While Wall Street’s attention has been fixed on Nvidia earnings, Fed chair transitions, and Iran ceasefire negotiations, something quieter has been happening at the smaller end of the market. The Russell Microcap Index is up 17.55% year to date. The S&P 500 is up 8.72%. Microcap stocks have more than doubled the return of the 500 largest companies in America through the first five months of 2026, and the story behind that performance is one that most mainstream financial coverage has almost entirely missed.

The Numbers in Full

The 2026 outperformance is not a short-term blip. It is the continuation of a trend that began building in the spring of 2025. Over the past twelve months, the Russell Microcap Index has gained more than 57%, compared to approximately 27% for the S&P 500 over the same period. Microcaps have now outperformed major large cap indices for four consecutive quarters, a streak that Franklin Templeton research confirmed through the end of Q1 2026.

The first quarter told a particularly clear story. Energy was the standout sector within the Russell 2000, delivering a gain of 38.2% — far outpacing every other sector as oil prices surged on the Iran conflict. Small cap value outperformed small cap growth. Higher quality, lower leverage companies outperformed. Dividend-paying names outperformed non-payers. This was not speculative froth driving microcaps higher. It was fundamentals.

Why the Headlines Keep Missing It

The reason this story stays under the radar is structural. The S&P 500 is increasingly a story of extreme concentration. The top ten companies in that index now account for approximately 40% of its total weighting. Last week specifically, just five companies — Nvidia, Micron, Apple, AMD, and Intel — accounted for 75% of the entire index’s weekly gain. When those five companies perform well, the S&P 500 performs well, and every headline reflects that. When they stumble, the index stumbles, even if hundreds of smaller companies are quietly compounding.

That concentration dynamic is precisely what makes the microcap outperformance this year so significant. It is happening despite the noise, not because of it.

The Valuation Story Has Not Closed

Despite the strong performance, microcap and small cap stocks remain historically cheap relative to large caps. The Russell 2000’s weight within the Russell 3000 — a broad measure of how much of total market capitalization small caps represent — sits at 4.6%, compared to a historical average of 7.6%. On a forward price-to-earnings basis, small caps trade at a 30% discount to the S&P 500, a gap that remains near its widest level in over two decades. EV/EBIT valuations for the Russell Microcap Index relative to large caps are near their lowest point in 25 years according to Royce Investment Partners.

The rotation is not a prediction anymore. It is already underway. The investors who noticed it early are two quarters ahead of the ones still watching the Magnificent Seven.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First quarter 2026 Financial Results. For the first quarter of 2026,Seanergy reported net revenues of $42.9 million, up 77% from $24.2 million in the prior-year period, driven by significantly stronger charter rates and improved fleet performance. EBITDA increased to $23.6 million from $6.6 million, while adjusted EBITDA rose to $28.1 million from $8.0 million. The company generated net income of $9.7 million, or $0.45 per diluted share, compared to a net loss of $6.8 million, or $0.34 per diluted share, in the first quarter of 2025. Adjusted net income totaled $13.4 million, or $0.63 per diluted share, versus an adjusted net loss of $5.5 million, or $0.27 per share, in the prior-year quarter.

Updating Estimates. We have increased our 2026 revenue, EBITDA, and EPS estimates to $198.3 million, $130.2 million, and $3.45, respectively, from $182.1 million, $106.7 million, and $2.40. The increase in our estimates reflects higher time charter equivalent rates. The company has 83% of its fleet expected operating days during the second quarter fixed at an estimated TCE rate of $29,725. During the first quarter, Seanergy earned an average fleet time charter equivalent rate of approximately $24,219 per day.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First-quarter 2026 Financial Performance.Kuya Silver generated first-quarter revenue of $1,464,997 compared to $225,997 during the first quarter of 2025. The company reported a loss of $1,237,166, or $(0.01) per share, compared to a loss of $1,348,986, or $(0.01) per share, during the prior year period. We have adjusted our 2026 estimates to reflect lower production than previously estimated due to a modestly slower ramp-up in production and expected variability in grade and recoveries. The company expects to produce between 150.0 thousand and 200.0 thousand silver equivalent ounces in 2026, and we think 2027 production could be in the range of 1.0 million and 1.5 million silver equivalent ounces.

Operational Momentum. The company remains focused on ramping up production at the Bethania project, with production expected to accelerate later in the year. Key underground development initiatives, including the construction of a new ramp and ore handling systems to support Phase 1 expansion to 350 tonnes per day, are progressing and are expected to improve operational stability and long-term production capacity. KuyaSilveris also advancing due diligence on the proposed Camila plant acquisition, which would give the company full control over processing schedules and ore blend strategies, eliminate future toll-milling costs, and improve costs and margins as production from the Bethania mine increases.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

There are strong earnings reports, and then there is whatever Dell Technologies just delivered. The computing giant posted fiscal Q1 2027 results Thursday evening that left Wall Street scrambling to revise models that were not even close to capturing what is actually happening in AI infrastructure spending right now. Dell shares surged more than 30% Friday, adding nearly $100 per share to close near $417.

The numbers are almost difficult to process at face value.

Revenue for the quarter came in at $43.8 billion, up 88% year over year and more than $8 billion above the analyst consensus estimate of $35.5 billion. Dell booked $24.4 billion in AI server orders in a single quarter, generated $16.1 billion in AI server revenue, and exited the period sitting on a backlog of $51.3 billion in unfilled AI server orders. For context, $51.3 billion in backlog represents more than the company’s entire revenue for a typical quarter just two years ago.

The guidance revision was equally staggering. Dell now projects $167 billion in fiscal year 2027 revenue, up sharply from a prior outlook of approximately $140 billion and nearly $25 billion above the analyst consensus of $142.1 billion. Embedded within that figure is a projection of $60 billion from AI server sales alone across the full fiscal year.

