Virginia City, Nevada, March 26, 2026 – Comstock Inc. (NYSE: LODE) (“Comstock” and the “Company”) is pleased to announce that its 2026 Annual Meeting of Shareholders has been scheduled for Thursday, May 28, 2026, starting at 9:00 a.m. Pacific Daylight Time in Reno, Nevada, at the Peppermill Hotel. The meeting will feature Comstock Metals, strategic investments, and clean energy systems.

The 2026 Annual Meeting schedule for May 28, 2026, is as follows:

8:00 am to 9:00 am PDT – Continental Breakfast 9:00 am to 11:30 am PDT – 2026 Annual Shareholders Meeting, Company Presentations, Q & A 12:00 pm to 1:00 pm PDT – Lunch and Conversations with Company Management and Directors

The record date for the Annual Meeting is March 31, 2026. Only shareholders of record at the close of business on March 31, 2026, may vote at the meeting. The Company’s proxy statement will be sent to shareholders of record and will describe all matters to be voted on. Shareholders are invited to register for the 2026 Annual Meeting: Register to Attend. About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics.

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 ir@comstockinc.com

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “forecast,” “seek,” “target,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: expectations regarding the completion of the proposed securities offering, future market conditions; future explorations or acquisitions, divestitures, spin-offs or similar distribution transactions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: sales of, and demand for, our products, services, and/or properties; industry market conditions, including the volatility and uncertainty of commodity prices; the speculative nature, costs, regulatory requirements, and hazards of natural waste resource identification, exploration, development, availability, recycling, extraction, processing, and refining activities, including operational or technical difficulties, and risks of diminishing quantities or insufficiency of grades of qualified resources;; changes in our planning, exploration, research and development, production, and operating activities; research and development, exploration, production, operating, and other variable and fixed costs; throughput rates, margins, earnings, debt levels, contingencies, taxes, capital expenditures, net cash flows, and growth; restructuring activities, including the nature and timing of restructuring charges and the impact thereof; employment and contributions of personnel, including our reliance on key management personnel; the costs and risks associated with developing new technologies; our ability to commercialize existing and new technologies; the impact of new, emerging, and competing technologies on our business; the possibility of one or more of the markets in which we compete being impacted by political, legal, and regulatory changes, or other external factors over which we have little or no control; the effects of mergers, consolidations, and unexpected announcements or developments from others; the impact of laws and regulations, including permitting and remediation requirements and costs; changes in or elimination of laws, regulations, tariffs, trade, or other controls or enforcement practices, including the potential that we may not be able to comply with applicable regulations; changes in generally accepted accounting principles; adverse effects of climate changes, natural disasters, and health epidemics, such as the COVID-19 outbreak; global economic and market uncertainties, changes in monetary or fiscal policies or regulations, the impact of terrorism and geopolitical events, volatility in commodity and/or other market prices, and interruptions in delivery of critical supplies, equipment and/or raw materials; assertion of claims, lawsuits, and proceedings against us; potential inability to satisfy debt and lease obligations, including because of limitations and restrictions contained in the instruments and agreements governing our indebtedness; our ability to raise additional capital and secure additional financing; interruptions in our production capabilities due to equipment failures or capital constraints; potential dilution from stock issuances, recapitalization, and balance sheet restructuring activities; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to maintain the listing of our securities on any securities exchange or market; and our ability to implement additional financial and management controls, reporting systems and procedures and comply with Section 404 of the Sarbanes-Oxley Act, as amended. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Initiating coverage with an Outperform. Resolution Minerals Ltd (ASX: RML, OTCQB: RLMLF) is advancing the Horse Heaven Gold–Antimony–Tungsten–Silver Project in Idaho, now covering 14,580 hectares. Following China’s December 2024 ban on antimony exports to the U.S., the country faces a structural supply deficit with no meaningful domestic mining or processing capacity. Resolution is positioned to address this gap through both resource development and intention to build a commercial-scale hydrometallurgical processing facility, aligning the project with U.S. policy priorities around domestic critical mineral supply chains.

Golden Gate. Phase 1 drilling at the Golden Gate Prospect confirmed a fault-controlled Intrusion Related Gold System with indications of meaningful scale. All 14 holes intersected mineralization from surface, including intercepts of 253m at 1.50 g/t Au, 265m at 0.60 g/t Au, and 189m at 1.30 g/t Au, all open at depth, while a second discovery at Golden Gate South expanded the mineralized footprint to more than 1.5km of strike. Importantly, the historical Golden Gate Tungsten Mine, last in production in 1980, is located within Resolution’s property boundary, with management evaluating a restart. A Phase 2 program of up to 45 diamond holes across 13,700 meters commences in early May 2026.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Investor webinar. CEO John Passalacqua recently presented to investors via Simone Capital. During the call, Mr. Passalacqua commented on the signed contribution agreement with Natural Resources Canada, the ongoing drill program and future feasibility study, the ADR launch, and the strength of the stock in recent weeks relative to a difficult broader market. Management attributed the stock’s resilience to the quality of the shareholder base, consistent milestone execution, and the visible de-risking effect of government backing.

NRCan contribution agreement signed. First Phosphate has executed a formal agreement with Natural Resources Canada providing up to C$16.7 million in non-repayable government funding under the Global Partnerships Initiative. The structure is a reimbursement model, whereby the company incurs eligible expenditures and receives reimbursement of up to 75% within approximately three months, supporting technical and engineering validation work through 2028. Combined with approximately C$20-C$22 million in cash on hand, we estimate total accessible financial resources of approximately C$36-C$38 million, sufficient to fund the company through drill completion, feasibility study, and final investment decision.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

A year of repositioning. During 2025, Comstock Inc. repositioned itself around two scalable growth businesses: Comstock Metals, which targets solar panel recycling and critical mineral recovery, and its investment in Bioleum Corporation, which is advancing biomass-based renewable fuels.

Near-term revenue visibility. Comstock Metals represents the most immediate catalyst for value creation. Comstock has validated a zero-landfill solar panel recycling process and completed permitting for its first industry-scale facility in Nevada, with operations expected to commence in the second quarter of 2026. The company has also secured logistics infrastructure and customer agreements across key U.S. regions, reflecting growing demand for end-of-life solar panel processing. Over time, the strategy could include multiple facilities and integrated refining capabilities that target recovery of higher-value metals such as silver.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Expands Board as Company Accelerates Growth in Solar Recycling and Critical Metals Recovery

VIRGINIA CITY, NEVADA, March 24, 2026 – Comstock Inc. (NYSE: LODE) (“Comstock,” “our” and the “Company”), today announced its full year 2025 results, 2025 summary achievements, and our 2026 business outlook.

“Last year marked a number of critical achievements that punctuated the turnaround from a junior mining opportunity into a validated, leading metals recovery company positioned for global growth, including final proof of our zero-landfill recycling concept from our demonstration facility, team-building, full permitting, final, first-of-its-kind engineered and tested designs, secured industrial scale facility and storage capacity and fully funded the facility and operations while also receiving direct investment from Marathon Petroleum Corp and another third party investor, directly into Bioleum Corp., validating our efforts,” stated Corrado De Gasperis, the Company’s Executive Chairman and Chief Executive Officer. “Comstock has now founded, developed and positioned two distinct, high-growth businesses: a Nevada-based metals recovery company and an Oklahoma-based renewable fuels company, each with sophisticated strategic and financial partners and clear paths toward commercialization and growth.”

Recent Corporate Transactional and Liquidity and Capital Resources Highlights

Completed, in early 2026, an oversubscribed equity financing of $57.5 million in gross proceeds and $53.0 million, net of offering expenses, driven by demand from leading institutional investors and further strengthening our capital base to accelerate the commercialization and development of the Comstock Metals recycling and refining processes;

Eliminated all debt obligations, including convertible and promissory notes, and extinguished multiple other non-debt obligations, resulting in a strong financial position for accelerating growth and further monetizing non-core assets;

Separated Bioleum Corp. from Comstock based on $35 million in direct strategic investments from Marathon Petroleum Corp and another investor and secured our investment through a $65 million Convertible Preferred Stock.

Secured power equivalent to 250-300 MW supporting a high value monetization of Nevada real estate investments;

Expands Board with three outstanding, experienced, independent directors representing two of the Company’s top four shareholders, reflecting support of the exceptional opportunity positioned for solar recycling and critical metals. Cash and cash Equivalents were $17.0 million at December 31, 2025, and of cash and cash equivalents, prior to the net proceeds from the 2026 financing; and $56.1 million at March 20, 2026.

Common shares outstanding were 51.9 million at December 31, 2025, and 74.1 million shares at March 20, 2026.

“The successful capitalization of our Company with aligned, long term investors positions and enables global industrial growth and further non-core asset and investment sales to become a highly focused, highly-profitable, multi-billion dollar valued corporation,” stated Mr. De Gasperis. “This also positioned the interest and opportunity to further align, expand and enhance our board and governance with the competencies and capacities for governing a multi-billion-dollar global enterprise. Having two of our top four investors excited to support and participate this remarkable opportunity is highly gratifying, to say the least.”

Selected Segment Highlights for Comstock Metals (for the year ended December 31, 2025)

“We have now received all permits for commissioning and operating our first industry-scale facility. Equipment is arriving daily with all equipment expected on site in early April, with commissioning underway, and operations start up, on plan, during the second quarter of this year just as our order pipeline grows,” said Dr. Fortunato Villamagna, President of Comstock Metals.

