Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Review. We reviewed the Company’s 10-K filing as well as went through the conference call transcript again. Both highlight the tremendous amount of opportunity available to the Company. Opportunity that we believe will begin to be realized this year and lead to improved operating performance.

A Key Change. While Kratos always has been open to partnering with prime contractors, the 10-K highlights, in our view, a mindset change in such partnerships. Kratos now will be more willing to enter such partnerships in all areas of the Company’s business when management’s assessment of the opportunities indicates such a partnership is the most favorable opportunity.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q23 Results. Kelly reported revenue of $1,232.2 million, essentially flat y-o-y and down just 1.3% on a constant currency basis. We had estimated $1,220 million. Adjusted net income was $34.1 million or EPS of $0.93, compared to $7 million, or $0.18/sh last year. We had estimated EPS of $0.56. Adjusted EBITDA was $32.5 million, or a 2.6% margin, up from $24.1 million and 2%, respectively, last year. We had forecast $33.8 million.

International Sale. As previously announced, Kelly completed the sale of its International staffing business in early January. This business generated some $810 million of revenue and $120 million of gross profit in 2023.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Revenues improve with the addition of vessels and higher shipping rates. EuroDry took possession of three ships during the quarter and put them into service, resulting in additional operating days. The average shipping rate of $14.570 rose 20% quarter over quarter. EuroDry continues to be the most sensitive to rate changes of all the shipping companies we follow.

Expenses went up with more ships, but costs per operating day were flat. Vessel operating and depreciation costs rose with an increase in voyage days. Vessel operating costs per voyage day were $5,421 in the most recent quarter versus $5,343 in the previous quarter and $5,366 in the same period last year. Financing costs rose with the issuance of $32.5 million to finance the acquisition of vessels.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The mining sector has experienced boom and bust cycles throughout history, but current trends suggest we may be entering a new era of growth and opportunity. With the world transitioning to clean energy and electric vehicles, demand is surging for key minerals like lithium, cobalt, nickel and copper. This creates an attractive investment case for the mining sector.

Historic Trends

Looking back, the mining industry has gone through periods of rapid expansion and painful contraction. During economic expansions and commodity bull markets, mining companies ramp up exploration, development and production to capitalize on high prices. This leads to oversupply and when demand eventually weakens, the cycle turns downward.

We saw this play out in dramatic fashion over the past decade. High prices in the 2000s encouraged massive investment in new mines and supply capacity. But when Chinese growth began to slow around 2012, demand weakened and prices collapsed. The mining sector was forced to drastically cut back on production and capital investment.

Many mining companies barely stayed afloat during this bust period. But this reduction in supply helped set the stage for the next upcycle. Now, after years of underinvestment, mines are depleting reserves faster than they are being replenished. With commodity demand picking up again, conditions are ripe for the next mining boom.

Current Market Trends

Several key trends suggest we are now in the early stages of a new mining upcycle:

Electric vehicle revolution – EV adoption is accelerating around the world, dramatically increasing demand for lithium, cobalt, nickel, copper and other key minerals. Total EV sales increased 70% in 2021 and are projected to rise more than 5-fold by 2030. This will require a massive increase in mineral supply.

Renewable energy expansion – Solar, wind and other renewables are seeing surging growth as countries aim to cut carbon emissions. This further increases metals demand for batteries, transmission lines, wiring and other components.

Supply chain vulnerabilities – The pandemic and geopolitics have exposed risks of relying on a few key countries for critical mineral supply. Governments are now focused on developing domestic mining capacity to ensure supply security.

Decarbonization efforts – Reaching net zero emissions will require a staggering volume of minerals for clean energy infrastructure buildout. Models estimate needing 30 times more lithium and 15 times more cobalt by 2040.

These trends all point to a pending boom in mining investment and production. The demand outlook has fundamentally shifted in a more positive direction.

For investors, this macro backdrop presents an opportunity to capitalize on the coming mining supercycle. Some ways to gain exposure include:

Lithium mining stocks – Lithium prices have skyrocketed 10-fold in the past two years as demand for electric vehicle batteries has soared. Leading lithium miners like Albemarle, SQM and Livent are seeing their earnings multiply. They are investing heavily to aggressively expand production capacity to ride the lithium boom. Their stocks still may have substantial upside given the tight supply and surging demand forecasts.

Nickel and cobalt miners – Clean energy technologies like batteries require vast amounts of nickel and cobalt. Both metals face looming supply deficits. Miners expanding production such as Glencore, Sherritt International and Giga Metals stand to benefit enormously from surging demand and higher prices over the coming decade. These miners offer some of the best leverage to capitalize on the EV battery revolution.

Copper miners – Copper is essential for global electrification and will be required by the millions of tons for EV charging networks, power grids, wiring and electronics. Leading copper miners like Freeport McMoRan, Southern Copper and First Quantum Minerals offer direct exposure to higher copper prices. Many are expanding production while also paying healthy dividends.

Diversified mining majors – Large diversified miners like BHP, Rio Tinto and Vale mine a broad mix of commodities from copper and iron ore to coal and potash. Their diversification provides stability while still benefiting from the overall minerals boom. These global giants pay some of the highest dividends in the market.

Junior mining stocks – Earlier stage mining companies developing new projects provide extreme upside potential leverage but also greater risk. Conduct thorough due diligence on management track record, finances, permitting status and feasibility studies before investing.

Physical gold and silver – Precious metals like gold and silver can provide a hedge against market volatility. Buying physical coins and bars or investing in ETFs offers exposure. Just a small allocation of 5-10% can help balance a portfolio.

Mining ETFs – Funds like the Global X Lithium ETF (LIT), VanEck Vectors Gold Miners ETF (GDX) and SPDR Metals & Mining ETF (XME) provide diversified exposure to mining stocks and commodities. This simplifies investing in the sector.

With mining poised to boom, investors have many options to position for the coming supercycle. As with any investment, proper due diligence and risk management remain critical. But the macro trends point to a bright future for mining stocks. For investors, now may be the ideal time to position for the coming mining supercycle.

Oil prices are on track to post gains this week, driven higher by geopolitical tensions in the Middle East despite ongoing concerns about still high inflation and a cloudy demand outlook.

West Texas Intermediate crude futures have risen approximately 2% week-to-date and were trading around $78 per barrel on Friday. Brent crude, the international benchmark, was up 1.8% on the week to $83 per barrel.

According to analysts, speculative traders and funds are bidding up oil futures based on worries that simmering conflicts in the Middle East could disrupt global supplies. Volatility and uncertainty in the region tends to spur speculative trading in oil markets.

