Research News and Market Data on FRSPF

May 04, 2026 7:11 AM EDT | Source: First Phosphate Corp.

Saguenay, Québec–(Newsfile Corp. – May 4, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the receipt of $3,070,549 in gross proceeds upon the exercise of 2,456,439 warrants prior to their expiry on April 24, 2026 and April 30, 2026, at an exercise price of $1.25 per share.

The Company now has 179,947,950 common shares, 2,625,000 warrants, 7,650,000 options and 1,975,000 restricted share units outstanding. All warrants, options and restricted share units outstanding are held by current Company staff, management and board members.

The Company remains debt-free and is on an accelerated development timeline thanks to a recent non-repayable, non-dilutive contribution of $16.7 million received from the Federal Government of Canada.

Since June 2022, the Company has raised approximately $62.5 million in 10 management-led non-brokered private-placement financings and from funds received from option and warrant exercise.

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

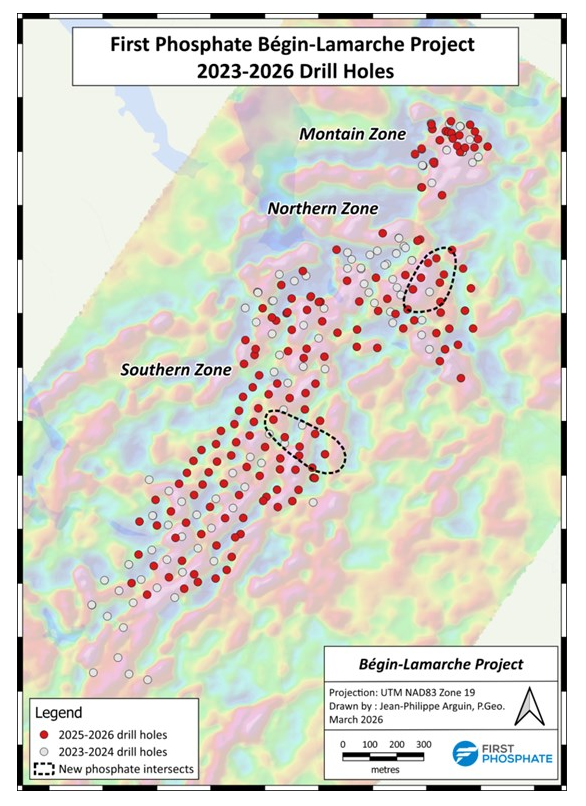

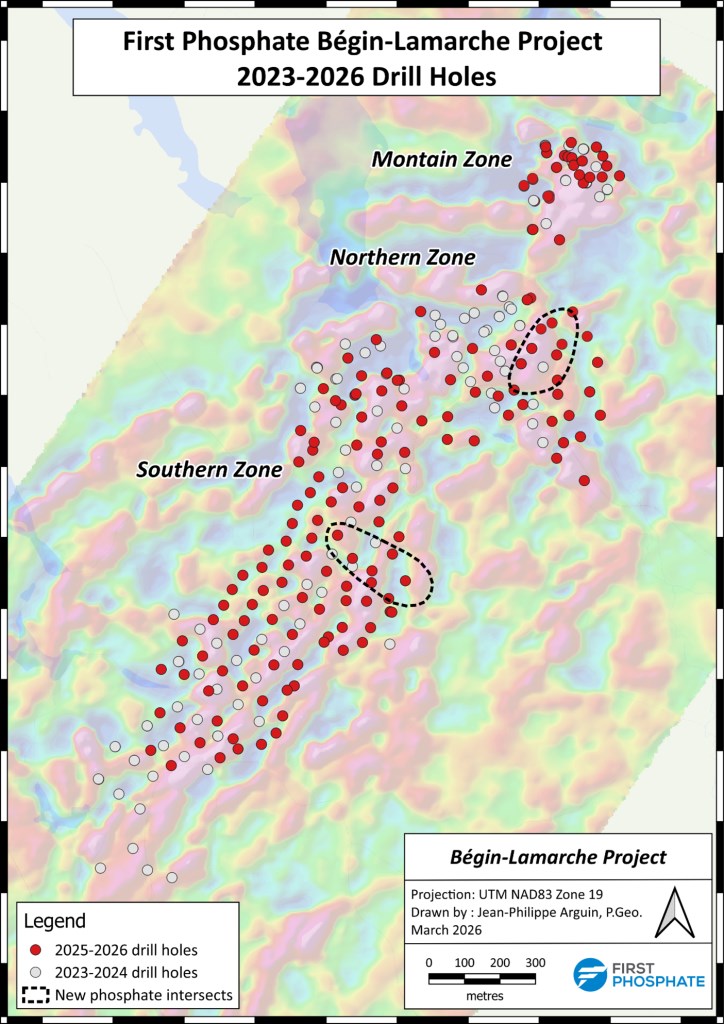

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay–Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

For additional information, please contact:

Bennett Kurtz

CFO, CAO

[email protected]

Tel : +1 (416) 200-0657

Investor Relations: [email protected]

Media Relations: [email protected]

Website: www.FirstPhosphate.com

Follow First Phosphate:

X : https://x.com/FirstPhosphate

LinkedIn : https://www.linkedin.com/company/first-phosphate

Forward-Looking Information and Cautionary Statement

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, this press release contains forward-looking information relating to, among other things: the timeframe for the development of the Company’s planned exploration and production activities; and the Company’s plans for vertical integration into North American supply chains. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things: that engineering and construction timetables and capital costs for the Company’s, exploration, development and expansion projects are correctly estimated and not affected by unforeseen circumstances; the ability to obtain financing for its proposed operations on acceptable terms; no material deterioration in general business and economic conditions; no material delays in obtaining permits and other approvals; no significant disruptions affecting the activities of the Company or its ability to access required project equipment and services, and operating supplies in sufficient quantities and on a timely basis; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the ability to complete the exploration and development programs consistent with the Company’s expectations; commodity price expectations including assumptions for P205; the Company’s relationship with local municipalities and First Nations remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

Source: First Phosphate Corp.

{kind=link}

{kind=link}

{kind=link}

{kind=link}