Comstock Metals

Certified the R2v3/RIOS Responsible Recycling Standard by Sustainable Electronics Recycling International (“SERI”), authenticating the first zero-landfill recycling process that safely repurposes all recycled materials;

Received all operating and storage permits for our first-of-its-kind industry-scale facility in Nevada;

Receiving and installing major precision-manufactured equipment for the industrial production line, with commissioning ongoing and continuous operations on schedule for commencement in the second quarter of 2026;

Secured Master Service Agreements with multiple major utilities, developers, EPC firms, contractors, installers, and asset owners across the Southwest and multiple other regions of the United States;

Secured permits and received approval from California’s Department of Toxic Substances Control (“DTSC”), becoming one of a select group of companies authorized and operating as a universal waste recycler in California;

Established an Ohio and California-based logistics and aggregation hubs supporting two of the largest end-of-life solar panel geographic markets in the United States;

Completed preliminary design and feasibility for a U.S.-based, industrial metal refining solution for our tailings; and

Selected and submitted state-level permit applications for a second industry-scale production facility in Nevada.

“We remain the only certified R2v3/RIOS Responsible Recycling Standard by SERI for solar panel recycling (100% of the entire panel) and, with permits secured, the only solution that can efficiently scale to meet our customers rapidly growing need for end-of-life panel disposal,” said Dr. Villamagna. “Our sales and marketing teams are solely focused on expanding and capturing that market while our facility planning team simultaneously coordinating strategic site selections (processing and storage) across the whole country.”

Selected Segment Highlights for Comstock Mining (for the year ended December 31, 2025)

Closed on the sale and monetization of the northern district claims for approximately $3.0 million in total proceeds, including the acquisition, for no additional consideration, of more than 238 acres of Lyon County mineral properties, further enhancing our portfolio of Lyon County mineral properties and directly supporting the Dayton resource mine plans;

Increased our internal economic mineralized material estimates based on significantly higher gold and silver prices;

Completed the purchase of the Haywood industrial mineral properties, a key location for processing Dayton materials, and further enhancing our Lyon County mineral holdings and directly supporting the Dayton resource plans; and

Engaged multiple, sophisticated mining companies about the sale and monetization of our mineral and mining assets.

“The rapidly rising industrial silver demand and ongoing geopolitical concerns created an unprecedented runup in gold and a possibly even greater set up for silver prices, benefitting both our recycling and mining businesses. Our historic, world-class Nevada mining assets are now very well positioned for monetization, and we are directly engaged with a number of sophisticated mining concerns,” said Comstock’s Chief Financial Officer and Comstock Mining President, Mr. Judd Merrill.

Selected Highlights for Bioleum Corporation (“Bioleum”) (for the year ended December 31, 2025)

Separated our fuels portfolio and resources into the newly-created, Oklahoma-headquartered Bioleum Corporation:

Agreed on a $13.0 million strategic pre-Series A investment from subsidiaries of Marathon Petroleum Corp. (“MPC”);

Closed on a $20.0 million Series A preferred equity financing, with additional Series A planned for early 2026;

Exchanged our five-year, $65.0 million funding into a Series 1 Convertible Preferred Stock that is convertible into 32.5 million of the underlying common shares of stock of Bioleum Corporation;

Advanced our Cooperative Research and Development Agreement (“CRADA”) activities with the National Laboratory of the Rockies (“NRL”) and MIT for advancements in our low cost, high energy solutions;

Restarted the Madison, Wisconsin MPC pilot facility, fully integrating the Madison development teams;

Secured the first site and advanced site-specific engineering for the planned Oklahoma-based Bioleum refinery; and

Earned the second $1 million of the $3 million in awards from Oklahoma’s Quick Action Closing Fund.

Acquired Hexas Biomass Inc. and the entire RenFuel IP portfolio in December 2025.

“Bioleum is positioned for an unprecedented, versatile, and exceptionally high-yielding, ultra-low-carbon biofuel solution that integrates waste streams and purpose-grown crops in an extending eco-system designed to produce an abundance of extremely low carbon liquid fuels,” said Mr. DeGasperis. “Bioleum’s working teams in Wisconsin and Oklahoma are integrating their efforts into a system designed for accelerating commercially viable technologies while working on commercializing a series of farm-and-waste woody biomass to fuels production platforms.”

Outlook for 2026

Comstock Metals has established the goal of setting the global standard for solar panel recycling. Our process creates no waste, no landfilled materials, and results in clean recycled products safe for reuse.

Bioleum seeks to commercialize technologies, systems and supply chains that produce renewable fuels from waste, purpose grown energy crops and other forms of woody biomass, enabling and integrating agricultural and clean energy economics.

The growth opportunities for both Comstock Metals and Bioleum have and continue developing beyond our original plans, and we have now realigned both the organizations and their respective capital bases with some of the most sophisticated partners for investment, feedstocks, technologies, operations, and offtakes, including significant investments.

The Company’s Corporate objectives for 2026 include:

Monetize our legacy mineral and mining properties, plants and equipment;

Secure sufficient power source to enable hyper-scale data center developments in Silver Springs, NV;

Restructure, align, power, and expand the ownership in the Sierra Springs Opportunity Fund Inc. and monetize;

Monetize all other legacy, non-core real estate in Silver Springs, NV;

Support the next phases of accelerating Metals growth, including refining; and

Support the next phases of accelerating Fuels growth, including the commercialization of Hexas-based biomass solutions.

The Company’s progress to date has now resulted in two, fully dedicated, high-growth potential companies: our Nevada-based renewable metals operation with expanding, multiple, industry-scale production sites and our Oklahoma-headquartered Bioleum Corporation, with major research, development and pilot production operations based in Wausau and Madison, Wisconsin and Hexas Biomass farming and purpose grown energy crop solutions in Olympia, Washington.

Comstock Metals

Comstock Metals has now been operating its first commercial demonstration facility for nearly two years and in November of 2024, submitted permits for the first industry-scale photovoltaic recycling facility in northern Nevada. The permits were received in early January of 2026. Comstock Metals has also selected its second site in the southern part of the State of Nevada. These industry-scale facilities are designed for recycling up to 3.3 million panels (or approximately 100,000 tons) of annual capacity, with operations for the first facility commencing post commissioning activities during the first quarter of 2026 for operations in the second quarter 2026.

Additional site selection activities are ongoing for the next five industry-scale facilities (that is, industry-scale recycling facilities #3-#7) and multiple associated storage sites and at least one centralized, industrial scale refining facility capable of handling the metals-rich tailings produced by its recycling facilities.

The Company’s Metals objectives for 2026 include:

Receive, deploy, assemble and commission our first industry-scale facility in Silver Springs, NV;

Operate our first industry-scale facility in Silver Springs profitably;

Secure additional Master Service Agreements (MSA) with national and regional customers;

Select and secure additional sites, expand storage capabilities and secure permits for these additional sites;

Submit permits for our second industry-scale facility in southern, NV;

Procure the equipment for our second industry-scale recycling and processing facility and commence commissioning;

Complete site selection for at least three additional solar panel recycling locations and commence permitting;

Evaluate international expansion opportunities with international strategic and capital partners; and

Advance development efforts, with strategic partners, to recover more and higher-purity materials from recycled streams.

The capital expenditures for each of the first and second facilities with 100,000 tons of annual capacity are expected to be approximately $14.0 million each, which includes expanded storage. The Company estimates total capital spending of approximately $13.0 million to be fully paid by the end of the first quarter of 2026. Revenues were three times greater in 2025 of $1.4 million, as compared to 2024 of $0.4 million. Total billings in 2025 were over $3.5 million. Master Service Agreements are being signed with major utility and electronic recycling aggregators across the U.S. and particularly in the southwest regions including California, Arizona and Nevada. Future revenue growth will depend on the rate of customer replacements, pricing, and operating performance as the Company scales production.

Comstock Mining

Comstock Mining has amassed the single largest known land position within the Comstock mineral district, including an extensive repository of drilling data, engineering, and gold and silver resources, including the Lucerne and Dayton resources.

The Company’s Mining objectives for 2026 include:

Commercialize agreements that monetize our mining and related mining beneficiation assets; and

Publish the Dayton Consolidated Project technical work with preliminary economics and sensitivities.

The Company’s 2026 efforts will be to monetize these assets completely or partially, with partners willing to acquire and deploy capital and capacity to develop, advance and ultimately further monetize these assets to the benefit our shareholders.

Bioleum

Bioleum is actively engaged in the expansion of its pilot production facilities and the planning for its first commercial demonstration facilities and the associated supply chain participants (including feedstock, site selection, engineering, construction and offtake).

Bioleum’s objectives for 2026 include:

Complete the remaining “Series A” equity financing for Bioleum;

Deploy a Hexas-based, commercial demonstration fuel farm;

Expand integrated pilot production capabilities to up to five barrels per week of intermediates and fuels;Commercialize at least one major new project for purpose grown feedstock applications;Commercialize at least one major new project for renewable fuel applications;Commercialize at least one major project that integrates our technology solutions into existing production platforms; andAdvance our innovation and development efforts toward even higher yields, lower costs and lower capital.

Bioleum also offers integrations of its solutions into existing agriculture, forestry, pulp and paper, ethanol, and existing petroleum infrastructures to generate additional capacities, revenues, technical services, engineering and royalties. The plans also include integrating Bioleum’s high yield Bioleum refining platform with Hexas’ high yield energy crops to provide enough feedstock to produce upwards of 100 barrels of fuel per acre per year, effectively transforming agricultural lands into perpetual “drop-in sedimentary oilfields” with the potential to dramatically boost domestic energy resources.

