Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Contracts. Kratos has been awarded some additional significant contracts over the past two weeks, maintaining the momentum of award receipt over the past couple of quarters. We believe the new awards demonstrate the Company’s multi-sector capabilities.

Award 1. Kratos received a single-award, indefinite-delivery/indefinite-quantity contract with a ceiling value of $579 million for the Command-and-Control System Consolidated (CCS-C) Sustainment and Resiliency. Space Systems Command (SSC) is the contracting activity for the award. Kratos will sustain and provide post-production development for the current CCS-C system for telemetry, tracking and commanding of current and future military communication satellites.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

As the next pivotal United Nations climate change conference quickly approaches, the COP28 summit to be held in Dubai has already attracted controversy before it even begins. Critics argue the UAE’s plans to use its host status to lobby for oil and gas deals creates an irreconcilable conflict of interest. This brewing scandal underscores risks for the energy investment community in navigating the global green transition.

Leaked documents revealed the summit’s president, Sultan Al-Jaber, intends to meet with officials from over a dozen countries to promote fossil fuel projects. As CEO of Abu Dhabi National Oil Company (ADNOC), the world’s 12th largest oil producer, Al-Jaber seemingly represents business as usual in the hydrocarbon sector – precisely as climate scientists urge rapid movement away from planet-warming emissions. This dual role as OPEC’s former president alongside COP28 president epitomizes the conference’s core tension.

While the UAE defends Al-Jaber’s energy background as an asset for summit leadership, others see an fox guarding the henhouse. Renewable energy interests hope COP meetings accelerate emissions cuts to open investment opportunities and meet targeted market shares. In contrast, unchecked fossil fuel dominance could strand assets and leave oil-rich economies behind. For financial institutions, balancing these competing interests grows increasingly complex.

As the global community seeks alignment on climate policy, COP28 takes on heightened importance after last year’s loss of momentum in Egypt. But with Al-Jaber pushing liquefied natural gas deals behind the scenes, the summit’s bold ambitions appear under threat – before even officially starting next week. This risks paralyzing investors betting on meaningful multilateral progress from the 12-day affair.

Rather than showcasing global unity, the conference could further fragment cooperative efforts. Those banking on strengthened commitments and standardized transparency may be severely disappointed. An already divided energy landscape would only become more fractured and filled with uncertainties.

While surging energy prices have boosted oil and gas profits recently, leaving firms cash rich for transitions, alerts sound over stranded asset dangers in the longer run. Without reliable political tailwinds, capital allocation planning swims in obscurity. Investors may continue clinging to the devil they know, slowing sustainability spending despite rhetorical Net Zero pledges.

ESG fund managers face particularly hard choices weighing reputational concerns with fiduciary obligations, as greenwashing allegations persist. Index providers must carefully contemplate emissions-heavy exposure amid heightening transition materiality. Even hydrocarbon majors pursuing renewables see climate credibility doubly damaged by COP28 coziness with embedded fossil fuel agendas.

In effect, the UAE’s COP28 aspirations throw harsh light on the messy entanglements linking energy incumbents to global cooperation imperatives. This summit was envisioned for closing gaps to carbon neutrality – not leveraging elite access for oil field services contracts or petrochemical exports. Dubai’s shone vision as progressive climate broker now sees tarnish.

While Al-Jaber resides at the controversy’s core, larger questions confront energy interests worldwide. How can multinational forums effectively drive sustainability without undermining diverse domestic interests or economic lifelines? Does climate progress rely on energy industrialists gradually conceding ground? Regardless of COP28’s impact, these dilemmas will persist in boardrooms everywhere industries collide with ecological boundaries.

For anxious energy investors, perhaps the greatest risk is policy paralysis. Without milestone markers implemented, capital deployment floats ambiguously while net-zero targets linger out of reach. Until political will consolidates around winding down emissions directly, bankers and shareholders face accumulating uncertainty handicapping strategic decision-making.

Of course, COP meetings have always brought thorny issues to the surface divisions easy to ignore otherwise. But the solution remains clear even if the path does not: economics needs ecology for human prosperity’s endurance. For financial players, that means sustained stakeholder value depends on sustainable business practices without exception. What hangs in the balance moving forward is how smoothly the global energy complex can stick that critical landing.

The Russell 2000 index has been an overlooked area of the stock market this year, dominated by the headlines and volatility of mega-cap tech and blue chips. However, a seismic shift occurred last Wednesday when the Russell 2000 rallied over 6% for its best day since March, turning positive for 2023.

This index of approximately 2,000 small-cap stocks just made Wall Street wake up and take notice thanks to this violent swing. Now is the time for investors to understand what’s driving the resurgence and how to capitalize in small caps.

What is the Russell 2000 and Why Does It Matter?

The Russell 2000 index measures the performance of U.S. small-cap stocks with market caps below $3.7 billion. Weights are assigned by market cap, so the index serves as a benchmark for bonafide smaller firms. These companies tend to be younger with higher volatility and growth prospects.

As a result, the Russell 2000 provides a barometer of investor sentiment towards risk assets. Turning points in the index can indicate shifts in the overall stock market as traders move towards or away from speculation.

The recent 6%+ rally last Wednesday jolted the Russell 2000 into positive return territory for the year so far, now up 4% year-to-date. This signals a potential appetite for risk returning to markets, with traders betting on outsized returns potential in small caps after a prolonged lull.

