dropping compared to the fourth quarter in consequence of the easing of market rates during the quarter. But as the market has increased during the last month and a half, so has our profitability, a development that we expect to be reflected in next quarter’s results.

“Whilst the global fleet is aging and the need to provide the market with newer and more efficient vessels is becoming apparent, we see that prices of modern secondhand vessels have significantly increased. Under the circumstances we believe that newbuilding orders which can be placed at prices below modern secondhand ship prices present a better opportunity. We have therefore decided to expand our newbuilding program to include two Kamsarmax vessels to complement the two Ultramaxes we had ordered earlier. After the delivery of all four vessels between Q2 2027 and Q2 2028, our fleet will consist almost entirely of modern eco vessels. As, I believe, we have demonstrated over the past eight years as an independent public company, we invest in a disciplined manner with the sole focus on identifying accretive opportunities for our shareholders and we intend to continue with the same philosophy.”

Tasos Aslidis, Chief Financial Officer of EuroDry commented: “Our net revenues for the first quarter of 2026 were higher by 38.9% as compared to the first quarter of 2025. This is primarily driven by the increase of 101.1% in average time charter equivalent rates our vessels earned during the current quarter as compared to the first quarter of 2025, partly offset by the decreased average number of vessels owned and operated in the current period compared to the same period of 2025.”

“Vessel operating expenses were $5.5 million for the first quarter of 2026 as compared to $6.6 million for the same period of 2025. The decrease is mainly attributable to the decreased average number of vessels owned and operated in the first quarter of 2026 compared to the corresponding period in 2025.“

