Results from two positive Phase 3 studies point to Tonmya’s (TNX-102 SL) potential as a new first-line medicine for chronic use in managing fibromyalgia, a debilitating condition suffered by 6-12 million adults in the U.S.

New Drug Application (NDA) submission to the FDA planned for second half of 2024 under the 505(b)(2) regulatory pathway

CHATHAM, N.J., Jan. 29, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a biopharmaceutical company with marketed products and a pipeline of development candidates, today announced that the U.S. Food and Drug Administration (FDA) has conditionally accepted the trade name, Tonmya™, for the Company’s drug product candidate TNX-102 SL for the management of fibromyalgia.

Tonmya is a patented sublingual tablet formulation of cyclobenzaprine hydrochloride developed for the management of fibromyalgia. In December 2023, the Company announced highly statistically significant and clinically meaningful topline results in RESILIENT, a second positive Phase 3 clinical trial of Tonmya for the management of fibromyalgia. In the study, Tonmya met its pre-specified primary endpoint, significantly reducing daily pain compared to placebo (p=0.00005) in participants with fibromyalgia. Statistically significant and clinically meaningful results were also seen in all key secondary endpoints related to improving sleep quality, reducing fatigue and improving overall fibromyalgia symptoms and function. RELIEF, the first positive Phase 3 trial of Tonmya in fibromyalgia, was completed in December 2020. It met its pre-specified primary endpoint of daily pain reduction compared to placebo (p=0.010) and showed activity in key secondary endpoints. Tonix plans to have a pre-NDA meeting with U.S. Food and Drug Administration (FDA) in the first half of 2024 and to submit a New Drug Application (NDA) to the FDA in the second half of 2024 for Tonmya for the management of fibromyalgia.

“We are very pleased with the FDA’s conditional acceptance of Tonmya as the brand name for TNX-102 SL,” said Seth Lederman, M.D., President and Chief Executive Officer of Tonix Pharmaceuticals. “With this acceptance, we remain excited for what we believe is an important opportunity to offer the first FDA-approved drug for fibromyalgia patients in more than a decade.”

About Tonmya™ (formerly known as TNX-102 SL)

Tonmya is a patented sublingual tablet formulation of cyclobenzaprine hydrochloride which is designed for daily administration at bedtime with a proposed mechanism of improving sleep quality in fibromyalgia. Tonmya provides rapid transmucosal absorption and reduced production of a long half-life active metabolite, norcyclobenzaprine, due to bypass of first-pass hepatic metabolism. As a multifunctional agent with potent binding and antagonist activities at the 5-HT2A-serotonergic, α1-adrenergic, H1-histaminergic, and M1-muscarinic cholinergic receptors, Tonmya is in development as a daily bedtime treatment for fibromyalgia, fibromyalgia-type Long COVID (formally known as post-acute sequelae of COVID-19 [PASC]), alcohol use disorder, and agitation in Alzheimer’s disease. The United States Patent and Trademark Office (USPTO) issued United States Patent No. 9636408 in May 2017, Patent No. 9956188 in May 2018, Patent No. 10117936 in November 2018, Patent No. 10,357,465 in July 2019, and Patent No. 10736859 in August 2020. The Protectic™ protective eutectic and Angstro-Technology™ formulation claimed in the patent are important elements of Tonix’s proprietary Tonmya composition. These patents are expected to provide Tonmya, upon NDA approval, with U.S. market exclusivity until 2034/2035. In addition, Tonix has pending but not issued U.S. patent applications directed to the transmucosal absorption of CBP-HCl, with U.S. market exclusivity expected until 2033, for treating depressive symptoms in fibromyalgia, with U.S. market exclusivity expected until 2032, and for treating pain in fibromyalgia with U.S. market exclusivity expected until 2041.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a biopharmaceutical company focused on commercializing, developing, discovering and licensing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s development portfolio is focused on central nervous system disorders. Tonix’s priority is to submit a New Drug Application (NDA) to the FDA for Tonmya, which has completed two positive Phase 3 studies for the management of fibromyalgia. Tonix intends to meet with the FDA in the first half of 2024 and submit an NDA for the approval of Tonmya for the management of fibromyalgia in the second half of 2024. TNX-102 SL is being developed to treat fibromyalgia-type Long COVID, a chronic post-acute COVID-19 condition, and topline results from a proof-of-concept study were reported in the third quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2024. Tonix’s rare disease development portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome (PWS). TNX-2900 has been granted Orphan Drug designation by the FDA and an investigational new drug (IND) application has been cleared to support a Phase 2 study in PWS patients. Tonix’s immunology development portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 was initiated in the third quarter of 2023. Tonix’s infectious disease pipeline includes TNX-801, a vaccine in development to prevent smallpox and mpox. TNX-801 also serves as the live virus vaccine platform or recombinant pox vaccine platform for other infectious diseases, including TNX-1800, in development as a vaccine to protect against COVID-19. During the fourth quarter of 2023, TNX-1800 was selected by the U.S. National Institutes of Health (NIH), National Institute of Allergy and Infectious Diseases (NIAID) Project NextGen for inclusion in Phase 1 clinical trials. The infectious disease development portfolio also includes TNX-3900 and TNX-4000, which are classes of broad-spectrum small molecule oral antivirals. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg under a transition services agreement with Upsher-Smith Laboratories, LLC from whom the products were acquired on June 30, 2023. Zembrace SymTouch and Tosymra are each indicated for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2022, as filed with the Securities and Exchange Commission (the “SEC”) on March 13, 2023, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

HOUSTON, Jan. 29, 2024 (GLOBE NEWSWIRE) — Orion Group Holdings, Inc. (NYSE: ORN) (the “Company”), a leading specialty construction company, today announced the rebranding of its subsidiary TAS Concrete Construction (“TAS”) as Orion. This move reflects the Company’s strategic initiative to integrate its different service offerings under one banner to leverage Orion’s brand reputation and to deliver greater value and seamless execution for its customers.

TAS Concrete Construction was acquired by Orion Group Holdings, Inc. in 2015 and has continued to operate under the TAS name until now. The Company’s concrete segment, formerly known as TAS, and its marine segment will now operate together under the Orion name providing its customers with a single source for specialty construction and engineering.

“By unifying under the Orion banner, we will have a more recognizable presence in the national market, enhancing our brand and market opportunities. This integration will unlock new potential for growth, foster collaboration across teams, and support our mission to deliver high-quality solutions with predictable excellence,” said Travis Boone, Chief Executive Officer of Orion Group Holdings, Inc.

Through the fourth quarter 2023 and January 2024, Orion was awarded $244.2 million in new contracts, including $38.7 million for a beach stabilization project in Texas and $24.1 million for dredging work in Louisiana.

About Orion Group Holdings, Inc.