Why Invest in Small Caps?

Investing in Russell 2000 companies over other stocks has compelling advantages if timed appropriately in the market cycle. First, smaller firms have lower visibility and coverage, so mispricings are more common. This creates pockets of opportunities for above-average returns compared to efficient larger cap markets.

Finally, identifying world-changing new products and innovations is easier in earlier stage small caps not yet on the main stage. Getting in early on the next Roku, Tesla, or Shake Shack while still qualifying for the 2000 index can deliver truly explosive portfolio growth.

What Investors Should Watch Next

Markets are now intently watching the Russell 2000 to see if last week’s awakening of small-cap animal spirits has true staying power. Traders want confirmation that the breakout can lead to a sustained run versus just being a short-lived dead cat bounce.

If the rally holds, it solidifies the thesis of rotating back towards risk—and earlier stage small names often lead the way in such environments. Savvy investors will use this volatility to start building positions in promising small caps with expanding growth prospects.

The secret is identifying the next crop of disruptors poised to multiply before the herd catches on. By getting ahead of the crowd now eyeing the Russell 2000’s surge, spectacular returns await those able to time the next leg up.

Bargain Hunting for Small Caps at NobleCon

One of the most effective ways to identify the small caps destined to drive the next market boom is to connect directly with leadership at the source. The annual NobleCon investor conference gives the opportunity for exactly that.

On December 3-5 in Boca Raton, Florida, small-cap firms will present their latest innovations, opportunities, and reasons to invest. Attendees gain first look access to fast-growing startups and tomorrow’s giants while they still qualify for the Russell 2000. Now in its 19th year, NobleCon19 promises to uncover the next crop of small cap innovators during the multi-day conference.

For investors looking to capitalize on the Russell 2000’s resurgence, NobleCon19 provides the direct pipeline to target ideas perfectly positioned to ride the reawakening wave in small caps. To learn more and register, visit www.noblecon19.com before discounted early bird rates expire.

Black Friday 2023 is officially here, kicking off the year’s biggest shopping weekend both online and in stores. Early indicators suggest consumers are hungry for deals, with e-commerce sales on Thanksgiving Day jumping 5.5% year-over-year to $5.6 billion according to Adobe Analytics.

The robust online sales activity on Turkey Day comes ahead of an expected $9.6 billion in Cyber Monday revenue, a 5.7% increase from last year. While these growth figures represent a slowdown from the blistering pace set during the pandemic, they highlight that holiday shoppers are still responding to discounts even amidst broader economic uncertainty.

This sets the stage for a pivotal Black Friday that may determine whether projections for up to 4% gains in total holiday sales materialize. Shoppers are expected to turn out in force to scoop up deals on popular items like toys, apparel, jewelry, and consumer tech that were top sellers online on Thanksgiving.

Mobile Shopping Surge Drives Online Revenue

Fueling the growth in Thanksgiving e-commerce sales is the continued surge in smartphone shopping. A record 59% of online revenue came from mobile devices as people browsed and bought gifts on the go. With mobile penetration rising every year, retailers have adapted their sites and apps to make it easier for iPhone and Android users to capitalize on promotions.

Savvy shoppers are discovering they can beat crowds and inventory shortages by taking advantage of online-only deals as well as ordering online and picking up in store. Retailers are encouraging this omnichannel behavior by making curbside pickup fast and frictionless. The convenience of mobile ordering combined with flexible fulfillment options underlies the shift towards more Thanksgiving and Black Friday spending happening digitally.

Top Deals Entice Consumers

Despite economic pressures from inflation and higher interest rates, consumers have shown a willingness to spend when the price is right. Adobe tracked toys discounted up to 28%, electronics up to 27% off, and computers 22% off on Thanksgiving, leading to triple-digit surge in those categories versus October.

Amazon and Target rolled out additional Black Friday toy deals with major markdowns on Barbie dream campers, Marvel action figures, and Nintendo Switch gaming bundles expected to rank among the most popular purchases.

Similarly, doors opening early at retailers like Best Buy, Walmart, and Apple will likely attract shoppers chasing deals on big-screen TVs, Bluetooth speakers, tablets, and the hot new Airpods Pro 2 earbuds. Though buying conditions are tougher this year, bargain hunters still prioritize snagging discounted must-have gifts for loved ones.

What’s at Stake for Retailers

While Thanksgiving and Black Friday don’t determine overall holiday fortunes, they set the tone for retailers during the critical year-end sales period. Those who miss targets this weekend play catch-up and may have to result to profit-busting promotions to move stagnant inventory later in December.

However, retailers who excite shoppers out the gates with alluring deals and experiences create positive momentum they can ride into the New Year. The outperformance of those players better able to adapt to the mobile and omnichannel-centric future of holiday shopping will be on full display this weekend.

For consumers, the state of Black Friday offers clues into buying conditions for the next month as they weigh completing wish lists amidst budget realities. With early reads tilting positive, cautious optimism seems warranted – though restraint may still pay off waiting to see if deals sweeten further in December.

One thing is certain: all eyes turn to how activity plays out on the unofficial start to the holiday sales season. Black Friday retains symbolic importance for retailers and consumers alike – so expect the 2023 version to again provide intrigue and insights into the health of the US consumer.

