Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results. The company reported Q1 revenue of €64.4 million and adj. EBITDA of €6.0 million, both of which surpassed our estimates of €59.0 million and €2.7 million, respectively. Notably, revenue was up 13% YoY, driven by strong growth in Mexico and Spain, both of which increased average monthly users over the prior year period.

Solid fundamentals. Notably, in Q1, the company benefited from strong activity in Mexico, which generated revenue of €34.6 million, up 13% YoY. The favorable performance in Mexico was supported by 98,000 average monthly users, up 20% YoY. Additionally, Spain performed strongly, with revenue growing 16% to €25.5 million and average monthly users reaching 59,000, up 13% YoY. On a consolidated basis, the company averaged 183,000 monthly active users, up 14% YoY.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Rocket Lab USA (Nasdaq: RKLB) extended one of the more remarkable two-day runs in the commercial space sector on Monday, adding another 14% gain on top of Friday’s 30% surge following a blowout first quarter earnings report. The back-to-back move pushed shares to a new all-time high and left the stock up 70% on the year — a return that reflects both the strength of the company’s underlying business and a wave of investor enthusiasm for the commercial space sector being driven by the looming SpaceX IPO.

The earnings report that ignited Friday’s move was genuinely strong across every metric that matters for a company at Rocket Lab’s stage. First quarter revenue came in at $200.3 million, a 63.5% year-over-year increase, on a loss per share of $0.07 — a penny better than analyst expectations. Second quarter guidance was set at $232.5 million at the midpoint, approximately 12% above what the Street had modeled. For a company still burning cash as it scales toward profitability, the combination of accelerating revenue growth and a beat-and-raise quarter is exactly what investors needed to see.

The backlog figures are where the story gets particularly compelling. Total backlog reached $2.2 billion — up 20% in a single quarter and up 108% year-over-year. CEO Peter Beck disclosed that Rocket Lab booked 31 Electron and HASTE rocket missions during Q1, the most ever signed in a single quarter, bringing total launches in backlog across those programs to more than 70. The company also signed five new dedicated launches for Neutron, its larger next-generation rocket currently in development. A backlog growing at three-digit rates year-over-year is not a company running out of demand — it is a company struggling to build supply fast enough to meet it.

The business wins extend well beyond launch contracts. Rocket Lab was selected alongside defense contractor RTX to support the Department of Defense’s Space Based Interceptor program — providing both launch and satellite technology as part of President Trump’s Golden Dome missile defense initiative. That contract positions Rocket Lab squarely in the defense-space convergence that has been one of the most significant and durable spending tailwinds in the sector. The company also announced plans to acquire Motiv Space Systems, a robotics firm whose technology has been deployed on NASA Mars rover missions — a move that adds in-space robotics capabilities to Rocket Lab’s already expanding portfolio.

All of this is unfolding against a backdrop of accelerating investor interest in the commercial space sector broadly, catalyzed by the anticipated SpaceX IPO — expected as early as June 2026. SpaceX is not yet publicly traded, which means Rocket Lab has functioned as the go-to pure-play proxy for investors who want direct exposure to the commercial launch market. As SpaceX’s IPO timeline comes into focus, capital has been flooding into RKLB and adjacent names in anticipation.

The key question from here is whether the fundamentals can keep pace with the valuation expansion. At 70% year-to-date with all-time highs on the board, Rocket Lab is no longer a deeply discounted bet on an unproven business. It is a high-momentum, high-expectation growth story that will need continued execution — on Neutron development, defense contract delivery, and the Motiv integration — to justify where the market has taken it.

For small and microcap investors who have been in RKLB since its earlier, less recognized days: this is what the patient capital trade looks like when it works.

Significant New Business Wins and Contract Renewals Realized Merger Synergies of $2.6 Million (1)

OLD GREENWICH, Conn., May 11, 2026 (GLOBE NEWSWIRE) — Star Equity Holdings, Inc. (Nasdaq: STRR and STRRP) (“Star” or the “Company”), a diversified holding company, announced today financial results for the first quarter ended March 31, 2026.

2026First Quarter Summary

Revenue of $50.1 million increased 57.1% from the first quarter of 2025.

Gross profit $20.6 million increased 25.4% from the first quarter of 2025.

Net loss attributable to common shareholders was $4.4 million, or $1.17 per diluted share, compared to net loss attributable to common shareholders of $1.8 million, or $0.59 per diluted share, for the first quarter of 2025. Adjusted net loss per diluted share (non-GAAP measure)* was $0.99 compared to adjusted net loss per diluted share of $0.38 in the first quarter of 2025. Pro forma adjusted net loss per diluted share was $0.22 in the first quarter of 2025.

Adjusted EBITDA loss (non-GAAP measure)* increased to $1.6 million versus adjusted EBITDA loss of $0.7 million in the first quarter of 2025; pro forma adjusted EBITDA loss was $1.2 million in the first quarter of 2025.

Total cash including restricted cash was $10.3 million at March 31, 2026.

Jeff Eberwein, CEO of Star, noted, “The first quarter is almost always our weakest quarter of the year and in this year’s first quarter, startup delays for new projects and broader macroeconomic conditions caused our Building Solutions and Business Services divisions to perform worse than expected. Our Energy Services division, however, maintained solid momentum. We believe our focus on operational and cost improvements and continued investments in growth and innovation are strengthening our competitive position and will drive significantly improved results as the year progresses.”

Jake Zabkowicz, Global CEO of Hudson Talent Solutions (“HTS”), added, “Gross profit increased 6.4% at HTS year-over-year, reflecting steady improvement despite continued macroeconomic uncertainty and sustained pressure in the talent market. We have maintained a strong focus on innovation and operational efficiency, including the expanded deployment of agentic AI solutions to enhance recruiter productivity, improve candidate matching, and deliver greater value to clients. These efforts are helping our ability to navigate the current environment while positioning us to capitalize on improving market conditions in the future. As an example, new business activity and contract renewals with legacy clients accelerated meaningfully in the first quarter of 2026, exceeding levels seen in any quarter of 2025.”

1 $2.6 million of synergies on an annualized basis. Please reference slide 4 of Star’s Q1 earnings call presentation.

Rick Coleman, COO of Star, added, “Residential and commercial construction markets remained soft in the first quarter causing our Building Solutions division to perform below internal expectations, primarily due to delays in several pending contract awards and severe winter weather in both of our key geographies. However, underlying demand remains intact, as evidenced by recently secured new business, including the $4.2 million multifamily housing project in New Hampshire for our KBS business we announced on April 30, 2026. In contrast, our Energy Services division delivered a strong quarter, continuing to gain share across core markets, with particularly strong performance in mining and geothermal end markets.”

Mr. Eberwein concluded, “We remain focused on disciplined execution, rigorous cost management, and prudent capital allocation, including the active evaluation of M&A opportunities across all three of our operating divisions, as we continue to advance our strategic priorities. We believe we are well positioned to navigate near-term market volatility while driving increased profitability and long-term shareholder value.”

* The Company provides non-GAAP measures as a supplement to financial results based on accounting principles generally accepted in the United States (“GAAP”). Adjusted EBITDA, EBITDA, adjusted net income or loss, and adjusted net income or loss per diluted share are defined in the division / segment tables at the end of this release and a reconciliation of such non-GAAP measures to the most directly comparable GAAP measures is included within such division / segment tables.

Division Highlights

Building Solutions

First quarter Building Solutions revenue was $11.6 million and gross profit was $1.6 million. Adjusted EBITDA loss was $0.9 million.

Pro forma (“PF”)(1) Building Solutions revenue was $12.1 million for the first quarter of 2025, and PF gross profit was $2.9 million. PF adjusted EBITDA was $0.3 million.

Building Solutions quarter-end backlog was $8.0 million, and the trailing 12-month book-to-bill ratio was 0.72.

Business Services

First quarter 2026 Business Services revenue was $35.0 million, up from $31.9 million in the prior year quarter, while gross profit was $17.4 million, up from $16.4 million a year ago. Business Services adjusted EBITDA loss was $0.3 million, down from adjusted EBITDA of $0.2 million in the prior year quarter.

Regionally, Americas and EMEA gross profit grew 21% and 11%, respectively. This growth was partially offset by APAC, where gross profit declined by 8%.

