Magnolia Oil and Gas (NYSE: MGY) announced Monday it has entered into a definitive purchase agreement to acquire WildFire Energy for approximately $4.06 billion, marking the largest acquisition in the company’s history and one of the most significant domestic upstream deals of 2026. WildFire, backed by private equity firms Warburg Pincus and Kayne Anderson, operates in the same South Texas basin where Magnolia has built its entire business, making this a pure concentration play rather than a diversification move.

Under the terms of the agreement, WildFire owners will receive 32.2 million shares of Magnolia’s Class A common stock, and Magnolia will assume $600 million in outstanding notes due in 2029. The transaction is expected to close in late Q3 2026. Committed financing has been arranged through JPMorgan Chase and Citigroup.

What Magnolia Is Actually Getting

The deal goes well beyond additional drilling locations. WildFire’s assets are concentrated in the Eagle Ford Shale and Austin Chalk formations in the Giddings area of South Texas, directly adjacent to and overlapping with Magnolia’s existing operations. That geographic overlap is central to the deal thesis because it allows Magnolia to integrate the acquired production into its existing infrastructure with minimal incremental investment.

Two components of the transaction stand out from a typical upstream acquisition. First, the deal includes a sand mine that supplies approximately 80% of Magnolia’s current annual sand consumption, including 100% of WildFire’s sand requirements, with additional third-party sales on top. Controlling your own frac sand supply in a market where sand costs represent a meaningful share of well completion expenses is a structural cost advantage that compounds over every well drilled.

Second, the transaction includes more than 500 miles of gas gathering pipelines in the Giddings area. Owning midstream infrastructure rather than paying third-party gathering and processing fees directly improves operating margins on every barrel produced. For investors who follow midstream economics, companies like Summit Midstream Partners understand exactly how valuable that kind of infrastructure control can be at scale.

The Shareholder Return Story

Magnolia is framing this as a free cash flow accretion story above all else. The confidence in the acquired asset quality translated into an immediate 9% increase in the quarterly dividend to $0.18 per share, payable in Q3 2026. The company also reaffirmed its ongoing commitment to repurchasing at least 1% of outstanding shares per quarter.

On the production side, Magnolia reported Q2 total production averaging 106,100 barrels of oil equivalent per day, with D&C capital of $125 million and $296 million of cash on the balance sheet at quarter end. The company raised its full-year 2026 standalone production growth guidance from 5% to 6% alongside the deal announcement.

The Broader E&P Consolidation Signal

For investors tracking domestic energy producers in the small and microcap space, the Magnolia-WildFire combination reinforces a consolidation pattern that has been accelerating throughout 2026. Private equity-backed E&P companies that built significant acreage positions during the downturn are now exiting to public company buyers at scale. The acquirers with the strongest balance sheets, the lowest cost structures, and the most disciplined capital allocation frameworks are the ones winning the assets.

That dynamic creates a dual opportunity for smaller energy names. Companies like InPlay Oil and Gas and Alliance Resource Partners that operate with similar discipline in their respective basins represent the kind of focused, well-run operators that either benefit from the same elevated pricing environment driving Magnolia’s economics or become attractive consolidation targets themselves as the deal cycle continues.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating coverage with an Outperform rating. We are initiating coverage on VivoPower International PLC (NASDAQ: VIVO) with an Outperform rating and $10 Price target. The company has recently pivoted toward acquiring and developing power-secured land and powered-shell data center infrastructure, targeting one of the most constrained inputs in the AI value chain: grid-connected power capacity.

Capital-Light Business Model. The company occupies an upstream position within the AI data center value chain. Rather than owning and operating IT infrastructure, it seeks to generate returns through land development, power procurement, and long-term leasing arrangements. In our view, this model provides exposure to AI infrastructure demand while reducing technology and operating risks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

LIFE Offering. Power Metallic Mines closed its previously announced brokered Listed Issuer Financing Exemption (LIFE) offering that raised C$28.2 million in gross proceeds. The company issued 22.583 million common shares of the company at a price of C$1.25 per share. The agents received an aggregate cash fee of C$1.4 million. We had already assumed the issuance of equity in our financial model. Prominent mining investor Mr. Eric Sprott invested C$2.0 million through his company, 2176423 Ontario Ltd., with the acquisition of 1.6 million shares.

Use of Proceeds. The proceeds will be used to advance the company’s flagship Nisk Project in Quebec and its Jabul Baudan exploration license in Saudi Arabia, and to fund general working capital and corporate needs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

George Proost, Research Intern, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Double E Expansion Gains Commercial Traction. Summit Midstream announced additional long-term transportation commitments on its Double E Pipeline, bringing open season commitments to 250 MMcf/d and total contracted capacity to approximately 1.9 Bcf/d. Demand has exceeded available expansion capacity, prompting the company to extend its open season through June 30, 2026, while continuing negotiations with prospective shippers. Management remains on track to reach a final investment decision by the end of summer and has secured key compressor equipment to support a targeted late-2028 in-service date.

Strong Demand Supports Capacity Expansion. The Double E Compression Expansion would increase pipeline capacity by approximately 50%, from 1.6 Bcf/d to 2.4 Bcf/d, further strengthening its role as a key natural gas takeaway system in the Delaware Basin. In addition to the 250 MMcf/d of binding commitments secured, Summit holds a firm option agreement for another 200 MMcf/d and continues discussions with shippers whose interest exceeds available capacity. The strong commercial response reduces project risk and underscores continued demand for Permian Basin natural gas infrastructure.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Stock Repurchase Authorization. Summit Midstream Corporation announced that its Board of Directors has authorized the company’s first stock repurchase program, allowing for the repurchase of up to $35 million of outstanding common stock. As of May 8, shares outstanding were 20.3 million, including 13.8 million common shares and 6.5 million Class B common shares.