Vancouver, British Columbia–(Newsfile Corp. – November 22, 2023) – Maple Gold Mines Ltd. (TSXV: MGM) (OTCQB: MGMLF) (FSE: M3G) (“Maple Gold” or the “Company“) today announced that its Board of Directors has appointed Mr. Kiran Patankar to the positions of President and Chief Executive Officer, effective immediately. Mr. Patankar had served as Interim President and Chief Executive Officer since August 28, 2023. Mr. Patankar has also joined the Board of Directors of Maple Gold.

“We are pleased to appoint Kiran Patankar as President and Chief Executive Officer of Maple Gold,” stated Michelle Roth, Maple Gold’s Chairperson, speaking on behalf of the Board. “From the time he was appointed Interim President and Chief Executive Officer in August 2023, Kiran has spearheaded the execution of the Company’s updated corporate strategy, which includes a thorough assessment of our district-scale Québec gold projects. He has fostered alignment between our technical team and our strategic and joint venture partner to improve exploration targeting and optimize results, while also driving significant overhead cost reductions. Kiran is an experienced corporate leader with a track record of successful team building and deep mining industry connections. We are fortunate to be able to harness his skills, temperament and steady hand to steer the Company in a new direction to enhance shareholder value.”

“I am delighted and honored to lead Maple Gold into its next phase of growth,” stated Kiran Patankar, President and CEO of Maple Gold. “While current market conditions remain challenging for junior gold explorers, our strong financial position, including nearly C$5 million of available liquidity as of September 30, 2023, combined with cost reduction efforts and a new value-oriented exploration approach in ongoing partnership with Canada’s largest gold producer ideally positions the Company to discover the next major gold camp in Québec’s prolific Abitibi Greenstone Belt. I look forward to working with the dedicated team and Board of Directors at Maple Gold to build upon the Company’s strong foundation and contribute to its future success.”

Mr. Patankar has more than 15 years of senior leadership experience in the mining industry. He has served as Maple Gold’s Interim President and Chief Executive Officer since August 2023, after serving as the Company’s Chief Financial Officer since 2022 and its Senior Vice President, Growth Strategy since 2021. From 2015 to 2018, Mr. Patankar served as President, CEO and a Director of two TSX-V listed gold exploration and development companies, where he led growth initiatives and orchestrated successful company turnarounds. As an investment banker with leading Canadian and global financial institutions from 2007 to 2014, he worked exclusively with mining companies on strategic corporate matters and executed M&A and corporate finance transactions totaling more than C$3 billion in value. Mr. Patankar holds a Bachelor of Science in Geological Engineering from the Colorado School of Mines and an MBA from the Yale School of Management.

Q3 2023 Financial Results

The Company filed its Q3 2023 Financial Statements and MD&A on SEDAR+ (www.sedarplus.ca) on November 20, 2023. The Company’s Q3 2023 Financial Statements and MD&A are also available on the Company’s website (www.maplegoldmines.com).

Equity Incentive Plan Grants

Pursuant to its Equity Incentive Plan (the “Plan”) dated December 17, 2020, as amended, and the policies of the TSX Venture Exchange, the Company’s Board of Directors granted stock options (“Options”) and Restricted Share Units (“RSUs”) to certain employees, officers, directors and consultants. The Company granted Options to purchase an aggregate of 3,825,000 common shares of the Company (each, a “Common Share”), with an exercise price of $0.06 per Common Share. Each Option grant vests in three equal tranches over a 24-month period. Once vested, each Option is exercisable into one Common Share for a period of five years from the date of the grant. The Company also granted a total of 400,000 RSUs. Each RSU grant vests in three equal tranches over a 24-month period. Once vested, each RSU entitles the holder thereof to receive either one Common Share, the cash equivalent of one Common Share or a combination of cash and Common Shares, as determined by the Company, net of applicable withholdings.

The Company also terminated an aggregate of 4,125,000 Options that were previously granted to certain former employees and consultants who are no longer providing services to the Company.

About Maple Gold

Maple Gold Mines Ltd. is a Canadian advanced exploration company in a 50/50 joint venture with Agnico Eagle Mines Limited to jointly advance the district-scale Douay and Joutel gold projects located in Québec’s prolific Abitibi Greenstone Gold Belt. The projects benefit from exceptional infrastructure access and boast ~400 km2 of highly prospective ground including an established gold resource at Douay (SLR 2022) that holds significant expansion potential as well as the past-producing Eagle, Telbel and Eagle West mines at Joutel. In addition, the Company holds an exclusive option to acquire 100% of the Eagle Mine Property.

The district-scale property package also hosts a significant number of regional exploration targets along a 55 km strike length of the Casa Berardi Deformation Zone that have yet to be tested through drilling, making the project ripe for new gold and polymetallic discoveries. The Company is well capitalized and is currently focused on carrying out exploration and drill programs to grow resources and make new discoveries to establish an exciting new gold district in the heart of the Abitibi. For more information, please visit www.maplegoldmines.com.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS PRESS RELEASE.

