Oil markets were thrown into turmoil on Wednesday after the OPEC+ alliance unexpectedly postponed a critical meeting to determine production levels. Prices promptly plunged over 5% as hopes for additional output cuts to stabilize crude markets were dashed, at least temporarily.

The closely-watched meeting was originally slated for December 3-4. But OPEC+, which includes the 13 member countries of the Organization of Petroleum Exporting Countries along with Russia and other non-members, said the summit would now take place on December 6 instead, offering no explanation for the delay.

The last-minute postponement fueled speculation that the group is struggling to build consensus around boosting production cuts aimed at reversing oil’s steep two-month slide. Disagreements apparently center on Saudi dissatisfaction with other nations flouting their output quotas. Compliance has emerged as a major flashpoint as oil revenue pressures intensify amid rising recession fears.

Prices Rally on Cut Hopes

In recent weeks, oil had rebounded from mid-October lows on mounting expectations that OPEC+ would intervene to tighten supply and put a floor under prices once more.

The alliance has already removed over 5 million barrels per day since 2023 through unilateral Saudi production cuts and collective OPEC+ reductions. But crude has continued drifting lower, with Brent plunging below $80 per barrel last week for the first time since January.

Demand outlooks have deteriorated significantly, especially in China where crude imports fell in October to their lowest since 2007. At the same time, releases from strategic petroleum reserves and resilient non-OPEC production have expanded inventories, exacerbating the supply glut.

Output Quotas Trigger Internal Rifts

Energy analysts widely anticipate that OPEC+ will finalize plans at next week’s rescheduled talks to extend existing production cuts until mid-2024. Saudi Arabia and Russia, the alliance’s de factor leaders, both support additional trims.

However, firming up commitments from the broader group may prove challenging. Crude exports are critical to the economies of many member nations. With government budgets squeezed by weakened prices, some countries have little incentive to curb production.

Unconfirmed reports suggest that Saudi Arabia demanded Iraq and several other laggards bolster compliance with quotas before it agrees to further output reductions. But getting all parties in line with their assigned targets has long confounded the alliance.

Where Oil Goes Next

For now, oil markets are in limbo awaiting next Thursday’s OPEC+ gathering. Prices could see added volatility until the cartel unveils its plans.

Most analysts still expect that additional cuts will emerge, possibly in the 500,000 barrels per day range. That may be enough to place a temporary floor under the market and keep Brent crude from approaching $70 per barrel.

But if internal dissent paralyzes OPEC+ from reaching an agreement, or one that falls significantly short of projections, another downward spiral is probable. Pressure would only escalate on the alliance to take more drastic actions to stabilize prices in 2024 as economic storm clouds gather.

In a watershed moment for cryptocurrency oversight, Changpeng Zhao, billionaire founder of crypto exchange Binance, pleaded guilty on Tuesday to charges related to money laundering and sanctions violations. Binance itself also pleaded guilty to similar criminal charges for failing to prevent illegal activity on its platform.

The guilty pleas are part of a sweeping, coordinated crackdown on Binance by U.S. law enforcement and regulators. As part of the settlement, Binance agreed to pay over $4 billion in fines and penalties to various government agencies. Zhao himself will personally pay $200 million in fines and has stepped down as CEO.

The implications of this development on the broader crypto sector could be profound. As the world’s largest crypto trading platform, Binance has played an outsized role in the growth of the industry. Its legal troubles and the record penalties imposed call into question the viability of exchanges that flout compliance rules in the name of rapid expansion.

Prosecutors allege that Binance repeatedly ignored anti-money laundering obligations and allowed drug traffickers, hackers, and even terrorist groups like ISIS to freely use its platform. According to the Department of Justice, Binance processed transactions for mixing services used to launder money and facilitated over 1.5 million trades in violation of U.S. sanctions.

U.S. authorities were unequivocal in their criticism of Binance’s focus on profits over meeting regulatory requirements. This suggests that other exchanges that aggressively pursued growth while turning a “blind eye” to compliance may face similar crackdowns in the future. The $3.4 billion civil penalty imposed on Binance also sets a benchmark for potential fines other non-compliant entities may confront.

The charges against the world’s largest crypto exchange and its high-profile leader represent federal authorities’ most aggressive action yet to rein in lawlessness in the cryptocurrency industry. Officials made clear they will continue targeting crypto companies that break laws around money laundering, sanctions evasion, and other illicit finance.

More broadly, CZ’s guilty plea underscores the pressing need for sensible guardrails if crypto is to shed its reputation as primarily facilitating illegal activity. Though blockchain technology offers many potential benefits, its pseudonymous nature makes it vulnerable to abuse by criminals and terrorists financing unless exchanges rigorously verify customer identities and the source of funds.

For the wider crypto sector, the Binance takedown may spur valuable change. Many experts argue overly lax regulation allowed crypto exchanges to ignore Anti-Money Laundering rules other financial institutions must follow. The billion-dollar penalties against Binance could convince the industry it’s cheaper to self-regulate.

