Rank Day is behind us. On April 30, FTSE Russell locked in the closing market capitalizations that will determine which companies get added to, removed from, or shuffled between the Russell 1000, Russell 2000, Russell 3000, and Russell Microcap indexes. The data is set. What comes next is where investor attention needs to be focused.

The first preliminary additions and deletions list publishes on May 22 — ten days from today — after 6 PM ET. If you’ve been following our coverage of this year’s reconstitution, you already know why 2026 carries more structural weight than any reconstitution in decades. If you’re just catching up, start here: Russell Reconstitution 2026 — What Investors Should Know and Rank Day Coverage.

Here’s what’s changed since April 30 and why it matters.

The Market Has Moved Since Rank Day

The twelve days since rank day have not been quiet. This morning, the Bureau of Labor Statistics reported April CPI came in at 3.8% year-over-year, with energy prices surging 3.8% in a single month on the back of ongoing Middle East conflict and elevated oil above $100 a barrel. Rate cut expectations for 2026 have effectively been wiped off the table. Consumer sentiment sits near historic lows.

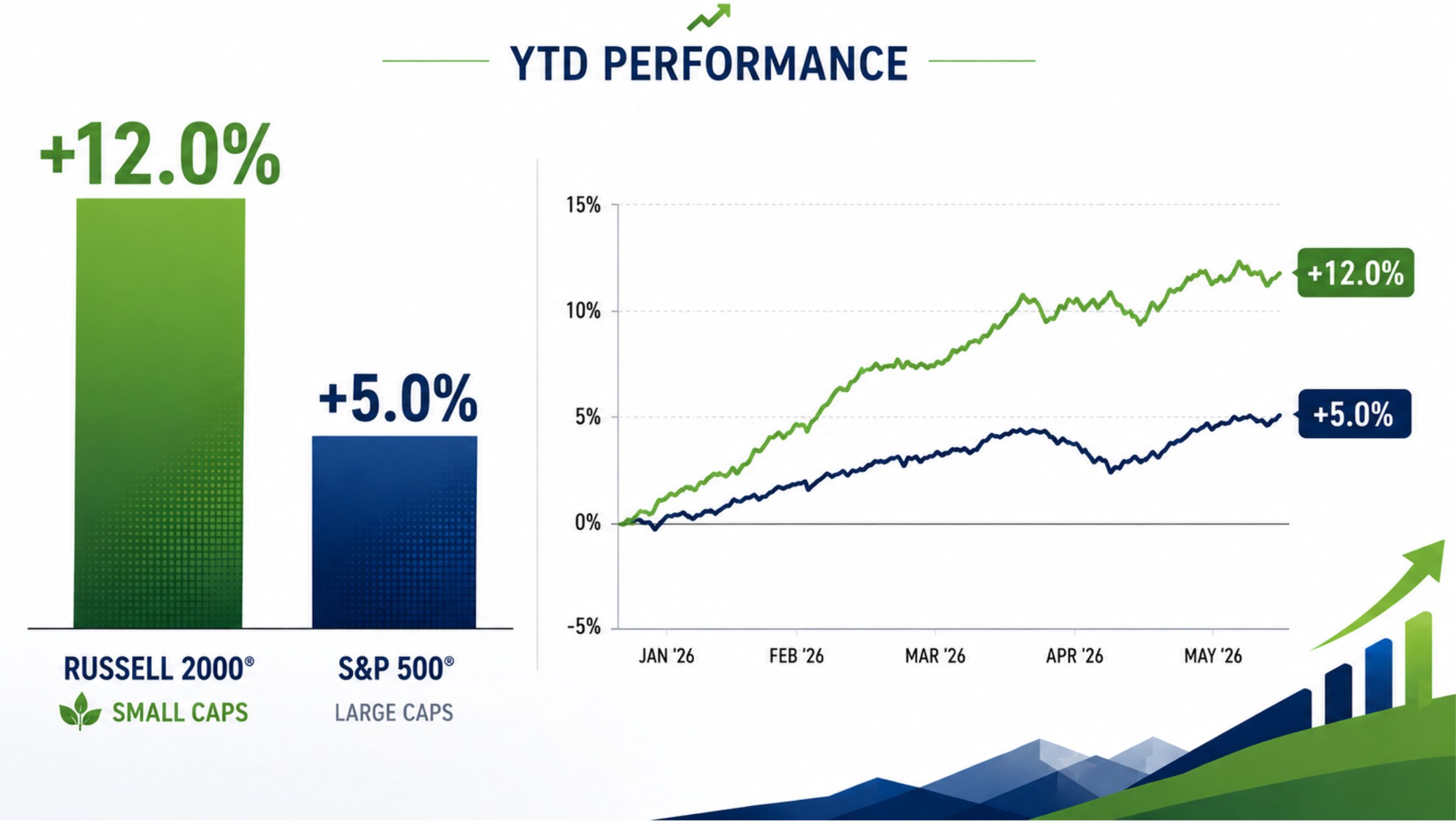

At the same time, small caps have been dealing with a bifurcated environment — some sectors, particularly defense and domestic manufacturing, have seen meaningful appreciation, while rate-sensitive and consumer-facing names continue to struggle. That divergence matters enormously in a reconstitution year, because companies near the market cap breakpoints on April 30 may have landed in very different positions than they would have a month earlier.

What the Preliminary Lists Could Show

The market volatility of the past twelve months has reshuffled market caps across the small and microcap universe more dramatically than most years. That sets up for a higher-than-normal number of index movers — companies graduating to the Russell 1000, falling into the Russell 2000, or dropping out of the Russell indexes entirely. Defense and energy-adjacent names that have appreciated significantly may be candidates for upward migration. On the other side, consumer discretionary and rate-sensitive small caps that have seen compression could face demotion or deletion.

The stocks to watch most closely are those sitting right at the boundary between indexes. For companies near the Russell 1000/2000 breakpoint, passive fund flows triggered by an index move can be substantial — and the price action in the weeks following the preliminary list often front-runs the actual reconstitution.

The Window That Matters Most

The preliminary list on May 22 is the starting gun, not the finish line. Updated lists follow on May 29, June 5, June 12, and June 18. The lock-down period — when membership is considered final — begins June 8. Reconstitution takes effect after the close on June 26.

That means the actionable window for investors runs from the moment the first preliminary list drops through the lockdown on June 8. Historically, the most significant price moves around reconstitution happen in this period, not on recon day itself. By the time June 26 arrives, passive funds benchmarked to Russell indexes are simply executing what the market has largely already priced in.

With more than $12 trillion benchmarked to Russell U.S. Equity indexes, the capital flows triggered by even a single significant addition or deletion can be meaningful — especially for smaller companies with lower liquidity.

Channelchek will be covering the May 22 preliminary list in detail as it’s released. Ten days. Watch this space.