Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

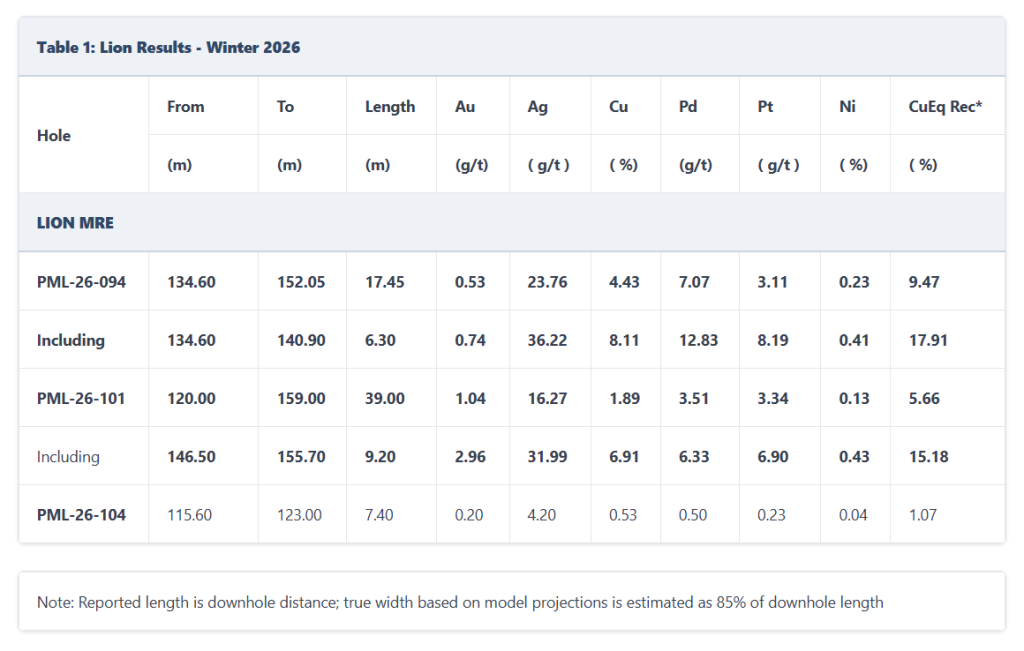

High-grade drill results confirm core mineralization. Power Metallic reported significant intercepts from the Lion Zone, including 17.45 meters at 9.47 percent copper equivalent in Hole PML 26-094 and 39 meters at 5.66 percent in Hole PML 26-101, both of which included higher grade sub-intervals. The assay results highlight the strength and continuity of near-surface mineralization within the core of the deposit.

Infill drilling supports resource growth and development potential. The Winter 2026 program is successfully defining mineralization across approximately 200 meters of strike length and supports the existing geological model. The results are expected to contribute to a 2026 Mineral Resource Estimate and may help advance portions of the deposit toward an Indicated classification suitable for potential open-pit mining.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Warrant exercise enhances capital structure and financial flexibility. First Phosphate Corp. announced the receipt of approximately C$3.07 million following the full exercise of its remaining warrants at C$1.25 per share, marking the exercise of all outstanding external dilutive instruments. This final round of warrant exercises represents a vote of confidence from shareholders and establishes a valuation benchmark for the company. As a result, the company’s capital structure is now notably streamlined, with no remaining dilutive securities other than those held by staff, management, and board members.

Strong balance sheet and funding provide a clear development runway. The company is in a strong financial position with no debt and benefits from a significant C$16.7 million non-repayable and non-dilutive contribution from the Government of Canada. Combined with funds raised since June 2022 totaling approximately C$62.5 million, First Phosphate has built a solid treasury exceeding C$20 million, placing it among a limited group of junior companies with comparable financial strength. This capital position provides a funding runway to advance development activities through to a final investment decision expected within approximately one and a half years.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

May 4, 2026 – Vancouver, Canada – Century Lithium Corp. (TSXV: LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or the “Company”) is pleased to announce the following management appointments. These individuals will reinforce the Company’s technical, environmental, and operational capabilities as it advances its 100%-owned Angel Island Lithium Project (“Angel Island”) in Esmeralda County, Nevada, USA through permitting and pre-construction development programs.

“Century Lithium’s leadership and success to date in bringing forward our Angel Island lithium project has been greatly due to the expertise and contributions of the individuals recognized today,” said Bill Willoughby, President and CEO of Century Lithium. “These appointments reflect our commitment to continue to advance Angel Island and the Company to achieve the milestones ahead, while driving active engagement with our communities, regulators, and investors.”

Management Appointments

Todd Fayram was appointed CTO of the Company, effective April 9, 2026. Mr. Fayram is a metallurgical engineer with over 40 years of experience leading process design, construction, start-up, and operations improvement on mineral projects across North and South America. He is a Qualified Person under NI 43-101 through Registered Member status with MMSA, and a member of SME and CIM. He holds a Master of Science (M.Sc.) degree in Mineral Processing/Metallurgical Engineering and a Bachelor of Science (B.Sc.) degree in Mineral Processing Engineering, Metallurgy from Montana Technology University. Since 2018, Mr. Fayram has played a key role in developing the Company’s chloride leaching process, related intellectual property, and the engineering and operations programs that have advanced Angel Island, joining the Company in 2023 as Senior Vice President, Metallurgy. As CTO, he will lead the technical direction of the Company’s metallurgy, process development, engineering, and the continued advancement of Century Lithium’s patent-pending chloride leaching and direct lithium extraction flowsheet.

Daniel Kalmbach is appointed Vice President, Exploration and Resource Development. Mr. Kalmbach is a geologist with 26 years of experience in the minerals industry. Since 2017, Mr. Kalmbach has led the Company’s mineral resource development, technical reporting, and permitting activities for Angel Island. Mr. Kalmbach holds a B.Sc. degree in Geology from the University of Idaho and is a Certified Professional Geologist with the American Institute of Professional Geologists. He is a Qualified/Competent Person under CRIRSCO-recognized reporting standards. He will lead the Company’s geological operations including exploration and resource development efforts, overseeing resource modeling, drill program design, and resource expansion at Angel Island and across the Company’s portfolio.

