Apple (NASDAQ: AAPL) dropped one of the biggest corporate leadership announcements in years on Monday: Tim Cook will step down as CEO on September 1, 2026, transitioning to executive chairman, while John Ternus — currently Senior Vice President of Hardware Engineering — becomes the company’s eighth chief executive. The move was unanimously approved by Apple’s board of directors.

Ternus, 50, is a 25-year Apple veteran who joined the company in 2001 as a product design engineer and rose through the ranks overseeing hardware development for the iPhone, iPad, AirPods, and Mac product lines. His appointment continues Apple’s tradition of internal succession — the same approach used when Cook replaced Steve Jobs in 2011.

The transition is effective September 1, with Cook remaining in his CEO role through the summer to ensure continuity. Arthur Levinson, Apple’s non-executive chairman for the past 15 years, will shift to lead independent director at the same time Ternus joins the board.

For investors, the leadership change raises a question that goes beyond Apple’s $4 trillion market cap: what does a hardware-first CEO mean for the company’s strategic direction — and who benefits downstream?

Cook’s tenure was defined by operational excellence and margin expansion. Under his leadership, Apple’s profit more than quadrupled, and the company became the first to achieve a $1 trillion market cap. But the knock on Cook heading into his final years was the same one analysts have leveled at Apple broadly — a lagging AI strategy relative to peers.

Ternus inherits that problem directly. Apple has faced a bumpy rollout of its AI-enhanced Siri platform and relied on Google’s Gemini in January as a bridge while its own large language model development hit snags. The company is now accelerating development of AI-driven wearables — reportedly including smart glasses, a pendant device, and camera-equipped AirPods — along with a foldable iPhone that some analysts are calling the most significant hardware moment in years. Bloomberg has also reported Apple is eyeing deeper moves into robotics.

That product roadmap matters significantly for the small and microcap companies sitting inside Apple’s supply chain. Shifts in hardware strategy at the CEO level translate directly into procurement decisions, component specifications, and manufacturing volumes that flow through dozens of smaller, publicly traded suppliers. When Apple pivots toward new form factors — AI wearables, foldable displays, edge-computing hardware — it creates winners and losers across a web of suppliers many of which operate well below the $2 billion market cap threshold.

Wall Street’s initial read on the Ternus appointment has been cautiously positive. Morgan Stanley noted that promoting a product-centric engineer signals Apple’s core hardware flywheel will remain intact. Wedbush’s lead tech analyst characterized the move as an opportunity for Apple to shift from a defensive to offensive posture in the AI hardware race.

Whether Ternus can deliver on both sides of that mandate — preserving Cook’s operational discipline while channeling the kind of product innovation the market has been waiting for — will define not just Apple’s next chapter, but the trajectory of an entire ecosystem of smaller companies built around it.

Apple is scheduled to report fiscal second-quarter earnings next week, with Cook still at the helm for that call. Ternus, however, will almost certainly face pointed questions from investors about his vision from day one.

STAFFORD, Texas, April 22, 2026 (GLOBE NEWSWIRE) — Greenwich LifeSciences, Inc. (Nasdaq: GLSI) (the “Company”), a clinical-stage biopharmaceutical company focused on its Phase III clinical trial, FLAMINGO-01, which is evaluating Fast Track designated GLSI-100, an immunotherapy to prevent breast cancer recurrences, today announced that on April 16, 2026, the Company received notification from the Listing Qualifications Department of The Nasdaq Stock Market LLC notifying the Company that, because it has not yet filed its Annual Report on Form 10-K for the fiscal year ended December 31, 2025, the Company is not currently in compliance with Nasdaq Listing Rule 5250(c)(1), which requires timely filing of periodic financial reports with the Securities and Exchange Commission. The notice has no immediate effect on the listing or trading of the Company’s common stock, which continues to trade on the Nasdaq Capital Market under the symbol “GLSI.”

The Company plans to file its Form 10-K for the fiscal year ended December 31, 2025 as soon as possible, working with both of its auditors where each auditor is responsible for their own periods ending in 2024 and 2025.

About Greenwich LifeSciences, Inc.

Greenwich LifeSciences is a clinical-stage biopharmaceutical company focused on the development of GP2, an immunotherapy to prevent breast cancer recurrences in patients who have previously undergone surgery. GP2 is a 9 amino acid transmembrane peptide of the HER2 protein, a cell surface receptor protein that is expressed in a variety of common cancers, including expression in 75% of breast cancers at low (1+), intermediate (2+), and high (3+ or over-expressor) levels. Greenwich LifeSciences has commenced a Phase III clinical trial, FLAMINGO-01. For more information on Greenwich LifeSciences, please visit the Company’s website at www.greenwichlifesciences.com and follow the Company’s Twitter at https://twitter.com/GreenwichLS.

