Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Another profitable quarter. Q2 revenue of $49.6 million exceeded the midpoint of guidance, while adjusted EBITDA of $6.7 million exceeded the high end and marked the company’s 11th consecutive quarter of positive adjusted EBITDA. While revenues were in line, the company exceeded our $4.5 million adj. EBITDA estimate.

Retail traction encouraging. Shakeology distribution expanded to 131 Sprouts stores, with early reorders supporting favorable sell-through, while the company recently launched in 481 Vitamin Shoppe locations. Approximately 12 additional retail decisions are expected between mid-September and late November.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 exceeded expectations. Revenue of $115.4 million and Adjusted EBITDA of $24.8 million were within management’s guidance, while Digital Advertising accelerated to 11% year-over-year growth,driven by continued strength in programmatic advertising, owned-and-operated digital properties, and Media Partnerships.

Digital transformation gaining traction. Townsquare’s Digital First strategy continues to differentiate the company from traditional radio peers. During the first half of 2026, digital businesses generated 57% of total revenue and 59% of total segment profit, while the Media Partnerships platform expanded to 16 partners, creating a scalable, capital-light growth opportunity beyond the company’s owned markets.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CULVER CITY, Calif., Aug. 06, 2026 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail Games” or the “Company”), a leading global independent developer and publisher of interactive digital entertainment, will hold a conference call and webcast on Tuesday, August 11, 2026 at 4:30 p.m. Eastern time (1:30 p.m. Pacific time) to discuss its financial results for the second quarter ended June 30, 2026.

Snail Games management will host the conference call and webcast, followed by a question-and-answer period. Participants may listen to the live webcast and replay via the link here or on the Company’s investor relations website at https://investor.snail.com/.

About Snail, Inc. Snail, Inc. (Nasdaq: SNAL) is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs, and mobile devices. For more information, please visit: https://snail.com/.

Investor Contact: John Yi and Steven Shinmachi Gateway Group, Inc. 949-574-3860 [email protected]

