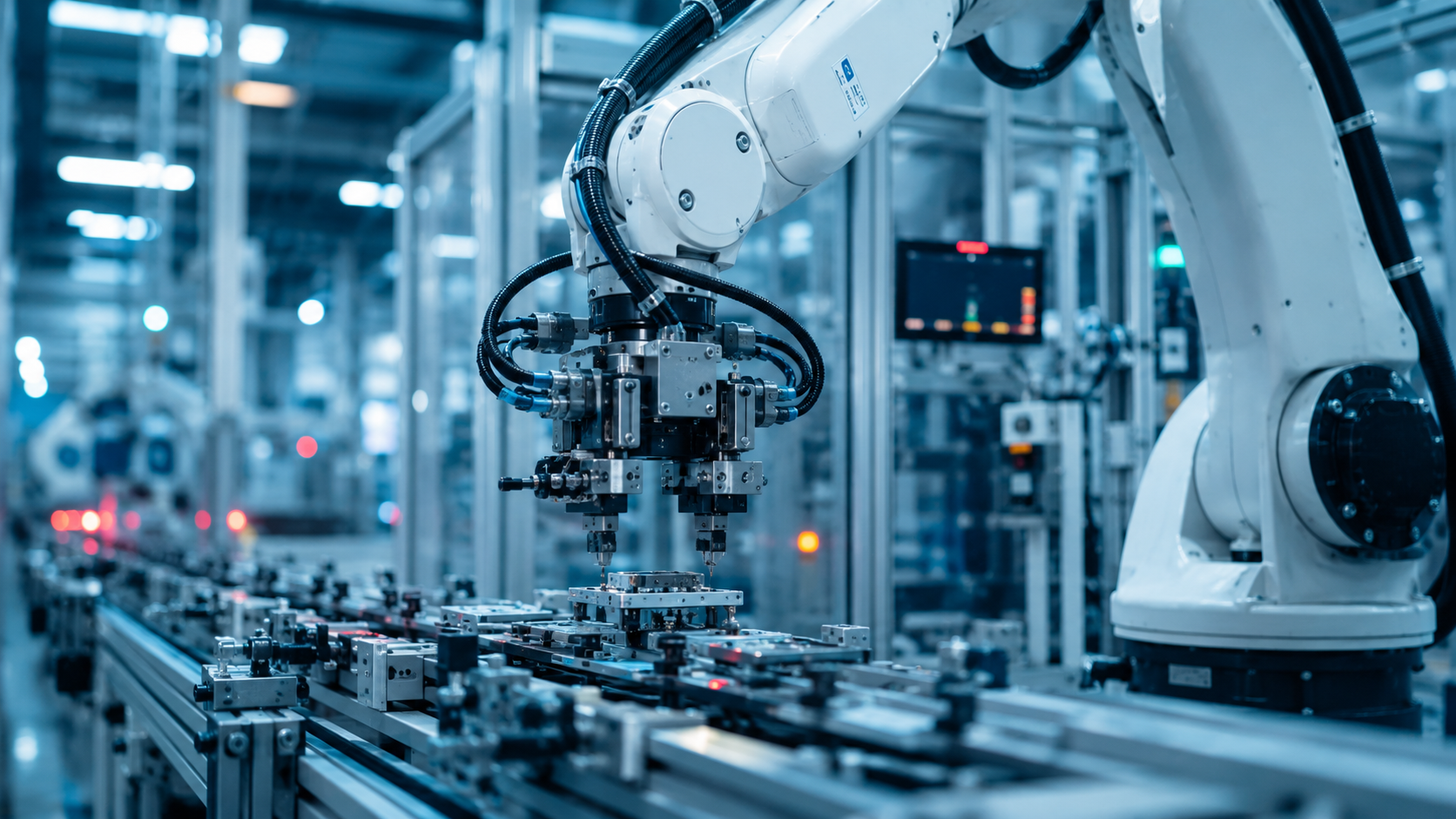

What was once one of the most high-profile partnerships in technology has turned into one of its most explosive legal battles. Apple filed a federal trade secret lawsuit against OpenAI on July 10 in the Northern District of California, alleging that the AI company orchestrated a systematic campaign to steal confidential hardware designs, supplier information, and product specifications through former Apple employees. The complaint also names io Products, the hardware design firm co-founded by former Apple design chief Jony Ive that OpenAI acquired last year.

The allegations are not subtle. Apple’s filing describes a coordinated effort at every level of OpenAI’s organization to acquire proprietary information about unreleased Apple hardware products. The two former employees at the center of the case are Tang Tan, who served as a vice president at Apple before becoming OpenAI’s Chief Hardware Officer, and engineer Chang Liu, who Apple alleges departed with an unreturned company laptop and exploited a software bug that gave him continued access to Apple’s internal file servers after his departure. Apple further claims that OpenAI interviewers encouraged job candidates to bring Apple prototypes and physical components to interviews as part of the hiring process.

OpenAI has denied the allegations, stating that the company has no interest in other companies’ trade secrets and remains focused on building its own technology.

From Partners to Adversaries

The lawsuit represents a dramatic reversal in the relationship between the two companies. As recently as mid-2025, Apple and OpenAI were working together to integrate ChatGPT into Apple’s software platforms and Siri digital assistant. That partnership has since dissolved entirely. In January 2026, Apple announced it was turning to Google for its Apple Intelligence initiatives, and the companies have been moving in increasingly competitive directions ever since, particularly in the emerging AI hardware device market.

