The artificial intelligence trade has spent two years concentrated almost entirely inside the data center. onsemi (Nasdaq: ON) just made a $7 billion wager that the next chapter takes place out in the physical world. The Scottsdale-based semiconductor company announced it has entered into a definitive agreement to acquire Synaptics (Nasdaq: SYNA) in an all-stock transaction valued at approximately $7 billion in enterprise value — the largest acquisition in onsemi’s history and one of the more strategically revealing deals in the chip sector this year.

Under the terms, Synaptics shareholders will receive 1.350 shares of onsemi common stock for each Synaptics share, representing roughly a 19% premium to the 10-day volume-weighted average closing prices of both companies. The transaction is expected to close in mid-2027, subject to Synaptics shareholder and regulatory approvals.

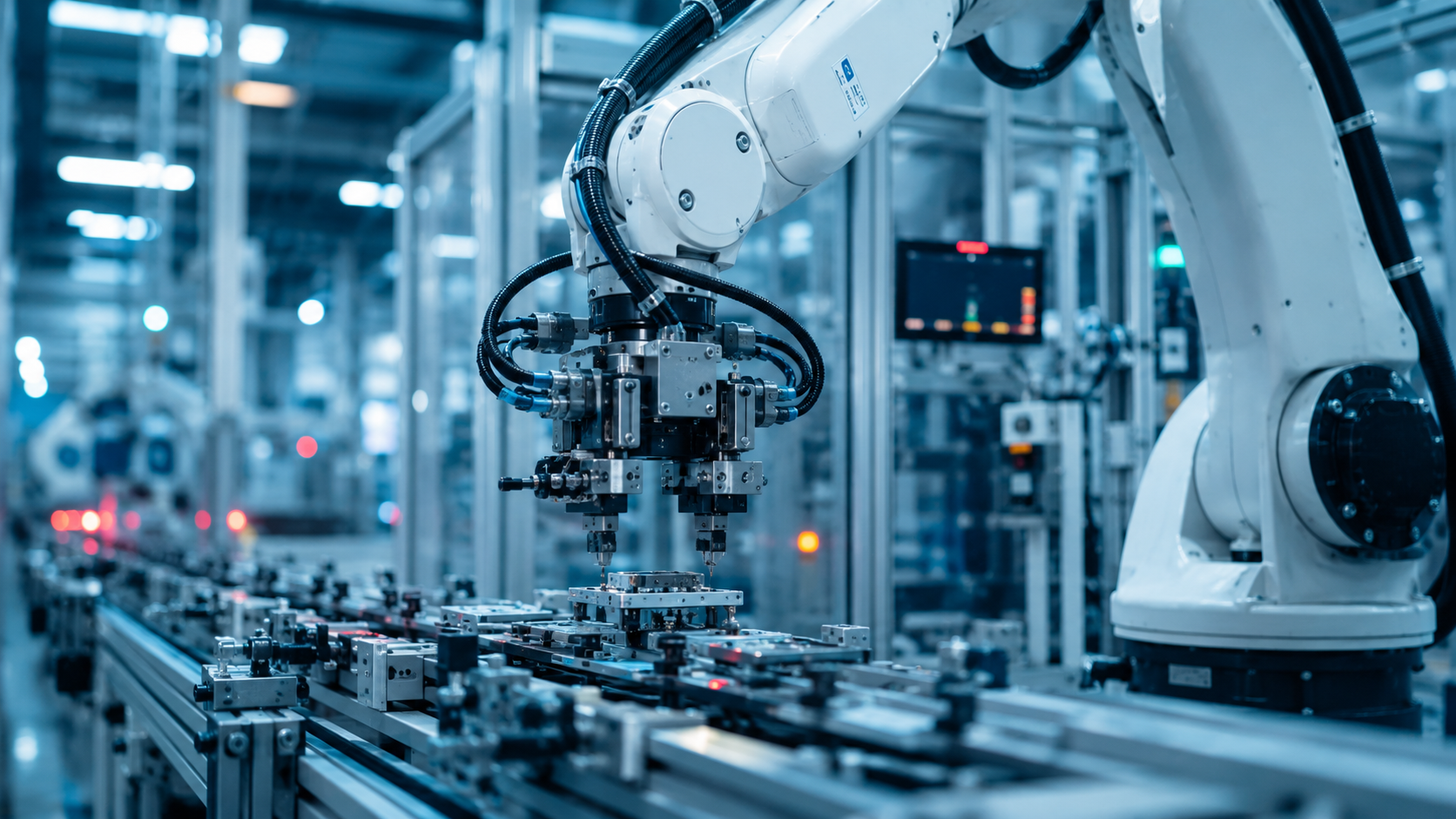

What “Physical AI” Actually Means

The strategic concept driving the deal is what onsemi calls Physical AI — artificial intelligence embedded directly into devices and machines, enabling them to sense their environment, make decisions, act, and adapt in the real world. This is distinct from the data center AI that has dominated headlines. Where data center AI trains and runs large models in centralized facilities, Physical AI lives at the edge: in automobiles, industrial robots, factory equipment, medical devices, and connected consumer products.

onsemi frames the combined company as sitting at the intersection of four pillars: Power, Sense, Connected Compute, and Control. The company has long held strength in the first two — intelligent power management and sensing technologies for automotive and industrial markets. What it lacked was the compute and connectivity layer that turns raw sensor data into intelligent action. That is precisely what Synaptics brings.

What Synaptics Adds

Synaptics contributes four decades of innovation in Edge AI compute, human-machine interface technology, and wireless connectivity solutions. Its portfolio enables the kind of on-device intelligence and interaction that Physical AI requires — touch, display, voice, and connectivity systems that allow machines to interface with both their environment and their users. Combining Synaptics’ edge compute franchise with onsemi’s power and sensing leadership creates a company able to offer integrated solutions across every layer of the Edge AI stack.

The financial logic is anchored in market expansion. onsemi expects the acquisition to increase its total addressable market by $30 billion, bringing it to $243 billion by 2030. That is the size of the opportunity onsemi believes Physical AI represents as intelligence migrates out of the data center and into the billions of devices and machines operating in the physical economy.

Why This Matters Beyond the Two Companies

For investors tracking the broader semiconductor landscape, the onsemi-Synaptics combination carries a signal that extends well past the deal itself. The AI investment narrative has been overwhelmingly concentrated in data center infrastructure — GPUs, memory, networking, and the hyperscaler buildout. This transaction is a high-conviction bet by an established player that the next phase of AI value creation happens at the edge, in the physical world, embedded in real machines.

That thesis has direct implications for smaller companies. As Physical AI demand accelerates, the suppliers of edge sensors, power management components, connectivity modules, embedded compute, and the specialized materials that go into device-level intelligence stand to benefit. Many of those companies operate well below the $2 billion market cap threshold and sit in exactly the part of the supply chain that a Physical AI buildout would pull forward.

The data center AI trade has been the story of the past two years. onsemi just put $7 billion behind the idea that the physical world is next.