Forward-Looking Statement Disclaimer

Statements in this press release contain “forward-looking statements” that are subject to substantial risks and uncertainties. All statements, other than statements of historical fact, contained in this press release are forward-looking statements. Forward-looking statements contained in this press release may be identified by the use of words such as “anticipate,” “believe,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “seek,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “target,” “aim,” “should,” “will,” “would,” or the negative of these words or other similar expressions, although not all forward-looking statements contain these words. Forward-looking statements are based on Greenwich LifeSciences Inc.’s current expectations and are subject to inherent uncertainties, risks and assumptions that are difficult to predict, including statements regarding the intended use of net proceeds from the public offering; consequently, actual results may differ materially from those expressed or implied by such forward-looking statements. Further, certain forward-looking statements are based on assumptions as to future events that may not prove to be accurate. These and other risks and uncertainties are described more fully in the section entitled “Risk Factors” in Greenwich LifeSciences’ Annual Report on the most recent Form 10-K for the year ended December 31, 2024, and other periodic reports filed with the Securities and Exchange Commission. Forward-looking statements contained in this announcement are made as of this date, and Greenwich LifeSciences, Inc. undertakes no duty to update such information except as required under applicable law.

CHARLOTTE, N.C., April 22, 2026 (GLOBE NEWSWIRE) — NN, Inc. (NASDAQ: NNBR), a global diversified industrial company that engineers and manufactures high-precision components and assemblies, announced today that it will release its first quarter 2026 financial results for the period ended March 31st, 2026, after the close of the market on Wednesday, May 6th, 2026. The Company will hold a related conference call on Thursday, May 7th, 2026, at 9:00 a.m. E.T. Participants on the call are asked to register five to ten minutes prior to the scheduled start time by dialing 800-715-9871 and from outside the U.S. at +1 646-307-1963.

The conference call will be webcast simultaneously and in its entirety through the NN, Inc. Investor Relations website. Shareholders, media representatives and others may participate in the webcast by registering through the Investor Relations section on the company’s website at https://investors.nninc.com/.

For those who are unavailable to listen to the live call, a replay will be available shortly after the call on NN’s website through May 7th, 2027.

About NN, Inc. NN, Inc., a global diversified industrial company, combines advanced engineering and production capabilities with in-depth materials science expertise to design and manufacture high-precision components and assemblies for a variety of markets on a global basis. Headquartered in Charlotte, North Carolina, NN has facilities in North America, Europe, South America, and China. For more information about the Company and its products, please visit www.nninc.com.

Investor Relations: Joe Caminiti or Abe Plimpton [email protected] 312-445-2870

Exits Q1 with 100 Metric Tonnes Per Day Production and Confirms Plan to Achieve 350 Metric Tonnes Per Day by the End of 2026

Kuya Silver to Report Q4/Year End Financial Results Prior to Market Open on Friday, April 24 and Hold a Conference Call Webinar on April 28, 2026 to Update Investors

All references to dollar amounts are references to U.S. Dollars, unless otherwise stated

Toronto, Ontario–(Newsfile Corp. – April 22, 2026) – Kuya Silver Corporation (CSE: KUYA) (OTCQB: KUYAF) (FSE: 6MR1) (the “Company” or “Kuya Silver“) is pleased to report record quarterly production and provide an operational update for the first quarter of 2026 at the Bethania silver project, which delivered record daily and quarterly production rates as the ramp-up continued to track higher during the three month period. In light of the significant progress to date, the Company continues to expect the completion of its Phase 1 ramp-up, achieving 350 metric tonnes per day (“tpd“) production, by the end of the year.