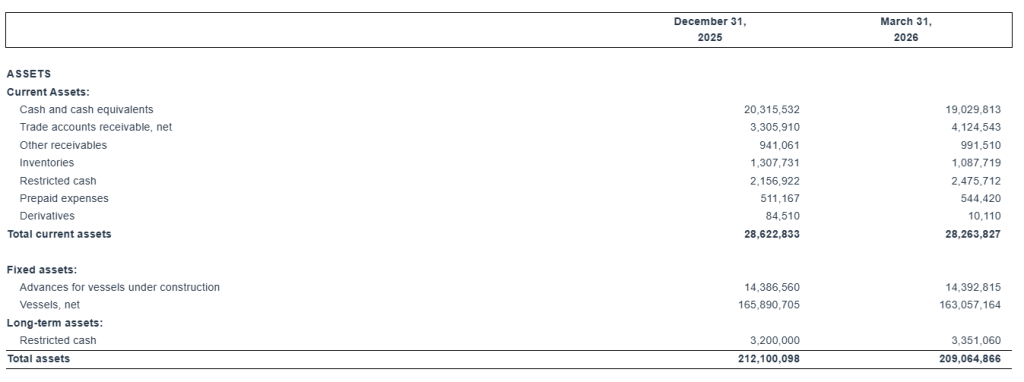

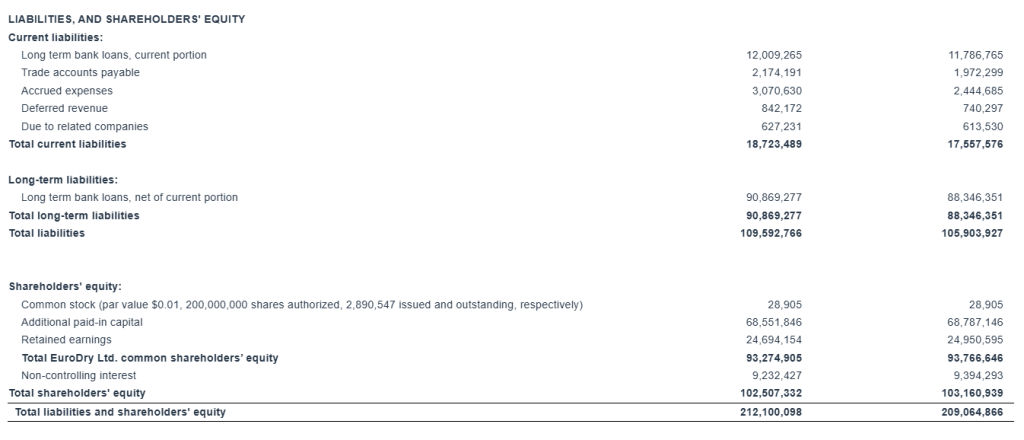

“Adjusted EBITDA during the first quarter of 2026 was $4.9 million compared to $(1.0) million achieved for the first quarter of last year. As of March 31, 2026, our outstanding debt (excluding the unamortized loan fees) was $100.9 million versus restricted and unrestricted cash of approximately $24.9 million.”

First Quarter 2026 Results: For the first quarter of 2026, the Company reported total net revenues of $12.8 million representing a 38.9% increase over total net revenues of $9.2 million during the first quarter of 2025, which was the result of the increased time charter rates our vessels earned during the first quarter of 2026, partly offset by the decreased average number of vessels owned and operated during the first quarter of 2026, compared to the same period of 2025. On average, 11.0 vessels were owned and operated during the first quarter of 2026 earning an average time charter equivalent rate of $14,416 per day compared to 12.8 vessels in the same period of 2025 earning on average $7,167 per day.

For the first quarter of 2026, a gain on bunkers resulted in positive voyage expenses of $0.3 million compared to voyage expenses of $1.7 million in the first quarter of 2025 that mainly related to vessels repositioning between charters and expenses during operational off-hire time.

Vessel operating expenses decreased to $5.5 million for the first quarter of 2026 from $6.6 million in the same period of 2025. The decrease is mainly attributable to the decreased average number of vessels owned and operated in the first quarter of 2026 compared to the corresponding period in 2025.

In the first quarter of 2026, one of our vessels completed its special survey with drydock for a total cost of $0.7 million. In the first quarter of 2025 one of our vessels completed its intermediate survey in water, for a total cost of $0.1 million.

Depreciation expense for the first quarter of 2026 was $2.9 million compared to $3.2 million for the same period of 2025 as a result of the lower number of vessels owned and operated in the first quarter of 2026.

Related party management fees for the period were $1.1 million remaining at the same level compared to the same period of 2025. This was the result of the decreased number of vessels owned and operated in the first quarter of 2026, offset by the adjustment for inflation in the daily vessel management fee, effective from January 1, 2026, increasing it from 850 Euros to 875 Euros, as well as by the unfavorable movement of the euro/dollar exchange rate during the period.

General and administrative expenses were $0.9 million for the first quarter of 2026, slightly increased compared to the same period of last year.

On January 29, 2025, the Company signed an agreement to sell M/V Tasos, a 75,100 dwt drybulk vessel, built in 2000, for demolition, for approximately $5 million. The vessel was delivered to its buyers, an unaffiliated third party, on March 17, 2025, resulting in a gain on sale of $2.1 million. No case of vessel sale exists within the first quarter of 2026.

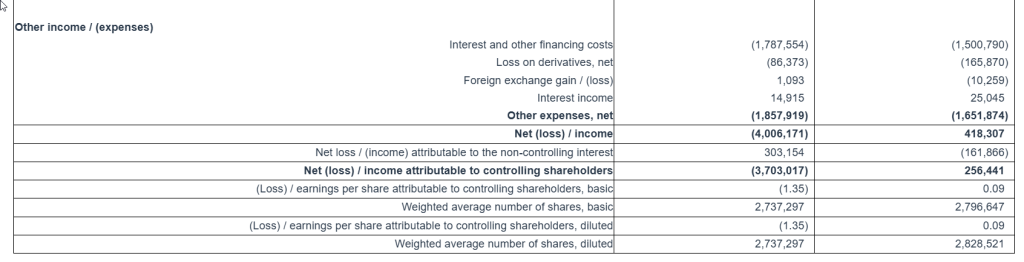

Interest and other financing costs for the first quarter of 2026 decreased to $1.5 million as compared to $1.8 million for the same period of 2025. Interest expense during the first quarter of 2026 was lower mainly due to the decreased benchmark rates of our loans and the decreased average debt during the first quarter of 2026, as compared to the same period of last year.