The Binance case may accelerate calls for a regulatory framework tailored to the unique risks posed by cryptocurrencies. Rather than stifle innovation in this nascent industry, thoughtful policies around KYC, anti-money laundering, investor protections and other issues could instill greater confidence in cryptocurrencies among mainstream investors and financial institutions.

Of course, because cryptocurrency transactions are pseudonymous, crypto will likely remain appealing for certain unlawful activities like narcotics sales and ransomware. But with Binance’s guilty plea, regulators sent the message that flagrant non-compliance will not fly. Exchanges allowing outright criminal abuse may face existential legal threats.

For exchanges determined to operate legally, the Binance debacle highlights the existential risks of non-compliance. No matter how large or influential, exchanges that refuse to meet their regulatory responsibilities risk jeopardizing their futures. Expect most exchanges to immediately review their KYC and AML policies in the wake of the Binance penalties.

At minimum, the charges will likely damage Binance’s reputation. Although the company remains operational, it could lose market share to competitors perceived as more law-abiding. For crypto investors, the uncertainty and loss of trust surrounding such a dominant player create fresh volatility in already turbulent markets.

Perhaps most profoundly, seeing handcuffs slapped on crypto’s one-time “king” punctures the industry’s former aura of impunity. After the Binance takedown, ongoing federal probes into FTX and other exchanges, and Sam Bankman-Fried’s criminal conviction, crypto fraudsters might finally fear the consequences many avoided for so long. For better or worse, crypto is evolving.

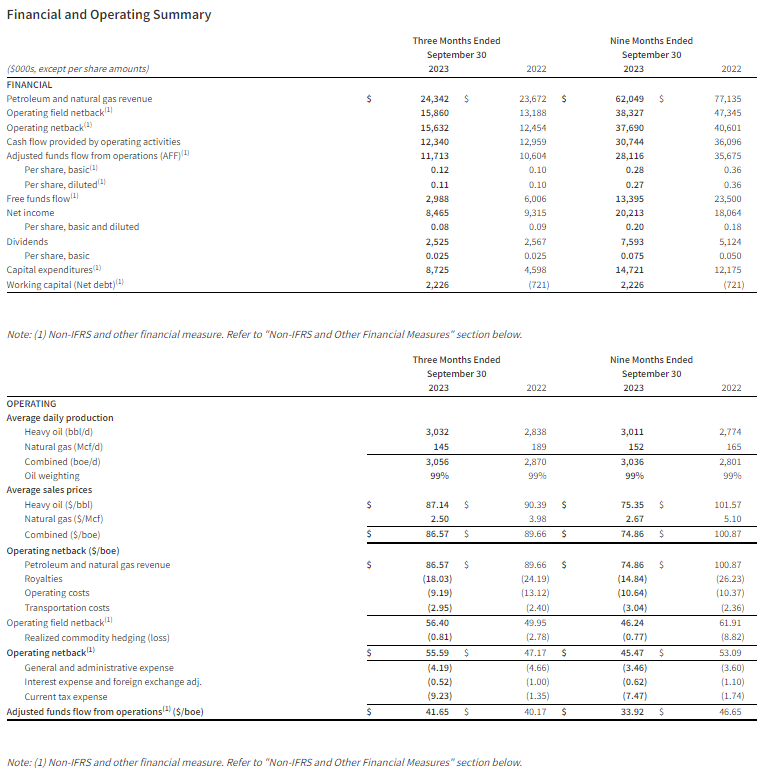

Vancouver, British Columbia–(Newsfile Corp. – November 21, 2023) – Hemisphere Energy Corporation (TSXV: HME)(OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the three and nine months ended September 30, 2023, announce the declaration of a quarterly dividend payment to shareholders, and provide an operations update.

Q3 2023 Highlights

Second best quarter in corporate history for production, revenue, operating field netback, and adjusted funds flow from operations (“AFF”)1.

Produced an average of 3,056 boe/d for the third quarter of 2023, a 6% increase over the same quarter last year.

Attained third quarter revenue of $24.3 million, a 3% increase over the third quarter last year.

Delivered an operating field netback1 of $15.9 million or $56.40/boe for the quarter.

Realized quarterly adjusted funds flow from operations (AFF) of $11.7 million or $41.70/boe.

Announced Hemisphere’s first ever special dividend to shareholders of $0.03 per common share ($3.0 million), paid on November 1, 2023.

Distributed $0.025 per common share ($2.5 million) in quarterly dividends to shareholders in accordance with the Company’s dividend policy.

Exited the third quarter of 2023 with a positive working capital1 position of $2.2 million, compared to net debt1 of $0.7 million at September 30, 2022.

Renewed the Company’s Normal Course Issuer Bid (“NCIB”).

Purchased and cancelled 519,400 shares under the Company’s NCIB during the third quarter (at an average price of $1.23 per common share).