What the Analysts Are Saying

Wall Street’s response was immediate and unanimous. Evercore ISI raised its price target from $270 to $450 and framed the quarter in terms that rarely appear in analyst notes: “This is what an AI supercycle looks like.” Citi lifted its target from $290 to $475 and noted that demand continues to exceed supply, supporting backlog visibility through year-end. JPMorgan pushed its target from $280 to $500, citing improved visibility into a higher sustainable earnings growth rate over the medium term. Loop Capital went furthest of all, raising to $550 from an undisclosed prior target and calling the quarter “historic” and “unprecedented.”

Critically, multiple analysts flagged that Dell remains supply-constrained. Better component allocations, particularly in AI server hardware, could push estimates even higher from current levels.

The Small Cap Read-Through

For investors focused on the sub-$2 billion market cap universe, Dell’s quarter is not just a large cap story. It is a demand confirmation signal for every company supplying components into the AI server ecosystem.

A $51.3 billion backlog and a company that is supply-constrained does not stay that way without pulling every link of its supply chain to maximum capacity. Memory, power delivery systems, advanced cooling solutions, networking hardware, printed circuit boards, specialty connectors, and server chassis components are all part of the AI server bill of materials. Many of the companies making those components operate well below the $2 billion market cap threshold and have yet to see their valuations fully reflect the demand environment Dell’s results just confirmed.

Dell is the clearest proof yet that the AI infrastructure buildout has moved well beyond chips into the full stack of server hardware. The companies supplying that stack, at every tier and every size, are now operating in one of the strongest demand environments in the history of enterprise technology.

One of the most recognized names in American casino entertainment is leaving the public markets. Caesars Entertainment (Nasdaq: CZR) announced Wednesday it has entered into a definitive agreement to be acquired by Fertitta Entertainment, the private holding company of Houston billionaire Tilman Fertitta, in an all-cash transaction valued at approximately $17.6 billion including the assumption of $11.9 billion in Caesars’ outstanding debt.

Caesars shareholders will receive $31.00 per share in cash, representing a 49% premium to the company’s unaffected share price as of February 25, 2026, the last trading session before deal rumors began circulating. The board of directors unanimously approved the transaction and is recommending shareholders do the same.

Who Is Buying and What They Are Building

Tilman Fertitta is not a name that needs introduction in the hospitality world. His private empire already encompasses the Golden Nugget Hotel and Casino brand with locations across Nevada, New Jersey, Mississippi, Louisiana, and Colorado, the Landry’s restaurant group operating more than 550 outlets including Morton’s The Steakhouse, Del Frisco’s, McCormick and Schmick’s, Mastro’s, and Bubba Gump Shrimp, entertainment venues including the Kemah Boardwalk and multiple aquarium properties, and the NBA’s Houston Rockets. He has built and operated one of the most diversified private hospitality portfolios in the country and has a well-documented track record of acquiring underperforming assets and extracting operational value from them.

Adding Caesars to that portfolio creates a combined entity spanning 60 casino resorts, an online gaming and sports betting platform operating under the Caesars Sportsbook brand, retail sports betting at more than 200 third-party locations through the William Hill brand, and more than 600 total food, beverage, and entertainment outlets. The Caesars Rewards loyalty program, one of the most extensive in the gaming industry, carries through to the combined company.

The deal is not subject to a financing condition and will be funded through a combination of Fertitta equity, assumption of Caesars’ existing debt, and new committed financing arranged by a consortium of 10 banks. The existing Caesars management team, including CEO Tom Reeg, CFO Bret Yunker, and President and COO Anthony Carano, are expected to remain in their roles. The Carano family, which holds approximately 5% of Caesars shares, has agreed to roll a portion of their equity into Fertitta Entertainment rather than taking cash.

A go-shop period runs through July 11, 2026, during which Caesars can solicit and consider competing proposals. There is no assurance a superior bid will or will not emerge before that window closes.

What It Signals for the Broader Gaming and Hospitality Sector

A 49% premium on a company the size of Caesars says something deliberate about where strategic buyers see value in gaming and hospitality right now. Public market valuations across the sector have been compressed by elevated interest rates, lingering consumer spending concerns, and the overhang of heavy debt structures. Private buyers with patient capital and operational expertise are stepping into that gap.

For investors tracking smaller gaming operators, regional casino companies, and independent hospitality names in the sub-$2 billion range, the Fertitta-Caesars deal is a reminder that depressed public valuations do not always reflect underlying asset quality. Consolidation at the top of the industry tends to draw attention to the middle and lower tiers, where the valuation gaps are often even wider.

Upon completion of the transaction, Caesars Entertainment common stock will be delisted from Nasdaq.

Real-world analysis of three years of closed claims data from Symphony Health, focused on the third year of the study (2023-2024), comprised of more than 261,000 U.S. adults with fibromyalgia

Data demonstrate a substantial and persistent health burden associated with prescribed opioid use among adults with fibromyalgia

Tonix commercially launched TONMYA® in November 2025, the first new fibromyalgia drug for adults in the U.S. in over 15 years approved by the U.S. Food and Drug Administration (FDA)

BERKELEY HEIGHTS, N.J., May 28, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully-integrated, commercial-stage biotechnology company, presented data from a real-world claims analysis of opioid use in U.S. adults with fibromyalgia at the 2026 ASCP Annual Meeting, held May 26-29, 2026, in Miami Beach, Florida.

“Opioids remain widely prescribed for fibromyalgia despite long-standing guidelines that discourage their use due to lack of efficacy, a growing concern that they worsen fibromyalgia symptoms and the risk of dependence,1-6” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “The discrepancy between real-world practice and evidence-based recommendations reveals a gap in knowledge and an urgent need to educate health care prescribers about the nature of fibromyalgia and the availability of non-opioid, FDA-approved medicines. Tonix is currently executing on the launch of TONMYA® (cyclobenzaprine HCl sublingual tablets), a first-in-class, first-line, non-opioid analgesic medicine FDA approved for daily bedtime administration and long-term use in adults with fibromyalgia.”