For the three months ended March 31, 2026, the Company recognized a $0.07 million unrealized loss and a $0.09 million realized loss on forward freight agreement contracts. For the three months ended March 31, 2025, the Company recognized a $0.13 million unrealized loss and a $0.04 million realized gain on one interest rate swap.

The Company reported a net income for the period of $0.4 million and a net income attributable to controlling shareholders of $0.3 million, as compared to a net loss of $4.0 million and a net loss attributable to controlling shareholders of $3.7 million for the same period of 2025. The net income attributable to the non-controlling interest of $0.2 million in the first quarter of 2026 represents the income attributable to the 39% ownership of the entities owning the M/V Christos K and M/V Maria represented by NRP Project Finance AS (“NRP investors”) (the “Partnership”).

Adjusted EBITDA for the first quarter of 2026 was $4.9 million compared to $(1.0) million achieved during the first quarter of 2025.

Basic and diluted earnings per share attributable to controlling shareholders for the first quarter of 2026 were $0.09, calculated on 2,796,647 and 2,828,521 basic and diluted weighted average number of shares outstanding, respectively, compared to a basic and diluted loss per share attributable to controlling shareholders of $1.35 for the first quarter of 2025, calculated on 2,737,297 basic and diluted weighted average number of shares outstanding.

Excluding the effect on the net (loss) / income attributable to controlling shareholders for the quarter of the unrealized loss on derivatives and the net gain on sale of vessel (if any), the adjusted earnings attributable to controlling shareholders for the quarter ended March 31, 2026 would have been $0.12 per share basic and diluted, compared to an adjusted loss of $2.07 per share, basic and diluted, attributable to controlling shareholders for the quarter ended March 31, 2025. Usually, security analysts do not include the above item in their published estimates of earnings per share.

Fleet Profile:

The EuroDry Ltd. fleet profile is as follows:

Note: (*) TC denotes time charter. Charter duration indicates the earliest redelivery date. (**) The entity owning the vessel is 61% owned by EuroDry and 39% by NRP Investors. (***) The average Baltic Supramax S10TC Index is an index based on ten Supramax time charter routes. (****) Gross Ballast Bonus (GBB), refers to the payments made by the charterer which serve as compensation for the ballast trip of the vessel from the last port of discharge to the delivery port.

Summary Fleet Data:

(1) Average number of vessels is the number of vessels that constituted the Company’s fleet for the relevant period, as measured by the sum of the number of calendar days each vessel was a part of the Company’s fleet during the period divided by the number of calendar days in that period.

(2) Calendar days. We define calendar days as the total number of days in a period during which each vessel in our fleet was owned by us including off-hire days associated with major repairs, drydockings or special or intermediate surveys or days of vessels in lay-up. Calendar days are an indicator of the size of our fleet over a period and affect both the amount of revenues and the amount of expenses that we record during that period.

(3) The scheduled off-hire days including vessels laid-up are days associated with scheduled repairs, drydockings or special or intermediate surveys or days of vessels in lay-up.

(4) Available days. We define available days as the total number of Calendar days in a period net of scheduled off-hire days incl. laid up. We use available days to measure the number of days in a period during which vessels were available to generate revenues.

(5) Commercial off-hire days. We define commercial off-hire days as days a vessel is idle without employment.

(6) Operational off-hire days. We define operational off-hire days as days associated with unscheduled repairs or other off-hire time related to the operation of the vessels.

(7) Voyage days. We define voyage days as the total number of days in a period during which each vessel in our fleet was in our possession net of commercial and operational off-hire days but including days our vessels were sailing for repositioning. We use voyage days to measure the number of days in a period during which vessels actually generate revenues or are sailing for repositioning purposes.