Teresa Conner is appointed Director of Permitting and Environmental Affairs. Ms. Conner has 45 years of experience in both the mining and oil and gas industries. Since 2021, Ms. Conner has led the Company’s permitting activities and strategy, environmental planning, regulatory coordination, and compliance activities for Angel Island. Ms. Conner holds a B.Sc. degree in Mining and Geological Engineering and a M.L.S. degree in Legal Studies with a focus in Mining Law and Policy from the University of Arizona. Ms. Conner is a member of the Society for Mining, Metallurgy, and Exploration, and a member and former Trustee of the American Exploration & Mining Association. Ms. Conner brings extensive experience in permitting, federal land management coordination, and environmental baseline programs in the western United States. She will lead the Company’s permitting activities and engagement with public and regulatory interests.

Adam Knight is appointed General Manager. Mr. Knight is a mining engineer with 31 years of experience in the mining industry. Since 2020, Mr. Knight has managed project operations and field programs supporting the pilot plant program, infrastructure development, mine planning, and community liaison for Angel Island. Mr. Knight holds a B.Sc. degree in Mining Engineering from the University of Nevada, Reno and is a Licensed Professional Engineer in the State of Nevada. He is a Qualified/Competent Person under CRIRSCO-recognized reporting standards. He will oversee the implementation of Angel Island’s development plan, including coordination of engineering, procurement, and construction activities, contractor management, and project controls as the Company progresses toward construction readiness.

Richard Alberthal is appointed Manager, Technical Services. Mr. Alberthal has over 30 years of experience in the mechanical and process disciplines, including leadership roles in management, design and operations. Since 2020, Mr. Alberthal has worked directly with the construction and operation of the Company’s Pilot and Demonstration Plants, and the chlor-alkali and lithium carbonate processes for Angel Island. He will oversee technical services for Angel Island, including process plant commissioning readiness, operator training, and integration of the lithium carbonate and chlor-alkali process flowsheets developed for Angel Island.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced-stage lithium development company focused on its 100%-owned Angel Island lithium project in Esmeralda County, Nevada. Angel Island hosts one of the largest known sedimentary lithium deposits in the United States and is designed with an integrated, end-to-end process for the on-site production of battery-grade lithium carbonate to support the electric vehicle and battery storage markets.

The Company has developed a patent-pending process that incorporates hydrochloric acid leaching combined with direct lithium extraction to produce battery-grade lithium carbonate. As part of the integrated chlor-alkali process, Angel Island is designed to produce sodium hydroxide as a co-product, with planned surplus sales expected to lower operating costs, reduce reliance on externally sourced reagents, and minimize environmental impacts.

Century Lithium is currently advancing Angel Island through the permitting process.

Century Lithium trades on the TSX Venture Exchange under the symbol “LCE” the OTCQX under the symbol “CYDVF”, and on the Frankfurt Stock Exchange under the symbol “C1Z”.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.

These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.ca. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

TORONTO, May 4, 2026 /CNW/ – Power Metallic Mines Inc. (the “Company” or “Power Metallic”) (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt: IVV1) is pleased to provide additional assays from its winter 2026 drill program.

Lion Zone MRE Infill Program

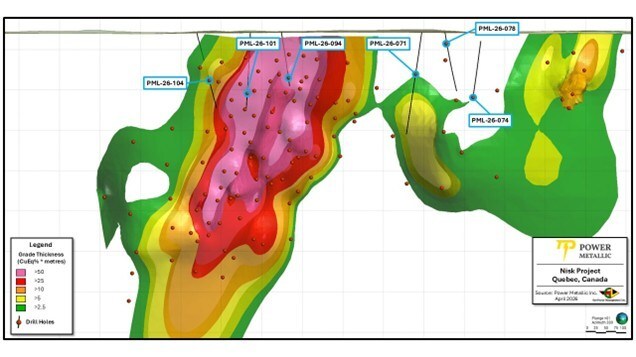

Drilling continued to define the high-grade Lion Zone in preparation for a 2026 Mineral Resource Estimate (MRE). The infill drill holes in this release are for holes that cover approximately 200 m of strike length from the middle core of the Lion Zone (PML-26-094) to the western edge (PML-26-104), defining mineralization at a vertical depth of approximately 100 m below surface (Figure 1). These holes will be important for future mineral resource estimates to an Indicated Resource classification, potentially for open pit exploitation.

The 2026 winter drill campaign continues to support the modelled interpretation of the Lion Zone based on earlier wider spaced drilling and includes PML-26-094 which intersected the interpreted core of the Lion Zone and adds further support to wide intersections of high-grade copper near surface with 17.45 m @ 9.47% CuEqRec1 including 6.30 m @ 17.91% CuEqRec1 (Table 1).

Hole PML-26-101 tested the zone approximately 100 m east of PML-26-094 at a slightly deeper vertical depth and contained high grade over a very wide intersection with 39.00 m @ 5.66% CuEqRec1 including 9.20 m @ 15.18% CuEqRec1. A further 100 m west hole PML-26-104 tested the western edge of the Lion Zone and intersected 7.40 m @ 1.07% CuEqRec1 and confirmed the expected mineralization modeled from the wider spaced earlier drilling in this area.

1Copper Equivalent Rec Calculation (CuEqRec1)

CuEqRec represents CuEq calculated based on the following metal prices (USD) : 2,360.15 $/oz Au, 27.98 $/oz Ag, 1,215.00 $/oz Pd, 1000.00 $/oz Pt, 4.00 $/lb Cu, 10.00 $/lb Ni and 22.50 $/lb Co., and recovered grades based on recent locked-cycle metallurgical recoveries by SGS Canada Inc (see press release Jan 21, 2006).

Figure 1 – Lion Drill holes reported in this news release (CNW Group/Power Metallic Mines Inc.)

Power Metallic is expecting more assay results from the MRE drilling and the regional exploration in the coming days and weeks.

Exploratory Drilling – Between Lion and Tiger

Drill holes PML-26-071, 074, and 078 were designed to test relatively shallow depths to explore for additional zones of mineralization between Lion and Tiger. While none of the holes hit sufficiently wide zones of mineralization, narrow zones included 0.8 meters @ 0.33% Cu, 0.78 g/t Pd, and 0.35 g/t Pt in hole PML-26-074, indicating the mineralizing structures are still present in the Lion to Tiger area.