The timing of Apple’s filing is significant for reasons beyond the legal merits. OpenAI confidentially filed for an IPO earlier this summer at a reported valuation of $730 billion to $850 billion, with Goldman Sachs and Morgan Stanley leading the offering. A trade secret lawsuit of this magnitude, filed by the most valuable company in the world, introduces material uncertainty into that process. Discovery alone could force OpenAI to disclose internal communications and hardware development timelines that it would strongly prefer to keep private during a pre-IPO quiet period.

The Three-Way AI Rivalry Deepens

The Apple-OpenAI conflict does not exist in isolation. It is playing out against the backdrop of an intensifying three-way rivalry between Apple, OpenAI, and SpaceX, whose CEO Elon Musk co-founded OpenAI before leaving and eventually launching the competing xAI platform. Musk weighed in immediately after the lawsuit was filed, and the public back-and-forth between Musk and OpenAI CEO Sam Altman escalated over the weekend as both companies simultaneously released competing AI models.

SpaceX completed its record $75 billion IPO in June and is pursuing a $60 billion acquisition of AI coding company Cursor. OpenAI is preparing its own public offering. Apple is navigating a CEO transition as Tim Cook prepares to step down later this year. All three companies are competing aggressively for AI talent, hardware capabilities, and market positioning at the same time.

What It Means for the Broader AI Ecosystem

For investors tracking the AI sector, particularly smaller companies operating in the hardware, semiconductor, and AI infrastructure space, the Apple-OpenAI dispute carries practical implications. If the lawsuit slows or disrupts OpenAI’s hardware ambitions, the competitive landscape for AI device development shifts. Smaller companies building AI edge hardware, consumer AI devices, and specialized components could find themselves operating in a market where one of the most well-funded competitors is legally constrained from executing its product roadmap on the original timeline.

The AI hardware race just became a legal battle. How it resolves will shape competitive dynamics across the sector for years.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a global leader in providing augmented reality (“AR”) and artificial intelligence (“AI”) Software-as-a-Service (“SaaS”) solutions to beauty and fashion industries, today announced that it plans to release its financial results for the second quarter of 2026 before U.S. markets open on Monday, July 27, 2026.

About Perfect Corp.

Founded in 2015, Perfect Corp. is a leading AI company offering self-developed AI- and AR- powered solutions dedicated to transforming the world with digital tech innovations that make your virtual world beautiful. On its direct to consumer business, Perfect operates a family of YouCam consumer apps and web-editing services for photo, video and camera users, centered on unleashing creativity with AI-driven features for creation, beautification and enhancement. On the enterprise business side, Perfect empowers major beauty, skincare, fashion, jewelry, and watch brands and retailers by supplying them with omnichannel shopping experiences through AR product try-ons and AI-powered skin diagnostics. With cutting-edge technologies such as Generative AI, real-time facial and hand 3D AR rendering and cloud solutions, Perfect enables personalized, enjoyable, and engaging shopping journey and helps brands elevate customer engagement, increase conversion rates, and propel sales growth. Throughout this journey, Perfect maintains its unwavering commitment to environmental sustainability and fulfilling social responsibilities. For more information, visit https://ir.perfectcorp.com/.

SK Hynix began trading on the Nasdaq this morning, and the market’s answer to seven-times oversubscribed demand was immediate. Shares opened at $170, up 14% from the $149 offer price, and were trading as much as 16.7% higher intraday under the temporary ticker SKHYV before the stock moves to its permanent symbol, SKHY, on Monday.

The final numbers on the raise came in at $26.5 billion, slightly below the roughly $28 billion initially targeted but still enough to make this the largest first-time listing by a foreign company in U.S. history, surpassing Alibaba’s American debut. The offering consisted of 177.9 million American depositary receipts, each representing one-tenth of a common share.

The scale of demand tells the real story here. SK Hynix’s South Korea-listed shares have climbed 174% over the past six months and 634% over the past year, and the company’s SEC filing disclosed it now holds 56.4% of the global high-bandwidth memory market, the largest share among the three companies, Micron, Samsung, and SK Hynix, that make this specialized chip. HBM sits directly next to AI processors like Nvidia’s GPUs, holding the data those chips need instantly rather than forcing them to reach across a data center for it. Every major AI buildout depends on it, and there currently isn’t enough to go around.

That shortage, according to industry estimates cited in today’s coverage, could persist into 2030 simply because new fabrication capacity takes years to bring online. It is precisely what SK Hynix’s listing is designed to help fix. Proceeds are earmarked for new manufacturing facilities and equipment, giving U.S. investors a rare direct stake in a name that has mostly been accessible only through Seoul-listed shares.

But the timing carries its own tension. Just three days before this debut, memory stocks including Micron, Samsung, and SK Hynix itself slid into a bear market, a reminder that this industry has a well-earned reputation for violent cycles. Patrick Moorhead, founder of Moor Insights & Strategy, put it bluntly, noting that memory makers were selling chips below cost with negative gross margins only a few years ago before capital expenditure pulled back sharply and demand caught fire again. Micron has responded by locking customers into five-year strategic supply agreements with large upfront payments, a structural shift from the one-year contracts that used to define the industry, aimed at smoothing out exactly this kind of boom-and-bust pattern. Whether that holds the next downturn at bay is an open question nobody can answer yet.