(8) Fleet utilization. We calculate fleet utilization by dividing the number of our voyage days during a period by the number of our available days during that period. We use fleet utilization to measure a company’s efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons such as unscheduled repairs or days waiting to find employment.

(9) Fleet utilization, commercial. We calculate commercial fleet utilization by dividing our available days net of commercial off-hire days during a period by our available days during that period.

(10) Fleet utilization, operational. We calculate operational fleet utilization by dividing our available days net of operational off-hire days during a period by our available days during that period.

(11) Average time charter equivalent rate, or average TCE, is a measure of the average daily net revenue performance of our vessels. Our method of calculating average TCE is determined by dividing time charter revenue and voyage charter revenue, if any, net of voyage expenses by voyage days for the relevant time period. Voyage expenses primarily consist of port, canal and fuel costs that are unique to a particular voyage, which would otherwise be paid by the charterer under a time charter contract or are related to repositioning the vessel for the next charter. Average TCE provides additional meaningful information in conjunction with time charter revenue and voyage charter revenue, if any, the most directly comparable GAAP measure, because it assists our management in making decisions regarding the deployment and use of our vessels and because we believe that it provides useful information to investors regarding our financial performance. Average TCE is a standard shipping industry performance measure used primarily to compare period-to-period changes in a shipping company’s performance despite changes in the mix of charter types (i.e., spot voyage charters, time charters, pool agreements and bareboat charters) under which the vessels may be employed between the periods. Our definition of average TCE may not be comparable to that used by other companies in the shipping industry.

(12) We calculate daily vessel operating expenses, which include crew costs, provisions, deck and engine stores, lubricating oil, insurance, maintenance and repairs and related party management fees by dividing vessel operating expenses and related party management fees by fleet calendar days for the relevant time period. Drydocking expenses are reported separately.

(13) Daily general and administrative expense is calculated by us by dividing general and administrative expenses by fleet calendar days for the relevant time period.

(14) Total vessel operating expenses, or TVOE, is a measure of our total expenses associated with operating our vessels. We compute TVOE as the sum of vessel operating expenses, related party management fees and general and administrative expenses; drydocking expenses are not included. Daily TVOE is calculated by dividing TVOE by fleet calendar days for the relevant time period.

(15) Daily drydocking expenses is calculated by us by dividing drydocking expenses by the fleet calendar days for the relevant period. Drydocking expenses include expenses during drydockings that would have been capitalized and amortized under the deferral method. Drydocking expenses could vary substantially from period to period depending on how many vessels underwent drydocking during the period. The Company expenses drydocking expenses as incurred.

Conference Call and Webcast: Today, May 20, 2026 at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13760747. Click here for additional participant International Toll -Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2026, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Operations (All amounts expressed in U.S. Dollars – except number of shares)

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Operations (All amounts expressed in U.S. Dollars – except number of shares)

EuroDry Ltd. Unaudited Consolidated Condensed Statements of Cash Flows (All amounts expressed in U.S. Dollars)

EuroDry Ltd. Reconciliation of Net (loss) / income to Adjusted EBITDA (All amounts expressed in U.S. Dollars)

Adjusted EBITDA Reconciliation: EuroDry Ltd. considers Adjusted EBITDA to represent net (loss) / income before interest and other financing costs, income taxes, vessel depreciation, unrealized loss on Forward Freight Agreements (“FFAs”), loss on interest rate swap derivative and net gain on sale of vessel. Adjusted EBITDA does not represent and should not be considered as an alternative to net loss, as determined by United States generally accepted accounting principles, or GAAP. Adjusted EBITDA is included herein because it is a basis upon which the Company assesses its financial performance because the Company believes that this non-GAAP financial measure assists our management and investors by increasing the comparability of our performance from period to period by excluding the potentially disparate effects between periods of, financial costs, unrealized loss on FFAs, loss on interest rate swap derivative, vessel depreciation and net gain on sale of vessel. The Company’s definition of Adjusted EBITDA may not be the same as that used by other companies in the shipping or other industries.