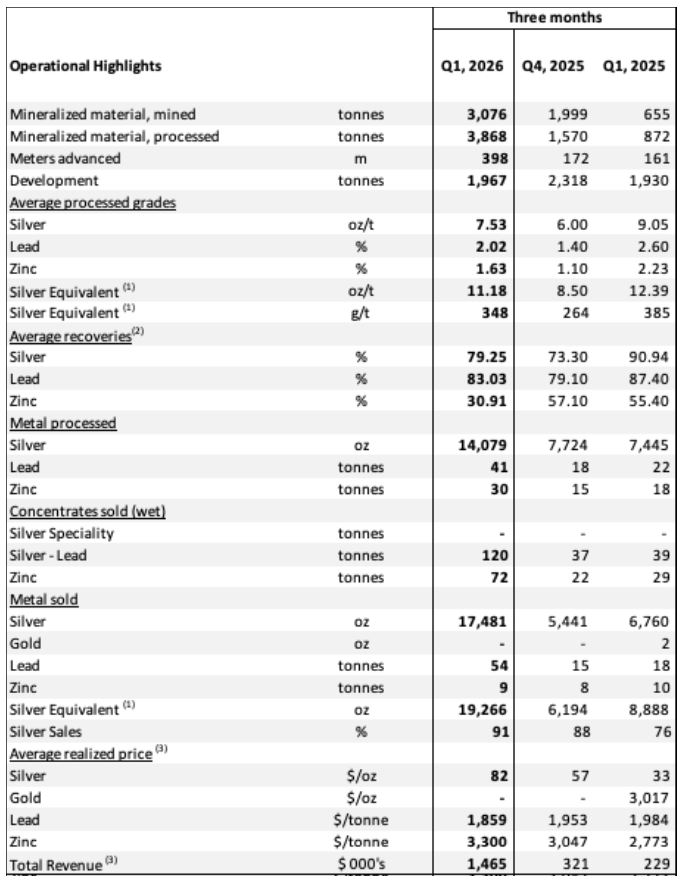

Operational Highlights

3,076 metric tonnes of mineralized material mined at Bethania, a significant improvement over Q4 2025

Milestone 100 tonne per day (tpd) throughput achieved at the end of March and early April, 2026

Continued strong underground development with record 398 meters advanced and 1,967 metric tonnes of development material moved to continue expansion of underground mining operations

91% of record quarterly revenue from Bethania came from silver in the quarter with an average selling price of $82/oz.

Announcement of fully funded letter of intent to acquire the Camila plant to improve silver recoveries and operational control of material processing

Cash position at the end of Q1 2026 of approximately $27 million

Kuya Silver On Track To Achieve 350 tpd Production Rate At Bethania By The End of 2026

Given the successful mine development to date, and strong financial position, Kuya Silver expects to complete its Phase 1 ramp-up at the Bethania silver project by the end of this year. The Company plans to keep the market informed of the progress and will continue to provide details on the production growth on a timely basis.

Christian Aramayo, Kuya Silver’s Chief Operating Officer commented, “Another pivotal quarter for Kuya Silver. We achieved 100 tpd in March and have sustained it into April — a clear proof point in our ramp-up. With continued investment in development, we have direct line-of-sight to completing Phase 1 at 350 tpd by year-end. Beyond that, integrating the Camila Plant gives us full operational control over processing, while our expanded drilling program continues to unlock district-scale upside. Bethania is not just ramping up — it represents a clear growth platform with potential upside from production, exploration, and operational efficiency.”

Mining Operations Continue To Improve In Q1 2026

Production of mineralized material at the Bethania Project totalled 3,076 metric tonnes, another quarterly record as production continues to steadily ramp up. Developing activities focused on driving drifts and a crosscut to access more mineralization material achieving 398 m of development. Importantly, Kuya Silver achieved a 100 tpd production rate at the end of March 2026 and this has been largely sustained in April. Modest increases in daily throughput are expected in Q2 and Q3 of 2026, with a more significant increase anticipated once the new 4.5 m x 4.5 m ramp has been deepened to the 640 level production level by Q4.

Grades improved to 7.53 oz/t during Q1 2026 even as development material — typically lower grade — contributed to throughput. Grades are expected to increase as the mine reaches a steady-state of production later this year and in the meantime grades will reflect a blend of ongoing development and run-of-mine stoping . Silver recoveries improved to 79.2% in Q1 2026 from 73.3% in Q4 2025, due to higher grade being processed during the quarter and a reduction of the lower-grade oxidized material (from historical stockpiles) processed in Q4 2025. Kuya Silver has previously achieved 90+% silver recoveries on specific mineralized batches, reflecting not only higher head grades but also favorable metallurgical composition and tighter moisture controls in the processing circuit. Leveraging that recent experience, the Company has implemented targeted adjustments to the Camila Plant’s operating parameters – including semi real-time monitoring of feed characteristics and moisture levels. Early results in April 2026 are encouraging, and management expects recoveries to continue improving as silver grades increase and operational refinements take full effect.

David Stein, Kuya Silver’s President and CEO remarked, “The first quarter of 2026 marked an important achievement with our ramp-up process, with the mine producing 100 tpd in March and sustaining that rate into April. While there is still significant underground development planned for the remainder of 2026 this new level of production, combined with our strong cash position, significantly improves the Company’s financial flexibility to continue growing silver production and aggressively exploring our now-5,600 ha land package in the Bethania district of Peru.”