“This is geopolitics with flashing flights, it points right to specs taking advantage of the situation,” said Bob Yawger, managing director at Mizuho America. “They’re rolling the dice expecting something will happen.”

Tensions have escalated on the border between Israel and Lebanon after Israel conducted airstrikes in southern Lebanon this week in retaliation for rocket attacks from the area. The powerful Lebanese militia Hezbollah has vowed to strike back against Israel in response.

There are worries the Israel-Lebanon clashes could spread to a wider conflict, potentially including Israel’s ongoing offensive in Gaza. This could disrupt oil production or transit through the critical Suez Canal. The Middle East accounted for nearly 30% of global oil production last year.

Prices Shake Off Demand Worries

Notably, crude prices have shaken off downward pressure this week from stubbornly high inflation as well as forecasts for weaker demand growth in 2024.

US consumer and wholesale inflation reports this week came in hotter than expected. Persistently high inflation reduces the chances of the Federal Reserve pivoting to interest rate cuts this year which could otherwise boost oil demand.

Demand outlooks for 2024 have also been murky. The International Energy Agency (IEA) downwardly revised its 2024 oil demand growth forecast to 1.2 million barrels per day, half of 2023’s pace. It sees supply growth outpacing demand this year.

However, OPEC offered a more bullish view in its latest report, projecting world oil demand will increase by 2.2 million barrels per day in 2024. The cartel sees demand growth exceeding non-OPEC supply growth.

Investors Shake Off Bearish Signals

Given the conflicting demand forecasts, the resilience of oil prices likely reflects investor optimism over tightening fundamentals outweighing potentially bearish signals.

“There is and has been a yawning chasm in demand estimates,” said Tamas Varga, analyst at PVM brokerage. “The difference of opinions in global oil consumption for this year and the individual quarters, even for the current one, is clearly puzzling.”

Ultimately, lingering Middle East geopolitical risks appear to be overshadowing inflation and demand concerns in driving investor sentiment. With tensions still elevated, investors seem positioned for further volatility and potential price spikes on any supply disruptions.

The diverging demand forecasts and data points mean uncertainty persists around whether markets will tighten as much as OPEC expects or remain oversupplied per the IEA outlook. But with inventories still low by historical standards, prices have room to run higher on any bullish shocks.

What’s Next For Oil Markets

Looking ahead, Middle East tensions, China’s reopening, and the extent of Fed rate hikes will be key drivers of oil price trends. Any military escalation or supply disruptions from the Israel-Lebanon tensions could send crude prices spiking higher.

China’s demand recovery as it exits zero-Covid policies will also remain in focus. Signs of China’s crude imports and manufacturing activity reviving could offer a bullish boost to prices.

At the same time, stubborn inflation likely keeps the Fed on track for further rate hikes in the near term. Only clear signs of slowing price growth might promptdiscussion of rate cuts to stimulate growth. For now, Fed policy looks set to weigh on oil demand and limit significant upside.

Overall, investors should brace for continued volatility in oil markets in 2024. While prices may trend higher on tight supplies, lingering demand uncertainties and geo-political tensions look set to drive choppy price action. Nimble investors able to capitalize on price spikes and dips may find opportunities. But those with a lower risk tolerance may wish to stay on the sidelines until fundamentals stabilize.

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that its board of directors has declared a quarterly cash dividend of $0.075 per share. The dividend will be paid on March 27, 2024, to stockholders of record as of the close of business on March 15, 2024.

“This is the Company’s 25th quarterly cash dividend since it began paying dividends in 2018. The Company’s dividend has become an important part of our capital allocation strategy and we remain committed to supporting our quarterly dividend with our robust free cash flow. At the current stock price, on an annualized basis, our shareholders are receiving a 5% yield on their investment,” said Tom Tedford, President, and Chief Executive Officer of ACCO Brands.

About ACCO Brands Corporation

ACCO Brands, the Home of Great Brands Built by Great People, designs, manufactures and markets consumer and end-user products that help people work, learn, play and thrive. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 103 facilities totaling approximately 83,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