Energy Services

First quarter 2026 Energy Services revenue was $3.5 million. Gross profit was $1.5 million. Energy Services adjusted EBITDA was $1.0 million in the first quarter.

PF Energy Services revenue for the first quarter of 2025 was $2.6 million and PF gross profit was $1.3 million. First quarter 2025 PF adjusted EBITDA was $0.5 million.

(1) Pro forma Building Solutions, Energy Services, and Investments results for the full first quarter of 2025. Alliance Drilling Tools was acquired by Star Operating Companies on March 3, 2025.

Corporate Costs

In the first quarter of 2026, the Company’s corporate costs were $1.9 million, up from $0.9 million in the prior year quarter, but down $0.7 million on a PF basis. Corporate costs in the first quarter of 2026 and 2025 excluded non-recurring expenses of $0.2 million and $0.3 million, respectively. The decrease in corporate costs was primarily driven by the Merger.

Liquidity and Capital Resources

The Company ended the first quarter of 2026 with $10.3 million in cash, including $2.2 million in restricted cash. The Company used $1.4 million in cash flow from operations during the first quarter of 2026 compared to using $0.8 million in cash flow from operations in the first quarter of 2025.

Share Repurchase Program

In the first quarter of 2026, the Company repurchased 70,424 shares for approximately $0.7 million As of the end of the first quarter of 2026, the Company has approximately $1.8 million remaining under its $3 million repurchase program authorized in September 2025 and continues to view share repurchases as an attractive use of capital.

NOL Carryforward

As of December 31, 2025, Star had $215 million of usable net operating losses (“NOL”) in the U.S., which the Company considers to be a very valuable asset for its stockholders. In order to protect the value of the NOL for all stockholders, the Company has a rights agreement and charter amendment in place that limit beneficial ownership of Star common stock to 4.99%. Stockholders who wish to own more than 4.99% of Star common stock, or who already own more than 4.99% of Star common stock and wish to buy more, may only acquire additional shares with the Board’s prior written approval.

Conference Call/Webcast

The Company will conduct a conference call on Tuesday, May 12, 2026 at 10:00 a.m. ET to discuss this announcement. Individuals wishing to listen can access the webcast on the investor information section of the Company’s web site at www.starequity.com.

If you wish to join the conference call, please use the dial-in information below:

Toll-Free Dial-In Number: (833) 890-6161

International Dial-In Number: (412) 504-9848

The archived call will be available on the investor relations section of the Company’s website at www.starequity.com.

About Star Equity Holdings, Inc. Star Equity Holdings, Inc. is a diversified holding company that seeks to build long-term shareholder value by acquiring, managing, and growing businesses with strong fundamentals and market opportunities. Its current structure comprises four divisions: Building Solutions, Business Services, Energy Services, and Investments. For more information visit www.starequity.com.

On August 22, 2025, the Company completed its previously announced acquisition of Star Operating Companies, Inc. (“Star Operating”, formerly known as Star Equity Holdings, Inc.), pursuant to the Agreement and Plan of Merger, dated as of May 21, 2025 (the “Merger Agreement”), by and among the Company, Star Operating and HSON Merger Sub, Inc., a wholly owned subsidiary of the Company (“Merger Sub”). Upon the terms and subject to the conditions of the Merger Agreement, on August 22, 2025, at the effective time of the merger pursuant to the Merger Agreement (the “Merger”), Merger Sub merged with and into Star Operating, with Star Operating continuing as the surviving corporation of the Merger as a wholly owned subsidiary of the Company. Effective September 5, 2025, the Company changed (i) its name to Star Equity Holdings, Inc. and (ii) its trading symbols on Nasdaq to STRR and STRRP.

Building Solutions The Building Solutions division operates in three specialties: (i) modular building manufacturing; (ii) structural wall panel and wood foundation manufacturing, including building supply distribution operations; and (iii) glue-laminated timber (glulam) column, beam, and truss manufacturing.

Business Services The Business Services division provides flexible and scalable recruitment solutions to a global clientele, servicing organizations at all levels, from entry-level positions to the C-suite. The division focuses on mid-market and enterprise organizations worldwide, partnering consultatively with talent acquisition, HR, and procurement leaders to build diverse, high-impact teams and drive business success.

Energy Services The Energy Services division engages in the rental, sale, and repair of downhole tools used in the oil and gas, geothermal, mining, and water-well industries.

Investments The Investments division manages and finances the Company’s real estate assets as well as its investment positions in private and public companies.

Investor Relations: The Equity Group Lena Cati (212) 836-9611 [email protected]

Forward-Looking Statements

This press release contains statements that the Company believes to be “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact included in this press release, including statements regarding the Company’s future financial condition, results of operations, business operations and business prospects, are forward-looking statements. Words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “predict,” “believe,” and similar words, expressions, and variations of these words and expressions are intended to identify forward-looking statements. All forward-looking statements are subject to important factors, risks, uncertainties, and assumptions, including industry and economic conditions that could cause actual results to differ materially from those described in the forward-looking statements. Such factors, risks, uncertainties, and assumptions include, but are not limited to, (1) global economic fluctuations, (2) changes in the cost and availability of commodities, materials, and equipment, (3) risks related to providing uninterrupted service to clients, (4) the ability of clients to terminate their relationship with the Company at any time, (5) risks associated with real estate ownership, (6) the Company’s ability to successfully achieve its strategic initiatives, (7) risks related to fluctuations in the Company’s operating results from quarter to quarter, (8) risks related to potential acquisitions or dispositions of businesses by the Company, (9) our profitability and growth being tied to the success of our operating businesses, (10) risks associated with our financial investments in other businesses, (11) our ability to improve existing products and services and develop, introduce, and market new products and services successfully, (12) the loss of or material reduction in our business with any of the Company’s largest customers, (13) competition in the Company’s markets, (14) risks related to potential decreases in demand for products, (15) our ability to maintain costs at an acceptable level, (16) the negative cash flows and operating losses that may recur in the future, (17) risks related to international operations, including foreign currency fluctuations, political events, trade wars, natural disasters or health crises, including the Russia-Ukraine war, and potential conflict in the Middle East, (18) risks relating to how future credit facilities may affect or restrict our operating flexibility, (19) our ability to generate or borrow sufficient cash to make payments on our indebtedness, (20) risks related to indebtedness, (21) risks associated with the Company’s investment strategy, (22) the Company’s dependence on key management personnel, (23) the Company’s ability to attract and retain highly skilled professionals, management, and advisors, (24) the Company’s ability to collect accounts receivable, (25) the Company’s exposure to legal proceedings, investigations and disputes, and limits on related insurance coverage, (26) the Company’s ability to utilize net operating loss carryforwards, (27) the potential for goodwill impairment, (28) volatility of the Company’s stock price, (29) risks related to our historically low trading volume, (30) risks related to securities or industry analysts, (31) the Company’s ability to declare dividends, (32) risks associated with failure to pay dividends on our Series A Preferred Stock, (33) our history of annual net losses, (34) risks related to our international operations, (35) risks related to compliance with federal and state laws, regulations, and other rules, (36) our exposure to employment-related claims, legal liability, and costs from clients, employees, and regulatory authorities, (37) risks related to the imposition of licensing or tax requirements or new regulations, (38) the effect of Anti-takeover provisions in our organizational documents, (39) the effect of the protective amendment contained in our Restated Certificate of Incorporation, (40) the impact of our stockholder rights plan, or “poison pill,” on stockholder decision making, (41) risks related to our scaled disclosure requirements as a smaller reporting company, (42) the Company’s heavy reliance on information systems and the impact of potentially losing or failing to develop technology, (43) the adverse impacts of cybersecurity threats and attacks, and (44) risks related to the use of new and evolving technologies, and (45) those risks set forth in “Risk Factors in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025.” The foregoing list should not be construed to be exhaustive. Actual results could differ materially from the forward-looking statements contained in this press release. In view of these uncertainties, you should not place undue reliance on any forward-looking statements, which are based on our current expectations. These forward-looking statements speak only as of the date of this press release. The Company assumes no obligation, and expressly disclaims any obligation, to update any forward-looking statements, whether as a result of new information, future events or otherwise.