For small and micro-cap investors, SK Hynix itself is now a trillion-dollar company well outside that world. But the moment matters anyway. When the second-largest foreign listing in U.S. history debuts to a 14% pop just days after its own sector fell into bear market territory, it captures the exact push and pull defining the memory trade in 2026: extraordinary current profitability sitting on top of an industry that has never once avoided the cycle eventually turning. The public companies feeding into this supply chain, from equipment makers to specialty materials suppliers, are all trading in that same shadow today.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a leading artificial intelligence (“AI”) company offering AI and augmented reality (“AR”)-powered solutions to beauty, fashion, photo and video creative industries, announced today that it has entered into a definitive Agreement and Plan of Merger (the “Merger Agreement”), dated as of July 10, 2026, with ProjectNY, an exempted company with limited liability incorporated under the laws of the Cayman Islands controlled by Ms. Alice H. Chang (“Merger Sub”), pursuant to which, and subject to the terms and conditions thereof, Merger Sub will merge with and into the Company (the “Merger”), with the Company surviving the Merger as the surviving company (the “Surviving Company”) and becoming a privately held company.

Pursuant to the terms of the Merger Agreement, at the effective time of the Merger (the “Effective Time”), each ordinary share of the Company issued and outstanding immediately prior to the Effective Time, other than the Excluded Shares, the Continuing Shares and the Dissenting Shares, each as defined in the Merger Agreement, will be cancelled and cease to exist in exchange for the right to receive US$2.00 in cash per share without interest (the “Per Share Merger Consideration”).

The Per Share Merger Consideration represents a premium of approximately 48.1% to the closing price of the Company’s Class A ordinary shares on March 17, 2026, the last trading day prior to the Company’s announcement on March 18, 2026 of its receipt of the preliminary non-binding going-private proposal, and a premium of approximately 39.6% to the volume-weighted average closing price of the Company’s Class A ordinary shares during the 30 trading days prior to that announcement.

Concurrently with the execution of the Merger Agreement, Merger Sub entered into separate voting and support agreements with Ms. Alice H. Chang and her controlled entities GOLDEN EDGE CO., LTD., DVDonet.com. Inc. and World Speed Company Limited (the “Chairwoman Parties”) as well as CyberLink International Technology Corp. (“CyberLink”). Pursuant to such agreements, Chairwoman Parties and CyberLink will vote all ordinary shares they hold directly or indirectly in favor of the authorization and approval of the Merger Agreement, the plan of merger and the transactions contemplated thereby, including the Merger. Such ordinary shares represent approximately 53.4% of the total issued and outstanding share capital of the Company and approximately 81.2% of the total voting power of the Company as of the date of the Merger Agreement.

The Merger is expected to be funded through available cash of the Company and its subsidiaries. The Continuing Shareholders will not receive cash consideration for their Continuing Shares, which will not be cancelled in the Merger and will remain outstanding and continue to exist as ordinary shares of the Surviving Company at the Effective Time.

The Company’s board of directors (the “Board”), acting upon the unanimous recommendation of the special committee of independent and disinterested directors established by the Board (the “Special Committee”), approved the Merger Agreement, the plan of merger, and the transactions contemplated thereby, including the Merger, and resolved to recommend that the Company’s shareholders vote to approve them. The Special Committee negotiated the terms of the Merger Agreement with the assistance of its own financial and legal advisors.

The Merger, which is currently expected to close during the last quarter of 2026, is subject to customary closing conditions, including the approval of the Merger Agreement, the plan of merger and the transactions contemplated thereby, including the Merger, by the affirmative vote of at least two-thirds of the votes cast by holders of the Company’s ordinary shares present and voting in person or by proxy as a single class at an extraordinary general meeting of the Company’s shareholders.

If completed, the Merger will result in the Company becoming a privately held company, its Class A ordinary shares will no longer be listed on the New York Stock Exchange, and the Company’s Class A ordinary shares and warrants will be deregistered under the U.S. Securities Exchange Act of 1934, as amended.

Advisors

Kroll, LLC is serving as financial advisor to the Special Committee; DLA Piper UK LLP is serving as international legal counsel to the Special Committee.

Sullivan & Cromwell LLP is serving as U.S. legal counsel to Merger Sub, the Chairwoman Parties and CyberLink; and Maples and Calder (Hong Kong) LLP is serving as Cayman Islands legal counsel to Merger Sub and the Chairwoman Parties.

Additional Information About the Merger

The Company will furnish to the U.S. Securities and Exchange Commission (the “SEC”) a current report on Form 6-K regarding the Merger, which will include as an exhibit thereto the Merger Agreement. All parties desiring details regarding the Merger are urged to review these documents, which will be available at the SEC’s website.