Forward-Looking Statements:

This press release contains “forward-looking information” and “forward-looking statements” (collectively referred to as “forward-looking statements”) within the meaning of applicable Canadian securities legislation in Canada, including statements about exploration work and results from current and future work programs. Forward-Looking statements are based on assumptions, uncertainties and management’s best estimate of future events. Actual events or results could differ materially from the Company’s expectations and projections. Investors are cautioned that forward-looking statements involve risks and uncertainties. Accordingly, readers should not place undue reliance on forward-looking statements. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to Maple Gold Mines Ltd.’s filings with Canadian securities regulators available on www.sedarplus.ca or the Company’s website at www.maplegoldmines.com. The Company does not intend, and expressly disclaims any intention or obligation to, update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by law.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. The company reported $2.9 million in revenue, which was in-line with our estimate of $2.6 million. Adj. EBITDA loss of $1.4 million was modestly lower than our estimate of a loss of $0.8 million. Notably, Q3 operating results were affected by less QVC programming due to talent scheduling conflicts related to a return to an in-studio production policy and non-recurring restructuring expenses.

Favorable licensing model. In November, the company completed its transition to a licensing model, and should report the last portion of its restructuring costs in Q4. Notably, we anticipate significant reductions in direct operating expenses from 2022 levels of roughly $7.5 million to roughly $4.0 million in 2024. Additionally, in Q4, we estimate sequential licensing revenue growth from Q3.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2023-2Q production rose as expected with new wells coming online. A robust summer of drilling resulted in higher production. Post-quarter flow rates allow us to bump up future production estimates.

Realized prices came in better than expected. The basin discount was reduced adding to the rise in oil index prices. Management added swaps at attractive prices in response to higher oil prices.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Oil markets were thrown into turmoil on Wednesday after the OPEC+ alliance unexpectedly postponed a critical meeting to determine production levels. Prices promptly plunged over 5% as hopes for additional output cuts to stabilize crude markets were dashed, at least temporarily.

The closely-watched meeting was originally slated for December 3-4. But OPEC+, which includes the 13 member countries of the Organization of Petroleum Exporting Countries along with Russia and other non-members, said the summit would now take place on December 6 instead, offering no explanation for the delay.

The last-minute postponement fueled speculation that the group is struggling to build consensus around boosting production cuts aimed at reversing oil’s steep two-month slide. Disagreements apparently center on Saudi dissatisfaction with other nations flouting their output quotas. Compliance has emerged as a major flashpoint as oil revenue pressures intensify amid rising recession fears.

Prices Rally on Cut Hopes

In recent weeks, oil had rebounded from mid-October lows on mounting expectations that OPEC+ would intervene to tighten supply and put a floor under prices once more.

The alliance has already removed over 5 million barrels per day since 2023 through unilateral Saudi production cuts and collective OPEC+ reductions. But crude has continued drifting lower, with Brent plunging below $80 per barrel last week for the first time since January.

Demand outlooks have deteriorated significantly, especially in China where crude imports fell in October to their lowest since 2007. At the same time, releases from strategic petroleum reserves and resilient non-OPEC production have expanded inventories, exacerbating the supply glut.

Output Quotas Trigger Internal Rifts

Energy analysts widely anticipate that OPEC+ will finalize plans at next week’s rescheduled talks to extend existing production cuts until mid-2024. Saudi Arabia and Russia, the alliance’s de factor leaders, both support additional trims.

However, firming up commitments from the broader group may prove challenging. Crude exports are critical to the economies of many member nations. With government budgets squeezed by weakened prices, some countries have little incentive to curb production.

Unconfirmed reports suggest that Saudi Arabia demanded Iraq and several other laggards bolster compliance with quotas before it agrees to further output reductions. But getting all parties in line with their assigned targets has long confounded the alliance.

Where Oil Goes Next

For now, oil markets are in limbo awaiting next Thursday’s OPEC+ gathering. Prices could see added volatility until the cartel unveils its plans.

Most analysts still expect that additional cuts will emerge, possibly in the 500,000 barrels per day range. That may be enough to place a temporary floor under the market and keep Brent crude from approaching $70 per barrel.

But if internal dissent paralyzes OPEC+ from reaching an agreement, or one that falls significantly short of projections, another downward spiral is probable. Pressure would only escalate on the alliance to take more drastic actions to stabilize prices in 2024 as economic storm clouds gather.

In a watershed moment for cryptocurrency oversight, Changpeng Zhao, billionaire founder of crypto exchange Binance, pleaded guilty on Tuesday to charges related to money laundering and sanctions violations. Binance itself also pleaded guilty to similar criminal charges for failing to prevent illegal activity on its platform.

The guilty pleas are part of a sweeping, coordinated crackdown on Binance by U.S. law enforcement and regulators. As part of the settlement, Binance agreed to pay over $4 billion in fines and penalties to various government agencies. Zhao himself will personally pay $200 million in fines and has stepped down as CEO.

The implications of this development on the broader crypto sector could be profound. As the world’s largest crypto trading platform, Binance has played an outsized role in the growth of the industry. Its legal troubles and the record penalties imposed call into question the viability of exchanges that flout compliance rules in the name of rapid expansion.

Prosecutors allege that Binance repeatedly ignored anti-money laundering obligations and allowed drug traffickers, hackers, and even terrorist groups like ISIS to freely use its platform. According to the Department of Justice, Binance processed transactions for mixing services used to launder money and facilitated over 1.5 million trades in violation of U.S. sanctions.

U.S. authorities were unequivocal in their criticism of Binance’s focus on profits over meeting regulatory requirements. This suggests that other exchanges that aggressively pursued growth while turning a “blind eye” to compliance may face similar crackdowns in the future. The $3.4 billion civil penalty imposed on Binance also sets a benchmark for potential fines other non-compliant entities may confront.