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

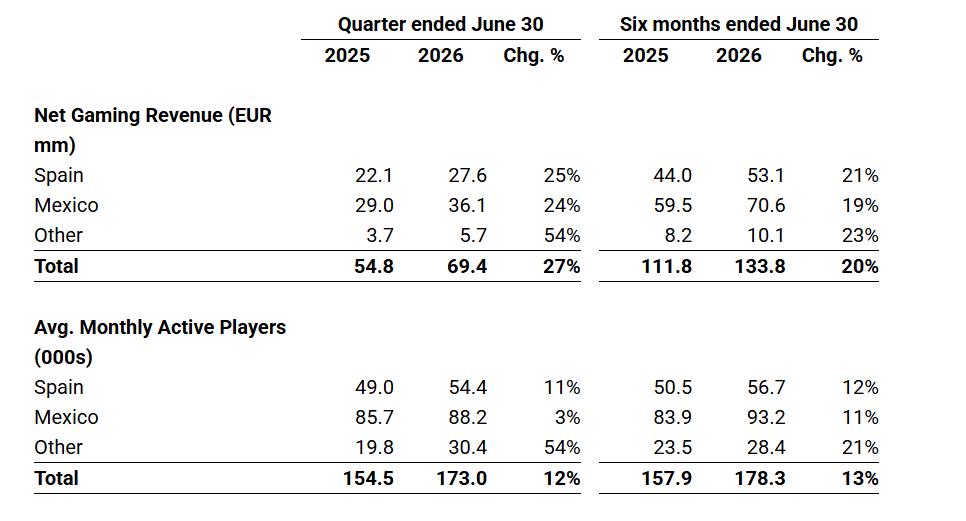

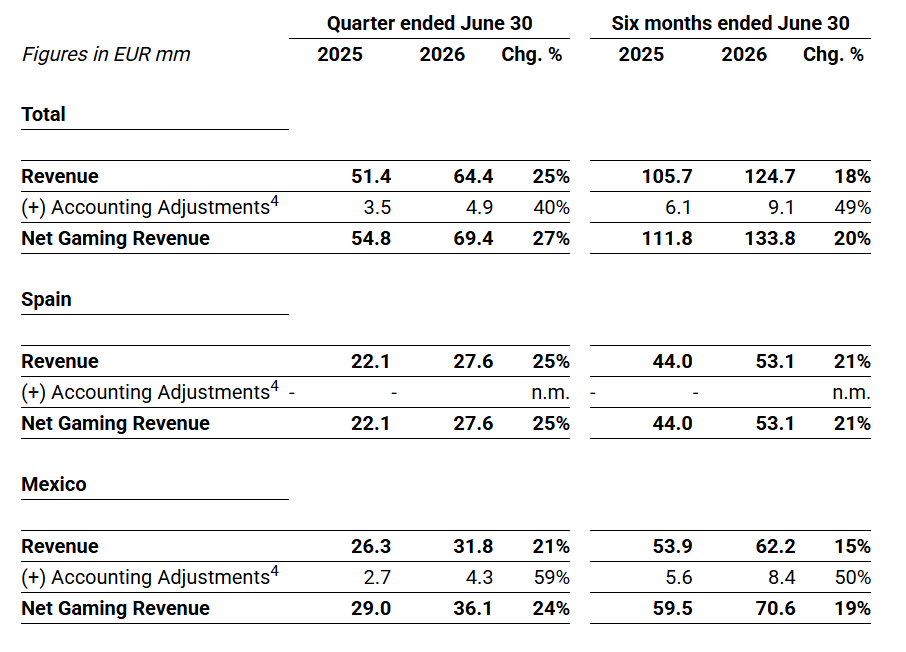

Strong Quarter Across Core Markets. Codere Online reported Q2 net gaming revenue of €69.4 million, up 27% year over year and above our €60.0 million estimate, driven by robust performance in both Spain (+25%) and Mexico (+24%). Active customers increased 12%, while average monthly spend per active customer rose 13%, demonstrating healthy customer engagement and monetization.

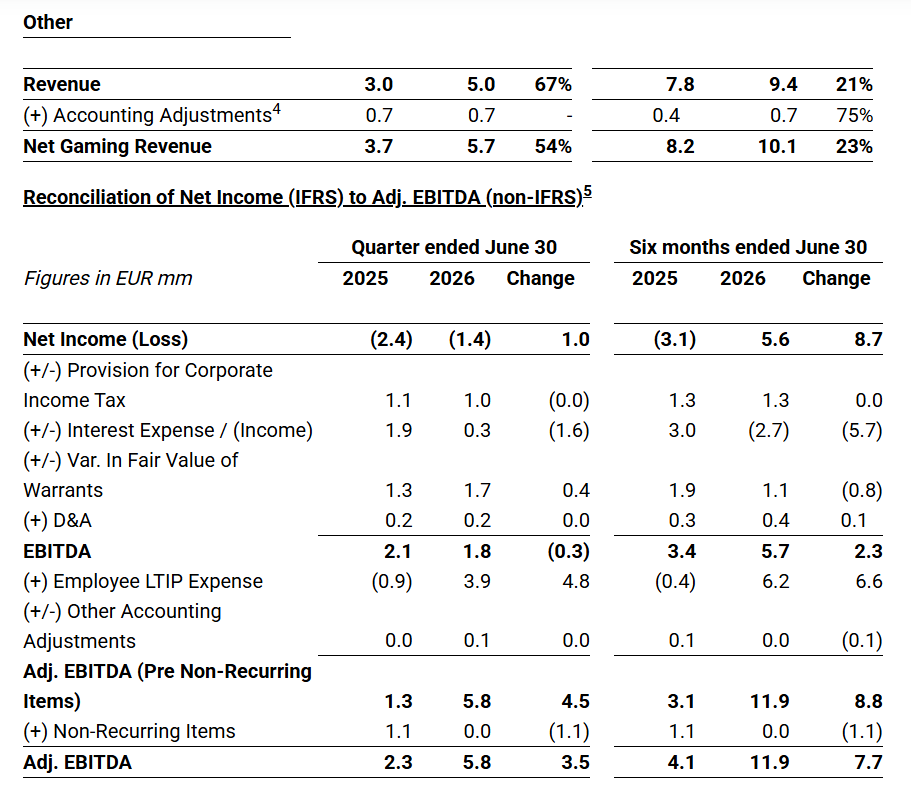

Profitability Continues to Improve. Adjusted EBITDA increased to €5.8 million, better than our €2.5 million estimate and €2.3 million in the prior-year period, reflecting improved marketing efficiency and operating leverage. Adjusted EBITDA margin expanded to 8.4% from 4.3% a year ago, highlighting the scalability of the company’s platform.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

George Proost, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q2 Results. The company achieved its highest quarterly revenue to date of €69.4 million, up 27% year over year and nearly 16% above our estimate of €60 million, as illustrated in Figure #1 Q2 Results. Reported adj. EBITDA of €5.8 million also beat our estimate of €2.5 million, driven primarily by exceptional World Cup engagement and robust performance in its core markets of Spain and Mexico.

World Cup Success. The company delivered strong performance around the World Cup. Total stakes during the event reached approximately €63 million, a 180% increase over the 2022 tournament’s levels. Additionally, the company acquired around 40,000 new customers during the event, with a 56% increase in unique users.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

BOCA RATON, FL / ACCESS Newswire / July 30, 2026 / Newsmax Inc. (NYSE:NMAX) (“Newsmax” or the “Company”) today announced that the Company will report financial results for the second quarter ended June 30, 2026 on Thursday, August 13, 2026, after the U.S. stock market closes.

