CHICAGO, Feb. 27, 2025 (GLOBE NEWSWIRE) — GoHealth, Inc. (NASDAQ: GOCO) (“GoHealth” or the “Company”), a leading health insurance marketplace and Medicare-focused digital health company, today announced financial results for the three and twelve months ended December 31, 2024.

Fourth Quarter Highlights

Achieved net revenues of $389.1 million, a substantial 41% increase compared to the prior year period.

Submissions grew to 481,445, representing a 67% increase compared to the prior year period.

Net income of $58.0 million, a substantial improvement of $60.3 million compared to the prior year period.

Adjusted EBITDA1 surged to $117.8 million, a significant 107% increase compared to the prior year period.

Compared to the prior year period, Direct Operating Cost per Submission2 improved 27%, to an industry leading $501.

The integration and transformation of e-TeleQuote Insurance, Inc. (“e-TeleQuote”) has driven growth and efficiency gains, delivering significant performance improvements in the 2024 Annual Enrollment Period.

Full-Year 2024 Highlights

Full-year net revenues reached $798.9 million, reflecting 9% growth compared to the prior year.

Submissions were 1,016,182, a 23% increase compared to the prior year.

Net loss of $7.3 million, an improvement of $144.0 million compared to the prior year.

Adjusted EBITDA1 of $120.3 million, a 60% increase compared to the prior year.

Successfully refinanced our credit facility with new five-year term and lender group.

Supported nearly 3 million Medicare consumers in assessing benefit options in 2024.

Implemented the PlanFit Save initiative and began receiving health plan compensation for membership retention.

Remained top partner to health plans based on Submission volume.

“GoHealth’s strong 2024 performance highlights our market-leading, technology-driven approach in the digital Medicare marketplace. While we predicted favorable market dynamics, we were even more pleased by the velocity of our efficiency improvements and the immediate impact of our technology initiatives on profitability. We are energized by the opportunities ahead and are already executing on them,” said Vijay Kotte, CEO of GoHealth. “The successful onboarding and optimization of e-TeleQuote, expansion of our health plan partnerships, and continued investment in artificial intelligence and advanced analytics have further strengthened GoHealth’s position as a leading digital Medicare marketplace. As we move into 2025, we continue to focus on driving sustainable, profitable growth, enhancing the consumer experience, and reinforcing our market leadership through continued innovation and operational excellence.”

“Our 2024 financial results demonstrate GoHealth’s capacity to achieve exceptional performance through disciplined execution and strategic investment,” said Brendan Shanahan, CFO of GoHealth. “The substantial year-over-year growth in net income and the 107% year-over-year growth in Adjusted EBITDA1 during Q4, coupled with significant gains in operating efficiency, reinforces the strength of our strategy. As we begin 2025, we are optimistic that the favorable market dynamics we experienced will persist through at least the first three quarters with cautious optimism for similar favorable dynamics for the fourth quarter, enabling us to build on this solid financial foundation.”

(1)

Adjusted EBITDA is a non-GAAP measure. For a definition of Adjusted EBITDA and a reconciliation to the most comparable GAAP measure, please see below.

(2)

Direct Operating Cost per Submission is an operating metric. For a definition of Direct Operating Cost per Submission and an explanation of its calculation, please see below.

Conference Call Details

The Company will host a conference call today, Thursday, February 27, 2025 at 8:00 a.m. (ET) to discuss its financial results. A live audio webcast of the conference call will be available via GoHealth’s Investor Relations website, https://investors.gohealth.com/. A replay of the call will be available via webcast for on-demand listening shortly after the completion of the call.

About GoHealth, Inc.

GoHealth is a leading health insurance marketplace and Medicare-focused digital health company whose purpose is to compassionately ensure consumers’ peace of mind when making healthcare decisions so they can focus on living life. For many of these consumers, enrolling in a health insurance plan is confusing and difficult, and seemingly small differences between health plans may lead to significant out-of-pocket costs or lack of access to critical providers and medicines. GoHealth’s proprietary technology platform leverages modern machine-learning algorithms, powered by over two decades of insurance purchasing behavior, to reimagine the process of matching a health plan to a consumer’s specific needs. Its unbiased, technology-driven marketplace coupled with highly skilled licensed agents has facilitated the enrollment of millions of consumers in Medicare plans since GoHealth’s inception. For more information, visit https://www.gohealth.com.

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements are made in reliance upon the safe harbor provision of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical facts contained in this press release may be forward-looking statements. Statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations, including, among others, statements regarding our expected growth, future capital expenditures, debt service obligations, adoption and use of artificial intelligence technologies, the impact on our business from the acquisition of e-TeleQuote and our ability to successfully integrate e-TeleQuote’s operations, technologies and employees into our business, are forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “aims,” “expects,” “plans,” “anticipates,” “could,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential,” “likely,” “future” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this press release are only predictions, projections and other statements about future events that are based on current expectations and assumptions. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

These forward-looking statements speak only as of the date of this press release and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including the factors described in the sections titled “Summary Risk Factors,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2023 (“2023 Annual Report on Form 10-K”) and our forthcoming Annual Report on Form 10-K for the fiscal year ended December 31, 2024 (“2024 Annual Report on Form 10-K”), as well as our other filings with the Securities and Exchange Commission. The factors described in our 2023 Annual Report on Form 10-K and our forthcoming 2024 Annual Report on Form 10-K should not be construed as exhaustive and should be read together with the other cautionary statements included in this press release, as well as the cautionary statements and other risk factors set forth in the Quarterly Report on Form 10-Q for the first fiscal quarter ended March 31, 2024, the Quarterly Report on Form 10-Q for the second fiscal quarter ended June 30, 2024, the Quarterly Report on Form 10-Q for the third quarter ended September 30, 2024 and in our other filings with the Securities and Exchange Commission.

You should read this press release and the documents that we reference in this press release completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 27, 2025– The GEO Group, Inc. (NYSE: GEO) (“GEO” or the “Company”) announced today that it has been awarded a 15-year, fixed-price contract by U.S. Immigration and Customs Enforcement (“ICE”) to provide support services for the establishment of a federal immigration processing center at the company-owned, 1,000-bed Delaney Hall Facility (the “Facility”) in Newark, New Jersey. GEO’s support services include the exclusive use of the Facility by ICE, along with security, maintenance, and food services, as well as access to recreational amenities, medical care, and legal counsel.