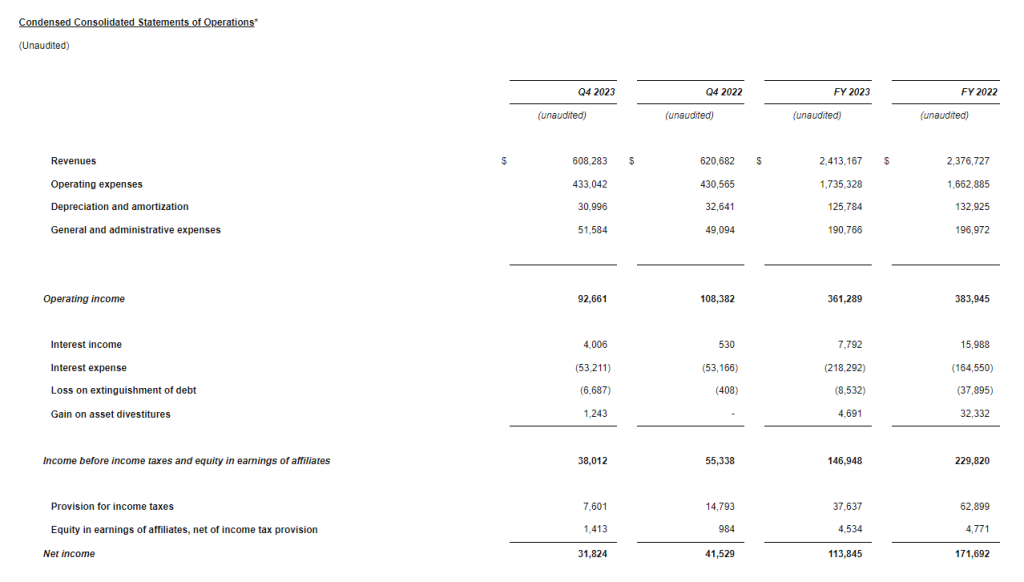

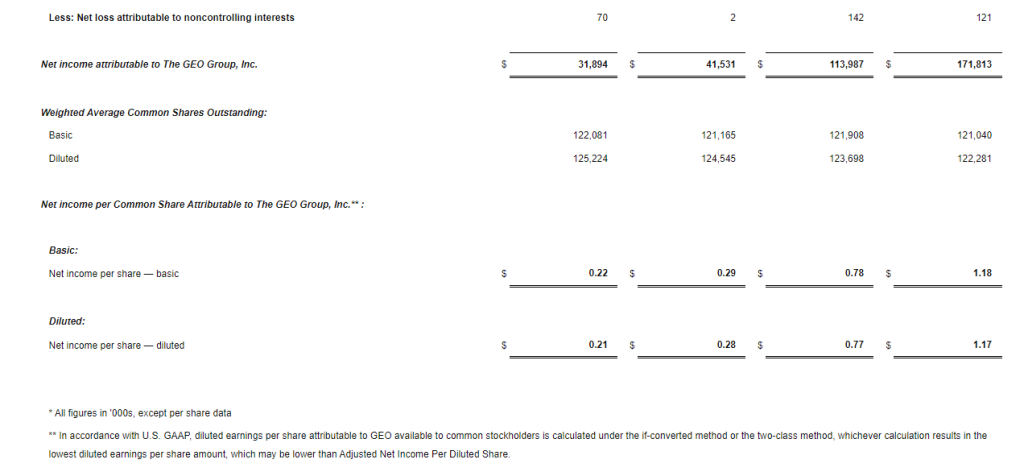

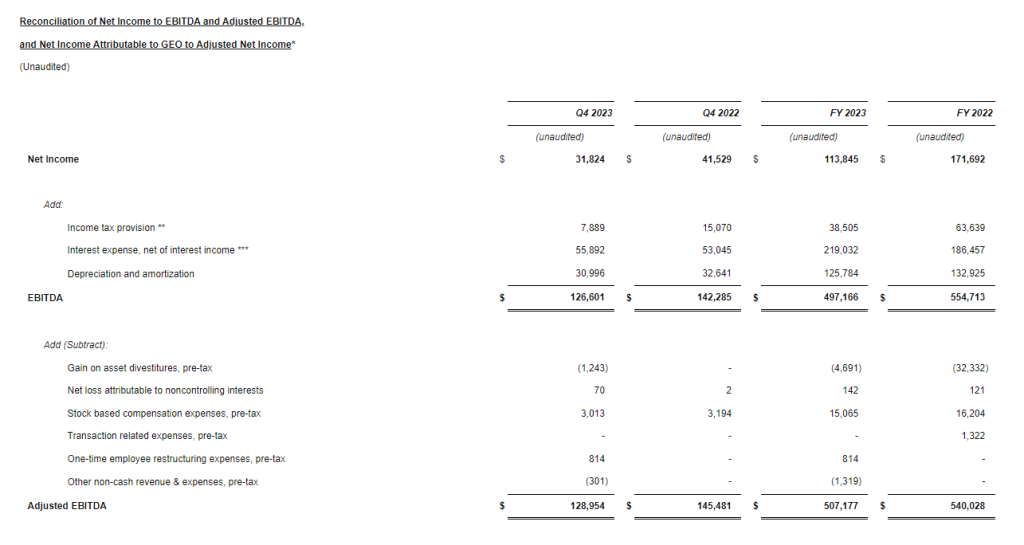

4Q23 Results. Revenue for the quarter came in at $608.3 million, compared to $620.7 million a year ago. Adjusted EBITDA totaled $129 million, EPS was $0.21, and adjusted EPS $0.29. In the year ago period, GEO reported $145.5 million, $0.28, and $0.34, respectively. We had forecast $600 million, $119.5 million, $0.19, and $0.19, respectively.

Debt Reduction. For the full year, GEO reduced net debt by some $197 million, ending the year with approximately $1.8 billion of net debt. We expect the Company to continue to reduce net debt by $175-$200 million annually.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 131-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q23 Results. Fourth quarter revenue came in at $181.7 million, slightly below our $190 million estimate, due to a delay in some work which has since commenced, but above the $146.7 million in 4Q22. Reported gross margin jumped to 21.3% from a negative last year. Net income came in at $21.6 million, or $0.32/sh, from a loss of $31.2 million, or a loss of $0.47/sh in 4Q22, which was impacted by the write-down of the Terrapin Island. Adjusted EBITDA came in at $40.8 million, up from a $24.2 million loss last year.

Solid Operating Environment. The dredging bid environment remains strong, with proposed increased funding and a number of key capital projects coming to bid in 2024. While the wind and LNG segments are more challenged, we believe both markets will prove fruitful for Great Lakes in the long-term.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mortgage rates have climbed over the past year, hovering around 7% for a 30-year fixed rate mortgage. This is significantly higher than the 3% rates seen during the pandemic in 2021. Rates are being pushed higher by several key factors.

Inflation has been the main driver of increased borrowing costs. The consumer price index rose 7.5% in January 2024 compared to a year earlier. While this was down slightly from December, inflation remains stubbornly high. The Federal Reserve has been aggressively raising interest rates to combat inflation. This has directly led to higher mortgage rates.

As the Fed Funds rate has climbed from near zero to around 5%, mortgage rates have followed. Additional Fed rate hikes are expected this year as well, keeping upward pressure on mortgage rates. Though inflation eased slightly in January, it remains well above the Fed’s 2% target. The central bank has signaled they will maintain restrictive monetary policy until inflation is under control. This means mortgage rates are expected to remain elevated in the near term.

Another factor pushing rates higher is the winding down of the Fed’s bond buying program, known as quantitative easing. For the past two years, the Fed purchased Treasury bonds and mortgage-backed securities on a monthly basis. This helped keep rates low by increasing demand. With these purchases stopped, upward pressure builds on rates.

The yield on the 10-year Treasury note also influences mortgage rates. As this yield has climbed from 1.5% to around 4% over the past year, mortgage rates have moved higher as well. Investors demand greater returns on long-term bonds as inflation eats away at fixed income. This in turn pushes mortgage rates higher.

With mortgage rates elevated, the housing market is feeling the effects. Home sales have slowed significantly as higher rates reduce buyer affordability. Prices are also starting to moderate after rapid gains the past two years. Housing inventory is rising while buyer demand falls. This should bring more balance to the housing market after it overheated during the pandemic.

For potential homebuyers, elevated rates make purchasing more expensive. Compared to 3% rates last year, the monthly mortgage payment on a median priced home is around 60% higher at current 7% rates. This prices out many buyers, especially first-time homebuyers. Households looking to move up in home size also face much higher financing costs.

Those able to buy may shift to adjustable rate mortgages (ARMs) to get lower initial rates. But ARMs carry risk as rates can rise substantially after the fixed period. Lower priced homes and smaller mortgages are in greater demand. Refinancing has also dropped off sharply as existing homeowners already locked in historically low rates.

