RESTON, Va., April 20, 2026 /PRNewswire/ — V2X, Inc., (NYSE: VVX), a leading provider of global mission solutions, will report first quarter 2026 financial results on Monday, May 4, 2026, after market close. Senior management will conduct a conference call at 4:30 p.m. ET that same day.

U.S.-based participants may dial in to the conference call at 877-300-8521, while international participants may dial 412-317-6026. A live webcast of the conference call as well as an accompanying slide presentation will be available at https://app.webinar.net/Q291YZzYJpN and on the Investors section of the V2X website at https://gov2x.com/.

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through May 18, 2026, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10208314.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations [email protected] 719-637-5773

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Shareholders approve CEO option grant. Travelzoo shareholders approved a 600,000-share non-qualified stock option grant to CEO Holger Bartel, formalizing a performance-based compensation structure tied directly to stock price appreciation and marking a clear inflection point in management incentives. The grant represents a significant 5.5% of the current total shares outstanding.

Structure emphasizes near-term performance and meaningful upside. The options carry a $5.05 exercise price, vest semi-annually over two years, and have a five-year term, creating a relatively short execution window in which management must deliver results to realize value.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

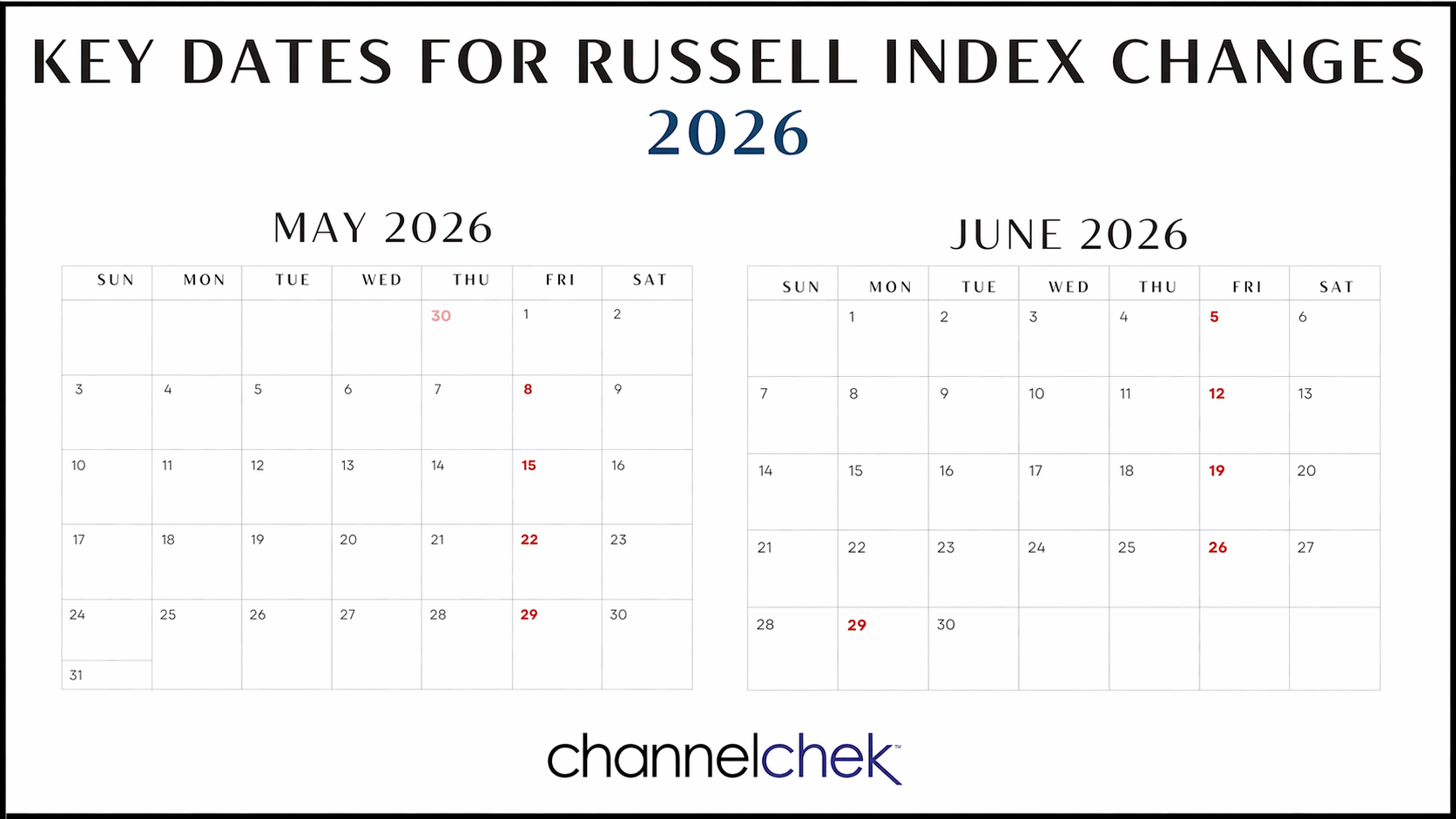

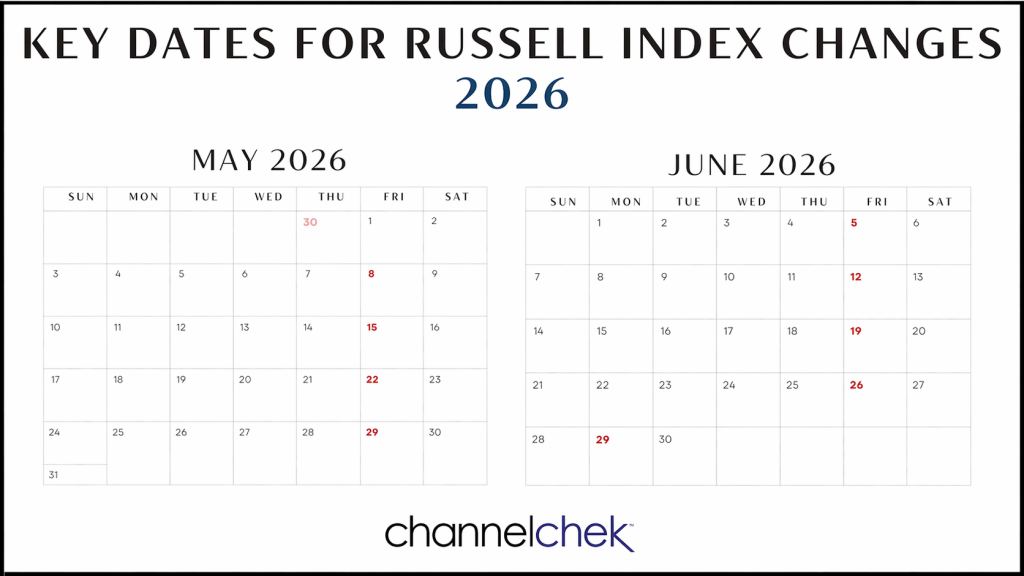

The Annual Russell Index Revision and Dates to Watch (2026)

The yearly process of recasting the Russell Indexes begins on Thursday, April 30 and will be complete by market opening on June 29. During the period in between, FTSE Russell will rank stocks for additions, for deletions and evaluate the companies to make sure they conform overall. The methodology for inserting and removing tickers in the Russell 3000, Russell 2000, and Russell 1000 is intentionally transparent to help eliminate price shocks. Price movements do of course occur along the way, and investors try to foresee and capitalize on them. Channelchek will be providing updates that may uncover opportunities, or at least provide an understanding of stock price swings during this period.

Background

Russell index products are widely used by institutional and retail investors throughout the world. There is more than $20.1 trillion currently benchmarked to a Russell index. This includes approximately $12.1 trillion benchmarked to the Russell US Equity indexes. The trading volume of some companies moving into an index will heighten around the last Friday in June as fund managers seek to maintain level tracking with their benchmark target.

Opportunity

For non-passive investing, determining which stocks may benefit from moving up to a large-cap index, down to a smaller one, or into or out of the measurements is an annual event causing volatility around stocks. There has, of course, the potential for very profitable long and short trades. And the potential for an unwitting investor to be holding a company moving out of an index, which could cause less interest in the stock, and perhaps unfortunate performance.

Active investors should make themselves aware of the forces at play so they may either get out of the way or determine if they should become involved by taking positions with those being added or those at the end of their reign within one of the Russell measurements.

Dramatic Valuation Shifts