The new support services contract is expected to generate in excess of $60 million in annualized revenues for GEO in the first full year of operations, with margins consistent with GEO’s company-owned Secure Services facilities. GEO estimates the 15-year value of the contract with normal cost of living adjustments to be approximately $1 billion. GEO expects to reactivate the Facility in the second quarter of 2025 with revenues and earnings from the new contract normalizing during the second half of 2025.

George C. Zoley, Executive Chairman of GEO, said, “Our company-owned Delaney Hall Facility will play an important role in providing needed detention bedspace and support services for ICE in the Northeast. We are continuing to prepare for what we believe is an unprecedented opportunity to help the federal government meet its expanded immigration enforcement priorities. We are taking several important steps to meet this opportunity, including making a previously announced $70 million investment in capital expenditures to strengthen our capabilities to deliver expanded detention capacity, secure transportation, and electronic monitoring and related services to ICE and the federal government.”

About The GEO Group The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 99 facilities totaling approximately 79,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Use of forward-looking statements This news release may contain “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the U.S. Private Securities Litigation Reform Act of 1995. Readers are cautioned not to place undue reliance on these forward-looking statements and any such forward-looking statements are qualified in their entirety by reference to the cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission including its Form 10-K, 10-Q and 8-K reports. All forward-looking statements speak only as of the date of this news release and are based on current expectations and involve a number of assumptions, risks and uncertainties that could cause the actual results to differ materially from such forward-looking statements. Readers are strongly encouraged to read the full cautionary statements and risk factors contained in GEO’s filings with the U.S. Securities and Exchange Commission, including those referenced above. GEO disclaims any obligation to update or revise any forward-looking statements, except as required by law.

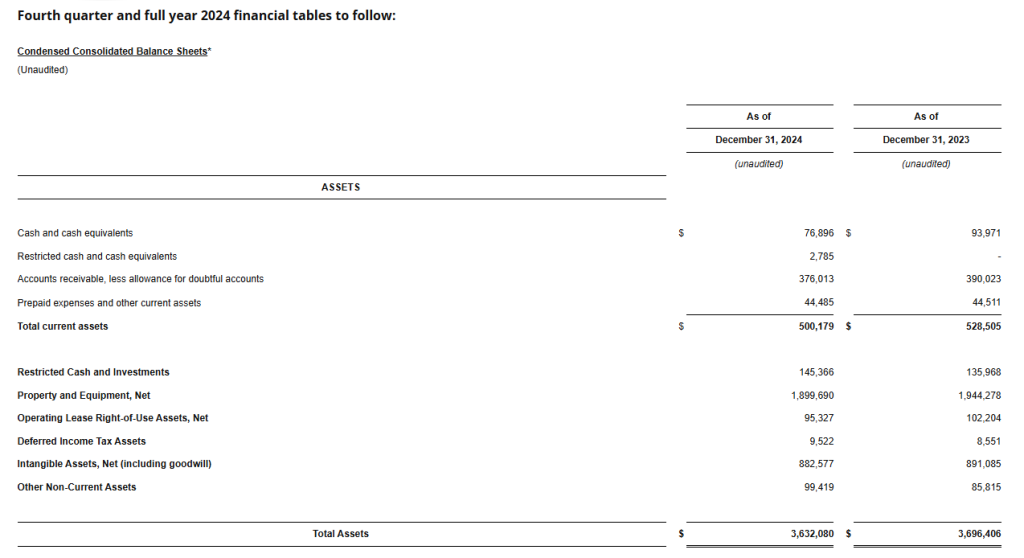

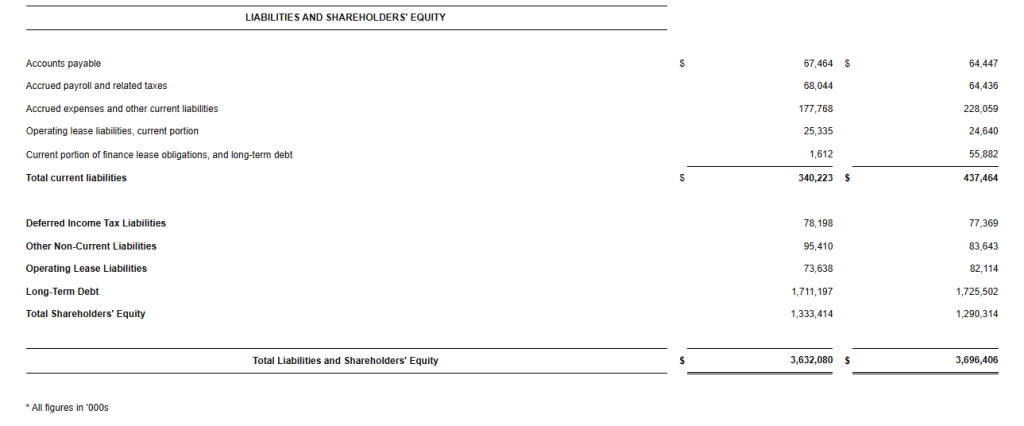

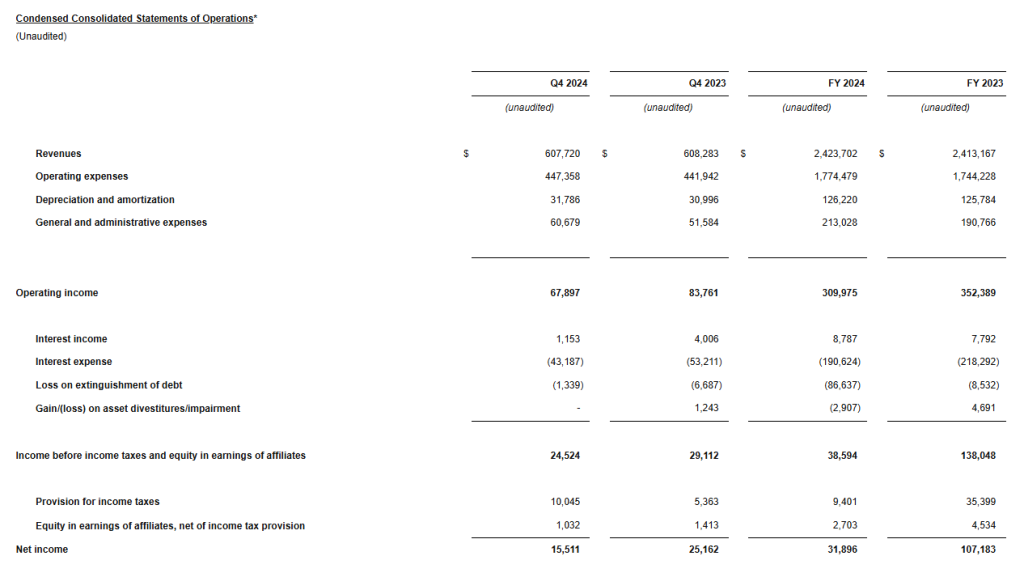

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 27, 2025– The GEO Group, Inc. (NYSE: GEO) (“GEO”), a leading provider of contracted support services for secure facilities, processing centers, and reentry centers, as well as enhanced in-custody rehabilitation, post-release support, and electronic monitoring programs, reported today its financial results for the fourth quarter and full year 2024.

