Clinical research company Science 37 announced Monday that it has entered into a definitive agreement to be acquired by telehealth provider eMed in a deal valued at approximately $38 million. Under the agreement, eMed will commence a tender offer to purchase all outstanding shares of Science 37 stock for $5.75 per share in cash, representing a 21.3% premium over Science 37’s share price last week.

The deal will allow eMed to leverage Science 37’s remote clinical trial capabilities and proprietary Metasite technology platform to expand patient access and accelerate enrollment for clinical studies. Science 37’s decentralized clinical trial model enables patients to participate from home via telehealth, rather than having to travel to physical trial sites.

This acquisition comes at a pivotal time, as the biotech industry embraces virtual and hybrid trial designs in the wake of the COVID-19 pandemic. Science 37 was an early pioneer in decentralized trials, giving the company a first-mover advantage. According to Science 37 CEO David Coman, “eMed provides the greatest value to our stockholders, customers, patients, and employees. Stockholders will receive a premium, trial sponsors will gain greater access to patients, faster enrollment, and confidence in the Company’s capital position.”

For eMed, the deal significantly expands its digital healthcare footprint, adding Science 37’s network of telehealth investigators, coordinators, and software platform to its existing suite of at-home diagnostics and virtual care services. eMed was an early mover as well, having developed the first at-home COVID-19 test kit in 2020. Since then, the company has expanded into at-home testing and treatment for flu, UTIs, and other conditions.

The combined resources of both companies will provide end-to-end support for decentralized clinical trials, from patient recruitment to at-home sample collection to telemedicine visits. This could be a game-changer in improving patient diversity in trials and enabling studies focused on rare diseases or targeted therapies.

According to Science 37’s latest financial update, the company expects approximately $58-59 million in revenue for 2023 and over $50 million in cash reserves as of December 31, 2023. The company projected 2023 revenue of $50-60 million.

Science 37’s board of directors unanimously approved the acquisition deal with eMed. Major Science 37 shareholders, including Redmile Group, LLC, have also agreed to tender their shares in support of the acquisition.

The deal is expected to close in Q1 2024, pending tender of a majority of outstanding Science 37 shares and satisfaction of other customary closing conditions. Once completed, Science 37 will become a privately held subsidiary of eMed.

This Science 37 acquisition comes on the heels of eMed’s parent company, Evernow Inc., raising $100 million in Series B funding last March. The current deal highlights continued investor appetite for telehealth and digital health companies that are expanding access to care.

The Science 37 and eMed deal also demonstrates the growing intersection between telehealth and clinical research. Other companies like Medable and Excelya are exploring how hybrid and decentralized trials can boost patient recruitment and retention. By meeting patients where they are, virtual trials enable more representative, diverse study populations.

While some industry experts say a hybrid approach will become the standard, decentralized trials are still a relatively new model. This acquisition provides eMed with a first-mover advantage, but expect other digital health companies to underscore their clinical trial offerings moving forward. In the meantime, all eyes will be on eMed and Science 37 as they pioneer the next generation of virtual clinical research.