Data presented at ASCP 2026 represent a retrospective cohort study using the Symphony Health closed claims database, encompassing administrative medical and pharmacy claims collected between April 2021 and April 2024, to evaluate opioid and benzodiazepine use among adults diagnosed with fibromyalgia (ICD-10-CM diagnosis code M79.7). The study’s objective was to quantify opioid and benzodiazepine use in patients diagnosed with fibromyalgia and characterize patients by age, insurance coverage, and polypharmacy. The Year 3 cohort (April 2023 to March 2024) included 261,776 adult patients, with a mean age of 52.3 years. The cohort was predominantly female (92.1%).

Among patients with Commercial or Medicare Advantage insurance, 40.2% of patients were prescribed at least one opioid, with most claims for tramadol (13.7%), followed by oxycodone (13.1%). Among Medicaid patients, 38.8% were prescribed at least one opioid, with most claims for oxycodone (15.7%), followed by tramadol (11.1%). The Medication Possession Ratio (MPR) for opioid use was similar for Commercial or Medicare Advantage patients (0.39) and Medicaid patients (0.40). Opioid use showed the highest prevalence in older age groups: 61-65 years (43.1%), 66-70 years (39.2%), 71-75 years (38.5%), and >75 years (34.4%), and was lower, but still common for younger adults 18-25 years (20.9%). Concomitant opioid and benzodiazepine use was similar in patients covered under Medicare Advantage or Commercial insurance (19.1%) and Medicaid patients (20.4%).

A copy of the Company’s poster presentation, “Opioid Use in Patients with Fibromyalgia: A Retrospective Claims Analysis,” is available under the Scientific Presentations tab on the Tonix website at https://www.tonixpharma.com/scientific-presentations/.

About Fibromyalgia

Fibromyalgia is a chronic pain disorder that is understood to result from amplified sensory and pain signaling within the central nervous system. Fibromyalgia afflicts more than 10 million adults in the U.S., predominantly in women. Symptoms of fibromyalgia include chronic widespread pain, nonrestorative sleep, fatigue, and morning stiffness. Other associated symptoms include cognitive dysfunction and mood disturbances, including anxiety and depression. Individuals suffering from fibromyalgia struggle with their daily activities, have impaired quality of life, and frequently are disabled. Physicians and patients report common dissatisfaction with currently marketed products.

About TONMYA® (cyclobenzaprine HCl sublingual tablets)

TONMYA (cyclobenzaprine HCl sublingual tablets) is a sublingual tablet formulation of cyclobenzaprine hydrochloride that was approved on August 15, 2025, by the FDA for the treatment of fibromyalgia in adults. TONMYA is the first new prescription medicine approved for fibromyalgia in more than 15 years. TONMYA provides rapid transmucosal absorption of cyclobenzaprine and reduced production of a long half-life active metabolite, norcyclobenzaprine, due to bypassing first-pass hepatic metabolism. TONMYA is a multifunctional agent with potent binding and antagonist activities at the 5-HT2A serotonergic, α1-adrenergic, H1-histaminergic, and M1-muscarinic receptors. TONMYA was investigated as TNX-102 SL. TNX-102 SL is also being developed to treat acute stress disorder (ASD)/acute stress reaction (ASR), and major depressive disorder (MDD). The United States Patent and Trademark Office (USPTO) issued United States Patent No. 9636408 in May 2017, Patent No. 9956188 in May 2018, Patent No. 10117936 in November 2018, Patent No. 10,357,465 in July 2019, and Patent No. 10736859 in August 2020. The Protectic™ protective eutectic and Angstro-Technology™ formulation claimed in the patent are important elements of Tonix’s proprietary TONMYA composition. These patents are expected to provide TONMYA with U.S. market exclusivity until 2034.

Citations

1Winslow BT, et al. Am Fam Physician. 2023;107(2):137–44. 2Macfarlane GJ, et al. Annals of the Rheumatic Diseases. 2017;76(2):318. 3Martucci KT, et al. Sci Rep. 2019;9(1):9633. 4Turner JA, et al. Pain. 2016;157(10):2208–2216. 5Fitzcharles MA, et al. J Rheumatol. 2013;40(8):1388–1393. 6American College of Rheumatology. Fibromyalgia. 2024. Available from: https://www.rheumatology.org/I-Am-A/Patient-Caregiver/Diseases-Conditions/Fibromyalgia.

Tonix Pharmaceuticals Holding Corp.

Tonix Pharmaceuticals* is a fully integrated, commercial-stage biotechnology company focused on central nervous system (CNS) disorders, infectious diseases, immunology conditions, and rare diseases where there exists high unmet medical need. TONMYA® (cyclobenzaprine HCl sublingual tablets 2.8mg), the Company’s flagship internally conceived and developed medicine, is the first new treatment for fibromyalgia in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® (sumatriptan injection 3 mg) and Tosymra® (sumatriptan nasal spray 10 mg). Tonix is extending the science behind TONMYA in Phase 2 clinical studies to evaluate its potential in major depressive disorder and acute stress disorder/acute stress reaction. Tonix is also advancing a pipeline of infectious disease programs, including monoclonal antibody TNX-4800 (anti-OspA mAb) for Lyme disease prevention in the U.S. and TNX-801 (horsepox, live virus vaccine), a vaccine in development for the prevention of mpox and smallpox. Within immunology, Tonix is developing TNX-1500 (anti-CD40L mAb), a third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. Finally, the Company’s rare disease portfolio includes TNX-2900, which is Phase 2 ready for the treatment of Prader-Willi syndrome. To learn more, visit www.tonixpharma.com.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. TONMYA is a registered trademark of Tonix Pharma Limited. All other marks are property of their respective owners.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the completion of the offering, the satisfaction of customary closing conditions, the intended use of proceeds from the offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to successfully launch and commercialize TONMYA® and any of our approved products; risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on March 12, 2026, and periodic reports filed with the SEC on or after the date thereof. Tonix does not undertake an obligation to update or revise any forward-looking statement. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

INDICATION TONMYA is indicated for the treatment of fibromyalgia in adults.