Fourth Quarter 2024 Highlights

Total revenues of $607.7 million

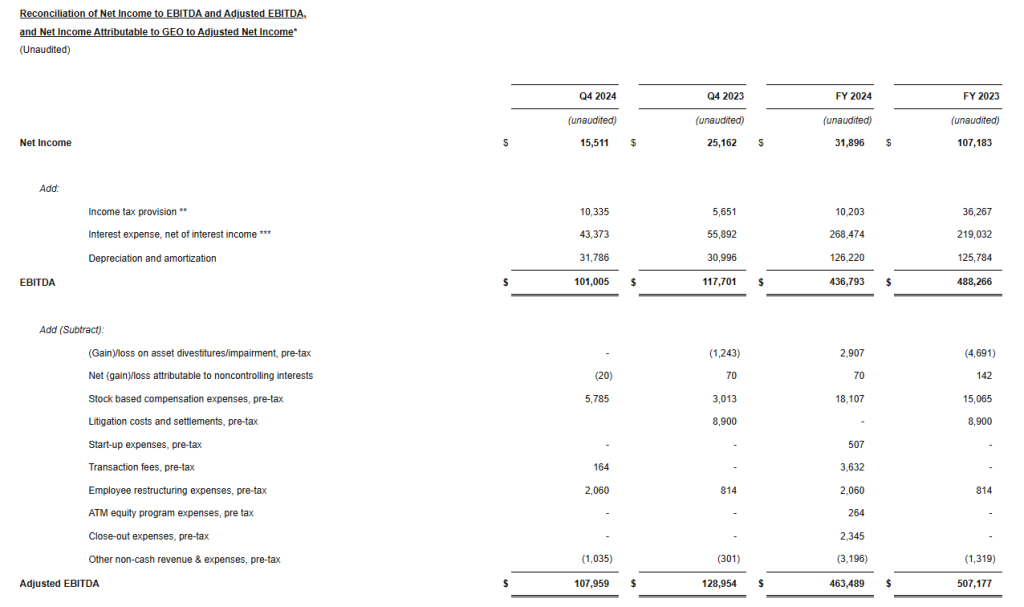

Net Income of $15.5 million

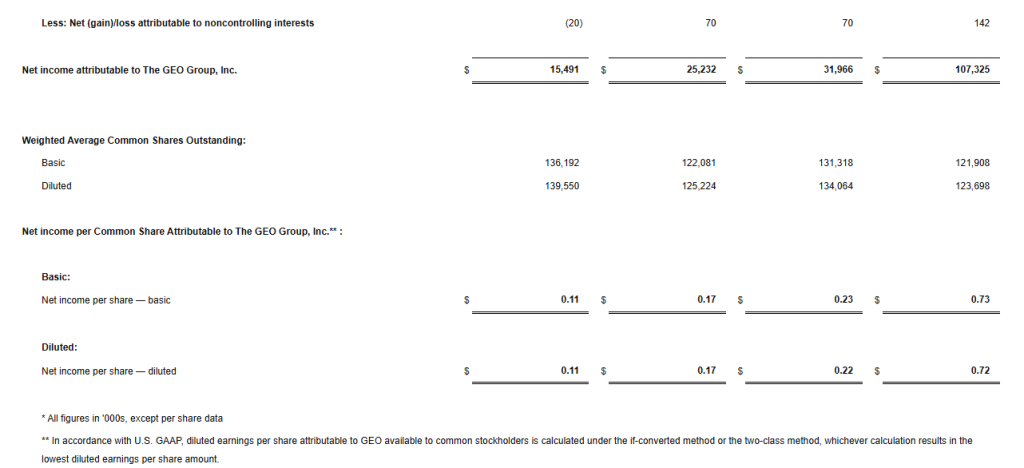

Net Income Attributable to GEO of $0.11 per diluted share

Adjusted Net Income of $0.13 per diluted share

Adjusted EBITDA of $108.0 million

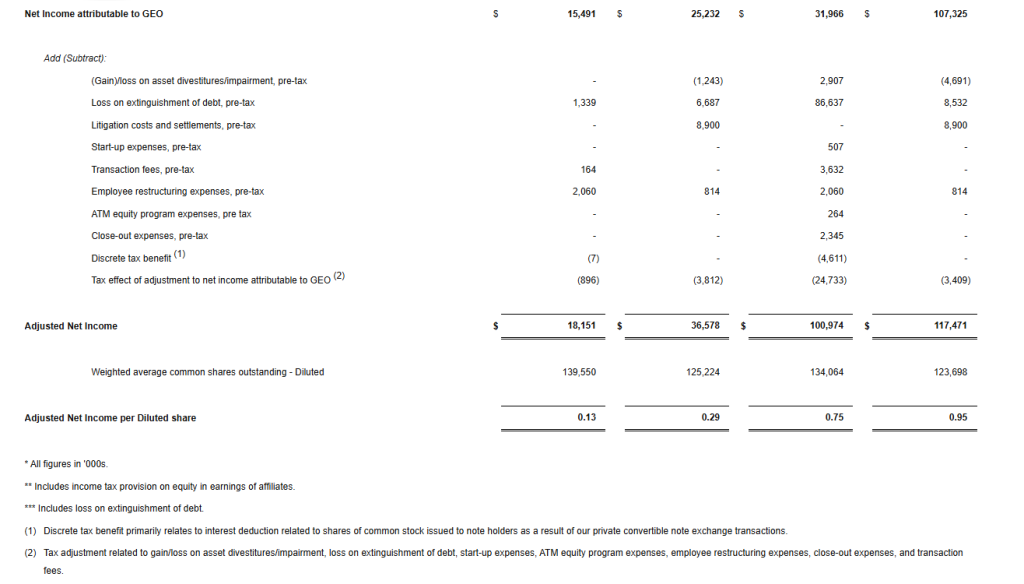

For the fourth quarter 2024, we reported net income attributable to GEO of $15.5 million, or $0.11 per diluted share, compared to net income attributable to GEO of $25.2 million, or $0.17 per diluted share, for the fourth quarter 2023.