In the first full quarter since launch, 2,145 healthcare providers prescribed TONMYA®, 3,588 patients initiated treatment, and ~5,400 prescriptions were filled

Agreement signed in May with leading group purchasing organization (GPO) that provides access to TONMYA for approximately 35 million U.S. commercial lives

Expect to initiate adaptive Phase 2 field study for the prevention of Lyme disease in the U.S. in the first half of 2027 for TNX-4800, pending FDA agreement

Approximately $185.5 million in cash and cash equivalents as of March 31, 2026

BERKELEY HEIGHTS, N.J., May 11, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully integrated, commercial biotechnology company, today announced financial results for the quarter ended March 31, 2026, and provided an overview of recent operational highlights.

“TONMYA is the first new fibromyalgia medicine in 15 years,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “TONMYA is a non-opioid analgesic designed for bedtime administration and long-term use by adults. Since launch in November 2025, TONMYA has shown growth in prescriptions, new writers, refills, and patient access. Our first managed care partnership was announced in May, providing access to approximately 35 million U.S. commercial lives. We will continue engagement with commercial and government payers to expand patient access. Our focus remains on operational excellence across sales, marketing, medical affairs, and market access to educate and deliver on TONMYA’s differentiated potential.”

Dr. Lederman continued, “We also continue to meaningfully advance our mid-stage clinical programs and our earlier-stage pipeline. For TNX-4800, our investigational long-acting borreliacidal, human monoclonal antibody targeting OspA on Borrelia burgdorferi, which causes the majority of Lyme disease in the U.S., we announced positive Phase 1 data and plans for an adaptive Phase 2 field study in 2027, pending FDA agreement. We look forward to our scheduled Type C meeting with the FDA early in the third quarter of 2026 to discuss the study. We believe TNX-4800 offers several advantages over vaccines in development, including onset of protection within two days and a simpler two-dose regimen with a second booster dose two months after the first. We also expect to begin our Phase 2 study of TONMYA for the treatment of Major Depressive Disorder (MDD) mid-year. Our other programs across CNS, infectious disease, immunology, and rare disease remain well positioned for near-term milestones.”

Commercial Updates

TONMYA (cyclobenzaprine HCl sublingual tablets): a centrally acting, non-opioid analgesic for the treatment of fibromyalgia in adults

On November 17, 2025, TONMYA became commercially available, following U.S. FDA approval in August 2025 for the treatment of fibromyalgia in adults. TONMYA is the first new prescription medicine approved for fibromyalgia in more than 15 years. The approval was based on two double-blind, randomized, placebo-controlled Phase 3 clinical studies of nearly 1,000 patients that demonstrated durable and statistically significant reduction in daily pain scores compared to placebo. There are now approximately 100 TONMYA sales reps in the field.

In the first quarter of 2026, the first full quarter since launch, key metrics include:

2,145 unique healthcare providers prescribed TONMYA to patients.

3,588 unique patients initiated treatment with TONMYA.

Approximately 5,400 prescriptions were filled. This includes bridge prescriptions that are facilitated through the Company’s specialty pharmacy channel. Bridge prescriptions represent initial patient fills provided while coverage determinations are pending and do not immediately generate net product revenue.

For the period beginning November 17, 2025, through April 24, 2026, cumulative key metrics include:

More than 2,700 unique healthcare providers have prescribed TONMYA to patients.

Approximately 5,618 unique patients have initiated treatment with TONMYA.

For the period beginning November 17, 2025, through May 1, 2026, cumulative key metrics include:

Approximately 11,016 prescriptions were filled. This includes bridge prescriptions that are facilitated through the Company’s specialty pharmacy channel.

Repeat prescriber and patient refill trends are encouraging.

The Company is prioritizing engagement with commercial payers, Medicare, and Medicaid to increase access:

In May 2026, Tonix secured commercial payer coverage with its first managed care partnership agreement with a leading GPO, which will provide access for approximately 35 million U.S. patients (20% of ~177 million commercial lives in the U.S.)

To date, TONMYA is covered under Medicaid in 38 states, for approximately 55 million lives, representing 73% of the roughly 75 million Medicaid lives.

Tonix has a robust patient access program and support services in place, including a TONMYA savings card, copay assistance, and prior authorization support, intended to reduce access barriers during early commercialization.

To educate healthcare providers (HCPs), the Company held a multidisciplinary dialogue about TONMYA via a national webcast. Tonix also launched a national speaker training program with approximately 100 HCPs to maximize peer-to-peer speaker programs expected to occur across target specialties and regions this year.

As part of a commitment to continued clinical evidence generation and education, Tonix presented clinical data on TONMYA at the 8th International Congress on Controversies in Fibromyalgia, 2026 American Academy of Pain Medicine (AAPM) PainConnect Annual Meeting, and 2026 Non-Opioid Pain Therapeutics Summit. The Company also published two articles in the peer-reviewed journal, Clinical Pharmacology in DrugDevelopment.

TNX-102 SL (cyclobenzaprine HCl sublingual tablets): in Phase 2 development for MDD; remains on track to initiate mid-year 2026

In November 2025, the FDA cleared the IND for TNX-102 SL 5.6 mg for the treatment of MDD in adults. The IND clearance enables Tonix to proceed with the HORIZON study, a potentially pivotal Phase 2, 6-week, randomized, double-blind, placebo-controlled study of TNX-102 SL as a first-line monotherapy in adults with MDD. About 360 patients will be enrolled at approximately 30 U.S. sites, with the primary endpoint being the MADRS total score change from baseline at Week 6. Tonix plans to initiate enrollment in mid-2026.

TNX-102 SL in Phase 2 development for the treatment of acute stress disorder (ASD) and acute stress reaction (ASR)

The U.S. Department of Defense-funded Optimizing Acute Stress Reaction Interventions (OASIS) study is being conducted by the University of North Carolina under an investigator-initiated IND. The OASIS study examines the safety and efficacy of TNX-102 SL to reduce adverse posttraumatic neuropsychiatric sequelae among patients in the emergency department after a motor vehicle collision. Topline data is expected to be reported in the second half of 2026.

TNX-1300 (double-mutant cocaine esterase) for cocaine intoxication; Phase 2-program has Breakthrough Therapy designation from the FDA, with no products on the market for this indication

The Company plans to meet with the FDA in 2026 to inform the clinical design of the next Phase 2 study (a Phase 2a study has been completed).

TNX-1900 (intranasal potentiated oxytocin): in development for several CNS disorders

TNX-1900 is currently being studied in four Phase 2 and one Phase 1 investigator-initiated studies. The Phase 2 investigator-initiated studies include binge-eating disorder (Massachusetts General Hospital, “MGH”), adolescent obesity (MGH), bone health in autism (MGH and University of Virgina), and arginine vasopressin deficiency (MGH).

In March 2026, Tonix announced the dosing of the first participant in a Phase 1 investigator-initiated pharmacodynamic study with Erasmus University of TNX-1900 in healthy female volunteers, using capsaicin and electrical stimulation to model trigeminal neurovascular reactivity.

Infectious Disease Pipeline

TNX-4800 (anti-OspA mAb): Phase 2-ready long-acting human monoclonal antibody in development for the seasonal prevention of Lyme disease in the U.S., which has no FDA-approved vaccines or prophylactics

In March 2026, Tonix presented Phase 1 data at the World Vaccine Congress Washington 2026 and announced plans to initiate an adaptive Phase 2 field study in the first half of 2027, pending FDA agreement. The Company also presented Phase 1 data in April 2026 at the 4th Annual Ticks and Tickborne Diseases Symposium at Johns Hopkins University.

TNX-4800 demonstrated encouraging safety, tolerability, pharmacokinetics, and immunogenicity, with serum TNX-4800 measurable at the earlier sampling time of 48 hours and no significant clinical or laboratory safety signals. The Phase 1 study was conducted by a team at UMass Chan Medical School led by Mark S. Klempner, MD, Professor of Medicine at UMass Chan and an inventor of TNX-4800.