In connection with the Merger, the Company will prepare and mail to its shareholders a proxy statement that will include a copy of the Merger Agreement. In addition, in connection with the Merger, the Company and certain other participants in the Merger will prepare and file with the SEC a Schedule 13E-3 transaction statement that will include the Company’s proxy statement (the “Schedule 13E-3”). INVESTORS AND SHAREHOLDERS ARE URGED TO READ CAREFULLY AND IN THEIR ENTIRETY THE SCHEDULE 13E-3, THE PROXY STATEMENT AND OTHER MATERIALS FILED WITH OR FURNISHED TO THE SEC WHEN THEY BECOME AVAILABLE, AS THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY, THE MERGER AND RELATED MATTERS. In addition to receiving the proxy statement and Schedule 13E-3 by mail, shareholders will also be able to obtain these documents, as well as other filings containing information about the Company, the Merger and related matters, without charge from the SEC’s website.

This announcement is neither a solicitation of proxy, an offer to purchase nor a solicitation of an offer to sell any securities, and it is not a substitute for any proxy statement, Schedule 13E-3 or other materials that may be filed with or furnished to the SEC in connection with the Merger.

About Perfect Corp.

Founded in 2015, Perfect Corp. is a leading AI company offering self-developed AI- and AR-powered solutions dedicated to transforming the world with digital tech innovations that make your virtual world beautiful. On Perfect’s direct consumer business side, Perfect operates a family of YouCam consumer apps and web-editing services for photo, video and camera users, centered on unleashing creativity with AI-driven features for creation, beautification and enhancement. On Perfect’s enterprise business side, Perfect empowers major beauty, skincare, fashion, jewelry, and watch brands and retailers by supplying them with omnichannel shopping experiences through AR product try-ons and AI-powered skin diagnostics. With cutting-edge technologies such as Generative AI, real-time facial and hand 3D AR rendering and cloud solutions, Perfect enables a personalized, enjoyable and engaging shopping journey and helps brands elevate customer engagement, increase conversion rates, and propel sales growth. Throughout this journey, Perfect maintains its unwavering commitment to environmental sustainability and fulfilling social responsibilities. For more information, visit https://ir.perfectcorp.com/.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act, that are based on beliefs and assumptions and on information currently available to Perfect. In some cases, forward-looking statements can be identified by words such as may, will, could, would, should, expect, intend, plan, anticipate, believe, estimate, predict, project, potential, continue, ongoing, target, seek or the negative or plural of these words, or other similar expressions that are predictions or indicate future events or prospects, although not all forward-looking statements contain these words. Forward-looking statements in this communication include, without limitation, statements regarding the proposed Merger, the expected timing and completion of the Merger, the expected funding of the Merger, the expected treatment of the Company’s ordinary shares, options, warrants, Company Earnout Shares and Continuing Shares, the expected delisting and deregistration of the Company’s Class A ordinary shares and warrants, the expected filing and mailing of transaction materials, the anticipated timing of the shareholders meeting and the expected benefits or effects of the Merger. These statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by these forward-looking statements. Factors that could cause actual results to differ materially include, among others, risks and uncertainties relating to the ability to complete the Merger on the proposed terms or anticipated timeline or at all; the possibility that competing offers or acquisition proposals will be made; the possibility that required shareholder approval, regulatory approvals or other consents may not be obtained; the failure to satisfy other conditions to the completion of the Merger; potential litigation relating to the Merger; the amount of costs, fees, expenses and charges related to the Merger; the effect of the announcement, pendency or completion of the Merger on the Company’s business, results of operations, financial condition, cash flows, prospects, relationships with customers, suppliers and employees, operating results and business generally; and other risks and uncertainties described in the Company’s filings with the SEC. Perfect cannot assure you that the forward-looking statements in this communication will prove to be accurate. There may be additional risks that Perfect presently does not know or that Perfect currently does not believe are material that could also cause actual results to differ from those contained in the forward-looking statements. Forward-looking statements speak only as of the date they are made. Except as required by applicable law, Perfect does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Ecolab just paid $4.75 billion in cash for a Calgary-based company most investors have never heard of, and that single transaction tells you more about where AI infrastructure spending is headed than almost anything happening in chips right now.

The March 2026 acquisition of CoolIT Systems came at a price of 29 times next-twelve-months adjusted EBITDA. That is not the kind of multiple a serious industrial buyer pays on a whim. It’s a signal that liquid cooling has moved from a nice-to-have into a required piece of the AI data center stack, and Ecolab is not the only one who has figured that out.

The math behind the move is simple physics more than anything else. Modern AI training runs on GPU servers packed with far more processing density than traditional data centers were ever built to handle, and that density generates heat that conventional air cooling simply cannot dissipate fast enough. Nvidia’s newest Blackwell racks push thermal loads that force operators into direct-to-chip cooling, rear-door heat exchangers, or full immersion systems just to keep the hardware running. ASHRAE’s 2026 AI Data Center Energy Performance Framework now names these approaches explicitly as requirements, not options, for high-density AI deployments. MarketsandMarkets pegs the global liquid cooling market at $4.07 billion this year, growing to $27.65 billion by 2033, a 31.5% annual growth rate that would make most industries jealous.

Ecolab’s purchase of CoolIT is just the most recent entry in a run of consolidation that has been building for over a year. Trane Technologies has announced plans to acquire LiquidStack. Schneider Electric bought Motivair in 2025 specifically to build out its liquid cooling capabilities. Vertiv closed its acquisition of ThermoKey on June 12 and opened a new manufacturing facility in Malaysia on July 1 just to keep up with AI infrastructure orders. Every major player in industrial thermal management has either bought a specialist in this space or announced plans to. When that many strategic acquirers are willing to pay near 30 times forward earnings for private cooling companies, the public small and micro-cap names sitting in the same value chain tend to get repriced whether or not they’re involved in a deal themselves.