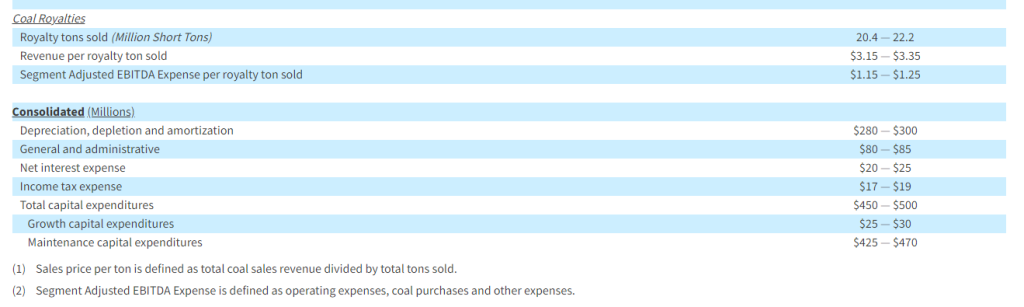

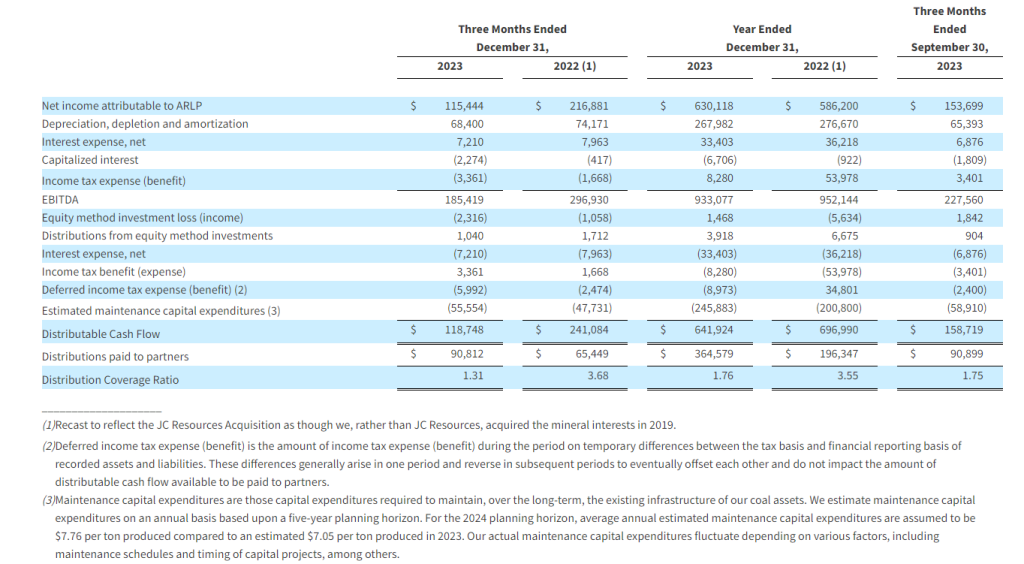

Record full year 2023 total revenue of $2.6 billion, coal sales price realizations of $64.17 per ton sold, and net income of $630.1 million

Full year 2023 EBITDA of $933.1 million

Fourth quarter 2023 total revenue of $625.4 million, EBITDA of $185.4 million, and net income of $115.4 million

Completed $24.8 million in oil & gas mineral interest acquisitions during fourth quarter 2023 and $110.9 million during full year 2023, resulting in record BOE volumes

Reduced debt by $22.9 million during fourth quarter 2023 and $85.0 million during full year 2023, resulting in total and net leverage ratios of 0.37 times and 0.31 times, respectively

In January 2024, declared quarterly cash distribution of $0.70 per unit, or $2.80 per unit annualized

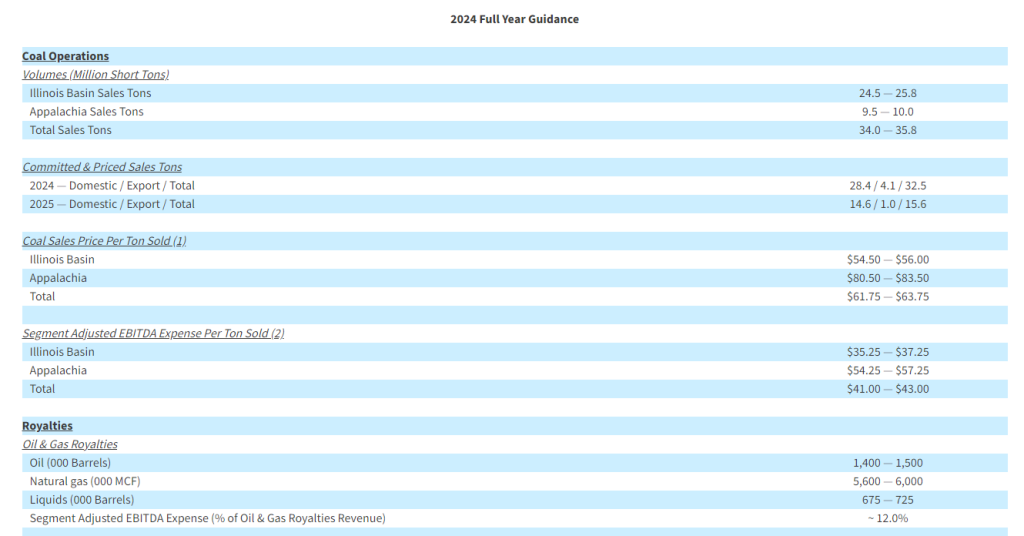

2024 expected coal sales volumes over 90% committed and priced at levels similar to 2023