Table 1: Production highlights from the Bethania silver mine

(1)prices for silver equivalent calculations use period ending spot prices and are as follows: Mar. 31 2026 silver $74./oz, lead $1,909/tonne, zinc$ 3,230/tonne Dec. 30, 2025 silver $70.13/oz, gold $4,326/oz, lead $2,005/tonne, zinc$ 3,122/tonne Mar. 31, 2025 period; silver $34.46/oz, gold $3122.80/oz, lead $2002/tonne, zinc $2829/tonne, and Dec. 31, 2024 period; silver $28.90/oz, gold $2606.72/oz, lead $1921.50/tonne, zinc $2974/tonne. (2)includes only payable recovery i.e. lead in the silver- lead concentrate and zinc in the zinc concentrate and silver in both concentrates. (3)may include provisional settlements at the end of the period, net of treatment and refining costs.

Camila Plant Acquisition Update

Kuya Silver continues to progress with due diligence and definitive documentation with regards to the Camila Plant acquisition announced on January 27, 2026 and expects to complete the transaction in due course.

Upcoming Conference Call Webinar

Kuya Silver will host a conference call webinar taking place on Tuesday, April 28th at 3 pm ET / 12 pm PT. The Company plans to cover the Q1 2026 production progress and 2025 year end financial reporting. A live Q&A will follow the presentation.

Quality assurance and quality control include two sampling procedures. Underground vein material from stopes are sampled to confirm vein grades and to reconcile against the mine model; and sampling of freshly mined material in stockpiles to determine dilution and the head grade that is sent to the processing plant.

Underground vein sampling was conducted systematically every 4 meters along the galleries. This involved excavating a narrow and continuous channel either parallel to the vein or perpendicular to its orientation. The entire volume of material excavated from the channel was collected as a sample.

Freshly mined material in the stockpiles and concentrate stockpiles were sampled using trenching, a method involving the excavation of narrow trenches perpendicular to the major axis of the pile. Trenches were systematically dug at regular intervals across all depths of the pile. The location of each trench was referenced to a topographic control point and recorded in the sampling log.

All material was carefully collected on plastic sheets, then pulverized at the mine site. The pulverized material was quartered, and one quarter was labeled and secured in vinyl sample bags. The samples were then transported to Dmtri I. Mendelejeff laboratory in Huancayo for processing using fire assay followed by atomic absorption spectroscopy (AAS).

All concentrate assay results are cross-checked against independent analyses conducted by the buyer. Furthermore, sample security protocols include sealed trucks for transporting run-of-mine (ROM) material and concentrate trucks with tamper-proof devices with safety seals, and a documented custody chain overseen by the mine superintendent (Bethania).

National Instrument 43-101 Disclosure

The technical content of this news release has been reviewed and approved by Mr. Kevin J. O’Connell, P.E., Independent Technical Advisor to of Kuya Silver and a Qualified Person as defined by National Instrument 43-101.

About Kuya Silver Corporation

Kuya Silver is a Canadian‐based, growth-oriented mining company with a focus on silver. Kuya Silver operates the Bethania silver mine in Peru, while developing district-scale silver projects in mining-friendly jurisdictions including Peru and Canada.

This news release contains statements that constitute “forward-looking information,” including statements regarding the plans, intentions, beliefs, and current expectations of the Company, its directors, or its officers with respect to the future business activities of the Company. The words “may,” “would,” “could,” “will,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “expect,” “must,” “next,” “propose,” “new,” “potential,” “prospective,” “target,” “future,” “verge,” “favorable,” “implications,” and “ongoing,” and similar expressions, as they relate to the Company or its management, are intended to identify such forward-looking information. Investors are cautioned that statements including forward-looking information are not guarantees of future business activities and involve risks and uncertainties, and that the Company’s future business activities may differ materially from those described in the forward-looking information as a result of various factors, including but not limited to fluctuations in market prices, successes of the operations of the Company, continued availability of capital and financing, and general economic, market, and business conditions. There can be no assurances that such forward-looking information will prove accurate, and therefore, readers are advised to rely on their own evaluation of the risks and uncertainties. The Company does not assume any obligation to update any forward-looking information except as required under the applicable securities laws.

Neither the Canadian Securities Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this release.