A handful of small-cap names sit right in the middle of this shift. Modine Manufacturing has spent the last three years transforming itself from a legacy automotive parts supplier into a company focused on data center thermal management, divesting older auto businesses along the way to sharpen that story. Limbach Holdings has leaned into the build-out from a different angle, highlighting its modular construction and prefabrication platform for data centers in a June announcement that positions the company squarely inside the high-density projects hyperscalers are commissioning right now. And nVent Electric, which has spent more than a decade building liquid cooling distribution and high-density power systems, saw organic orders jump roughly 65% in a recent quarter driven almost entirely by large cooling orders tied to hyperscaler programs. The company has already deployed more than a gigawatt of cooling capacity across its installed base.

The AI investment story so far has mostly been about chips, and understandably so. But chips are useless if you can’t keep them cool enough to run at full capacity, and that second half of the equation is where the next wave of investment dollars appears to be heading. Power, water, and industrial thermal management are becoming just as important to the AI buildout as the silicon itself, and the M&A activity happening right now is the clearest evidence yet that the biggest names in industrial equipment already see it that way. Modine, Limbach, and nVent aren’t household names, and that’s exactly the point. When a $77 billion company pays nearly $5 billion for a private cooling specialist, the small-cap names doing similar work for the same customers are the ones worth watching next.

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a global AI-centered technology research and advisory firm, said today it will release its second-quarter financial results on Wednesday, August 5, 2026, at approximately 4:15 p.m., U.S. Eastern Time.

The firm will host a conference call with investors and industry analysts at 9 a.m., U.S. Eastern Time, the following day, Thursday, August 6. Dial-in details are as follows:

The dial-in number for U.S. participants is +1 (800) 715-9871.

International participants should call +1 (646) 307-1963.

The security code to access the call is 2802159.

Participants are requested to dial in at least five minutes before the scheduled start time.

A recording of the conference call will be accessible on ISG’s investor relations page for approximately four weeks following the call.

About ISG

ISG (Nasdaq: III) is a global AI-centered technology research and advisory firm. A trusted partner to more than 900 clients, including 75 of the world’s top 100 enterprises, ISG is a long-time leader in technology and business services that is now at the forefront of leveraging AI to help organizations achieve operational excellence and faster growth. The firm, founded in 2006, is known for its proprietary market data and research, in-depth knowledge and governance of provider ecosystems, and the expertise of its 1,500 professionals worldwide working together to help clients maximize the value of their technology investments.

Michael Burry just shorted one of the best-performing stocks in the market, and the reasoning behind it is worth understanding whether you own semiconductor stocks or not.

The Scion Asset Management founder disclosed a new short position in Micron Technology (NASDAQ: MU) in a Substack post on July 2, entering at $1,051.87 per share. The stock dropped roughly 5.5% on the news, closing at $975.56. Burry also holds existing short positions in Nvidia, Applied Materials, and the iShares Semiconductor ETF (SOXX), and has said publicly that AI-related chip stocks could see a 30% correction from here.

Burry’s argument centers on one word: cyclicality. “Micron defines cyclical like no other,” he wrote, and he backed it up with numbers that are hard to wave away. The stock has suffered 34 drawdowns of more than 30% over the past 42 years. Its median return on invested capital sits at just 4%. Median return on equity comes in at 7%, which Burry called “frankly terrible.” Free cash flow has gone negative in 48% of quarters historically. And right now, Micron is trading further above its 200-day moving average than at any point since 1984, a stretch that includes the dot-com bubble. Burry dismissed the high-bandwidth memory business fueling the current rally as “just another in a very long series” of Micron products rather than a durable competitive edge.

It’s a compelling case built on four decades of history. The problem is that Micron’s most recent quarter does not look like the start of a downturn. For the period ending May 2026, the company posted $41.5 billion in revenue, up 345.7% year over year, with gross margin expanding to 84.6% from 37.7% a year earlier. On the June 24 earnings call, Chief Business Officer Sumit Sadana said customer demand for memory chips remains “well above our ability to supply” across nearly every product category through 2028. Long-term supply contracts, some running five years with prepayments attached, now account for at least half of the company’s revenue. That is not the profile of a business quietly cracking under the weight of a boom-and-bust cycle. It looks like a company locking in demand years in advance.

So which read is right? The piece of Burry’s argument that deserves the most attention isn’t the historical volatility data, it’s what he pointed to as the actual catalyst. South Korea recently announced mega semiconductor projects worth at least 1.35 trillion won, roughly $880 billion, including new fabrication plants from Samsung and SK Hynix. Burry called this “the beginning of the end.” Samsung, SK Hynix, and Micron together control close to 90% of the global DRAM market. When two of the three dominant players start committing hundreds of billions of dollars to new capacity, the pricing power that has driven this year’s memory rally typically doesn’t last forever. Supply eventually catches up to demand, and when it does in this industry, it tends to overshoot.

That dynamic is becoming more real by the day. SK Hynix debuted its U.S. listing today, raising approximately $28 billion in fresh capital, much of which is aimed squarely at expanding memory production capacity. Meanwhile, insiders at Micron have sold $124.9 million worth of shares over the past three months, a detail that doesn’t prove anything on its own but is worth filing away.