(1) Operating field netback, adjusted funds flow from operations (AFF), free funds flow, working capital, and net debt are non-IFRS measures that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s Financial Statements and related Management’s Discussion and Analysis for the quarter ended September 30, 2023, which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend and Shareholder Return

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 28, 2023 to shareholders of record as of the close of business on December 15, 2023. The dividend is designated as an eligible dividend for income tax purposes.

With $13.1 million distributed through quarterly and special dividends by year-end and $3.7 million spent on NCIB year-to-date, a minimum of $16.8 million is anticipated to have been returned to shareholders in 2023. Based on the Company’s current market capitalization of $128 million (99.7 million shares issued and outstanding at market close price of $1.28 per share on November 20, 2023), this represents an annualized yield of 13% to Hemisphere’s shareholders.

Operations Update

During the third quarter, Hemisphere completed the majority of its planned 2023 capital expenditure program. By the end of September, the Company had brought on 7 new wells and completed one new well as an injector in the Atlee Buffalo area. Subsequent to quarter-end, the Company also shut one producing well in to convert it to an injector.

Current corporate production sits at approximately 3,350 boe/d (99% heavy oil, based on field estimates between October 1 – November 15, 2023). The Company’s assets continue to perform well under Enhanced Oil Recovery (“EOR”) with current corporate production almost 20% higher than full-year 2022 production, which was just over 2,800 boe/d. Operating and transportation costs during the first nine months of 2023 total just $13.68/boe, and are fully reflective of the chemical costs required for the Company’s two EOR projects. This makes Hemisphere one of the lowest cost operators of heavy oil in the Canadian oil industry.

Looking ahead into 2024, Hemisphere is actively preparing for a new pilot polymer flood on its recently acquired land base. Management anticipates that a test pad could be drilled and on production with a polymer skid installed by as early as July 2024. The Company expects to release more details on its 2024 guidance in January.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets using EOR techniques. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a dividend will be paid December 28, 2023 to shareholders of record as of the close of business on December 15, 2023; that a minimum of $16.8 million is anticipated to have been returned to shareholders in 2023; Hemisphere’s plans for a new pilot polymer flood on its recently acquired land base and the timing for test pad drilling, polymer skid installation, and production dates thereof; and timing for further details on its planned operations or guidance.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the effects of inflation of Hemisphere’s budgeted costs; the perspectivity of recently acquired properties and the timing and manner to explore and develop the same; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Market, Independent Third Party and Industry Data

This news release set forth Hemisphere’s belief with respect to being one of the lowest cost operators of heavy oil in the Canadian oil industry. Such statement is based, in part, on third party information, including from industry participant public filings or government or other independent industry publications and reports or based on estimates derived from such publications and reports. Government and industry publications and reports generally indicate that they have obtained their information from sources believed to be reliable, but Hemisphere has not conducted its own independent verification of such information. This news release also includes certain data derived from independent third parties. While Hemisphere believes this data to be reliable, market and industry data is subject to variations and cannot be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey. Hemisphere has not independently verified any of the data from independent third party sources referred to in this news release or ascertained the underlying assumptions relied upon by such sources.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, operating field netback and operating netback, capital expenditures and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe or share basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered to be more meaningful than IFRS measures in evaluating the Company’s performance.

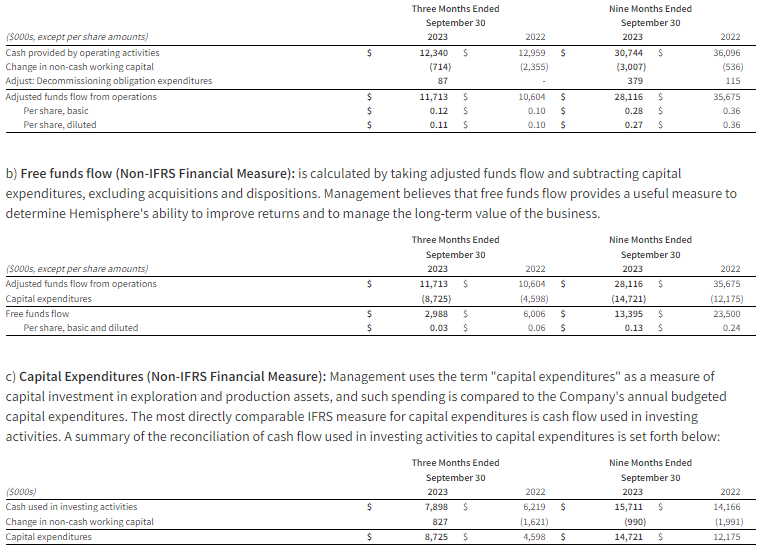

a) Adjusted funds flow from operations “AFF” (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): the Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures, and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period. AFF per boe is calculated by dividing AFF by the total production in boe for the reporting period.