CONTRAINDICATIONS TONMYA is contraindicated:

In patients with hypersensitivity to cyclobenzaprine or any inactive ingredient in TONMYA. Hypersensitivity reactions may manifest as an anaphylactic reaction, urticaria, facial and/or tongue swelling, or pruritus. Discontinue TONMYA if a hypersensitivity reaction is suspected. With concomitant use of monoamine oxidase (MAO) inhibitors or within 14 days after discontinuation of an MAO inhibitor. Hyperpyretic crisis seizures and deaths have occurred in patients who received cyclobenzaprine (or structurally similar tricyclic antidepressants) concomitantly with MAO inhibitors drugs.

During the acute recovery phase of myocardial infarction, and in patients with arrhythmias, heart block or conduction disturbances, or congestive heart failure. In patients with hyperthyroidism.

WARNINGS AND PRECAUTIONS Embryofetal toxicity: Based on animal data, TONMYA may cause neural tube defects when used two weeks prior to conception and during the first trimester of pregnancy. Advise females of reproductive potential of the potential risk and to use effective contraception during treatment and for two weeks after the final dose. Perform a pregnancy test prior to initiation of treatment with TONMYA to exclude use of TONMYA during the first trimester of pregnancy.

Serotonin syndrome: Concomitant use of TONMYA with selective serotonin reuptake inhibitors (SSRIs), serotonin norepinephrine reuptake inhibitors (SNRIs), tricyclic antidepressants, tramadol, bupropion, meperidine, verapamil, or MAO inhibitors increases the risk of serotonin syndrome, a potentially life-threatening condition. Serotonin syndrome symptoms may include mental status changes, autonomic instability, neuromuscular abnormalities, and/or gastrointestinal symptoms. Treatment with TONMYA and any concomitant serotonergic agent should be discontinued immediately if serotonin syndrome symptoms occur and supportive symptomatic treatment should be initiated. If concomitant treatment with TONMYA and other serotonergic drugs is clinically warranted, careful observation is advised, particularly during treatment initiation or dosage increases.

Tricyclic antidepressant-like adverse reactions: Cyclobenzaprine is structurally related to TCAs. TCAs have been reported to produce arrhythmias, sinus tachycardia, prolongation of the conduction time leading to myocardial infarction and stroke. If clinically significant central nervous system (CNS) symptoms develop, consider discontinuation of TONMYA. Caution should be used when TCAs are given to patients with a history of seizure disorder, because TCAs may lower the seizure threshold. Patients with a history of seizures should be monitored during TCA use to identify recurrence of seizures or an increase in the frequency of seizures.

Atropine-like effects: Use with caution in patients with a history of urinary retention, angle-closure glaucoma, increased intraocular pressure, and in patients taking anticholinergic drugs.

CNS depression and risk of operating a motor vehicle or hazardous machinery: TONMYA monotherapy may cause CNS depression. Concomitant use of TONMYA with alcohol, barbiturates, or other CNS depressants may increase the risk of CNS depression. Advise patients not to operate a motor vehicle or dangerous machinery until they are reasonably certain that TONMYA therapy will not adversely affect their ability to engage in such activities. Oral mucosal adverse reactions: In clinical studies with TONMYA, oral mucosal adverse reactions occurred more frequently in patients treated with TONMYA compared to placebo. Advise patients to moisten the mouth with sips of water before administration of TONMYA to reduce the risk of oral sensory changes (hypoesthesia). Consider discontinuation of TONMYA if severe reactions occur.

ADVERSE REACTIONS The most common adverse reactions (incidence ≥2% and at a higher incidence in TONMYA-treated patients compared to placebo-treated patients) were oral hypoesthesia, oral discomfort, abnormal product taste, somnolence, oral paresthesia, oral pain, fatigue, dry mouth, and aphthous ulcer.

DRUG INTERACTIONS MAO inhibitors: Life-threatening interactions may occur. Other serotonergic drugs: Serotonin syndrome has been reported. CNS depressants: CNS depressant effects of alcohol, barbiturates, and other CNS depressants may be enhanced.

Tramadol: Seizure risk may be enhanced. Guanethidine or other similar acting drugs: The antihypertensive action of these drugs may be blocked.

USE IN SPECIFIC POPULATIONS Pregnancy: Based on animal data, TONMYA may cause fetal harm when administered to a pregnant woman. The limited amount of available observational data on oral cyclobenzaprine use in pregnancy is of insufficient quality to inform a TONMYA-associated risk of major birth defects, miscarriage, or adverse maternal or fetal outcomes. Advise pregnant women about the potential risk to the fetus with maternal exposure to TONMYA and to avoid use of TONMYA two weeks prior to conception and through the first trimester of pregnancy. Report pregnancies to the Tonix Medicines, Inc., adverse-event reporting line at 1-888-869-7633 (1-888-TNXPMED).

Lactation: A small number of published cases report the transfer of cyclobenzaprine into human milk in low amounts, but these data cannot be confirmed. There are no data on the effects of cyclobenzaprine on a breastfed infant, or the effects on milk production. The developmental and health benefits of breastfeeding should be considered along with the mother’s clinical need for TONMYA and any potential adverse effects on the breastfed child from TONMYA or from the underlying maternal condition.

Pediatric use: The safety and effectiveness of TONMYA have not been established. Geriatric patients: Of the total number of TONMYA-treated patients in the clinical trials in adult patients with fibromyalgia, none were 65 years of age and older. Clinical trials of TONMYA did not include sufficient numbers of patients 65 years of age and older to determine whether they respond differently from younger adult patients.

Hepatic impairment: The recommended dosage of TONMYA in patients with mild hepatic impairment (HI) (Child Pugh A) is 2.8 mg once daily at bedtime, lower than the recommended dosage in patients with normal hepatic function. The use of TONMYA is not recommended in patients with moderate HI (Child Pugh B) or severe HI (Child Pugh C). Cyclobenzaprine exposure (AUC) was increased in patients with mild HI and moderate HI compared to subjects with normal hepatic function, which may increase the risk of TONMYA-associated adverse reactions.