The charges against the world’s largest crypto exchange and its high-profile leader represent federal authorities’ most aggressive action yet to rein in lawlessness in the cryptocurrency industry. Officials made clear they will continue targeting crypto companies that break laws around money laundering, sanctions evasion, and other illicit finance.

More broadly, CZ’s guilty plea underscores the pressing need for sensible guardrails if crypto is to shed its reputation as primarily facilitating illegal activity. Though blockchain technology offers many potential benefits, its pseudonymous nature makes it vulnerable to abuse by criminals and terrorists financing unless exchanges rigorously verify customer identities and the source of funds.

For the wider crypto sector, the Binance takedown may spur valuable change. Many experts argue overly lax regulation allowed crypto exchanges to ignore Anti-Money Laundering rules other financial institutions must follow. The billion-dollar penalties against Binance could convince the industry it’s cheaper to self-regulate.

The Binance case may accelerate calls for a regulatory framework tailored to the unique risks posed by cryptocurrencies. Rather than stifle innovation in this nascent industry, thoughtful policies around KYC, anti-money laundering, investor protections and other issues could instill greater confidence in cryptocurrencies among mainstream investors and financial institutions.

Of course, because cryptocurrency transactions are pseudonymous, crypto will likely remain appealing for certain unlawful activities like narcotics sales and ransomware. But with Binance’s guilty plea, regulators sent the message that flagrant non-compliance will not fly. Exchanges allowing outright criminal abuse may face existential legal threats.

For exchanges determined to operate legally, the Binance debacle highlights the existential risks of non-compliance. No matter how large or influential, exchanges that refuse to meet their regulatory responsibilities risk jeopardizing their futures. Expect most exchanges to immediately review their KYC and AML policies in the wake of the Binance penalties.

At minimum, the charges will likely damage Binance’s reputation. Although the company remains operational, it could lose market share to competitors perceived as more law-abiding. For crypto investors, the uncertainty and loss of trust surrounding such a dominant player create fresh volatility in already turbulent markets.

Perhaps most profoundly, seeing handcuffs slapped on crypto’s one-time “king” punctures the industry’s former aura of impunity. After the Binance takedown, ongoing federal probes into FTX and other exchanges, and Sam Bankman-Fried’s criminal conviction, crypto fraudsters might finally fear the consequences many avoided for so long. For better or worse, crypto is evolving.

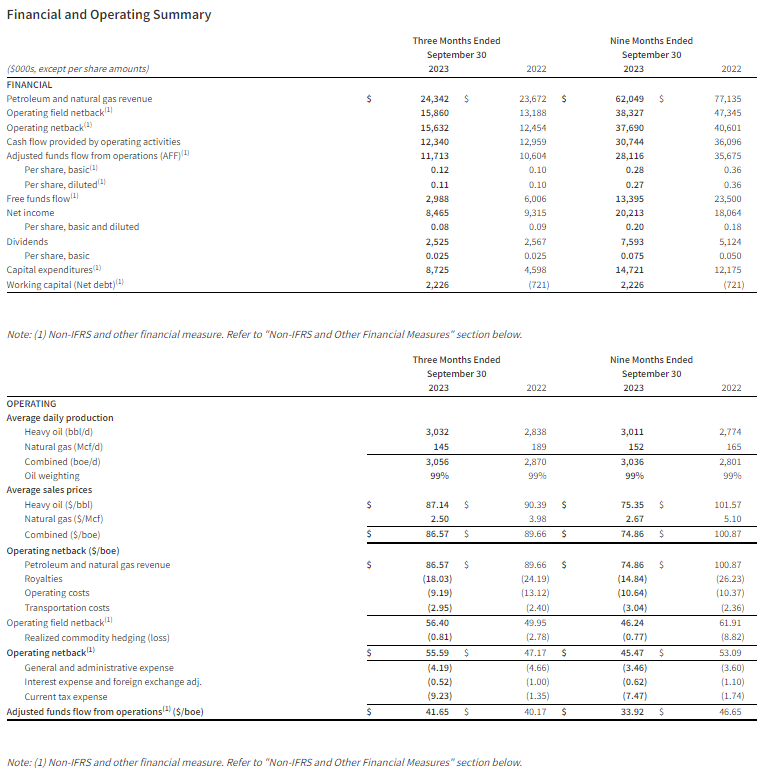

Vancouver, British Columbia–(Newsfile Corp. – November 21, 2023) – Hemisphere Energy Corporation (TSXV: HME)(OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide its financial and operating results for the three and nine months ended September 30, 2023, announce the declaration of a quarterly dividend payment to shareholders, and provide an operations update.

Q3 2023 Highlights

Second best quarter in corporate history for production, revenue, operating field netback, and adjusted funds flow from operations (“AFF”)1.

Produced an average of 3,056 boe/d for the third quarter of 2023, a 6% increase over the same quarter last year.

Attained third quarter revenue of $24.3 million, a 3% increase over the third quarter last year.

Delivered an operating field netback1 of $15.9 million or $56.40/boe for the quarter.

Realized quarterly adjusted funds flow from operations (AFF) of $11.7 million or $41.70/boe.

Announced Hemisphere’s first ever special dividend to shareholders of $0.03 per common share ($3.0 million), paid on November 1, 2023.