During the Course of the Agreement the Prominent European Development Group OTT Heritage Hospitality Expects to Market and Deploy SKYX’s Disruptive Technologies into Hundreds of European Hotels, Buildings and Developments

Throughout the Term of the Agreement Prominent Developer and SKYX Expect to Deploy and Market Hundreds of Thousands of Products into Massive European Hospitality Market

124,000 Hotel Rooms are Projected to Open in Europe in 2026, with Over 250,000 Additional Rooms in the Development Pipeline Industry-Wide

Through Its Platform and Network, OTT Heritage Hospitality Provides Access to a Broad Pipeline of Hospitality Projects Across Europe and Intends to Actively Market and Facilitate the Adoption of SKYX’s Technologies Across a Range of Hotel, Building, and Development Opportunities Leveraging Significant Time and Cost Efficiencies of Up to 90%

SKYX’s Technologies are Expected to Offer Long-Term Recurring Revenue Opportunities Through Monitoring, Subscriptions, and AI Services, in Addition to Product Upgrades, Interchangeability and Platform-Wide Integrations for Future Development

MIAMI, April 22, 2026 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), an award winning highly disruptive advanced and smart home and AI platform technology company with over 100 U.S. and global pending and issued patents and a portfolio of 60 lighting and home décor websites, with a mission to make homes and buildings become advanced-safe-smart instantly as the new standard, today announced that it has entered into an agreement with OTT Heritage Hospitality, a prominent European developer, to deploy and market its technologies across the vast European hotel chains segment and buildings.

This agreement marks a significant step in SKYX’s global expansion strategy as it continues to advance its mission to make hotels, homes, and buildings smarter, safer, and advanced.

Under the agreement, SKYX’s advanced and smart home and building technologies are expected to penetrate the vast European hotel market with over 132,000 hotels with hundreds of thousands of additional rooms in the development pipeline in addition to residential and commercial projects throughout Europe.

During the course of the agreement SKYX and OTT Heritage Hospitality expect to deploy and market SKYX’s disruptive technologies to hundreds of European hotels, buildings and developments with the aim of deploying hundreds of thousands of units across European hotel and real estate developments.

OTT Heritage Hospitality provides its platform and network as well as access to a broad pipeline of hospitality projects across Europe and intends to actively market and facilitate the adoption of SKYX’s technologies across a range of hotel, building, and development opportunities, leveraging the significant time and cost efficiencies of up to 90% provided by SKYX’s technologies.

Jean-François Ott, Founder of OTT Heritage Hospitality, said; “As a long-time developer of hotel and real estate projects, I see a tremendous opportunity in marketing and facilitating the penetration of SKYX’s highly disruptive technologies into hotels and real estate projects across Europe. By leveraging significant time and cost efficiencies of up to 90% for hotel renovations as well as new builds, we can enable properties to become smarter, safer, and more technologically advanced.”

Rani Kohen, Founder and Executive Chairman of SKYX Platforms, said; “This partnership marks a significant step in our global expansion strategy as we continue with our goal and mission to advance hotels, homes, and buildings by making them smarter and safer. We look forward to partnering with such an established European hotel and real estate developer.”

For more information about SKYX click here: www.skyx.com

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://www.skyx.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s ability to achieve positive cash flows; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

NEW ALBANY, Ohio, April 22, 2026 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI) will hold its quarterly conference call on Wednesday, May 6, 2026, at 8:30 a.m. ET, to discuss first quarter 2026 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (833) 461-5787 using conference code 496990489. International participants dial (585) 542-9983 using conference code 496990489. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

About CVG

Commercial Vehicle Group, Inc. and its subsidiaries, is a global provider of systems, assemblies and components to global commercial vehicle markets and electric vehicle markets. We deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Nathan Skown Alpha IR Group [email protected]

Amneal Pharmaceuticals (Nasdaq: AMRX) announced on April 21 that it has entered into a definitive agreement to acquire 100% of Kashiv BioSciences, LLC in a transaction that could exceed $1.1 billion in total value — a strategic bet on one of the most significant inflection points in the pharmaceutical industry in decades.

The deal structure includes $375 million in cash and $375 million in equity payable at closing, plus up to $350 million in potential payments tied to regulatory milestones, royalties, and funding of operations through closing. The Manila Times The transaction is subject to Amneal shareholder approval, regulatory clearance, and customary closing conditions, with an expected close in the second half of 2026. The Manila Times

What Kashiv Brings to the Table

Kashiv isn’t just another acquisition target — it’s a rare asset. Kashiv BioSciences is a vertically integrated biopharmaceutical company among the few U.S.-based firms to both manufacture and receive marketing authorization for multiple biosimilars Business Wire, giving it end-to-end capabilities that most companies in the space simply don’t have. That combination of R&D, clinical, manufacturing, and regulatory infrastructure is precisely what Amneal is paying a premium to absorb.