“The heart of Lion continues to deliver impressive results. Both of these holes would have broken into our top six holes at the Lion Zone. We continue to build towards what we believe will be a very positive Mineral Resource Estimate in third quarter of this year,” commented Terry Lynch, CEO & Director.

Qualified Person

Joseph Campbell, P. Geo, VP Exploration at Power Metallic, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Metallic Mines Inc.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)—a high–grade Copper–PGE, Nickel, gold and silver system—toward Canada’s next polymetallic mine.

On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~330 km² and roughly 50 km of prospective basin margins.

Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs.

Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025.

It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s Jabal Said Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

For further information, readers are encouraged to contact: Power Metallic Mines Inc. The Canadian Venture Building 82 Richmond St East, Suite 202 Toronto, ON

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

QAQC and Sampling

GeoVector Management Inc (“GeoVector”) is the Consulting company retained to perform the actual drilling program, which includes core logging and sampling of the drill core.

All core in this news release is NQ sized core. Drill core is re-fitted and measured. Geotech on core includes photographs (wet & dry), rock quality index, magnetic susceptibility, conductivity, and recovery estimates. Core is logged for lithology, mineralogy, and structural features, and sample intervals are delineated and tagged.

Sampled core is mechanically sawn, and half-core is retained for future reference. GeoVector’s QAQC program includes regular insertion of CRM standards, duplicates, and blanks into the sample stream with a stringent review of all results. QAQC and data validation was performed, and no material errors were observed.

All samples were submitted to and analyzed at Activation Laboratories Ltd (“Actlabs”), a commercial laboratory independent of Power Metallic with no interest in the Project. Actlabs is an ISO 9001 and 17025 certified and accredited laboratories. Samples submitted through Actlabs are run through standard preparation methods and analysed using RX-1 (Dry, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 μm) preparation methods, and using 1F2 (ICP-OES) and 1C-OES – 4-Acid near total digestion + Gold-Platinum-Palladium analysis and 8-Peroxide ICP-OES, for regular and over detection limit analysis. Pegmatite samples are analyzed using UT7 – Li up to 5%, Rb up to 2% method. Actlabs also undertake their own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibration.

This message contains certain statements that may be deemed “forward-looking statements” concerning the Company within the meaning of applicable securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential,” “indicates,” “opportunity,” “possible” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, are subject to risks and uncertainties, and actual results or realities may differ materially from those in the forward-looking statements. Such material risks and uncertainties include, but are not limited to, among others; the timing for various drilling plans; the ability to raise sufficient capital to fund its obligations under its property agreements going forward and conduct drilling and exploration; to maintain its mineral tenures and concessions in good standing; to explore and develop its projects; changes in economic conditions or financial markets; the inherent hazards associates with mineral exploration and mining operations; future prices of nickel and other metals; changes in general economic conditions; accuracy of mineral resource and reserve estimates; the potential for new discoveries; the ability of the Company to obtain the necessary permits and consents required to explore, drill and develop the projects and if accepted, to obtain such licenses and approvals in a timely fashion relative to the Company’s plans and business objectives for the applicable project; the general ability of the Company to monetize its mineral resources; and changes in environmental and other laws or regulations that could have an impact on the Company’s operations, compliance with environmental laws and regulations, dependence on key management personnel and general competition in the mining industry.

Saguenay, Québec–(Newsfile Corp. – May 4, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the receipt of $3,070,549 in gross proceeds upon the exercise of 2,456,439 warrants prior to their expiry on April 24, 2026 and April 30, 2026, at an exercise price of $1.25 per share.

The Company now has 179,947,950 common shares, 2,625,000 warrants, 7,650,000 options and 1,975,000 restricted share units outstanding. All warrants, options and restricted share units outstanding are held by current Company staff, management and board members.

The Company remains debt-free and is on an accelerated development timeline thanks to a recent non-repayable, non-dilutive contribution of $16.7 million received from the Federal Government of Canada.

Since June 2022, the Company has raised approximately $62.5 million in 10 management-led non-brokered private-placement financings and from funds received from option and warrant exercise.

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay–Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

Forward-Looking Information and Cautionary Statement

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, this press release contains forward-looking information relating to, among other things: the timeframe for the development of the Company’s planned exploration and production activities; and the Company’s plans for vertical integration into North American supply chains. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things: that engineering and construction timetables and capital costs for the Company’s, exploration, development and expansion projects are correctly estimated and not affected by unforeseen circumstances; the ability to obtain financing for its proposed operations on acceptable terms; no material deterioration in general business and economic conditions; no material delays in obtaining permits and other approvals; no significant disruptions affecting the activities of the Company or its ability to access required project equipment and services, and operating supplies in sufficient quantities and on a timely basis; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the ability to complete the exploration and development programs consistent with the Company’s expectations; commodity price expectations including assumptions for P205; the Company’s relationship with local municipalities and First Nations remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Exploration Momentum. Resolution Mineralscontinues to demonstrate strong exploration results across its Horse Heaven Project, confirming a large-scale, multi-commodity system. High-grade antimony at Antimony Ridge and extensive gold mineralization at Golden Gate highlight the project’s scale, with drilling confirming continuous mineralization that remains open in multiple directions. A major 13,700-meter Phase 2 drilling program is expected to commence this week to further define resource potential and support a maiden Mineral Resource Estimate targeted for Q1 2027.

Advancing Metallurgy and Development Pathways. Resolution is making significant progress in metallurgical testing and project development, particularly with tungsten and antimony processing. Test work has successfully produced high-grade tungsten concentrates and high-purity antimony products, demonstrating viable processing pathways and near-term production potential. Combined with the acquisition of processing infrastructure at Johnson Creek, these developments position the company to advance toward a vertically integrated, U.S.-based critical minerals platform.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strategic partnership. Aurania Resources Ltd. entered into a definitive earn-in agreement with St-Georges Eco-Mining Corp. (CSE: SX) and its subsidiary Iceland Resources to advance the Thormodsdalur gold project (Thor’s Valley) in Iceland. Located near Reykjavik, the project is considered a highly prospective epithermal gold system, and the partnership is intended to support a structured exploration program aimed at defining its resource potential.