A reconciliation of AFF to cash provided by operating activities is presented as follows:

d) Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): is a benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e) Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): calculated as the operating field netback plus the Company’s realized commodity hedging gain (loss) on an absolute and per barrel of oil equivalent basis.

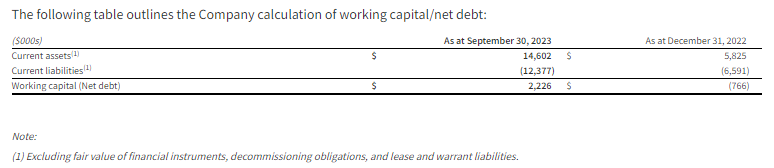

f) Working Capital/Net debt (Non-IFRS Financial Measure): is closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/Net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding the fair value of financial instruments, decommissioning obligations, and lease liabilities, and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

g)Supplementary Financial Measures and Non-GAAP Ratios

“Transportation costs per boe” is comprised of transportation expense, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2022 and the interim period ended September 30, 2023, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to production rates, which may include initial production rates for certain wells (including as a result of recent EOR activities), may be useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

Barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Despite growing fears of an impending recession, the Federal Reserve is showing no signs of pivoting towards interest rate cuts any time soon, according to minutes from the central bank’s early-November policy meeting.

The minutes underscored Fed officials’ steadfast commitment to taming inflation through restrictive monetary policy, even as markets widely expect rate cuts to begin in the first half of 2024.

“The fact is, the Committee is not thinking about rate cuts right now at all,” Fed Chair Jerome Powell asserted bluntly in his post-meeting press conference.

The summary of discussions revealed Fed policymakers believe keeping rates elevated will be “critical” to hit their 2% inflation target over time. And it gave no indication that the group even considered the appropriate timing for eventually lowering rates from the current range of 5.25-5.50%, the highest since 2000.

Despite investors betting on cuts starting in May, the minutes signaled the Fed intends to stand firm and base upcoming policy moves solely on incoming data, rather than forecasts. Officials stressed the need for “persistently restrictive” policy to curb price increases.

Still, Fed leaders acknowledged they must remain nimble in response to shifting financial conditions or economic trajectories that could alter the monetary path.

The minutes linked this upward pressure on benchmark yields to several key drivers, including increased Treasury issuance to finance swelling federal deficits.

Analysts say the Fed’s aggressive rate hikes are also forcing up yields on government bonds. Meanwhile, any hints around the Fed’s own policy outlook can sway rate expectations.

Fed participants decided higher term premiums rooted in fundamental supply and demand forces do not necessarily warrant a response. However, the reaction in financial markets will require vigilant monitoring in case yield spikes impact the real economy.

Moderating Growth, Elevated Inflation Still Loom

Despite the tightening already underway, the minutes paint a picture of an economy still battling high inflation even as growth shows signs of slowing markedly.

Participants expect a significant deceleration from the third quarter’s 4.9% GDP growth pace. And they see rising risks of below-trend expansion looking ahead.

The Fed’s preferred PCE inflation gauge has also moderated over recent months. But at 3.7% annually in September, it remains well above the rigid 2% target.

Considering lags in policy impacts, the minutes indicated Fed officials believe the cumulative effect of 375 basis points worth of interest rate hikes this year should help restore price stability over the medium term.

Markets Still Misaligned with Fed’s Outlook

Despite the Fed’s clear messaging, futures markets continue to forecast rate cuts commencing in the first half of 2023. Traders are betting on a recession forcing the Fed’s hand.

However, several Fed policymakers have recently pushed back on expectations for near-term policy pivots.

For now, the Fed seems inclined to stick to its guns, rather than bowing to market hopes or economic worries. With inflation still unacceptably high amid a strong jobs market, policymakers are staying the course on rate hikes for the foreseeable future, according to the latest minutes.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. The company reported $2.9 million in revenue, which was in-line with our estimate of $2.6 million. Adj. EBITDA loss of $1.4 million was modestly lower than our estimate of a loss of $0.8 million, as illustrated in Figure #1 Q3 Results. Notably, Q3 operating results were affected by less QVC programming due to talent scheduling conflicts related to a return to an in-studio production policy and non-recurring restructuring expenses.

Transition toward a licensing model. In November, the company completed a restructuring process by entering into licensing agreements for its Longaberger and made in the US baskets businesses. The new licensing model is expected to significantly lower operating costs and be a key catalyst toward a swing to positive cash flow in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Chipmaker Nvidia (NVDA) is slated to report fiscal third quarter financial results after Tuesday’s closing bell, with major implications for tech stocks as investors parse the numbers for clues about the artificial intelligence boom.

Heading into the print, Nvidia shares closed at an all-time record high of $504.09 on Monday, capping a momentous run over the last year. Bolstered by explosive growth in data center revenue tied to AI applications, the stock has doubled since November 2022.