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) (“ARLP” or the “Partnership”) today reported financial and operating results for the quarter and full year ended December 31, 2023 (the “2023 Quarter” and “2023 Full Year”). This release includes comparisons of results to the quarter and year ended December 31, 2022 (the “2022 Quarter” and “2022 Full Year”, respectively), as well as the quarter ended September 30, 2023 (the “Sequential Quarter”). All references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure, please see the end of this release.

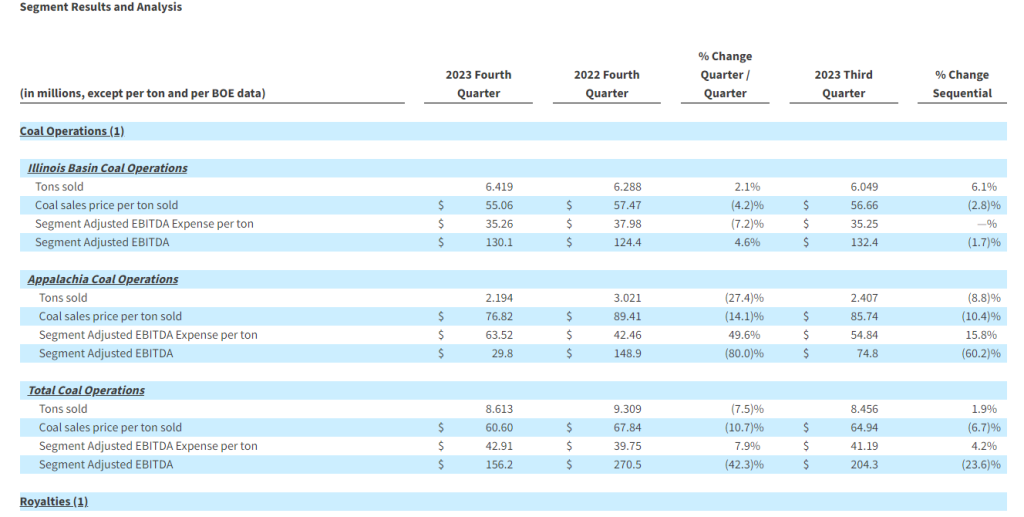

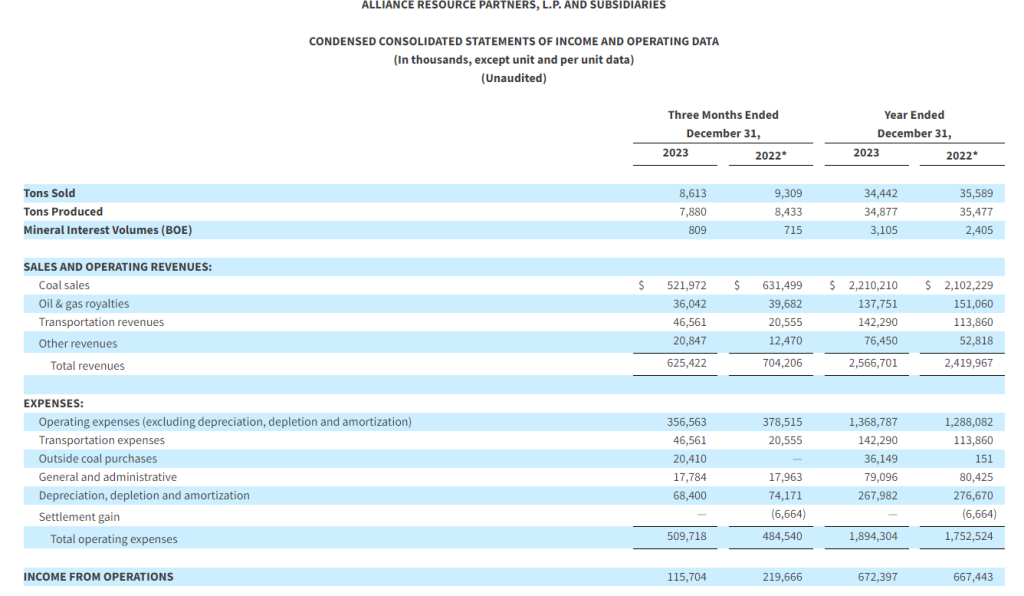

2023 Full Year performance saw total revenues increase $146.7 million to a record $2.6 billion primarily due to higher coal sales revenues. Coal sales prices and coal sales revenues during the 2023 Full Year were higher by 8.6% and 5.1%, respectively, compared to the 2022 Full Year. Increased revenues and lower income tax expense were partially offset by higher total operating expenses in the 2023 Full Year, resulting in record net income of $630.1 million, or $4.81 per basic and diluted limited partner unit, for the 2023 Full Year, compared to $586.2 million, or $4.39 per basic and diluted limited partner unit, for the 2022 Full Year, a 7.5% increase.

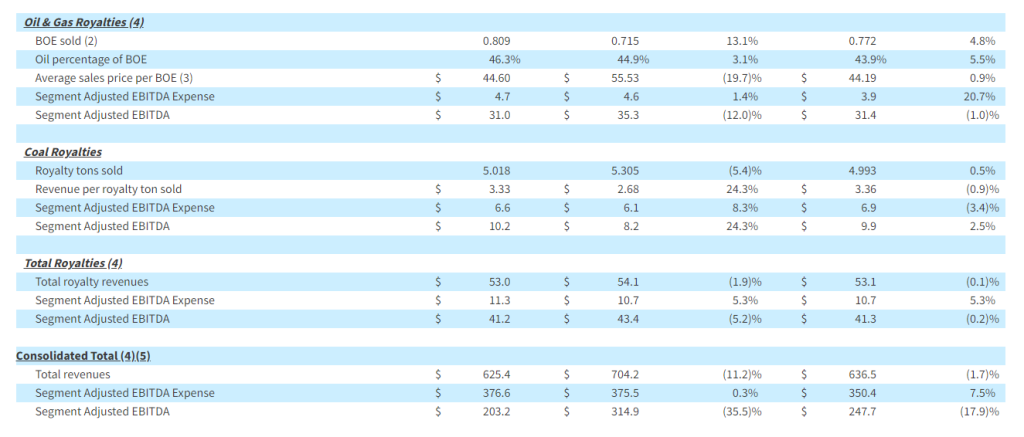

Total revenues in the 2023 Quarter decreased to $625.4 million compared to $704.2 million for the 2022 Quarter primarily as a result of lower coal and oil & gas prices and reduced coal sales volumes, partially offset by record oil & gas royalty volumes