Research News and Market Data on GHM

August 06, 2026 6:30am EDT Download as PDF

First Quarter Fiscal 2027 Highlights:

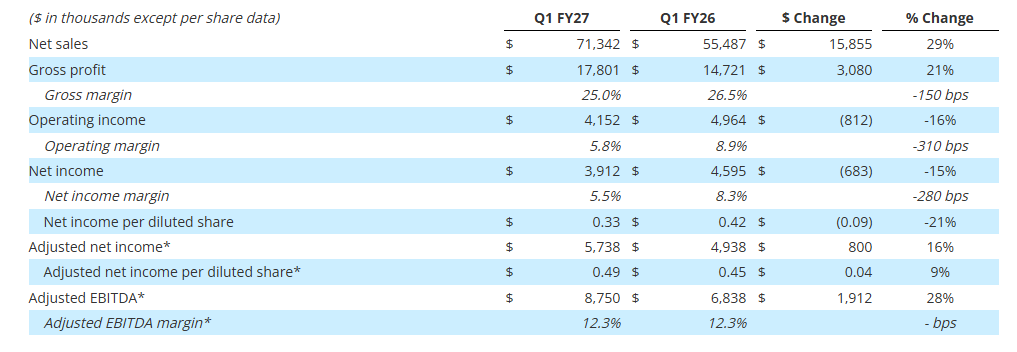

- Record net sales of $71.3 million, increased 29% compared to the prior year reflecting strength of diversified revenue base

- Gross profit increased 21% to $17.8 million; Gross profit margin was 25.0%

- Net income per diluted share was $0.33; Adjusted net income per diluted share(1) was $0.49

- Adjusted EBITDA (1) increased 28% to $8.8 million; Adjusted EBITDA margin(1) was 12.3%

- Orders (2) were $95.9 million; Book-to-Bill (2) ratio of 1.3x and record backlog (2) of $557.2 million

- Strengthened balance sheet with $27.0 million in cash and no outstanding debt following $50.0 million stock issuance and repayment of $13.0 million of debt during the quarter

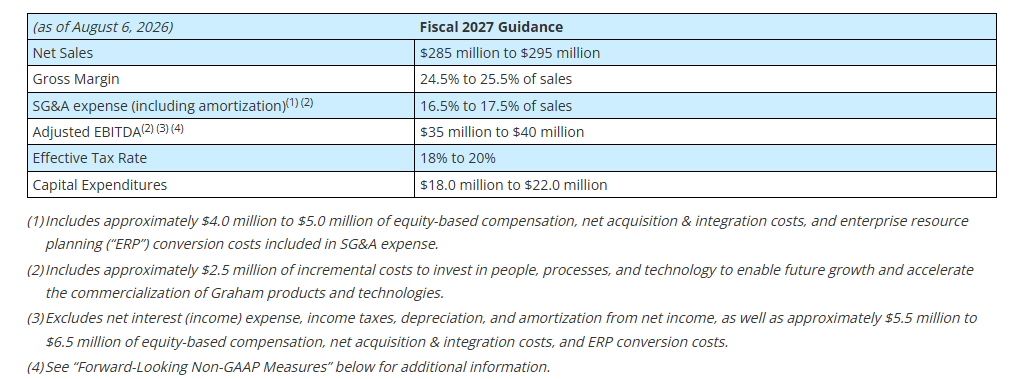

- Reaffirming full year fiscal 2027 guidance

BATAVIA, N.Y.–(BUSINESS WIRE)– Graham Corporation (NYSE: GHM) (“GHM” or the “Company”), a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Space, and Energy & Process industries, today reported financial results for its first quarter for the fiscal year ending March 31, 2027 (“fiscal 2027”).

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “Our first quarter results reflect continued disciplined execution and give us confidence as we look ahead to the remainder of fiscal 2027. Our revenue growth was across all of our business units, and bookings remained strong, which we believe, along with our record backlog, positions us well to achieve our long-term growth and profitability goals.”

Mr. Malone continued, “At our Investor Day in June 2026, we introduced our three-year financial framework as we enter our next phase of growth which reflects the favorable tailwinds we see across our end markets. As we execute against our strategy, we remain focused on converting these opportunities into profitable growth, expanding margins and delivering long-term value for our shareholders.”

| 1 Adjusted net income per diluted share, Adjusted EBITDA and Adjusted EBITDA margin are non-GAAP measures. See attached tables and other information for important disclosures regarding Graham’s use of these non-GAAP measures. | ||

| 2 Orders, backlog and book-to-bill ratio are key performance metrics. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics. |

First Quarter Fiscal 2027 Performance Review

(All comparisons are with the same prior-year period unless noted otherwise.)