In April 2026, the Company announced it expects to lead a randomized, double-blind, placebo-controlled, adaptive Phase 2 field study to evaluate the efficacy of a two-dose regimen of TNX-4800 subcutaneous (SC) in preventing the first occurrence of confirmed Lyme disease during the primary efficacy surveillance period (Day 3 through Month 6 following administration). Each fixed dose is expected to provide exposures comparable to the 5 mg/kg dose evaluated in Phase 1. The first dose will be administered in the Spring and the second booster dose will be administered two months later. Participants will include adolescents and adults 16 years of age and older in Lyme-endemic areas in the U.S. The primary endpoint will be the prevention of Lyme disease for six months (comparison of TNX-4800 group and placebo group) following the initial dose.

In April 2026, the Company announced it has scheduled a Type C meeting with the FDA early in the third quarter of 2026 to discuss the planned adaptive Phase 2 field study design.

The Company expects to have GMP investigational product available for clinical testing in early 2027.

TNX-801 (recombinant horsepox virus): attenuated, pre-clinical live orthopoxvirus vaccine candidate for the prevention of smallpox and mpox

In March 2026, Tonix presented animal and in vitro data on TNX-801 at the World Vaccine Congress Washington 2026. TNX-801 is expected to enter a Phase 1 study in 2027 pending FDA clearance of the Investigational New Drug (IND) application.

TNX-4200 (small molecule): broad spectrum anti-viral to protect against viral diseases

TNX-4200 is a small molecule broad-spectrum antiviral agent targeting CD45 for the prevention or treatment of high lethality infections to improve the medical readiness of military personnel in biological threat environments.

The TNX-4200 program is supported by an up to $34 million contract over five years from the Department of Defense’s Defense Threat Reduction Agency (DTRA). In the first quarter of 2026, the Company received confirmation that the project was cleared to enter the next budgetary and developmental phase.

Immunology Pipeline

TNX-1500 (dimeric Fc modified anti-CD40L, humanized mAb): Phase 2-ready third generation anti-CD40L for prophylaxis of kidney transplant rejection and treatment of autoimmune disorders

In November 2025, Tonix announced a collaboration with MGH to advance a Phase 2, open-label, investigator-initiated clinical study of TNX-1500 in kidney transplant recipients, planned for initiation mid-year 2026, pending FDA clearance of the IND. The study is expected to enroll five adult kidney transplant recipients.

Rare Disease Pipeline

TNX-2900 (intranasal potentiated oxytocin): in development for Prader-Willi syndrome, with Orphan Drug designation as well as Rare Pediatric Disease designation that could make Tonix eligible for a Priority Review Voucher upon approval

In September 2025, Tonix announced plans to initiate a Phase 2, randomized, double-blind, placebo-controlled study in children and adolescents with Prader-Willi syndrome. The study is expected to initiate in the first quarter of 2027.

Immuno-oncology Pipeline

TNX-1700 (TFF2-albumin fusion protein): in preclinical development for gastric and colorectal cancer

In March 2026, Tonix presented preclinical data at the American Association for Cancer Research (AACR) Annual Meeting 2026. Data presented in an oral presentation showed how TNX-1700 reversed aging-associated gastric inflammation and significantly attenuated tumor progression in an aged gastric microenvironment in preclinical models. Data in a poster presentation demonstrated TNX-1700 exhibited dose-independent, linear pharmacokinetics in animals.

TNX-4700 (human anti-BTLA mAb): in preclinical development for immuno-oncology indications

In March 2026, Tonix presented preclinical data in a poster presentation at the AACR Annual Meeting 2026 demonstrating TNX-4700 demonstrated potent, high-affinity binding and functional antagonism. The mAb technology was licensed from Curia.

Financial: Recent Highlights

Tonix had approximately $185.5 million of cash and cash equivalents as of March 31, 2026, compared to approximately $207.6 million as of March 31, 2025. Net cash used in operations was approximately $42.3 million for the first quarter ended March 31, 2026, compared to $16.6 million for the same period in 2025.

Subsequent to quarter-end, the Company has raised $22.6 million proceeds using its at-the-market (ATM) facility.

The Company believes that its cash resources as of March 31, 2026, together with the net proceeds that it raised from equity offerings in the second quarter of 2026, will fund its planned operating and capital expenditure requirements into early second quarter of 2027.

As of May 8, 2026, the Company had 15,940,601 shares of common stock outstanding.

First Quarter 2026 Financial Results

Net product revenue for the first quarter 2026 was approximately $6.9 million, compared to $2.4 million for the same period in 2025, and consisted of combined net sales of TONMYA, Zembrace® SymTouch®, and Tosymra®. Net revenue from sales of TONMYA for the first quarter was approximately $3.7 million. TONMYA was launched in November 2025. Net revenue from sales of TONMYA for the period from November 17, 2025, to December 31, 2025, was approximately $1.4 million. Net revenue from sales of Zembrace® SymTouch® and Tosymra® for the was approximately $3.2 million compared to $2.4 million for the same quarter in 2025. Cost of sales for the first quarter 2026 was approximately $1.6 million, compared to $0.9 million for the same period in 2025.

Research and development expenses for the first quarter 2026 were approximately $18.2 million, compared to $7.4 million for the same period in 2025. This increase is predominately due to pipeline prioritization period over period, and increased headcount.

Selling, general, and administrative expenses for the first quarter 2026 were $28.6 million, compared to $10.1 million for the same period in 2025. The increase is predominately due to spending on sales and marketing related to TONMYA, as well as increased headcount.

Net loss available to common stockholders was $40.2 million, or $2.93 per basic and diluted share, for the first quarter 2026, compared to net loss available to common stockholders of $16.8 million, or $2.84 per basic and diluted share, for the same period in 2025. The basic and diluted weighted average common shares outstanding for the first quarter 2026 was 13,707,104 compared to 5,927,231 shares for the same period in 2025.

Tonix Pharmaceuticals Holding Corp.

Tonix Pharmaceuticals* is a fully integrated, commercial-stage biotechnology company focused on central nervous system (CNS) disorders, infectious diseases, immunology conditions, and rare diseases where there exists high unmet medical need. TONMYA® (cyclobenzaprine HCl sublingual tablets 2.8mg), the Company’s recently approved flagship medicine, is the first new treatment for fibromyalgia in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® and Tosymra®. Tonix is maximizing the science behind TONMYA in Phase 2 clinical studies to evaluate its potential in major depressive disorder and acute stress disorder/acute stress reaction. Tonix is also advancing a pipeline of infectious disease programs, including monoclonal antibody TNX-4800 for Lyme disease prevention in the U.S. and TNX-801, a vaccine in development for the prevention of mpox and smallpox. Within immunology, Tonix is developing TNX-1500, a third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. Finally, the Company’s rare disease portfolio includes TNX-2900, which is Phase 2 ready for the treatment of Prader-Willi syndrome. To learn more, visit www.tonixpharma.com.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace® SymTouch® and Tosymra® are registered trademarks of Tonix Medicines. TONMYA® is a registered trademark of Tonix Pharma Limited. All other marks are property of their respective owners.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the completion of the offering, the satisfaction of customary closing conditions, the intended use of proceeds from the offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially as a result of a number of factors, including the ability of the Company to satisfy the conditions to the closing of the offering and the timing thereof, as well as those described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on March 12, 2026, and periodic reports filed with the SEC on or after the date thereof. Tonix does not undertake an obligation to update or revise any forward-looking statement. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

HOUSTON, May 11, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit”, “SMC” or the “Company”) announced today its financial and operating results for the three months ended March 31, 2026.