The leading industries and altered market-cap of companies of a year ago have changed dramatically from last year’s reconstitution. This will be reflected in the 2026 rebalancing and is going to impact a much larger number of companies than most years. That is to say, a higher percentage of companies than normal will move in, out, or to another index, and may be subject to amplified price movement.

The 2026 Russell Reconstitution Schedule:

• Thursday, April 30th – “Rank Day” – Index membership eligibility for 2026 Russell Reconstitution determined from constituent market capitalization at market close.

• Friday, May 22nd – Preliminary index additions & deletions membership lists posted to the FTSE Russell website after 6 PM US eastern time.

• Friday, May 29th, June 5th, June 12th and Thursday June18th – Preliminary membership lists (reflecting any updates) posted to the FTSE Russell website after 6 PM US eastern time.

• Monday, June 8th – “Lock-down” period begins with the updates to reconstitution membership considered to be final.

• Friday, June 26th – Russell Reconstitution is final after the close of the US equity markets.

• Monday, June 29th – Equity markets open with the newly reconstituted Russell US Indexes.

Take-Away

The annual reconstitution is a significant driver of dramatic shifts in some stock prices as portfolio managers have their holding needs shifted within a very short period of time. Longer-term demand for certain equities is altered as well. Sizable price movements and volatility are expected, especially around the last week in June. In fact, the opening day of the reconstitution is typically one of the highest trading-volume days of the year in the US equity markets.

The market event impacts more than $9 trillion of investor assets benchmarked to or invested in products based on the Russell US Indexes. Portfolio managers that are required to track one of these indexes will work to have minimal portfolio slippage away from their benchmark. The days and weeks from April 30th through the last Friday in June can create opportunities for investors seeking to benefit from price moves, Channelchek will be covering the event as stocks to be added to, or removed from this year’s Russell Reconstitution and other information plays out.

Eli Lilly is writing another large check in its aggressive diversification push, this time targeting one of oncology’s most promising frontiers. The pharmaceutical giant announced Monday it has agreed to acquire Kelonia Therapeutics in a deal valued at up to $7 billion — $3.25 billion upfront with the remainder tied to clinical, regulatory, and commercial milestones. The transaction is expected to close in the second half of 2026.

The strategic rationale centers on Kelonia’s proprietary in vivo CAR-T technology — a next-generation approach to cancer immunotherapy that sets itself apart from everything currently on the market. Traditional CAR-T treatments require physicians to extract a patient’s T-cells, engineer them in a laboratory setting outside the body, then reinfuse them — a complex, time-consuming process requiring chemotherapy preconditioning and specialized academic medical centers capable of managing the procedure. Kelonia’s platform eliminates all of that. The therapy is delivered intravenously in a single infusion, reprogramming T-cells to attack cancer directly inside the body, with no preconditioning required.

The commercial implications are significant. The existing ex-vivo CAR-T market is already producing blockbuster revenue — Johnson & Johnson’s Carvykti generated nearly $1.9 billion in sales last year for multiple myeloma alone. Gilead recently paid $7.8 billion to acquire Arcellx and its competing asset. A one-time, broadly accessible in vivo alternative that sidesteps the logistical barriers of ex-vivo therapy could expand the addressable patient population dramatically and reach community oncology settings currently unable to administer existing treatments.