Orion Group Holdings, Inc., a leading specialty construction company serving the infrastructure, industrial and building sectors, provides services both on and off the water in the continental United States, Alaska, Hawaii, Canada and the Caribbean Basin through its marine segment and its concrete segment. The Company’s marine segment provides construction and dredging services relating to marine transportation facility construction, marine pipeline construction, marine environmental structures, dredging of waterways, channels and ports, environmental dredging, design, and specialty services. Its concrete segment provides turnkey concrete construction services including place and finish, site prep, layout, forming, and rebar placement for large commercial, structural and other associated business areas. The Company is headquartered in Houston, Texas with regional offices strategically located across its operating areas. (oriongroupholdingsinc.com)

Forward-Looking Statements

The matters discussed in this press release may constitute or include projections or other forward-looking statements within the meaning of the “safe harbor” provisions of Section 27A of the Securities Exchange Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, of which provisions the Company is availing itself. Certain forward-looking statements can be identified by the use of forward-looking terminology, such as ‘believes’, ‘expects’, ‘may’, ‘will’, ‘could’, ‘should’, ‘seeks’, ‘approximately’, ‘intends’, ‘plans’, ‘estimates’, or ‘anticipates’, or the negative thereof or other comparable terminology, or by discussions of strategy, plans, objectives, intentions, estimates, forecasts, outlook, assumptions, or goals. In particular, statements regarding future operations or results, including those set forth in this press release, and any other statement, express or implied, concerning future operating results or the future generation of or ability to generate revenues, income, net income, gross profit, EBITDA, Adjusted EBITDA, Adjusted EBITDA margin, or cash flow, including to service debt, and including any estimates, forecasts or assumptions regarding future revenues or revenue growth, are forward-looking statements. Forward-looking statements also include project award announcements, estimated project start dates, anticipated revenues, and contract options which may or may not be awarded in the future. Forward-looking statements involve risks, including those associated with the Company’s fixed price contracts that impacts profits, unforeseen productivity delays that may alter the final profitability of the contract, cancellation of the contract by the customer for unforeseen reasons, delays or decreases in funding by the customer, levels and predictability of government funding or other governmental budgetary constraints, and any potential contract options which may or may not be awarded in the future, and are at the sole discretion of award by the customer. Past performance is not necessarily an indicator of future results. In light of these and other uncertainties, the inclusion of forward-looking statements in this press release should not be regarded as a representation by the Company that the Company’s plans, estimates, forecasts, goals, intentions, or objectives will be achieved or realized. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company assumes no obligation to update information contained in this press release whether as a result of new developments or otherwise, except as required by law.

Please refer to the Company’s 2022 Annual Report on Form 10-K, filed on March 16, 2023, which is available on its website at www.oriongroupholdingsinc.com or at the SEC’s website at www.sec.gov, for additional and more detailed discussion of risk factors that could cause actual results to differ materially from our current expectations, estimates or forecasts.

WillScot Mobile Mini Holdings Corp. announced Monday that it will acquire modular rental provider McGrath RentCorp in a $3.8 billion deal. The acquisition aims to solidify WillScot’s position as a leading provider of modular space and portable storage solutions across North America.

Under the terms of the agreement, McGrath shareholders will receive $123 per share, comprised of 60% cash and 40% WillScot stock. This reflects a 10.1% premium over McGrath’s share price as of January 26th. Once completed, McGrath shareholders will own approximately 12.6% of the combined company.

The deal comes as WillScot looks to expand its footprint and diversify its customer segments through McGrath’s complementary business. McGrath serves over 10,000 business customers with modular building leasing and sales solutions across the U.S.

According to WillScot CEO Brad Soultz, “The transaction will further accelerate our growth, with combined 2023 pro forma revenue of $3.2 billion and adjusted EBITDA of $1.4 billion, we will be on path to achieve a $700 million free cash flow run-rate twelve months after we close.”

WillScot expects to realize $50 million in run-rate cost synergies within two years following the close of the acquisition in Q2 2024. The company has a track record of successfully integrating past deals and meeting synergy targets.

The combined company will be able to cross-sell value-added products and services and roll out operations best practices across the broader customer base. It will also have increased scale and expanded infrastructure to accelerate organic growth strategies already in place.

Along with revenue and cost synergies, the deal provides WillScot with greater geographic diversification and depth in adjacent sectors like electronic test equipment rental through McGrath’s TRS-RenTelco business.

On the financial front, the combined company is projected to generate approximately $3.2 billion in revenue and $1.4 billion in adjusted EBITDA in 2023. It expects to produce around $700 million in free cash flow within twelve months after the merger is finalized.

To fund the cash component of the acquisition, WillScot has secured committed bridge financing of $1.75 billion, along with expanded capacity from its existing credit facilities. The company is committed to rapid deleveraging and plans to achieve a 3.0-3.5x net leverage ratio within a year post-close.

McGrath’s board has unanimously approved the transaction. With shareholder approval and regulator sign-off, the buyout is anticipated to close during Q2 2024. Until then, McGrath will operate as an independent, publicly traded company.

The acquisition is the latest in WillScot’s strategy to capitalize on demand growth for modular space and storage solutions. The company has acquired over 15 businesses since going public in 2017, including the transformative $1.2 billion merger with Mobile Mini in 2020.

For McGrath shareholders, the deal provides a significant premium and ongoing upside through ownership stake in WillScot. It also enables McGrath’s rental solutions to reach a wider audience through WillScot’s expansive branch network and customer base.

Clinical research company Science 37 announced Monday that it has entered into a definitive agreement to be acquired by telehealth provider eMed in a deal valued at approximately $38 million. Under the agreement, eMed will commence a tender offer to purchase all outstanding shares of Science 37 stock for $5.75 per share in cash, representing a 21.3% premium over Science 37’s share price last week.

The deal will allow eMed to leverage Science 37’s remote clinical trial capabilities and proprietary Metasite technology platform to expand patient access and accelerate enrollment for clinical studies. Science 37’s decentralized clinical trial model enables patients to participate from home via telehealth, rather than having to travel to physical trial sites.

This acquisition comes at a pivotal time, as the biotech industry embraces virtual and hybrid trial designs in the wake of the COVID-19 pandemic. Science 37 was an early pioneer in decentralized trials, giving the company a first-mover advantage. According to Science 37 CEO David Coman, “eMed provides the greatest value to our stockholders, customers, patients, and employees. Stockholders will receive a premium, trial sponsors will gain greater access to patients, faster enrollment, and confidence in the Company’s capital position.”

For eMed, the deal significantly expands its digital healthcare footprint, adding Science 37’s network of telehealth investigators, coordinators, and software platform to its existing suite of at-home diagnostics and virtual care services. eMed was an early mover as well, having developed the first at-home COVID-19 test kit in 2020. Since then, the company has expanded into at-home testing and treatment for flu, UTIs, and other conditions.

The combined resources of both companies will provide end-to-end support for decentralized clinical trials, from patient recruitment to at-home sample collection to telemedicine visits. This could be a game-changer in improving patient diversity in trials and enabling studies focused on rare diseases or targeted therapies.

According to Science 37’s latest financial update, the company expects approximately $58-59 million in revenue for 2023 and over $50 million in cash reserves as of December 31, 2023. The company projected 2023 revenue of $50-60 million.

Science 37’s board of directors unanimously approved the acquisition deal with eMed. Major Science 37 shareholders, including Redmile Group, LLC, have also agreed to tender their shares in support of the acquisition.

The deal is expected to close in Q1 2024, pending tender of a majority of outstanding Science 37 shares and satisfaction of other customary closing conditions. Once completed, Science 37 will become a privately held subsidiary of eMed.

This Science 37 acquisition comes on the heels of eMed’s parent company, Evernow Inc., raising $100 million in Series B funding last March. The current deal highlights continued investor appetite for telehealth and digital health companies that are expanding access to care.