Highlights

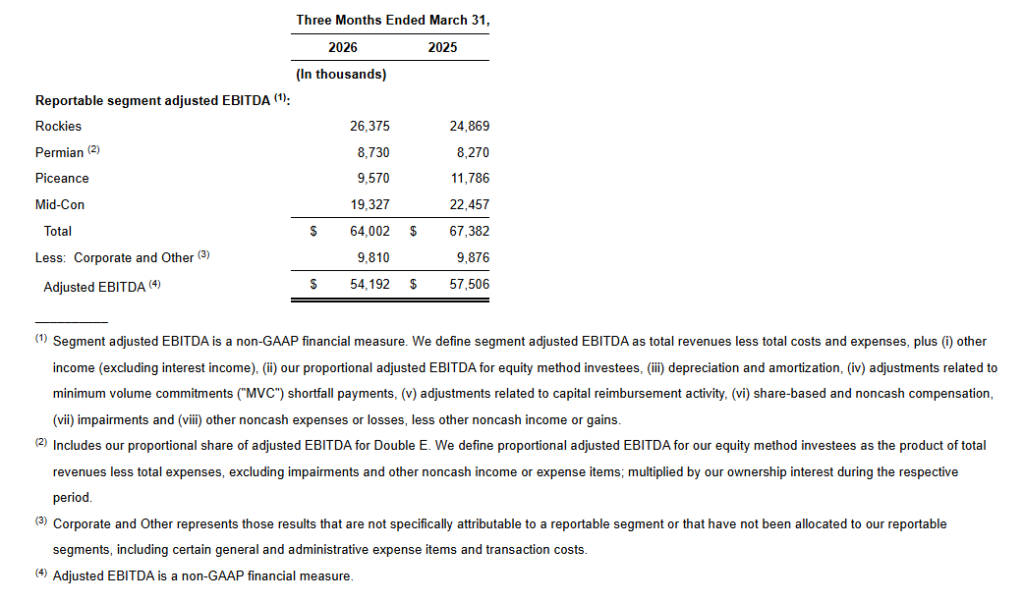

First quarter 2026 net loss of $3.2 million, Adjusted EBITDA of $54.2 million, cash flow available for distributions (“Distributable Cash Flow” or “DCF”) of $26.9 million and free cash flow (“FCF”) of $11.4 million

Connected 37 wells during the first quarter, including four Williston wells from the new 10-year crude gathering agreement; five rigs currently running with approximately 80 DUCs behind the systems

Executed a new precedent agreement for 100 MMcf/d of firm capacity on the Double E Pipeline, with Q1 2027 expected in-service date and 10-year term

Repaid all $45 million of accrued Series A Preferred Stock dividends clearing a key milestone toward reinstating a common dividend

Completed a $42 million private placement of common stock to an affiliate of Tailwater Capital LLC, Summit’s largest shareholder, providing additional financial flexibility to execute on high-return growth projects and reduce ABL borrowings

Reiterating 2026 full-year Adjusted EBITDA guidance of $225 million to $265 million, supported by accelerating producer activity in the Rockies and anticipated Mid-Con volume ramp

Management Commentary

Heath Deneke, President, Chief Executive Officer and Chairman, commented, “First quarter results reflected favorable crude oil prices primarily impacting our Rockies segment, offset by lower realized residue gas prices and lower than expected volumes in the Mid-Con Segment. We continue to expect the business to trend toward the midpoint of our original guidance range and are seeing a lot of momentum across our portfolio, particularly in the Permian and Rockies segments.

“Subsequent to quarter end, Double E executed another new 10-year take-or-pay precedent agreement for 100 MMcf/d of firm capacity behind an operational processing plant in Eddy County, New Mexico, with the lateral connecting the plant expected to be in-service in the first quarter of 20271. This agreement, along with those previously announced, brings total contracted volume on Double E to 1.755 Bcf/d, and we remain encouraged by the continued commercial progress on the pipeline. We are evaluating significant shipper interest in the recently launched open season, and remain optimistic there will be sufficient commercial support to make a final investment decision on the approximately 800 MMcf/d mid-point compression expansion project.

“In the Rockies Segment, the favorable crude oil price environment is expected to improve our product margin over the coming quarters and several customers are actively working to accelerate and increase activity beyond our original expectations. We are also encouraged by the preliminary results of four wells behind the new Williston Basin commercial contract we secured last quarter. We have 40 new wells expected across the portfolio in the second quarter, including 20 in the Mid-Con segment.”

__________________________

1 The agreement is contingent upon satisfaction of certain customary conditions, including Double E board approval.

First Quarter 2026 Business Highlights

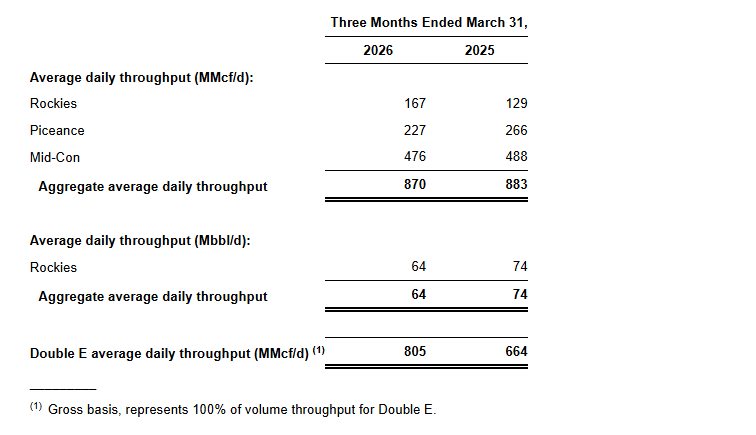

SMC’s average daily natural gas throughput on its wholly owned, operated systems decreased 2.7% to 870 MMcf/d, while liquids volumes decreased 3.0% to 64 Mbbl/d, relative to the fourth quarter of 2025. Double E Pipeline averaged 805 MMcf/d and contributed $8.7 million in Adjusted EBITDA, net to SMC, for the first quarter of 2026.

Natural gas price-driven segments:

Natural gas price-driven segments generated $28.9 million in combined Segment Adjusted EBITDA, a $2.6 million decrease relative to the fourth quarter of 2025, with combined capital expenditures of $7.6 million

Mid-Con Segment Adjusted EBITDA totaled $19.3 million, a decrease of $2.1 million relative to the fourth quarter of 2025, primarily due to lower natural gas throughput as a result of natural production declines, partially offset by six new Arkoma well connections. Subsequent to quarter end, three additional Arkoma wells were connected to the system and there are currently 17 Barnett DUCs expected to come online in the second quarter of 2026.

Piceance Segment Adjusted EBITDA totaled $9.6 million, a decrease of $0.4 million relative to the fourth quarter of 2025, primarily due to a 7.3% decline in volume throughput driven by temporary shut-ins of approximately 8.0 MMcf/d, natural production declines, and no new well connections during the quarter. Customers currently have ~20 MMcf/d of natural gas shut-in as a result of low regional gas prices. Based on current forecasted prices in the region, we expect this production to resume beginning in the third quarter of 2026.

Oil price-driven segments:

Oil price-driven segments generated $35.1 million in combined Segment Adjusted EBITDA, a $1.5 million decrease relative to the fourth quarter of 2025, with combined capital expenditures of $11.0 million

Rockies Segment Adjusted EBITDA totaled $26.4 million, a decrease of $1.5 million relative to the fourth quarter of 2025, driven by a $1.2 million non-cash imbalance, lower realized residue gas prices negatively impacting percent-of-proceeds contracts and lower fresh water sales, partially offset by a 4.4% increase in natural gas volume throughput and higher realized crude oil and NGL prices beginning in March 2026. 18 wells were connected in the DJ Basin and 13 in the Williston Basin, including the first four 3-mile lateral wells under the new 10-year crude gathering agreement. Five rigs are currently running with approximately 60 DUCs behind the system.

Permian Segment Adjusted EBITDA totaled $8.7 million, flat relative to the fourth quarter of 2025.

The following table presents average daily throughput by reportable segment for the periods indicated:

The following table presents adjusted EBITDA by reportable segment for the periods indicated:

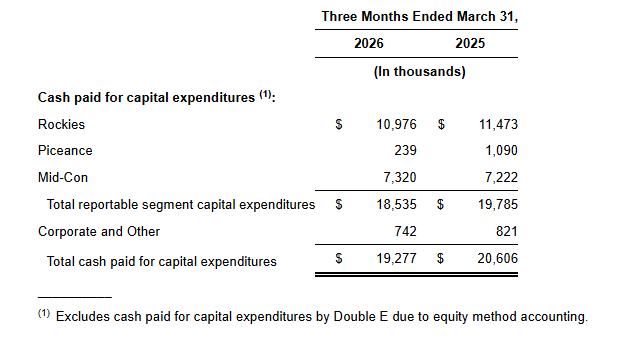

Capital Expenditures

Capital expenditures totaled $19.3 million in the first quarter of 2026, inclusive of maintenance capital expenditures of $3.7 million. Capital expenditures in the first quarter of 2026 were primarily related to pad connections in the Rockies and Mid-Con segments.