Management will host a conference call at 4:30 PM ET the same day to discuss the results. The live webcast and replay will be available on the Newsmax Investor Relations website at ir.newsmax.com.

About Newsmax

Newsmax Inc. is listed on the NYSE (NMAX) and operates, through Newsmax Broadcasting LLC, one of the nation’s leading news outlets, the Newsmax channel. The fourth highest-rated network is carried on all major pay TV providers. Newsmax’s media properties reach more than 50 million Americans regularly through Newsmax TV, the Newsmax App, its popular website Newsmax.com, and publications such as Newsmax Magazine. Through its social media accounts, Newsmax reaches over 26 million combined followers. Reuters Institute says Newsmax is one of the top U.S. news brands and Forbes has called Newsmax “a news powerhouse.”

The Company once again delivered record quarterly net gaming revenue of €69.4 million and Adj. EBITDA of €5.8 million

Total revenue was €64.4 mm in Q2 2026, while net gaming revenue1 was €69.4 mm, 27% above Q2 2025.

Spain revenue and net gaming revenue were €27.6 mm in Q2 2026, 25% above Q2 2025.

Mexico revenue was €31.8 mm in Q2 2026, while net gaming revenue was €36.1 mm, 24% above Q2 2025.

Adj. EBITDA reached €5.8 mm in Q2 2026, €3.5 mm above Q2 2025.

Net income was €5.6 mm in H1 2026 versus a net loss of €3.1 mm in H1 2025.

Total cash position of €62.6 mm and no financial debt as of June 30, 2026.

Increasing FY 2026 outlook of net gaming revenue to €255-265 mm and Adj. EBITDA2 to €20-25 mm.

Madrid, Spain and Tel Aviv, Israel, July 30, 2026 – (GLOBE NEWSWIRE) Codere Online (Nasdaq: CDRO / CDROW, the “Company”), a leading online gaming operator in Spain and Latin America, has released its preliminary unaudited3 financial results for the quarter ended June 30, 2026.

Below are the main financial and operating metrics of the period.

Aviv Sher, Chief Executive Officer of Codere Online, commented, “After a strong start to the year, Q2 showed even further acceleration and delivered our strongest quarterly performance to date. Net gaming revenue in the second quarter reached approximately €69 million, up 27% year-on-year, with the World Cup providing an additional boost to customer activity and engagement. This performance was broad-based across our core markets and we are very pleased with the momentum we are seeing in the business.”

Marcus Arildsson, CFO of Codere Online, commented, “Q2 represented another major step forward in our financial performance, with net gaming revenue being around €15 million above the prior-year period, and Adjusted EBITDA of approximately €6 million, more than doubling compared to Q2 2025. This strong profitability was achieved while continuing to invest behind growth and taking advantage of the increased activity generated around the World Cup. We closed June with approximately €63 million of total cash and no financial debt.

Mr. Arildsson further added, “Given our record Q2 performance and the continued acceleration of the business, we are raising our outlook for the full year 2026 and now expect to generate between €255 – 265 million of net gaming revenue, which is €20 million more than the prior range and represents a growth of 16% year-on-year at the midpoint, and between €20 – 25 million of Adjusted EBITDA, €5 million above the prior range”.

Recent Events

World Cup Performance

World Cup performance has been outstanding, with results materially ahead of the 2022 tournament and underscoring the step-change in scale, engagement and monetization achieved by the Company:

Unique users were approximately 56% above World Cup 2022 levels (excluding Colombia) and we acquired nearly 40 thousand new customers just around the event;

Stakes reached 63 million euros, 180% above World Cup 2022 levels, demonstrating the significantly greater scale of the business and strong customer activity around the event;

Net gaming revenue more than doubled World Cup 2022 levels, reflecting strong monetization of the increased betting volumes despite generally favorable customer results (i.e. relatively low sports betting margin).

Conference Call Information

Codere Online’s management will host a conference call to discuss the results and provide a business update at 8:30 am US Eastern Time today, July 30, 2026. Access links to the audio webcast and presentation will be accessible on Codere Online’s website at www.codereonline.com. A recording of the webcast will also be available following the conference call.

Reconciliation of Revenue (IFRS) to Net Gaming Revenue (non-IFRS)

About Codere Online

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online, launched in 2014 as part of the renowned casino operator Codere Group, offers online sports betting and online casino through its state-of-the art website and mobile applications. Codere Online currently operates in its core markets of Spain, Mexico, Colombia, Panama and Argentina; this online business is complemented by Codere Group’s physical presence in Spain and throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence.

About Codere Group Codere Group is a multinational group dedicated to entertainment and leisure. It is a leading player in the private gaming industry, with four decades of experience and with presence in seven countries in Europe (Spain and Italy) and Latin America (Argentina, Colombia, Mexico, Panama, and Uruguay).