Fourth quarter 2024 results reflect costs associated with the extinguishment of debt of $1.3 million, pre-tax, $0.2 million in transaction fees, pre-tax, and $2.1 million in employee restructuring expenses, pre-tax. Excluding these unusual items, we reported adjusted net income for the fourth quarter 2024 of $18.2 million, or $0.13 per diluted share, compared to $36.6 million, or $0.29 per diluted share, for the fourth quarter 2023.

We reported total revenues for the fourth quarter 2024 of $607.7 million compared to $608.3 million for the fourth quarter 2023. We reported fourth quarter 2024 Adjusted EBITDA of $108.0 million, compared to $129.0 million for the fourth quarter 2023.

Our fourth quarter of 2024 results reflect higher general and administrative expenses, which were partly the result of the previously announced reorganization of our management team and additional professional fees we incurred in anticipation of future growth projects and related operational activity during 2025.

Our revenues for the fourth quarter of 2024 increased sequentially from the third quarter of 2024 and were in line with our previous guidance; however, our earnings and Adjusted EBITDA were below our previous expectations, primarily due to the higher general and administrative expenses incurred during the fourth quarter of 2024.

George C. Zoley, Executive Chairman of GEO, said, “During the fourth quarter of 2024, we completed the previously announced reorganization of our senior management team and incurred additional professional fees in anticipation of what we expect to be unprecedented future growth opportunities and significant operational activity during 2025. In 2024, we also incurred $9 million of our previously announced $70 million investment to strengthen our capabilities to deliver expanded detention capacity, secure transportation, and electronic monitoring services to U.S. Immigration and Customs Enforcement (“ICE”) and the federal government.

In addition to taking these important steps, we remain focused on reducing our net debt, deleveraging our balance sheet, and exploring options to return capital to shareholders in the future. In 2025, we expect to further reduce our total net debt by approximately $150 million to $175 million, bringing our total net debt to approximately $1.55 billion.”

Full Year 2024 Highlights

Total revenues of $2.42 billion

Net Income of $31.9 million

Net Income Attributable to GEO of $0.22 per diluted share, reflects costs associated with the extinguishment of debt of $86.6 million, pre-tax

Adjusted Net Income of $0.75 per diluted share

Adjusted EBITDA of $463.5 million

For the full year 2024, we reported net income attributable to GEO of $32.0 million, or $0.22 per diluted share, compared to net income attributable to GEO of $107.3 million, or $0.72 per diluted share, for the full year 2023. Results for the full year 2024 reflect costs associated with the extinguishment of debt of $86.6 million, pre-tax.

Excluding the costs associated with the extinguishment of debt and other unusual items, we reported adjusted net income for the full year 2024 of $101.0 million, or $0.75 per diluted share, compared to $117.5 million, or $0.95 per diluted share, for the full year 2023.

We reported total revenues for the full year 2024 of $2.42 billion compared to $2.41 billion for the full year 2023. We reported Adjusted EBITDA for the full year 2024 of $463.5 million, compared to $507.2 million for the full year 2023.

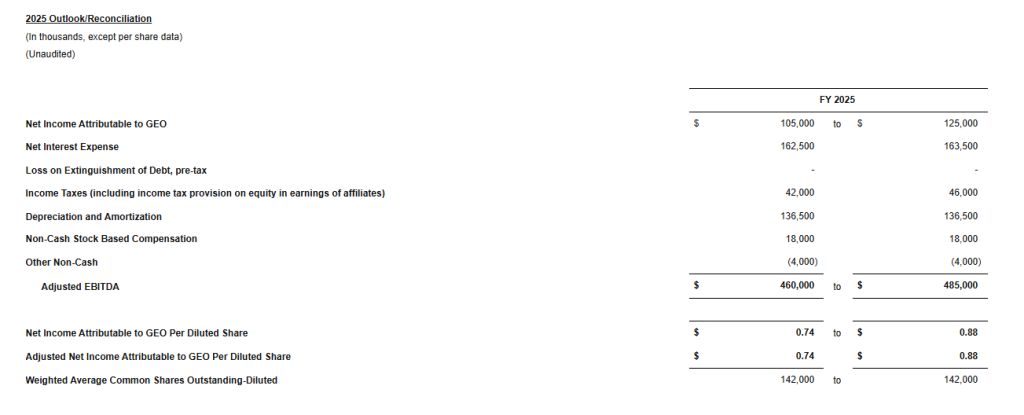

Financial Guidance

Today, we issued our initial financial guidance for 2025. Consistent with our long-standing practice, our initial guidance does not include the impact of any new contract awards that have not been previously announced.

For the full year 2025, we expect Net Income Attributable to GEO to be in a range of 74 cents to 88 cents per diluted share, on revenues of approximately $2.5 billion and based on an effective tax rate of approximately 28 percent, inclusive of known discrete items. We expect our full year 2025 Adjusted EBITDA to be between $460 million and $485 million.

While our initial financial guidance for 2025 does not include an assumption for any new contract awards that have not been previously announced, we anticipate several additional opportunities could materialize during the year, which would provide significant upside to our current forecast. As we progress through the year and the likelihood and timing of these opportunities become clearer, we will adjust our 2025 financial guidance accordingly.

We expect total Capital Expenditures for the full year 2025 to be between $125 million and $145 million, including the impact of the $70 million investment we announced in December of 2024 to strengthen our capabilities to deliver expanded detention capacity, secure transportation, and electronic monitoring services to ICE and the federal government. This incremental $70 million investment is comprised of $47 million to renovate existing Secure Services facilities, $9 million of which was already spent in 2024; $16 million to ramp up the production of additional GPS tracking devices; and $7 million to expand our secure transportation assets.

Recent Developments

We announced today that we have been awarded a 15-year, fixed-price contract by ICE to provide support services for the establishment of a federal immigration processing center at the company-owned, 1,000-bed Delaney Hall Facility (the “Facility”) in Newark, New Jersey. GEO’s support services include the exclusive use of the Facility by ICE, along with security, maintenance, and food services, as well as access to recreational amenities, medical care, and legal counsel.

The new support services contract is expected to generate in excess of $60 million in annualized revenues for GEO in the first full year of operations, with margins consistent with GEO’s company-owned Secure Services facilities. GEO estimates the 15-year value of the contract with normal cost of living adjustments to be approximately $1 billion. GEO expects to reactivate the Facility in the second quarter of 2025 with revenues and earnings from the new contract normalizing during the second half of 2025.