Please see additional safety information in the full Prescribing Information. To report suspected adverse reactions, contact Tonix Medicines, Inc. at 1-888-869-7633, or the FDA at 1-800-FDA-1088 or www.fda.gov/medwatch.

The most consequential macro story of 2026 may be moving toward resolution. The United States and Iran are now describing a draft memorandum of understanding to end their three-month conflict as “largely negotiated,” and oil markets are responding decisively. West Texas Intermediate crude fell to $89.97 per barrel Wednesday and Brent dropped to approximately $95, with both benchmarks down more than 10% since President Trump called off an imminent military strike on Iran ten days ago. That is a significant and rapid repricing for a commodity that was trading above $107 as recently as last week.

What the Draft Deal Actually Says

Iran’s state television and multiple US officials briefed on the talks have outlined the framework of the proposed MOU, which was brokered through indirect negotiations with Pakistan playing a central mediating role. Under the draft terms, Iran would restore commercial shipping through the Strait of Hormuz to pre-war levels within 30 days, and would clear the mines it deployed in the waterway. In exchange, the United States would lift its naval blockade of Iranian ports, withdraw military forces from Iran’s vicinity, and issue sanctions waivers allowing Iran to sell oil on global markets during a 60-day negotiating period.

The framework also includes the release of approximately $12 billion in frozen Iranian assets as part of a wider $25 billion package under discussion, and envisions Iran managing ship traffic through the strait in cooperation with Oman. If a final agreement is reached within the 60-day window, the MOU could be elevated to a binding UN Security Council resolution.

Trump described the deal as “largely negotiated” over the weekend after consulting with leaders from Saudi Arabia, the UAE, Qatar, Pakistan, Turkey, Egypt, Jordan, Bahrain, and Israel. Secretary of State Marco Rubio confirmed “good signs” and “progress” earlier this week. The deal has not yet been signed and Trump’s formal approval is still pending, while Iran has stated it will take no steps without “tangible verification” of US commitments.

Why This Matters for the Small Cap Universe

The Strait of Hormuz conflict has functioned as a slow-moving tax on the entire small and microcap economy since February 28. Oil above $100 compressed margins for consumer-facing companies, accelerated inflation, pushed Treasury yields to 19-year highs, and sharply reduced the probability of Fed rate cuts that smaller, variable-rate borrowers were counting on. The gradual unwinding of that pressure, if the deal holds, is not a single-day event. It plays out over weeks and quarters.

The most immediate beneficiaries are consumer-facing small caps in transportation, logistics, food service, and retail that have been absorbing elevated fuel costs with limited ability to pass them through to customers. Diesel prices remain significantly elevated, but a sustained move toward $80 WTI would represent meaningful operating cost relief for companies in these sectors.

The flip side is domestic energy producers. Independent oil and gas operators that benefited from WTI above $100 face a direct revenue headwind as prices normalize. Energy services companies and oilfield operators in the small cap space will need to watch production economics carefully if crude continues its descent.

The deal is not yet done. Multiple rounds of progress have collapsed in this conflict before, and outstanding issues including Iran’s nuclear program and enriched uranium stockpile remain unresolved. Energy executives have cautioned that full normalization of Middle East oil supply may not occur until 2027 given the scale of infrastructure disruption caused by the three-month closure. The IEA has also warned that global oil inventories remain dangerously depleted and markets could enter a supply “red zone” as summer travel demand builds.

A deal at $90 oil is not the same as a deal at $75 oil. But the direction of travel is clear, and for the half of the small cap economy that has been squeezed by elevated energy costs since late February, every dollar WTI moves lower is a dollar back in the margin structure.