None of this settles the debate, and it shouldn’t. Micron is not a small or micro-cap company, but the memory supply chain it sits atop runs through dozens of smaller public names in testing, packaging, specialty materials, and thermal management, all of which trade on the same underlying cycle. When one of the most recognizable short sellers in the market publicly challenges the sustainability of an AI-driven supercycle in the exact stock that anchors that supply chain, the ripple effects extend well past Micron’s own share price. Investors holding exposure anywhere in the memory ecosystem now have a credible bear case sitting alongside the bull case, and the coming quarters, particularly how HBM pricing holds up against the wave of new South Korean capacity, will likely determine who was right.

Conduent Will Also Receive a 7% Interest in Quarterhill Inc.

Conduent Bolsters Financial Position

Tolling Agreement Follows Recently Announced Agreement to Sell Its Public Transit Business

FLORHAM PARK, N.J., June 30, 2026 — Conduent Incorporated (Nasdaq: CNDT), a global technology-driven business solutions and services provider, today announced that it has entered into a definitive agreement to sell its Tolling business (a division of Conduent Transportation) to Quarterhill Inc. (TSX: QTRH) (OTCQX: QTRHF), a leading global provider of intelligent transportation system solutions.

The sale has a purchase price of $70 million in cash, and Quarterhill will assume most liabilities associated with the business, including all surety bond obligations, further improving Conduent’s financial profile. The structure of the transaction enhances Conduent’s financial flexibility and reduces exposure to non-core obligations.

The transaction is expected to close before the end of 2026.

This agreement follows a separate transaction, announced in May, to sell the Public Transit business, also part of Conduent’s Transportation division, which is similarly expected to close before the end of 2026.

Together, these transactions simplify Conduent’s portfolio and increase focus on its core businesses, enhancing the predictability and durability of Conduent’s earnings profile.

“This Tolling transaction, alongside the previously announced Public Transit agreement, advances our strategy to simplify our portfolio, sharpen focus on our core businesses, and strengthen our financial foundation,” said Harsha V. Agadi, Conduent President and Chief Executive Officer. “We are continuing our strategic journey to enhance long-term value creation, including simplifying our business, strengthening the balance sheet, and increasing sustainable free cash flow.

“With more than four decades of experience in tolling, Quarterhill is extremely well positioned to support the Conduent Tolling team and its clients. As we move toward closing, we remain committed to delivering outstanding quality and performance for all Transportation clients while ensuring smooth transitions for both clients and associates.”

As part of the transaction, Conduent will also receive a 7% interest in Quarterhill Inc. along with registration rights and board observer rights, providing potential upside participation in future value creation.

With operations in the United States and United Kingdom, Conduent’s Tolling business provides mission‑critical technology that enables all‑electronic tolling, roadside and back‑office processing, image review, violation enforcement, and analytics. It supports more than 14 million tolling transactions per day.

Additional details of the transaction are outlined in Conduent’s 8-K filed with the U.S. Securities and Exchange Commission (SEC) today.

About Conduent Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 48,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $80 billion in government payments annually, enabling approximately 2.0 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 14 million tolling transactions every day. Learn more at www.conduent.com.

About Quarterhill Quarterhill is a global leader in the Intelligent Transportation System (ITS) industry, advancing mobility through smart infrastructure solutions that reduce congestion, improve roadway safety, and create more sustainable travel. Each year, Quarterhill’s platforms process billions of transactions, perform compliance and safety inspections on millions of commercial vehicles, and enable transportation agencies worldwide to optimize thousands of lanes of traffic to improve travel for everyone. Leveraging advanced artificial intelligence and machine learning technologies, Quarterhill’s platform delivers automation and predictive insight to help agencies manage transportation networks more efficiently. By working in close partnership with governments, communities, and industry leaders, Quarterhill is building today’s connected roadways while shaping the next generation of intelligent, resilient mobility. Quarterhill is listed on the TSX under the symbol QTRH and on the OTCQX Best Market under the symbol QTRHF. Learn more at www.quarterhill.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Awards. NN has secured a significant amount of additional 2026 immediate-supply awards for liquid cooling products that go into NVIDIA AI data center racks. The new awards are additive to prior communicated awards and greatly increase the size of NN’s liquid cooling product portfolio for AI data center racks. NN’s combined Data Center and Electric Grid business is already its 2nd-largest business, with a goal to grow it into the Company’s largest business by sales. The Data Center & Electric Grid end markets are the top targeted growth markets for the Company.

Successful Launch. In 1Q26, NN announced the launch of a custom-designed stainless-steel product line for the liquid-cooled data center market. Since then, the Company has secured multiple AI data center awards, invested in an initial complement of 17 next-generation, high-speed, high-precision CNC machines at its Wuxi, China, plant, and begun production.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Award. DLH has been awarded a multiple-award indefinite delivery/indefinite quantity (MAC ID/IQ) contract to provide a full range of logistics information technology services for U.S. Navy integrated platforms and DevSecOps pipelines. Under the contract, DLH will implement mission-driven, interoperable, and cost-effective solutions for customers as they confront critical system integration challenges. This new award should enable DLH to expand its offerings to the Navy, opening a new growth channel for the Company.