The Science 37 and eMed deal also demonstrates the growing intersection between telehealth and clinical research. Other companies like Medable and Excelya are exploring how hybrid and decentralized trials can boost patient recruitment and retention. By meeting patients where they are, virtual trials enable more representative, diverse study populations.

While some industry experts say a hybrid approach will become the standard, decentralized trials are still a relatively new model. This acquisition provides eMed with a first-mover advantage, but expect other digital health companies to underscore their clinical trial offerings moving forward. In the meantime, all eyes will be on eMed and Science 37 as they pioneer the next generation of virtual clinical research.

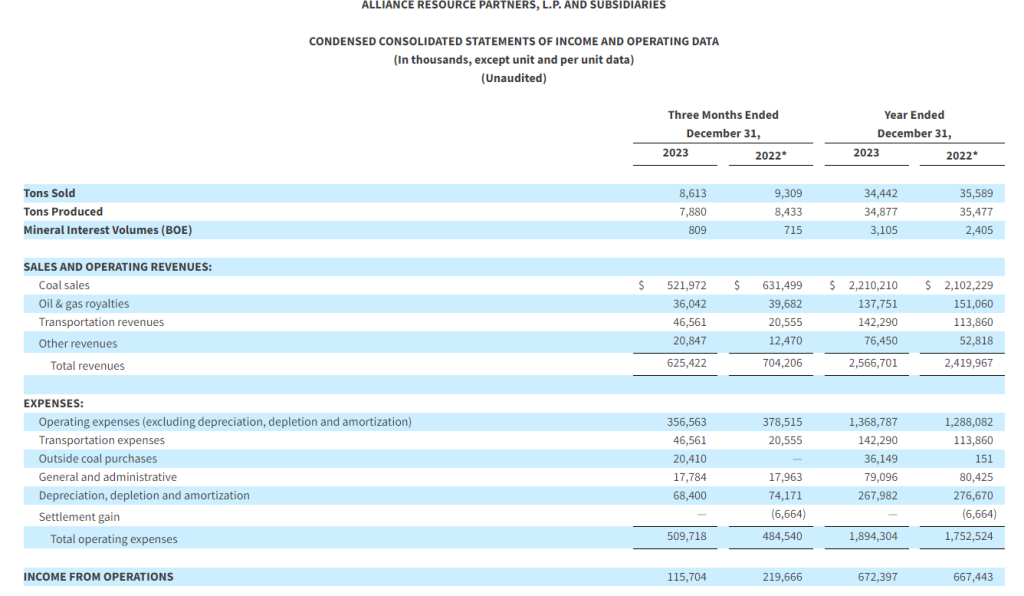

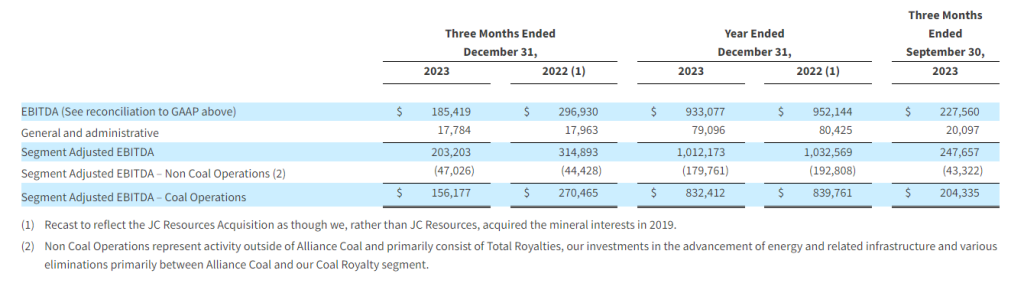

Record full year 2023 total revenue of $2.6 billion, coal sales price realizations of $64.17 per ton sold, and net income of $630.1 million

Full year 2023 EBITDA of $933.1 million

Fourth quarter 2023 total revenue of $625.4 million, EBITDA of $185.4 million, and net income of $115.4 million

Completed $24.8 million in oil & gas mineral interest acquisitions during fourth quarter 2023 and $110.9 million during full year 2023, resulting in record BOE volumes

Reduced debt by $22.9 million during fourth quarter 2023 and $85.0 million during full year 2023, resulting in total and net leverage ratios of 0.37 times and 0.31 times, respectively

In January 2024, declared quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized

2024 expected coal sales volumes over 90% committed and priced at levels similar to 2023

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter and full year ended December 31, 2023 (the “2023 Quarter” and “2023 Full Year”). This release includes comparisons of results to the quarter and year ended December 31, 2022 (the “2022 Quarter” and “2022 Full Year”, respectively), as well as the quarter ended September 30, 2023 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.

2023 Full Year performance saw total revenues increase $146.7 million to a record $2.6 billion primarily due to higher coal sales revenues. Coal sales prices and coal sales revenues during the 2023 Full Year were higher by 8.6% and 5.1%, respectively, compared to the 2022 Full Year. Increased revenues and lower income tax expense were partially offset by higher total operating expenses in the 2023 Full Year, resulting in record net income of $630.1 million, or $4.81 per basic and diluted limited partner unit, for the 2023 Full Year, compared to $586.2 million, or $4.39 per basic and diluted limited partner unit, for the 2022 Full Year, a 7.5% increase.

Total revenues in the 2023 Quarter decreased to $625.4 million compared to $704.2 million for the 2022 Quarter primarily as a result of lower coal and oil & gas prices and reduced coal sales volumes, partially offset by record oil & gas royalty volumes and higher transportation and other revenues. Lower revenues and higher total operating expenses reduced net income for the 2023 Quarter to $115.4 million, or $0.88 per basic and diluted limited partner unit, compared to $216.9 million, or $1.63 per basic and diluted limited partner unit, for the 2022 Quarter. EBITDA for the 2023 Quarter was $185.4 million compared to $296.9 million in the 2022 Quarter.

Compared to the Sequential Quarter, total revenues in the 2023 Quarter decreased 1.7% primarily as a result of lower average coal sales prices of $60.60 per ton sold compared to $64.94 per ton sold in the Sequential Quarter, partially offset by higher coal sales volumes, which increased 1.9% to 8.6 million tons sold in the 2023 Quarter. Lower revenues and higher total operating expenses contributed to a reduction in net income and EBITDA of 24.9% and 18.5%, respectively, compared to the Sequential Quarter.

CEO Commentary

“For the 2023 Full Year, we once again delivered record revenues and net income, relying upon the strength of our well-contracted coal order book and the resilience of the entire ARLP team who persevered through volatile market challenges and difficult mining conditions,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Our strategic relationships with our long-standing customers were evident in the 2023 Quarter as we contracted an additional 12.0 million tons for domestic deliveries over the 2024 through 2028 time period at attractive, escalating prices, bringing our committed and priced order book for 2024 to over 90% of expected shipments.”

Mr. Craft added, “We believe the worst of the adverse geological conditions, which delayed development of a new district at Mettiki, idling the longwall there for essentially the entire second half of the 2023 Full Year, are behind us. With the longwall at Mettiki resuming production in late December 2023, we are expecting production in the first quarter of 2024, for our Appalachia operations, to compare favorably to the first quarter of 2023.”