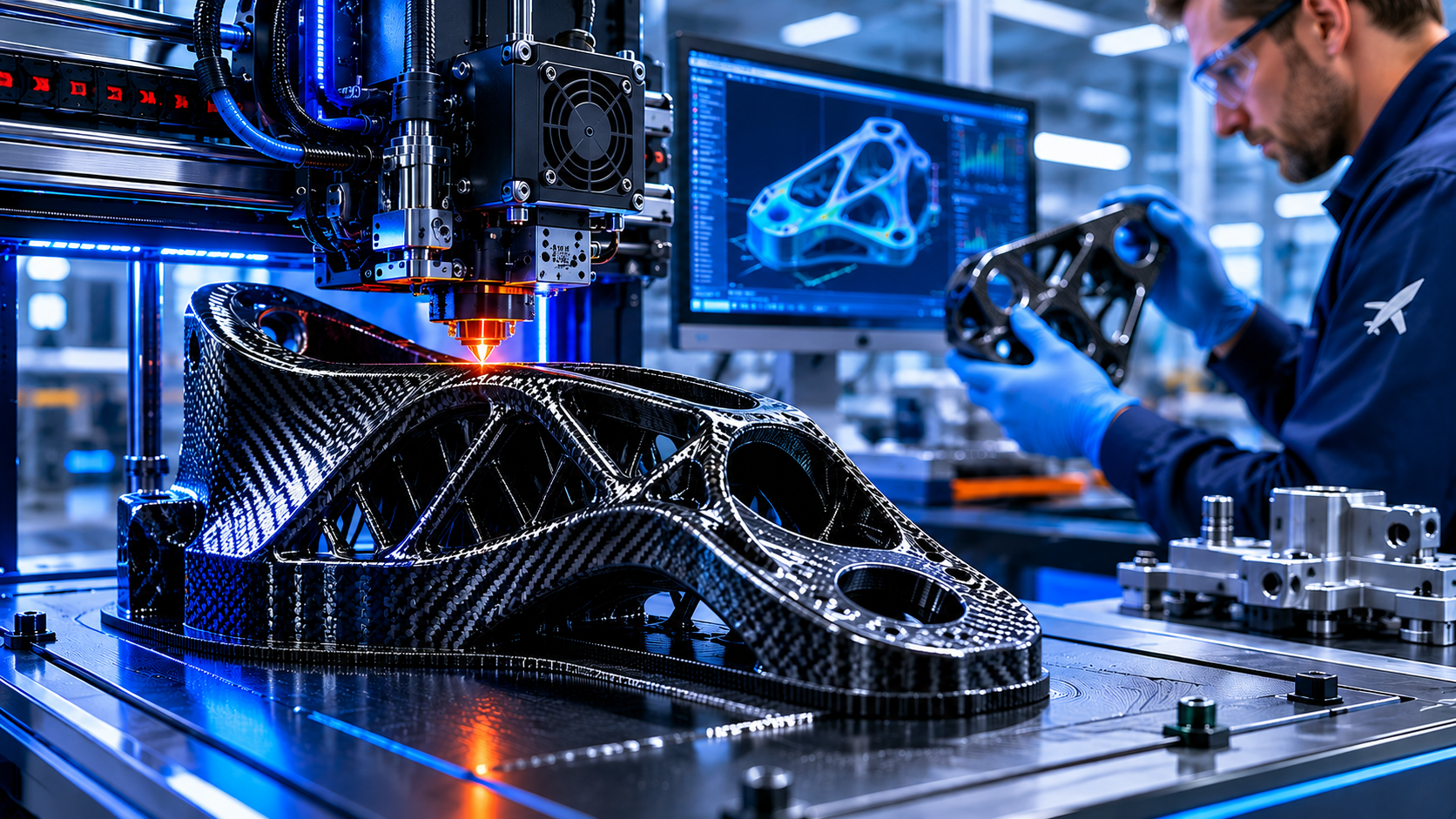

Stratasys Ltd. (Nasdaq: SSYS), a Minnesota and Israel-based leader in additive manufacturing solutions, announced Wednesday it has entered into a definitive agreement to acquire MarkForged, Inc. in an all-cash transaction valued at $42.5 million, subject to customary adjustments. MarkForged is currently a wholly owned subsidiary of Nano Dimension (Nasdaq: NNDM), which will retain MarkForged’s Metal Binder Jetting product line as part of the deal structure. The transaction is expected to close in the second half of 2026, subject to regulatory approvals and customary closing conditions.

At $42.5 million for a business that generated approximately $70 million in revenue in 2025, the transaction reflects an implied revenue multiple of roughly 0.6 times trailing sales. Stratasys expects the deal to be accretive to gross margins and generate positive adjusted EBITDA contribution within the first year following close, though actual results may differ from these forward-looking projections.

What Stratasys Is Acquiring

MarkForged built its core technology around Continuous Carbon Fiber Fused Filament Fabrication, a manufacturing approach that enables production of parts that are lighter and stronger than traditional alternatives. Its integrated platform, the Digital Forge, combines 3D printing hardware, proprietary high-performance materials, and a software ecosystem that includes simulation, part management, and automated print optimization designed with security and compliance requirements in mind.

The acquisition adds a broad portfolio of high-performance polymer and metal filaments to Stratasys’ existing materials capabilities, expanding the combined company’s addressable market across aerospace, defense, automotive, and industrial production verticals. MarkForged’s partner and reseller network is also expected to generate cross-selling opportunities across both companies’ existing customer bases.

The Industry Context

The additive manufacturing sector has been undergoing consolidation as demand for production-grade 3D printing grows in defense and aerospace applications. Government agencies including the Air Force Research Laboratory, DARPA, and the Space Force have expanded procurement of components produced through additive manufacturing for tooling, fixtures, ground support equipment, and select production parts.

Supply chain resilience has emerged as a structural driver of this demand. The ability to produce certified, production-ready components digitally on demand reduces dependence on traditional global supply chains, a priority that has gained urgency across both commercial and defense manufacturing environments since 2020. Stratasys positions this acquisition as a response to that demand shift, strengthening its capabilities in sectors where performance, reliability, and manufacturing agility are operational requirements.

Key Risks to Monitor

As with any acquisition, execution risk exists. The successful integration of MarkForged’s operations, technology, and personnel into Stratasys is not guaranteed. Stratasys is itself a small cap company operating in a competitive and evolving technology sector. The additive manufacturing market continues to face headwinds including longer-than-anticipated enterprise adoption cycles, pricing pressure from emerging competitors, and macroeconomic factors that can compress capital equipment budgets at customer organizations. The projected synergies and EBITDA accretion within the first year are forward-looking estimates and may not materialize as projected.

Stratasys has indicated it will update its financial guidance following the closing of the transaction.

Phase 1 data support TNX-1500 as a potentially first-in-class, best-in-class, third-generation anti-CD40L monoclonal antibody for the prevention of kidney transplant rejection

Phase 2 investigator-initiated study in adult kidney transplant at Massachusetts General Hospital (MGH) expected to initiate in the 2nd half of 2026 pending U.S. Food and Drug Administration (FDA) clearance of MGH’s Investigational New Drug (IND) application

BERKELEY HEIGHTS, N.J., May 27, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully integrated, commercial-stage biotechnology company, today announced the publication of a paper, “First-in-Human, Phase 1, Randomized, Double-Blind, Placebo-Controlled Study of TNX-1500, an Fc-Modified anti-CD154 Monoclonal Antibody, Evaluating the Safety, Tolerability, Pharmacokinetics, and Pharmacodynamics of Single-Ascending Doses in Healthy Adults,” in the peer-reviewed Journal of Clinical Immunology. TNX-1500 is an investigational, third-generation Fc-modified IgG4 anti-CD40L (also known as CD154) monoclonal antibody (mAb) in development for the prevention of organ transplant rejection and the treatment of autoimmune diseases. The manuscript can be accessed at https://pubmed.ncbi.nlm.nih.gov/42053701/.

“The CD40L is a validated target for preventing organ rejection in transplant and treating autoimmune disease, yet no anti-CD40L mAb has been approved for any indication,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “TNX-1500 is a Phase 2 ready humanized mAb engineered to improve safety and tolerability relative to first-generation anti-CD40L mAbs, while preserving the durable half-life and certain effector functions associated with the Fc or crystallizable fragment. We believe the Phase 1 results show that these design objectives were achieved in TNX-1500.”