Summary

“In 2026, we plan on increasing our early mover advantage in solar panel recycling as we commission our first industry-scale facility, select and secure the next three sites for processing and storage and rapidly expand our national footprint,” concluded Mr. De Gasperis. “We are winning in the market and continue securing and forging market share from the largest and fasting growing customers while advancing refining development efforts to recover more and higher-purity metals and materials.”

CONFERENCE CALL DETAILS

Comstock’s Chief Executive Officer, Corrado De Gasperis, and its Chief Financial Officer, Judd Merrill, will present an overview of the year end 2025 financial results, upcoming commercial and monetization milestones, and how the Company’s systemic platform is optimizing results on Tuesday, March 24, 2026, via a webinar.

Investors and all other interested parties are invited to register below.

HAVE QUESTIONS? There will be an allotted time following the results presentation for a Q&A session. Unaddressed questions will be reviewed by management and responded to accordingly. You may submit your question(s) beforehand in the registration form (linked above) or by email at: ir@comstockinc.com.

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 ir@comstockinc.com

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “forecast,” “seek,” “target,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: expectations regarding the completion of the proposed securities offering, future market conditions; future explorations or acquisitions, divestitures, spin-offs or similar distribution transactions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: sales of, and demand for, our products, services, and/or properties; industry market conditions, including the volatility and uncertainty of commodity prices; the speculative nature, costs, regulatory requirements, and hazards of natural waste resource identification, exploration, development, availability, recycling, extraction, processing, and refining activities, including operational or technical difficulties, and risks of diminishing quantities or insufficiency of grades of qualified resources;; changes in our planning, exploration, research and development, production, and operating activities; research and development, exploration, production, operating, and other variable and fixed costs; throughput rates, margins, earnings, debt levels, contingencies, taxes, capital expenditures, net cash flows, and growth; restructuring activities, including the nature and timing of restructuring charges and the impact thereof; employment and contributions of personnel, including our reliance on key management personnel; the costs and risks associated with developing new technologies; our ability to commercialize existing and new technologies; the impact of new, emerging, and competing technologies on our business; the possibility of one or more of the markets in which we compete being impacted by political, legal, and regulatory changes, or other external factors over which we have little or no control; the effects of mergers, consolidations, and unexpected announcements or developments from others; the impact of laws and regulations, including permitting and remediation requirements and costs; changes in or elimination of laws, regulations, tariffs, trade, or other controls or enforcement practices, including the potential that we may not be able to comply with applicable regulations; changes in generally accepted accounting principles; adverse effects of climate changes, natural disasters, and health epidemics, such as the COVID-19 outbreak; global economic and market uncertainties, changes in monetary or fiscal policies or regulations, the impact of terrorism and geopolitical events, volatility in commodity and/or other market prices, and interruptions in delivery of critical supplies, equipment and/or raw materials; assertion of claims, lawsuits, and proceedings against us; potential inability to satisfy debt and lease obligations, including because of limitations and restrictions contained in the instruments and agreements governing our indebtedness; our ability to raise additional capital and secure additional financing; interruptions in our production capabilities due to equipment failures or capital constraints; potential dilution from stock issuances, recapitalization, and balance sheet restructuring activities; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to maintain the listing of our securities on any securities exchange or market; and our ability to implement additional financial and management controls, reporting systems and procedures and comply with Section 404 of the Sarbanes-Oxley Act, as amended. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

For decades, the playbook has been simple: when war breaks out, buy gold. But the ongoing U.S.-Israeli conflict with Iran is rewriting that script in real time, and investors are scrambling to make sense of a metal that is behaving more like a speculative trade than the world’s oldest store of value.

Gold has dropped nearly 10% this week, putting it on track for its worst weekly performance in 43 years, with the metal’s total decline since the war began now sitting at approximately 13%. On Friday, gold was trading around $4,570 per troy ounce — erasing two months of gains in a matter of days.

The Rate Problem Nobody Saw Coming

The paradox at the heart of gold’s collapse is this: the same war that should theoretically be sending investors rushing into safe-haven assets is also the reason central banks are slamming the door on interest rate cuts.

The Federal Reserve held rates steady and cited uncertain impacts from the conflict, while the Bank of Japan kept rates unchanged, noting that inflation risks are now tilted to the upside. Central banks across Europe — including the U.K. and the eurozone — followed suit. Market expectations for Fed rate cuts have shifted dramatically, with traders now pricing in no cuts until as late as June 2027 — a full twelve months later than pre-war projections. That matters enormously for gold, which pays no yield. When bonds and other interest-bearing assets become more attractive, gold loses its competitive edge almost immediately.

The Dollar Is Doing Gold No Favors Either

The U.S. dollar has rebounded approximately 2.2% since the Iran war began, halting a months-long slide. Because gold is priced in dollars, a stronger greenback makes the metal relatively more expensive for international buyers, dampening global demand.

Oil prices have remained above $100 per barrel following attacks on major energy infrastructure, including one of the world’s largest natural gas fields shared by Iran and Qatar, with the conflict showing no signs of resolution. Energy-driven inflation is now feeding directly into the rate calculus that is punishing gold.

From Safe Haven to Meme Trade — and Back?

Part of what’s happening is a hangover from an extraordinary run. Gold surged 66% in 2025, its best annual performance since 1979, before hitting $5,000 per troy ounce for the first time in January 2026. Retail investors piled in chasing momentum, and when that momentum began to reverse, the selling accelerated. Some analysts have raised the possibility that central banks, which were previously aggressive buyers, may now be turning into net sellers — an additional headwind few had anticipated.

The longer-term bull case hasn’t disappeared. J.P. Morgan maintains a 2026 year-end target of $6,300 per ounce, while Deutsche Bank holds firm at $6,000 — though both forecasts were set before the Iran escalation.

For long-term holders, the fundamental case remains intact. Real interest rates, global monetary policy, and persistent geopolitical uncertainty have historically been the primary drivers of sustained gold bull markets, and none of those underlying forces have been resolved.

The question isn’t whether gold’s story is over. The question is whether the market has finally priced in a world where geopolitical chaos and monetary tightening can coexist — and where gold, at least temporarily, is caught in the crossfire.

VANCOUVER, BC, March 19, 2026 – Nicola Mining Inc. (the “Company” or “Nicola”) (TSX: NIM) (OTCQB: HUSIF) (FSE: HLIA) is pleased to announce that Warren Wagner has completed his Master of Science (M.Sc.) thesis, at the university of British Columba’s (UBC) Mineral Deposit Research Unit (MRDU), on the New Craigmont copper project[1]. His thesis is titled The Skarn to Porphyry Transition: Establishing Links Between Skarn and Porphyry-Type Mineralization at New Craigmont British Columbia. The full publication and supplementary data tables are available for download on the UBC website: https://open.library.ubc.ca/soa/cIRcle/collections/ubctheses/24/items/1.0451531

The purpose of the thesis was to examine the potential connection between the historically mined Craigmont skarn and undiscovered porphyry systems in the surrounding area. Using field observations, petrography, whole-rock and mineral chemistry, and integrated geochronology, Warren’s thesis has redefined Craigmont as a porphyry-linked skarn system genetically tied to multi-pulsed Late Triassic magmatism within the Guichon Creek batholith’s Border Phase.

Mineral ages determined through geochronology lab work defined two discrete hydrothermal stages: massive calcsilicate skarn alteration at ~215 Ma related to the earliest Border Phase intrusions and overprinting, vein-hosted porphyry-type mineralization at ~209 Ma associated with later, oxidized intrusions.

Potassic, phyllic, calc-potassic, and propylitic alteration styles indicate the presence of a larger porphyry system proximal to the skarn deposit. Epidote mineral chemistry from propylitic assemblages further supports this. New Craigmont epidote contains elevated porphyry indicator trace elements consistent with other porphyry deposits in British Columbia and worldwide. Finally, epidote mineral chemistry systematics within the Guichon Creek batholith reveal that New Craigmont contains a separate, porphyry centre, unrelated to those of the Highland Valley district. The study also highlights the importance of structural permeability and reactive Nicola Group host rocks in focusing hydrothermal fluids and controlling the distribution of skarn and porphyry-style mineralization.

Conclusions of the study have positive implications for ongoing exploration at New Craigmont. The study confirms Nicola’s ongoing hypothesis that the historical skarn is driven by a nearby porphyry system. Detailed geochemistry work has helped narrow exploration to broadly two regions within the property: West Craigmont (where the Draken target is located), and east of the historical mine (where the Jotun target is located). Nicola is integrating MRDU data into ongoing vectoring work and target generation.

Peter Espig, CEO of Nicola, stated, “We applaud Warren and MRDU on two years of fruitful work at our New Craigmont Copper Project. The thesis’ conclusion aligns with our growing confidence in our three years of geological work, mapping and 2025 porphyry vectoring. Given the size of our land package and location, which includes sharing Guichon Batholith with Highland Valley Copper, the prospect of having one or more porphyries at New Craigmont is increasingly compelling, as highlighted in the thesis. We are very encouraged to commence our 2026 Exploration Program.”

