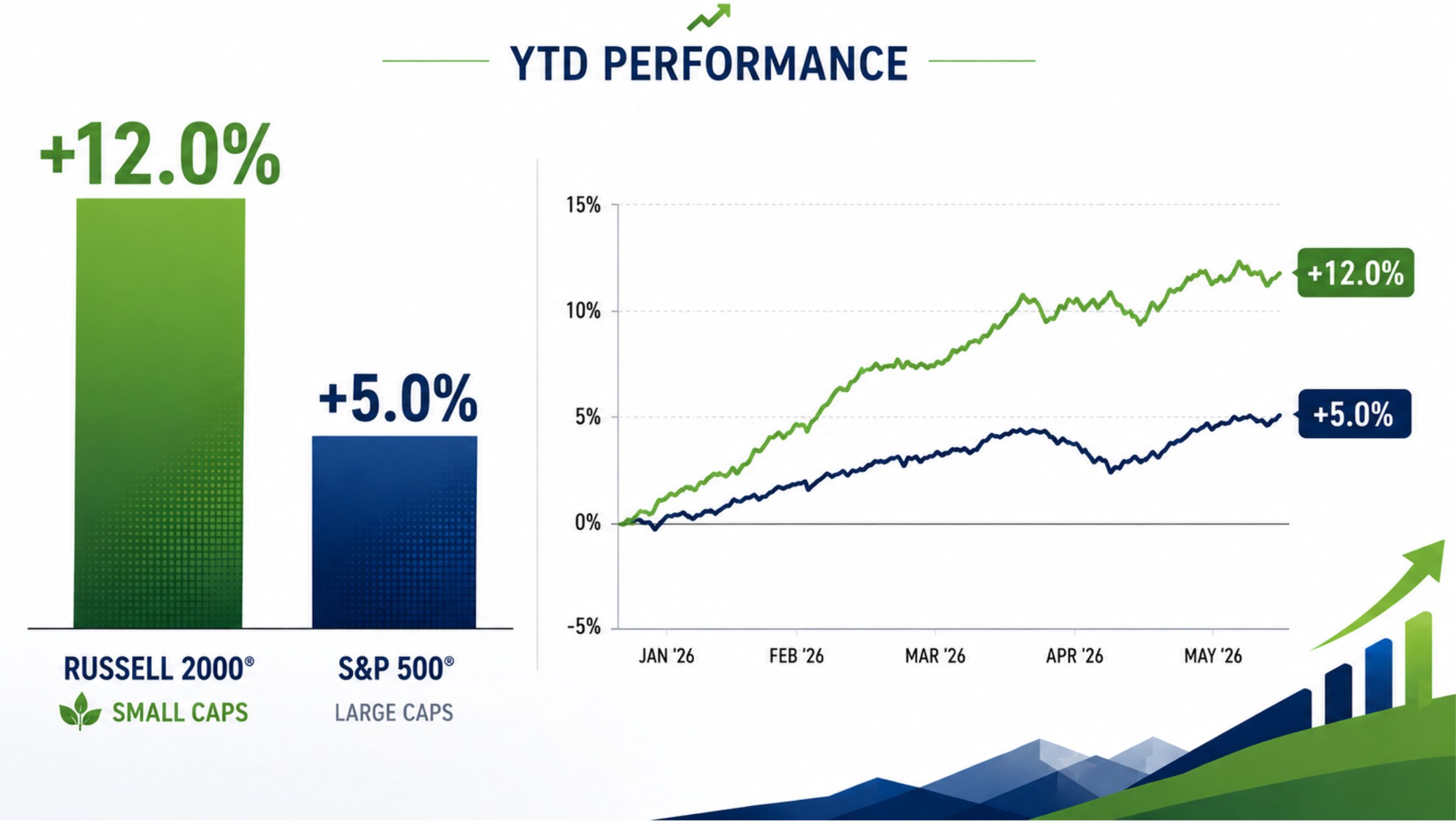

The numbers are now official and they tell a story that most of the financial media spent the first six months of 2026 largely ignoring. The Russell 2000 surged nearly 22% through the first half of the year, marking its strongest January-through-June performance since 1991. That is not a typo. Small caps have not started a year this strong in 35 years.

For context, the Dow Jones Industrial Average gained 8.9% over the same period. The S&P 500 rose 9.6%. The Nasdaq climbed 12.8%. Small caps outperformed all of them, and it was not particularly close.

How We Got Here

The first half was anything but smooth. The US went to war with Iran in late February, sending oil above $100 and inflation to a three-year high. Treasury yields hit levels not seen since 2007. Consumer sentiment fell to an all-time record low. A new Federal Reserve chair took office and immediately dropped the central bank’s easing bias. By any conventional reading, this should have been a terrible environment for small caps.

Instead, the Russell 2000 powered through it. The index staged a historic 15-session winning streak against the S&P 500 in January, posted the strongest microcap returns in years through the spring, and held its ground even as chip stocks sold off and large cap technology leadership faltered in June. Active managers had their best month of the year in June as market breadth expanded and capital rotated away from a handful of mega cap names and into the broader market.

Why the Second Half Setup Is Compelling

Three forces that weighed on small caps during the first half are now either reversing or stabilizing, and that shift is what makes the second half particularly interesting.

First, oil prices. Brent crude has fallen below $75 after trading above $110 at its peak. The Iran ceasefire and the gradual reopening of the Strait of Hormuz are removing the energy cost pressure that squeezed consumer-facing small caps all spring. Lower fuel costs flow almost immediately into improved operating margins for the transportation, logistics, food service, and retail companies that bore the brunt of the spring squeeze.

Second, yields. The 10-year Treasury has dropped below 4.5% as oil declines ease inflation expectations. That matters directly for the small and microcap companies carrying variable-rate debt, because lower yields translate into lower borrowing costs and a more favorable refinancing environment heading into the back half of the year.

Third, market breadth. The rotation out of concentrated mega cap technology positions and into the broader market accelerated meaningfully in June. More than 63% of S&P 500 stocks now trade above their 50-day moving average, up from 50% at the start of the month. The correlation between cap-weighted and equal-weighted S&P returns fell to its lowest level since 2003. Capital is spreading out, and small caps are catching it.

The Valuation Case Has Not Closed

Despite a 22% first-half gain, the Russell 2000 still trades at a meaningful discount to the S&P 500 on a forward earnings basis. The valuation gap has narrowed but remains near historically wide levels. Consensus earnings growth estimates for small caps continue to run well above large cap projections. The fundamentals that drove the first-half rally have not been exhausted. They have been reinforced.

History offers one more data point worth noting. When the Russell 2000 has posted a first-half gain of 15% or more, the second half has been positive roughly 80% of the time.

Thirty-five years is a long time between records. The small cap market just set one. The conditions heading into the second half suggest it has room to keep going.