Balance Sheet

At the end of the fourth quarter 2024, our net debt totaled approximately $1.7 billion, and our net leverage was approximately 3.7 times Adjusted EBITDA. We ended the fourth quarter of 2024 with approximately $77 million in cash and cash equivalents and approximately $214 million in total available liquidity.

Conference Call Information

We have scheduled a conference call and webcast for today at 11:00 AM (Eastern Time) to discuss our fourth quarter and full year 2024 financial results as well as our outlook. The call-in number for the U.S. is 1-877-250-1553 and the international call-in number is 1-412-542-4145. In addition, a live audio webcast of the conference call may be accessed on the Webcasts section under the News, Events and Reports tab of GEO’s investor relations webpage at investors.geogroup.com. A replay of the webcast will be available on the website for one year. A telephonic replay of the conference call will be available through March 6, 2025, at 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The participant passcode for the telephonic replay is 3882673.

About The GEO Group

The GEO Group, Inc. (NYSE: GEO) is a leading diversified government service provider, specializing in design, financing, development, and support services for secure facilities, processing centers, and community reentry centers in the United States, Australia, South Africa, and the United Kingdom. GEO’s diversified services include enhanced in-custody rehabilitation and post-release support through the award-winning GEO Continuum of Care®, secure transportation, electronic monitoring, community-based programs, and correctional health and mental health care. GEO’s worldwide operations include the ownership and/or delivery of support services for 99 facilities totaling approximately 79,000 beds, including idle facilities and projects under development, with a workforce of up to approximately 18,000 employees.

Reconciliation Tables and Supplemental Information

GEO has made available Supplemental Information which contains reconciliation tables of Net Income Attributable to GEO to Adjusted Net Income, and Net Income to EBITDA and Adjusted EBITDA, along with supplemental financial and operational information on GEO’s business and other important operating metrics. The reconciliation tables are also presented herein. Please see the section below titled “Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures” for information on how GEO defines these supplemental Non-GAAP financial measures and reconciles them to the most directly comparable GAAP measures. GEO’s Reconciliation Tables can be found herein and in GEO’s Supplemental Information available on GEO’s investor webpage at investors.geogroup.com.

Note to Reconciliation Tables and Supplemental Disclosure – Important Information on GEO’s Non-GAAP Financial Measures

Adjusted Net Income, EBITDA, and Adjusted EBITDA are non-GAAP financial measures that are presented as supplemental disclosures. GEO has presented herein certain forward-looking statements about GEO’s future financial performance that include non-GAAP financial measures, including Net Debt, Net Leverage, and Adjusted EBITDA.

The determination of the amounts that are included or excluded from these non-GAAP financial measures is a matter of management judgment and depends upon, among other factors, the nature of the underlying expense or income amounts recognized in a given period.

While we have provided a high level reconciliation for the guidance ranges for full year 2025, we are unable to present a more detailed quantitative reconciliation of the forward-looking non-GAAP financial measures to their most directly comparable forward-looking GAAP financial measures because management cannot reliably predict all of the necessary components of such GAAP measures.

The quantitative reconciliation of the forward-looking non-GAAP financial measures will be provided for completed annual and quarterly periods, as applicable, calculated in a consistent manner with the quantitative reconciliation of non-GAAP financial measures previously reported for completed annual and quarterly periods.

Net Debt is defined as gross principal debt less cash from restricted subsidiaries. Net Leverage is defined as Net Debt divided by Adjusted EBITDA.

EBITDA is defined as net income adjusted by adding provisions/(benefit) for income tax, interest expense, net of interest income, and depreciation and amortization. Adjusted EBITDA is defined as EBITDA adjusted for (gain)/loss on asset divestitures/impairment, pre-tax, net loss attributable to non-controlling interests, stock-based compensation expenses, pre-tax, litigation costs and settlements, pre-tax, start-up expenses, pre-tax, transaction fees, pre-tax, one-time employee restructuring expenses, pre-tax, ATM equity program expenses, pre-tax, close-out expenses, pre-tax, other non-cash revenue and expenses, pre-tax, and certain other adjustments as defined from time to time.

Given the nature of our business as a real estate owner and operator, we believe that EBITDA and Adjusted EBITDA are helpful to investors as measures of our operational performance because they provide an indication of our ability to incur and service debt, to satisfy general operating expenses, to make capital expenditures, and to fund other cash needs or reinvest cash into our business.

We believe that by removing the impact of our asset base (primarily depreciation and amortization) and excluding certain non-cash charges, amounts spent on interest and taxes, and certain other charges that are highly variable from year to year, EBITDA and Adjusted EBITDA provide our investors with performance measures that reflect the impact to operations from trends in occupancy rates, per diem rates and operating costs, providing a perspective not immediately apparent from net income.

The adjustments we make to derive the non-GAAP measures of EBITDA and Adjusted EBITDA exclude items which may cause short-term fluctuations in income from continuing operations and which we do not consider to be the fundamental attributes or primary drivers of our business plan and they do not affect our overall long-term operating performance.

EBITDA and Adjusted EBITDA provide disclosure on the same basis as that used by our management and provide consistency in our financial reporting, facilitate internal and external comparisons of our historical operating performance and our business units and provide continuity to investors for comparability purposes.

Adjusted Net Income is defined as net income/(loss) attributable to GEO adjusted for certain items which by their nature are not comparable from period to period or that tend to obscure GEO’s actual operating performance, including for the periods presented (gain)/loss on asset divestitures/impairment, pre-tax, loss on the extinguishment of debt, pre-tax, litigation costs and settlements, pre-tax, start-up expenses, pre-tax, transaction fees, pre-tax, one-time employee restructuring expenses, pre-tax, ATM equity program expenses, pre-tax, close-out expenses, pre-tax, discrete tax benefit, and tax effect of adjustments to net income attributable to GEO.