Qualified Person

The scientific and technical disclosures included in this news release have been reviewed and approved by Will Whitty, P.Geo., who is the Qualified Person as defined by NI 43-101. Mr. Whitty is Vice President, Exploration for the Company.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the TSX-V Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia. It has signed Mining and Milling Profit Share Agreements with high-grade BC-based gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a property that hosts historical high-grade copper mineralization and covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

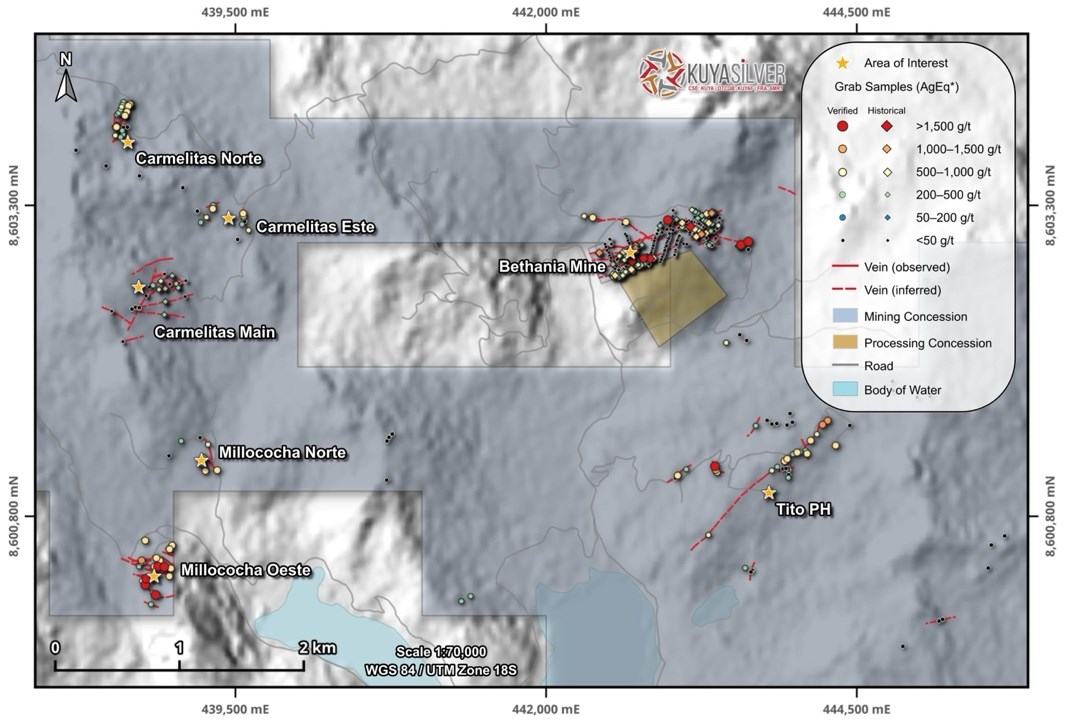

Kuya Silver is significantly scaling its exploration efforts at Bethania. The company has expanded its fully funded 2026 drill program to approximately 20,000 meters, making it the largest drilling campaign in the project’s history. By combining 10,000 meters of surface and 10,000 meters of underground drilling, Kuya seeks to extend known mineralization near existing operations and test new district scale targets, positioning the project for meaningful resource growth.

High-grade regional targets highlight strong expansion potential. Exploration has identified multiple vein systems beyond the current mine area, with high priority prospects such as Millococha, Tito PH, and Carmelitas demonstrating encouraging grades and geological continuity. These areas, supported by historic artisanal mining and recent sampling, suggest the presence of a broader mineralized system that could materially increase the overall resource base.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

President Trump issued a 60-day waiver of the Jones Act on Wednesday in a bid to cool surging domestic energy prices as the Iran conflict continues to hammer global oil markets. The move, confirmed by White House press secretary Karoline Leavitt, opens U.S. ports to foreign-flagged vessels for the next two months — covering crude oil, refined products like gasoline and diesel, natural gas, coal, fertilizer, and other energy-derived commodities.

The decision comes as Brent crude crossed $109 per barrel Wednesday morning — up more than 7% on the day — while WTI traded above $97. Gas prices at the pump have climbed to a national average of $3.84 per gallon, up sharply from $2.92 just one month ago, according to AAA data. Diesel has already crossed $5 per gallon nationally. The administration is clearly feeling political pressure to act ahead of the midterm cycle, and the Jones Act waiver is the most tangible move it has made so far.

What the Jones Act Actually Does

The Jones Act — formally the Merchant Marine Act of 1920 — requires that any cargo transported between U.S. ports be carried by vessels that are U.S.-built, U.S.-owned, U.S.-flagged, and U.S.-crewed. The law was designed to protect the domestic shipping industry after World War I, but has long been criticized by economists as an inflationary form of protectionism that raises the cost of moving goods within the country. With fewer than 100 Jones Act-compliant vessels in existence, the waiver immediately opens the door to a much larger pool of international tankers to move fuel between domestic ports.

The Practical Impact — And Its Limits

In theory, the waiver should have its biggest effect on refined product shipments from Gulf Coast refinery complexes to the more isolated East Coast — a corridor that has historically been a bottleneck during supply disruptions. Cheaper, more accessible shipping capacity means fuel can theoretically move faster and at lower cost to the regions that need it most.

But experts are already tempering expectations. The core problem isn’t moving fuel — it’s refining it. Most U.S. refineries are configured to process heavier Middle Eastern crude grades, while domestic shale production yields lighter oil. That structural mismatch means the U.S. still cannot fully self-supply even with more flexible shipping rules. The waiver makes domestic logistics more efficient, but it does not solve the underlying supply equation.

The Broader Policy Picture

The Jones Act move is reportedly just one item on a broader White House menu of potential energy interventions being considered, including possible Treasury-led action in energy futures markets and export bans on crude and refined products. Any of those measures — if enacted — would carry significant market implications across the energy sector.

For small and microcap investors, the read-through is layered. Domestic shippers and Jones Act operators could see near-term pricing pressure as foreign competition enters the market. Refiners with Gulf Coast exposure and East Coast distribution capability may benefit from improved logistics economics. And any company with meaningful fuel cost exposure — from regional truckers to agricultural operators to industrial manufacturers — should be watching this space closely as the administration continues to improvise policy responses to a crisis with no clear end date.

Toronto, Ontario–(Newsfile Corp. – March 17, 2026) – Kuya Silver Corporation (CSE: KUYA) (OTCQB: KUYAF) (FSE: 6MR1) (the “Company” or “KuyaSilver“) is pleased to announce an expansion of its fully-funded 2026 drill program at the Bethania Silver Project in central Peru designed to unlock value by focusing on delineating mineralized silver vein systems which have been historically underexplored. The program, expected to total approximately 20,000 metres combined underground and surface diamond drilling, would represent the largest drill program ever at the Bethania project.

The surface drill program is planned for approximately 10,000 metres and will focus on priority targets associated with historical artisanal mining areas identified during the Company’s recent regional exploration work, located outside the immediate Bethania mine area (Figure 1 below). These targets represent potential additions to the district-scale mineralized system and may also have potential for future production. Over the coming months Kuya Silver plans to conduct additional work to prioritize targets for the 2026 drill program which may include any of the six previously identified regional silver vein systems (e.g. Carmelitas, Tito PH, Millococha)

The Company also plans to expand on its previously announced underground drilling program to approximately 10,000 metres in 2026 (from 5,000 metres announced previously). Drilling will be conducted from established mine levels and is designed to test extensions of known mineralized structures that remain open along strike and at depth. This approach allows the Company to expand resources adjacent to current mine infrastructure while testing high-priority targets at relatively low cost and improving the geological continuity of the known vein system.

The combined surface and underground programs are expected to improve the geological understanding of the mineralized systems and support the Company’s ongoing efforts to grow resources within the broader Bethania district. Initial results from the underground drilling campaign are expected in Q2 2026 and additional drill results from underground and initial surface drilling results are expected over the second half of 2026.

“Following encouraging surface exploration results across the Bethania property, we are excited to begin the next phase of drilling,” stated Osbaldo Zamora, VP Exploration of Kuya Silver. “By combining surface drilling with underground drilling from existing workings, we are able to efficiently test both district-scale targets and near-mine extensions that could meaningfully expand the project’s resource base.”

David Stein, Kuya Silver’s President and CEO also remarked, “The Company is excited to embark on a much larger drill campaign covering multiple targets across the Bethania district. Given our significant cash position in excess of USD $25 million and expected cash flow from the Bethania mine, this more aggressive exploration strategy should be fully funded from internal sources and can be maintained and expanded over the coming years as we grow our silver mining operations.”

Figure 1: Bethania historical surface exploration results up to February 2026 showing all sample locations.

Surface drilling is expected to commence in the coming months following final permitting and logistical preparations. Over the past five plus years, Kuya Silver has consolidated in excess of 4,500 ha surrounding the Bethania mine. Various surface prospecting campaigns over the past several years has identified six different silver vein systems characterized by historical evidence of artisanal mining and outcropping veins with silver-polymetallic mineralization which have been mapped and sampled by Kuya Silver’s geologists. These additional vein systems can be subdivided into three areas located south (Tito PH), west (Carmelitas) and southwest (Millococha) of the Bethania silver mine.