There is hope that mortgage rates could decline later this year if inflation continues easing. However, most experts expect rates to remain above 6% at least through 2024 until inflation is clearly curtailed. This will require the Fed to maintain their aggressive stance. For those able to buy at current rates, refinancing in the future is likely if rates fall. But higher rates look to be the reality for 2024.

CULVER CITY, Calif., Feb. 15, 2024 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail Games” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, announces significant strides with the launch of West Hunt on Nintendo Switch and the introduction of ASA Premium Mods for ARK Survival Ascended. These initiatives underscore Snail Games’ unwavering commitment to continuously improving and enhancing its current portfolio of game titles.

West Hunt on Nintendo Switch

Snail Games’ independent game branch, Wandering Wizard, in collaboration with developing studio New Gen, recently launched West Hunt on Nintendo Switch. This highly anticipated game transports players into the heart of the Wild West, enabling them to embark on manhunts wherever they go. The launch of West Hunt on Nintendo Switch marks a significant milestone in Snail Games’ journey, as it extends the game’s reach beyond Steam into the thriving console gaming community. As players immerse themselves in the role of law-abiding Sheriffs or cunning outlaws, they are invited to experience the Wild West like never before. Snail Games’ commitment to broadening West Hunt’s success on Steam to new platforms exemplifies its dedication to continually growing its current titles.

ASA Premium Mods

Snail Games is also set to introduce ARK Survival Ascended’s Premium Mods program. This innovative initiative revolutionizes the modding landscape by providing unprecedented opportunities for monetization. With one of the most competitive revenue-sharing models in the industry, ARK Survival Ascended’s Premium Mods program ensures that modders are duly recognized and rewarded for their creativity and dedication. Moreover, ASA Premium Mods’ cross-platform compatibility across PC, Xbox, and PlayStation amplifies modders’ reach, enabling them to maximize their earnings and connect with a broader audience. ARK Survival Ascended’s mod program is committed to fostering an environment that encourages innovation, collaboration, and fair compensation for modders. The program aims to be a catalyst for positive change within the modding community, empowering creators to thrive in their craft. The premium mod program has launched on the PC platform with other platforms to follow in time.

“We remain committed to improving and elevating our current portfolio of games, ensuring that every player finds adventure and excitement in our diverse offerings. We embark on these exciting new ventures with our community and partners at the forefront of our strategy,” said Jim Tsai, Chief Executive Officer of Snail Games.

With the launch of West Hunt on Nintendo Switch and the introduction of ASA Premium Mods for ARK Survival Ascended, Snail Games believes that it will continue to lead the way in the gaming industry, driving forward its vision of innovation and growth.

Snail, Inc. is a leading global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PC’s and mobile devices.

About Wandering Wizard

Wandering Wizard is passionately committed to championing indie game developers. We provide a platform for fresh voices, revolutionary ideas, and daring experiments within the indie gaming realm. Embracing the inherent risks of indie game development, we partner with creators worldwide to enrich the global gaming community with inclusive, inspiring, and innovative gaming experiences.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future results of Snail’s business, financial condition, results of operations, liquidity, plans and objectives. The statements Snail makes regarding the following matters are forward-looking by their nature: growth prospects and strategies; launching new games and additional functionality to games that are commercially successful, including the launch of ARK: Survival Ascended, ARK: The Animated Series and ARK 2; expectations regarding significant drivers of future growth; its ability to retain and increase its player base and develop new video games and enhance existing games; competition from companies in a number of industries, including other game developers and publishers and both large and small, public and private Internet companies; its relationships with third-party platforms such as Xbox Live and Game Pass, PlayStation Network, Steam, Epic Games Store, the Apple App Store, the Google Play Store, My Nintendo Store and the Amazon Appstore; expectations for future growth and performance; and assumptions underlying any of the foregoing.

Colossus SSP’s Inclusive Marketplace Approach to Further Advance SHE Media’s Work in Fueling Growth of Women-Owned & Diverse-Owned Properties

HOUSTON and NEW YORK, Feb. 15, 2024 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses, LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), announced today that SHE Media, the top 10 lifestyle media group that includes SheKnows, Flow Space, StyleCaster, Soaps and BlogHer, has selected Colossus SSP as a new supply-side platform partner. Colossus SSP has a strong track-record in connecting advertisers with a truly inclusive audience, at scale, tapping into a range of multicultural / diverse publishers, as well as top-tier general market media.

Colossus SSP will serve as a programmatic exchange sell-side partner for SHE Media’s flagship brands and other properties, all of which are focused on providing useful and inspiring high-quality content for women, reaching a total audience of 74+ million users per month[1]. Key to the partnership, Colossus SSP will provide access to inventory across SHE Media’s Meaningful Marketplaces – a robust community of independent, premium, women-owned and diverse-owned publishers that SHE Media assists with monetization, operations and educational services.

“The tens of millions of women that visit SHE Media properties and engage with its content are a tremendous asset to advertisers across category sectors,” said Mark D. Walker, CEO and Co-Founder, Direct Digital Holdings. “Not only do women represent more than half of the U.S. population, they are responsible for 85 percent of the day-to-day spending decisions and 80 percent of all healthcare choices for the family. Partnering with SHE Media will open Colossus SSP’s pipeline of advertisers to this valuable audience. In addition, it’s an honor to work with a company that also champions inclusivity across the media and marketing ecosystem.”

“SHE Media’s strategic partnership with Direct Digital Holding’s Colossus SSP will further solidify both companies’ deep-seated commitment to the economic growth of women-owned and diverse-owned media,” said Kate Calabrese, SVP, Media Solutions, SHE Media. “This integration will deliver an additional pathway to match advertisers with both the audiences they intend to reach and with the independent publishers whose businesses they are dedicated to support.”

“We are excited to be working with SHE Media because it is such a perfect fit for Colossus SSP. Their dynamic female-focused content and coveted female audience are very much aligned with the needs of the advertisers that we serve,” added Lashawnda Goffin, CEO, Colossus SSP.

Forward-Looking Statements This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

About SHE Media As a top 10 lifestyle media company reaching 74+ million monthly visitors, SHE Media focuses on the power of content and community to move our culture forward. SHE Media believes that media companies can and should be a force for good in the world. The company’s rich editorial ranges from health, food, and family to career and entertainment. SHE Media’s flagship brands, SheKnows, Flow Space, StyleCaster, Soaps and BlogHer, produce award-winning lifestyle content and events that reflect the passion and purpose of the company. In addition to the flagship brands, the SHE Media Collective supports thousands of independent publishers and content creators with technology, education, and monetization opportunities to grow their businesses.