Note on Rounding. Due to decimal rounding, numbers presented throughout this report may not add up precisely to the totals and subtotals provided, and percentages may not precisely reflect the absolute figures.

Forward-Looking Statements Certain statements in this document may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements regarding Codere Online Luxembourg, S.A. and its subsidiaries (collectively, “Codere Online”) or Codere Online’s or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this document may include, for example, statements about Codere Online’s financial performance and, in particular, the potential evolution and distribution of its net gaming revenue; any prospective and illustrative financial information; and changes in Codere Online’s strategy, future operations and target addressable market, financial position, estimated revenues and losses, projected costs, prospects and plans.

These forward-looking statements are based on information available as of the date of this document and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Codere Online’s or its management team’s views as of any subsequent date, and Codere Online does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, Codere Online’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. There may be additional risks that Codere Online does not presently know or that Codere Online currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Some factors that could cause actual results to differ include (i) changes in applicable laws or regulations, including online gaming, privacy, data use and data protection rules and regulations as well as consumers’ heightened expectations regarding proper safeguarding of their personal information, (ii) the impacts and ongoing uncertainties created by regulatory restrictions, changes in perceptions of the gaming industry, changes in policies and increased competition, and geopolitical events such as war, (iii) the ability to implement business plans, forecasts, and other expectations and identify and realize additional opportunities, (iv) the risk of downturns and the possibility of rapid change in the highly competitive industry in which Codere Online operates, (v) the risk that Codere Online and its current and future collaborators are unable to successfully develop and commercialize Codere Online’s services, or experience significant delays in doing so, (vi) the risk that Codere Online may never achieve or sustain profitability, (vii) the risk that Codere Online will need to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all, (viii) the risk that Codere Online experiences difficulties in managing its growth and expanding operations, (ix) the risk that third-party providers, including the Codere Group, are not able to fully and timely meet their obligations, (x) the risk that the online gaming operations will not provide the expected benefits due to, among other things, the inability to obtain or maintain online gaming licenses in the anticipated time frame or at all, (xi) the risk that Codere Online is unable to secure or protect its intellectual property, (xii) the risk that Codere Online’s securities may be delisted from Nasdaq and (xiii) the possibility that Codere Online may be adversely affected by other political, economic, business, and/or competitive factors. Additional information concerning certain of these and other risk factors is contained in Codere Online’s filings with the U.S. Securities and Exchange Commission (the “SEC”). All subsequent written and oral forward-looking statements concerning Codere Online or other matters and attributable to Codere Online or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements above.

Financial Information and Non-GAAP Financial Measures Codere Online’s financial statements are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), which can differ in certain significant respects from generally accepted accounting principles in the United States of America (“U.S. GAAP”).

This document includes certain financial measures not presented in accordance with U.S. GAAP or IFRS (“non-GAAP”), such as, without limitation, net gaming revenue, Adjusted EBITDA and constant currency information. These non-GAAP financial measures are not measures of financial performance in accordance with U.S. GAAP or IFRS and may exclude items that are significant in understanding and assessing Codere Online’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to revenue, net income, cash flows from operations or other measures of profitability, liquidity or performance under U.S. GAAP or IFRS. You should be aware that Codere Online’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. In addition, the audit of Codere Online’s financial statements in accordance with PCAOB standards, may impact how Codere Online currently calculates its non-GAAP financial measures, and we cannot assure you that there would not be differences, and such differences could be material.

Codere Online believes that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in comparing Codere Online’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Reconciliations of non-GAAP financial measures to their most directly comparable measure under IFRS are included herein.

This document may include certain projections of non-GAAP financial measures. Codere Online is unable to quantify certain amounts that would be required to be included in the most directly comparable U.S. GAAP or IFRS financial measures without unreasonable effort, due to the inherent difficulty and variability of accurately forecasting the occurrence and financial impact of the various adjusting items necessary for such comparable measures or such reconciliation that have not yet occurred, are out of our control, or cannot be reasonably predicted, ascertained or assessed, which could have a material impact on its future IFRS financial results. Consequently, no disclosure of estimated comparable U.S. GAAP or IFRS measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included.

Use of Projections This document contains financial forecasts with respect to Codere Online’s business and projected financial results, including net gaming revenue and adjusted EBITDA. Codere Online’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this document, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this document. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Codere Online or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this document should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

For further information on the limitations and assumptions underlying these projections, please refer to Codere Online’s filings with the SEC.