EuroDry Ltd. Reconciliation of Net (loss) / income attributable to controlling shareholders to Adjusted net (loss) / income attributable to controlling shareholders (All amounts expressed in U.S. Dollars – except share data and number of shares)

Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders Reconciliation:

EuroDry Ltd. considers Adjusted net (loss) / income attributable to controlling shareholders, to represent net (loss) / income before unrealized loss on derivatives, which includes FFAs and interest rate swaps, and net gain on sale of vessel. Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders is included herein because we believe they assist our management and investors by increasing the comparability of the Company’s fundamental performance from period to period by excluding the potentially disparate effects between periods of the abovementioned items, which may significantly affect results of operations between periods.

Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders do not represent and should not be considered as an alternative to net (loss) / income attributable to controlling shareholders or (loss) / earnings per share attributable to controlling shareholders, as determined by GAAP. The Company’s definition of Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders may not be the same as that used by other companies in the shipping or other industries. Adjusted net (loss) / income attributable to controlling shareholders and Adjusted (loss) / earnings per share attributable to controlling shareholders are not adjusted for all non-cash income and expense items that are reflected in our statement of cash flows.

About EuroDry Ltd. EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun-off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 12 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027 and the delivery of the two Kamsarmax vessels in 2028, the Company’s fleet will consist of 15 vessels with a total carrying capacity of 1,050,420 dwt.

Forward Looking Statement This press release contains forward-looking statements (as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended) concerning future events and the Company’s growth strategy and measures to implement such strategy; including expected vessel acquisitions and entering into further time charters. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of the Company. Actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially include, but are not limited to changes in the demand for dry bulk vessels, competitive factors in the market in which the Company operates; risks associated with operations outside the United States; and other factors listed from time to time in the Company’s filings with the Securities and Exchange Commission. The Company expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

ATHENS, Greece, May 18, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the first quarter ended March 31, 2026, on May 20, 2026 before market opens in New York.

On the same day, Wednesday, May 20, 2026, at 9:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13760747. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

Audio Webcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the first quarter ended March 31, 2026, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

AboutEuroDryLtd. EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd into a separate listed public company. EuroDry was spun-off from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 12 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027, the Company’s fleet will consist of 13 vessels with a total carrying capacity of 893,420 dwt.

Investor Relations /Financial Media Nicolas Bornozis Markella Kara Capital Link, Inc. 230 Park Avenue, Suite 1540 New York, NY 10169 Tel. (212) 661-7566 E-mail: [email protected]

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and full year results. EuroDry reported fourth-quarter net revenues of $17.4 million, exceeding our estimate of $16.5 million, driven by a stronger average TCE rate of $16,262 per day versus our $15,900 estimate and lighter drydocking of 13.7 days against our 22-day assumption. Adjusted EBITDA of $7.5 million and adjusted EPS of $0.88 came in ahead of our estimates of $6.7 million and $0.78, respectively. For the full year, net revenues of $52.3 million, adjusted EBITDA of $12.5 million, and an adjusted net loss of $2.50 per share all modestly surpassed our estimates of $51.4 million, $11.7 million, and a loss of $2.57.

Market update. Dry-bulk fundamentals strengthened in the fourth quarter, with average TCE rates rising to the highest levels in approximately two years. The global order book remains near historically low levels, at approximately 13.4% of the existing fleet, providing structural support. Near-term demand tailwinds include growing bauxite trade from West Africa, continued grain flows following the U.S.–China trade truce, and longer voyage distances due to Red Sea disruptions, though geopolitical uncertainty and tariff-related volatility remain risks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

ATHENS, Greece, Feb. 18, 2026 (GLOBE NEWSWIRE) — EuroDry Ltd. (NASDAQ: EDRY, the “Company” or “EuroDry”), an owner and operator of drybulk vessels and provider of seaborne transportation for drybulk cargoes, announced today that it will release its financial results for the fourth quarter ended December 31, 2025, on Thursday, February 19, 2026 after market closes in New York.