Now, Wall Street awaits Nvidia’s latest earnings and guidance with bated breath, eager to gauge the pace of expansion in the company’s most promising segments serving AI needs.

Consensus estimates call for dramatic sales and profit surges versus last year’s third quarter results. But in 2022, Nvidia has made beating expectations look easy.

This time, another strong showing could validate nosebleed valuations across tech stocks and reinforce the bid under mega-cap names like Microsoft and Alphabet that have ridden AI fervor to their own historic highs this month.

By contrast, any signs of weakness threatening Nvidia’s narrative as an AI juggernaut could prompt the momentum-driven sector to stumble. An upside surprise remains the base case for most analysts. But with tech trading at elevated multiples, the stakes are undoubtedly high heading into Tuesday’s report.

AI Arms Race Boosting Data Center Sales

Nvidia’s data center segment, which produces graphics chips for AI computing and data analytics, has turbocharged overall company growth in recent quarters. Third quarter data center revenue is expected to eclipse $12.8 billion, up 235% year-over-year.

Strength is being driven by demand from hyperscale customers like Amazon Web Services, Microsoft Azure, and Alphabet Cloud racing to build out AI-optimized infrastructure. The intense competition has fueled a powerful upgrade cycle benefiting Nvidia.

Now, hopes are high that Nvidia’s next-generation H100 processor, unveiled in late 2021 and ramping production through 2024, will drive another leg higher for data center sales.

Management’s commentary around H100 adoption and trajectory will help investors gauge expectations moving forward. An increase to the long-term target for overall company revenue, last quantified between $50 billion and $60 billion, could also catalyze more upside.

What’s Next for Gaming and Auto?

Beyond data center, Nvidia’s gaming segment remains closely monitored after a pandemic-era boom went bust in 2022 amid fading consumer demand. The crypto mining crash also slammed graphics card orders.

Gaming revenue is expected to grow 73% annually in the quarter to $2.7 billion, signaling a possible bottom but well below 2021’s peak near $3.5 billion. Investors will watch for reassurance that the inventory correction is complete and gaming sales have stabilized.

Meanwhile, Nvidia’s exposure to AI extends across emerging autonomous driving initiatives in the auto sector. Design wins and partnerships with electric vehicle makers could open another massive opportunity. Updates on traction here have the potential to pique further interest.

Evercore ISI analyst Julian Emanuel summed up the situation: “It’s still NVDA’s world when it comes to [fourth quarter] reports – we’ll all just be living in it.”

In other words, Nvidia remains the pace-setter steering tech sector sentiment to kick off 2024. And while AI adoption appears inevitable in the long run, the market remains keenly sensitive to indications that roadmap is progressing as quickly as hoped.

Pharmaceutical giant Merck announced Tuesday that it will acquire Caraway Therapeutics, a preclinical biotech company pursuing novel approaches to treating genetically defined neurodegenerative and rare diseases. The deal reflects Merck’s ongoing commitment to developing much-needed disease-modifying therapies for progressive brain conditions.

Under the agreement, Merck will make an upfront payment to obtain Caraway, followed by additional milestone payments contingent upon the progress of certain Caraway pipeline assets. Though financial terms were not disclosed, the total potential consideration could reach up to $610 million.

“Caraway’s multidisciplinary approach has yielded important progress in evaluating novel mechanisms of modulation of lysosomal function with potential for the treatment of progressive neurodegenerative diseases,” said George Addona, Merck’s head of discovery. “We look forward to applying our expertise to build upon this work with the goal of developing much needed disease-modifying therapies for these conditions.”

Unlike symptomatic treatments, disease-modifying therapies aim to directly impact underlying disease processes and ultimately alter the course of a condition’s progression. This has remained an elusive goal for brain diseases like Alzheimer’s and Parkinson’s.

Caraway’s work targets dysfunctions in cellular “recycling” processes that clear toxic materials from the brain. Its treatments stimulate lysosomes, which act as cell disposal units, to boost their activity. Researchers believe a boost in waste clearance could counter neurodegeneration.

Merck has been an investor in Caraway since 2018 through its venture capital arm MRL Ventures Fund. Now, by folding Caraway’s team and portfolio into its research labs, Merck aims to leverage its considerable drug development capabilities to advance lysosomal modulation treatments for neurodegeneration.

“This is a testament to the hard work and dedication of the Caraway team and our mission to develop therapeutics with the potential to alter the progression of devastating neurodegenerative diseases and help patients,” said Caraway CEO Martin D. Williams in a statement. “This acquisition leverages Merck’s industry-leading research and development capabilities to help further advance our discovery and preclinical programs.”

Alongside Merck, Caraway has been backed by several high-profile life sciences investors including SV Health Investors, AbbVie Ventures, Amgen Ventures, and Eisai Innovation.

An Urgent Need for Better Brain Treatments

Currently available medications can only manage symptoms for a period of time for Alzheimer’s, Parkinson’s, and related neurodegenerative diseases. None treat underlying pathologies or substantially slow worsening cognition and functionality.