For Lilly, this deal is part of a deliberate strategy to reduce its dependence on GLP-1 drugs for obesity and diabetes — the products that have defined the company’s recent run. Management has been explicit: the goal is to deploy the cash flow generated by its weight-loss franchise into therapeutic diversification. Recent deals include Centessa Pharmaceuticals for sleep disorder drugs and Orna Therapeutics for cell therapy. Kelonia extends that footprint into hematology and potentially solid tumors.

What makes this acquisition particularly noteworthy for investors watching the oncology space is what it signals downstream. Lilly’s willingness to spend $3.25 billion upfront on a platform still in early clinical stages — while acknowledging that many early-stage bets will fail — reflects a maturing view of how large pharma is valuing novel modalities. Smaller biotech companies developing differentiated delivery mechanisms, novel immune engineering platforms, or next-generation cell therapies should expect intensifying M&A interest from strategic acquirers flush with capital.

The Kelonia deal also raises the stakes for any company developing competing in vivo CAR-T or similar tumor-targeting platforms. With Lilly now in the race alongside J&J and Gilead, the race to make cancer immunotherapy more accessible — and more scalable — is entering a new, better-funded chapter. For small and microcap biotech names working in adjacent spaces, that’s both a competitive threat and a significant validation of the underlying science.

ST. PETERSBURG, Fla., April 20, 2026 (GLOBE NEWSWIRE) — Superior Group of Companies, Inc. (NASDAQ: SGC) (the “Company”) today announced that it will release the results of its operations for the first quarter 2026 before the market open on Monday, May 4, 2026. Michael Benstock, Chairman and Chief Executive Officer, and Mike Koempel, President and Chief Financial Officer, will host a teleconference at 8:00 am Eastern Time that day to discuss the Company’s results.

The live webcast and archived replay can be accessed in the investor relations section of the Company’s website at https://ir.superiorgroupofcompanies.com/presentations. Interested individuals may also join the teleconference by dialing 1-844-861-5505 for U.S. dialers and 1-412-317-6586 for international dialers. The Canadian toll-free number is 1-866-605-3852. Please ask to join the Superior Group of Companies call.

A telephone replay of the teleconference will be available through May 11, 2026. To access the replay, dial 1-855-669-9658 in the United States and Canada or 1-412-317-0088 from international locations. Please reference conference number 4789430 for replay access.

About Superior Group of Companies, Inc. (SGC): Established in 1920, Superior Group of Companies is comprised of three attractive business segments each serving large, fragmented and growing addressable markets. Across Healthcare Apparel, Branded Products and Contact Centers, each segment enables businesses to create extraordinary brand engagement experiences for their customers and employees. SGC’s commitment to service, quality, advanced technology, and omnichannel commerce provides unparalleled competitive advantages. We are committed to enhancing shareholder value by continuing to pursue a combination of organic growth and strategic acquisitions. For more information, visit www.superiorgroupofcompanies.com.

CHICAGO, April 20, 2026 (GLOBE NEWSWIRE) — FreightCar America, Inc. (NASDAQ: RAIL), a diversified manufacturer of railroad freight cars, today announced that it will release its first quarter 2026 financial results on Monday, May 4, 2026, after the market close, and host a teleconference to discuss its first quarter 2026 results on the following day. Teleconference details are as follows:

Please note that the webcast is listen-only and webcast participants will not be able to participate in the question and answer portion of the conference call. Interested parties are asked to dial in approximately 10 to 15 minutes prior to the start time of the call.

An audio replay of the conference call will be available beginning at 3:00 p.m. (Eastern Time) on Tuesday, May 5, 2026, until 11:59 p.m. (Eastern Time) on Tuesday, May 19, 2026. To access the replay, please dial (844) 512-2921 or (412) 317-6671. The replay passcode is 13760024. An archived version of the webcast will also be available on the FreightCar America Investor Relations website.

About FreightCar America

FreightCar America, headquartered in Chicago, Illinois, is a leading designer, producer and supplier of railroad freight cars, railcar parts and components. We also specialize in railcar repairs, complete railcar rebody services and railcar conversions that repurpose idled rail assets back into revenue service. Since 1901, our customers have trusted us to build quality railcars that are critical to economic growth and instrumental to the North American supply chain. To learn more about FreightCar America, visit www.freightcaramerica.com.

Two of the most dominant component suppliers in the recreational vehicle and outdoor enthusiast markets may be on the verge of combining. Patrick Industries (NASDAQ: PATK) and LCI Industries (NYSE: LCII) — both headquartered in Elkhart, Indiana — confirmed on April 17 that they are in active discussions regarding a potential merger of equals. Bloomberg first reported the deal would be structured as an all-stock transaction.

The announcement, delivered via separate press releases after Friday’s market close, sent LCI’s trading volume to nearly 3.8 times its 20-day average — a clear signal that the market is treating this as a high-conviction event.

The strategic logic is straightforward. Patrick Industries, founded in 1959, manufactures and distributes component products for the RV, marine, powersports, and housing markets. The company operates more than 190 facilities across a portfolio of over 85 brands and employs more than 10,000 people. LCI Industries, through its Lippert Components subsidiary, is a global leader in engineered components for outdoor recreation and transportation markets, with over 140 manufacturing and distribution facilities across North America, Africa, and Europe.

These are not two fringe players. Together, they supply a substantial portion of the infrastructure that goes into RVs, marine vessels, and powersports units built across North America. A combined entity would carry significant scale advantages — from raw material procurement and logistics to technology investment and aftermarket distribution. As of April 17, Patrick carried a market cap of approximately $3.54 billion and LCI sat at roughly $3 billion. A successful all-stock merger would create an outdoor recreation supply chain player worth approximately $6.5 billion.

The timing is deliberate. The RV industry has been navigating a post-pandemic normalization cycle, with unit shipments softening from their 2021 highs. Consolidation at the supplier tier is a rational response — two companies with overlapping market footprints, shared OEM customers, and comparable operational infrastructure have more to gain together than competing independently. The potential synergies are tangible: combined purchasing power, reduced overhead duplication across facilities, stronger pricing leverage with customers, and a platform large enough to accelerate investment in connected vehicle and smart RV technology.