and higher transportation and other revenues. Lower revenues and higher total operating expenses reduced net income for the 2023 Quarter to $115.4 million, or $0.88 per basic and diluted limited partner unit, compared to $216.9 million, or $1.63 per basic and diluted limited partner unit, for the 2022 Quarter. EBITDA for the 2023 Quarter was $185.4 million compared to $296.9 million in the 2022 Quarter.

Compared to the Sequential Quarter, total revenues in the 2023 Quarter decreased 1.7% primarily as a result of lower average coal sales prices of $60.60 per ton sold compared to $64.94 per ton sold in the Sequential Quarter, partially offset by higher coal sales volumes, which increased 1.9% to 8.6 million tons sold in the 2023 Quarter. Lower revenues and higher total operating expenses contributed to a reduction in net income and EBITDA of 24.9% and 18.5%, respectively, compared to the Sequential Quarter.

CEO Commentary

“For the 2023 Full Year, we once again delivered record revenues and net income, relying upon the strength of our well-contracted coal order book and the resilience of the entire ARLP team who persevered through volatile market challenges and difficult mining conditions,” commented Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Our strategic relationships with our long-standing customers were evident in the 2023 Quarter as we contracted an additional 12.0 million tons for domestic deliveries over the 2024 through 2028 time period at attractive, escalating prices, bringing our committed and priced order book for 2024 to over 90% of expected shipments.”