Alzheimer’s alone impacts more than 6 million Americans and the prevalence is expected to triple in the next 30 years if no new treatments emerge. Experts have emphasized the urgent need for innovations.

Major players in the pharmaceutical industry have confronted disappointed late-stage clinical trial results among proposed Alzheimer’s treatments over the past decade, suffering high-profile setbacks.

Yet Merck’s buy-in suggests promise still exists in Caraway’s early-stage lysosomal modulation approach, even though treatments haven’t advanced to human testing yet. Merck aims to apply its extensive expertise to push potential therapies over the finish line where others have stumbled before.

Continuing a Neuroscience Focus

Alongside this deal, Merck continues to expand its research across neurodegenerative diseases in other ways. Thus far in 2023, Merck has also entered into research collaborations to pursue non-amyloid targets for Alzheimer’s and chiral chemistry for better brain penetrance among compounds targeting neurological conditions.

“The alignment with Caraway’s innovative science and focus on elucidating disease-modifying neurotherapeutics dovetails nicely with our ongoing work,” said Addona.

Overall, Merck’s acquisition of Caraway signals both increasing momentum around emerging theories of neurodegeneration—like waste clearance’s role—and a formidable commitment by the pharma organization to translating the latest science into paradigm-shifting treatments for patients.

HOUSTON, Nov. 20, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today announced that management will participate in the Noble Capital Markets 19th Annual Emerging Growth Equity Conference on December 3-5, 2023 at Florida Atlantic University in Boca Raton, FL.

The conference will consist of one-on-one and small group meetings providing investors the opportunity to hear from and meet with Direct Digital Holdings’ management team. For more information, or to schedule a meeting with management, please contact your Noble representative.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses, and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The Company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Year-to-date, Direct Digital Holdings’ sell- and buy-side solutions have managed on average over 125,000 clients monthly, generating over 300 billion impressions per month across display, CTV, in-app and other media channels.

Microsoft emerged victorious in the artificial intelligence talent wars by hiring ousted OpenAI CEO Sam Altman and other key staff from the pioneering startup. This coup ensures Microsoft retains exclusive access to OpenAI’s groundbreaking AI technology for its cloud and Office products.

OpenAI has been a strategic partner for Microsoft since 2019, when the software giant invested $1 billion in the nonprofit research lab. However, the surprise leadership shakeup at OpenAI late last week had sparked fears that Microsoft could lose its AI edge to hungry rivals.

Hiring Altman and other top OpenAI researchers nullifies this threat. Altman will lead a new Microsoft research group developing advanced AI. Joining him from OpenAI are co-founder Greg Brockman and key staff like Szymon Sidor.

The poaching also prevents Altman from jumping ship to competitors, according to analysts. “If Microsoft lost Altman, he could have gone to Amazon, Google, Apple, or a host of other tech companies,” said analyst Dan Ives of Wedbush Securities. “Instead he is safely in Microsoft’s HQ now.”

OpenAI Turmoil Prompted Microsoft’s Bold Move

The impetus for Microsoft’s talent grab was OpenAI’s messy leadership shakeup last week. Altman and other executives were reportedly forced out by OpenAI board chair.

The nonprofit recently created a for-profit subsidiary to commercialize its research. This entity was prepping for a share sale at an $86 billion valuation that would financially reward employees. But with Altman’s ouster, these lucrative payouts are now in jeopardy.

This uncertainty likely prompted top OpenAI staff to leap to the stability of Microsoft. Analysts believe more employees could follow as doubts grow about OpenAI’s direction under Emmett Shear.

Microsoft’s infrastructure and resources also make it an attractive home. The tech giant can provide the enormous computing power needed to develop ever-larger AI models. OpenAI’s latest system, GPT-3, required 285,000 CPU cores and 10,000 GPUs to train.

By housing OpenAI’s brightest minds, Microsoft aims to supercharge its AI capabilities across consumer and enterprise products.

The Rise of AI and Competition in the Cloud

Artificial intelligence is transforming the technology landscape. AI powers everything from search engines and digital assistants to facial recognition and self-driving cars.

Tech giants are racing to lead this AI revolution, as it promises to reshape industries and create trillion-dollar markets. This battle spans hardware, software and talent acquisition.

Microsoft trails category leader Google in consumer AI, but leads in enterprise applications. Meanwhile, Amazon dominates the cloud infrastructure underpinning AI development.

Cloud computing and AI are symbiotic technologies. The hyperscale data centers operated by Azure, AWS and Google Cloud provide the computational muscle for AI training. These clouds also allow companies to access AI tools on-demand.

This has sparked intense competition between the “Big 3” cloud providers. AWS currently has 33% market share versus 21% for Azure and 10% for Google Cloud. But Microsoft is quickly gaining ground.

Hiring Altman could significantly advance Microsoft’s position. His team can create exclusive AI capabilities that serve as a differentiator for Azure versus alternatives.