Safe-Harbor Statement

This press release contains forward-looking statements regarding future events and future performance of GEO that involve risks and uncertainties that could materially and adversely affect actual results, including statements regarding GEO’s financial guidance for the full year of 2025, statements regarding GEO’s focus on reducing net debt, deleveraging its balance sheet, positioning itself to explore options to return capital to shareholders in the future, making investments to strengthen GEO’s capabilities and deliver expanded detention capacity, secure transportation, and electronic monitoring services, pursuing unprecedented future growth opportunities and significant operational activity, and the upside this could have on GEO’s future financial results and financial guidance, and GEO’s ability to scale up the delivery of diversified services to support the future needs of its government agency partners. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” or “continue” or the negative of such words and similar expressions. Risks and uncertainties that could cause actual results to vary from current expectations and forward-looking statements contained in this press release include, but are not limited to: (1) GEO’s ability to meet its financial guidance for 2025 given the various risks to which its business is exposed; (2) GEO’s ability to deleverage and repay, refinance or otherwise address its debt maturities in an amount and on terms commercially acceptable to GEO, and on the timeline it expects or at all; (3) GEO’s ability to identify and successfully complete any potential sales of company-owned assets and businesses or potential acquisitions of assets or businesses on commercially advantageous terms on a timely basis, or at all; (4) changes in federal and state government policy, orders, directives, legislation and regulations that affect public-private partnerships with respect to secure, correctional and detention facilities, processing centers and reentry centers; (5) changes in federal immigration policy; (6) public and political opposition to the use of public-private partnerships with respect to secure correctional and detention facilities, processing centers and reentry centers; (7) any continuing impact of the COVID-19 global pandemic on GEO and GEO’s ability to mitigate the risks associated with COVID-19; (8) GEO’s ability to sustain or improve company-wide occupancy rates at its facilities; (9) fluctuations in GEO’s operating results, including as a result of contract terminations, contract renegotiations, changes in occupancy levels and increases in GEO’s operating costs; (10) general economic and market conditions, including changes to governmental budgets and its impact on new contract terms, contract renewals, renegotiations, per diem rates, fixed payment provisions, and occupancy levels; (11) GEO’s ability to address inflationary pressures related to labor related expenses and other operating costs; (12) GEO’s ability to timely open facilities as planned, profitably manage such facilities and successfully integrate such facilities into GEO’s operations without substantial costs; (13) GEO’s ability to win management contracts for which it has submitted proposals and to retain existing management contracts; (14) risks associated with GEO’s ability to control operating costs associated with contract start-ups; (15) GEO’s ability to successfully pursue growth opportunities and continue to create shareholder value; (16) GEO’s ability to obtain financing or access the capital markets in the future on acceptable terms or at all; and (17) other factors contained in GEO’s Securities and Exchange Commission periodic filings, including its Form 10-K, 10-Q and 8-K reports, many of which are difficult to predict and outside of GEO’s control.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 results. The company reported Q4 revenue of $15.9 million, largely in line with our estimate of $16.2 million, illustrated in Figure #1 Q4 Results. Adj. EBITDA of $0.25 million was below our estimate of $0.91 million, due primarily to lower-than-expected gross margins.

Adding customers. Subscriptions to the company’s top B2C app, the YouCam beauty app, were up 14.3% over the prior year period, eclipsing 1 million subscribers. Additionally, the company’s brand client base increased to 732 from 708 at the end of Q3.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

FBI Award. Yesterday, V2X announced a $100 million contract award to provide aviation maintenance and support services for the Federal Bureau of Investigation’s (FBI) Critical Incident Response Group. Under this contract, V2X will deliver mission-critical aviation resources that enable the FBI to conduct intelligence gathering, investigate operations, and law-enforcement activities.

Contract Details. The indefinite-delivery, indefinite-quantity contract includes a five-year ordering period with four 12-month options. V2X will operate at multiple locations across the United States for the FBI. We view this award as further client diversification for the Company.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Challenging Conditions. Continuing challenging macroeconomic and business conditions impacted ODP in Q4. ODP Business Solutions faced economic factors that caused enterprise spending constraints in the quarter, while Office Depot had more cautious consumer spending (along with 47 fewer stores). However, fiscal year figures were in-line with management guidance, and management is executing on initiatives to improve traction on both fronts.

4Q Results. Sales for the fourth quarter were $1.62 billion compared to $1.80 billion last year but were above our expectations at $1.55 billion and consensus at $1.61 billion. Net loss totaled $3 million, or $0.10/sh, compared to a loss of $37 million, or $0.96/sh, in the prior year. Adjusted EPS was $0.66 versus $1.13 last year. We were at $0.40 and $0.68, respectively. Adjusted EBITDA totaled $58 million, down from $83 million last year, and we were at $49 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 2 Trial Tests THIO Against THIO With Libtayo. MAIA announced the design of the third stage of the THIO-101 Phase 2 trial, consisting of Expansion and Registration stages. Both stages will enroll patients with non-small cell lung cancer (NSCLC) receiving the regimens as third-line treatment, expected to begin in 1Q25. Following the conclusion of the trial around 4Q25, we expect MAIA to apply for Accelerated Approval from the FDA.

Expansion Stage Is Expected To Begin In 1Q25. The THIO-101 Expansion stage will have two arms to determine the contributions of each drug to patient outcomes. In the first arm, 30 patients will receive the THIO-Libtayo (cemiplimab) combination at the 180mg dose. The second arm will treat 7 patients who were treated with THIO monotherapy to determine its efficacy. If the outcomes of THIO alone are moderate, the treatment arm will be discontinued. If sufficient efficacy is seen, up to 8 more patients will be enrolled for a total maximum enrollment of 48 patients. The primary endpoint is Overall Response Rate (ORR).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q Results. Revenue for the fourth quarter was $283.1 million, an increase from $273.8 million last year but slightly below our $290 million estimate. Gross margin was 24.7% compared to 26.3%. Net income was $3.9 million, or $0.03/sh, from $2.4 million, or $0.02/sh, last year. We estimated net income of $2.5 million or $0.02/sh. Adjusted EPS was $0.13 from $0.12 last year and our $0.10 estimate. Adjusted EBITDA was $25.2 million from $29.1 million last year and our $24 million estimate.

New Joint Venture. Alongside the results was the announcement of a new joint venture with the Company and RAFAEL. The roughly 50/50 partnership is to establish a U.S.-based merchant supplier of solid rocket motors (SRMs) and other energetics named Prometheus Energetics. Up to $175 million in capital is committed between the two companies, with the venture currently forecasted an annual base case revenue of several $100 million a year once at rate production. In our view, the venture can represent a substantial value-creation driver and could potentially drive top and bottom-line growth once up and running.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

More Integration. As promised, Kelly continues to take steps to integrate the Motion Recruitment Partners offerings with Kelly’s offerings. Kelly announced the formation of an integrated permanent hiring solutions business line resulting from the combination of KellyOCG’s global recruitment process outsourcing (RPO) specialty and MRPs’ talent acquisition solutions brand, Sevenstep. The integrated business creates a leading talent solutions offering that ranks among the top five globally.