Key agreement terms. Under the agreement, Aurania will issue shares valued at US$150.0 thousand and commit to USD $5.0 million in exploration spending over four years in order to earn a 70% interest in the project. St-Georges retains the option to hold a minority interest or a royalty, while Aurania may increase its ownership to full control through additional investment. We expect the transaction to close in early May pending the satisfaction of certain conditions, including approval by the TSX Venture Exchange. We will update our estimates to reflect planned expenditures once the transaction closes.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

This release corrects and replaces the press release issued by Aurania Resources Ltd. on April 28, 2026 – 7:25AM EDT, correcting the anniversary timelines of exploration expenditures under the heading Summary of Terms under the Agreement.

Toronto, Ontario–(Newsfile Corp. – April 28, 2026) – Aurania Resources Ltd. (TSXV: ARU) (OTCQB: AUIAF) (FSE: 20Q) (“Aurania” or the “Company”) is pleased to announce that it has entered into a definitive option agreement (the “Agreement”) dated April 27, 2026 (the “Execution Date”) with St-Georges Eco-Mining Corp (CSE: SX) (“St-Georges“), a Canadian incorporated mineral exploration company and its wholly owned subsidiary Iceland Resources ehf (“IR”), an Icelandic incorporated precious metals exploration company to work collaboratively to define and execute a phased exploration program aimed at advancing the Thormodsdalur gold project (“Thor’s Valley” or the “Project”), towards initial modern resource definition. The Thor’s Valley project is held by IR and is located approximately 20 kilometres east of Reykjavík, the capital of Iceland.

Aurania’s President and CEO, Dr. Keith Barron commented, “After visiting the project area and personally reviewing the archived drill core, the Thor’s Valley project represents a compelling opportunity with strong exploration upside. By formalizing our collaboration with St-Georges, we are positioning ourselves to unlock the potential of an under-explored geological district. Thor’s Valley displays all the key signatures of a robust epithermal gold system, supported by a history of documented high-grade mineralization and a suite of compelling structural targets that remain largely untested by modern exploration methods. This Agreement allows Aurania to deploy its technical expertise toward a highly prospective gold project. We look forward to progressing this Project with discipline, technical rigour, and a strong commitment to unlocking its full potential.”

Comment from Thordis Bjork Sigurbjornsdottir, CEO of Iceland Resources: “This is an important partnership for Iceland Resources, and we are pleased to welcome Aurania Resources Ltd. as a partner on the Thormodsdalur project. Over the past several years, we have engaged in discussions with several groups with the objective of identifying a partner with the right technical experience and approach for this type of epithermal gold system. We believe Aurania brings that combination, supported by relevant experience in advancing high-grade epithermal discoveries. We look forward to working together to advance Thormodsdalur in a disciplined and value-focused manner.”

Summary of Terms under the Agreement

Initial payment of US$150,000 in common shares of Aurania (the “Shares”) to be issued to St. Georges on the closing date of the Agreement at a deemed price per Share equal to the volume weighted average price of the Shares on each business day commencing on the Execution Date and ending on the last business day prior to the closing date of the Agreement.

Aurania to incur exploration expenditures of US$5 million over four years to earn a 70% interest in the Project, such exploration expenditures to be incurred as follows:

At least US$500,000 prior to the first anniversary of the Execution Date;

At least US$1,000,000 prior to the second anniversary of the Execution Date;

At least US$1,500,000 prior to the third anniversary of the Execution Date;

At least US$2,000,000 prior to the fourth anniversary of the Execution Date;

Upon completing the First Option, St-Georges will have the option to choose between maintaining a 30% interest in the Project through a joint venture or retain an up to 3% net smelter return royalty on the Project (the “Royalty”), with such Royalty to be reduced as necessary such that the aggregate royalty burden on the Project shall not exceed 3%, inclusive of any pre-existing NSR royalties; and

If St. Georges elects to retain the Royalty, Aurania will have the right, in its sole discretion, to increase its ownership to in the Project to 100% by incurring an additional US$2,000,000 of exploration expenditures.

A joint exploration committee will be established between Aurania and St-Georges, with Aurania being the technical operator.

The Agreement is subject to certain conditions, including the approval of the TSX Venture Exchange. The Shares will be subject to a hold period of four months and one day from the date of issuance.

Thor’s Valley is a historically known gold-bearing, low-sulphidation epithermal system that was initially discovered in 1903 when two Icelandic farm boys picked up pieces of white quartz from a stream, which proved to be gold-bearing. A number of ventures were organized from 1911 to 1924 using German or British capital. Two shafts were sunk and approximately 400 metres of lateral workings performed. As a result of this, the productive vein was estimated to be 1 metre wide and at least 1 kilometre long. Reported grades were 11 g/t to 315 g/t gold[1]. The ore was “direct shipping” and initially sent to Norway and later to Germany for treatment. There are no historic tailings on site. Perhaps significantly, the historical record indicates that the last operator, Arcturus, a German company, failed due to the Weimar hyperinflation rather than ore depletion.

In the 1990’s, several programmes of geochemical and petrographical studies were done, including a vertical geothermal well to a depth of 455 metres which encountered multiple mineralized quartz veins, including one at the bottom of the hole. In 1997, a total of 1069.21metres were diamond drilled in nine holes, however, average core recovery was only 52%. The intervals sampled graded 1.13 g/t to 46.10 g/t Au but this is not considered representative and true widths could not be calculated.

Between 2005 and 2006, the private exploration company Melmi ehf drilled 32 holes totaling 2431m, which returned results up to 415.40 g/t Au. Melmi ehf was acquired by Iceland Resources in 2020, which completed 11 additional drill holes totaling 1780m with results of up to 113 g/t Au1.