Terms of the Program. Summit may repurchase shares through open market transactions, privately negotiated purchases, block trades, or other methods permitted under applicable securities laws. Repurchase activity will depend on market conditions, share price, debt covenant compliance, and other factors. The program has no expiration date, does not require the company to buy back any specific number of shares, and may be suspended or terminated at any time.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

TSX approves share repurchase program. InPlay Oil Corp. announced that the Toronto Stock Exchange has approved its normal course issuer bid (NCIB), allowing the company to repurchase and cancel up to 1.79 million common shares, representing 10% of its public float. Purchases may be made through the TSX and other Canadian trading systems beginning May 25, 2026, and ending May 24, 2027, subject to daily purchase limits and applicable securities regulations.

Automatic repurchase plan provides flexibility. An automatic share purchase plan allows for repurchases to continue during self-imposed blackout periods. Outside of blackout periods, management will retain discretion over the timing and amount of share repurchases. Any shares acquired under the program will be canceled, reducing the company’s overall share count.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

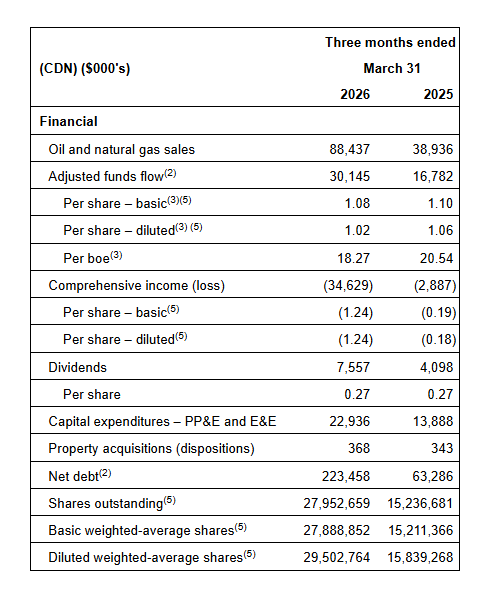

CALGARY, AB, May 8, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (TASE: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to announce its financial and operating results for the three months ended March 31, 2026. InPlay’s unaudited interim financial statements and notes, and Management’s Discussion and Analysis (“MD&A”) for the three months ended March 31, 2026 will be available at “www.sedarplus.ca” and the Company’s website at “www.inplayoil.com“. An updated corporate presentation will be available on our website in due course.

First Quarter 2026 Highlights:

Closed an oversubscribed offering of senior unsecured bonds for total gross proceeds of C$244 million maturing on December 15, 2030 at an attractive interest rate of 6.23%. InPlay has fully hedged all cashflows relating to the New Israeli Shekel denominated bonds over the next four years.

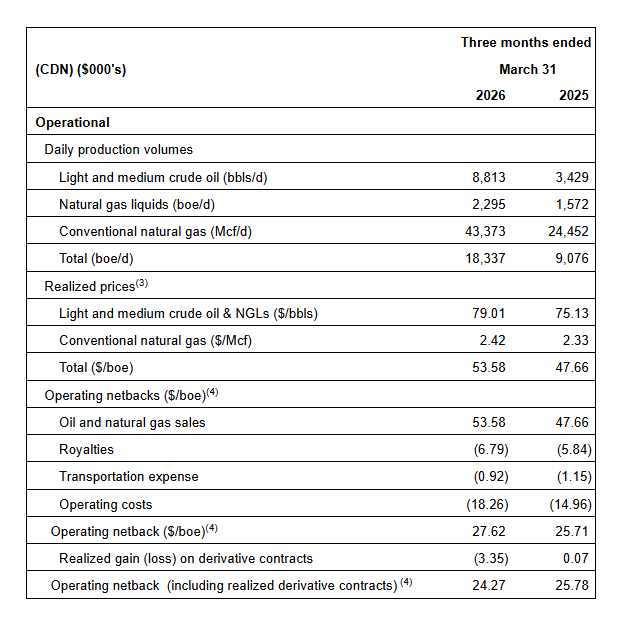

Achieved average quarterly production of 18,337 boe/d(1) (61% light crude oil and NGLs), a 102% increase from Q1 2025.

Improved light oil production to 8,813 bbl/d, a 157% increase from Q1 2025. Light crude oil weighting improved by 10% from Q1 2025 driving stronger per boe netbacks and returns.

Realized strong operating income of $45.6 million, a 117% increase from Q1 2025 and a 20% increase from Q4 2025. This resulted in an operating income profit margin(4) of 52%, an 11% improvement from Q4 2025.

Enhanced field operating netbacks(3) to $27.62/boe, an increase of 31% compared to Q4 2025.

Generated AFF(2) of $30.1 million ($1.08 per weighted average basic share(3)), an 80% increase from Q1 2025.

Returned $7.6 million to shareholders via monthly dividends (6.4% yield relative to current share price). Since November 2022, InPlay has distributed $75 million in dividends, including dividends declared to date in the second quarter.

Message to Shareholders:

The ongoing conflict in the Middle East and associated uncertainty has driven extreme and unprecedented volatility in oil and gas commodity prices. Concerns surrounding the largest oil supply shock in recent history has led to significantly higher crude oil prices. The Company believes this supply shortfall, combined with years of underinvestment and relatively modest global reserve additions compared to global consumption of approximately 38 billion barrels per year, supports a higher WTI pricing environment going forward relative to the ~US$60 WTI prices experienced in recent years.