Historically, LCI has grown through bolt-on acquisitions of product lines and smaller businesses. A merger of equals with Patrick would represent a significant departure from that playbook — a transformational combination rather than incremental expansion. For Patrick, it would provide immediate global distribution reach through Lippert’s international footprint, something the company would otherwise take years to build organically.

There are still material unknowns. No definitive agreement has been signed. Both companies stated they will not comment further until a formal deal is announced or discussions are terminated. Regulatory review of a transaction this size would also be expected, given the combined company’s market share across several RV and marine component categories.

For investors in small and mid-cap industrials, this is a developing story with real consequences for the outdoor recreation supply chain. If Patrick and LCI formalize this combination, it would stand as one of the more significant sector realignments of 2026 — and a signal that the Elkhart manufacturing corridor is entering a new phase of consolidation.

No assurance of a transaction has been given. Watch for an 8-K filing or formal press release for the next material development.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a leading artificial intelligence (“AI”) company offering AI and augmented reality (“AR”) powered solutions to beauty, fashion, photo and video creative industries, today announced that the independent special committee (the “Special Committee”) of the Company’s board of directors (the “Board”), formed to evaluate and consider the previously announced preliminary non-binding proposal letter dated March 18, 2026 (the “Proposal”), has selected Kroll LLC. as its financial advisor and DLA Piper as its international legal counsel.

The Special Committee is continuing its review and evaluation of the Proposal. The Board cautions its shareholders and others considering trading in its securities that neither the Board nor the Special Committee has made any decision with respect to the Proposal. There can be no assurance that any definitive offer will be received, that any definitive agreement will be executed relating to the transaction contemplated by the Proposal, or that the transaction contemplated by the Proposal or any other similar transaction will be approved or consummated. The Company does not undertake any obligation to provide any updates with respect to any transaction, except as required under applicable law.

About Perfect Corp.

Founded in 2015, Perfect Corp. is a leading AI company offering self-developed AI- and AR- powered solutions dedicated to transforming the world with digital tech innovations that make your virtual world beautiful. On Perfect’s direct consumer business side, Perfect operates a family of YouCam consumer apps and web-editing services for photo, video and camera users, centered on unleashing creativity with AI-driven features for creation, beautification and enhancement. On Perfect’s enterprise business side, Perfect empowers major beauty, skincare, fashion, jewelry, and watch brands and retailers by supplying them with omnichannel shopping experiences through AR product try-ons and AI-powered skin diagnostics. With cutting-edge technologies such as Generative AI, real-time facial and hand 3D AR rendering and cloud solutions, Perfect enables personalized, enjoyable, and engaging shopping journey and helps brands elevate customer engagement, increase conversion rates, and propel sales growth. Throughout this journey, Perfect maintains its unwavering commitment to environmental sustainability and fulfilling social responsibilities. For more information, visit https://ir.perfectcorp.com/.

Forward-Looking Statements

This communication contains forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act, that are based on beliefs and assumptions and on information currently available to Perfect. In some cases, you can identify forward-looking statements by the following words: “may,” “will,” “could,” “would,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” “target,” “seek” or the negative or plural of these words, or other similar expressions that are predictions or indicate future events or prospects, although not all forward-looking statements contain these words. Any statements that refer to expectations, projections or other characterizations of future events or circumstances, including strategies or plans, are also forward-looking statements. These statements involve risks, uncertainties and other factors that may cause actual results, levels of activity, performance or achievements to be materially different from those expressed or implied by these forward-looking statements. These statements are based on Perfect’s reasonable expectations and beliefs concerning future events and involve risks and uncertainties that may cause actual results to differ materially from current expectations. These factors are difficult to predict accurately and may be beyond Perfect’s control. Forward-looking statements in this communication or elsewhere speak only as of the date made. New uncertainties and risks arise from time to time, and it is impossible for Perfect to predict these events or how they may affect Perfect. In addition, risks and uncertainties are described in Perfect’s filings with the Securities and Exchange Commission. These filings may identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. Perfect cannot assure you that the forward-looking statements in this communication will prove to be accurate. There may be additional risks that Perfect presently does not know or that Perfect currently does not believe are immaterial that could also cause actual results to differ from those contained in the forward looking statements. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by Perfect, its directors, officers or employees or any other person that Perfect will achieve its objectives and plans in any specified time frame, or at all. Except as required by applicable law, Perfect does not have any duty to, and does not intend to, update or revise the forward-looking statements in this communication or elsewhere after the date of this communication. You should, therefore, not rely on these forward-looking statements as representing the views of Perfect as of any date subsequent to the date of this communication.

STAFFORD, Texas, April 20, 2026 (GLOBE NEWSWIRE) — Greenwich LifeSciences, Inc. (Nasdaq: GLSI) (the “Company”), a clinical-stage biopharmaceutical company focused on its Phase III clinical trial, FLAMINGO-01, which is evaluating Fast Track designated GLSI-100, an immunotherapy to prevent breast cancer recurrences, today presents the published abstract and poster from the AACR Meeting 2026.

The abstract is shown below and the poster being presented today can be seen and downloaded at the bottom of Phase III clinical trial tab on the Company’s website here.

This is the first abstract and poster presented jointly with the Steering Committee of FLAMINGO-01 with statistically significant delayed-type-hypersensitivity (DTH) immune response data, with subgroup analysis by the most prevalent HLA types.

In the non-HLA-A*02 open label arm where all patients (n=247) were treated with GLSI-100, immune responses to GP2 were measured at baseline and over time using skin tests and other methods. The other methods will be presented at a future conference.

A DTH reaction (redness and/or induration) was used to assess in vivo immune responses in patients. The DTH orthogonal mean was also measured 48-72 hours after injection but is not reported here.