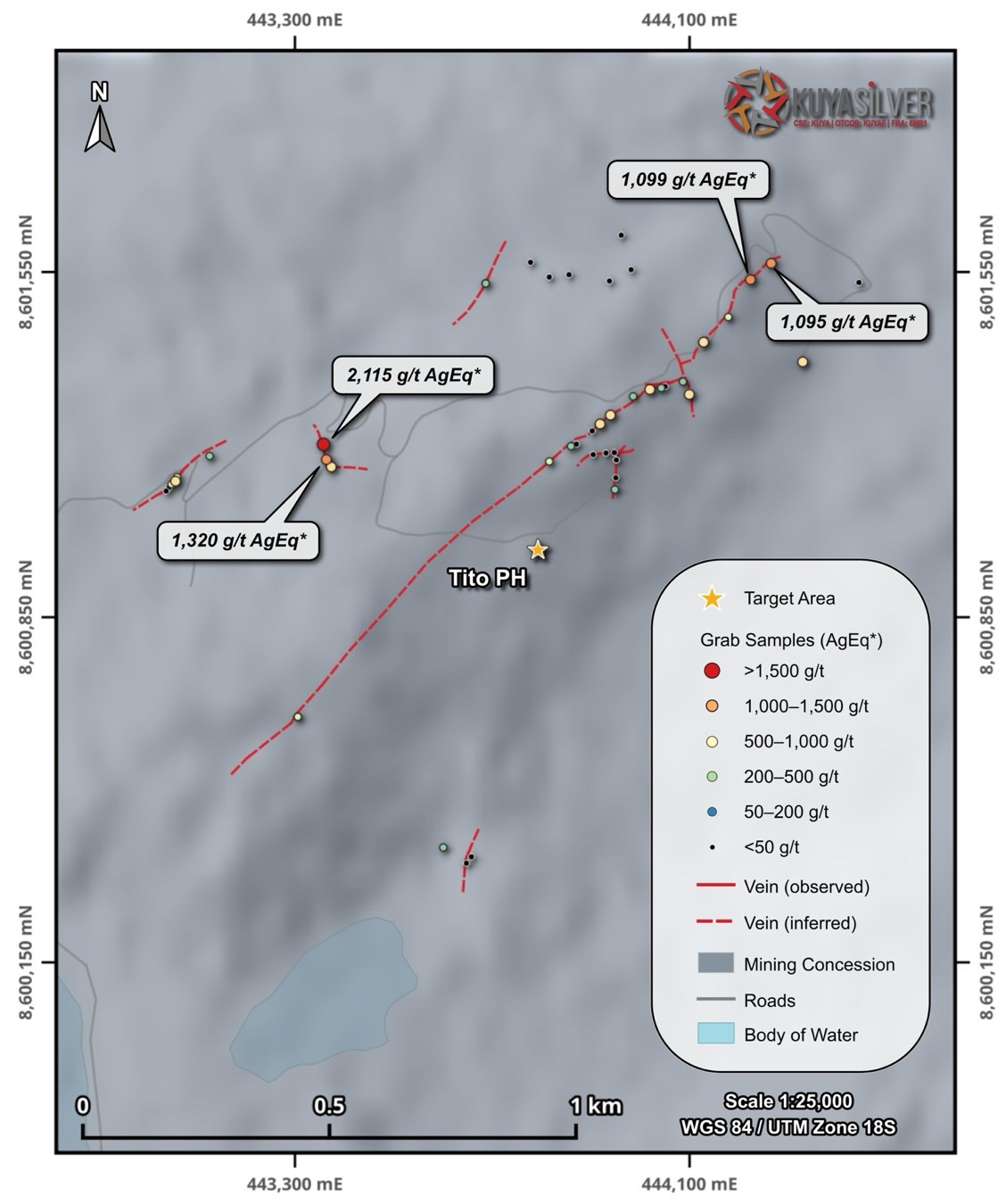

Tito PH

Tito PH is a priority exploration target consisting of one main vein and at least seven additional subparallel veins (Figure 2 below). The main vein has been mapped over approximately 600 metresof strike and may extend up to 1,500 metres, although a 700 metres gap in surface exposure remains to be tested by drilling.

Minor artisanal workings, including two shallow adits and an open stope, occur along the vein cluster. A total of 55grab samples collected by Kuya Silver geologists returned an arithmetic average grade of 285.7 g/t AgEq* and a maximum value of 2,114.7 g/t AgEq*. The interpreted strike length and high-grade surface samples suggest the system could be comparable in scale to the veins currently mined at Bethania.

Figure 2. Detailed map showing interpreted veins, grab sample locations, and assays at the Tito PH prospect.

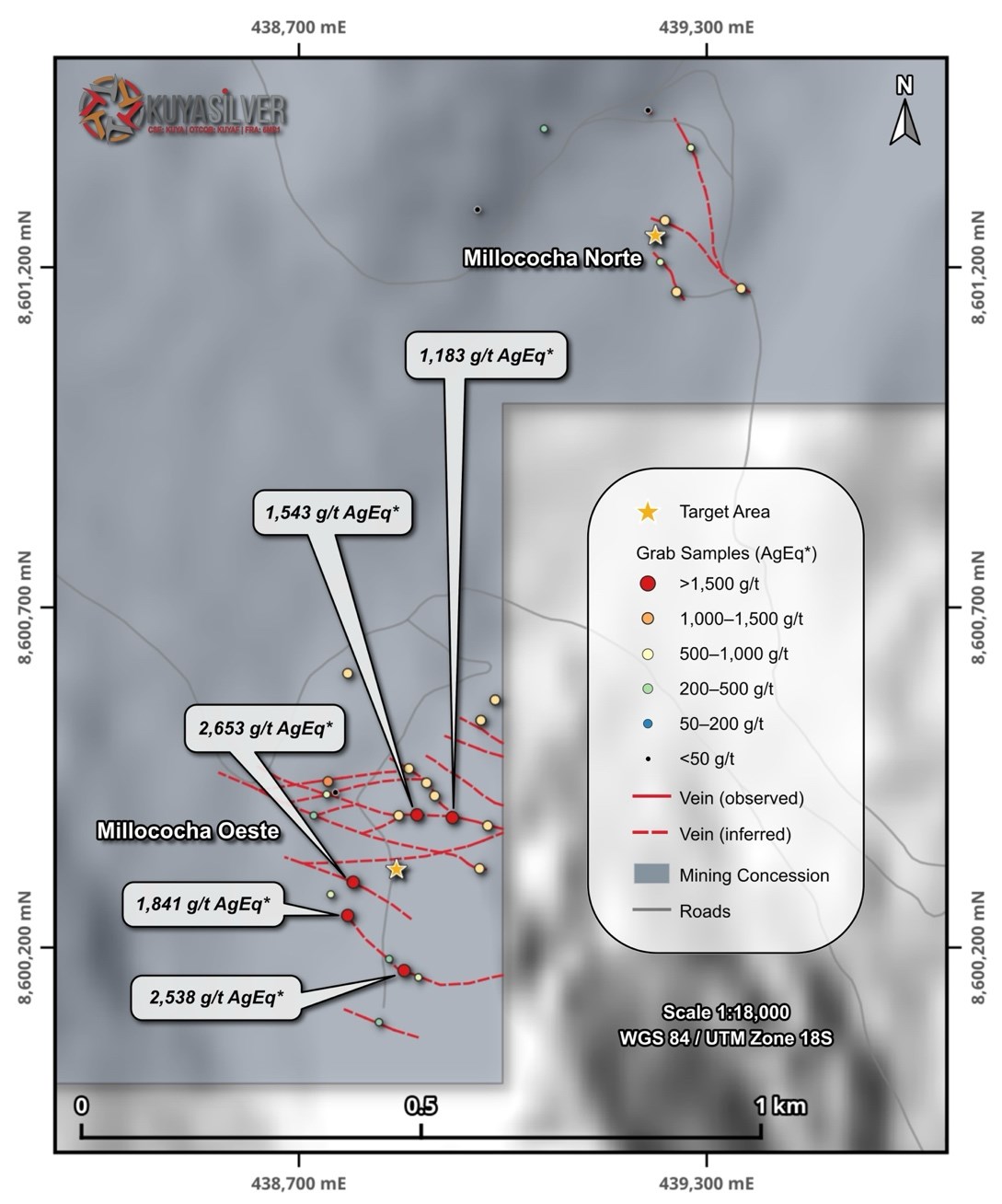

Millococha Oeste is one of the most prospective targets identified within the Bethania land package due to the presence of more than 10 mapped veins with consistently high grades. A total of 40 grab samples collected by Kuya Silver geologists returned an arithmetic average grade of 690.4 g/t AgEq* and a maximum value of 2,652.7 g/t AgEq* (Figure 3 below).

Artisanal workings on Kuya Silver’s claims represent the most significant historic activity outside the Santa Elena concession, but remain relatively shallow and poorly explored, highlighting the potential for additional mineralization at depth.

Figure 3. Detailed map showing interpreted veins, grab sample locations, and assays at the Millococha prospect.