The combined entity is designed to function as a fully integrated global biosimilars platform — built to scale and launch multiple new biosimilar products each year.

The Market Opportunity Driving This Deal

The timing is deliberate. More than $300 billion in global biologics are expected to lose exclusivity over the next decade, and as biosimilars expand patient access while delivering meaningful savings, adoption is accelerating across physicians, patients, and payers. The Manila Times Amneal is positioning itself ahead of that wave rather than chasing it.

The company highlighted $400 million to $500 million in anticipated financial benefits from the transaction, along with a path to maintain a modest leverage profile. TipRanks That’s not a speculative projection — Kashiv already has commercial biosimilars on the market and a robust pipeline moving through regulatory channels.

Strong Financial Momentum Behind the Move

The acquisition announcement came alongside strong preliminary Q1 2026 results that gave management the confidence to pull the trigger. For the quarter ended March 31, 2026, revenue climbed 4% to $723 million, with net income reaching $78 million and significant margin expansion driven by Specialty segment growth and a higher-value product mix. TipRanks On the strength of those results, Amneal raised its standalone full-year 2026 guidance, positioning the Kashiv acquisition as an accelerator of an already-strengthening growth trajectory. TipRanks

Transaction Oversight and Advisors

The transaction was endorsed by an independent conflicts committee TipRanks, a notable governance detail given the pre-existing commercial relationship between the two companies. J.P. Morgan Securities is serving as financial advisor to Kashiv, with Holland & Knight LLP as legal counsel.

The Bottom Line

This deal is a direct statement about where pharmaceutical value creation is headed. As blockbuster biologics lose patent protection at an accelerating clip, the companies with the infrastructure to develop, manufacture, and commercialize biosimilars at scale will control a growing share of one of healthcare’s most important markets. Amneal is making its move now — and the Kashiv acquisition gives it the fully integrated platform to compete at the highest level.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Model Tweaks. With 1Q26 results to be released next week, we reviewed our assumptions and resulting estimates for the quarter. Titan continues to face inflation and tariff pressure and, more recently, extra pricing pressure from OEMs facing their own end market challenges. In addition, after speaking with management, we were too low on our tax assumption. Given the above, we lowered our earnings expectations, although we are maintaining our revenue and adjusted EBITDA projections.

Details. Revenue for 1Q26 is estimated at $495 million, consistent with our prior expectation. Adjusted EBITDA is $21.5 million, also consistent with our prior projections. We did lower our gross profit assumption to 13.9% from 14.9% and increased our tax expense assumption from $2.5 million to $5 million. As a result of the changes, our projected EPS goes from $0.09/sh to a loss of $0.02 per share.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 3 FLAMINGO-01 Data Presented. Greenwich LifeSciences and the FLAMINGO-01 Steering Committee made two presentations at the American Association of Cancer Research (AACR) 2026 Meeting. One detailed the FLAMINGO-01 trial design while the other presented preliminary results from delayed-type hypersensitivity (DTH) response data showing a statistically significant immune response.

First Poster Presentation Included DTH Data. As discussed in our Research Note on March 18, the company announced a preliminary analysis of recurrence rates in the non-HLA-A*02 arm. Immune responses to GP2 were measured using Delayed-Type Hypersensitivity (DTH) skin tests at baseline, then after 4 or 6 months. This open-label arm of the trial has enrolled about 250 patients, with data reported for 191 patients who completed the six-monthly doses of GLSI-100 at four-month or six-month evaluation points.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, April 21, 2026 /PRNewswire/ — Travelzoo® (NASDAQ: TZOO):

WHAT:

Travelzoo, the club for travel enthusiasts, will host a conference call to discuss the Company’s financial results for the first quarter ended March 31, 2026. Travelzoo will issue a press release reporting its results before the market opens on April 23, 2026.

WHEN:

April 23, 2026 at 11:00 AM ET

HOW:

A live webcast of Travelzoo’s Q1 2026 earnings conference call can be accessed at http://ir.travelzoo.com/events-presentations. The webcast will be archived within 2 hours of the end of the call and will be available through the same link.

AboutTravelzoo We, Travelzoo®, are the club for travel enthusiasts. We reach 30 million travelers. Club Members receive Club Offers negotiated and rigorously vetted by our deal experts around the globe. Our relationships with thousands of top travel companies give us access to irresistible deals. Our club and its benefits are built around the lifestyle of a modern travel enthusiast.