Preliminary Information This document contains figures, financial metrics, statistics and other information that is preliminary and subject to change (the “Preliminary Information”). The Preliminary Information has not been audited, reviewed, or compiled by any independent registered public accounting firm. This Preliminary Information is subject to ongoing review including, where applicable, by Codere Online’s independent auditors. Accordingly, no independent registered public accounting firm has expressed an opinion or any other form of assurance with respect to the Preliminary Information. During the course of finalizing such Preliminary Information, adjustments to such Preliminary Information presented herein may be identified, which may be material. Codere Online undertakes no obligation to update or revise the Preliminary Information set forth in this document as a result of new information, future events or otherwise, except as otherwise required by law. The Preliminary Information may differ from actual results. Therefore, you should not place undue reliance upon this Preliminary Information. The Preliminary Information is not a comprehensive statement of financial results, and should not be viewed as a substitute for full financial statements prepared in accordance with IFRS. In addition, the Preliminary Information is not necessarily indicative of the results to be achieved in any future period.

No Offer or Solicitation This document does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor will there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended, or an exemption therefrom.

Industry and Market Data In this document, Codere Online relies on and refers to certain information and statistics obtained from publicly available information and third-party sources, which it believes to be reliable. Codere Online has not independently verified the accuracy or completeness of any such publicly-available and third-party information, does not make any representation as to the accuracy or completeness of such data and does not undertake any obligation to update such data after the date of this document. You are cautioned not to give undue weight to such industry and market data.

Contacts:

Investors and Media Guillermo Lancha Director, Investor Relations and Communications [email protected] (+34) 628.928.152

1 Net Gaming Revenue is a non-IFRS measure; please see reconciliation of Net Gaming Revenue to Revenue at the end of the report.

2 Adjusted EBITDA is a non-IFRS measure; please see reconciliation of Adjusted EBITDA to Net Income at the end of the report. Net gaming revenue and Adjusted EBITDA outlooks are forward-looking non-IFRS measures; please see important disclaimers at the end of the report. 3 See “Preliminary Information” below.

4 Figures primarily reflect differences in recognition of revenue related to certain partner and affiliate agreements in place in Colombia, VAT impact from service fees in Mexico and the impact from the application of inflation accounting (IAS 29) in Argentina. 5 Please refer to page 23 of our Q2 2026 Earnings Presentation for further details regarding this reconciliation.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Governance Structure Simplified. Alliance Entertainment has amended its Certificate of Incorporation to eliminate the voting rights of its Class E common stock, leaving Class A common stockholders with exclusive voting control while preserving the Class E shares’ economic conversion rights. We view the amendment as a meaningful simplification of the company’s capital structure that should improve governance transparency.

Economic Interests Remain Unchanged. Importantly, the amendment does not affect the economic value of the Class E shares. The shares remain convertible into Class A stock upon specified triggering events and continue to participate economically on an as-converted basis, indicating that the amendment is purely a governance enhancement rather than a dilution event.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

BOCA RATON, FL / ACCESS Newswire / July 28, 2026 / Newsmax Inc. (NYSE:NMAX) (“Newsmax” or the “Company”) announced today that the Company has entered into an AI content partnership with Meta Platforms (“Meta”).

Under the agreement, Meta will have access to Newsmax’s digital news content. Meta will be able to draw upon Newsmax’s significant current reporting as well as archived content across its platforms to support AI queries across Meta’s apps and devices.

“Newsmax applauds the significant resources Meta is putting into AI to keep America at the forefront of this emerging technology,” commented Chris Ruddy, CEO of Newsmax. “We are pleased to work with Meta to help ensure users have access to timely, high-quality journalism through AI technologies.”

Newsmax views this agreement as an important step in its broader strategy to work with leading technology companies, expand the reach of its journalism and make the Company’s distinctive perspective available through emerging AI technologies.

About Newsmax

Newsmax Inc. is listed on the NYSE (NMAX) and operates, through Newsmax Broadcasting LLC, one of the nation’s leading news outlets, the Newsmax channel. The fourth highest-rated network is carried on all major pay TV providers. Newsmax’s media properties reach more than 50 million Americans regularly through Newsmax TV, the Newsmax App, its popular website Newsmax.com, and publications such as Newsmax Magazine. Through its social media accounts, Newsmax reaches over 26 million combined followers. Reuters Institute has said Newsmax is one of the top U.S. news brands and Forbes has called Newsmax “a news powerhouse.”

This press release contains forward-looking statements, including statements regarding expected international revenue growth, anticipated partner launches, advertising and licensing opportunities, distribution expansion, geographic growth, future business performance, timing of localized channel launches, partner performance, and anticipated benefits of international distribution and licensing arrangements. Forward-looking statements are based on current expectations and assumptions and are subject to risks and uncertainties that could cause actual results to differ materially, including delays or changes in partner launches, failure of partners to launch or operate localized channels as expected, termination or modification of agreements, lower-than-expected advertising demand, changes in distribution arrangements, foreign currency fluctuations, regulatory, political and geopolitical risks, local market conditions, competitive conditions, revenue recognition timing, collection risk, and the other risks described in the Company’s filings with the SEC. The Company undertakes no obligation to update forward-looking statements except as required by law.