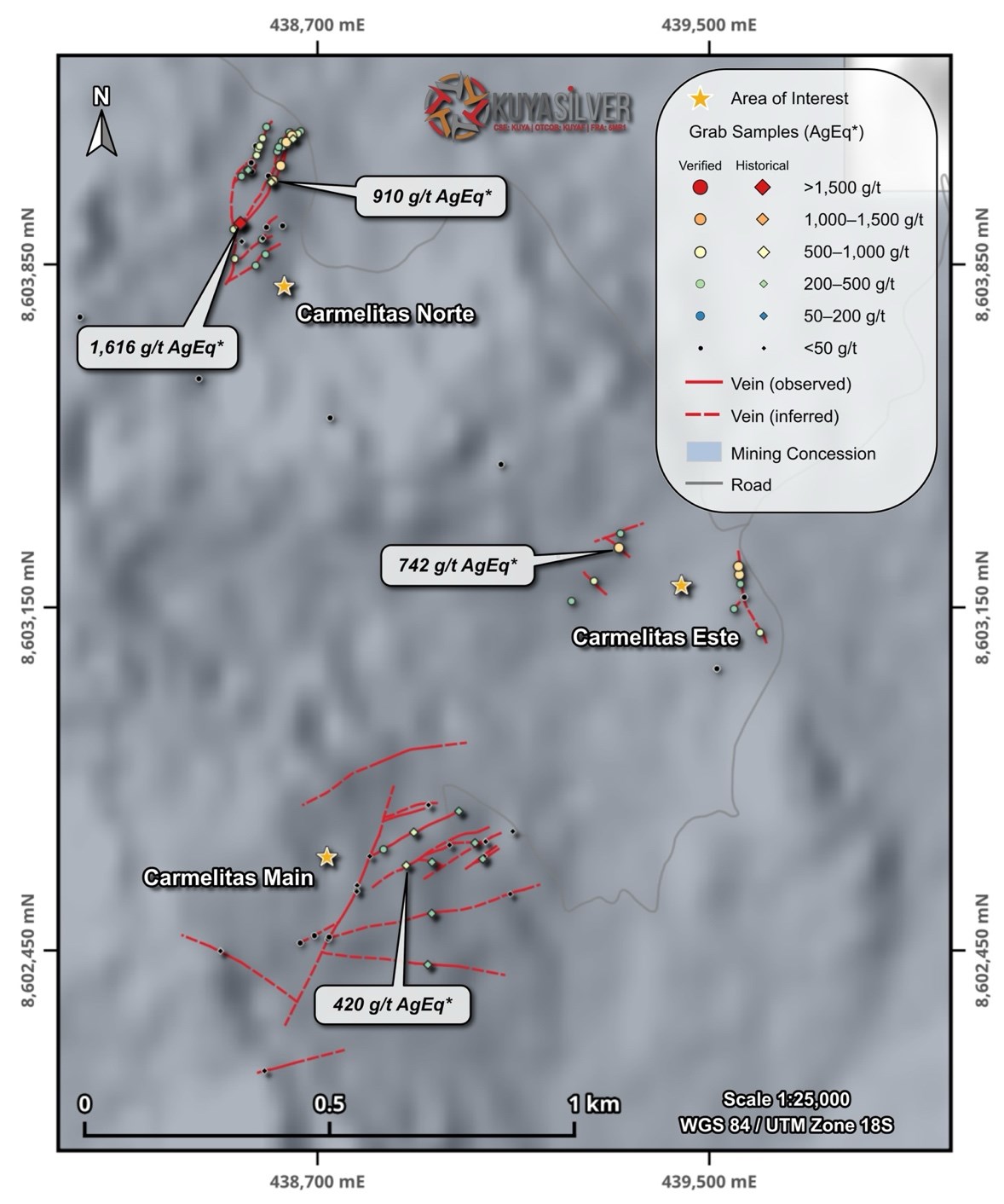

The Carmelitas prospect includes three vein clusters within an area of approximately 800 metres, comprising the main Carmelitas artisanal mine as well as the Carmelitas Norte and Carmelitas Este showings (Figure 4 below). A total of 125 grab samples collected by Kuya Silver returned grades up to 1,771.5 g/t Ag and an arithmetic average of 145.2g/t AgEq*.

Although vein density is lower than at other targets, the prospect remains attractive due to the presence of high-grade mineralization and potential structural connections between the three vein clusters.

*Silver Equivalency (AgEq) was calculated using silver ($85.74 USD/troy oz), gold ($5,177.70 USD/troy oz), copper ($12,815.48 USD/tonne), lead ($1,892.0 USD/tonne) and zinc ($3,286.76 USD/tonne) values, obtained on March 3, 2026 from Kitco, and do not consider metal recovery.

Figure 4. Detailed map showing interpreted veins, grab sample locations, and assays at the Carmelitas prospect.

A total of 940 grab samples (plus QA/QC) were collected in different exploration campaigns from 2021 to 2026. Only 192 samples collected from 2024 to 2026 count with proper QA/QC assessment. The coordinates of the locations of each sample were measured by handheld GPS and the samples dispatched to the ALS Peru S.A. laboratory in Lima for geochemical analysis. The analyses were carried out using the following methods:

ME-OG61a – Multi-acid digestion with ICP-AES detection for 33 elements

Au-AA23 – Fire assay for gold

Ag-OG62 – Four-acid digestion with ICP-AES detection for overlimit silver

All QA/QC standards were acceptable and within two standard deviations of certified values.

As these samples include a mix of early-stage grab, chip, and channel samples and do not include details on vein width, they are not fully representative of total vein mineralization.

National Instrument 43-101 Disclosure

The technical content of this news release has been reviewed and approved by Osbaldo Zamora, PhD., P.Geo., Vice President Exploration with Kuya Silver Corp. and a Qualified Person as defined by National Instrument 43-101.

About Kuya Silver Corporation

Kuya Silver is a Canadian‐based, growth-oriented mining company with a focus on silver. Kuya Silver operates the Bethania silver mine in Peru, while developing district-scale silver projects in mining-friendly jurisdictions including Peru and Canada.

This news release contains statements that constitute “forward-looking information,” including statements regarding the plans, intentions, beliefs, and current expectations of the Company, its directors, or its officers with respect to the future business activities of the Company. The words “may,” “would,” “could,” “will,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “expect,” “must,” “next,” “propose,” “new,” “potential,” “prospective,” “target,” “future,” “verge,” “favorable,” “implications,” and “ongoing,” and similar expressions, as they relate to the Company or its management, are intended to identify such forward-looking information. Investors are cautioned that statements including forward-looking information are not guarantees of future business activities and involve risks and uncertainties, and that the Company’s future business activities may differ materially from those described in the forward-looking information as a result of various factors, including but not limited to fluctuations in market prices, successes of the operations of the Company, continued availability of capital and financing, and general economic, market, and business conditions. There can be no assurances that such forward-looking information will prove accurate, and therefore, readers are advised to rely on their own evaluation of the risks and uncertainties. The Company does not assume any obligation to update any forward-looking information except as required under the applicable securities laws.

Neither the Canadian Securities Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this release.

HOUSTON, March 16, 2026 /PRNewswire/ — Summit Midstream Corporation (NYSE: SMC) (“Summit”, “SMC” or the “Company”) announced today its financial and operating results for fourth quarter and full-year 2025, Permian and Rockies segment growth update, and provided full-year 2026 financial guidance.

Highlights

Fourth quarter net loss of $7.3 million, Adjusted EBITDA of $58.5 million, cash flow available for distributions (“Distributable Cash Flow” or “DCF”) of $33.7 million and free cash flow (“FCF”) of $17.0 million

Recently signed three 10+-year firm take-or-pay contracts on Double E that are expected to drive Permian Segment Adjusted EBITDA from $34 million in 2025 to approximately $60 million in 2029

Launched a binding open season on Double E to secure market commitments to support a mainline compression project to increase firm capacity by up to 50% from 1.6 Bcf/d to approximately 2.4 Bcf/d

Refinanced Double E capital structure1 with a new term loan that will fund Double E capital projects (including the mainline compression project) and provide an $85 million one-time distribution to Summit to pay down debt and repay $45 million of arrears on its corporate Series A Preferred Stock

Executed a new 10-year crude oil gathering agreement covering more than 200,000 acres in the Williston

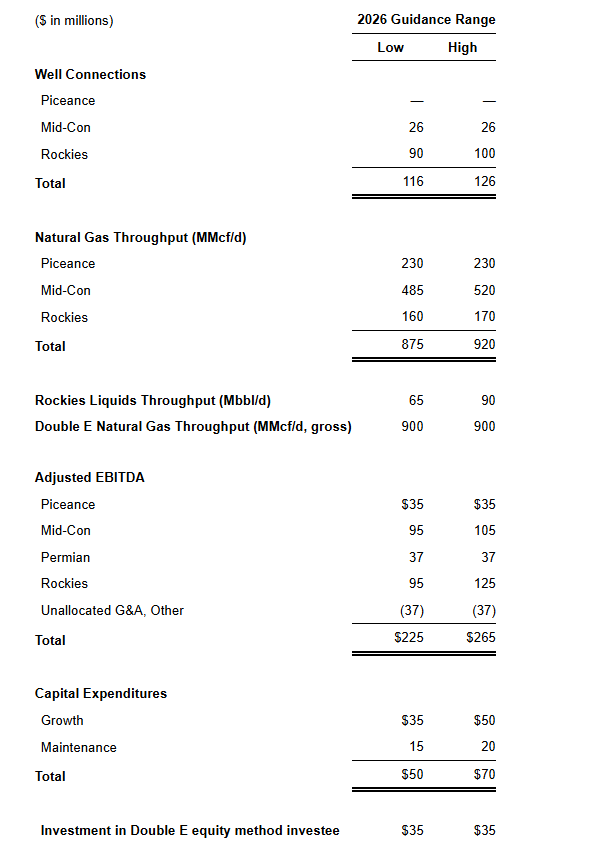

Active customer base with seven rigs running, approximately 90 DUCs and 116 to 126 wells expected in 2026

Provided 2026 full-year financial guidance range of $225 million to $265 million in Adjusted EBITDA and total capital expenditures of $85 million to $105 million, including $35 million attributable to Double E

Management Commentary

Heath Deneke, President, Chief Executive Officer and Chairman, commented, “We are pleased with the commercial and financial progress achieved over the past two quarters, which underscore the strategic value of our infrastructure, embedded growth opportunities, and our continued focus on execution with financial discipline. With the signing of major long-term agreements on the Double E Pipeline and in the Williston Basin, we are building on strong commercial momentum in our Permian and Rockies segments, while maintaining steady operational performance, strengthening our balance sheet and allocating capital prudently. We’re also further advancing Double E’s growth with a new open season to support a mainline compression project that could expand pipeline capacity by 50% by the end of 2028. Additionally, the Double E refinancing underscores Summit’s financial flexibility and ability to execute on important growth initiatives while continuing to maintain focus on reaching long-term corporate leverage targets. The planned repayment of the arrears on the Series A Preferred Stock further simplifies Summit’s balance sheet and is also an important step towards enabling a sustainable return of capital program for our shareholders in the future.