SAN DIEGO, April 21, 2026 (GLOBE NEWSWIRE) — Cardiff Oncology, Inc. (Nasdaq: CRDF), a clinical-stage biotechnology company leveraging PLK1 inhibition to develop novel cancer therapies, today announced it will present updated data from CRDF-004, a randomized dose-finding Phase 2 clinical trial evaluating onvansertib in combination with standard of care (SoC) regimens (FOLFIRI/bevacizumab (bev) or FOLFOX/bev) in patients with first-line RAS-mutated metastatic colorectal cancer (mCRC). The data will be reviewed in a rapid oral presentation at the 2026 American Society of Clinical Oncology (ASCO) Annual Meeting, taking place May 29–June 2 in Chicago.

Rapid Oral Presentation Details:

Abstract Title: Onvansertib plus standard-of-care chemotherapy plus bevacizumab in first-line RAS-mutated metastatic colorectal cancer (mCRC): Interim results from the phase 2 randomized CRDF-004 trial Abstract Number: 3510 Session Title: Gastrointestinal Cancer—Colorectal and Anal Session Date and Time: June 2, 2026, 8:00-9:30 AM CDT

The abstract will be publicly available on Thursday, May 21, 2026 on ASCO’s website, and the presentation will be made available on the Scientific Publications page of the Company’s website following its presentation.

About Onvansertib Onvansertib is a highly specific, oral PLK1 inhibitor currently in mid-stage clinical development for RAS-mutated metastatic colorectal cancer. It is also being evaluated in multiple other cancers through investigator-initiated studies, including metastatic pancreatic ductal adenocarcinoma (mPDAC), small cell lung cancer (SCLC), triple-negative breast cancer (TNBC), and chronic myelomonocytic leukemia (CMML).

About Cardiff Oncology, Inc. Cardiff Oncology is a clinical-stage biotechnology company advancing innovative cancer treatments focused on PLK1 inhibition, a validated oncology target with practice-changing potential. Our lead asset, onvansertib, is a highly specific, oral PLK1 inhibitor currently being evaluated in a Phase 2 trial for first-line treatment of RAS-mutated metastatic colorectal cancer (mCRC), addressing a large, underserved patient population with high unmet need. Onvansertib is also under investigation in other PLK1-driven cancers through ongoing investigator-initiated trials and has shown robust single agent clinical activity in hard-to-treat tumors. By targeting tumor vulnerabilities, we aim to overcome treatment resistance and deliver improved clinical outcomes for patients.

Forward-Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified using words such as “anticipate,” “believe,” “forecast,” “estimated” and “intend” or other similar terms or expressions that concern Cardiff Oncology’s expectations, strategy, plans or intentions. These forward-looking statements are based on Cardiff Oncology’s current expectations and actual results could differ materially. There are several factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, clinical trials involve a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results; our clinical trials may be suspended or discontinued due to unexpected side effects or other safety risks that could preclude approval of our product candidate; results of preclinical studies or clinical trials for our product candidate could be unfavorable or delayed; our need for additional financing; risks related to business interruptions, including the outbreak of COVID-19 coronavirus and cyber-attacks on our information technology infrastructure, which could seriously harm our financial condition and increase our costs and expenses; uncertainties of government or third party payer reimbursement; dependence on key personnel; limited experience in marketing and sales; substantial competition; uncertainties of patent protection and litigation; dependence upon third parties; and risks related to failure to obtain FDA clearances or approvals and noncompliance with FDA regulations. There are no guarantees that our product candidate will be utilized or prove to be commercially successful. Additionally, there are no guarantees that future clinical trials will be completed or successful or that our product candidate will receive regulatory approval for any indication or prove to be commercially successful. Investors should read the risk factors set forth in Cardiff Oncology’s Form 10-K for the year ended December 31, 2025, and other periodic reports filed with the Securities and Exchange Commission. While the list of factors presented here is considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements. Forward-looking statements included herein are made as of the date hereof, and Cardiff Oncology does not undertake any obligation to update publicly such statements to reflect subsequent events or circumstances.

New, Leading Technology Engine Configuration of Firejet is First-to-Market Tactical Jet UAS in the High-Performance, Affordable sub-$500,000 Class

SAN DIEGO, April 21, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, today announces that it has completed the initial flight series of the Kratos J85 engine version of the Firejet unmanned aerial system (UAS), dubbed Mk1 Firejet. This second major configuration of the Firejet enables users/customers to select the model that best suits their operational requirements. With the new J85 engine configuration, the Firejet takes a major step forward in the aero-performance category for customers who need the extra performance.