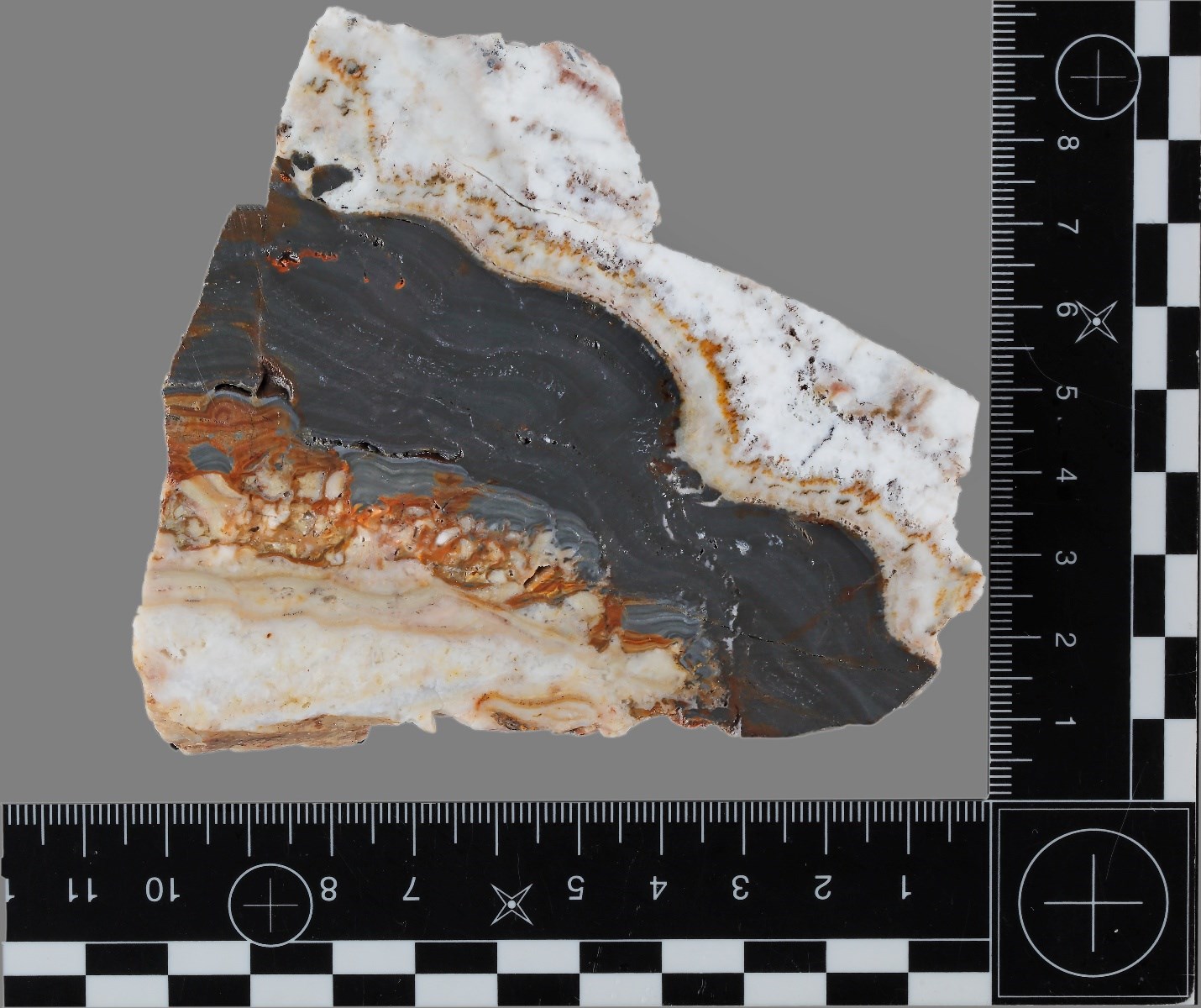

Figure 1. Sample of historic drill core from 1996. This is a typical hydrothermal breccia, as commonly seen in epithermal systems. This type of ore deposit is the same as that at Fruta del Norte in Ecuador.

The Thor Valley mineralization is a classic banded epithermal chalcedony-ginguro vein system with gold occurring both in free form and in association with sulphides. There are obviously a number of different vein sets here that appear controlled by regional and local structures.

The Project consists of a National Exploration Permit covering approximately 51,300 hectares in Iceland.

Figure 2: Hand sample of mineralization with typical rhythmic banding. The black area is composed of very fine-grained pyrite. This sample was found as float on the site and will be sent in for assay.

Planned Work Program Aurania anticipates completing an initial exploration program focused on targeted drilling and surface exploration designed to test deeper and along-strike continuity of the known mineralized zones, utilising both historical data and newly generated technical information. Several of the previous drill holes with poor recovery will be twinned.

The Company cautions the reader that the historical information referred to herein is based on data compiled by previous operators and publicly available sources and is being provided for reference purposes only. A qualified person retained by Aurania has not undertaken sufficient work to verify the historical data, and such information should not be relied upon. Further exploration work, including drilling and data verification, is required and may or may not result in the delineation of a mineral resource.

No current mineral resources or mineral reserves, as defined under National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”), have been established on the Project.

The technical and scientific information contained in this news release has been reviewed and approved by Jean-Paul Pallier, MSc., Vice-President Exploration of the Company. Mr. Pallier is a designated EurGeol by the European Federation of Geologists and a Qualified Person as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators.

About St-Georges Eco-Mining Corp. St-Georges develops new technologies and holds a diversified portfolio of assets and patent-pending Intellectual Property within several highly prospective subsidiaries including: EVSX, a leading North American advanced battery processing and recycling initiative; St-Georges Metallurgy, with metallurgical R&D and related IP, including processing and recovering high grade lithium from spodumene; Iceland Resources, with high grade gold exploration projects including the flagship Thor Project; H2SX, developing technology to convert methane into solid carbon and turquoise hydrogen; and Quebec exploration projects including the Manicouagan and Julie nickel, Copper and PGE critical mineral projects on Quebec’s North Shore, and Notre-Dame niobium Project in Lac St Jean.

About Iceland Resources Iceland Resources is an Icelandic mineral exploration company focused on early-stage precious metal projects, including Thormodsdalur. The company’s exploration strategy emphasizes systematic, data-driven evaluation of prospective targets in under-explored volcanic terrains.

About Aurania Aurania is a mineral exploration company engaged in the identification, evaluation, acquisition, and exploration of mineral property interests, with a focus on precious metals and critical energy in Europe and abroad.

Neither the TSX-V nor its Regulation Services Provider (as that term is defined in the policies of the TSX-V) accepts responsibility for the adequacy or accuracy of this release.