Microsoft’s Prospects in AI and the Stock Market

Microsoft’s big OpenAI poach turbocharged its already strong prospects in artificial intelligence. With Altman on board, Microsoft is better positioned than any rival to lead the next wave of AI innovation.

This coup should aid Microsoft’s fast-growing cloud business. New AI tools could help Microsoft chip away at AWS’s dominance while holding off Google Cloud.

If Microsoft extends its edge in enterprise AI, that would further boost revenue and earnings. This helps explain Wall Street’s positive reaction lifting Microsoft’s stock 1.5% and adding $30 billion in market value.

The success of cloud and AI has fueled Microsoft’s transformation from a stagnant also-ran to a Wall Street darling. Its stock has nearly tripled since early 2020 as earnings rapidly appreciate thanks to its cloud and subscription-based revenue.

Microsoft stock trades at a reasonable forward P/E of 25 and offers a dividend yield around 1%. If Microsoft keeps leveraging AI to expand its cloud business, its stock could have much further to run.

Hiring Altman and deploying OpenAI’s technology across Microsoft’s vast resources places a momentous technology advantage within the company’s grasp. Realizing this potential would be a major coup for Satya Nadella as CEO. With OpenAI’s crown jewels now safely in house, Microsoft’s tech lead looks more secure than ever.

Haynes International, Inc. is a leading developer, manufacturer and marketer of technologically advanced, nickel and cobalt-based high-performance alloys, primarily for use in the aerospace, industrial gas turbine and chemical processing industries.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and fiscal year 2023 financial results. Haynes reported fourth-quarter net income of $13.1 million or $1.02 per share compared to $16.3 million or $1.30 per share during the prior year period. Fiscal year 2023 net income was $42.0 million or $3.26 per share compared to $45.1 million or $3.57 per share during the prior period. We had forecast fourth quarter and fiscal year 2023 net income of $12.4 million and $41.1 million, respectively, or $0.97 per share and $3.22 per share. Compared to the prior year periods, fourth quarter and fiscal year net revenues increased by 11.7% and 20.3%, respectively, to $160.6 million and $590.0 million. On a year-over-year basis, the product average selling price during the fourth quarter and fiscal year increased 11.5% and 14.9%, respectively. Fiscal year 2023 adjusted EBITDA increased to $79.0 million compared to $77.4 million in fiscal year 2022.

Updating estimates. While our 2024 EPS estimate remains $4.50, we have made some quarterly adjustments. Revenue and earnings in the first quarter of fiscal 2024 are expected to be higher compared to the first quarter of fiscal 2023, but lower than the fourth quarter of fiscal 2023. First quarter results are generally lower due to holidays and planned equipment maintenance. Additionally, management expects commodity price fluctuations to have a greater negative impact in the first quarter of fiscal 2024 than in the fourth quarter of fiscal year 2023. We project fiscal 2024 EBITDA of $100.3 million compared to our $104.3 million estimate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Business. Last week, CoreCivic announced two additional management contracts, continuing the momentum exhibited since September. Significantly, the new business is with states and counties, two areas of focus for CoreCivic for growth. We believe the recent contract wins demonstrate both strong contracting progress and the high levels of interest in the Company’s services from governmental partners. Notably, utilizing existing bed inventory will help drive margin improvement at CoreCivic.

Wyoming. CoreCivic entered into a new management contract with the state of Wyoming for the housing of up to 240 male inmates at the Company’s 2,672-bed Tallahatchie County Correctional Facility in Tutwiler, Mississippi. The Company previously housed inmates for Wyoming under a management contract that had not been utilized since 2019. The term of the new contract runs through June 30, 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Treasury Secretary Janet Yellen recently pointed to persistently high food and rent prices as a major reason why public perception of the economy remains negative, despite progress on overall inflation. With President Biden’s reelection chances closely tied to economic views, this consumer disconnect poses a threat.

In an interview with CNBC, Yellen acknowledged inflation rates have meaningfully declined from last year’s 40-year highs. However, she noted that “Americans still see increases in some important prices, including food, from where we were prior to the pandemic.”

While the administration touts top-line statistics pointing to economic strength, Yellen admitted that “this remains notable to people who go to the store and shop.”

Rent inflation also sticks out painfully to consumers, even as broader price growth cools. “Rents are rising less quickly now, but are certainly higher than they were before the pandemic,” Yellen said.

Polls Reveal Sour Public Mood Despite “Bidenomics”

This stubborn inflation in highly visible categories is clashing with the White House’s rosier messaging. The administration has dubbed the economy “Bidenomics” and trumpets metrics like robust job gains.

But almost 60% of voters disapprove of Biden’s economic leadership in the latest polling. His approval rating lags the economic data as people feel pinched by prices at the grocery store and housing costs.

Per Yellen, the disconnect boils down to prices remaining “higher than they used to be accustomed to.” She stressed the administration must now “explain to Americans what President Biden has done to improve the economy.”