Capital & Liquidity

As of March 31, 2026, SMC had $43.4 million in unrestricted cash on hand and $116 million drawn under its $500 million ABL Revolver with $381 million of borrowing availability, after accounting for $2.7 million of issued, but undrawn letters of credit. As of March 31, 2026, SMC’s gross availability based on the borrowing base calculation in the credit agreement was $802 million, which is $302 million greater than the $500 million of lender commitments to the ABL Revolver. As of March 31, 2026, SMC was in compliance with all financial covenants, including interest coverage of 2.7x relative to a minimum interest coverage covenant of 2.0x and first lien leverage ratio of 0.4x relative to a maximum first lien leverage ratio of 2.5x. As of March 31, 2026, SMC reported a total leverage ratio of approximately 4.2x.

During the first quarter, Summit Permian Transmission, LLC entered into a new $440 million senior secured term facility, which includes a $50 million committed accordion feature and a $50 million uncommitted accordion feature (the “Term Facility”) maturing in March 2031. Proceeds from the Term Facility were used to refinance Summit Permian Transmission’s existing credit facility, redeem Summit Permian Transmission Holdco’s preferred units, fund an $85 million restricted payment to SMC, provide liquidity to fund SMC’s share of capital expenditures including those associated with the recently announced expansion projects, and pay other fees and expenses.

As of March 31, 2026, the Summit Permian Transmission Term Loan Facility had a balance of $340 million. Summit Midstream Permian has $6.1 million of cash-on-hand as of March 31, 2026. The Permian Transmission Term Loan remains non-recourse to SMC.

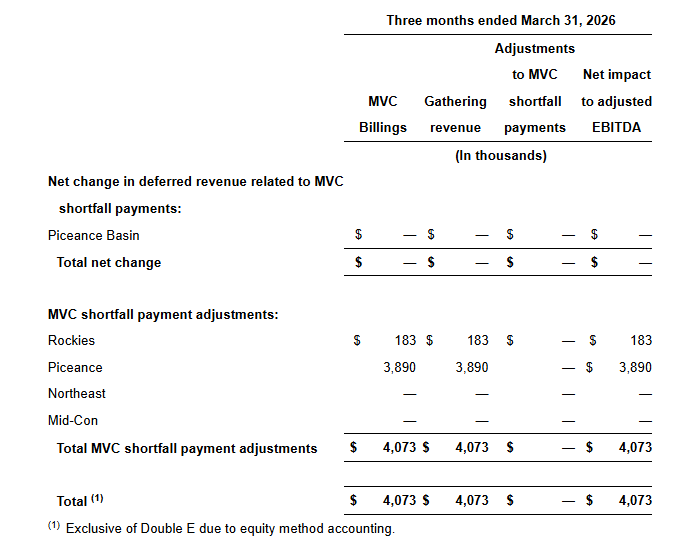

MVC Shortfall Payments

SMC billed its customers $4.1 million in the first quarter of 2026 related to MVC shortfalls. For those customers that do not have MVC shortfall credit banking mechanisms in their gathering agreements, the MVC shortfall payments are accounted for as gathering revenue in the period in which they are earned. In the first quarter of 2026, SMC recognized $4.1 million of gathering revenue associated with MVC shortfall payments. SMC had no adjustments to MVC shortfall payments in the first quarter of 2026. SMC’s MVC shortfall payment mechanisms contributed $4.1 million of total Adjusted EBITDA in the first quarter of 2026.

Quarterly Dividend

The Board of Directors of Summit Midstream Corporation continued to suspend cash dividends payable on the common stock for the period ended March 31, 2026. The quarterly cash dividend on the Series A Preferred Stock, for the period ended June 14, 2026, will be paid to preferred shareholders of record as of the close of business on June 1, 2026.

On March 27, 2026, all unpaid dividends of $46.3 million on the Series A Preferred Stock were paid to holders of record as of the close of business on March 17, 2026.

First Quarter 2026 Earnings Call Information

SMC will host a conference call at 10:00 a.m. Eastern on May 12, 2026, to discuss its quarterly operating and financial results. The call can be accessed via teleconference at the following link: Q1 2026 Summit Midstream Corporation Earnings Conference Call (https://register-conf.media-server.com/register/BI874f39fdf8c54b499c4ac477755fbcad). Once registration is completed, participants will receive a dial-in number along with a personalized PIN to access the call. While not required, it is recommended that participants join 10 minutes prior to the event start. The conference call, live webcast and archive of the call can be accessed through the Investors section of SMC’s website at www.summitmidstream.com.

Upcoming Investor Conferences

Members of SMC’s senior management team will attend the 2026 Energy Infrastructure CEO & Investor Conference which will take place on May 18–20, 2026, the 2026 RBC Capital Markets Global Energy, Power & Infrastructure Conference taking place on June 2–3, 2026, and the BofA Energy and Power Credit Conference on June 3–4, 2026. The presentation materials associated with each event will be accessible through the Investors section of SMC’s website at www.summitmidstream.com prior to the beginning of the conference.

Use of Non-GAAP Financial Measures

We report financial results in accordance with U.S. generally accepted accounting principles (“GAAP”). We also present adjusted EBITDA, segment adjusted EBITDA, Distributable Cash Flow, and Free Cash Flow, non-GAAP financial measures.

Adjusted EBITDA

We define adjusted EBITDA as net income or loss, plus interest expense, income tax expense, depreciation and amortization, our proportional adjusted EBITDA for equity method investees, adjustments related to MVC shortfall payments, adjustments related to capital reimbursement activity, share-based and noncash compensation, impairments, items of income or loss that we characterize as unrepresentative of our ongoing operations and other noncash expenses or losses, income tax benefit, income (loss) from equity method investees and other noncash income or gains. Because adjusted EBITDA may be defined differently by other entities in our industry, our definition of this non-GAAP financial measure may not be comparable to similarly titled measures of other entities, thereby diminishing its utility.

Management uses adjusted EBITDA in making financial, operating and planning decisions and in evaluating our financial performance. Furthermore, management believes that adjusted EBITDA may provide external users of our financial statements, such as investors, commercial banks, research analysts and others, with additional meaningful comparisons between current results and results of prior periods as they are expected to be reflective of our core ongoing business.

Adjusted EBITDA is used as a supplemental financial measure to assess:

the ability of our assets to generate cash sufficient to make future potential cash dividends and support our indebtedness;

the financial performance of our assets without regard to financing methods, capital structure or historical cost basis;

our operating performance and return on capital as compared to those of other entities in the midstream energy sector, without regard to financing or capital structure;

the attractiveness of capital projects and acquisitions and the overall rates of return on alternative investment opportunities; and

the financial performance of our assets without regard to (i) income or loss from equity method investees, (ii) the impact of the timing of MVC shortfall payments under our gathering agreements or (iii) the timing of impairments or other income or expense items that we characterize as unrepresentative of our ongoing operations.

Adjusted EBITDA has limitations as an analytical tool and investors should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. For example:

certain items excluded from adjusted EBITDA are significant components in understanding and assessing an entity’s financial performance, such as an entity’s cost of capital and tax structure;

adjusted EBITDA does not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments;

adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; and

although depreciation and amortization are noncash charges, the assets being depreciated and amortized will often have to be replaced in the future, and adjusted EBITDA does not reflect any cash requirements for such replacements.

We compensate for the limitations of adjusted EBITDA as an analytical tool by reviewing the comparable GAAP financial measures, understanding the differences between the financial measures and incorporating these data points into our decision-making process.

Distributable Cash Flow

We define Distributable Cash Flow as adjusted EBITDA, as defined above, less cash interest paid, cash paid for taxes, net interest expense accrued and paid on the senior notes, and maintenance capital expenditures.

Free Cash Flow

We define free cash flow as distributable cash flow attributable to common and preferred shareholders less growth capital expenditures, less investments in equity method investees, less dividends to common and preferred shareholders. Free cash flow excludes proceeds from asset sales and cash consideration paid for acquisitions.