Mr. Craft concluded, “Our Oil & Gas Royalty business completed $24.8 million in oil & gas mineral interest acquisitions during the 2023 Quarter and $110.9 million for the 2023 Full Year, resulting in record BOE volumes. We plan to continue allocating capital to grow this business line in 2024. Combining the stability of our heavily contracted coal order book with continued growth in our Oil & Gas Royalty business, we are well-positioned for another record year of revenues in 2024.”

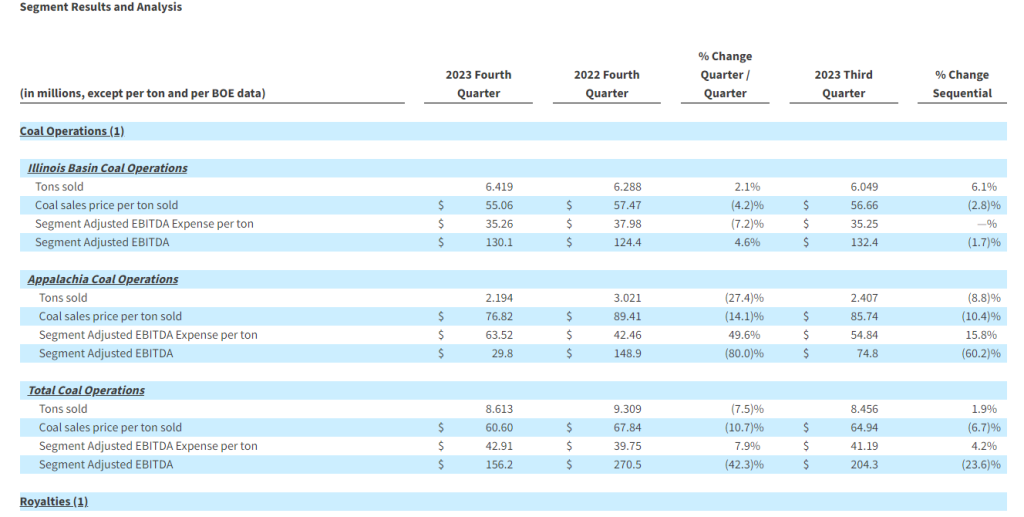

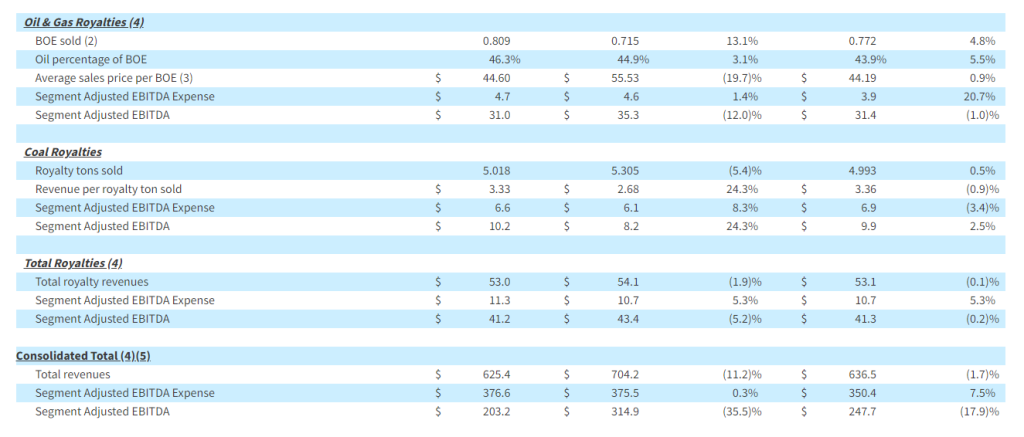

Coal Operations

ARLP’s coal sales prices per ton declined in both regions compared to the 2022 and Sequential Quarters. Lower export pricing in the Illinois Basin reduced coal sales prices by 4.2% in the region compared to the 2022 Quarter. Compared to the Sequential Quarter, Illinois Basin coal sales prices were lower by 2.8% as a result of reduced domestic price realizations. In Appalachia, coal sales price per ton decreased by 14.1% and 10.4% compared to the 2022 and Sequential Quarters, respectively, as a result of lower domestic pricing, partially offset by higher export price realizations. Illinois Basin coal sales volumes increased by 2.1% and 6.1% compared to the 2022 and Sequential Quarters, respectively, as a result of increased volumes from our Hamilton and Warrior mines compared to the 2022 Quarter and from our Gibson South operation sequentially. Tons sold decreased in Appalachia compared to the 2022 and Sequential Quarters due to reduced volumes across the region, primarily caused by lower recoveries, fewer operating units at MC Mining, the previously mentioned challenging geologic conditions that delayed development of a new district at our Mettiki longwall operation, customer plant maintenance and a longwall move at our Tunnel Ridge mine during the 2023 Quarter. ARLP ended the 2023 Quarter with total coal inventory of 1.3 million tons, representing an increase of 0.8 million tons compared to the end of the 2022 Quarter and a decrease of 0.5 million tons compared to the end of the Sequential Quarter. 2023 Quarter coal inventory and tons sold were negatively impacted by approximately 0.6 million tons due to an unexpected temporary outage at a Gulf Coast export terminal we use for export market sales.

Segment Adjusted EBITDA Expense per ton for the 2023 Quarter decreased by 7.2% in the Illinois Basin compared to the 2022 Quarter, due primarily to increased volumes and lower expenses at our Hamilton mine, that experienced an unexpected outage in the 2022 Quarter. Segment Adjusted EBITDA Expense per ton in Appalachia increased compared to the 2022 and Sequential Quarters due primarily to lower volumes as discussed above and purchased coal.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $31.0 million in the 2023 Quarter compared to $35.3 million and $31.4 million in the 2022 and Sequential Quarters, respectively. Compared to the 2022 Quarter, the decrease was due to lower price realizations, partially offset by record oil & gas volumes, which increased 13.1% to 809 MBOE sold in the 2023 Quarter. Higher volumes during the 2023 Quarter resulted from increased drilling and completion activities on our interests and acquisitions of additional oil & gas mineral interests.

Segment Adjusted EBITDA for the Coal Royalties segment increased to $10.2 million for the 2023 Quarter compared to $8.2 million and $9.9 million for the 2022 and Sequential Quarters, respectively. Compared to the 2022 Quarter, the increase resulted from higher average royalty rates per ton, partially offset by lower royalty tons sold and increased selling expenses. Sequentially, the increase in Segment Adjusted EBITDA for Coal Royalties primarily resulted from lower selling expenses.