In this preliminary data analysis, there was a significant increase in percentage of patients experiencing a DTH reaction (redness) in month 4 or month 6 compared to baseline. There were 191 patients with both baseline and month 4 or 6 assessments.

The frequency of DTH reactions increased by approximately 4x (290%) in the total open-label non-HLA-A*02 population, increasing from 5.2% of the patients experiencing a DTH reaction at baseline, prior to any GLSI-100 administration, to 20.4% of the patients experiencing a DTH reaction in month 4 or month 6 (McNemar, p < 0.001).

As reported in Table 1 of the poster, each HLA-A type exhibited more frequent immune reactivity after treatment with GLSI-100 than at baseline with frequency increasing from 100% to 700%.

Baseline DTH reaction prior to any treatment suggests that GP2 may be a natural antigen and that GP2 specific T cells may exist in some patients prior to any treatment with GLSI-100. Baseline immune response to GP2 prior to any vaccination with GP2 was also observed in the Phase IIb trial and is being observed in the blinded randomized arms of FLAMINGO-01, where HLA-A*02 only patients are being vaccinated.

Mechanism of Action: A positive immune response is an indicator that the immune system has been activated against recurring cancer cells, potentially leading to the prevention of metastatic breast cancer. The Company previously announced that in the non-HLA-A*02 arm, a preliminary analysis of recurrence rates after the Primary Immunization Series (PIS) is completed shows an approximately 70-80% reduction in recurrence rate. Thus, the immune response data is supporting the mechanism of action that reduces recurrences and prevents metastatic breast cancer.

This statistically significant non-HLA-A*02 open label arm immune response data is trending similarly to the immune response data in the HLA-A*02 patients in the Phase IIb study and the HLA-A*02 arms of FLAMINGO-01. The study is ongoing and data collection and cleaning continue, while some patients may still be in their PIS vaccination phase, so final results may vary.

A 1% per year recurrence rate is so low that the number of recurrence events is too few to correlate a negative or lack of immune response to recurrence. The same constraint existed with the Phase IIb data which has a similarly low recurrence rate per year. While DTH immune response may be valuable at an aggregate level looking at whole patient populations, the recurrence rate is too low to validate any immune response measure as a biomarker for individual patient treatment decisions. It is also likely that some responding patients may not exhibit any immune response but still could be protected by GLSI-100 vaccination, thus helping to preserve the blind on the randomized arms of FLAMINGO-01.

The immune response abstract and poster conclusion: The statistically significant increase in the incidence of DTH reactions over time found in this preliminary analysis of GLSI-100 treated non-HLA-A*02 patients shows that GLSI-100 treatment should not be limited to HLA-A*02 patients. Patients treated with GLSI-100 were increasingly able to mount an immune response to GP2 as evidenced in this preliminary data. Future investigations may explore the use of immune responses to assess correlation of DTH to ISRs, immunogenicity of GLSI-100 by specific HLA type, timing of boosters to sustain immunity, clinical site performance, and the discontinuation of treatment for non-responders.

In addition, the second poster describing the Phase III trial design, which is being presented on Tuesday, April 21, can be downloaded and seen on the website using the same link. This poster provides an update that over 1,300 patients have been screened to date in FLAMINGO-01. The new protocol amendment, which is still under regulatory review in certain countries, is not discussed.

CEO Snehal Patel commented, “This new immune response data further supports the combination of HLA-A*02 and non-HLA-A*02 patients in the same randomized arms. In the US, the FDA recently reviewed such protocol changes and the many non-HLA-A*02 patients on waiting lists that were previously screened are now being enrolled. The screen rate continues to be encouraging, reflecting the high patient interest in the study as we have now screened over 1,300 patients. The Company will have the option to pursue approval for both HLA-A*02 and non-HLA-A*02 patients together using the increased statistical power of a combined analysis of the two patient groups or to pursue subgroups based on planned multiple interim analyses.”

The abstract from today’s immune response data and the members of the Steering Committee follow:

Abstract Number: CT138 – Poster Section 52 on April 20, 2026, 2-5pm PT

Abstract Title: Preliminary delayed-type-hypersensitivity immune response results from open-label arm of on-going Phase III study to evaluate the efficacy and safety of GLSI-100 (GP2 + GM-CSF) in breast cancer patients with residual disease or high-risk PCR after both neo-adjuvant and postoperative adjuvant anti-HER2 therapy, Flamingo-01

Snehal S. Patel1, Jaye Thompson1, F. Joseph Daugherty1, Francois-Clement Bidard2, William J. Gradishar3, Marcus Schmidt4, Miguel Martin5, Joyce A. O’Shaughnessy6, Hope S. Rugo7, Cesar A. Santa-Maria8, Laura M. Spring9, Mothaffar F. Rimawi10

1Greenwich LifeSciences, Stafford, TX,2Institut Curie, Paris, France,3Northwestern University, Chicago, IL,4University Medical Center Mainz, Mainz, Germany,5GEICAM, Madrid, Spain,6Sarah Cannon Research Institute, Dallas, TX,7City of Hope Comprehensive Cancer Center, Duarte, CA,8Johns Hopkins University, Baltimore, MD,9Massachusetts General Hospital, Boston, MA,10Lester and Sue Smith Breast Center, Dan L Duncan Comprehensive Cancer Center, Baylor College of Medicine, Houston, TX

Background: This Phase III trial is a prospective, randomized, double-blinded, multi-center study (NCT05232916) in HLA-A*02 patients at approximately 140 sites in the US and Europe. A third non-randomized arm of approximately 250 non-HLA-A*02 patients is now fully enrolled and preliminary immune response data is presented below. GP2 is a biologic nine amino acid peptide of the HER2/neu protein delivered in combination with Granulocyte-Macrophage Colony Stimulating Factor (GM-CSF) that stimulates an immune response targeting HER2/neu expressing cancers, the combination known as GLSI-100.