NEW YORK, July 28, 2026 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO):

Revenue of $23.2 million, down 3% year-over-year

Consolidated operating loss of $2.8 million

Non-GAAP consolidated operating loss of $2.1 million

Cash flow from operations of $(1.7) million

Earnings per share (EPS) of $(0.21)

Travelzoo, the club for travel enthusiasts, today announced financial results for the second quarter ended June 30, 2026. Consolidated revenue was $23.2 million, down 3% from $23.9 million year-over-year. In constant currencies, revenue was $23.1 million. Travelzoo’s reported revenue consists of advertising revenues and commissions, derived from and generated in connection with purchases made by Travelzoo members, and membership fees.

During Q2, international conflicts created uncertainty among advertisers and travelers. All of Travelzoo’s business segments were negatively impacted. Management considers this a temporary effect. In Q2, we continued to invest significantly in growing Club Members and accelerated the shift towards recurring membership revenues. Marketing costs were expensed immediately. Membership fees revenue is recognized ratably over the subscription period of 12 months. In Q2, the number of renewals of memberships jumped to the highest ever. Going forward, we expect renewals of memberships to further increase because of a growing base of members. We refer to our investor presentation.

Net Loss attributable to Travelzoo was $2.1 million for Q2 2026, or $(0.21) per share, compared with $0.12 per share in the prior-year period.

Non-GAAP operating loss was $2.1 million. Non-GAAP operating loss excludes stock option expenses ($684,000). Please refer to “Non-GAAP Financial Measures” and the tabular reconciliation below.

“We will continue to leverage Travelzoo’s global reach, trusted brand, and strong relationships with top travel suppliers to negotiate more Club Offers for Club Members and add new benefits, such as our popular complimentary airport lounge access worldwide in case of a delayed flight,” said Holger Bartel, Travelzoo’s Global CEO. “Travelzoo members are affluent, active, and open to new experiences. We inspire travel enthusiasts to travel to places they never imagined they could. Travelzoo is the must-have membership for those who love to travel as much as we do.”

Travelzoo North America North America business segment revenue decreased 3% year-over-year to $15.7 million. Operating loss for Q2 2026 was $1.5 million, or 10% of revenue, compared to operating profit of $2.8 million or 17% of revenue in the prior-year period.

Travelzoo Europe Europe business segment revenue decreased 2% year-over-year to $6.2 million. Operating loss for Q2 2026 was $1.2 million, or 19% of revenue, compared to operating loss of $0.9, or 14% of revenue in the prior-year period.

Jack’s Flight Club Jack’s Flight Club is a membership subscription service in which Travelzoo has a 60% ownership interest. Revenue decreased 7% year-over-year to $1.3 million. Jack’s Flight Club’s revenue from subscriptions is recognized ratably over the subscription period (quarterly, semi-annually, annually). Operating loss for Q2 2026 was $34,000, compared to operating profit of $156,000 in the prior-year period.

New Initiatives New Initiatives business segment revenue, which includes Licensing and Travelzoo META, was $17,000. Operating loss for Q2 2026 was $35,000.

In 2020, Travelzoo entered into royalty-bearing licensing agreements with local licensees for the exclusive use of Travelzoo’s brand, business model, and members in Australia, Japan, New Zealand, and Singapore. Under these arrangements, Travelzoo’s existing members in Australia, Japan, New Zealand, and Singapore will continue to be owned by Travelzoo as the licensor. Licensing revenue from the licensee in Australia was $10,000 for Q2 2026. Licensing revenue from the licensee in Japan was $7,000 for Q2 2026. Licensing revenue is expected to increase going forward.

Reach Travelzoo reaches 30 million travelers. This includes Jack’s Flight Club. Comparisons to prior periods are no longer meaningful due to strategic developments of the Travelzoo membership.

Income Taxes The reported income tax benefit for Q2 2026 was $(382,000).

Balance Sheet As of June 30, 2026, cash, cash equivalents and restricted cash were $7.6 million. Cash flow from operations was $(1.7) million.

Deferred revenue increased because membership fees are earned over the subscription period. Membership fees revenue is recognized ratably over the subscription period.

Share Repurchase Program During Q2 2026, the Company repurchased 200,000 shares of its outstanding common stock.

Looking Ahead For Q3 2026, we expect year-over-year revenue growth. We also expect revenue growth in subsequent quarters, as membership fees revenue is recognized ratably over the subscription period of 12 months, as we grow Club Members, and as more Legacy Members become Club Members. Over time, we expect profitability to increase as recurring membership fees revenue will be recognized. In the short-term, fluctuations in reported net income are likely.