SHE Media has a longstanding commitment to the advancement of equity and inclusion through media. In 2021, SHE Media launched Meaningful Marketplaces enabling advertisers to buy media at scale from a community of women and minority-owned publishers, ensuring that independent media receives the economic support to thrive. SHE Media is also dedicated to advancing women’s health. In 2023, SHE Media launched Flow Space, an all-new digital and live media platform providing content, community, and commerce in service of women’s whole life health. Part of Penske Media Corporation (PMC), SHE Media is based in New York, with offices in Los Angeles. Follow SHE Media on LinkedIn, Instagram, Facebook and Twitter.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The Company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage on average over 125,000 clients monthly, generating over 300 billion impressions per month across display, CTV, in-app and other media channels.

Q4 operating earnings of $7.3 million, or up 59% to $22.1 million on an adjusted basis

Q4 revenue was flat; down 1.3% in constant currency

Q4 adjusted EBITDA margin increased 60 basis points to 2.6% driven by meaningful reduction in operating expenses resulting from business transformation initiatives

Company expects Q1 2024 sale of European staffing operations, sustained structural expense reductions and near-term outcome from growth initiatives to drive further expansion of EBITDA margin

TROY, Mich., Feb. 15, 2024 (GLOBE NEWSWIRE) — Kelly (Nasdaq: KELYA, KELYB), a leading specialty talent solutions provider, today announced results for the fourth quarter of 2023.

Peter Quigley, president and chief executive officer, announced revenue for the fourth quarter of 2023 totaled $1.2 billion, a 0.1% decrease, or a 1.3% decrease in constant currency, compared to the corresponding quarter of 2022. Year-over-year revenue trends were impacted by customers’ more guarded approach to hiring and initiating new projects or capital spending partially offset by favorable foreign currency impacts.

Kelly reported operating earnings in the fourth quarter of 2023 of $7.3 million, compared to earnings of $4.6 million reported in the fourth quarter of 2022. Earnings in the fourth quarter of 2023 include $14.8 million of charges related to transformation actions and the first-quarter 2024 sale of our European staffing operations. Excluding those charges, adjusted earnings were $22.1 million in the fourth quarter of 2023. Earnings in the fourth quarter of 2022 included a $10.3 million goodwill impairment charge related to RocketPower. Excluding the impairment charge and a $0.9 million gain related to the sale of real property, adjusted earnings from operations were $14.0 million. Adjusted earnings improved primarily as a result of lower selling, general and administrative expenses, partially offset by unfavorable business mix and lower permanent placement fees which resulted in lower gross profit.

Earnings per share in the fourth quarter of 2023 were $0.31 compared to a loss per share of $0.02 in the fourth quarter of 2022. Included in earnings per share in the fourth quarter of 2023 were restructuring charges, net of tax, of $0.16. In addition, there were $0.46 per share of tax adjustments, transaction costs, and an unrealized loss on a forward contract, all net of tax, related to the first-quarter 2024 sale of our European staffing operations. Included in the loss per share in the fourth quarter of 2022 is a $0.23 per share goodwill impairment charge, net of tax, related to RocketPower, partially offset by a $0.02 per share gain on sale of real property, net of tax. On an adjusted basis, earnings per share were $0.93 in the fourth quarter of 2023, an improvement from $0.18 per share in the corresponding quarter of 2022.

“In the fourth quarter, we captured steady demand in Education and most of our outcome-based specialties in P&I, which continue to demonstrate resilience amid a challenging operating environment. We remained focused on the future as well, driving significant progress on our transformation initiatives while completing the sale of Kelly’s European staffing operations which we closed in early January, unlocking more than $100 million of capital and additional net margin expansion,” said Quigley. “Taken together, these accomplishments have propelled Kelly’s EBITDA margin to 3% entering 2024 – a step change from the company’s historical average of approximately 2%. As we continue to build a more efficient, effective, and focused enterprise, I am confident we are well positioned to capture increased customer demand when the operating environment rebounds and accelerate profitable growth.”

Kelly also reported that on February 13, its board of directors declared a dividend of $0.075 per share. The dividend is payable on March 13, 2024, to stockholders of record as of the close of business on February 27, 2024.

In conjunction with its fourth-quarter earnings release, Kelly has published a financial presentation on the Investor Relations page of its public website and will host a conference call at 9 a.m. ET on February 15 to review the results and answer questions. The call may be accessed in one of the following ways:

Via the Telephone (877) 692-8955 (toll free) or (234) 720-6979 (caller paid) Enter access code 5728672 After the prompt, please enter “#”

A recording of the conference call will be available after 1:30 p.m. ET on February 15, 2024, at (866) 207-1041 (toll-free) and (402) 970-0847 (caller-paid). The access code is 5856971#. The recording will also be available at kellyservices.com during this period.

This release contains statements that are forward looking in nature and, accordingly, are subject to risks and uncertainties. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements that are not historical facts, including statements about Kelly’s financial expectations, are forward-looking statements. Factors that could cause actual results to differ materially from those contained in this release include, but are not limited to, (i) changing market and economic conditions, (ii) disruption in the labor market and weakened demand for human capital resulting from technological advances, loss of large corporate customers and government contractor requirements, (iii) the impact of laws and regulations (including federal, state and international tax laws), (iv) unexpected changes in claim trends on workers’ compensation, unemployment, disability and medical benefit plans, (v) litigation and other legal liabilities (including tax liabilities) in excess of our estimates, (vi) our ability to achieve our business’s anticipated growth strategies, (vii) our future business development, results of operations and financial condition, (viii) damage to our brands, (ix) dependency on third parties for the execution of critical functions, (x) conducting business in foreign countries, including foreign currency fluctuations, (xi) availability of temporary workers with appropriate skills required by customers, (xii) cyberattacks or other breaches of network or information technology security, and (xiii) other risks, uncertainties and factors discussed in this release and in the Company’s filings with the Securities and Exchange Commission. In some cases, forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “target,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions. All information provided in this press release is as of the date of this press release and we undertake no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

About Kelly®

Kelly Services, Inc. (Nasdaq: KELYA, KELYB) helps companies recruit and manage skilled workers and helps job seekers find great work. Since inventing the staffing industry in 1946, we have become experts in the many industries and local and global markets we serve. With a network of suppliers and partners around the world, we connect more than 500,000 people with work every year. Our suite of outsourcing and consulting services ensures companies have the people they need, when and where they are needed most. Headquartered in Troy, Michigan, we empower businesses and individuals to access limitless opportunities in industries such as science, engineering, technology, education, manufacturing, retail, finance, and energy. Revenue in 2023 was $4.8 billion. Learn more at kellyservices.com.