Methods: After standard of care neoadjuvant and adjuvant therapy, 6 intradermal injections of GLSI-100 will be administered over the first 6 months and 5 subsequent boosters will be administered over the next 2.5 years. The participant duration of the trial will be 3 years treatment plus 1 additional year follow-up. Immune responses to GP2 were measured over time using delayed-type-hypersensitivity (DTH) skin tests and injection site reactions (ISRs). The patient population is defined by these key eligibility criteria: 1) HER2/neu positive and HLA, 2) Residual disease or High risk pCR (Stage III at presentation) post neo-adjuvant therapy, 3) Exclude Stage IV, and 4) Completed at least 90% of planned trastuzumab-based therapy.

Results: All patients (n=247) were vaccinated with GLSI-100 and continue in treatment and follow-up. A DTH reaction (redness) was used to assess in vivo immune responses in patients. The DTH orthogonal mean was measured 48-72 hours after injection. In this preliminary data analysis, there was a significant increase in percentage of subjects experiencing a DTH reaction in month 4 or month 6 compared to baseline. The frequency of DTH reactions increased by approximately 4x from 5.2% of the patients experiencing a DTH reaction at baseline, prior to any GLSI-100 administration, to 20.4% of the patients experiencing a DTH reaction in month 4 or month 6 (McNemar, p < 0.001). The study is ongoing and data collection and cleaning continue so final results may vary.

Conclusions: The increase in the incidence of DTH reactions over time found in this preliminary analysis of GLSI-100 treated non-HLA-A*02 patients shows that GLSI-100 treatment should not be limited to the HLA-A*02 genotype. Subjects treated with GLSI-100 were increasingly able to mount an immune response to GP2 as evidenced in this preliminary data. Future investigations may explore the use of immune responses to assess: correlation of DTH to ISRs, immunogenicity of GLSI-100 by specific HLA type, timing of boosters to sustain immunity, clinical site performance, and the discontinuation of treatment for non-responders.

The Steering Committee authoring abstract CT138 is comprised of the following experts in the field of breast cancer oncology representing prominent teaching hospitals in the US and 4 of the largest breast oncology networks in the US, Germany, France, and Spain:

Dr. Mothaffar F. Rimawi – Professor of Medicine at the Baylor College of Medicine and Executive Medical Director and Co-Leader, Breast Cancer Program of the Dan L Duncan Comprehensive Cancer Center

Dr. Francois-Clement Bidard – Professor of Medical Oncology, UVSQ/Paris Saclay University, Head of Breast Cancer Group, Institut Curie, Vice-Chair of the French Breast Cancer research group UCBG (Unicancer)

Dr. William J. Gradishar – Professor of Medicine at the Feinberg School of Medicine at Northwestern University, Chief of Hematology and Oncology in the Department of Medicine, and Betsy Bramsen Professor of Breast Oncology

Dr. Sibylle Loibl – Professor (apl) Goethe University Frankfurt/M, Clinical Consultant Centre for Haematology and Oncology/Bethanien Frankfurt/M, CEO of GBG Forschungs GmbH & Chair of the German Breast Group (GBG)

Dr. Miguel Martin – Professor of Medicine, Head, Medical Oncology Service, Gregorio Marañón General University Hospital, Complutense University, Madrid, CEO of GEICAM

Dr. Joyce A. O’Shaughnessy – Celebrating Women Chair in Breast Cancer, Baylor University Medical Center and Chair, Breast Cancer Program, Texas Oncology, US Oncology, Dallas, Texas

Dr. Hope S. Rugo – Director, Women’s Cancers Program, Division Chief, Breast Medical Oncology, Professor, Department of Medical Oncology & Therapeutics Research, City of Hope Comprehensive Cancer Center, Professor Emeritus, University of California, San Francisco

Dr. Cesar A. Santa-Maria – Associate Professor of Oncology, Breast and Gynecological Malignancies Group, Director of Breast Cancer Trials, Johns Hopkins Sidney Kimmel Comprehensive Cancer Center

Dr. Laura M. Spring – Assistant Professor, Medicine, Harvard Medical School, Attending Physician, Medical Oncology, Massachusetts General Hospital

About the AACR Annual Meeting 2026

The AACR is the first and largest cancer research organization dedicated to accelerating the conquest of cancer and has more than 61,000 members residing in 143 countries and territories. The AACR Annual Meeting is the focal point of the cancer research community, where scientists, clinicians, other health care professionals, survivors, patients, and advocates gather to share the latest advances in cancer science and medicine. From population science and prevention; to cancer biology, translational, and clinical studies; to survivorship and advocacy; the AACR Annual Meeting highlights the work of the best minds in cancer research from institutions all over the world.

About FLAMINGO-01 Open Label Phase III Data More than 1,000 patients have been screened with a current screen rate of approximately 800 patients per year. The 250 patient non-HLA-A*02 arm is now fully enrolled, where all patients received GLSI-100, which is 5 times more treated patients and recurrence rate data than the approximately 50 patients treated in the Phase IIb trial. The Primary Immunization Series (PIS), which includes the first 6 GLSI-100 injections over the first 6 months and is required to reach peak protection, is followed by 5 booster injections given every 6 months to prolong the immune response, thereby providing longer-term protection.

In the non-HLA-A*02 arm, a preliminary analysis of recurrence rates after the PIS is completed shows an approximately 70-80% reduction in recurrence rate.

This observation is trending similarly to the Phase IIb trial results and hazard ratio where HLA-A*02 patients were treated and where breast cancer recurrences were reduced up to 80% compared to a 20-50% reduction in recurrence rate by other approved products.

The immune response at baseline prior to any GLSI-100 treatment, the increasing immune response during the PIS, and the safety profile of non-HLA-A*02 patients is trending similarly to the HLA-A*02 arms of FLAMINGO-01 and to the Phase IIb study.

Analysis of the open label data from FLAMINGO-01 has been conducted in a manner that maintains the study blind. The open label recurrence rate, immune response, and safety data is based on the patients enrolled to date in FLAMINGO-01 and the data provided by the clinical sites so far, which is not completed or fully reviewed, and is thus preliminary. While comparing any preliminary FLAMINGO-01 data to the Phase IIb clinical trial data may be possible, these preliminary results are not a prediction of future results, and the results at the end of the study may differ.