Details. DLH is one of multiple prime awardees on the contract, which includes a 5-year base period. The contract has a $250 million ceiling for all awardees. Task orders are expected to be released under the contract, for which DLH expects to compete.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The artificial intelligence trade has spent two years concentrated almost entirely inside the data center. onsemi (Nasdaq: ON) just made a $7 billion wager that the next chapter takes place out in the physical world. The Scottsdale-based semiconductor company announced it has entered into a definitive agreement to acquire Synaptics (Nasdaq: SYNA) in an all-stock transaction valued at approximately $7 billion in enterprise value — the largest acquisition in onsemi’s history and one of the more strategically revealing deals in the chip sector this year.

Under the terms, Synaptics shareholders will receive 1.350 shares of onsemi common stock for each Synaptics share, representing roughly a 19% premium to the 10-day volume-weighted average closing prices of both companies. The transaction is expected to close in mid-2027, subject to Synaptics shareholder and regulatory approvals.

What “Physical AI” Actually Means

The strategic concept driving the deal is what onsemi calls Physical AI — artificial intelligence embedded directly into devices and machines, enabling them to sense their environment, make decisions, act, and adapt in the real world. This is distinct from the data center AI that has dominated headlines. Where data center AI trains and runs large models in centralized facilities, Physical AI lives at the edge: in automobiles, industrial robots, factory equipment, medical devices, and connected consumer products.

onsemi frames the combined company as sitting at the intersection of four pillars: Power, Sense, Connected Compute, and Control. The company has long held strength in the first two — intelligent power management and sensing technologies for automotive and industrial markets. What it lacked was the compute and connectivity layer that turns raw sensor data into intelligent action. That is precisely what Synaptics brings.

What Synaptics Adds

Synaptics contributes four decades of innovation in Edge AI compute, human-machine interface technology, and wireless connectivity solutions. Its portfolio enables the kind of on-device intelligence and interaction that Physical AI requires — touch, display, voice, and connectivity systems that allow machines to interface with both their environment and their users. Combining Synaptics’ edge compute franchise with onsemi’s power and sensing leadership creates a company able to offer integrated solutions across every layer of the Edge AI stack.

The financial logic is anchored in market expansion. onsemi expects the acquisition to increase its total addressable market by $30 billion, bringing it to $243 billion by 2030. That is the size of the opportunity onsemi believes Physical AI represents as intelligence migrates out of the data center and into the billions of devices and machines operating in the physical economy.

Why This Matters Beyond the Two Companies

For investors tracking the broader semiconductor landscape, the onsemi-Synaptics combination carries a signal that extends well past the deal itself. The AI investment narrative has been overwhelmingly concentrated in data center infrastructure — GPUs, memory, networking, and the hyperscaler buildout. This transaction is a high-conviction bet by an established player that the next phase of AI value creation happens at the edge, in the physical world, embedded in real machines.

That thesis has direct implications for smaller companies. As Physical AI demand accelerates, the suppliers of edge sensors, power management components, connectivity modules, embedded compute, and the specialized materials that go into device-level intelligence stand to benefit. Many of those companies operate well below the $2 billion market cap threshold and sit in exactly the part of the supply chain that a Physical AI buildout would pull forward.

The data center AI trade has been the story of the past two years. onsemi just put $7 billion behind the idea that the physical world is next.

New capabilities combine real-time translation, AI-driven training simulation and voice enhancement technologies to improve customer satisfaction and help organizations scale service delivery globally

Conduent Incorporated (Nasdaq: CNDT), a global technology-driven business solutions and services company, today introduced new AI-powered capabilities within its Next Generation CX Platform designed to help organizations overcome language barriers, accelerate agent readiness and improve customer interactions. The platform combines real-time translation, AI-driven training simulation and voice enhancement technologies to help clients expand into new markets, improve service quality and increase customer satisfaction.

The Next Generation CX Platform is comprised of modular solutions that leverage AI, automation and advanced analytics to optimize customer interactions, enhance agent performance, improve contact center operations and generate actionable insights. Together, these capabilities help organizations deliver more consistent, personalized and efficient customer experiences across channels and geographies.

Real-Time Translation Helps Organizations Reach More Customers

As organizations expand globally, delivering support in customers’ preferred languages can be costly and complex. Recruiting multilingual agents, relying on interpreters or routing customers through multiple touchpoints can increase costs and create friction in the customer experience.

Conduent’s AI-powered real-time translation solution helps remove those barriers by enabling seamless conversations between customers and agents across more than 90 languages. Customers receive support in their preferred language while organizations continue to leverage their existing agent workforce and subject matter expertise. The solution enables organizations to expand into new markets more quickly while maintaining a consistent, high-quality customer experience.

AI-Powered Training Accelerates Agent Readiness

Effective training is critical to delivering exceptional customer service. Conduent’s AI-driven training simulation solution enables agents to practice realistic customer scenarios and receive targeted coaching based on analysis of voice, chat and screen interactions.

The solution provides consistent training experiences across languages and globally distributed teams, helping organizations onboard agents more efficiently and maintain service quality at scale. For clients with seasonal or cyclical customer service demands, such as tax season or holiday peaks, the solution can accelerate time to proficiency by up to 40%, enabling agents to become customer-ready faster.