In 2024, we introduced a membership fee for Travelzoo. Legacy Members, who joined prior to 2024, continue to receive certain travel offers. However, Club Offers and new benefits are only available to Club Members, who pay the membership fee. Therefore, we are seeing many Legacy Members become Club Members over time—in addition to new members who join.

Non-GAAP Financial Measures Management calculates non-GAAP operating income when evaluating the financial performance of the business. Calculation of non-GAAP operating income, also called “non-GAAP operating profit” in this press release and today’s earnings conference call, excludes the following items: amortization of intangibles, stock option expenses, and severance-related expenses. This press release includes a table which reconciles GAAP operating income to the calculation of non-GAAP operating income. Non-GAAP operating income is not required by, or presented in accordance with, generally accepted accounting principles in the United States of America (“GAAP”). This information should be considered as supplemental in nature and should not be considered in isolation or as a substitute for the financial information prepared in accordance with GAAP. In addition, these non-GAAP financial measures may not be the same as similarly titled measures reported by other companies.

Conference Call Travelzoo will host a conference call to discuss second quarter 2026 results today at 11:00 a.m. ET. Please visit http://ir.travelzoo.com/events-presentations to

download the management presentation (PDF format) to be discussed in the conference call

access the webcast.

About Travelzoo We, Travelzoo®, are the club for travel enthusiasts. We reach 30 million travelers. Club Members receive Club Offers negotiated and rigorously vetted by our deal experts around the globe. Our relationships with thousands of top travel companies give us access to irresistible deals. Our club and its benefits are built around the lifestyle of a modern travel enthusiast.

Certain statements contained in this press release that are not historical facts may be forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities and Exchange Act of 1934. These forward-looking statements may include, but are not limited to, statements about our plans, objectives, expectations, prospects and intentions, markets in which we participate and other statements contained in this press release that are not historical facts. When used in this press release, the words “expect”, “predict”, “project”, “anticipate”, “believe”, “estimate”, “intend”, “plan”, “seek” and similar expressions are generally intended to identify forward-looking statements. Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause actual results to differ materially from those expressed or implied by these forward-looking statements, including changes in our plans, objectives, expectations, prospects and intentions and other factors discussed in our filings with the SEC. We cannot guarantee any future levels of activity, performance or achievements. Travelzoo undertakes no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this press release.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Executing a multi-year turnaround strategy. Management is focused on three strategic priorities: stabilizing local direct advertising, expanding higher-margin owned-and-operated digital products, and strengthening the balance sheet through disciplined deleveraging. We believe successful execution could materially improve the company’s earnings profile over the next several years.

Digital mix continues to improve. Digital revenue represented more than 25% of total company revenue during the first quarter of 2026, while owned-and-operated digital products increased to approximately 65% of digital revenue. We believe the improving revenue mix should support higher margins, stronger customer retention, and improved free cash flow generation over time.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

A Classic Since Always™ – From Revolutionary Pinsetters to Everyday Family Traditions

RICHMOND, Va.–(BUSINESS WIRE)– Lucky Strike Entertainment (NYSE: LUCK) today announced the launch of a refreshed identity for AMF (American Machine & Foundry), one of the most iconic names in American bowling. Rooted in AMF’s 126-year heritage, the rebrand positions the brand for the future and reflects its evolution into a modern bowling destination where families and communities come together for birthday parties, league nights, and social outings.

AMF’s refreshed shield logo marks a new chapter for an American classic.

Founded in 1900 as American Machine & Foundry, AMF helped shape modern bowling through innovations, including the automatic pinsetter and the world’s first automatic scoring system. Over the decades, the brand played a significant role in expanding bowling’s popularity across the United States and around the world, helping establish it as one of America’s most participated-in sports. Today, AMF remains a cornerstone of that legacy, welcoming approximately 10.4 million guests annually across more than 80 locations nationwide. With approximately 60 locations planned to transition to the AMF brand, Lucky Strike Entertainment is investing in the brand’s future while building on the foundation that made it an icon of the sport.

The AMF rebrand reflects Lucky Strike Entertainment’s vision to reintroduce AMF as a welcoming “house” with a refreshed identity that still honors the beloved sport. Rooted in AMF’s heritage, AMF destinations will begin to transform with bold new visuals led by Department of Branding and Design (DoBad) that lean into the brand’s ownable red, complemented by supporting tones of varsity blue, heritage white, and gold. The iconic shield logo will be updated with new lettering and bright red hues that will be reflected across digital and physical touchpoints. Consumers will be introduced to the new AMF brand platform, A Classic Since Always™, which celebrates modern bowling experiences while preserving the familiar, dependable atmosphere guests expect. Altogether, these elements position AMF as a timeless neighborhood destination designed to be the top bowling hub in neighborhoods across the country.