Net sales for the first quarter of fiscal 2027 were $71.3 million, up $15.9 million, or 29%, compared with the first quarter of fiscal 2026, reflecting the strength of our diversified revenue base, as well as the acquisition of FlackTek, which added $6.6 million to revenue during the quarter. The increase for the quarter was across multiple markets, including an $11.8 million, or 40%, increase in sales to the Defense market, primarily due to the timing of project milestones, as well as new programs and growth in existing programs. Sales to the Space market increased $2.9 million, or 86%, over the prior year first quarter, due to new programs and the ramp up of existing programs, as well as the FlackTek acquisition. Sales to the Energy & Process markets increased $1,098, or 5%, as increases in Aftermarket sales are partially offset by push outs on large capital project activity. Aftermarket sales to the Energy & Process and Defense markets of $9.7 million remained strong, increasing 20% over the first quarter of the prior year.

Gross profit for the first quarter of fiscal 2027 was $17.8 million or 25.0% of sales, compared with $14.7 million, or 26.5% of sales, in the prior-year period. The 150-basis point decline in gross profit margin reflects the mix of sales in the first quarter of fiscal 2027, and in particular, a higher level of Defense sales and material receipts, which carry a lower profit margin.

Selling, general and administrative expense (“SG&A”), including intangible amortization, for the first quarter of fiscal 2027 increased $3.2 million or 33%, over the prior year first quarter. Acquisition and integration expenses contributed $0.6 million of the increase compared to the prior year first quarter. Additionally, incremental SG&A from the acquisition of FlackTek accounted for $1.8 million of the increase. The remaining increase primarily reflects investments the Company is making in its people, processes, and technology, which we expect to be approximately $2.5 million of incremental costs for fiscal 2027, partially offset by a reduction in costs related to the Barber-Nichols Performance Bonus, which is no longer in effect in fiscal 2027. During the first quarter of fiscal 2026, the Company recorded $1.1 million related to the Barber-Nichols Performance Bonus, inclusive of applicable payroll taxes and no corresponding expense was recorded in the first quarter of fiscal 2027.

Cash Management and Balance Sheet

Cash and cash equivalents as of June 30, 2026, were $27.0 million, compared with $6.6 million in the previous quarter. During the quarter, the Company strengthened its balance sheet through a $50.0 million investment from accounts advised by T. Rowe Price, of which $13.0 million of the proceeds were used for debt repayment, with the remaining proceeds expected to fund future organic and inorganic growth opportunities.

Net cash used by operating activities was $12.7 million during the first quarter of fiscal 2027, primarily due to the timing of billing and collection of accounts receivable and unbilled revenue and customer deposits, as well as the payment of fiscal 2026 bonuses, including the Barber-Nichols Performance Bonus, during the quarter.

Capital expenditures, net for the first quarter of fiscal 2027 were $2.6 million, focused on capacity expansion, increasing capabilities, and productivity improvements.

The Company had no debt outstanding as of June 30, 2026, with $74.5 million available on its revolving credit facility after taking into account outstanding letters of credit.

Orders, Backlog, and Book-to-Bill Ratio

See supplemental data filed with the Securities and Exchange Commission on Form 8-K and provided on the Company’s website for a further breakdown of orders and backlog by market. See “Key Performance Indicators” below for important disclosures regarding Graham’s use of these metrics ($ in millions).

Orders for the first quarter of fiscal 2027 were $95.9 million, compared with $125.9 million in the prior year first quarter, which included $86.5 million of follow-on orders to support the U.S. Navy’s Virginia Class Submarine program. Order activity in the quarter continued to reflect strong demand in the Defense market, including approximately $61.8 million of new and follow-on orders to support the U.S. Navy’s Columbia and Virginia Class Submarine programs, as well as to provide mission-critical hardware for the MK48 Mod 7 Heavyweight Torpedo. Space market orders totaled $14.4 million, or 2.3x net Space sales for the quarter. Total Aftermarket orders for the Energy & Process and Defense markets increased 5% to $10.9 million and FlackTek contributed $13.2 million to orders during the quarter or 2.0x net FlackTek sales.

Note that our orders tend to be lumpy given the nature of our business (i.e. large capital projects) and in particular, orders to the Defense industry, which span multiple years and can be significantly larger in size.