About GLSI-100 Phase IIb Study

In the prospective, randomized, single-blinded, placebo-controlled, multi-center (16 sites led by MD Anderson Cancer Center) Phase IIb clinical trial of HLA-A*02 breast cancer patients, 46 HER2/neu 3+ over-expressor patients were treated with GLSI-100, and 50 placebo patients were treated with GM-CSF alone. After 5 years of follow-up, there was an 80% or greater reduction in cancer recurrences in the HER2/neu 3+ patients who were treated with GLSI-100, followed, and remained disease free over the first 6 months, which we believe is the time required to reach peak immunity and thus maximum efficacy and protection. The Phase IIb results can be summarized as follows:

80% or greater reduction in metastatic breast cancer recurrence rate over 5 years of follow-up with a peak immune response at 6 months and well-tolerated safety profile.

The PIS elicited a potent immune response as measured by local skin tests and immunological assays.

About FLAMINGO-01 and GLSI-100

FLAMINGO-01 (NCT05232916) is a Phase III clinical trial designed to evaluate the safety and efficacy of Fast Track designated GLSI-100 (GP2 + GM-CSF) in HER2 positive breast cancer patients who had residual disease or high-risk pathologic complete response at surgery and who have completed both neoadjuvant and postoperative adjuvant trastuzumab based treatment. The trial is led by Baylor College of Medicine and currently includes US and European clinical sites from university-based hospitals and academic and cooperative networks with plans to open up to 150 sites globally. In the double-blinded arms of the Phase III trial, approximately 500 HLA-A*02 patients are planned to be randomized to GLSI-100 or placebo, and up to 250 patients of other HLA types are planned to be treated with GLSI-100 in a third arm. The trial has been designed to detect a hazard ratio of 0.3 in invasive breast cancer-free survival, where 28 events will be required. An interim analysis for superiority and futility will be conducted when at least half of those events, 14, have occurred. This sample size provides 80% power if the annual rate of events in placebo-treated subjects is 2.4% or greater.

For more information on FLAMINGO-01, please visit the Company’s website here and clinicaltrials.gov here. Contact information and an interactive map of the majority of participating clinical sites can be viewed under the “Contacts and Locations” section. Please note that the interactive map is not viewable on mobile screens. Related questions and participation interest can be emailed to: [email protected]

About Breast Cancer and HER2/neu Positivity

One in eight U.S. women will develop invasive breast cancer over her lifetime, with approximately 300,000 new breast cancer patients and 4 million breast cancer survivors. HER2 (human epidermal growth factor receptor 2) protein is a cell surface receptor protein that is expressed in a variety of common cancers, including in 75% of breast cancers at low (1+), intermediate (2+), and high (3+ or over-expressor) levels.

About Greenwich LifeSciences, Inc.

Greenwich LifeSciences is a clinical-stage biopharmaceutical company focused on the development of GP2, an immunotherapy to prevent breast cancer recurrences in patients who have previously undergone surgery. GP2 is a 9 amino acid transmembrane peptide of the HER2 protein, a cell surface receptor protein that is expressed in a variety of common cancers, including expression in 75% of breast cancers at low (1+), intermediate (2+), and high (3+ or over-expressor) levels. Greenwich LifeSciences has commenced a Phase III clinical trial, FLAMINGO-01. For more information on Greenwich LifeSciences, please visit the Company’s website at www.greenwichlifesciences.com and follow the Company’s Twitter at https://twitter.com/GreenwichLS.

Forward-Looking Statement Disclaimer

Statements in this press release contain “forward-looking statements” that are subject to substantial risks and uncertainties. All statements, other than statements of historical fact, contained in this press release are forward-looking statements. Forward-looking statements contained in this press release may be identified by the use of words such as “anticipate,” “believe,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “seek,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “target,” “aim,” “should,” “will,” “would,” or the negative of these words or other similar expressions, although not all forward-looking statements contain these words. Forward-looking statements are based on Greenwich LifeSciences Inc.’s current expectations and are subject to inherent uncertainties, risks and assumptions that are difficult to predict, including statements regarding the intended use of net proceeds from the public offering; consequently, actual results may differ materially from those expressed or implied by such forward-looking statements. Further, certain forward-looking statements are based on assumptions as to future events that may not prove to be accurate. These and other risks and uncertainties are described more fully in the section entitled “Risk Factors” in Greenwich LifeSciences’ Annual Report on the most recent Form 10-K for the year ended December 31, 2024, and other periodic reports filed with the Securities and Exchange Commission. Forward-looking statements contained in this announcement are made as of this date, and Greenwich LifeSciences, Inc. undertakes no duty to update such information except as required under applicable law.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Metallurgical Progress. Resolution has advanced metallurgical work at its Antimony Ridge project in Idaho, successfully producing a high-purity antimony trioxide intermediate (99.38% Sb2O3) from stibnite using conventional pyrometallurgical processing. Test work across pyrometallurgy, hydrometallurgy, and ore concentration continues to advance, with further results expected in the near term. The project is supported by high-grade antimony mineralization, consistently exceeding 30% and reaching up to 50%, underscoring its development potential as a domestic source of critical minerals.

Strategic U.S. Processing Opportunity. Resolution is also advancing a strategic plan to establish a U.S.-based antimony processing hub in Idaho, addressing the current lack of modern domestic processing capacity. By leveraging existing infrastructure at the Johnson Creek Mill site, Resolution aims to fast-track development of an integrated “mine-to-product” solution, strengthening supply chains for critical minerals essential to U.S. defense and industrial sectors.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Time charter contract extension. Euroseas Ltd. executed a time charter contract extension for the EM Kea at a gross daily rate of $30,000 for a minimum period of 36 months to a maximum of 38 months, at the charterer’s option. The EM Kea is a 2007-built 3,100 twenty-foot equivalent unit (TEU) feeder container ship. The new charter will commence on July 14, 2026, in direct continuation of its present charter. The charter underscores the shortage of prompt tonnage, which, along with macroeconomic disruptions and uncertainty caused by the war in the Middle East, continues to sustain the firmness of the containership market.