InPlay has maintained a smart and disciplined business approach through the previous US$60 WTI pricing environment, achieving one of the highest free cash flow yields amongst our peers, which is expected to increase materially in a US $70+ WTI price environment. This increase is anticipated to drive meaningful net debt reduction, further strengthening the Company’s ability to execute our strategy of disciplined organic growth coupled with our strong track-record of accretive acquisitions, while reinforcing our focus on Free Adjusted Funds Flow and delivering strong returns to shareholders.

Our strategically aligned relationship with Delek Group Ltd. (“Delek”), who have a solid track record of value creation in the oil and gas industry, puts us in an advantageous position to execute our strategy. This relationship has already created meaningful value through Delek’s support in facilitating the successful issuance of unsecured bonds on the Tel Aviv Stock Exchange (“TASE”). The bonds were issued at favorable rates and terms, and we are confident we will have continued access to this advantageous cost of capital resource going forward.

During the first quarter, InPlay continued to build on the strong momentum generated from our transformational 2025 acquisition and results. The Company executed an active drilling program in the first quarter with five (5.0 net) Pembina Extended Reach Horizontal (“ERH”) wells drilled. The first two wells were brought on production in mid-February and have delivered strong results ahead of internal expectations. Initial production (“IP”) rates for these two wells were 333 boe/d (88% light oil and NGLs) per well over the first 60 days of production (45% above type curve) and they are currently producing at a rate of 278 boe/d (83% light oil and NGLs) per well. The last three wells were brought on production in April and are currently in the clean-up phase. These wells have delivered initial production (“IP”) rates of 351 boe/d (91% light oil and NGLs) per well over the first 27 days of production and are currently producing at a rate of 462 boe/d (90% light oil and NGLs) per well. To date, results indicate performance is significantly ahead of internal estimates.

The Company was able to access the field early in the second quarter during spring break-up, allowing us to accelerate our capital program. Drilling operations recently finished three (3.0 net) ERH Pembina wells that are expected to be on-production in early June, approximately 40 days earlier than originally planned. Unlimited use of access roads that are owned and maintained by the Company and unrestricted entry to surface locations with minimal road bans in effect allowed us to advance drilling operations in response to the significantly improved crude oil commodity price environment. Given the Company’s financial flexibility and ability to quickly adjust operations, further modifications to upcoming capital programs can be made in response to changing market conditions.

Driven by strong production exiting the first quarter, InPlay reiterates its 2026 average annual production guidance of 18,600 boe/d – 19,200 boe/d(1) (60% – 62% light oil and NGLs). The Company is now forecasting WTI prices to average US$81.50 for the remainder of the year (compared to our previous estimate of US$63.00). This results in an increase in AFF(2) from $125 million (mid-point) to $147 million (mid-point), with estimated FAFF(3) increasing from $55 million (mid-point) to $77 million (mid-point), equating to a FAFF yield(3) of 15% (mid-point). The Company’s leverage metrics are projected to remain strong with net debt to EBITDA(3) forecasted to be 1.1x for 2026 (mid-point).

The Company continues to monitor the evolving pricing environment and remains focused on disciplined but flexible capital allocation and maintaining financial strength to support long-term sustainability and returns to shareholders.

First Quarter 2026 Financial & Operations Overview:

InPlay completed an active capital program during the first quarter investing $22.9 million in drilling five (5.0 net) Pembina ERH wells and related infrastructure. Operational execution remained strong during the quarter, with drilling and completion operations on budget and consistent with recent capital programs. Some service equipment delays and unseasonably warm weather in March impacted completion operations on the three-well pad, resulting in a three-week delay in bringing these wells on production. The Company benefitted from new flush production coming on-line into a favorable oil pricing environment, with WTI prices averaging US $91.00 and US $98.06 in March and April respectively, compared to approximately US $62.50 during the first two months of 2026.

Quarterly production averaged 18,337 boe/d(1) (61% light crude oil and NGLs), representing a 102% increase from the first quarter of 2025. Quarterly crude oil production averaged 8,813 bbl/d, a 157% increase from the first quarter of 2025. The Company forecasts an estimate of 3% – 5% of downtime per month, the first quarter was impacted by some extraordinary one-time events, resulting in incremental downtime of approximately 475 boe/d (47% light oil and NGLs). This included a severe windstorm in March which damaged power infrastructure affecting the Company’s core Pembina properties, resulting in downtime of approximately 300 boe/d (55% light oil and NGLs) for the quarter. The low-decline nature of the Company’s base production, combined with strong performance of recently drilled wells, continues to benefit the Company.

Quarterly operating costs decreased on an absolute basis compared to the fourth quarter of 2025, but were slightly higher on a per boe basis reflecting the impact of fixed operating costs on per boe metrics due to production downtime from the one-time events described above. In addition, the Company performed service operations on five low-rate wells that have been offline for up to three years. At current crude oil prices, these wells are estimated to payout in 6 – 9 months and are anticipated to produce without issues for an additional 5 – 10 years with minimal decline. InPlay will look to complete similar well servicing operations in the upcoming months given the current pricing environment.

InPlay generated AFF of $30.1 million ($1.08 per basic share), representing an 80% increase from the first quarter of 2025. These results were achieved despite $5.5 million in realized hedging losses, primarily due to the significant increase in WTI in March relative to the hedges required by our first lien bank lenders to facilitate the acquisition in 2025. The Company has significantly less crude oil volumes hedged in the second half of 2026 and all of 2027 and intends to remain opportunistic with future hedging activity while monitoring the current backwardation in the WTI forward price curve. Details of the Company’s current hedges are provided in the “Hedging Summary” section of the Reader Advisories.

During the quarter, InPlay paid dividends of $7.6 million to shareholders, representing a 6.1% yield relative to our current share price. Since November 2022, InPlay has distributed $75 million in dividends, including dividends declared to date in the second quarter.