Dr. Gregory Sullivan, M.D., Chief Medical Officer of Tonix Pharmaceuticals added, “The Phase 1 study evaluated TNX-1500’s safety, tolerability, pharmacokinetics, and pharmacodynamics. TNX-1500 was generally well tolerated, demonstrated a favorable safety profile, suppressed the primary and secondary T cell-dependent antibody responses (TDARs) to keyhole limpet hemocyanin (KLH) antigen, and showed a half-life which supports monthly intravenous dosing. We expect a Phase 2, investigator-initiated study of TNX-1500 in the prevention of kidney allograft rejection at MGH to begin in the 2nd half of 2026 pending clearance of the IND by the FDA.”

The publication reports findings from a single-center, first-in-human, Phase 1, randomized, double-blind, placebo-controlled, single-ascending dose escalation study in 26 healthy adult volunteers. Participants were enrolled across three ascending dose cohorts (3, 10, and 30 mg/kg) or placebo and received a single intravenous infusion of TNX-1500 or placebo, followed by intramuscular injections of KLH on days 2 and 29 to assess the TDAR, and monitored over a 120-day follow-up period. TNX-1500 blocked the primary T cell–dependent antibody response to KLH at all doses, blocked the secondary response at the 10 and 30 mg/kg doses, and reduced peak secondary response to KLH by ~70% relative to placebo at the 3 mg/kg dose.

TNX-1500 was generally well tolerated, with no serious adverse events, and no discontinuations due to adverse events. The only treatment-emergent adverse event (TEAE) deemed possibly related to study drug was aphthous ulcer, which occurred in 1 participant in each of the three TNX-1500 groups; all TEAEs were rated as mild and resolved in 2-10 days. No TEAEs were determined to be related to KLH administration. There were no administration or injection site reactions (one of the prespecified TEAEs of special interest). Pharmacokinetic analyses suggested approximately dose-proportional exposure across the 3 to 30 mg/kg range, with mean terminal elimination half-lives of 37.8 and 33.8 days at the 10 and 30 mg/kg dose levels, respectively. TNX-1500 at 10 and 30 mg/kg blocked the primary and secondary anti-KLH TDAR through day 120, and at 3 mg/kg reduced the peak secondary response by approximately 70% relative to placebo. Across all dose cohorts, TNX-1500 was associated with a rapid (less than one-hour post-dose) and sustained reduction in soluble CD40L (sCD154) over the 120-day study period.

About TNX-1500

TNX-1500 (Fc-modified humanized anti-CD40L mAb) is a Phase 2 ready, humanized monoclonal antibody that interacts with the CD40-ligand (CD40L), also known as CD154. TNX-1500 is being developed for the prevention of kidney transplant rejection and the treatment of autoimmune diseases. Anti-CD40L has multiple potential indications in addition to solid organ and bone marrow transplantation including autoimmune diseases. Collaborations are ongoing with MGH on allo-heart and -kidney transplantation in nonhuman primates, as well as prevention of xenograft rejection, preclinical studies, and prevention of allograft rejection in sensitized patients. The Phase 2 investigator-initiated study by MGH is expected to initiate enrollment in the 2nd half of 2026, pending FDA clearance of the IND, to evaluate TNX-1500 in five kidney transplant recipients. The study is designed to assess the safety, tolerability, and activity of TNX-1500 in preventing kidney transplant rejection while decreasing the exposure to conventional immunosuppressive drugs, which are associated with infection, cancer, cardiovascular side effects, and various metabolic derangements with long term use.

Tonix Pharmaceuticals Holding Corp.

Tonix Pharmaceuticals* is a fully integrated, commercial-stage biotechnology company focused on central nervous system (CNS) disorders, infectious diseases, immunology conditions, and rare diseases where there exists high unmet medical need. TONMYA® (cyclobenzaprine HCl sublingual tablets 2.8mg), the Company’s flagship internally conceived and developed medicine, is the first new treatment for fibromyalgia in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® (sumatriptan injection 3 mg) and Tosymra® (sumatriptan nasal spray 10 mg). Tonix is extending the science behind TONMYA in Phase 2 clinical studies to evaluate its potential in major depressive disorder and acute stress disorder/acute stress reaction. Tonix is also advancing a pipeline of infectious disease programs, including monoclonal antibody TNX-4800 (anti-OspA mAb) for Lyme disease prevention in the U.S. and TNX-801 (horsepox, live virus vaccine), a vaccine in development for the prevention of mpox and smallpox. Within immunology, Tonix is developing TNX-1500 (anti-CD40L mAb), a third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. Finally, the Company’s rare disease portfolio includes TNX-2900, which is Phase 2 ready for the treatment of Prader-Willi syndrome. To learn more, visit www.tonixpharma.com.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. TONMYA is a registered trademark of Tonix Pharma Limited. All other marks are property of their respective owners.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the completion of the offering, the satisfaction of customary closing conditions, the intended use of proceeds from the offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to successfully launch and commercialize TONMYA® and any of our approved products; risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on March 12, 2026, and periodic reports filed with the SEC on or after the date thereof. Tonix does not undertake an obligation to update or revise any forward-looking statement. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

The preliminary list of stocks to be included in the Russell Reconstitution, and also which Russell Index, is a significant day for many stock investors and the impacted companies as well. This year, it occurred on Friday, May 22. The list, although preliminary and subject to refinements each Friday through June, includes the stocks believed to meet the requirements based on valuations taken on April 30. This is the first official filing from the popular index provider, and it gives the investor public an early look at what to expect when the indexes are reconstituted. The reconstitution can be expected to impact prices as index fund managers readjust their holdings. The event also, for many, redefines the market-cap levels that are considered small-cap, mid-cap, and large-cap. This year carries an added dimension: for the first time since 1989, FTSE Russell has moved to a semi-annual reconstitution schedule. That means the June event will be followed by a second reconstitution in December.