Distributed $0.025 per common share ($2.5 million) in quarterly dividends to shareholders in accordance with the Company’s dividend policy.

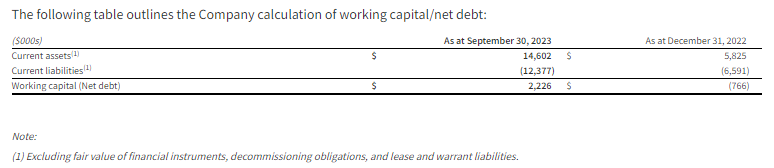

Exited the third quarter of 2023 with a positive working capital1 position of $2.2 million, compared to net debt1 of $0.7 million at September 30, 2022.

Renewed the Company’s Normal Course Issuer Bid (“NCIB”).

Purchased and cancelled 519,400 shares under the Company’s NCIB during the third quarter (at an average price of $1.23 per common share).

(1) Operating field netback, adjusted funds flow from operations (AFF), free funds flow, working capital, and net debt are non-IFRS measures that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s Financial Statements and related Management’s Discussion and Analysis for the quarter ended September 30, 2023, which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend and Shareholder Return

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on December 28, 2023 to shareholders of record as of the close of business on December 15, 2023. The dividend is designated as an eligible dividend for income tax purposes.

With $13.1 million distributed through quarterly and special dividends by year-end and $3.7 million spent on NCIB year-to-date, a minimum of $16.8 million is anticipated to have been returned to shareholders in 2023. Based on the Company’s current market capitalization of $128 million (99.7 million shares issued and outstanding at market close price of $1.28 per share on November 20, 2023), this represents an annualized yield of 13% to Hemisphere’s shareholders.

Operations Update

During the third quarter, Hemisphere completed the majority of its planned 2023 capital expenditure program. By the end of September, the Company had brought on 7 new wells and completed one new well as an injector in the Atlee Buffalo area. Subsequent to quarter-end, the Company also shut one producing well in to convert it to an injector.

Current corporate production sits at approximately 3,350 boe/d (99% heavy oil, based on field estimates between October 1 – November 15, 2023). The Company’s assets continue to perform well under Enhanced Oil Recovery (“EOR”) with current corporate production almost 20% higher than full-year 2022 production, which was just over 2,800 boe/d. Operating and transportation costs during the first nine months of 2023 total just $13.68/boe, and are fully reflective of the chemical costs required for the Company’s two EOR projects. This makes Hemisphere one of the lowest cost operators of heavy oil in the Canadian oil industry.

Looking ahead into 2024, Hemisphere is actively preparing for a new pilot polymer flood on its recently acquired land base. Management anticipates that a test pad could be drilled and on production with a polymer skid installed by as early as July 2024. The Company expects to release more details on its 2024 guidance in January.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value per share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets using EOR techniques. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that a dividend will be paid December 28, 2023 to shareholders of record as of the close of business on December 15, 2023; that a minimum of $16.8 million is anticipated to have been returned to shareholders in 2023; Hemisphere’s plans for a new pilot polymer flood on its recently acquired land base and the timing for test pad drilling, polymer skid installation, and production dates thereof; and timing for further details on its planned operations or guidance.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the effects of inflation of Hemisphere’s budgeted costs; the perspectivity of recently acquired properties and the timing and manner to explore and develop the same; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Market, Independent Third Party and Industry Data

This news release set forth Hemisphere’s belief with respect to being one of the lowest cost operators of heavy oil in the Canadian oil industry. Such statement is based, in part, on third party information, including from industry participant public filings or government or other independent industry publications and reports or based on estimates derived from such publications and reports. Government and industry publications and reports generally indicate that they have obtained their information from sources believed to be reliable, but Hemisphere has not conducted its own independent verification of such information. This news release also includes certain data derived from independent third parties. While Hemisphere believes this data to be reliable, market and industry data is subject to variations and cannot be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey. Hemisphere has not independently verified any of the data from independent third party sources referred to in this news release or ascertained the underlying assumptions relied upon by such sources.

Non-IFRS and Other Financial Measures

This news release contains the terms adjusted funds flow from operations, operating field netback and operating netback, capital expenditures and working capital/net debt, which are considered “non-IFRS financial measures” and any of these measures calculated on a per boe or share basis, which are considered “non-IFRS financial ratios”. These terms do not have a standardized meaning prescribed by IFRS. Accordingly, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. Investors are cautioned that these measures should not be construed as an alternative to net income (loss) or cashflow from operations determined in accordance with IFRS and these measures should not be considered to be more meaningful than IFRS measures in evaluating the Company’s performance.