Detail. The integrated business will oversee a team supporting 71 countries with 33 in-country teams and 19 global hub locations. Sevenstep brings an industry-leading brand and attractive client base to KellyOCG, expanding its RPO scale and capabilities. We believe the KellyOCG and Sevenstep businesses are highly complementary and will deliver an unmatched breadth of service, a high delivery footprint, and innovative technology offerings to clients.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Apollo Global Management in talks to lead $35 billion financing package for Meta’s US data centers – Funding will support Meta’s planned $65 billion AI investment strategy announced by Zuckerberg – Deal represents growing private credit market for AI infrastructure as tech giants race to build capacity

Meta Platforms is pursuing a groundbreaking $35 billion financing package led by Apollo Global Management to accelerate the development of artificial intelligence data centers across the United States, according to sources familiar with the negotiations.

The Facebook parent company is engaging with the alternative asset manager to secure this substantial funding as part of its previously announced $65 billion investment in AI infrastructure planned for 2025. While discussions remain in early stages with no guarantee of completion, the deal represents one of the largest private financing arrangements for technology infrastructure to date.

“The race to build AI infrastructure is creating unprecedented investment opportunities,” said a market analyst who requested anonymity due to the sensitive nature of the ongoing negotiations. “Tech giants are competing for computing power, and Meta is positioning itself to avoid falling behind competitors like Microsoft.”

Meta CEO Mark Zuckerberg outlined the company’s aggressive AI strategy last month, emphasizing plans to construct massive new data centers and expand AI-focused teams. A key component of this vision includes bringing approximately one gigawatt of computing power online in 2025 – enough electricity to power roughly 750,000 homes.

The company has already announced a $10 billion data center in Louisiana and has been actively purchasing advanced computer chips to power its growing suite of AI products and services. This financing arrangement would provide Meta with the capital flexibility to accelerate these initiatives without compromising its balance sheet strength.

For Apollo, the deal aligns with its recent strategy of providing large-scale financing to investment-grade corporations while typically retaining a portion of the funding and syndicating the remainder to other investors. The firm has been expanding its capacity to write substantial checks as it pushes deeper into what it considers the next frontier of private credit markets.

The AI infrastructure boom is creating enormous demand for capital across the technology sector. Industry experts estimate hundreds of billions of dollars will be required to build the necessary data centers, power facilities, and networking infrastructure to support the computing demands of advanced AI systems.

Microsoft, one of Meta’s primary competitors in the AI space, recently announced plans to spend $80 billion on data centers in the current fiscal year. CEO Satya Nadella emphasized that sustaining this level of investment is essential to meet “exponentially more demand” for AI services.

Bankers and investors have been eager to participate in AI-related financing deals after witnessing stock markets heavily reward companies central to the AI ecosystem throughout the past year. Private credit providers like Apollo are increasingly stepping in to fill funding gaps as traditional banks face regulatory constraints on large-scale lending.

Neither Meta nor Apollo provided official comments regarding the potential financing arrangement, maintaining standard practice for deals at this preliminary stage. However, industry observers note that securing this funding would represent a significant strategic advantage for Meta as it competes for AI dominance against tech rivals including Microsoft, Google, and Amazon.

Key Points: – Patient small cap investors view market downturns as chances to acquire quality businesses at discounted prices. – Thorough analysis of small cap companies can uncover exceptional businesses with strong fundamentals before they attract mainstream attention. – The greatest advantage in small cap investing comes from maintaining conviction during periods of underperformance that drive away less patient investors.

In a market often dominated by mega-cap tech stocks and headline-grabbing trends, small cap investing remains a powerful avenue for those willing to embrace patience as their primary strategy. While these smaller companies may lack the immediate name recognition of their larger counterparts, they offer distinct advantages to investors who can weather short-term volatility in pursuit of long-term gains.

The Virtue of Patience in Small Cap Investing

The true edge in small cap investing isn’t found in rapid trading or timing market swings—it’s discovered through patient capital deployment and a steadfast focus on fundamentals. Small cap stocks, typically defined as companies with market capitalizations between $300 million and $2 billion, often experience greater price volatility than large caps. This volatility, rather than representing inherent risk, actually creates opportunities for patient investors.

When market sentiment shifts and institutional investors flee to perceived safety, small caps frequently bear the brunt of the selling pressure. This creates temporary dislocations between price and value that patient investors can explore. While others panic during downturns, disciplined small cap investors recognize these moments as rare opportunities to acquire ownership in quality businesses at discounted prices.

Filtering the Noise to Find Value

Today’s financial ecosystem bombards investors with constant commentary, predictions, and “expert” opinions. Patient small cap investors develop the crucial skill of filtering this noise to identify genuine value. They understand that short-term price movements often reflect temporary factors rather than fundamental business changes.

The ability to separate market noise from meaningful information allows these investors to maintain conviction in their small cap holdings through inevitable periods of underperformance. They recognize that small companies need time to execute their business plans, expand their market presence, and ultimately deliver value to shareholders.

The Power of Thorough Equity Research

In the small cap universe, thorough equity research becomes an invaluable competitive advantage. While large caps are constantly scrutinized by hundreds of analysts, dedicated research into smaller companies can uncover hidden gems before they appear on the institutional radar. Patient investors who commit to comprehensive due diligence often identify promising businesses with robust fundamentals that remain undervalued.

This research advantage becomes especially powerful when investors develop expertise in specific sectors or industries. By understanding the competitive landscape, technological trends, and regulatory environments that shape small cap businesses, patient investors can accurately assess both risks and growth catalysts that casual market participants might miss. This deep research foundation also provides the conviction necessary to hold positions through inevitable market fluctuations.

Embracing the Long View

The most successful small cap investors share a common trait: they evaluate investments through a multi-year lens rather than quarterly results. They understand that compound growth in small businesses can eventually translate into extraordinary investment returns. A company growing earnings at 15-20% annually will double its profits approximately every four years—a powerful driver of long-term stock performance that patient investors can capture.

The Psychological Challenge

Perhaps the greatest challenge in small cap investing isn’t analytical but psychological. It requires the fortitude to remain invested when markets turn negative, when positions move against you, and when the temptation to chase better-performing assets becomes strongest. Patient investors understand that their edge comes precisely from accepting short-term discomfort that others refuse to endure.

For those willing to cultivate patience, small cap investing continues to offer one of the most compelling risk-reward propositions in public markets. By focusing on long-term business value rather than short-term price fluctuations, investors can position themselves to achieve returns that make the occasional storms worth weathering.