Higher rate and improved charter coverage. The new time charter is an improvement over the previous contract rate of $19,000 per day and is expected to contribute EBITDA of $22.5 million during the minimum contracted period. The new time charter enhances charter coverage for 2025, 2026, and 2027 to approximately 91%, 76%, and 44%, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

USA Rare Earth (Nasdaq: USAR) announced this morning a definitive agreement to acquire 100% of Serra Verde Group — owner of the Pela Ema rare earth mine and processing plant in Goiás, Brazil — in a transaction valued at approximately $2.8 billion. The deal is structured as $300 million in cash plus 126.849 million newly issued shares of USAR common stock, based on the company’s April 17 closing price of $19.95.

The acquisition is expected to close in the third quarter of 2026, pending regulatory approvals and customary closing conditions.

This is not a routine tuck-in. It is one of the most strategically significant critical minerals transactions to emerge from the Western world in years — and the timing is deliberate.

Serra Verde’s Pela Ema operation holds a distinction that very few assets in the world can claim: it is the only scaled producer outside of Asia capable of supplying all four magnetic rare earth elements — Neodymium (Nd), Praseodymium (Pr), Dysprosium (Dy), and Terbium (Tb) — at meaningful commercial volumes. These are the materials that go into permanent magnets, which in turn power electric vehicle motors, wind turbines, defense systems, and advanced electronics. China currently controls the overwhelming majority of global rare earth production and processing. Serra Verde represents a direct challenge to that dominance.

The operation is fully permitted and entered production in 2024 after more than $1.1 billion in capital investment. At Phase 1 nameplate capacity — expected to be reached by the end of 2027 — the mine is projected to produce approximately 6,400 metric tons of total rare earth oxide per year and generate annualized EBITDA of $550 to $650 million. The combined company is targeting approximately $1.8 billion in EBITDA by 2030.

The financial structure of this deal is notable beyond the headline price. Serra Verde has already secured a $565 million financing package from the U.S. International Development Finance Corporation to fund optimization and expansion through to positive cash flow. It has also locked in a 15-year, 100% offtake agreement with a special purpose vehicle capitalized by various U.S. government agencies and private capital sources — with guaranteed minimum floor prices for each of the four magnetic rare earths. That government-backed revenue floor substantially de-risks the asset and signals how seriously Washington views rare earth supply chain security as a national priority.

By end of 2027, Serra Verde’s output is expected to represent more than 50% of total non-China heavy rare earth supply globally — a figure that underscores just how critical this asset is to Western supply chain independence.

For USAR, the transaction adds Serra Verde leadership to its board, including Chairman Sir Mick Davis and CEO Thras Moraitis, who will also become President of the combined company. Pro-forma liquidity for the combined entity stands at approximately $3.2 billion.

Moelis & Company acted as exclusive financial advisor to USA Rare Earth. Goldman Sachs advised Serra Verde.

For small-cap investors tracking the critical minerals space, this is the deal that has been anticipated for years — and it closed on one of the most strategically defensible assets available outside of China.

Biotech’s long IPO drought may finally be breaking — but don’t mistake a crack in the window for a wide-open door.

This week, two biopharma companies launched roadshows that signal a cautious return of investor appetite to the public markets. GLP-1 developer Kailera Therapeutics hit the road at a $1.9 billion valuation, while proteomics company Alamar Biosciences priced at $17 per share — the top of its marketed range — and opened trading on the Nasdaq Friday with a 33% pop, valuing the company at roughly $1.53 billion. The upsized offering raised $191.3 million, a meaningful signal that institutional demand is real, not manufactured.

But the story isn’t really about IPOs. It’s about M&A.

The primary engine driving this biotech resurgence is an aggressive acquisition cycle fueled by the pharmaceutical industry’s looming patent cliff. Major drug companies are racing to backfill pipelines before blockbuster drugs lose exclusivity, and that urgency is translating into deal flow at a historic pace. According to a Stifel report, 19 biopharma M&A transactions of $1 billion or more were announced between January 1 and April 7 alone — putting the industry on pace for its second-highest annual total ever. Marquee deals include Merck’s $6.7 billion acquisition of Terns Pharmaceuticals and Eli Lilly’s $6.3 billion upfront commitment for Centessa Pharmaceuticals, both announced last month.

That M&A velocity matters beyond the deal itself. When large acquisitions close, venture investors recycle that capital back into the ecosystem — funding the next generation of companies and, critically, making investors more willing to participate in secondary offerings and IPOs. It’s a flywheel, and right now it’s spinning.

Valuations in the private markets are reflecting it. Median pre-money valuations for venture-growth biopharma companies jumped from $65 million to $247 million in 2025, according to PitchBook’s Q4 2025 Biopharma VC Trends report. And the Russell 2000 Biotech Index is up 9.7% year-to-date, outperforming the S&P 500.

That said, the numbers tell a sobering parallel story: of the six biopharma companies that have gone public since January, four are currently trading below their offer price. The market is rewarding quality — and punishing everyone else.

The threshold to go public has risen considerably since the 2020–2021 boom years, when companies with minimal patient data could attract institutional money. Today, clinical-stage companies are bringing 50 or more patients’ worth of data to the roadshow. Pre-clinical companies aren’t even in the conversation.

For small and microcap investors, this environment requires nuance. The biotech IPO window is open — but narrowly, and selectively. Companies that are scientifically de-risked, operationally sound, and well-positioned relative to M&A comps are getting deals done. Everything else is waiting.

The broader implication: as Big Pharma’s acquisition appetite grows, smaller biotech names that could plausibly become targets deserve a closer look. The deals are getting done — the question is who’s next on the list.