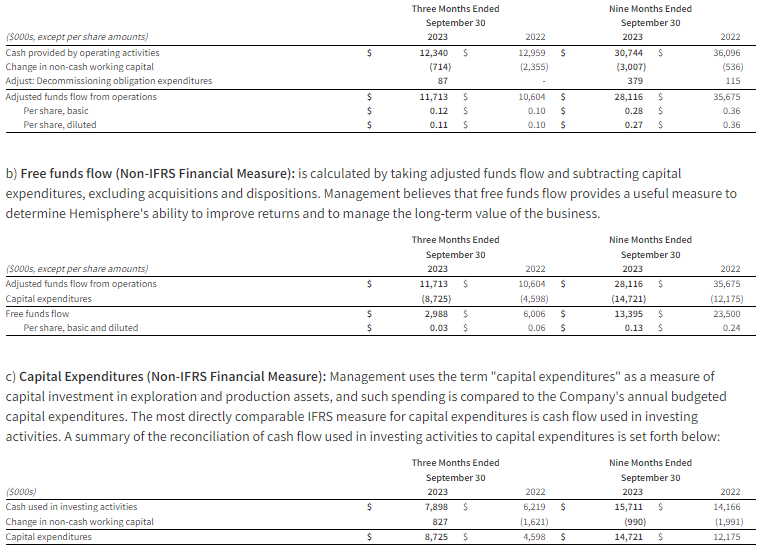

a) Adjusted funds flow from operations “AFF” (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): the Company considers AFF to be a key measure that indicates the Company’s ability to generate the funds necessary to support future growth through capital investment and to repay any debt. AFF is a measure that represents cash flow generated by operating activities, before changes in non-cash working capital and adjusted for decommissioning expenditures, and may not be comparable to measures used by other companies. The most directly comparable IFRS measure for AFF is cash provided by operating activities. AFF per share is calculated using the same weighted-average number of shares outstanding as in the case of the earnings per share calculation for the period. AFF per boe is calculated by dividing AFF by the total production in boe for the reporting period.

A reconciliation of AFF to cash provided by operating activities is presented as follows:

d) Operating field netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): is a benchmark used in the oil and natural gas industry and a key indicator of profitability relative to current commodity prices. Operating field netback is calculated as oil and gas sales, less royalties, operating expenses and transportation costs on an absolute and per barrel of oil equivalent basis. These terms should not be considered an alternative to, or more meaningful than, cash flow from operating activities or net income or loss as determined in accordance with IFRS as an indicator of the Company’s performance.

e) Operating netback (Non-IFRS Financial Measure and Ratio if calculated on a per boe basis): calculated as the operating field netback plus the Company’s realized commodity hedging gain (loss) on an absolute and per barrel of oil equivalent basis.

f) Working Capital/Net debt (Non-IFRS Financial Measure): is closely monitored by the Company to ensure that its capital structure is maintained by a strong balance sheet to fund the future growth of the Company. Working capital/Net debt is used in this document in the context of liquidity and is calculated as the total of the Company’s current assets, less current liabilities, excluding the fair value of financial instruments, decommissioning obligations, and lease liabilities, and including any bank debt. There is no IFRS measure that is reasonably comparable to working capital/net debt.

g)Supplementary Financial Measures and Non-GAAP Ratios

“Transportation costs per boe” is comprised of transportation expense, as determined in accordance with IFRS, divided by the Company’s total production.

The Company has provided additional information on how these measures are calculated in the Management’s Discussion and Analysis for the year ended December 31, 2022 and the interim period ended September 30, 2023, which are available under the Company’s SEDAR+ profile at www.sedarplus.ca.

Oil and Gas Advisories

Any references in this news release to production rates, which may include initial production rates for certain wells (including as a result of recent EOR activities), may be useful in confirming the presence of hydrocarbons; however, such rates are not determinative of the rates at which such wells will continue production and decline thereafter and are not necessarily indicative of long-term performance or ultimate recovery. While encouraging, readers are cautioned not to place reliance on such rates in calculating the aggregate production for the Company. Such rates are based on field estimates and may be based on limited data available at this time.

A barrel of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of 6 Mcf:1 Bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. In addition, given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

Definitions and Abbreviations

bbl

Barrel

Mcf

thousand cubic feet

bbl/d

barrels per day

Mcf/d

thousand cubic feet per day

$/bbl

dollar per barrel

$/Mcf

dollar per thousand cubic feet

boe

barrel of oil equivalent

IFRS

International Financial Reporting Standards

boe/d

barrel of oil equivalent per day

$/boe

dollar per barrel of oil equivalent

US$

United States Dollar

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Despite growing fears of an impending recession, the Federal Reserve is showing no signs of pivoting towards interest rate cuts any time soon, according to minutes from the central bank’s early-November policy meeting.

The minutes underscored Fed officials’ steadfast commitment to taming inflation through restrictive monetary policy, even as markets widely expect rate cuts to begin in the first half of 2024.

“The fact is, the Committee is not thinking about rate cuts right now at all,” Fed Chair Jerome Powell asserted bluntly in his post-meeting press conference.

The summary of discussions revealed Fed policymakers believe keeping rates elevated will be “critical” to hit their 2% inflation target over time. And it gave no indication that the group even considered the appropriate timing for eventually lowering rates from the current range of 5.25-5.50%, the highest since 2000.

Despite investors betting on cuts starting in May, the minutes signaled the Fed intends to stand firm and base upcoming policy moves solely on incoming data, rather than forecasts. Officials stressed the need for “persistently restrictive” policy to curb price increases.

Still, Fed leaders acknowledged they must remain nimble in response to shifting financial conditions or economic trajectories that could alter the monetary path.

The minutes linked this upward pressure on benchmark yields to several key drivers, including increased Treasury issuance to finance swelling federal deficits.

Analysts say the Fed’s aggressive rate hikes are also forcing up yields on government bonds. Meanwhile, any hints around the Fed’s own policy outlook can sway rate expectations.

Fed participants decided higher term premiums rooted in fundamental supply and demand forces do not necessarily warrant a response. However, the reaction in financial markets will require vigilant monitoring in case yield spikes impact the real economy.