Voice Enhancement Improves Customer Interactions

Conduent is also introducing AI-powered accent smoothing and noise cancellation capabilities to improve the clarity and effectiveness of customer-agent conversations. By reducing communication barriers and minimizing background distractions, these technologies help improve customer engagement, increase interaction quality and support faster issue resolution. The result is a more seamless customer experience and greater confidence in every interaction.

“The future of customer experience isn’t AI or people, it’s AI and people working together,” said George Wehbe, President, Commercial Solutions at Conduent. “Our Next Generation CX Platform has arrived. It helps clients reach more customers, onboard agents faster and deliver more consistent service across languages and geographies. By combining AI-powered automation with experienced agents, we’re helping organizations improve customer satisfaction while scaling more efficiently.”

About Conduent’s Next Generation CX Platform

Conduent’s Next Generation CX Platform combines AI-powered automation, agent enablement, operational intelligence and customer insights into a flexible suite of solutions that can be deployed across the customer experience lifecycle. The platform is designed to help organizations improve customer outcomes, increase operational efficiency and adapt to evolving customer expectations while maintaining the human expertise required to resolve complex issues and build long-term loyalty.

About Conduent

Conduent delivers digital business solutions and services spanning the commercial, government and transportation spectrum – creating valuable outcomes for its clients and the millions of people who count on them. The Company leverages cloud computing, artificial intelligence, machine learning, automation and advanced analytics to deliver mission-critical solutions. Through a dedicated global team of approximately 48,000 associates, process expertise and advanced technologies, Conduent’s solutions and services digitally transform its clients’ operations to enhance customer experiences, improve performance, increase efficiencies and reduce costs. Conduent adds momentum to its clients’ missions in many ways including disbursing approximately $80 billion in government payments annually, enabling approximately 2.0 billion customer service interactions annually, empowering millions of employees through HR services every year and processing over 14 million tolling transactions every day. Learn more at www.conduent.com .

Conduent is a trademark of Conduent Incorporated in the United States and/or other countries. Other names may be trademarks of their respective owners.

Intel (Nasdaq: INTC) stock soared more than 11% Thursday after President Trump posted on Truth Social that Apple has agreed to work with the chipmaker to build its processors. The announcement followed an earlier Wall Street Journal report that the two companies had reached a preliminary agreement under which Intel would manufacture chips for the iPhone maker. Intel declined to comment on the report.

The move caps an extraordinary run for a company that was written off by much of Wall Street barely a year ago. Intel stock has now climbed more than 250% since the start of 2026 and roughly 500% over the past twelve months, making it one of the most dramatic corporate turnarounds in the technology sector.

Why the Apple Report Matters

The significance of a potential Apple partnership is as much symbolic as it is financial. Apple previously relied on Intel chips for its laptops and desktops before abandoning the company in favor of designing its own custom silicon — a high-profile departure that came to symbolize Intel’s competitive decline over the past decade. A renewed manufacturing relationship, even a modest one, would represent a meaningful reversal of that narrative.

Industry analysts have tempered expectations on the initial scope. Early commentary suggests any first agreement would likely involve lower-volume, less critical components rather than Apple’s flagship processors. Intel will need to prove its manufacturing reliability before earning more substantial business. But as analysts noted, the first step is always the hardest — and Intel appears to be taking it.

A Foundry Strategy Finally Paying Off

The Apple report does not exist in isolation. It is the latest in a series of developments validating Intel’s multi-year effort to build out its foundry business — the arm of the company that manufactures chips for third-party customers rather than just for Intel itself. Recent reports indicate Intel will build three million Tensor Processing Units for Google, and that Nvidia is exploring using Intel to fabricate some of its own processors. Earlier this week, Intel announced that its latest 18A-P processor node has entered initial production, a key step toward full-volume manufacturing.

The turnaround effort began under former CEO Pat Gelsinger and has continued under current CEO Lip-Bu Tan, who has focused on aggressive cost-cutting while driving the foundry arm to secure external manufacturing deals. That strategy is now benefiting from favorable industry dynamics. TSMC, the world’s largest chip manufacturer, has been unable to provide enough capacity for all of its customers, forcing fabless chip companies — those without their own manufacturing capabilities — to seek alternative production partners. Intel has emerged as one of the few viable options.

The AI Tailwind Beneath It All

Underpinning the entire Intel story is the AI build-out and a structural shift in chip demand. While graphics processing units remain central to AI data centers, central processing units have become increasingly important as AI firms lean into agentic applications — digital assistants capable of performing tasks on a user’s behalf. As AI agents begin running more operations across networks, they increasingly rely on CPUs to complete requests, a segment where Intel holds genuine strength.

For investors tracking the broader semiconductor ecosystem, Intel’s resurgence carries a wider signal. The capacity constraints pushing major customers toward Intel are the same constraints reshaping the entire chip supply chain. Smaller semiconductor companies, specialty foundry service providers, and advanced packaging firms operating in adjacent parts of that supply chain are positioned within the same demand environment driving Intel’s recovery. When the largest chip customers cannot get enough capacity from the dominant manufacturer, the effects ripple across the entire sector — and the smaller companies serving that demand are worth watching closely.

Intel was left for dead a year ago. A 500% move later, the turnaround is no longer a thesis. It is happening.