Classic Firejet, the baseline Firejet target system, supports key missions for the U.S. Army Target Systems Management Office (TSMO) at a high level of aerodynamic performance. Flying since the early 2010s with JetCat engines, Classic Firejet has evolved and been adapted to meet the customer performance and threat representation requirements over time. In addition to the U.S. Army operating the Classic Firejet, ally countries around the world operate the Classic Firejet, most recently including Taiwan, which has selected the Tactical Firejet named Mighty Hornet IV for their configuration.

With the new Kratos Spartan engine production facility established in late 2025, production is ramping up for the J85 and other Spartan engine models. Production rates are expected to be in the thousands by later this year and tens of thousands over the next few years meeting the demand for recapitalization which is becoming even more important this year with depletion of U.S. and ally inventories.

Steve Fendley, President of Kratos Unmanned Systems, said, “Kratos is committed to developing and providing threat-representative target aircraft systems and to offering survivable tactical UAS. With this new version of the Firejet in both target or tactical applications, we increase range, endurance, speed, and climb rate without penalizing survivability. Importantly, we also reduce supply chain risk by using an American-made Kratos engine with engine components sourced in the U.S.A. With the two Firejet models, Mk1 and Classic Firejet, we can now meet the cost-performance levels aligned with various customers’ needs.”

Eric DeMarco, President and CEO of Kratos, said, “With our rapid advancement and in production, military-grade jet engines, Kratos is making internal investments to answer the Department of War’s call to industry to deliver affordable, high performance, military capability today. Kratos has invested significant internal resources and together with Army TSMO, have integrated a leading technology engine with the Firejet jet drone system. In addition to the increased performance as a target, this engine configuration of Firejet is first-to-market as a CCA type, tactical jet UAS, in the high-performance, sub-$500,000 arena; another example where affordability is a technology.”

At the high-performance end of the low-cost or affordable jet aerial target market, Kratos’ Firejet delivers unmatched fighter-like performance and versatility, representing the most lethal threats of the United States and its allies’ potential adversaries. Kratos’ Firejet provides the opportunity for customers to train their military personnel and to test multiple weapon systems with a single flexible and affordable high performance unmanned aerial target drone system. The Firejet supports both surface-to-air and air-to-air engagements with a combination of internal and external mission kits including tow targets, proximity scoring, passive & active RF augmentation, and infrared (IR) augmentation.

Additionally, the Tactical Firejet, a variant of the baseline Firejet developed in response to recent years’ world events and configured to enable and perform key tactical drone operations, rather than use for target missions, maintains key Kratos platform features, including high subsonic speed, high-g maneuverability, optimized performance-per-cost class, and sensor/weapons capability.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 28, 2025, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

OVERLAND PARK, Kan.–(BUSINESS WIRE)– SelectQuote, Inc. (NYSE: SLQT), a leading distributor of Medicare insurance policies and owner of a rapidly growing healthcare services platform, today announced it will release its fiscal third quarter 2026 financial results before market open on Tuesday, May 5, 2026. Chief Executive Officer, Tim Danker, and Chief Financial Officer, Ryan Clement, will host a conference call on the day of the release (May 5, 2026) at 8:30 am ET to discuss the results.

For those interested in dialing into the conference call, please register using this link. After registering, confirmation will be sent via email, including dial in details and unique conference call codes for entry. Registration is open through the live call, but to ensure you are connected for the full call, we suggest registering a day in advance or at least 10 minutes before the start of the call.

About SelectQuote:

Founded in 1985, SelectQuote (NYSE: SLQT) pioneered the model of providing unbiased comparisons from multiple, highly rated insurance companies, allowing consumers to choose the policy and terms that best meet their unique needs. Two foundational pillars underpin SelectQuote’s success: a strong force of highly trained and skilled agents who provide a consultative needs analysis for every consumer, and proprietary technology that sources and routes high-quality leads. Today, the Company operates an ecosystem offering high touchpoints for consumers across insurance, pharmacy, and virtual care.

With an ecosystem offering engagement points for consumers across insurance, Medicare, pharmacy, and value-based care, the company now has three core business lines: SelectQuote Senior, SelectQuote Healthcare Services, and SelectQuote Life. SelectQuote Senior serves the needs of a demographic that sees around 10,000 people turn 65 each day with a range of Medicare Advantage and Medicare Supplement plans. SelectQuote Healthcare Services is comprised of the SelectRx Pharmacy, a Patient-Centered Pharmacy Home™ (PCPH) accredited pharmacy, SelectPatient Management, a provider of chronic care management services, and Healthcare Select, which proactively connects consumers with a wide breadth of healthcare services supporting their needs.

{kind=link}