We do not provide the GAAP financial measures of net income or loss or net cash provided by operating activities on a forward-looking basis because we are unable to predict, without unreasonable effort, certain components thereof including, but not limited to, (i) income or loss from equity method investees and (ii) asset impairments. These items are inherently uncertain and depend on various factors, many of which are beyond our control. As such, any associated estimate and its impact on our GAAP performance and cash flow measures could vary materially based on a variety of acceptable management assumptions.

About Summit Midstream Corporation

SMC is a value-driven corporation focused on developing, owning and operating midstream energy infrastructure assets that are strategically located in the core producing areas of unconventional resource basins, primarily shale formations, in the continental United States. SMC provides natural gas, crude oil and produced water gathering, processing and transportation services pursuant to primarily long-term, fee-based agreements with customers and counterparties in five unconventional resource basins: (i) the Williston Basin, which includes the Bakken and Three Forks shale formations in North Dakota; (ii) the Denver-Julesburg Basin, which includes the Niobrara and Codell shale formations in Colorado and Wyoming; (iii) the Fort Worth Basin, which includes the Barnett Shale formation in Texas; (iv) the Arkoma Basin, which includes the Woodford and Caney shale formations in Oklahoma; and (v) the Piceance Basin, which includes the Mesaverde formation as well as the Mancos and Niobrara shale formations in Colorado. SMC has an equity method investment in Double E Pipeline, LLC, which provides interstate natural gas transportation service from multiple receipt points in the Delaware Basin to various delivery points in and around the Waha Hub in Texas. SMC is headquartered in Houston, Texas.

Forward-Looking Statements

This press release includes certain statements concerning expectations for the future that are forward-looking within the meaning of the federal securities laws. Forward-looking statements include, without limitation, any statement that may project, indicate or imply future results, events, performance or achievements and may contain the words “expect,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result,” and similar expressions, or future conditional verbs such as “may,” “will,” “should,” “would” and “could.” In addition, any statement concerning future financial performance (including future revenues, earnings or growth rates), payment of dividends on any series of stock, ongoing business strategies and possible actions taken by SMC or its subsidiaries are also forward-looking statements. Forward-looking statements also contain known and unknown risks and uncertainties (many of which are difficult to predict and beyond management’s control) that may cause SMC’s actual results in future periods to differ materially from anticipated or projected results. An extensive list of specific material risks and uncertainties affecting SMC is contained in its 2025 Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 16, 2026, as amended and updated from time to time. Any forward-looking statements in this press release are made as of the date of this press release and SMC undertakes no obligation to update or revise any forward-looking statements to reflect new information or events.

SKYX Reports over $32 Million in Cash and Cash Equivalents as of March 31, 2026, Management Believes It Has Sufficient Cash to Achieve Its Goals Including Becoming Cash Flow Positive in 2026

Gross Profit Continues to Improve with 16% Increase to $7.0 Million in Q-1 of 2026 Compared to $6 Million in Q-1 2025

Gross Margin Continues to Improve to 30% in Q-1 2026 from 28% in Q-1 2025

SKYX Entered into a Strategic Partnership Agreement with Prominent European Hotel and Real Estate Developer Group OTT, to Deploy Its Advanced Smart and AI Platform Technologies as a Brand Standard Throughout Its Hotels and Buildings. Group OTT Has Developed Over 250 Hotels and Buildings Across Europe

In May 2026 SKYX Announced It Will Deploy Its Advanced and Smart Technologies to Its First European Hotel During a Master Renovation of an Historical Architectural Preservation Hotel, The Grand Hotel du Parc (formerly The Grand Medicis Hotel), in La Bourboule, France

SKYX Signed Additional Agreement with Group OTT Heritage Hospitality Group to Deploy and Market Its Technologies to Vast European Hotel Market of Over 132,000 Hotels

SKYX Technologies Reduces Up to 90% Time and Cost of Buildings and Hotel Renovation/Installations or New Build and is Continuing Discussions with Additional Hotel Groups and Owners Regarding Utilization of its Game-Changing Advanced and Smart Platform Technologies

SKYX Is Expected to Supply Its Advanced Smart Home Technologies to Upcoming and Future Key Projects in the U.S. and Globally, Including New York, North Carolina, Austin, San Antonio, South Florida (Including Miami’s New $4 Billion Smart City), Europe, Saudi Arabia, and Egypt

SKYX Is Expected to Deploy Over 1-Million Units of Its Products including Its Advanced Smart Home Plug-and-Play Technologies During These Projects and to Over 100,000 Units/Homes by the End of 2026 Through Its Pro and Retail Segments

Despite Warmer Weather, SKYX’s Sales of Its Patented Turbo Heater Fan are Continuing to Grow and Company Will Be Expanding the Category of the “All-Season Ceiling Fan” — Heat in Winter and Cool in Summer — to Provide Additional Products in New Designs and Larger Sizes

In Q-1 SKYX Announced Beginning of Its Collaboration with NVIDIA AI Ecosystem Connect Program, Expecting to Grow Its Collaboration with NVIDIA into Future Smart Home Projects

SKYX’s Technology Expansion Provides Additional Opportunities for Future Recurring Revenues Through Interchangeability, Upgrades, AI Services, Monitoring, Subscriptions, and More

SKYX’s Enhanced Safety Code Standardization Team Continues Its Progress Toward Its Goal of a Safety-Mandated Standardization in Homes/Buildings of Its Life-Saving Ceiling Outlet/Receptacle Technology

MIAMI, May 11, 2026 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive advanced smart home and AI platform technology company with over 100 pending and issued patents globally and 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today reported its financial and operational results for the first quarter ended March 31, 2026.

SKYX will hold a conference call today, May 11, 2026, at 4:30 pm, Eastern Time, to discuss the results. See below for dial-in information.

First Quarter 2026 Highlights and Recent Events

Generated its greatest increase in YoY revenues of 10% with record $22 million in revenues in first quarter of 2026 compared to $20 million for the first quarter of 2025.

Reporting 9 consecutive YoY quarters of growth.

As of March 31, 2026, Company reported $32 million in total cash, cash equivalents, and restricted cash compared to $10 million as of December 31, 2025.

SKYX’s continues to leverage the rapid conversion of its e-commerce sales into cash, advancing it cash position often referred to as the “Dell Working Capital Model”, lowering its cost of capital.

Management believes it has sufficient cash to achieve its goals including becoming cash flow positive exiting 2026.

The gross profit for the first quarter ending March 31, 2026, increased comparatively by 16% to $7 million, compared to the first quarter ending March 31, 2025.

The gross margin for the first quarter ending March 31, 2026, increased comparatively by 2% to 30%, compared to 28% in the first quarter ending March 31, 2025.

Net loss per share decreased by $0.02 to $0.07 per share in the first quarter of 2026 compared to $0.09 in the first quarter of 2025. Adjusted EBITDA loss per share, a non-GAAP measure, decreased to $0.03 per share in the first quarter of 2026, as compared to $0.04 per share, in the first quarter of 2025.

Builder / Hotel Segments and General Market Acceptance

SKYX is continuing its significant progress with the hotel and builder segments.

SKYX technologies reduces up to 90% time and cost of buildings and hotel renovations/ installations or new build and is continuing discussions with additional developers, hotel groups and owners regarding utilization of its game-changing advanced and smart platform technologies.

Company entered into a strategic partnership agreement with prominent European hotel and real estate developer, Jean-François Ott, Founder of Group OTT, to deploy Its advanced and smart electrical technologies as a brand standard throughout its hotels and buildings.

Over the past 35 years Group OTT have developed more than 250 hospitality, residential, and commercial buildings valued at over $4 billion throughout Europe.

In May 2026 SKYX announced it will deploy its advanced and smart technologies to its first European hotel during a master renovation of an historical architectural preservation hotel, The Grand Hotel du Parc (formerly The Grand Medicis Hotel), in La Bourboule, France.

SKYX has signed an additional agreement with OTT Heritage Hospitality group to deploy and market its technologies to the vast European hospitality market of more than 132,000 hotels.

During the course of this additional agreement, OTT Heritage Hospitality expects to market and deploy SKYX’s disruptive technologies into hundreds of European hotels, buildings, and developments. Approximately 124,000 hotel rooms are projected to open in Europe in 2026, with over 250,000 additional rooms in the industry-wide development pipeline.