The Company realized a net loss of $34.6 million ($1.24 per basic share; $1.24 per diluted share), which includes a $39 million impact from the unrealized future mark-to-market value of the Company’s hedges required by our first lien bank lenders to facilitate our acquisition in 2025.

Financial and Operating Results:

On behalf of our employees, management team and Board of Directors, we thank our shareholders for their continued support and look forward to providing updates on our progress throughout the year.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Kevin Leonard Vice President Corporate & Business Development InPlay Oil Corp. Telephone: (587) 955-0635

Notes:

1.

See “Production Breakdown by Product Type” at the end of this press release.

2.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

3.

Supplementary financial measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

4.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release and in our most recently filed MD&A.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President Corporate & Business Development, InPlay Oil Corp., Telephone: (587) 955-0635

CALGARY, AB, April 30, 2026 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on May 29, 2026, to shareholders of record at the close of business on May 15, 2026. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp. InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632, www.inplayoil.com; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

HOUSTON, April 29, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit”, “SMC” or the “Company”) announced today that it will report operating and financial results for the first quarter of 2026 on Monday, May 11, 2026, after the close of trading on the New York Stock Exchange.

First Quarter 2026 Earnings Call

SMC will host a conference call at 10:00 a.m. Eastern on May 12, 2026, to discuss its quarterly operating and financial results. The call can be accessed via teleconference at: Q1 2026 Summit Midstream Corporation Earnings Conference Call (https://register-conf.media-server.com/register/BI874f39fdf8c54b499c4ac477755fbcad). Once registration is completed, participants will receive a dial-in number along with a personalized PIN to access the call. While not required, it is recommended that participants join 10 minutes prior to the event start. The conference call, live webcast and archive of the call can be accessed through the Investors section of SMC’s website at www.summitmidstream.com

Upcoming Investor Conferences

Members of SMC’s senior management team will attend the 2026 Energy Infrastructure CEO & Investor Conference which will take place on May 18–20, 2026, the 2026 RBC Capital Markets Global Energy, Power & Infrastructure Conference taking place on June 2–3, 2026, and the BofA Energy and Power Credit Conference on June 3–4, 2026. The presentation materials associated with this event will be accessible through the Investors section of SMC’s website at www.summitmidstream.com prior to the beginning of the conference.

About Summit Midstream Corporation

SMC is a value-driven corporation focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in the core producing areas of unconventional resource basins, primarily shale formations, in the continental United States. SMC provides natural gas, crude oil and produced water gathering, processing and transportation services pursuant to primarily long-term, fee-based agreements with customers and counterparties in five unconventional resource basins: (i) the Williston Basin, which includes the Bakken and Three Forks shale formations in North Dakota; (ii) the Denver-Julesburg Basin, which includes the Niobrara and Codell shale formations in Colorado and Wyoming; (iii) the Fort Worth Basin, which includes the Barnett Shale formation in Texas; (iv) the Arkoma Basin, which includes the Woodford and Caney shale formations in Oklahoma; and (v) the Piceance Basin, which includes the Mesaverde formation as well as the Mancos and Niobrara shale formations in Colorado. SMC has an equity method investment in Double E Pipeline, LLC, which provides interstate natural gas transportation service from multiple receipt points in the Delaware Basin to various delivery points in and around the Waha Hub in Texas. SMC is headquartered in Houston, Texas.

Forward-Looking Statements

This press release includes certain statements concerning expectations for the future that are forward-looking within the meaning of the federal securities laws. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements and may contain the words “expect,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result,” and similar expressions, or future conditional verbs such as “may,” “will,” “should,” “would” and “could.” In addition, any statement concerning future financial performance (including future revenues, earnings or growth rates), payment of dividends on any series of stock, ongoing business strategies and possible actions taken by SMC or its subsidiaries are also forward-looking statements. Forward-looking statements also contain known and unknown risks and uncertainties (many of which are difficult to predict and beyond management’s control) that may cause SMC’s actual results in future periods to differ materially from anticipated or projected results. An extensive list of specific material risks and uncertainties affecting SMC is contained in its 2025 Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 16, 2026, as amended and updated from time to time. Any forward-looking statements in this press release are made as of the date of this press release and SMC undertakes no obligation to update or revise any forward-looking statements to reflect new information or events.

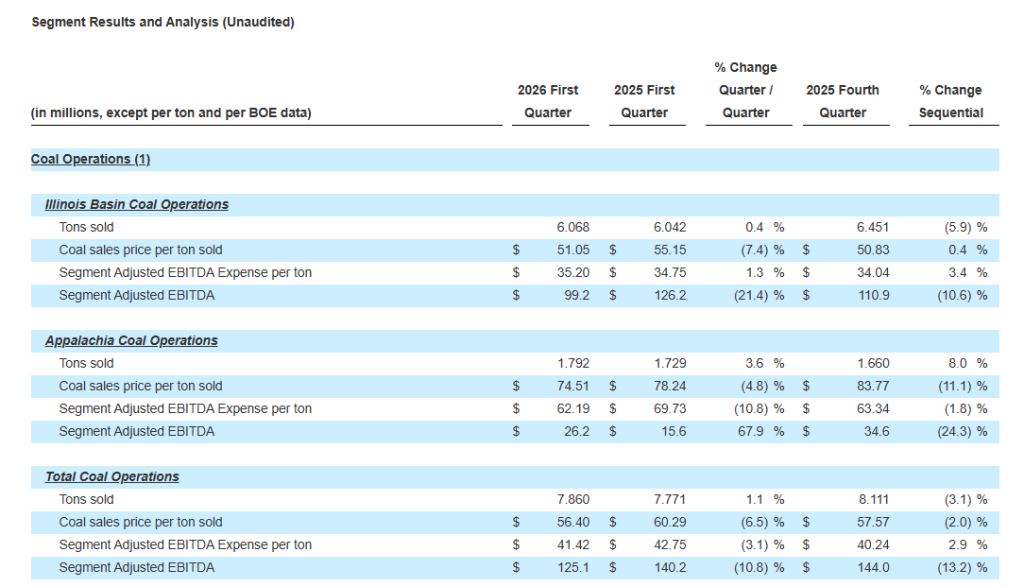

Total revenue of $516.0 million, net income of $9.1 million, and Adjusted EBITDA of $155.0 million