On the next day, Friday, February 20, 2026, at 8:00 a.m. Eastern Time, the Company’s management will host a conference call and webcast to discuss the results.

ConferenceCalldetails: Participants should dial into the call 10 minutes before the scheduled time using the following numbers: 877 405 1226 (US Toll-Free Dial In) or +1 201 689 7823 (US and Standard International Dial In). Please quote “EuroDry” to the operator and/or conference ID 13758897. Click here for additional participant International Toll-Free access numbers.

Alternatively, participants can register for the call using the call me option for a faster connection to join the conference call. You can enter your phone number and let the system call you right away. Click here for the call me option.

AudioWebcast-SlidesPresentation: There will be a live and then archived webcast of the conference call and accompanying slides, available on the Company’s website. To listen to the archived audio file, visit our website http://www.eurodry.gr and click on Company Presentations under our Investor Relations page. Participants to the live webcast should register on the website approximately 10 minutes prior to the start of the webcast.

The slide presentation for the fourth quarter ended December 31, 2025, will also be available in PDF format 10 minutes prior to the conference call and webcast, accessible on the company’s website (www.eurodry.gr) on the webcast page. Participants to the webcast can download the PDF presentation.

About EuroDryLtd. EuroDry Ltd. was formed on January 8, 2018, under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spunoff from Euroseas Ltd on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY.

EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day-to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

The Company has a fleet of 11 vessels, including 3 Panamax drybulk carriers, 5 Ultramax drybulk carriers, 2 Kamsarmax drybulk carriers and 1 Supramax drybulk carrier. EuroDry’s 11 drybulk carriers have a total cargo capacity of 766,420 dwt. After the delivery of two Ultramax vessels in 2027, the Company’s fleet will consist of 13 vessels with a total carrying capacity of 893,420 dwt.

InvestorRelations/FinancialMedia Nicolas Bornozis Markella Kara Capital Link, Inc. 230 Park Avenue, Suite 1540 New York, NY 10169 Tel. (212) 661-7566 E-mail: [email protected]

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Increasing FY 2026 estimates. We have increased our FY 2026 revenue, adjusted EBITDA, and adjusted EPS estimates to $60.8 million, $25.5 million, and $2.82, respectively, from $57.3 million, $22.4 million, and $1.46. The upward revisions are driven by higher expected vessel earnings, with our forecast average TCE rate rising to $14,743 from $13,873 previously.

Eurodry’s sweet spot. Eurodry owns and operates vessels in the middle of the size range of dry bulk carriers, or 50,000 to 85,000 dead weight tons (dwt), which present the most flexible employment opportunities. EDRY’s fleet consists of 11 vessels with a total carrying capacity of 766,420 dwt. With two Ultramax vessels of 63,500 dwt each under construction and scheduled for delivery in the second and third quarters of 2027, the total carrying capacity will increase to 893,000 dwt. Growth will be driven by the charter rate environment, coupled with fleet growth. While EDRY continues to renew and modernize its fleet, it expects to acquire and consolidate smaller owners.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Third quarter financial results. EuroDry reported third quarter 2025 revenues of $15.3 million, in line with expectations of $15.1 million and down slightly from $15.8 million last year due to a smaller fleet. Adjusted EBITDA improved sharply to $4.1 million, up from $0.5 million in Q3 2024, due to lower expenses and stronger utilization. The company operated an average of 12 vessels at a TCE of $13,232/day, modestly above $13,105/day in the prior-year period. Adjusted net loss narrowed to $0.6 million, or $(0.23)/share, compared to a loss of $3.9 million, or $(1.42)/share, last year.