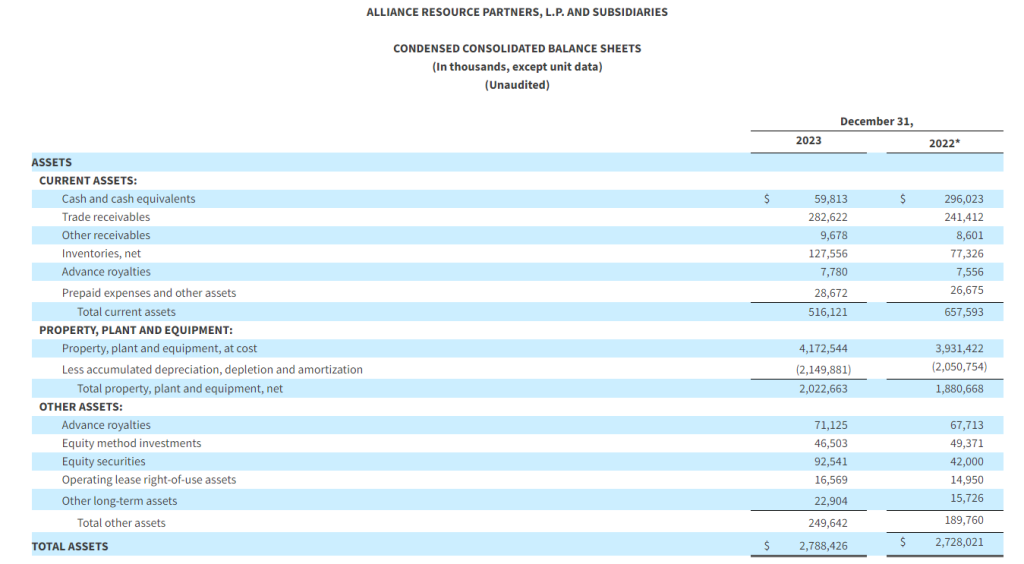

Balance Sheet and Liquidity

As of December 31, 2023, total debt and finance leases outstanding were $348.1 million, including $284.6 million in ARLP’s 2025 senior notes. During the 2023 Quarter, ARLP reduced its total debt and finance leases by $22.9 million. The Partnership’s total and net leverage ratios were 0.37 times and 0.31 times, respectively, as of December 31, 2023. ARLP ended the 2023 Quarter with total liquidity of $492.1 million, which included $59.8 million of cash and cash equivalents and $432.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

On January 26, 2024, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2023 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2024, to all unitholders of record as of the close of trading on February 7, 2024. The announced distribution is consistent with the cash distributions for the 2022 and Sequential Quarters.

Acquisition of Oil & Gas Mineral Interests

In December 2023, ARLP closed on an acquisition of mineral interests in approximately 2,372 oil & gas net royalty acres in the Anadarko, Williston and Delaware Basins for a purchase price of $14.5 million. During the 2023 Quarter, ARLP also separately purchased approximately 864 net royalty acres in the Permian Basin for $10.3 million.

Outlook

“As we look to 2024, our coal sales book is expected to be equally as strong as last year and be the anchor to deliver another record year of revenues,” commented Mr. Craft. “Our dependability and the reliability of our coal quality is highly valued by our customers, evidenced by the premium pricing we have received, relative to the spot market, on recent commitments with domestic customers for multi-year contracts. We are entering 2024 with over 90% of our coal sales volumes committed and priced at similar levels relative to 2023. We are expecting our production to be more consistent in 2024, believing we have moved beyond the several negative geological areas that we faced in 2023.”

“We expect to complete the major infrastructure projects at Tunnel Ridge, Hamilton, Warrior and the River View complex in 2024,” Mr. Craft continued. “ARLP will start to recognize the benefits from these strategic investments in 2025 as total capital expenditures will be significantly lower and these mines will be more productive, ensuring we maintain our position as one of the most reliable, low-cost producers in the eastern United States over the next decade. We are forecasting domestic natural gas prices to rise in 2025 as new LNG terminal capacity comes online, driving an increase in natural gas exports, benefitting both our Coal and Royalties segments.”

Mr. Craft added, “As we think about the outlook for the coal industry and the markets we serve, we should all take notice that grid planners have nearly doubled five-year load growth forecasts in support of ongoing investments in U.S. industrial and manufacturing sectors, as well as rising energy needs associated with datacenters and artificial intelligence. While the speed of electrifying the transportation sector may have slowed, the enthusiasm for AI has accelerated.”

Mr. Craft concluded, “We remain confident in our projections for sustained coal demand for ARLP and the likelihood that the pre-mature closures of coal-fired power plants in the eastern U.S. will be delayed.”

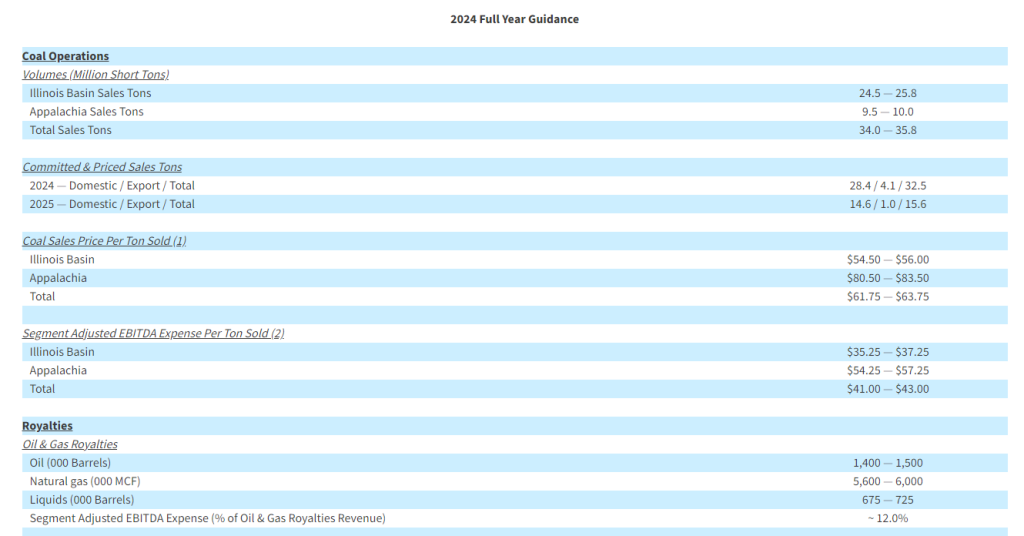

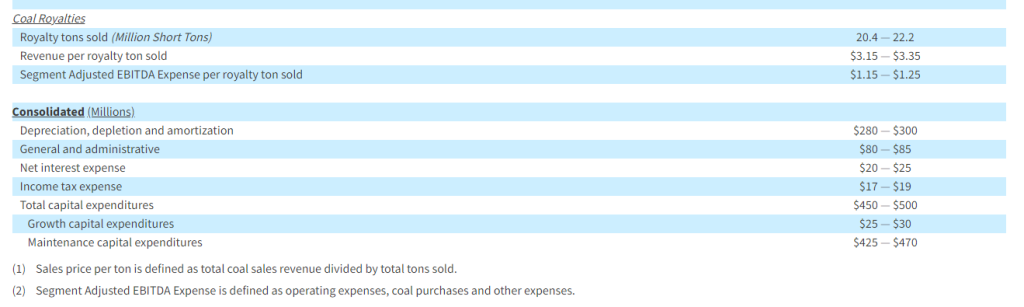

ARLP is providing the following updated guidance for the full year ended December 31, 2024 (the “2024 Full Year”):

Conference Call

A conference call regarding ARLP’s 2023 Quarter and Full Year financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13743714.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws; central bank policy actions including interest rates, bank failures and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2022, filed on February 24, 2023,and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2023, June 30, 2023 and September 30, 2023, filed on May 9, 2023, August 8, 2023 and November 8, 2023, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures

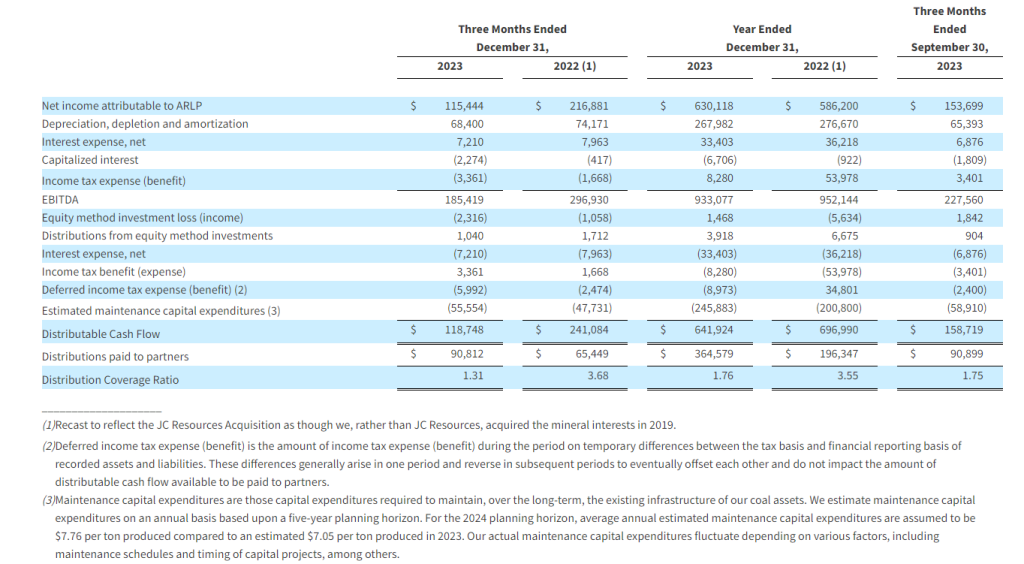

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding equity method investment earnings, interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures and adding distributions from equity method investments. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e., public reporting versus computation under financing agreements).

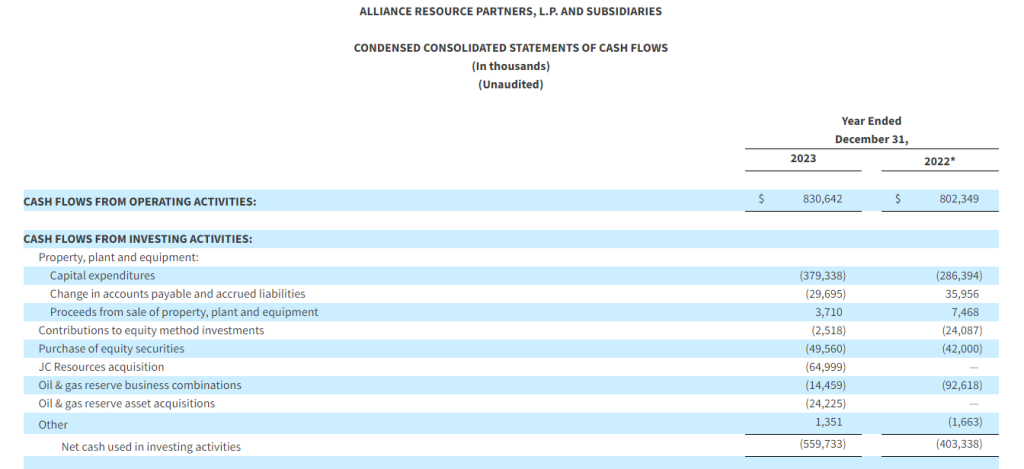

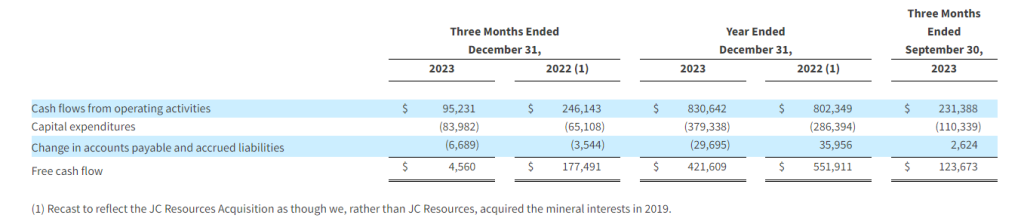

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property, plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

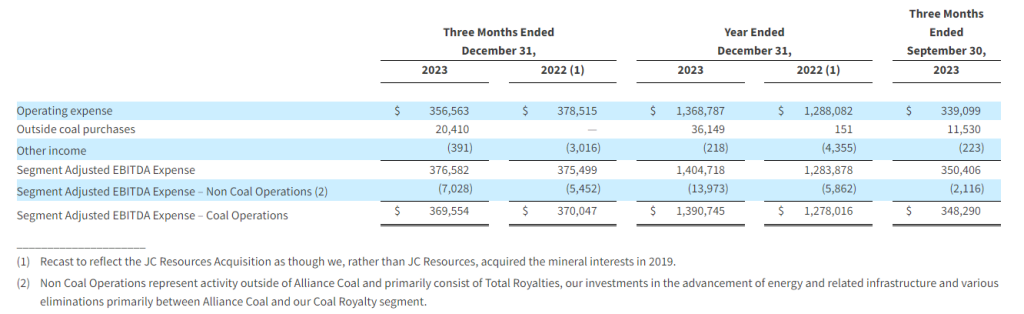

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases, if applicable, and other income or expense. Transportation expenses are excluded as these expenses are passed on to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations represents Segment Adjusted EBITDA Expense from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities.

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization and general and administrative expenses. Segment Adjusted EBITDA – Coal Operations represents Segment Adjusted EBITDA from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities and allows management to focus primarily on the operating performance of our Illinois Basin and Appalachia segments.

Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

ID/IQ Award. According to the daily Department of Defense contract award release, on Friday, Kratos Space & Missile Defense Systems Inc. was one of three firms awarded a multiple-award, indefinite-delivery/indefinite-quantity, cost-plus-incentive-fee, cost-plus-fixed-fee, and firm-fixed-price contract with a combined maximum ceiling of $877 million with a nine-year ordering period for Sounding Rocket Program-4.

Sounding Rocket. Sounding Rocket is a multiyear contract where companies compete for orders to launch small rockets used to carry scientific instruments and experiments into suborbital space. Started in 2018, the original awardees for the seven year $424 million ID/IQ were Northrop Grumman and Space Vector. With the three new awardees announced Friday, the program has been extended until 2029 and the total projected value increased to $877 million. SRP-4 is run by the Space Systems Command’s small rocket program office.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Addition Of Rodriguez Will Shift Representation Of Women On Board To 78%

FORT WAYNE, Ind., Jan. 26, 2024 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (the “Company”) today announced that Jessica Rodriguez, media business executive and former President of Entertainment and Chief Brand Officer for Univision Communications, Inc., has been elected to join its Board of Directors. With this appointment, representation of women on the Vera Bradley, Inc. Board of Directors will be 78%.

“Jessica Rodriguez brings a wealth of experience, supported by an exceptional record of driving innovation and executing future-focused, transformational strategies that deliver value and profitability in a rapidly changing business environment,” commented Jackie Ardrey, Chief Executive Officer of Vera Bradley, Inc. “Jessica’s unique perspective will be an excellent addition to the Vera Bradley, Inc. Board of Directors as we continue to focus on driving long-term, profitable growth for the Company and delivering value to our shareholders.”

