For years, the story of the U.S. equity market was written by a handful of mega-cap technology names. That story is being rewritten in 2026, and small-cap investors are the ones holding the pen.

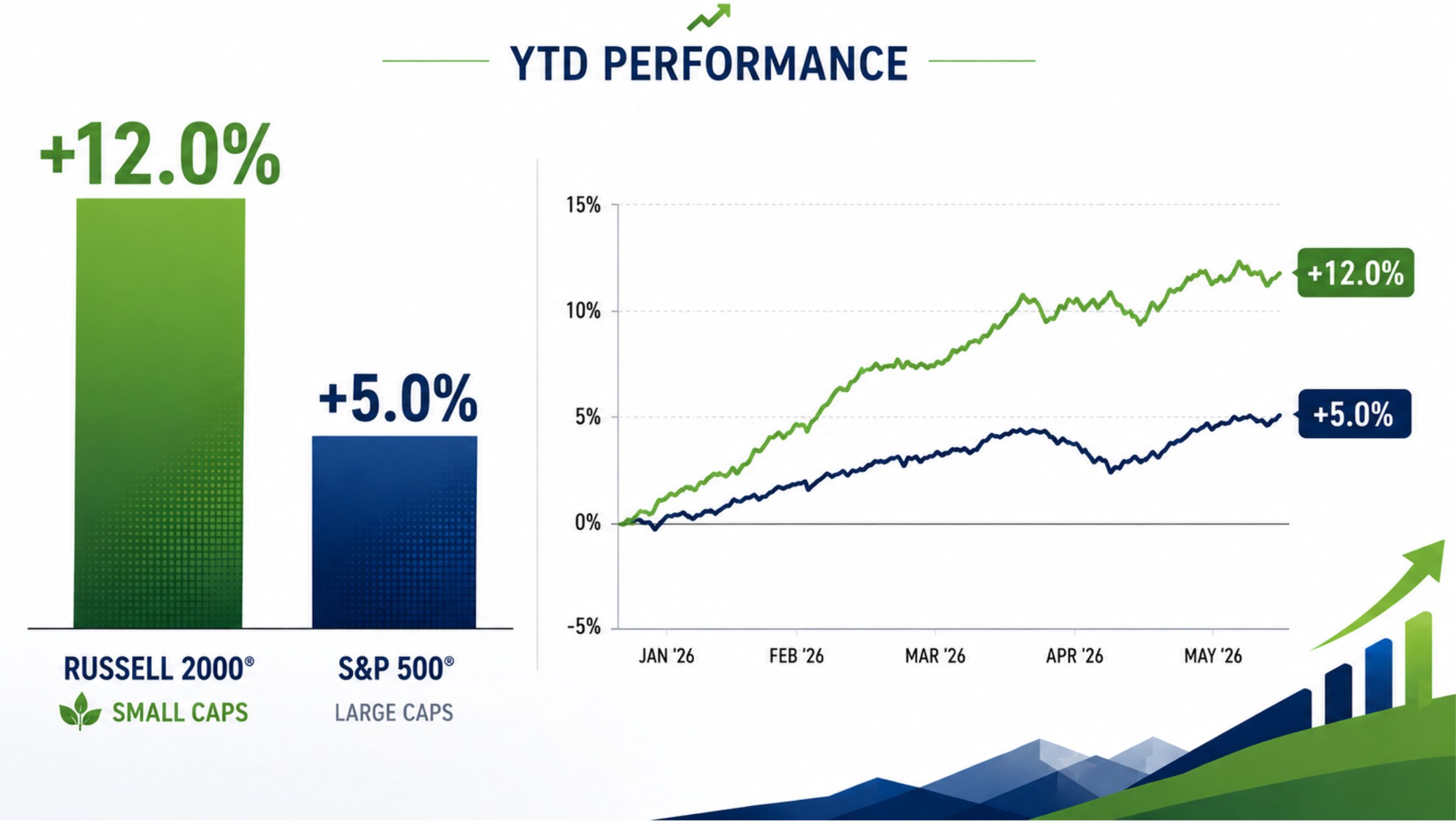

The Russell 2000 is up approximately 12% year-to-date, more than double the S&P 500’s roughly 5% gain over the same period. That gap isn’t noise — it reflects a meaningful structural shift in where capital is flowing and why.

The earnings picture is the starting point. Small-cap companies are projected to deliver 18% to 22% earnings growth for the full year in 2026, compared to roughly 13% for large caps. Analyst forecasts extend that outperformance into 2027 as well, with another 17–18% growth expected — suggesting this isn’t a one-quarter anomaly but the early stage of a sustained cycle.

The valuation argument reinforces the case. The S&P 500 currently trades near 28 times earnings. The Russell 2000 trades around 18 times. The S&P 600 — widely considered the higher-quality small-cap benchmark — sits near 16 times forward earnings. That’s a discount of roughly 40% to large caps. Historically, gaps of that magnitude don’t persist; they close, and when they do, small-cap investors collect outsized returns.

The macro setup has been equally supportive. The Federal Reserve’s rate-cutting cycle throughout 2025, which brought the federal funds rate to the 3.50%–3.75% range, disproportionately benefited smaller companies that carry more floating-rate debt. As interest expense declined, margins expanded — and earnings started to catch up to valuations.

M&A activity is amplifying the opportunity. U.S. transaction volume for deals over $100 million is up 25% by deal count and 43% by value in early 2026, with private equity firms deploying capital after years of sitting on record dry powder. For small-cap shareholders, that dealmaking environment creates a meaningful premium opportunity — acquisitions of quality small-cap targets at 30–40% premiums are not uncommon in the current environment.

Domestic revenue exposure is adding another layer of appeal. In an environment where tariff uncertainty and global supply chain risk remain real considerations, companies with predominantly U.S.-focused revenue streams are commanding renewed investor attention. Many small and microcap companies fit that profile by nature.

None of this means every small-cap stock is a buy. The rotation is rewarding companies with strong balance sheets, reliable cash flow, and a defensible market position. Those carrying excessive debt or lacking a clear path to profitability are being bypassed. The quality filter is real.

But for investors who track the small and microcap space — the roughly $250 million to $2 billion market cap range where institutional coverage is thin and price discovery is still happening — the current setup represents one of the more compelling opportunities in recent memory. The window doesn’t stay open indefinitely.