Moderating Growth, Elevated Inflation Still Loom

Despite the tightening already underway, the minutes paint a picture of an economy still battling high inflation even as growth shows signs of slowing markedly.

Participants expect a significant deceleration from the third quarter’s 4.9% GDP growth pace. And they see rising risks of below-trend expansion looking ahead.

The Fed’s preferred PCE inflation gauge has also moderated over recent months. But at 3.7% annually in September, it remains well above the rigid 2% target.

Considering lags in policy impacts, the minutes indicated Fed officials believe the cumulative effect of 375 basis points worth of interest rate hikes this year should help restore price stability over the medium term.

Markets Still Misaligned with Fed’s Outlook

Despite the Fed’s clear messaging, futures markets continue to forecast rate cuts commencing in the first half of 2023. Traders are betting on a recession forcing the Fed’s hand.

However, several Fed policymakers have recently pushed back on expectations for near-term policy pivots.

For now, the Fed seems inclined to stick to its guns, rather than bowing to market hopes or economic worries. With inflation still unacceptably high amid a strong jobs market, policymakers are staying the course on rate hikes for the foreseeable future, according to the latest minutes.

Xcel Brands, Inc. 1333 Broadway 10th Floor New York, NY 10018 United States https:/Sector(s): Consumer Cyclical Industry: Apparel Manufacturing Full Time Employees: 84 Key Executives Name Title Pay Exercised Year Born Mr. Robert W. D’Loren Chairman, Pres & CEO 1.27M N/A 1958 Mr. James F. Haran CFO, Principal Financial & Accou

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. The company reported $2.9 million in revenue, which was in-line with our estimate of $2.6 million. Adj. EBITDA loss of $1.4 million was modestly lower than our estimate of a loss of $0.8 million, as illustrated in Figure #1 Q3 Results. Notably, Q3 operating results were affected by less QVC programming due to talent scheduling conflicts related to a return to an in-studio production policy and non-recurring restructuring expenses.

Transition toward a licensing model. In November, the company completed a restructuring process by entering into licensing agreements for its Longaberger and made in the US baskets businesses. The new licensing model is expected to significantly lower operating costs and be a key catalyst toward a swing to positive cash flow in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Chipmaker Nvidia (NVDA) is slated to report fiscal third quarter financial results after Tuesday’s closing bell, with major implications for tech stocks as investors parse the numbers for clues about the artificial intelligence boom.

Heading into the print, Nvidia shares closed at an all-time record high of $504.09 on Monday, capping a momentous run over the last year. Bolstered by explosive growth in data center revenue tied to AI applications, the stock has doubled since November 2022.

Now, Wall Street awaits Nvidia’s latest earnings and guidance with bated breath, eager to gauge the pace of expansion in the company’s most promising segments serving AI needs.

Consensus estimates call for dramatic sales and profit surges versus last year’s third quarter results. But in 2022, Nvidia has made beating expectations look easy.

This time, another strong showing could validate nosebleed valuations across tech stocks and reinforce the bid under mega-cap names like Microsoft and Alphabet that have ridden AI fervor to their own historic highs this month.

By contrast, any signs of weakness threatening Nvidia’s narrative as an AI juggernaut could prompt the momentum-driven sector to stumble. An upside surprise remains the base case for most analysts. But with tech trading at elevated multiples, the stakes are undoubtedly high heading into Tuesday’s report.

AI Arms Race Boosting Data Center Sales

Nvidia’s data center segment, which produces graphics chips for AI computing and data analytics, has turbocharged overall company growth in recent quarters. Third quarter data center revenue is expected to eclipse $12.8 billion, up 235% year-over-year.

Strength is being driven by demand from hyperscale customers like Amazon Web Services, Microsoft Azure, and Alphabet Cloud racing to build out AI-optimized infrastructure. The intense competition has fueled a powerful upgrade cycle benefiting Nvidia.

Now, hopes are high that Nvidia’s next-generation H100 processor, unveiled in late 2021 and ramping production through 2024, will drive another leg higher for data center sales.

Management’s commentary around H100 adoption and trajectory will help investors gauge expectations moving forward. An increase to the long-term target for overall company revenue, last quantified between $50 billion and $60 billion, could also catalyze more upside.

What’s Next for Gaming and Auto?

Beyond data center, Nvidia’s gaming segment remains closely monitored after a pandemic-era boom went bust in 2022 amid fading consumer demand. The crypto mining crash also slammed graphics card orders.

Gaming revenue is expected to grow 73% annually in the quarter to $2.7 billion, signaling a possible bottom but well below 2021’s peak near $3.5 billion. Investors will watch for reassurance that the inventory correction is complete and gaming sales have stabilized.

Meanwhile, Nvidia’s exposure to AI extends across emerging autonomous driving initiatives in the auto sector. Design wins and partnerships with electric vehicle makers could open another massive opportunity. Updates on traction here have the potential to pique further interest.

Evercore ISI analyst Julian Emanuel summed up the situation: “It’s still NVDA’s world when it comes to [fourth quarter] reports – we’ll all just be living in it.”

In other words, Nvidia remains the pace-setter steering tech sector sentiment to kick off 2024. And while AI adoption appears inevitable in the long run, the market remains keenly sensitive to indications that roadmap is progressing as quickly as hoped.