This news release contains forward-looking information as such term is defined in applicable securities laws, which relate to future events or future performance and reflect management’s current expectations and assumptions. The forward-looking information includes: statements regarding the terms of the Agreement, earn-in requirements, anticipated exploration programs, timing of activities, the potential to advance the Project, Aurania’s objectives, goals or future plans, statements, exploration results, potential mineralization, the tonnage and grade of mineralization which has the potential for economic extraction and processing, the merits and effectiveness of known process and recovery methods, the corporation’s portfolio, treasury, management team and enhanced capital markets profile, the estimation of mineral resources, exploration, timing of the commencement of operations, the commencement of any drill program and estimates of market conditions. Such forward-looking statements reflect management’s current beliefs and are based on assumptions made by and information currently available to Aurania, including the assumption that there will be no material adverse change in metal prices, all necessary consents, licenses, permits and approvals will be obtained, including various local government licenses and the market. Investors are cautioned that these forward-looking statements are neither promises nor guarantees and are subject to risks and uncertainties that may cause future results to differ materially from those expected. Risk factors that could cause actual results to differ materially from the results expressed or implied by the forward-looking information include, among other things: failure to achieve the anticipated results, incorrect assumptions made in the initial evaluation of the Project, failure to identify mineral resources; failure to convert estimated mineral resources to reserves; the inability to complete a feasibility study which recommends a production decision; the preliminary nature of metallurgical test results; the inability to recover and process mineralization using known mining methods; the presence of deleterious mineralization or the inability to process mineralization in an environmentally acceptable manner; commodity prices, supply chain disruptions, restrictions on labour and workplace attendance and local and international travel; a failure to obtain or delays in obtaining the required regulatory licenses, permits, approvals and consents; an inability to access financing as needed; a general economic downturn, a volatile stock price, labour strikes, political unrest, changes in the mining regulatory regime governing Aurania; a failure to comply with environmental regulations; a weakening of market and industry reliance on precious metals and base metals; and those risks set out in the Company’s public documents filed on SEDAR+. Aurania cautions the reader that the above list of risk factors is not exhaustive. Although the Company believes that the assumptions and factors used in preparing the forward-looking information in this news release are reasonable, undue reliance should not be placed on such information, which only applies as of the date of this news release, and no assurance can be given that such events will occur in the disclosed time frames or at all. The Company disclaims any intention or obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, other than as required by law.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong mineral continuity and expansion potential. First Phosphate Corp. reported strong results from its 2025/2026 infill drill program at the Begin–Lamarche property, confirming continuous phosphate mineralization across all zones and identifying two new intersections. The results will support an updated geological model expected next month and underscore the potential for resource expansion.

Geological consistency across zones. Drilling confirmed consistent geology across the Mountain, Northern, and Southern zones. High-grade apatite mineralization and similar structural features across zones reinforce confidence in a cohesive and predictable deposit.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Significant progress in 2025. Kuya reported its financial and operational results for the fourth quarter and FY 2025, while also announcing key leadership appointments to strengthen its operations in Peru. Edgardo Orderique was named General Manager for Peru, bringing senior-level experience from major mining operations, and will oversee mining and processing at the Bethania Silver Project. He is supported by Jesus Palomino as Operations Manager and German Minaya as Finance and Administration Manager. These additions are intended to enhance execution as the company transitions from early-stage production to scaled operations with higher throughput.

Operational momentum. The company made steady progress, achieving record processing volumes and improved production consistency. Production reached approximately 100 tonnes per day in March, with a target of 350 tonnes per day by the end of 2026 under its Phase One expansion plan. This growth is supported by investments in underground development, infrastructure, and workforce training, along with modernization efforts to improve efficiency. Kuya increased its exploration program to 20,000 meters of drilling in 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Toronto, Ontario–(Newsfile Corp. – April 24, 2026) – Kuya Silver Corporation (CSE: KUYA) (OTCQB: KUYAF) (FSE: 6MR1) (the “Company” or “KuyaSilver“) is pleased to announce financial and operating results for the three months and full year ending December 31, 2025, while also announcing a significant strengthening of its in-country leadership – appointing Edgardo Orderique, former General Manager of MMG’s Las Bambas mine, as General Manager, Peru, alongside a seasoned operational and finance team.

The fourth quarter marked another period of meaningful progress at the Bethania Silver Project in Peru, highlighted by record tonnes processed, significant upgrades to infrastructure, and a strengthened balance sheet, which was further bolstered in Q1 2026. As disclosed more recently in the Kuya Silver Press Release dated April 22, 2026, Kuya Silver has achieved sustained production of approximately 100 tonnes per day (“tpd“) and is advancing toward its Phase 1 target of approximately 350 tpd by the end of 2026.

Strengthens Peru Management Team Including New High Profile General Manager

Kuya Silver is also pleased to announce the appointment of three senior managers to lead its operations in Peru, as the Company advances the production ramp-up at its Bethania silver mine. These appointments are intended to strengthen operational, financial, and administrative execution as production increases. With Mr. Orderique’s appointment, a leader who ran a 150,000 tonne-per-day mine with 8,800 personnel, a significant addition enhancing the operating team in Peru as the Company ramps up production at the Bethania project to 350 tpd.

David Stein, President and Chief Executive Officer of Kuya Silver, remarked: “As we advance the Bethania mine toward higher, steady-state production levels, it is important that our operational and financial leadership is aligned with that growth. The addition of experienced senior leaders in Peru strengthens our ability to execute safely, efficiently, and in accordance with our development plans.”

Edgardo Orderique – General Manager, Peru

Mr. Orderique has been appointed General Manager, Peru, with responsibility for all Peruvian operations, including both mining and future processing business units. He is a senior mining executive with extensive experience managing large-scale operations in Peru.

Mr. Orderique previously served as General Manager of Minera Crespo, part of the Apucorp Group, where he led the construction of the industrial processing facilities and the development of the mining operation. He also served at MMG’s Las Bambas copper operation, where he oversaw approximately 2,800 employees and 6,000 contractors, improved throughput from 140,000 tpd to 150,000 tpd, reduced unit operating costs, and maintained a low total recordable injury frequency rate (TRIFR).

Prior to Las Bambas, he served as General Manager of Glencore’s Antapaccay mine, where he led a capital expansion program, improved operating performance, and managed community and stakeholder relations without disruption to operations.

He has held various leadership roles within Peru’s mining sector, including President of the XV National Mining Congress (2024), President of the Sustainability Forum at the XVI National Mining Congress (2026), and current Director of the Mining Engineering Institute of Peru (IIMP).

Jesus Palomino – Operations Manager

Mr. Palomino is a mining engineer with over 14 years of experience in underground mining operations in Peru and internationally. Most recently, he served as Underground Mine Manager at Calibre Mining Corp. in Nicaragua, overseeing mine planning, safety, cost control, and underground mining methods.