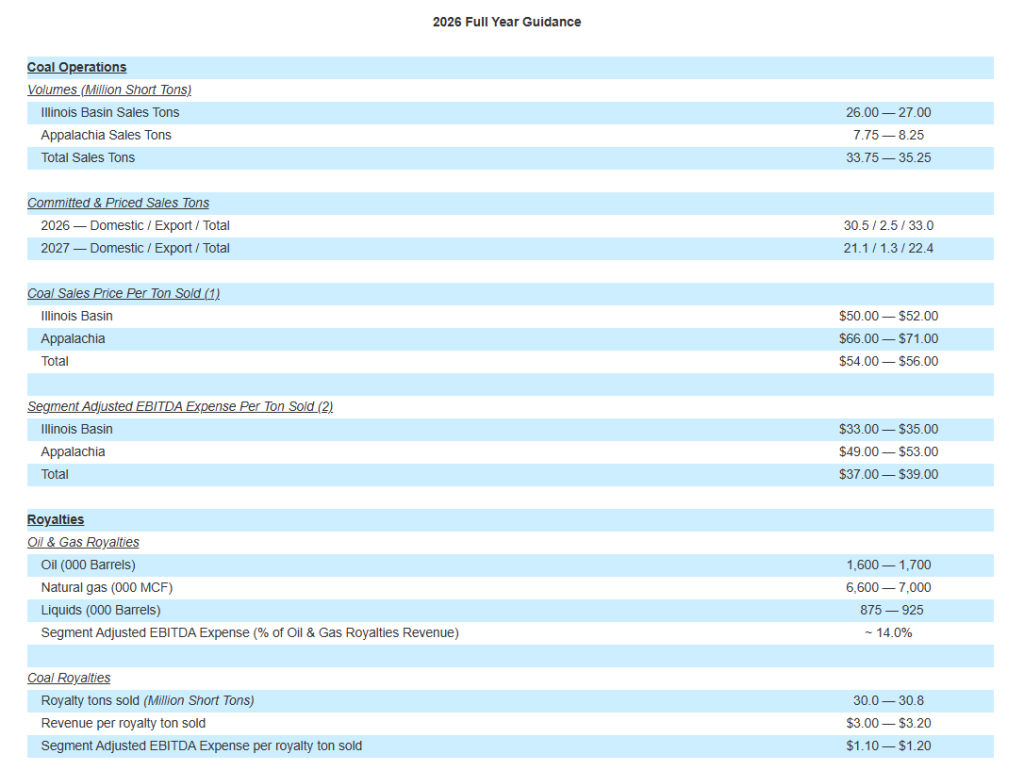

2026 expected coal sales volumes over 95% committed and priced at the midpoint of 2026 guidance

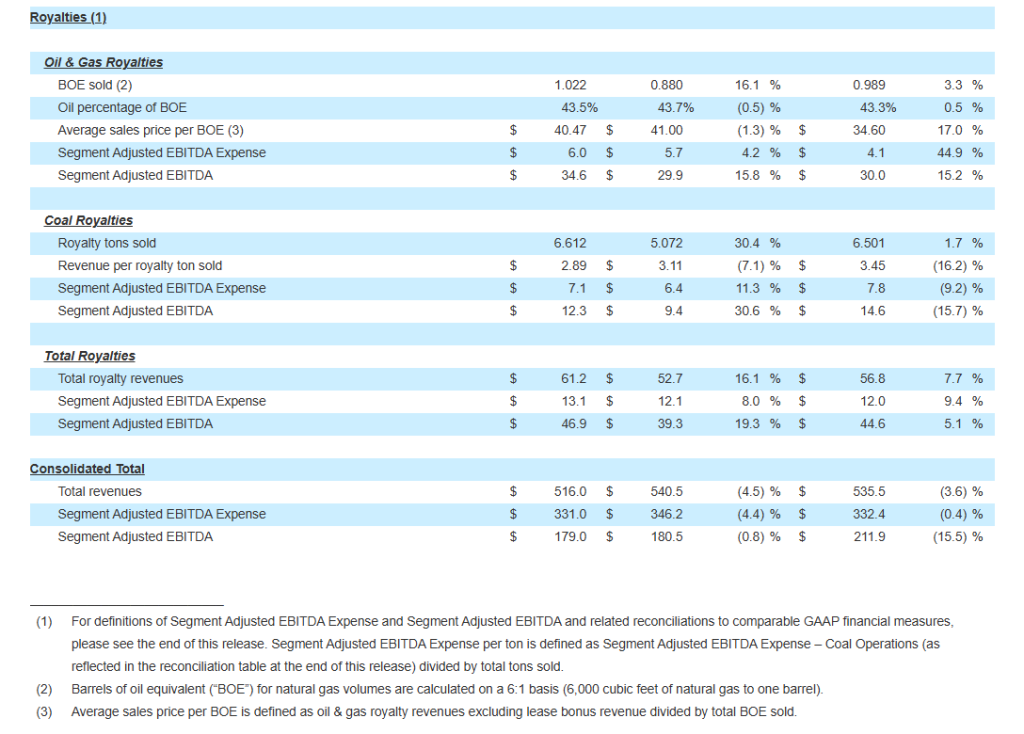

Record oil & gas royalty revenues and volumes, up 14.6% and 16.1%, respectively, year-over-year