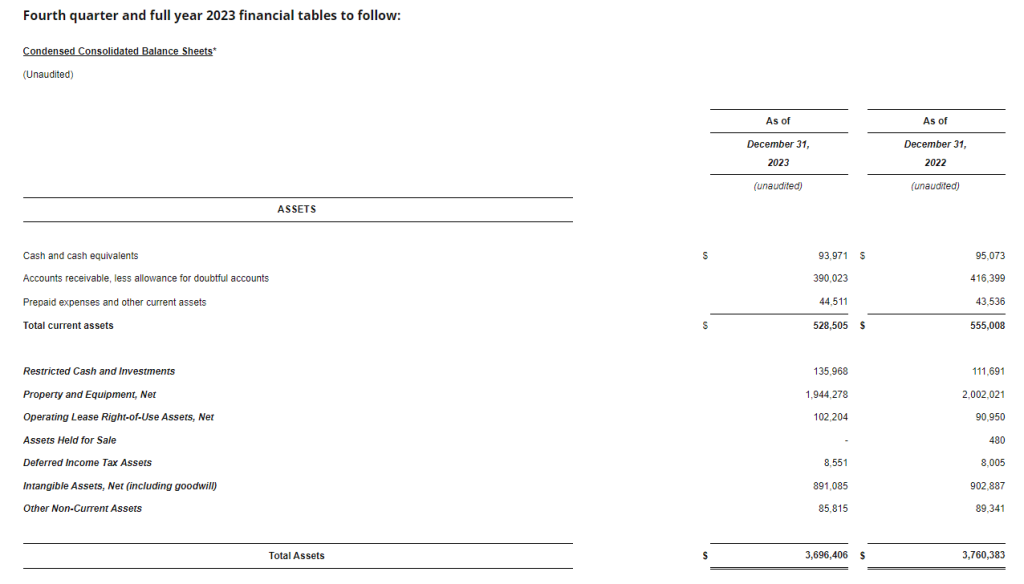

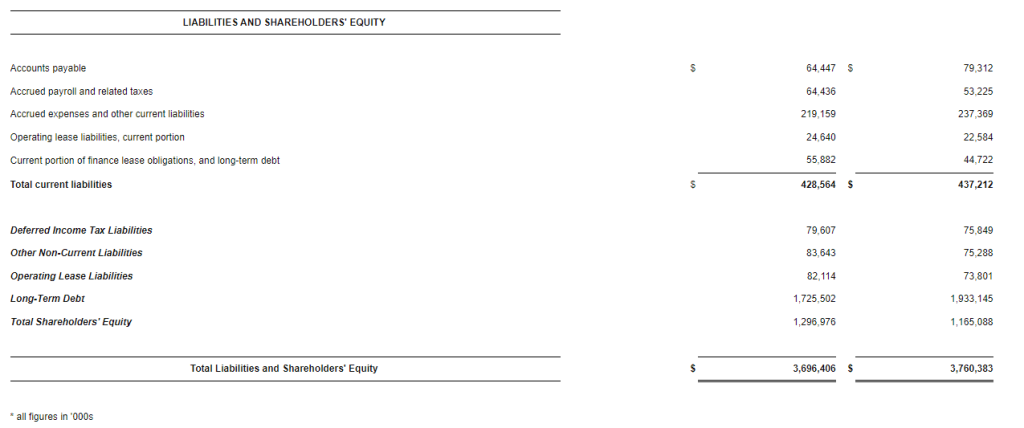

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 15, 2024– The GEO Group, Inc. (NYSE: GEO) (“GEO”), a leading provider of support services for secure facilities, processing centers, and reentry centers, as well as enhanced in-custody rehabilitation, post-release support, and electronic monitoring programs, reported today its financial results for the fourth quarter and full year 2023.

Full Year 2023 Highlights

Total revenues of $2.41 billion

Net Income of $113.8 million

Adjusted EBITDA of $507.2 million

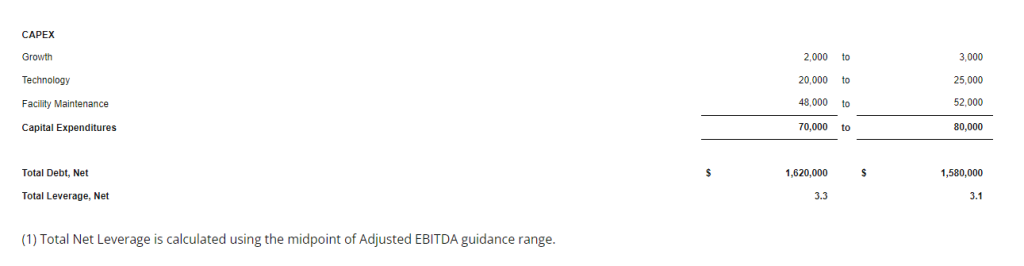

Reduced Total Net Debt by Approximately $197.0 million in FY23 to $1.78 billion

For the full year 2023, we reported total revenues of $2.41 billion compared to $2.38 billion for the full year 2022. We reported net income for the full year 2023 of $113.8 million, compared to $171.7 million for the full year 2022. Results for the full year 2023 reflect a year-over-year increase of $61.9 million in net interest expense as a result of the transactions we completed in August 2022 to address the substantial majority of our outstanding debt and the impact of higher interest rates. For the full year 2023, we reported Adjusted EBITDA of $507.2 million, compared to $540.0 million for the full year 2022. During 2023, we reduced our total net debt by approximately $197.0 million to approximately $1.78 billion.

Fourth Quarter 2023 Highlights

Total revenues of $608.3 million

Net Income of $31.8 million

Adjusted EBITDA of $129.0 million

For the fourth quarter 2023, we reported net income of $31.8 million, compared to $41.5 million for the fourth quarter 2022. We reported total revenues for the fourth quarter 2023 of $608.3 million compared to $620.7 million for the fourth quarter 2022. We reported fourth quarter 2023 Adjusted EBITDA of $129.0 million, compared to $145.5 million for the fourth quarter 2022.