Previously, Mr. Palomino was General Manager of Glencore’s Sinchi Wayra operation in Bolivia and held senior operational roles at Glencore Antapaccay, Hochschild Mining, and Minera Santa Luisa. At Santa Luisa, he oversaw a production increase from approximately 800 tpd to 2,000 tpd while reducing operating costs.

German Minaya – Finance & Administration Manager

Mr. Minaya is a finance executive with an MSc in Finance and an MBA, with experience across mining operations in Peru, Chile, Argentina, Brazil, and Zambia. He most recently served as Finance Director at Tumi Technology & Innovation.

Prior roles include Regional Risk Manager and financial subject matter expert for copper projects at Glencore, where he implemented risk governance frameworks for large capital projects, and Chief of Finance and Risk Management at Minsur, where he led financial initiatives related to tax exposure mitigation and cash flow generation. Mr. Minaya has also held senior finance roles at Chinalco, Anglo American, and Newmont, and is currently completing the Emerging CFO Programme at The Wharton School.

Edgardo Orderique, General Manager, Peru, added: “Bethania is transitioning from early production into a period of operational scaling. My focus will be on execution discipline, safety performance, and stable operating results as the Company advances its production objectives.”

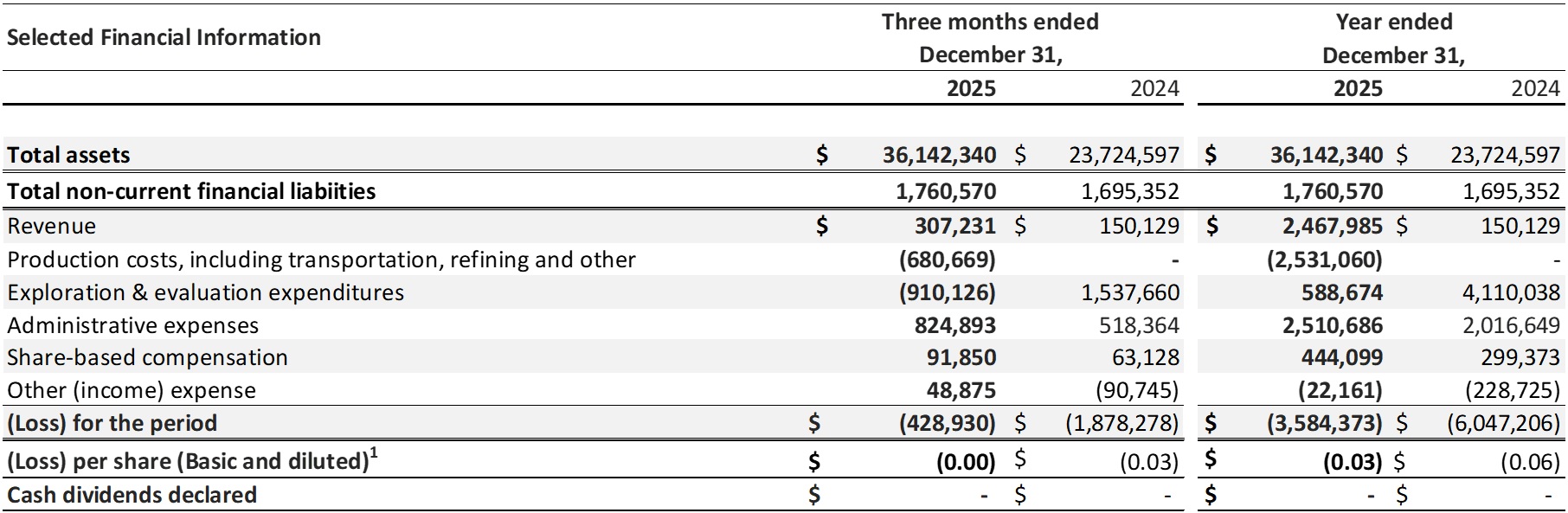

Q4 2025 and Full Year Financial Highlights

For the three months and year ended December 31, 2025, the Company recorded revenue of $307,331 from Bethania concentrate sales, compared to $150,129 revenue in the prior-year quarter (Q4 2024). Production costs totaled $680,669 – which is expected during the pre-steady-state ramp-up phase, as the company continued to develop multiple underground faces, expand ventilation and haulage infrastructure, and train personnel. Importantly, these costs are investments in future production capacity, and cash operating costs per tonne are expected to decline meaningfully as throughput increases toward 350 tpd.

The Company recorded a net loss of $428,930 for Q4 2025, significantly improved from a net loss of $1,878,279 in Q4 2024 primarily due to increased revenue and lower exploration costs, the latter reflecting the impact of a VAT of $1,361,530 recovery recognized in 2025.

For the full year ended December 31, 2025, Kuya Silver recorded a net loss of $3,584,373, a 41% improvement over the $6,047,203 net loss in the same period of 2024. The improvement reflects improved revenue generation from Bethania due to increasing production and higher silver prices and reduced exploration spending as the operation moved further into development and ramp-up and significantly less was spent on the Silver Kings project compared to 2024.

1 In periods when the Company has a loss, diluted loss per share is the same as basic loss per share.

Year End Overview – Strong Financial Position

Kuya Silver ended the year with a significantly strengthened balance sheet. Cash at the end of 2025 increased to $9,339,023, and net working capital surplus of $9,862,354, compared to a working capital deficit of $677,145 at December 31, 2024.

The improvement was primarily driven by the Company’s Q3 2025 financing, in which it issued raised gross proceeds of $6,566,000 (CAD $9,070,000) as well as warrant exercises in the quarter that raised an additional $4,875,539. These funds provided the near-term capital required to support the ongoing production ramp-up at Bethania and other growth initiatives such as exploration. Also in Q3 2025, the Company completed an early settlement of its remaining convertible debentures, further strengthening the working capital position.

Subsequent to quarter-end, 5,674,353 warrants have been exercised for proceeds of CAD $2,132,136 in addition to the previously disclosed January 2026 equity financing (gross proceeds of CAD $25.5 million).

As a result, Kuya Silver held approximately $27.0 million in cash as of March 31, 2026 – fully funding the current expectations for investment in the Phase 1 ramp-up to 350 tpd, the Camila plant acquisition, and the expanded 20,000-metre exploration program in 2026. The Company does not expect to require additional financing to achieve these milestones.