Market outlook. Management indicated that dry-bulk fundamentals continued to strengthen through Q3, supported by improving Chinese import activity, firmer demand across key cargo segments, and increased ton-mile requirements. Limited fleet growth and a historically low orderbook continue to support a tightening supply backdrop as the market moves into 2026. We expect Q4 results to capture more of the recent improvement as earlier charters roll off, though geopolitical uncertainty remains a risk to global trade flows.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter financial results. EuroDry generated Q2 net revenues of $11.3 million, in line with our $11.4 million estimate but down about $6 million year-over-year due to a decline in average time charter equivalent (TCE) rates. Adjusted EBITDA of $1.9 million and a loss per share of $1.10 per share were better than our forecasts of $1.6 million and a loss of $1.23 per share, aided by lower voyage expenses, but trailed last year’s $5.0 million and $0.17 loss.

Market Outlook. The dry-bulk market saw a brief improvement in the second quarter as rates recovered from early-year lows, though momentum slowed later in the period amid trade policy developments and softer Chinese import activity. However, since the start of the third quarter, rates have improved, and the IMF slightly raised its 2025 global GDP guidance. Red Sea disruptions have continued to extend voyage distances, and demand has picked up slightly based on improved sentiment toward growth in China. The orderbook remains near historical lows, so while rates hover below 2024 levels, we expect the recent improvement to hold for the remainder of the year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Second quarter estimates. We are lowering our Q2 2025 revenue and adjusted earnings per share estimates to $11.4 million and a loss of $1.23, respectively, from $14.1 million and a loss of $0.76. Additionally, we are reducing our operating expenses to $13.0 million from $14.4 million, as dry docking expenses have been pushed into the third quarter. Despite lower operating expenses, we are decreasing our adjusted EBITDA estimate to $1.6 million from $2.9 million. The decrease in our earnings estimates is mainly due to lower-than-expected time charter equivalent (TCE) rates.

Full-Year 2025 estimates. We are lowering our 2025 revenue and adjusted earnings per share estimates to $46.0 million and a loss of $4.41, respectively, from $50.3 million and a loss of $3.79. We are trimming our operating expenses to $51.4 million from $51.8 million, due to lower expected voyage expenses. Our adjusted EBITDA estimates were lowered to $5.6 million from $9.3 million. The lower estimates are driven by soft market rates.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter financial results. Eurodry Ltd. reported an adjusted first quarter net loss of $5.7 million, or ($2.07) per share, compared to a loss of $3.2 million, or ($1.18) per share, during the same period last year. Adjusted EBITDA came in at a loss of $1.0 million, down from a gain of $2.1 million during the first quarter of last year. While revenue was slightly above our expectations, operating expenses were approximately $2.0 million higher than estimated due to increased repair costs. Overall, the quarterly results reflected the ongoing market challenges as charter rates remain near five-year lows due to challenging supply and demand trends.

Updating 2025 estimates. Based on the lower-than-expected first quarter results and management’s outlook, we are lowering our full year 2025 adjusted EBITDA and earnings per share (EPS) estimates to $9.3 million and ($3.79), respectively, down from $19.6 million and ($0.43). While we expect the second quarter to show a slight rebound, the weak market conditions are expected to persist and could constrain rates through the balance of the year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter financial results. EuroDry Ltd. reported an adjusted fourth-quarter net loss to controlling shareholders of $0.7 million, or ($0.25) per share, compared to adjusted net income of $1.9 million, or $0.70 per share, during the prior year period. Adjusted EBITDA declined to $4.8 million compared to $6.6 million during the prior year period. The year-over-year decline is due to low market rates as trade volume has fallen amid a slowdown in the Chinese economy.

Full year 2024 earnings and updated 2025 estimates. For the full year 2024, adjusted EBITDA and earnings per share declined to $12.4 million and ($3.02), respectively, from $14.6 million and $0.12 in 2023. We have lowered our 2025 adjusted EBITDA and EPS estimates to $19.6 million and ($0.43), respectively, from $22.0 million and ($0.34). While we expect spot and one-year time charter equivalent rates to improve throughout the year, our estimates have been lowered compared to our previous expectations due to weak market conditions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.