George C. Zoley, Executive Chairman of GEO, said, “Our company delivered strong operational and financial performance in 2023, resulting in the second-best year in our company’s 40-year history. We believe that the unparalleled scope of our diversified services platform, which allows us to offer a full spectrum of innovative solutions to our government agency partners, gives GEO a unique competitive advantage to capture future quality growth opportunities. We are also pleased with the substantial progress we made in 2023 towards our objective of reducing our net debt, deleveraging our balance sheet, and positioning GEO to explore options to return capital to shareholders in the future. We believe that our disciplined allocation of capital to reduce debt, along with our demonstrated track record delivering strong and predictable annual cash flows, will meaningfully enhance value for our shareholders over time.”

Financial Guidance

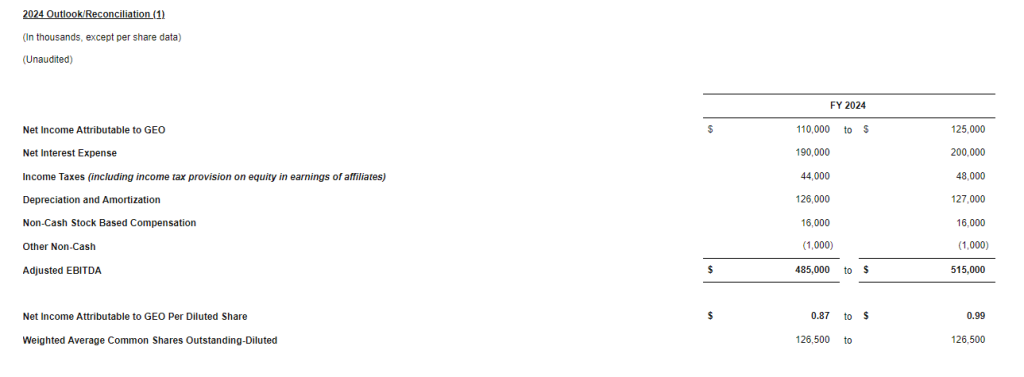

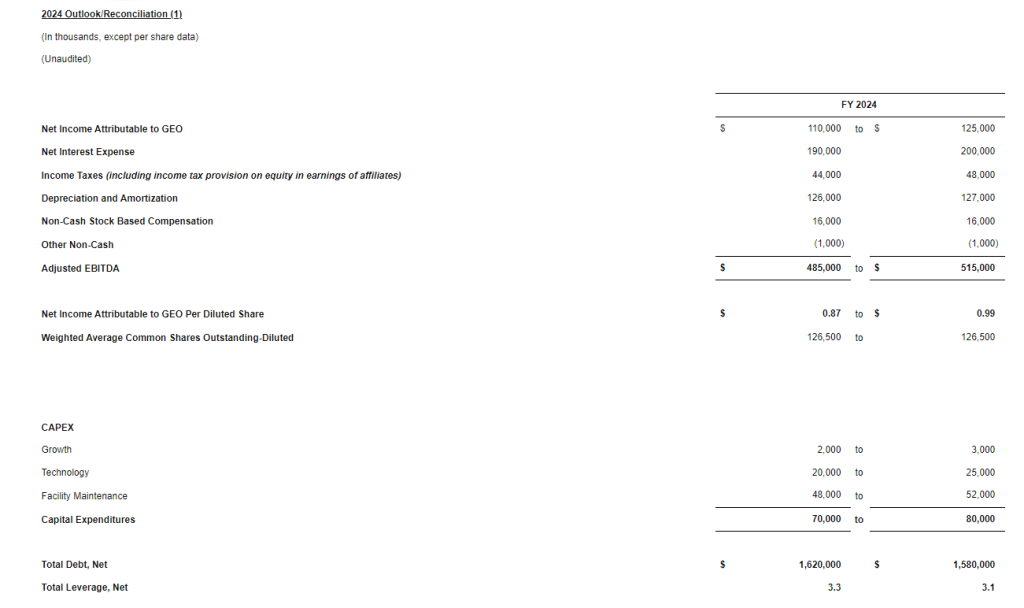

Today, we issued our initial financial guidance for 2024. For the full year 2024, we expect Net Income to be in a range of $110 million to $125 million on annual revenues of approximately $2.4 billion and reflecting an effective tax rate of approximately 28 percent, exclusive of any discrete items. We expect full year 2024 Adjusted EBITDA to be between $485 million and $515 million.

We believe that U.S. Immigration and Customs Enforcement (“ICE”) continues to face budgetary pressures, and the outcome and timing of ongoing federal government appropriations discussions in the United States Congress remain uncertain. As a result of these factors, our initial financial guidance for 2024 incorporates a range of assumptions.

The midpoint of our guidance range assumes stable populations across our ICE Processing Centers and stable participant counts under the federal government’s Intensive Supervision and Appearance Program (“ISAP”) contract. On the low end of our range, our guidance assumes that federal government appropriations discussions continue to be delayed throughout the year and that ongoing budgetary pressures result in some moderate decreased utilization of both ICE Processing Centers and the ISAP contract. On the high end of our range, our guidance assumes only some moderate increases in the utilization of ICE Processing Centers and the ISAP contract should additional funding be appropriated for ICE during this federal fiscal year.

Additionally, our initial 2024 guidance does not include the potential reactivation of any of our remaining idle Secure Services facilities, which total approximately 9,000 beds, or any potential new contract wins by our diversified business segments.

For the first quarter of 2024, we expect Net Income to be in a range of $22 million to $24 million and quarterly revenues in a range of $600 million to $610 million. We expect first quarter 2024 Adjusted EBITDA to be in a range of $117 million to $122 million. Compared to fourth quarter 2023, our first quarter 2024 guidance reflects the impact of having one fewer day in the quarter. Additionally, our first quarter of the year is impacted by higher costs related to payroll taxes, which are frontloaded in the beginning of each year.

Conference Call Information

We have scheduled a conference call and webcast for today at 11:00 AM (Eastern Time) to discuss our fourth quarter and full year 2023 financial results as well as our outlook. The call-in number for the U.S. is 1-877-250-1553 and the international call-in number is 1-412-542-4145. In addition, a live audio webcast of the conference call may be accessed on the Webcasts section under the News, Events and Reports tab of GEO’s investor relations webpage at investors.geogroup.com. A replay of the webcast will be available on the website for one year. A telephonic replay of the conference call will be available through February 22, 2024, at 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The participant passcode for the telephonic replay is 5397718.