SKYX has successfully demonstrated its technology during a Marriott Hotel renovation and expects to grow its hotel segment during 2026.

Marriott Hotel chain owner, The Shaner Group, led a $16.5 million investment round. The Shaner Group is an owner and developer of more than 70 hotels worldwide.

SKYX is expected to supply its advanced smart home technologies to upcoming and future key projects in the U.S. and globally, including projects in Pittsford, New York; North Carolina; Austin, Texas; San Antonio, Texas; South Florida including the new $4 billion smart city in Miami, Florida; Europe; Saudi Arabia; and Egypt; among others.

SKYX is expected to deploy over 1 million units of its advanced smart home plug-and-play technologies during these projects.

SKYX continues its growth and expects to deploy over 100,000 of its products into homes/units during 2026 through retail and pro segments.

SKYX announced the launch of its patented advanced SKYFAN and Turbo Heater to the leading U.S. retailer Home Depot, including a new SkyPlug branding page on HomeDepot.com.

SKYX recently announced the launch of its Turbo Heater fan at leading U.S. retailers Target, Walmart, and Lowe’s, and on its e-commerce platform across 60 websites.

Based on the Growing Sales of Its Patented Turbo Heater Fan, SKYX Is Expanding the Category of the “All-Season Ceiling Fan” — Heat in Winter and Cool in Summer — to Provide Additional Products in New Designs and Larger Sizes.

Technology Roadmap

SKYX announced a collaboration with the NVIDIA AI Ecosystem Connect Program. SKYX expects to grow its collaboration with NVIDIA through its existing and future smart home projects.

SKYX’s technologies expansion provides additional opportunities for future recurring revenues through interchangeability, upgrades, AI services, monitoring, subscriptions, and more.

SKYX will be launching a new AI-driven system and infrastructure for its e-commerce platform of 60 websites, expected to increase its conversion rate and sales up to 30%.

The Company secured U.S. and global strategic manufacturing partnerships with premier manufacturers including in the U.S., Vietnam, Taiwan, China, and Cambodia.

Financing Highlights

SKYX cash, cash equivalents and restricted cash increased to $32 million as of March 31, 2026, as compared to $10 million as of December 31, 2025, as we raised $29 million in straight equity, with no warrants during January 2026 through two fundamental institutional investors, $25 million at $2.50 per share with $4 million at $2.00 per share.

In 2025 we extended and converted $13.5 million in notes coming due with maturity out to 5 years until 2030.

Safety Standardization Mandatory Code and Insurance Exposure

SKYX’s Safety Code Standardization Team is receiving support from a new significant prominent leader with its government safety agency’s process for a safety mandatory standardization of its electrical ceiling outlet/receptacle technology.

SKYX’s code team is led by industry veterans Mark Earley, former head of the National Electrical Code (NEC), and Eric Jacobson, former President and CEO of the American Lighting Association (ALA). The Company’s safety Code Standardization team believes it will garner assistance from additional safety organizations with its code mandatory safety standardization efforts based on the product’s significant safety aspects. Mr. Earley and Mr. Jacobson were instrumental in numerous code and safety changes in both the electrical and lighting industries. Both strongly believe that, considering the Company’s standardization progress including its product specification approval voting for by ANSI / NEMA (American National Standardization Institute / National Electrical Manufacturers Association) and being voted into 10 segments in the NEC Code Book, it has met the necessary safety conditions for becoming a ceiling safety standardization requirement for homes and buildings.

The Company strongly believes its products can save insurance companies many billions of dollars annually by minimizing risks (e.g., reducing fires, ladder fall injuries, and electrocutions). Management expects that insurance companies will use the Company’s range and variations of its safe advanced plug & play products to reduce its exposure and minimize its risks.

First Quarter 2026 Financial Results

The Company’s financial statements for the quarter ended March 31, 2026, are filed with the SEC and are available on the Company’s investor relations website. https://ir.skyplug.com/sec-filings/

Management Commentary

Company’s Management, Board members, and Senior Advisors include former CEO’s and executives from Fortune 100 companies including Nielsen, Microsoft, Disney, GE, Home Depot, Office Depot, Chrysler, among others.

The Company is trending positively, generating record first quarter 2026 revenues of $22 million as compared to $20 million for the first quarter of 2025, a gross profit for the first quarter ending March 31, 2026, increasing comparatively by 16% to $7 million, compared to the first quarter ending March 31, 2025 and a gross margin for the first quarter ending March 31, 2026, increasing comparatively by 2% to 30%, compared to 28% in the first quarter ending March 31, 2025. We believe our positive trends will accelerate going into 2026 as we build out and execute on our channel strategy.

We are encouraged by the recently announced initiatives where we could supply hundreds of thousands of units in Europe, the Middle East including Saudi Arabia and Egypt, the $4 billion mixed-use smart city development in the Little River District in the heart of Miami, and projects in Pittsford, New York; North Carolina; Austin, Texas; and San Antonio, Texas. We continue to address the builder/commercial segments, large online and brick-and-mortar retail partners as well as our future potential to realize incremental licensing, subscription, and AI/data aggregation revenues.

Furthermore, our e-commerce website platform with 60 websites enhances the acceleration of marketing and distribution channels, collaborations, licensing, and sales to both professional and retail segments. Our websites include banners, videos, and educational materials regarding the simplicity, cost savings, time-saving, and life-saving aspects of the Company’s patented technologies.

We have accelerated our pace of sales and strategic initiatives with a robust gross margin profile, notably reducing the adjusted EBITDA loss of SKYX on a comparative quarterly basis. Our e-commerce platform with 60 websites is expected to continue to provide additional cash flow to the Company.

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced smart home and AI platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts, but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with First-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions, including recent measures adopted by the federal government, on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Non-GAAP Financial Measures

Management considers earnings (loss) before interest, taxes, depreciation and amortization, or EBITDA, as adjusted, an important indicator in evaluating the Company’s business on a consistent basis across various periods. Due to the significance of non-recurring items, EBITDA, as adjusted, enables management to monitor and evaluate the business on a consistent basis. The Company uses EBITDA, as adjusted, as a primary measure, among others, to analyze and evaluate financial and strategic planning decisions regarding future operating investments and potential acquisitions. The Company believes that EBITDA, as adjusted, eliminates items that are not part of the Company’s core operations, such as interest expense and amortization expense associated with intangible assets, or items that do not involve a cash outlay, such as share-based payments and non-recurring items, such as transaction costs. EBITDA, as adjusted, should be considered in addition to, rather than as a substitute for, pre-tax income (loss), net income (loss) and cash flows used in operating activities. This non-GAAP financial measure excludes significant expenses that are required by GAAP to be recorded in the Company’s financial statements and is subject to inherent limitations. Investors should review the reconciliation of this non-GAAP financial measure to the comparable GAAP financial measure. Investors should not rely on any single financial measure to evaluate the Company’s business.

Please dial in at least 10 minutes before the start of the call to ensure timely participation.

A replay of the call will be available through June 11, 2026. To access the replay, please dial 1-844-512-2921 within the United States and Canada or 1-412-317-6671 internationally and enter Access ID 13760591.

HOUSTON, May 11, 2026 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Orange 142, LLC (“Orange 142”) and Colossus Media, LLC (“Colossus SSP”), today announced financial results for the first quarter ended March 31, 2026.

Mark D. Walker, Chairman and Chief Executive Officer, commented, “We remain focused on organically growing our sales pipeline by enhancing how we reach and support customers across a broader set of go‑to‑market channels. Alongside product innovation initiatives such as Ignition+, our sales teams are seeing encouraging engagement through expanded enterprise outreach, diversified combination of enterprise sales, inside and outside sales efforts, and new distribution and lead‑generation channels. This multi‑channel approach is broadening our reach, improving sales efficiency, and positioning us to drive more consistent, scalable growth over time.”

Keith Smith, President, commented, “With a more streamlined operating model and a clearer focus on our core strengths, we believe we are positioned to thoughtfully evaluate strategic opportunities that could complement our existing platform. While our primary focus remains execution and organic growth, we continually assess potential partnerships or acquisitions that align with our long‑term objectives and shareholder value creation.”