Backlog at quarter end was a record $557.2 million, a 15% increase over the prior-year period, driven by strong bookings in the Defense and Space markets, and contributions from the FlackTek acquisition. For the quarter, the Company achieved a book-to-bill ratio of 1.3x, continuing momentum from a book-to-bill ratio of 1.5x in FY 2026. Approximately 35% to 40% of orders currently in backlog are expected to be converted to sales in the next twelve months, another 20% to 25% are expected to convert to sales within one to two years, and the remaining beyond two years. Approximately 84% of our backlog as of June 30, 2026, was to the Defense industry, which provides stability and visibility for future revenue.

Fiscal 2027 Outlook

Graham’s Chief Financial Officer, Christopher J. Thome, said, “Our first quarter results reflect the discipline we have applied across the business, and we enter fiscal 2027 with a stronger, more flexible balance sheet and no outstanding debt. This financial flexibility supports our ability to continue investing in both organic and inorganic growth while maintaining the operating discipline that has defined our performance.”

Mr. Thome continued, “With our first quarter results in line with our expectations, we are reaffirming our full year fiscal 2027 guidance. We remain focused on converting our record backlog into profitable growth as we execute throughout the remainder of the year.”

Webcast and Conference Call

GHM’s management will host a conference call and live webcast on August 6, 2026, at 11:00 a.m. Eastern Time (“ET”) to review its financial results as well as its strategy and outlook. The review will be accompanied by a slide presentation, which will be made available immediately prior to the conference call on GHM’s investor relations website.

A question-and-answer session will follow the formal presentation. GHM’s conference call can be accessed by calling (877) 407-0784, or (201) 689-8560 (International). Alternatively, the webcast can be monitored from the events section of GHM’s investor relations website.

A telephonic replay will be available from 3:00 p.m. ET today through Thursday, August 13, 2026. To listen to the archived call, dial (844) 512-2921 and enter conference ID number 13761669, or access the webcast replay via the Company’s website at ir.grahamcorp.com, where a transcript will also be posted once available.

About Graham Corporation

Graham is a global leader in the design and manufacture of mission critical fluid, power, heat transfer, vacuum, and advanced mixing technologies for the Defense, Space, Energy & Process industries. Graham Corporation and its family of global brands are built upon world-renowned engineering expertise, proprietary technologies, as well as its responsive and flexible service and the unsurpassed quality customers have come to expect from the Company’s products and systems. Graham Corporation routinely posts news and other important information on its website, grahamcorp.com, where additional information on Graham Corporation and its businesses can be found.

Safe Harbor Regarding Forward Looking Statements

This news release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements are subject to risks, uncertainties and assumptions and are identified by words such as “continue,” “estimate,” “expects,” “focus,” “future,” “opportunities,” “outlook,” “believes,” “could,” “guidance,” “may”, “will,” “plan,” “strategy,” and other similar words. All statements addressing operating performance, events, or developments that Graham Corporation expects or anticipates will occur in the future, including but not limited to, profitability of future projects and the business, its ability to deliver to plan, its ability to continue to strengthen relationships with customers in the Defense industry, its ability to secure future projects and applications, expected expansion and growth opportunities, anticipated sales, revenues, adjusted EBITDA, adjusted EBITDA margins, capital expenditures and SG&A expenses, the timing of conversion of backlog to sales, orders, market presence, profit margins, tax rates, foreign sales operations, customer preferences, changes in market conditions in the industries in which it operates, changes in general economic conditions and customer behavior, forecasts regarding the timing and scope of the economic recovery in its markets, and its acquisition and growth strategy, are forward-looking statements. Because they are forward-looking, they should be evaluated in light of important risk factors and uncertainties. These risk factors and uncertainties are more fully described in Graham Corporation’s most recent Annual Report filed with the Securities and Exchange Commission (the “SEC”), included under the heading entitled “Risk Factors”, and in other reports filed with the SEC.

Should one or more of these risks or uncertainties materialize or should any of Graham Corporation’s underlying assumptions prove incorrect, actual results may vary materially from those currently anticipated. In addition, undue reliance should not be placed on Graham Corporation’s forward-looking statements. Except as required by law, Graham Corporation disclaims any obligation to update or publicly announce any revisions to any of the forward-looking statements contained in this news release.

View source version on businesswire.com: https://www.businesswire.com/news/home/20260805783838/en/

For more information, contact:

Christopher J. Thome

Vice President – Finance and CFO

Phone: (585) 343-2216

Tom Cook

Investor Relations

(203) 682-8250

[email protected]

Source: Graham Corporation

Released August 6, 2026