“This is more than a brand refresh. It’s an investment in the future of AMF,” said Thomas Shannon, Founder and CEO of Lucky Strike Entertainment. “We are building on the strength of an iconic brand and positioning it for long-term growth. As we expand the AMF brand across the country, our focus remains the same: delivering great bowling experiences, supporting league play, and providing an affordable destination for families and communities.”

Guests will begin to see the new AMF brand across digital platforms, social media, and select in-center materials, with additional updates rolling out over time. Future enhancements will include heritage walls showcasing memorabilia from AMF’s bowling legacy, along with nostalgic, varsity-inspired design elements such as swallowtail pennants and signage. While the look evolves, Lucky Strike Entertainment remains committed to AMF’s high-quality lanes, welcoming atmosphere, and experiences that bring people together, including leagues, open play, youth programs, family celebrations, and premier PBA Tour events such as the Tournament of Champions and AMF PBA World Championships. AMF also continues to offer affordable, value-driven birthday party options, with packages like Family Unlimited and the All Star Package designed to make celebrations easy, convenient, and accessible for families.

As AMF enters its next chapter, Lucky Strike Entertainment remains focused on elevating the traditional neighborhood bowling center, rooted in heritage, shaped by the local community, and designed to create moments of connection for generations to come.

For more information on AMF and AMF locations near you, please visit AMF.com and follow AMF on Instagram, and Facebook.

About Lucky Strike Entertainment

Lucky Strike Entertainment is one of the world’s premier location-based entertainment platforms. With over 360 locations across North America, Lucky Strike Entertainment provides experiential offerings in bowling, amusements, water parks, and family entertainment centers. The company also owns the Professional Bowlers Association, the major league of bowling and a growing media property that boasts millions of fans around the globe. For more information on Lucky Strike Entertainment, please visit LuckyStrikeEnt.com.

Netflix dropped 11% at the open Friday, erasing roughly $100 billion in market value in a single session. The trigger was not a collapse in the business. It was a third-quarter revenue guidance figure of $12.86 billion that came in approximately $140 million below what Wall Street had been expecting. To put that in proportion, the guidance miss that wiped out $100 billion in shareholder value represented barely 1% of the number analysts had modeled.

The second-quarter results themselves were solid by any conventional standard. Revenue grew 13.4% year over year to $12.56 billion. Earnings per share of $0.80 beat the $0.79 consensus estimate. Net income reached $3.4 billion. Subscribers streamed more than 97 billion hours of content in the first half of 2026, up nearly 2% from the prior year. The advertising business is on track to generate approximately $3 billion in full-year revenue, nearly double last year’s figure.

None of it mattered. The stock opened at its lowest level in over a year, down 46% from its 52-week high, trading at roughly 18 times forward earnings with a PEG ratio below 1.0. By most traditional valuation frameworks, Netflix now looks undervalued relative to its growth rate. The market does not care. It is punishing the guidance, not the business.

The Pattern That Should Concern Every Large Cap Investor

This is now the second time in 48 hours that a dominant technology company has posted strong results and been met with aggressive selling. Earlier this week, TSMC reported 77% annual earnings growth and fell 4%. Broadcom beat estimates last month and dropped 15%. SK Hynix debuted on Nasdaq with a 13% pop and gave it all back the next day.

The common thread connecting all of these moves is not deteriorating fundamentals. It is elevated expectations meeting reality. When stocks are priced for perfection across an entire sector, even slight misses on forward guidance trigger outsized reactions because the margin for error has been completely compressed out of the valuation. Netflix guided Q3 revenue 1% below consensus and lost 11%. That math only works when the stock was priced as though every quarter would exceed expectations indefinitely.

Where the Capital Is Going

The more important story for investors is not what Netflix lost on Friday. It is where the money leaving these positions is landing. Yesterday, eight of eleven S&P 500 sectors finished positive while technology, communications, and consumer discretionary fell. Consumer Staples gained 2.9%. Healthcare rallied. REITs outperformed. The Russell 2000 was green while the Nasdaq dropped more than 1%.

That pattern has now repeated for three consecutive sessions. Capital is not leaving the equity market. It is leaving the most crowded, most expensive positions in the market and rotating into sectors and market cap segments where valuations have not been stretched to the point where a 1% guidance miss destroys $100 billion in value.

For companies in the sub-$2 billion market cap space, this dynamic is the investment case in real time. Smaller companies with reasonable multiples, growing earnings, and domestic revenue exposure do not carry the same expectation burden that is currently crushing the largest names in technology and media. When a Netflix or TSMC sells off on strong results because the price already assumed perfection, the relative attractiveness of companies that never priced in perfection to begin with becomes considerably harder to ignore.

The market is not punishing bad businesses. It is punishing expensive ones. That distinction is everything right now.