Rodriguez is a visionary, results-driven leader and award-winning media business executive with a keen focus on creating, leading, and motivating high-performing, diverse, purpose-driven organizations. Rodriguez began her 20+ year career in media as Vice President and Station Manager for Univision Puerto Rico. From there, she successfully progressed through the organization in roles of increasing responsibility, including Vice President and Special Assistant to the President for Univision Networks, Inc.; Senior Vice President, Univision Cable Networks; Executive Vice President and Chief Marketing Officer, Univision; and Chief Operating Officer, Univision Networks. In 2018, Rodriguez was named President of Entertainment and Chief Brand Officer for Univision Communications, Inc., a post she held until 2022.

Rodriguez holds a bachelor’s degree in finance and economics from Fordham University and an MBA from the Stanford University Graduate School of Business. She currently serves as a member of the Burlington Stores, Inc. Board of Directors.

Rodriguez will join Vera Bradley Inc.’s eight other board members: Jackie Ardrey, CEO; Barbara Bradley Baekgaard, Co-Founder of Vera Bradley; Kristina Cashman, former Chief Financial Officer of P.F. Chang’s; Robert J. Hall, Chairman of the Vera Bradley Board of Directors and President of Green Gables Partners; Mary Lou Kelley, former President, E-Commerce for Best Buy; Frances P. Philip, Lead Independent Director of the Vera Bradley Board of Directors and former Chief Merchandising Officer of L.L. Bean, Inc.; Carrie Tharp, Vice President of Strategic Industries for Google Cloud; and recently appointed member Bradley Weston, former Chief Executive Officer of Party City Holdings, Inc.

About Vera Bradley, Inc. Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

The Company has three reportable segments: Vera Bradley Direct (“VB Direct”), Vera Bradley Indirect (“VB Indirect”), and Pura Vida. The VB Direct business consists of sales of Vera Bradley products through Vera Bradley Full-Line and Factory Outlet stores in the United States, www.verabradley.com, Vera Bradley’s online outlet site, and the Vera Bradley annual outlet sale in Fort Wayne, Indiana. The VB Indirect business consists of sales of Vera Bradley products to approximately 1,600 specialty retail locations throughout the United States, as well as select department stores, national accounts, third party e-commerce sites, and third-party inventory liquidators, and royalties recognized through licensing agreements related to the Vera Bradley brand. The Pura Vida segment consists of sales of Pura Vida products through the Pura Vida websites, www.puravidabracelets.com, www.puravidabracelets.ca, and www.puravidabracelets.eu; through the distribution of its products to wholesale retailers and department stores; and through its Pura Vida retail stores.

Vera Bradley Safe Harbor Statement Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 28, 2023. We undertake no obligation to publicly update or revise any forward-looking statement.

The latest inflation reading is providing critical evidence that the Federal Reserve’s interest rate hikes through 2023 have begun to achieve their intended effect of cooling down excessively high inflation. However, the timing of future Fed rate cuts remains up in the air despite growing optimism among investors.

On Friday, the Commerce Department reported that the Fed’s preferred inflation gauge, the core personal consumption expenditures (PCE) index, rose 2.9% in December from a year earlier. This marked the first time since March 2021 that core PCE dipped below 3%, a major milestone in the fight against inflation.

Even more encouraging is that on a 3-month annualized basis, core PCE hit 1.5%, dropping below the Fed’s 2% target for the first time since 2020. The deceleration of price increases across categories like housing, goods, and services indicates that tighter monetary policy has started rebalancing demand and supply.

As inflation falls from 40-year highs, pressure on the Fed to maintain its restrictive stance also eases. Markets now see the central bank initiating rate cuts at some point in 2024 to stave off excess weakness in the economy.

However, policymakers have been pushing back on expectations of cuts as early as March, emphasizing the need for more consistent data before declaring victory over inflation. Several have suggested rate reductions may not occur until the second half of 2024.

This caution stems from the still-hot economy, with Q4 2023 GDP growth hitting a better-than-expected 3.3% annualized. If consumer spending, business activity, and the job market stay resilient, the Fed may keep rates elevated through the spring or summer.

Still, traders are currently pricing in around a 50/50 chance of a small 0.25% rate cut by the May Fed meeting. Just a month ago, markets were far more confident in a March cut.

While the inflation data provides breathing room for the Fed to relax its hawkish stance, the timing of actual rate cuts depends on the path of the economy. An imminent recession could force quicker action to shore up growth.

Meanwhile, stock markets cheered the evidence of peaking inflation, sending the S&P 500 up 1.9% on Friday. Lower inflation paves the way for the Fed to stop raising rates, eliminating a major headwind for markets and risk assets like equities.

However, some analysts caution that celebratory stock rallies may be premature. Inflation remains well above the Fed’s comfort zone despite the recent progress. Corporate earnings growth is also expected to slow in 2024, especially if the economy cools faster than expected.

Markets are betting that Fed rate cuts can spur a “soft landing” where growth moderates but avoids recession. Yet predicting the economy’s path is highly challenging, especially when it has proven more resilient than anticipated so far.

If upcoming data on jobs, consumer spending, manufacturing, and GDP point to persistent economic strength, markets may have to readjust their optimistic outlook for both growth and Fed policy. A pause in further Fed tightening could be the best-case scenario for 2024.

While lower inflation indicates the Fed’s policies are working, determining the appropriate pace of reversing course will require delicate judgment. Moving too fast risks re-igniting inflation later on.

The détente between inflation and the Fed sets the stage for a pivotal 2024. With core PCE finally moving decisively in the right direction, Fed Chair Jerome Powell has some latitude to nurse the economy toward a soft landing. But stability hinges on inflation continuing to cool amid resilient growth and spending.

For investors, caution and flexibility will be key in navigating potentially increased market volatility around Fed policy. While lower inflation is unambiguously good news, its impact on growth, corporate profits, and asset prices may remain murky until more economic tea leaves emerge through the year.

Earnings Release Scheduled for Thursday, February 15, 2024 Before the Market Opens

Conference Call Scheduled for Thursday, February 15, 2024 at 11:00 AM (Eastern Time)

BOCA RATON, Fla.–(BUSINESS WIRE)–Jan. 25, 2024– The GEO Group, Inc. (NYSE:GEO) (“GEO”) will release its fourth quarter 2023 financial results on Thursday, February 15, 2024 before the market opens. GEO has scheduled a conference call and simultaneous webcast for 11:00 AM (Eastern Time) on Thursday, February 15, 2024.

Hosting the call for GEO will be George C. Zoley, Executive Chairman of the Board, Brian R. Evans, Chief Executive Officer, Shayn March, Acting Chief Financial Officer, Wayne Calabrese, President and Chief Operating Officer, and James Black, President, GEO Secure Services.

To participate in the teleconference, please contact one of the following numbers 5 minutes prior to the scheduled start time:

In addition, a live audio webcast of the conference call may be accessed on the Webcasts section of GEO’s investor relations home page at investors.geogroup.com. A webcast replay will remain available on the website for one year.

A telephonic replay will also be available through February 22, 2024. The replay numbers are 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The passcode for the telephonic replay is 5397718. If you have any questions, please contact GEO at 1-866-301-4436.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent drilling results. Labrador Gold released results from recent drilling targeting the Appleton Fault Zone. The drilling is part of the company’s 100,000-meter diamond drilling program at its 100%-owned Kingsway project. The most recent results are for holes drilled at Pristine, the northeast extension of Big Vein, initial holes at Knobby and Peter Easton, and the first hole in the recently identified HM occurrence.