Background

The Russell Reconstitution reconfigures the membership of the Russell indexes by defining the top 3,000 stocks based on market cap (Russell 3000), then the top 1,000 stocks (Russell 1000), and reclassifying the remaining 2,000 stocks to form the Russell 2000 Small Cap Index. These serve as a benchmark for many institutional investors, as the indexes reflect the performance of the U.S. equity market across different market-cap classifications. An estimated $11 trillion in assets are benchmarked to the Russell Indexes, which makes the annual reconstitution process one of the most consequential events in the equity markets each year. By adding, removing, and reweighting stocks, the reconstitution process ensures the indexes accurately represent the market.

The Preliminary List, published after the market closed on May 22, 2026, is a critical step in the market cap reclassification process. It gives market participants an initial look at potential additions and deletions from the indexes. Stocks on this preliminary roster often experience increased attention from investors, since the list signals where buying or selling pressure could build once the final reconstitution is completed.

The June 2026 reconstitution reflects a U.S. equity market with continued strength among mega-cap leaders and improving breadth in small-cap segments. Technology and Industrials led movement into the Russell 1000, while companies across several industries replenished the Russell 2000, reinforcing its role as a pipeline for emerging companies.

The newly reconstituted indexes become live after the market close on June 26, 2026.

Implications for Investors

The release of the Russell Preliminary List on May 22 could provide opportunities for investors, including:

Enhanced Market Visibility. Companies listed on the Preliminary List may experience increased trading volumes and heightened market attention, or even scrutiny, as investors evaluate their potential inclusion in the Russell indexes.

Potential Price Movements. Stocks slated for addition or deletion from the indexes can experience price volatility as market participants adjust their positions ahead of the anticipated reconstitution changes.

Portfolio Adjustments. Active managers who track the Russell indexes may need to realign their portfolios to reflect the new index constituents, which can trigger buying or selling activity in affected stocks.

Semi-Annual Impact. The move to a twice-yearly reconstitution schedule in 2026 means these dynamics will now play out two times per year. Investors and IR teams should start preparing for a December reconstitution cycle as well, with a second rank day expected in the fall.

Investor Considerations

Stock market participants should keep the following in mind when analyzing the Preliminary List and its potential impact:

Upcoming Update Dates. Following the May 22 preliminary release, updated lists will be posted after 6 PM ET on May 29, June 5, June 12, and June 18. The reconstitution becomes final after the close of U.S. equity markets on June 26, 2026. Watching these updates is the best way to track actual index membership changes as they develop.

Final Reconstitution. The Preliminary List is subject to changes before the final reconstitution. Updates may occur due to faulty data or significant corporate changes, such as a merger, that took place after the April 30 market cap snapshot.

Fundamental Analysis. The fundamentals and financial health of the companies should always be among the most important factors for non-index investors to consider. Historically, potential additions have often presented attractive investment opportunities, while potential deletions may result in a stock receiving less attention from the broader market.

Take Away

The Preliminary List released on May 22, 2026, is an important early step in the Russell Reconstitution process. This year it also marks a structural change in how the reconstitution works, with the shift to semi-annual rebalancing adding a new layer of relevance for investors and companies alike. The stocks listed may experience increased market visibility and price movement in the weeks ahead, but the list remains subject to changes through June 18. The final reconstitution takes effect after market close on June 26. As always, thorough fundamental analysis, including earnings, growth potential, and liquidity, should guide investment decisions. For more information to evaluate small-cap names, look to Channelchek as a source of data on over 6,000 small-cap companies

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Resources To Focus On Current Market Needs. GeoVax has reviewed its pipeline products in infectious disease and oncology programs. Preparations will continue for the Phase 3 immunobridging trial in Mpox, expected to begin later this year. A Phase 2 for Gedeptin is planned for FY2027. Development of CM-04S1 has been terminated, as the diminished need for a vaccine to protect immunocompromised patients from COVID-19 no longer justifies its continuation.

GEO-MVA and Infectious Diseases Remain A Priority. As discussed in our Research Note on May 19, 2026, GeoVax is preparing for a Phase 3 immunobridging trial in Mpox that could meet EMA requirements for accelerated approval. The trial is expected to begin in 2H26 with a planned enrollment of about 500 participants. The preclinical pipeline includes products for other infectious viruses that could be developed if grant or other funding were available.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Proprietary Technology Has Produced A Large Library Of Novel Antivirals. Cocrystal has developed a library of antivirals based on its proprietary technology. While clinical development has prioritized products with clear medical needs and regulatory pathways to approval, it continues to research new compounds that can be moved into development as public health needs change. After the recent outbreaks of hantavirus, Ebola, and several previously lesser-known viruses, the company tested some of these compounds and found them to be effective.

Cocrystal’s Proprietary Technology Acts Early In The Viral Lifecycle. Cocrystal drugs target enzymes essential to the viral life cycle and reproductive process. These enzymes are highly conserved across viral families and rarely mutate, allowing compounds to show broad efficacy against multiple strains. This differs from vaccines that train the immune system to recognize and kill a virus. Vaccines often target surface proteins that can mutate, rendering the vaccine ineffective.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Unique within the junior mining space. Nicola Mining (NASDAQ: NICM, TSX.V: NIM) combines near-term cash flow generation with significant exploration upside across a portfolio of gold, silver, and copper assets in British Columbia. A key strategic asset is the fully permitted Merritt Mill, the only facility in British Columbia allowed to process third-party gold and silver ore, with expansion plans underway to increase throughput capacity. Nicola seeks to leverage its mill by providing milling services under profit-sharing agreements to third parties and consolidating small high-grade gold and silver projects in British Columbia, while advancing its New Craigmont Copper, Treasure Mountain Silver, and Dominion Creek Gold projects.

Advancing multiple avenues of growth. Nicola’s flagship New Craigmont Copper Project is a significant value driver, with ongoing drilling targeting a potential large-scale porphyry copper system adjacent to the Highland Valley Copper Mine. Nicola is also advancing the high-grade Treasure Mountain Silver Project and the Dominion Creek Gold Project, both of which are expected to see increased exploration and development activity later this year.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.