Yellen expressed optimism views will shift “as inflation comes down, prices stop rising, and the labor market remains strong.” Time will tell if this turnaround happens soon enough to impact the 2024 election.

Food Prices Remain a Stinging Reminder of Inflation’s Sting

Of all consumer goods, food prices stand out as a persistent driver of inflation angst. Grocery bills grew 12% year-over-year in October, far above the 7.7% overall inflation rate. From eggs to lunch meats, few foods escape sticker shock at the store.

Russia’s invasion of Ukraine damaged vital grain supplies, resulting in huge price spikes for wheat, corn and cooking oils. Lingering supply chain dysfunction continues hampering food transport and packaging.

Restaurants also face higher food costs, which owners pass along through bigger menu price tags. Rising labor costs further squeeze restaurant margins.

In all, grocery and dining prices have become stinging daily reminders that inflation remains an economic burden. This clouds public sentiment despite falling gas prices and cheaper consumer goods.

Rents and Housing Costs Also Weigh Heavily on Consumers

Along with food, Yellen called out persistent rent inflation as a culprit of economic gloom. Annual rent growth sits around 7%, down from last year but still squeezing household budgets.

Low rental vacancy rates give landlords continued pricing power in many markets. While mortgage rates have shot higher, rents have yet to meaningfully slow for lack of alternatives.

Surging rents are especially painful due to housing’s outsize impact on living costs. One report estimated that housing accounts for 40% of a typical family’s inflation burden.

Beyond rent, housing costs like property taxes, homeowner insurance, and home services are also outpacing overall inflation. And higher mortgage rates make buying a home even less affordable.

These housing stresses help explain why such a large majority of Americans still rate current economic conditions as poor. With shelter eating up more paychecks, consumers feel deprived despite broader progress.

All Eyes on Food and Housing Costs as Midterms Approach

Yellen made clear that stubborn inflation in categories like food and rent is the administration’s biggest obstacle to touting economic gains. As President Biden gears up for a likely 2024 reelection bid, perceptions of the economy will carry substantial weight.

Democrats are hoping the public mood brightens as the impact of cooling prices materializes. But that remains uncertain with high-visibility costs still stinging consumers.

If relief arrives soon across grocery aisles and rent rolls, voters may yet reward President Biden and Democrats for delivering an overdue inflation reprieve. But the clock is ticking with the 2024 campaign cycle fast approaching.

For now, Biden’s political fate remains tied to the cost of bread and monthly housing bills. If lidding inflation can make such necessities feel affordable again, the president may stand to benefit.

BRENTWOOD, Tenn., Nov. 16, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (“CoreCivic”) announced today it signed a new management contract with the state of Wyoming for the housing of up to 240 male inmates at the Company’s 2,672-bed Tallahatchie County Correctional Facility in Tutwiler, Mississippi. We previously housed inmates for Wyoming under a management contract that had not been utilized since 2019. The term of the new contract runs through June 30, 2026.

Additionally, CoreCivic signed a new management contract with Harris County, Texas, to house up to 360 male inmates at the Tallahatchie County Correctional Facility. Upon mutual agreement, the County may access an additional 360 beds at the Tallahatchie facility. The initial contract term begins on December 1, 2023, and ends November 30, 2024. The contract may be extended at the County’s option for four additional one-year terms.

Since September 2023, CoreCivic has added contracts with the State of Montana at the Saguaro Correctional Facility as well as with Hinds County (MS), Harris County (TX), and the State of Wyoming at the Tallahatchie County Correctional Facility. CoreCivic anticipates the combined annual revenue of these four contacts to be approximately $25 million.

Damon T. Hininger, President and Chief Executive Officer commented, “We are honored to once again assist the Wyoming Department of Corrections with their correctional needs, and believe this contract demonstrates the essential solutions that we provide to federal, state, and local government agencies. Harris County is a new partnership for CoreCivic, and we look forward to providing the County with a flexible capacity solution.”

Hininger continued, “These new contracts further reinforce the versatility of our real estate assets. Utilizing existing bed inventory is key to driving margin improvement at CoreCivic. These recent contract wins demonstrate both strong contracting progress and the high levels of interest in our services and assets from existing and new governmental partners.”

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice, or DOJ, not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, impacting utilization primarily by the Federal Bureau of Prisons and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) the impact resulting from the termination of Title 42, the federal government’s policy to deny entry at the United States southern border to asylum-seekers and anyone crossing the southern border without proper documentation or authority in an effort to contain the spread of the coronavirus and related variants, or COVID-19; (vii) government budget uncertainty, the impact of the debt ceiling and the potential for government shutdowns and changing funding priorities; (viii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (ix) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (x) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

Contact:

Investors: Michael Grant – Managing Director, Investor Relations – (615) 263-6957 Financial Media: David Gutierrez, Dresner Corporate Services – (312) 780-7204