A new discovery at HM. The HM occurrence was discovered by prospecting and is roughly 570 meters along strike to the southwest of Big Vein. Hole K-23-334 tested for gold mineralization at depth below the quartz vein at surface. The hole returned gold grading 0.87 grams of gold per tonne over 55.9 meters, including a zone with visible gold that graded 38.37 grams of gold per tonne over 0.8 meters. Hole K-23-334 is the only hole drilled into this occurrence to date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere Energy reported 2024-4Q production results. Hemisphere Energy reported production of 3,375 boe/d, a 16% increase over the same period in 2022 and an 11% increase over 2023-3Q results. Production for the most recent quarter surpassed the 3,325 boe/d rate we had been using in our models.

Management gives initial 2024 production, pricing, and cost guidance. Management gave initial 2024 production, cash flow and capital expenditure guidance. Guidance was largely in line with our expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Healthcare technology firm HEALWELL AI is starting 2024 off strong with the strategic acquisition of Intrahealth Systems, a global provider of electronic health record (EHR) software. This $24 million deal provides HEALWELL with a platform to showcase and scale up its impressive AI capabilities within the massive EHR solutions market.

For investors focused on healthcare tech and AI, this is an exciting play on some of the most promising trends reshaping the industry. As digital health and telemedicine expand rapidly, there is surging demand for next-gen EHR systems equipped with cutting-edge analytics and AI.

HEALWELL is aiming to be at the forefront of this movement by uniting its physician-designed AI with Intrahealth’s established EHR solutions and multi-national customer base.

With over 15,000 clinicians and millions of patients served across Canada, Australia, and New Zealand, Intrahealth boasts an impressive footprint and high-margin recurring revenue exceeding $12 million annually.

HEALWELL plans to turbocharge Intrahealth’s offerings by embedding its own AI-powered clinical decision support software. This technology has already demonstrated major promise in preventative care by enabling earlier disease detection and personalized interventions.

Integrating these AI capabilities into a widely adopted EHR platform like Intrahealth opens up tremendous possibilities to amplify outcomes and lower costs for healthcare providers globally. This direction aligns perfectly with growing adoption of value-based care models that prioritize proactive, tech-enabled, and patient-centric treatment.

For HEALWELL specifically, the benefits of acquiring Intrahealth extend well beyond the technology integration upside. This established player provides HEALWELL with a stable source of profitable SaaS revenue to complement its R&D pipeline. And Intrahealth’s international reach significantly expands HEALWELL’s total addressable market.

The deal also furthers HEALWELL’s broader acquisition-driven strategy focused on consolidating AI, data science, and digital health assets. Intrahealth delivers an ideal platform to demonstrate the power of HEALWELL’s innovations to a large audience of potential customers and partners.

With healthcare spending continuing to spiral globally, there is tremendous appetite for tools that can optimize care and reduce waste. This thematic tailwind, combined with Intrahealth’s impressive financials and HEALWELL’s tech prowess, makes the acquisition look like a savvy move.

The opportunity in AI-enhanced software platforms like EHR looks especially strong when considering the sheer size of the healthcare IT market. According to Grand View Research, this sector is projected to reach $230 billion by 2028, expanding at nearly 12% annually.

Within this landscape, EHR systems are a central focus, with MarketsandMarkets forecasting this specific niche to be worth $48 billion globally by 2027. First movers with differentiated offerings stand to grab significant market share as adoption of next-gen EHR accelerates.

By snapping up Intrahealth, HEALWELL is positioning itself as a frontrunner in this race to redefine the EHR status quo. Investors interested healthcare technology and AI should keep a close eye on how successfully HEALWELL leverages this strategic acquisition. The company’s progress integrating its robust AI into Intrahealth’s solutions will be an important proof point.

Overall, the Intrahealth deal provides HEALWELL with both an immediate boost in revenue and profitability, plus a long-term growth driver if the combined EHR/AI offering gains traction. This is exactly the sort of calculated, opportunistic move investors should want to see in an emerging healthcare technology leader like HEALWELL.

The New Year has kicked off with a bang in biotech, as CG Oncology has completed the first initial public offering in the space for 2024. The cancer-focused biotech raised a whopping $380 million in its IPO on the Nasdaq, sailing past its initial target range of $181 million.

CG Oncology priced its shares at $19 apiece, above the $16-18 range it had set ahead of the IPO. The impressive deal is being viewed by many analysts and investors as a positive indicator that the biotech IPO market is rebounding in 2024 after a relatively slow 2023.

The robust demand for CG Oncology stock reflects renewed optimism and openness to investing in early-stage biotech companies, especially those with innovative science and strong leadership teams.

CG Oncology is developing a novel oncolytic virus therapy known as cretostimogene grenadenorepvec for the treatment of non-muscle invasive bladder cancer. Oncolytic viruses represent an exciting new approach in cancer treatment, wherein specially engineered viruses are able to infect and destroy cancer cells directly while also stimulating anti-tumor immune responses.

Cretostimogene grenadenorepvec is an adenovirus that has been engineered to replicate selectively in bladder cancer cells and stimulate the immune system by expressing granulocyte-macrophage colony-stimulating factor (GM-CSF). Early stage clinical data have shown promising signs of efficacy.

The company plans to use the IPO proceeds to fund a Phase 3 clinical trial of its lead candidate as well as earlier stage pipeline programs. Success in the Phase 3 study could support regulatory approval and commercialization.

CG Oncology was founded in 2018 by a veteran team of biotech entrepreneurs and scientists. The company pursued a pre-IPO crossover financing round in 2022, enabling it to build momentum heading into its public debut.

The IPO success places CG Oncology in a strong position to advance its pipeline. With the influx of capital, the company will be able to aggressively pursue its clinical development plans without relying heavily on external partners.

Moreover, the validation and visibility provided by being a public company can potentially help CG Oncology forge productive collaborations and access additional funding in the future.

Looking ahead, the positive investor response to CG Oncology seems likely to pave the way for more biotech IPOs in 2024. A robust IPO market provides fuel for innovation and discoveries that can transform patient lives.

The biotech sector sputtered in 2022, with only around 20 IPOs completed versus more than 50 in 2021. However, sentiment appears to be shifting, perhaps signaling sunnier days ahead.

In addition to favorable market conditions, biotech companies pursuing IPOs seem to be taking valuable lessons from 2022 by tightening focus on fundamentals like drug efficacy and visibility on clinical milestones.

Other than CG Oncology, a host of biotechs have already filed with SEC intentions to go public in 2024, spanning exciting areas like gene therapy, neurology, and synthetic biology.

With fresh capital and investor enthusiasm, the next generation of biotech companies can pursue ambitious goals to develop innovative medicines. More early-stage companies may also gain the funding needed to initiate or advance clinical trials.

CG Oncology’s big IPO pop reflects the right combination of cutting-edge science, unmet medical need, and strong leadership. This formula will likely be replicated by other emerging biotech stars in the making.

In all, the successful CG Oncology IPO kicks off 2024 as a promising year for biotech funding, innovation, and progress against once intractable diseases. Investors and industry observers will be tracking the IPO market closely through the year for signs of sustained momentum. If the appetite for compelling biotech stories persists, it could drive a much-needed renaissance helping to unlock new medical frontiers.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available.