SAN DIEGO, Feb. 26, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in the defense, national security and global markets, and RAFAEL Advanced Defense Systems Ltd., today announced an approximate 50/50 partnership for the establishment of a U.S.-based merchant supplier of solid rocket motors (SRMs) and other energetics. The new joint venture, named Prometheus Energetics (“Prometheus”), is set to be headquartered on an approximate 500-acre site near the United States Navy and Army facility in Crane, Indiana.

Kratos and RAFAEL (through its U.S. based subsidiary RAFAEL USA) have jointly committed up to $175 million in capital for the establishment of Prometheus and required property, plant, equipment and personnel needed for the new, state-of-the-art energetics manufacturing campus and facilities. After construction of the plant and once RAFAEL’s technology transfer is completed and certified for operations, Prometheus is projected to begin production in 2027 of SRMs.

RAFAEL is the developer and manufacturer of unique, world-renowned systems such as the Iron Dome and the TROPHY APS which are in service in the Israeli Defense Forces as well as the David’s Sling which provides the middle layer of air defense for the state of Israel. The company, originally established as the IDF Science Corps, has developed groundbreaking technologies like high energy laser solutions like the Iron Beam which are expected to be operational by the end of 2025. The company functions through a vertical integration structure that enables a unique ability to meet the demands and overcome the challenges of the global market and supply chain. RAFAEL offers a diverse portfolio from new space to the ground battlespace with battle-proven technologies.

Kratos is a leader in hypersonic or advanced systems, strategic systems, ballistic missile targets, sub-orbital research vehicles, sounding rockets, and solid rocket motors. Kratos has served the U.S. advanced systems and missile defense communities for decades, delivering numerous novel systems and vehicle flight tests. Kratos is the only company today delivering both propulsion and advanced flight systems, with Kratos advanced systems including the low-cost Erinyes Glide Vehicle, Dark Fury, Zeus and Oriole Solid Rocket Motors, and other Kratos systems and technologies. Kratos provides unmatched innovation, disruptive capabilities, mission responsiveness and affordability to our customers across our portfolio of systems.

Eric DeMarco, President and CEO of Kratos Defense, said, “We believe Prometheus, once up and running at full rate production, will be a step function catalyst in value creation for Kratos’ stakeholders and the U.S. defense industrial base, similar to Kratos’ recent MACH-TB contract award—the largest single-award contract in Kratos history. Like other major Kratos investments such as Oriole, Zeus, and Erinyes, Prometheus responds to a critical need to strengthen the U.S. Industrial Base and will also provide tens of thousands of SRMs and casted warheads supporting both America’s most reliable partner in the Middle East and United States national security related demand from a true SRM and energetics merchant supplier.”

Kratos will reflect Prometheus in its consolidated financial statements on the Equity Method of Accounting, under which Kratos will record approximately 50 percent of Prometheus Net Income on a single line “Net Income from Prometheus Energetics” in its income statement, and Kratos will annually receive approximately 50 percent of the Free Cash Flow generated from Prometheus. Kratos intends to continue to report Kratos Operating Income, Net Income, Adjusted EBITDA and other financial matrices separate from the Prometheus results, in order for all Kratos stakeholders to be able to follow the progress of each Company, the investment made in Prometheus and the future return on Kratos’ investment in Prometheus.

RAFAEL Advanced Defense Systems Ltd., one of Israel’s largest defense contractors, develops, manufactures, and sustains combat-proven technologies, products, and systems-of-systems for air, land, naval, space and digital applications. RAFAEL’s delivery of combat-proven systems is supported by vertically integrated facilities and engineering teams servicing the development and production of SRMs and warhead (WH) products that play a critical role in Israel’s Iron Dome, the world’s premier air defense system designed to intercept and destroy short-range rockets, artillery shells, UAVs, and other aerial threats. This vertical integration has made RAFAEL a leading expert in SRMs and WH development and production, allowing it to continuously expand capabilities and push the envelope in technology, performance, and fielding of effective systems. RAFAEL’s multi-dimensional portfolio and unique innovative capabilities have enabled the development of world-leading technologies across all spheres.

Yoav Tourgeman, President and CEO of RAFAEL Advanced Defense Systems Ltd., said: “The establishment of Prometheus Energetics is a strategic leap forward, reinforcing RAFAEL’s commitment to strengthening the U.S. defense industrial base while ensuring our allies and partners have access to the most advanced, combat-proven energetics solutions. This step constitutes a strategic vector that combines business considerations in the American market with the increasing demand for energetic products, while significantly enhancing our ability to deliver resilient and reliable supply solutions to our customers. Through this joint venture, we are deepening our longstanding partnership with the United States, strengthening supply chain independence, and bolstering the critical capabilities needed to address evolving national security challenges.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

About RAFAEL Advanced Defense Systems Ltd. Established in 1948, RAFAEL Advanced Defense Systems Ltd. develops, manufactures, and sustains combat-proven technologies, products, and systems-of-systems for air, land, naval, space and digital applications. As the developer of two integral layers of Israel’s multi-layered air defense array and the developer of the world’s only operation active protection system TROPHY APS, the company offers innovative and proven solutions for the global market. RAFAEL’s air defense portfolio has achieved international recognition from Iron Dome to David’s Sling and is expected to provide the first ever operational high-energy laser weapon system to the IDF by 2025. The company has bolstered its international standing as a top-tier defense manufacturer by through an innovative approach of vertical integration enabling seamless technology transfer and local production, making it a trusted partner for defense solutions in global markets, particularly in the U.S. where its systems strengthen national security priorities. Leveraging its technological ingenuity, operational experience, and unparalleled understanding of evolving combat requirements, RAFAEL provides global warfighters with today’s most advanced technologies and life-saving defense solutions that ensure operational superiority. RAFAEL’s strategy includes strategic international partnerships and localization to ensure customer sovereignty. For more information on RAFAEL, please visit https://www.rafael.co.il/

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

NEW ALBANY, Ohio, Feb. 26, 2025 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI) will hold its quarterly conference call on Tuesday, March 11, 2025, at 8:30 a.m. ET, to discuss fourth quarter and full year 2024 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (800) 549-8228 using conference code 45919. International participants dial (289) 819-1520 using conference code 45919. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

A telephonic replay of the conference call will be available until March 25, 2025. To access the replay, toll-free callers can dial (+1) 888 660 6264 using access code 45919#, and toll callers in North America and other locations can dial (+1) 289 819 1325.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com