Operationally, despite the earlier oil price headwinds, we maintained an active customer base with seven rigs currently running behind our systems, approximately 90 DUCs and between 116 to 126 wells expected to be turned in line in 2026. Our 2026 outlook reflects sustained activity across our systems and incremental investment in high-return growth projects, which we expect will drive EBITDA growth in 2027 and beyond. Furthermore, given the mid-$60 oil price assumption embedded in our 2026 guidance, we are optimistic that customer activity levels could further increase in the second half of the year if the recent spike in oil prices continues to lift the backend of the forward price curve.”

Double E Commercial Update

Producers Midstream II reached a final investment decision on Train II of its Dude processing plant in Lea County, New Mexico, which was a condition precedent to the commencement of the previously announced 10-year, 100 MMcf/d firm transportation agreement. The new contract is expected to commence service in the fourth quarter of 2026.

Double E Pipeline entered into a new 11-year take-or-pay natural gas firm transportation agreement with a large, investment-grade shipper for 210 MMcf/d of capacity, including 80 MMcf/d expected to commence in the fourth quarter of 2026 and an additional 130 MMcf/d expected to commence in the second half of 2028. These commitments also expand Double E’s downstream connectivity with new delivery points into the Transwestern Central Pool, the Hugh Brinson Pipeline and a planned future connection with the Desert Southwest Pipeline. The new delivery points will significantly broaden Double E Shipper’s access to diverse and growing end use markets in addition to the multiple interconnects with downstream egress pipelines connecting the Waha Hub to Gulf Coast markets.

Double E Pipeline also entered into a new 11+ year natural gas transportation agreement with an undisclosed shipper for 230 MMcf/d of firm capacity, with 100 MMcf/d expected to start in the fourth quarter of 2027, 80 MMcf/d in the fourth quarter of 2028, and an additional 50 MMcfd in the second quarter of 2029. The agreement is contingent upon satisfaction of certain customary conditions precedent and is subject to shipper providing notice of its final investment decision to construct an expansion of its processing facility prior to October 1, 2026.

With the additional contracts, Summit expects its 70% interest in Double E to generate approximately $60 million of Segment Adjusted EBITDA in 2029, representing an approximate 76% increase to the $34 million of Segment Adjusted EBITDA generated in 2025. These projects are expected to cost approximately $50 million, net to Summit’s 70% interest, with approximately $35 million expected in 2026 and the remainder in 2027. These capital requirements are expected to be fully funded with the new term loan at Summit Permian Transmission which is non-recourse to Summit. Further, Double E has launched a binding open season to secure market commitments to support a mainline compression project to expand the pipeline’s capacity from approximately 1.6 Bcf/d to over 2.4 Bcf/d by the end of 2028. The compression expansion remains subject to additional commercial support via incremental long-term take-or-pay agreements and FERC and other regulatory approvals.

Double E Refinancing Transaction

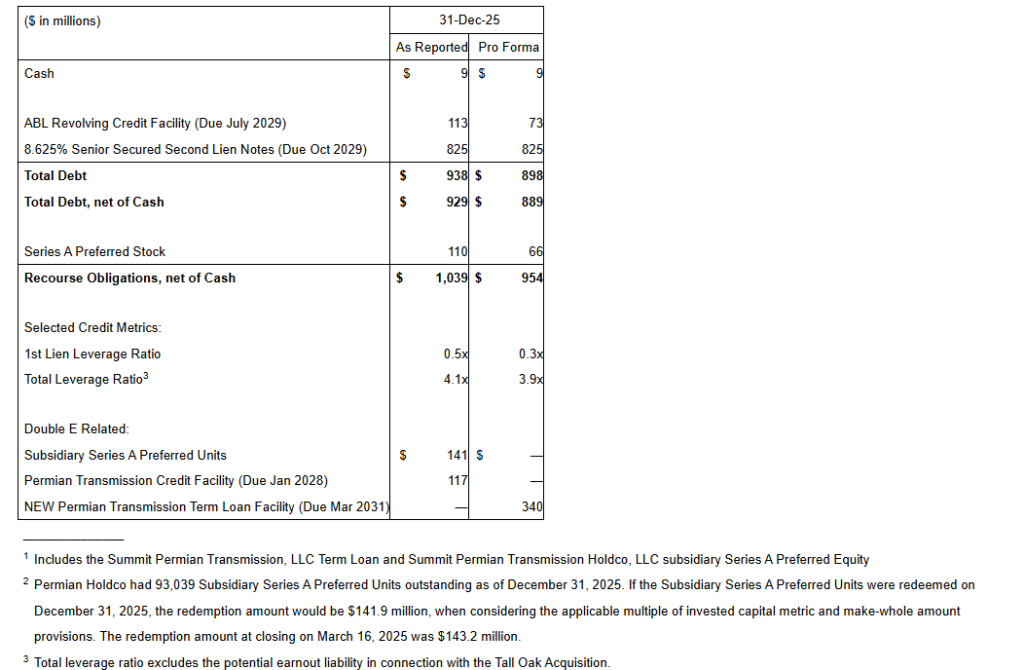

Subsequent to quarter-end, Summit refinanced the Summit Permian Transmission, LLC and Summit Permian Transmission Holdco, LLC capital structure with a new $440 million term loan facility, including a $340 million borrowing at closing, $50 million committed delayed draw facility used to fund the Producers Midstream and other expansion projects, as well as a $50 million uncommitted accordion to fund the expected mainline compression expansion project. Proceeds from the new facility were used to refinance the $112.7 million Summit Permian Transmission term loan, $141.9 million Summit Permian Transmission Holdco’s preferred units2, an $85 million one-time distribution to Summit, and pay other fees and expenses. Summit intends to use the $85 million one-time distribution to pay down approximately $45 million of accrued and unpaid dividends on its Series A Preferred Stock and approximately $40 million of ABL borrowings. Repayment of the accrued and unpaid dividends represents a critical step of Summit’s objective to resume dividend payments on its common stock once Summit achieves its long-term leverage target of 3.5x. In addition, the $40 million ABL repayment reduces Summit’s leverage by approximately 0.2x, aligning with its continued focus on corporate de-levering.

Pro Forma Capitalization

Williston Commercial Update

During the fourth quarter, Summit executed a new 10-year crude gathering agreement with a Bakken producer, anchored by a large Area of Dedication covering more than 200,000 acres across its existing footprint in Divide County, North Dakota. The first new pad — consisting of four 3-mile laterals — is expected to be turned in line in the first quarter of 2026. This agreement meaningfully expands Summit’s dedicated acreage and long-term economic inventory supporting its infrastructure, while positioning the Company to pursue additional development opportunities across northern Williams and southern Divide Counties. With the efficiency gains associated with 3-mile laterals, these areas have become economically attractive in the current oil price environment. As Bakken producers continue expanding activity in the northern and western portions of the basin, Summit expects increasing commercial momentum and growth around its Polar and Divide systems.