Completed $16.2 million in oil & gas mineral interest acquisitions during the 2026 Quarter

Total and net leverage ratios as of March 31, 2026, were 0.73 times and 0.69 times, respectively

Declares quarterly cash distribution of $0.60 per unit, or $2.40 per unit annualized

TULSA, Okla.–(BUSINESS WIRE)–Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter ended March 31, 2026 (the “2026 Quarter”). This release includes comparisons of results to the quarter ended March 31, 2025 (the “2025 Quarter”) and to the quarter ended December 31, 2025 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of Adjusted EBITDA and Segment Adjusted EBITDA Expense and related reconciliations to comparable GAAP financial measures, please see the end of this release.

Total revenues decreased 4.5% to $516.0 million for the 2026 Quarter compared to $540.5 million for the 2025 Quarter primarily due to lower coal sales pricing, partially offset by record oil & gas royalty revenues and higher coal sales volumes. Net income for the 2026 Quarter was $9.1 million, or $0.07 per basic and diluted limited partner unit, compared to $74.0 million, or $0.57 per basic and diluted limited partner unit, for the 2025 Quarter. Net income was impacted by lower coal sales and higher depreciation, as well as an $11.6 million decrease in the fair value of our digital assets and a $37.8 million non-cash asset impairment charge in the 2026 Quarter due to ceasing longwall production and uncertainty regarding future operations at our Mettiki mine. Adjusted EBITDA decreased 3.1% to $155.0 million in the 2026 Quarter compared to $159.9 million in the 2025 Quarter.

Compared to the Sequential Quarter, total revenues decreased by 3.6% due to lower coal sales volumes and prices, partially offset by higher oil & gas royalty revenues. Net income decreased by 89.0% compared to the Sequential Quarter primarily due to lower production and lower coal sales volumes from our Hamilton mine as a result of a planned extended longwall move during the 2026 Quarter that led to higher per ton operating expenses. In addition, increased depreciation, non-cash asset impairment charges at Mettiki and lower investment income contributed to lower net income in the 2026 Quarter. Adjusted EBITDA for the 2026 Quarter decreased by 18.9% compared to the Sequential Quarter primarily due to higher costs at Hamilton and Mettiki.

CEO Commentary

“Most of our coal operations performed better than expected during the quarter, however meaningful weather-related shipment disruptions relating to Winter Storm Fern delayed sales volumes for the quarter,” said Joseph W. Craft III, Chairman, President and Chief Executive Officer. “In the Illinois Basin, increased productivity at River View and Gibson South helped offset some of the impact of the planned extended longwall move at Hamilton. In Appalachia, Tunnel Ridge had production gains of approximately 28% compared to both the 2025 Quarter and the Sequential Quarter, while results at Mettiki reflected lower production and a non-cash impairment associated with ceasing longwall production and uncertainty regarding future operations as previously discussed.”

Mr. Craft added, “We delivered another record quarter in our oil & gas royalties segment, driven by increased production volumes and higher oil prices. Increased drilling and completion activity across our core basins continues to validate the quality of our mineral portfolio, and for the second consecutive quarter, we expanded our portfolio, completing $16.2 million in acquisitions during the quarter. These results underscore the durability of our asset base and reinforce our disciplined approach to allocating capital to attractive, long-lived mineral interests. We believe our oil and gas royalties portfolio enhances our cash flow stability and long-term optionality across commodity cycles.”

Coal Operations

Coal sales volumes decreased by 5.9% in the Illinois Basin compared to the Sequential Quarter due primarily to decreased tons sold from our Hamilton mine as a result of a planned extended longwall move during the 2026 Quarter. In Appalachia, tons sold increased by 3.6% and 8.0% compared to the 2025 Quarter and Sequential Quarter, respectively, primarily as a result of fewer production days in the prior periods at our Tunnel Ridge mine due to longwall moves. Coal sales price per ton sold decreased by 7.4% in the Illinois Basin compared to the 2025 Quarter as a result of the expiration of higher priced legacy contracts. In Appalachia, coal sales price per ton sold decreased by 4.8% and 11.1% compared to the 2025 Quarter and Sequential Quarter, respectively, primarily due to an increased sales mix of lower priced Tunnel Ridge sales volumes in the 2026 Quarter and reduced domestic sales price per ton. ARLP ended the 2026 Quarter with total coal inventory of 1.2 million tons, representing a decrease of 0.2 million tons and an increase of 0.1 million tons compared to the end of the 2025 Quarter and Sequential Quarter, respectively.

Segment Adjusted EBITDA Expense per ton in the Illinois Basin increased 3.4% compared to the Sequential Quarter due primarily to the planned extended longwall move at our Hamilton mine during the 2026 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton for the 2026 Quarter decreased by 10.8% compared to the 2025 Quarter as a result of increased production at our Tunnel Ridge operation primarily as a result of fewer production days due to the longwall moves in the 2025 Quarter.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment increased to $34.6 million in the 2026 Quarter compared to $29.9 million and $30.0 million in the 2025 Quarter and Sequential Quarter, respectively, due to record oil & gas royalty volumes, which increased 16.1% and 3.3%, respectively, as a result of increased drilling and completion activities on our interests and acquisitions of additional oil & gas mineral interests. Improved commodity pricing also contributed to the increase in Segment Adjusted EBITDA compared to the Sequential Quarter.