About The GEO Group

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 100 facilities totaling approximately 81,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Reconciliation Tables and Supplemental Information

GEO has made available Supplemental Information which contains reconciliation tables of Net Income Attributable to GEO to Adjusted Net Income, and Net Income to EBITDA and Adjusted EBITDA, along with supplemental financial and operational information on GEO’s business and other important operating metrics. The reconciliation tables are also presented herein. Please see the section below titled “Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures” for information on how GEO defines these supplemental Non-GAAP financial measures and reconciles them to the most directly comparable GAAP measures. GEO’s Reconciliation Tables can be found herein and in GEO’s Supplemental Information available on GEO’s investor webpage at investors.geogroup.com.

Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures

Adjusted Net Income, EBITDA, and Adjusted EBITDA are non-GAAP financial measures that are presented as supplemental disclosures. GEO has presented herein certain forward-looking statements about GEO’s future financial performance that include non-GAAP financial measures, including Net Debt, Net Leverage, and Adjusted EBITDA. The determination of the amounts that are included or excluded from these non-GAAP financial measures is a matter of management judgment and depends upon, among other factors, the nature of the underlying expense or income amounts recognized in a given period.

While we have provided a high level reconciliation for the guidance ranges for full year 2024, we are unable to present a more detailed quantitative reconciliation of the forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because management cannot reliably predict all of the necessary components of such GAAP measures. The quantitative reconciliation of the forward-looking non-GAAP financial measures will be provided for completed annual and quarterly periods, as applicable, calculated in a consistent manner with the quantitative reconciliation of non-GAAP financial measures previously reported for completed annual and quarterly periods.

Net Debt is defined as gross principal debt less cash from restricted subsidiaries. Net Leverage is defined as Net Debt divided by Adjusted EBITDA.

EBITDA is defined as net income adjusted by adding provisions for income tax, interest expense, net of interest income, and depreciation and amortization. Adjusted EBITDA is defined as EBITDA adjusted for (gain)/loss on asset divestitures, pre-tax, net loss attributable to non-controlling interests, stock-based compensation expenses, pre-tax, transaction related expenses, pre-tax, one-time employee restructuring expenses, pre-tax, other non-cash revenue and expenses, pre-tax, and certain other adjustments as defined from time to time.

Given the nature of our business as a real estate owner and operator, we believe that EBITDA and Adjusted EBITDA are helpful to investors as measures of our operational performance because they provide an indication of our ability to incur and service debt, to satisfy general operating expenses, to make capital expenditures, and to fund other cash needs or reinvest cash into our business.

We believe that by removing the impact of our asset base (primarily depreciation and amortization) and excluding certain non-cash charges, amounts spent on interest and taxes, and certain other charges that are highly variable from year to year, EBITDA and Adjusted EBITDA provide our investors with performance measures that reflect the impact to operations from trends in occupancy rates, per diem rates and operating costs, providing a perspective not immediately apparent from net income.

The adjustments we make to derive the non-GAAP measures of EBITDA and Adjusted EBITDA exclude items which may cause short-term fluctuations in income from continuing operations and which we do not consider to be the fundamental attributes or primary drivers of our business plan and they do not affect our overall long-term operating performance.

EBITDA and Adjusted EBITDA provide disclosure on the same basis as that used by our management and provide consistency in our financial reporting, facilitate internal and external comparisons of our historical operating performance and our business units and provide continuity to investors for comparability purposes.

Adjusted Net Income is defined as net income attributable to GEO adjusted for certain items which by their nature are not comparable from period to period or that tend to obscure GEO’s actual operating performance, including for the periods presented (gain)/loss on asset divestitures, pre-tax, (gain)/loss on the extinguishment of debt, pre-tax, transaction related expenses, pre-tax, one-time employee restructuring expense, pre-tax, and tax effect of adjustments to net income attributable to GEO.

Safe-Harbor Statement

This press release contains forward-looking statements regarding future events and future performance of GEO that involve risks and uncertainties that could materially and adversely affect actual results, including statements regarding GEO’s financial guidance for the full year and first quarter of 2024, statements regarding GEO’s efforts to market its current idle facilities, GEO’s focus on reducing net debt, deleveraging its balance sheet, and positioning itself to explore options to return capital to shareholders, and GEO’s assumptions regarding the utilization of ICE Processing Centers and the ISAP contract during 2024. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” or “continue” or the negative of such words and similar expressions. Risks and uncertainties that could cause actual results to vary from current expectations and forward-looking statements contained in this press release include, but are not limited to: (1) GEO’s ability to meet its financial guidance for 2024 given the various risks to which its business is exposed; (2) GEO’s ability to deleverage and repay, refinance or otherwise address its debt maturities in an amount and on terms commercially acceptable to GEO, and on the timeline it expects or at all; (3) GEO’s ability to identify and successfully complete any potential sales of company-owned assets and businesses on commercially advantageous terms on a timely basis, or at all; (4) changes in federal and state government policy, orders, directives, legislation and regulations that affect public-private partnerships with respect to secure, correctional and detention facilities, processing centers and reentry centers, including the timing and scope of implementation of President Biden’s Executive Order directing the U.S. Attorney General not to renew the U.S. Department of Justice contracts with privately operated criminal detention facilities; (5) changes in federal immigration policy; (6) public and political opposition to the use of public-private partnerships with respect to secure correctional and detention facilities, processing centers and reentry centers; (7) any continuing impact of the COVID-19 global pandemic on GEO, GEO’s ability to mitigate the risks associated with COVID-19, and the efficacy and distribution of COVID-19 vaccines; (8) GEO’s ability to sustain or improve company-wide occupancy rates at its facilities in light of any continuing impact of the COVID-19 global pandemic and policy and contract announcements impacting GEO’s federal facilities in the United States; (9) fluctuations in GEO’s operating results, including as a result of contract terminations, contract renegotiations, changes in occupancy levels and increases in GEO’s operating costs; (10) general economic and market conditions, including changes to governmental budgets and its impact on new contract terms, contract renewals, renegotiations, per diem rates, fixed payment provisions, and occupancy levels; (11) GEO’s ability to address inflationary pressures related to labor related expenses and other operating costs; (12) GEO’s ability to timely open facilities as planned, profitably manage such facilities and successfully integrate such facilities into GEO’s operations without substantial costs; (13) GEO’s ability to win management contracts for which it has submitted proposals and to retain existing management contracts; (14) risks associated with GEO’s ability to control operating costs associated with contract start-ups; (15) GEO’s ability to successfully pursue growth and continue to create shareholder value; (16) GEO’s ability to obtain financing or access the capital markets in the future on acceptable terms or at all; and (17) other factors contained in GEO’s Securities and Exchange Commission periodic filings, including its Form 10-K, 10-Q and 8-K reports, many of which are difficult to predict and outside of GEO’s control.