Fourth Quarter 2025 Business Highlights

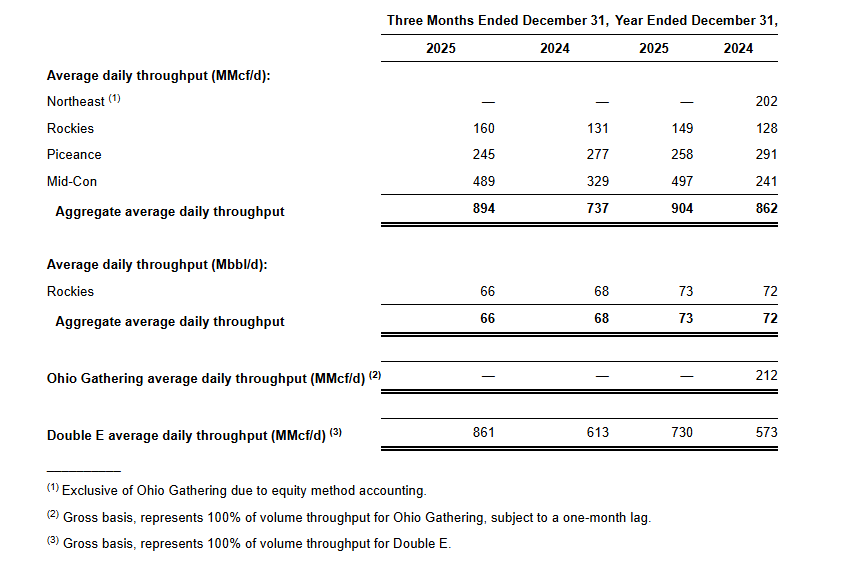

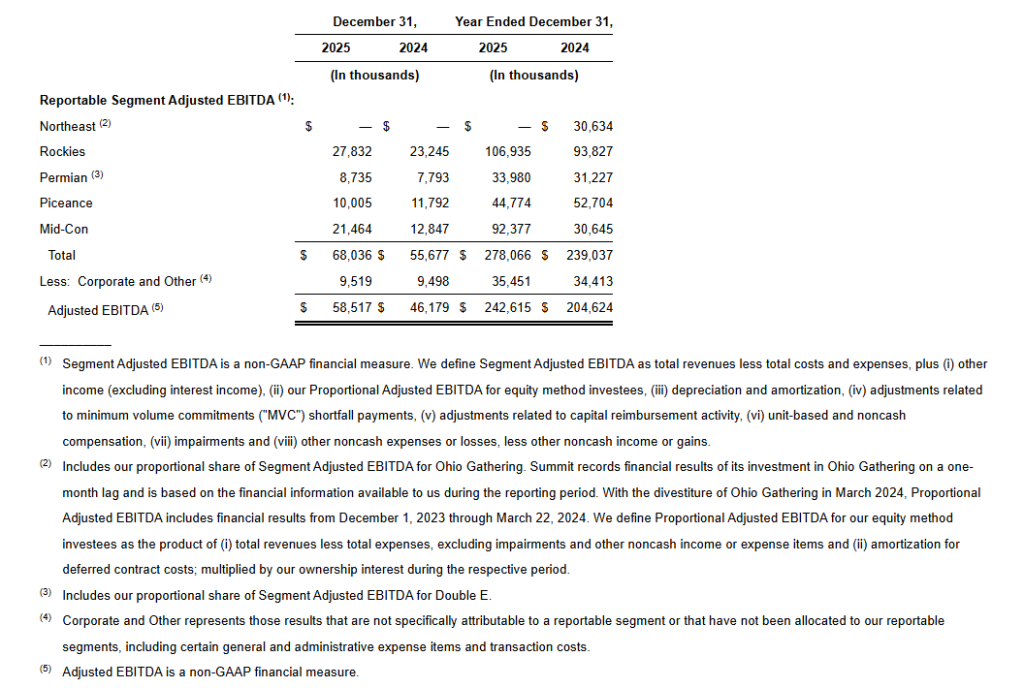

SMC’s average daily natural gas throughput on its wholly owned operated systems decreased 3.4% to 894 MMcf/d, while liquids volumes decreased 8.3% to 66 Mbbl/d, relative to the third quarter of 2025. Double E pipeline transported an average of 861 MMcf/d and contributed $8.7 million in Adjusted EBITDA, net to SMC, for the fourth quarter of 2025.

Natural gas price-driven segments:

Natural gas price-driven segments generated $31.5 million in combined Segment Adjusted EBITDA, a $4.6 million decrease relative to the third quarter and combined capital expenditures of $9.2 million.

Mid-Con Segment Adjusted EBITDA totaled $21.5 million, a decrease of $2.1 million relative to the third quarter of 2025, primarily due to a decrease in volume throughput on the system. Volume throughput on the system decreased by 3.7% primarily due to natural production declines partially offset by six new well connections in the Arkoma. Subsequent to quarter end, six new wells were connected in the Arkoma. There is currently one rig running in the Arkoma, with 21 DUCs behind the system, including 17 DUCs in the Barnett, which are all expected to come online in 2026.

Piceance Segment Adjusted EBITDA totaled $10.0 million, a decrease of $2.5 million relative to the third quarter of 2025, primarily due to realization of previously deferred revenue in the third quarter and a 5.4% decrease in volume throughput. There were no new wells connected to the system during the fourth quarter.

Oil price-driven segments:

Oil price-driven segments generated $36.6 million of combined Segment Adjusted EBITDA, representing a $1.1 million decrease relative to the third quarter of 2025, and had combined capital expenditures of $9.0 million.

Rockies Segment Adjusted EBITDA totaled $27.8 million, a decrease of $1.2 million relative to the third quarter of 2025, primarily driven by a 8.3% decrease in liquids volume throughput, partially offset by a 1.3% increase in natural gas volume throughput, relative to the third quarter of 2025. The decrease in liquids volumes was primarily driven by natural production declines and no new well connections in the Williston Basin during the quarter. Natural gas volume growth was supported by 33 new well connections in the DJ Basin, which are expected to reach peak production in the second quarter of 2026. There are currently six rigs running and approximately 65 DUCs behind the system.

Permian Segment Adjusted EBITDA totaled $8.8 million, an increase of $0.1 million relative to the third quarter of 2025, primarily due to a 20.9% increase in volumes shipped on the Double E Pipeline leading to an increase in proportionate Adjusted EBITDA from our Double E joint venture.

The following table presents average daily throughput by reportable segment for the periods indicated:

The following table presents Adjusted EBITDA by reportable segment for the periods indicated:

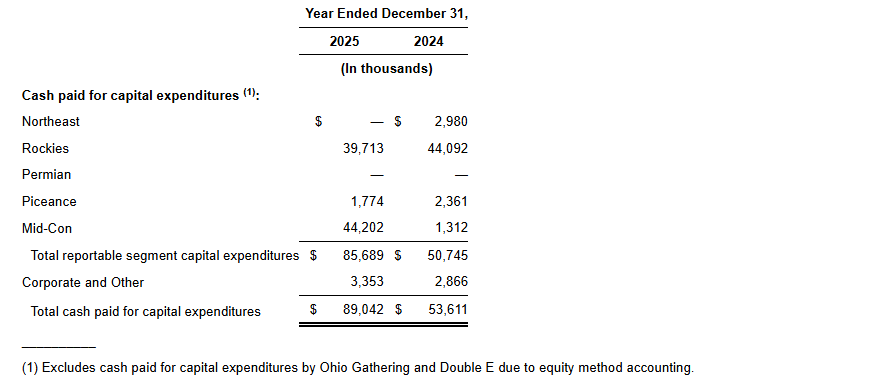

Capital Expenditures

Capital expenditures totaled $19.1 million in the fourth quarter of 2025, inclusive of maintenance capital expenditures of $4.0 million. Capital expenditures in the fourth quarter of 2025 were primarily related to pad connections in the Rockies and Mid-Con segments.

2026 Guidance

SMC is releasing guidance for 2026, which is summarized in the table below. These projections are subject to risks and uncertainties as described in the “Forward-Looking Statements” section at the end of this release.

SMC’s guidance range is anchored by recent drilling and completion schedules provided by its customers and is reflective of the current commodity price environment. The Company’s approach to its 2026 guidance is consistent with the framework used for its 2025 guidance range. If SMC’s producer customers hit their production targets and timing of planned well connects, the Company would expect to be near the high end of the 2026 guidance range. The midpoint of the guidance range reflects a conservative, yet appropriate, level of risking to the most recent drill schedules and volume forecasts provided by its customers. The low end of the guidance range reflects additional delays to customer drilling and completion schedules and planned well connects.

SMC expects approximately 116 to 126 well connections in 2026. Of the expected well connections in 2026, approximately 20% are natural gas-oriented wells and approximately 80% are crude oil-oriented wells. Customers are currently running seven rigs behind SMC systems, with approximately 90 DUCs, providing line of sight to the 2026 estimated well connections and associated volume growth.

SMC expects its natural gas gathering system throughput to range from 875 MMcf/d to 920 MMcf/d. Double E existing take-or-pay contracts of 1,115 MMcf/d is expected to increase to 1,285 MMcf/d when the Producers Midstream II and other projects are placed into service, as early as the fourth quarter of 2026. Liquids volumes are expected to range from 65 Mbbl/d to 90 Mbbl/d.

The guidance outlook also reflects a reduction in MVC shortfall payments in the Piceance from $16.9 million in 2025 to approximately $13.0 million in 2026, and excludes approximately $2 million of deferred revenue that benefited 2025 results.

The midpoint of the guidance range assumes strip commodity prices as of February 19, 2026, implying an average 2026 Henry Hub price of approximately $3.40 per MMBtu and WTI of approximately $64 per barrel.

Adjusted EBITDA is expected to range from $225 million to $265 million. SMC’s 2026 capital expenditure guidance of $50 million to $70 million, excluding Double E, includes capital reimbursements related to specific development projects with certain customers. The Company’s full year 2026 growth capex guidance range is primarily related to new pad connections in the Rockies and Mid-Con segments. Included in this range is approximately $15 million to $20 million of maintenance capex. Double E capital expenditures for 2026 are expected to be approximately $35 million, net to SMC, primarily related to a new plant connection and downstream connections associated with the recently announced shipper contracts.

Capital & Liquidity

As of December 31, 2025, SMC had $9.3 million in unrestricted cash on hand and $113 million drawn under its $500 million ABL Revolver with $386 million of borrowing availability, after accounting for $0.8 million of issued, but undrawn letters of credit. As of December 31, 2025, SMC’s gross availability based on the borrowing base calculation in the credit agreement was $810 million, which is $310 million greater than the $500 million of lender commitments to the ABL Revolver. As of December 31, 2025, SMC was in compliance with all financial covenants, including interest coverage of 2.7x relative to a minimum interest coverage covenant of 2.0x and first lien leverage ratio of 0.5x relative to a maximum first lien leverage ratio of 2.5x. As of December 31, 2025, SMC reported a total leverage ratio of approximately 4.1x, excluding the potential earnout liability in connection with the Tall Oak Acquisition.

As of January 2, 2026, the Permian Transmission Credit Facility balance was $112.7 million a reduction of $4.3 million relative to the September 30, 2025 balance of $117.0 million due to scheduled mandatory amortization. Summit Midstream Permian has $3.8 million of cash-on-hand as of January 2, 2026.