Segment Adjusted EBITDA for the Coal Royalties segment increased to $12.3 million in the 2026 Quarter compared to $9.4 million in the 2025 Quarter due to higher royalty tons sold, primarily from Tunnel Ridge, partially offset by lower average royalty rates per ton received from the Partnership’s mining subsidiaries. Compared to the Sequential Quarter, Segment Adjusted EBITDA for the Coal Royalties segment decreased 15.7%, primarily reflecting lower realized royalty rates per ton.

Balance Sheet and Liquidity

As of March 31, 2026, total debt and finance leases were outstanding in the amount of $507.7 million. The Partnership’s total and net leverage ratios were 0.73 times and 0.69 times debt to trailing twelve months Adjusted EBITDA, respectively, as of March 31, 2026. ARLP ended the 2026 Quarter with total liquidity of $431.2 million, which included $28.9 million of cash and cash equivalents and $402.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities. In addition, ARLP held 618 bitcoins valued at $42.2 million as of March 31, 2026.

Distributions

ARLP announced today that the Board of Directors of ARLP’s general partner approved a cash distribution to unitholders for the 2026 Quarter of $0.60 per unit (an annualized rate of $2.40 per unit), payable on May 15, 2026, to all unitholders of record as of the close of trading on May 8, 2026.

Concurrent with this announcement we are providing qualified notice to brokers and nominees that hold ARLP units on behalf of non-U.S. investors under Treasury Regulation Section 1.1446-4(b) and (d) and Treasury Regulation Section 1.1446(f)-4(c)(2)(iii). Brokers and nominees should treat one hundred percent (100%) of ARLP’s distributions to non-U.S. investors as being attributable to income that is effectively connected with a United States trade or business. In addition, brokers and nominees should treat one hundred percent (100%) of the distribution as being in excess of cumulative net income for purposes of determining the amount to withhold. Accordingly, ARLP’s distributions to non-U.S. investors are subject to federal income tax withholding at a rate equal to the highest applicable effective tax rate plus ten percent (10%). Nominees, and not ARLP, are treated as the withholding agents responsible for withholding on the distributions received by them on behalf of non-U.S. investors.

Outlook

“Looking ahead, contracting activity with domestic utility customers for 2026 has remained active, though the pace has varied as some customers continue to evaluate summer burn requirements,” commented Mr. Craft. “During the quarter, the Iran conflict briefly reopened U.S. thermal coal export activity in early March, enabling us to enter into contracts for 1.8 million tons to be delivered in 2026 and 2027. In addition, we sold an additional 0.5 million tons to domestic customers, bringing our sales book to more than 95% committed and priced for 2026 assuming production comes in at the midpoint of our guidance range. Our remaining open position is concentrated in the second half of 2026, where additional commitments will depend on summer burn and customer requirements. More broadly, we continue to see a constructive demand backdrop as growing power demand, particularly from data centers, reinforces the importance of reliable baseload generation.”

Mr. Craft continued, “We expect first quarter shipment disruptions tied to Winter Storm Fern and subsequent high-water conditions to be recovered over the balance of the year. In addition, once the planned longwall moves at Hamilton and Tunnel Ridge are completed in the second quarter, we do not expect any further longwall moves in 2026, which should improve operating visibility for the back half of the year.”

Mr. Craft concluded, “Based on year-to-date outperformance of our oil & gas royalties, we are increasing our volume guidance for the segment. Recent strength and volatility in crude oil prices have increased the near-term outlook and, because our current portfolio is unhedged, changes in market prices are reflected directly in our realized pricing. If current market conditions persist, we would expect realized BOE prices to be higher than last year, contributing to stronger segment results.”

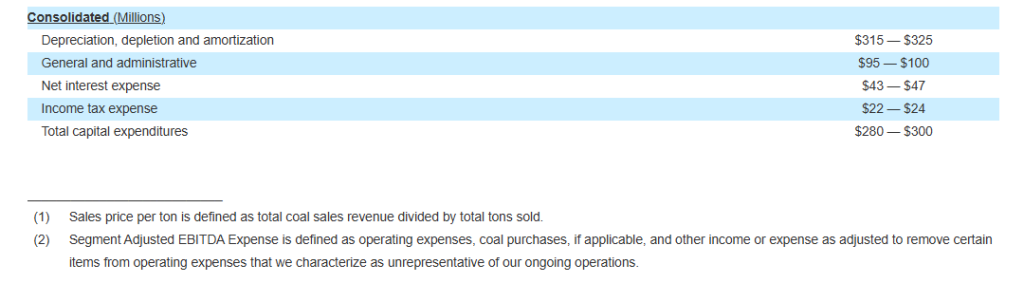

ARLP is updating the following guidance for the full year ending December 31, 2026:

Conference Call

A conference call regarding ARLP’s 2026 Quarter financial results and updated 2026 guidance is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13759702.

About Alliance Resource Partners, L.P.

ARLP is a diversified natural resource company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as a reliable energy partner for the future by pursuing opportunities that support the growth and development of energy-related technologies and infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at [email protected].

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

Two of the offshore energy sector’s most recognized names are joining forces. Helix Energy Solutions Group (NYSE: HLX) and Hornbeck Offshore Services have announced a definitive all-stock merger agreement that will create one of the most comprehensive integrated deepwater services companies in the world — and the timing couldn’t be more calculated.

Under the terms of the deal, Hornbeck shareholders will own approximately 55% of the combined company while Helix shareholders retain roughly 45% on a fully diluted basis. The newly formed entity will operate under the Hornbeck Offshore Services name and trade on the New York Stock Exchange under the ticker symbol “HOS.” Todd Hornbeck, currently Chairman, President and CEO of Hornbeck, will lead the combined company, with William Transier serving as Chairman of a seven-member board comprised of three Helix directors and four from Hornbeck.