Outlook

Kuya Silver’s primary near-term objective remains maintaining stable production of 100 tpd at the Bethania Silver Project as a pathway to advancing production growth and development to reach its phase one production target of 350 tpd in 2026. Kuya Silver is also implementing a modernization program focused on improving underground haulage and material handling efficiency to support higher and more consistent throughput.

The Company increased its exploration program to target 20,000 metres of drilling in 2026, combining underground and surface diamond drilling. Underground drilling will be focused on the Santa Elena concession to enhance geological understanding at depth and assist with future mine planning. Surface program is designed to expand known mineralized structures near existing operations and test high-priority regional silver vein systems within trucking distance to the Bethania mine.

National Instrument 43-101 Disclosure

The technical content of this news release has been reviewed and approved by Mr. Kevin J. O’Connell, P.E., Independent Technical Advisor to Kuya Silver and a Qualified Person as defined by National Instrument 43-101.

About Kuya Silver Corporation

Kuya Silver is a Canadian‐based mineral exploration and development company with a focus on acquiring, exploring, and advancing precious metals assets in Peru and Canada.

For further information, please contact: David Stein, President & Chief Executive Officer Telephone: (604) 398-4493 Email: [email protected] Website: www.kuyasilver.com

Reader Advisory

This news release contains statements that constitute “forward-looking information,” including statements regarding the plans, intentions, beliefs, and current expectations of the Company, its directors, or its officers with respect to the future business activities of the Company. The words “may,” “would,” “could,” “will,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “expect,” “must,” “next,” “propose,” “new,” “potential,” “prospective,” “target,” “future,” “verge,” “favorable,” “implications,” and “ongoing,” and similar expressions, as they relate to the Company or its management, are intended to identify such forward-looking information. Investors are cautioned that statements including forward-looking information are not guarantees of future business activities and involve risks and uncertainties, and that the Company’s future business activities may differ materially from those described in the forward-looking information as a result of various factors, including but not limited to fluctuations in market prices, successes of the operations of the Company, continued availability of capital and financing, and general economic, market, and business conditions. There can be no assurances that such forward-looking information will prove accurate, and therefore, readers are advised to rely on their own evaluation of the risks and uncertainties. The Company does not assume any obligation to update any forward-looking information except as required under the applicable securities laws.

Neither the Canadian Securities Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A step forward in Century’s development strategy. The company is advancing the relocation of its lithium extraction demonstration plant to Tonopah, Nevada, with commissioning expected in the second half of 2026. This facility previously operated in Amargosa Valley, where it successfully validated the company’s integrated process for producing battery-grade lithium carbonate from claystone. Current efforts include equipment transfer, construction of a new processing facility, and permitting activities, alongside planned metallurgical testing to further refine extraction efficiency and production methods.

The company’s process technology provides a notable competitive advantage. Century Lithium’s patent-pending chlor-alkali process utilizes salt-based reagents generated on-site, eliminating reliance on sulfuric acid and external supply chains. This design is particularly advantageous given the significant increase in global sulfur and sulfuric acid prices, allowing the company to maintain cost stability with the use of domestically available inputs such as sodium chloride and electricity while also enabling potential revenue from surplus by-products.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Two of the offshore energy sector’s most recognized names are joining forces. Helix Energy Solutions Group (NYSE: HLX) and Hornbeck Offshore Services have announced a definitive all-stock merger agreement that will create one of the most comprehensive integrated deepwater services companies in the world — and the timing couldn’t be more calculated.

Under the terms of the deal, Hornbeck shareholders will own approximately 55% of the combined company while Helix shareholders retain roughly 45% on a fully diluted basis. The newly formed entity will operate under the Hornbeck Offshore Services name and trade on the New York Stock Exchange under the ticker symbol “HOS.” Todd Hornbeck, currently Chairman, President and CEO of Hornbeck, will lead the combined company, with William Transier serving as Chairman of a seven-member board comprised of three Helix directors and four from Hornbeck.

Why This Deal Makes Strategic Sense

This isn’t a merger of desperation — it’s a merger of expansion. Helix brings deep subsea expertise, well intervention capabilities, and a global robotics fleet with operations spanning the Gulf of America, Brazil, North Sea, West Africa and Asia Pacific. Hornbeck contributes a fleet of technologically advanced, high-specification offshore support vessels with a strong concentration in the Americas, including Brazil and Mexico, along with meaningful exposure to U.S. government and offshore wind contracts.

Together, the combined company covers the entire life cycle of deepwater field operations — from installation and production enhancement to decommissioning — across energy, defense and renewables. That kind of end-to-end service coverage significantly reduces the cyclicality risk that has historically plagued pure-play offshore services companies.

The Numbers Behind the Deal

The transaction is expected to generate $75 million or more in annual revenue and cost synergies within three years of closing. Those synergies will come from integrated service offerings, expanded customer reach and fleet optimization that reduces reliance on expensive third-party vessel charters.

The combined backlog currently stands at approximately $2 billion — split evenly between the two companies — with $1 billion tied to long-term contracts in Hornbeck’s military and specialty vessel segments. That backlog provides meaningful near-term revenue visibility as the integration unfolds.

Helix also reported Q1 2026 revenue of $287.95 million, beating analyst estimates by roughly $24 million, and reiterated full-year 2026 guidance of $1.2 billion to $1.4 billion in revenue with EBITDA projected between $230 million and $290 million. The company closed Q1 with $501 million in cash and just $10 million in funded debt — a balance sheet position that gives the combined entity significant flexibility for organic growth or further M&A post-close.

What to Watch

The merger requires Helix shareholder approval and customary regulatory sign-offs, with closing expected in the second half of 2026. Notably, Ares Management funds, representing a significant portion of Hornbeck’s ownership, have already delivered written consent approving the transaction — removing one of the more common deal-risk variables upfront.

For investors tracking the small and midcap offshore services space, this deal reshapes the competitive landscape. The combined HOS will be a scaled, diversified operator in a sector where scale increasingly determines who wins long-term contracts and who gets squeezed out.

The deepwater services consolidation wave continues — and this merger puts the new Hornbeck Offshore squarely at its center.

{kind=link}

{kind=link}

{kind=link}