Why This Deal Makes Strategic Sense

This isn’t a merger of desperation — it’s a merger of expansion. Helix brings deep subsea expertise, well intervention capabilities, and a global robotics fleet with operations spanning the Gulf of America, Brazil, North Sea, West Africa and Asia Pacific. Hornbeck contributes a fleet of technologically advanced, high-specification offshore support vessels with a strong concentration in the Americas, including Brazil and Mexico, along with meaningful exposure to U.S. government and offshore wind contracts.

Together, the combined company covers the entire life cycle of deepwater field operations — from installation and production enhancement to decommissioning — across energy, defense and renewables. That kind of end-to-end service coverage significantly reduces the cyclicality risk that has historically plagued pure-play offshore services companies.

The Numbers Behind the Deal

The transaction is expected to generate $75 million or more in annual revenue and cost synergies within three years of closing. Those synergies will come from integrated service offerings, expanded customer reach and fleet optimization that reduces reliance on expensive third-party vessel charters.

The combined backlog currently stands at approximately $2 billion — split evenly between the two companies — with $1 billion tied to long-term contracts in Hornbeck’s military and specialty vessel segments. That backlog provides meaningful near-term revenue visibility as the integration unfolds.

Helix also reported Q1 2026 revenue of $287.95 million, beating analyst estimates by roughly $24 million, and reiterated full-year 2026 guidance of $1.2 billion to $1.4 billion in revenue with EBITDA projected between $230 million and $290 million. The company closed Q1 with $501 million in cash and just $10 million in funded debt — a balance sheet position that gives the combined entity significant flexibility for organic growth or further M&A post-close.

What to Watch

The merger requires Helix shareholder approval and customary regulatory sign-offs, with closing expected in the second half of 2026. Notably, Ares Management funds, representing a significant portion of Hornbeck’s ownership, have already delivered written consent approving the transaction — removing one of the more common deal-risk variables upfront.

For investors tracking the small and midcap offshore services space, this deal reshapes the competitive landscape. The combined HOS will be a scaled, diversified operator in a sector where scale increasingly determines who wins long-term contracts and who gets squeezed out.

The deepwater services consolidation wave continues — and this merger puts the new Hornbeck Offshore squarely at its center.

West Texas Intermediate crossed $104 per barrel Monday morning as the U.S. formally blockaded the Strait of Hormuz, putting an official military stamp on a crisis that has already cut the waterway’s commercial traffic by more than 90% since late February. Oil has surged more than 55% since the U.S.-Israel air campaign against Iran began. The large-cap conversation around this move centers on inflation, rate policy, and Big Oil earnings. The small-cap opportunity underneath it is considerably more specific — and considerably less crowded.

Domestic energy producers don’t carry the insurance exposure, rerouting costs, or geopolitical risk that’s hammering international supply chains. When global energy flows are disrupted at the source — and the Strait of Hormuz handles roughly 25% of the world’s seaborne oil and 20% of global LNG exports — the demand vacuum gets filled by producers operating entirely outside the conflict zone. U.S. domestic natural gas producers, onshore oil operators, and domestic refiners are each collecting a demand premium that didn’t exist eight weeks ago.

The LNG dynamic is particularly important for small-cap energy investors. Qatar and the UAE supply a substantial share of LNG to Asian buyers. With Qatari LNG facilities struck by Iranian drones and Gulf shipping lanes effectively closed, Asian markets are competing aggressively for alternative supply — pulling from U.S. export terminals at a pace that is tightening the domestic natural gas market. That demand surge is landing at exactly the moment AI infrastructure is driving electricity consumption higher. Data centers require massive volumes of consistent baseload power, and natural gas remains the backbone of that grid in the United States. The theoretical “AI-Energy Nexus” that analysts have been discussing is no longer theoretical — it is being forced into reality by a geopolitical event that knocked out the world’s primary LNG export corridor.

Domestic refiners are in a comparably favorable position. With crude prices elevated and refining margins widening as global capacity strains, mid-size operators processing domestic crude are capturing spread that simply wasn’t available in a $70-per-barrel world. Large-cap refining names have already moved. Many small and microcap upstream producers with pure domestic production profiles have lagged the repricing — a pattern that historically corrects as the supply story matures and investors rotate down the market cap spectrum.

The broader implications extend beyond hydrocarbons. The Hormuz crisis is accelerating a policy conversation with real capital allocation consequences: the shift from “green energy” to “secure energy.” Nuclear, domestic grid hardening, and U.S.-based energy infrastructure are being reconsidered as national security imperatives rather than purely climate investments. That reframing is attracting new institutional attention to sectors that were previously viewed as transitional.

The primary risk is speed. A diplomatic breakthrough or a durable ceasefire could reverse oil toward the $80 range and compress margins that have only recently expanded. Energy executives are warning, however, that even if the Strait reopens, infrastructure damage and the global shipping backlog could take months to fully unwind — putting a floor under the repricing that has already occurred.

For investors focused on the small and microcap space, the Hormuz crisis is not just an oil price story. It is a structural demand signal for domestic producers operating in a global market that suddenly cannot source enough of what they have.

TULSA, Okla.–(BUSINESS WIRE)–Alliance Resource Partners, L.P. (NASDAQ: ARLP) will report its first quarter 2026 financial results before the market opens on Monday, April 27, 2026. Alliance management will discuss these results during a conference call beginning at 10:00 a.m. Eastern that same day.

To participate in the conference call, dial U.S. Toll Free (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13759702.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the second largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as a reliable energy partner for the future by pursuing opportunities that support the growth and development of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at [email protected].

Contacts

Investor Relations Contact

Cary P. Marshall Senior Vice President and Chief Financial Officer (918) 295-7673 [email protected]

")

")