Mr. Craft added, “We believe the worst of the adverse geological conditions, which delayed development of a new district at Mettiki, idling the longwall there for essentially the entire second half of the 2023 Full Year, are behind us. With the longwall at Mettiki resuming production in late December 2023, we are expecting production in the first quarter of 2024, for our Appalachia operations, to compare favorably to the first quarter of 2023.”

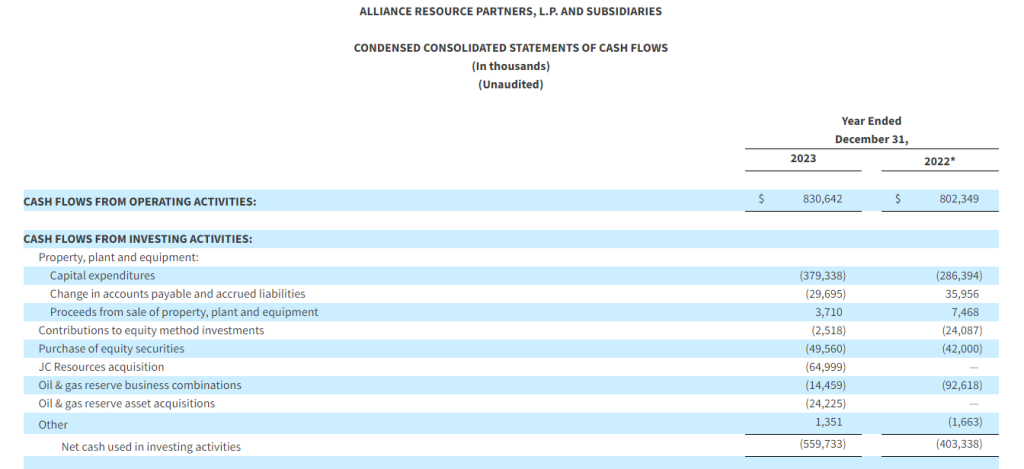

Mr. Craft concluded, “Our Oil & Gas Royalty business completed $24.8 million in oil & gas mineral interest acquisitions during the 2023 Quarter and $110.9 million for the 2023 Full Year, resulting in record BOE volumes. We plan to continue allocating capital to grow this business line in 2024. Combining the stability of our heavily contracted coal order book with continued growth in our Oil & Gas Royalty business, we are well-positioned for another record year of revenues in 2024.”

Coal Operations

ARLP’s coal sales prices per ton declined in both regions compared to the 2022 and Sequential Quarters. Lower export pricing in the Illinois Basin reduced coal sales prices by 4.2% in the region compared to the 2022 Quarter. Compared to the Sequential Quarter, Illinois Basin coal sales prices were lower by 2.8% as a result of reduced domestic price realizations. In Appalachia, coal sales price per ton decreased by 14.1% and 10.4% compared to the 2022 and Sequential Quarters, respectively, as a result of lower domestic pricing, partially offset by higher export price realizations. Illinois Basin coal sales volumes increased by 2.1% and 6.1% compared to the 2022 and Sequential Quarters, respectively, as a result of increased volumes from our Hamilton and Warrior mines compared to the 2022 Quarter and from our Gibson South operation sequentially. Tons sold decreased in Appalachia compared to the 2022 and Sequential Quarters due to reduced volumes across the region, primarily caused by lower recoveries, fewer operating units at MC Mining, the previously mentioned challenging geologic conditions that delayed development of a new district at our Mettiki longwall operation, customer plant maintenance and a longwall move at our Tunnel Ridge mine during the 2023 Quarter. ARLP ended the 2023 Quarter with total coal inventory of 1.3 million tons, representing an increase of 0.8 million tons compared to the end of the 2022 Quarter and a decrease of 0.5 million tons compared to the end of the Sequential Quarter. 2023 Quarter coal inventory and tons sold were negatively impacted by approximately 0.6 million tons due to an unexpected temporary outage at a Gulf Coast export terminal we use for export market sales.

Segment Adjusted EBITDA Expense per ton for the 2023 Quarter decreased by 7.2% in the Illinois Basin compared to the 2022 Quarter, due primarily to increased volumes and lower expenses at our Hamilton mine, that experienced an unexpected outage in the 2022 Quarter. Segment Adjusted EBITDA Expense per ton in Appalachia increased compared to the 2022 and Sequential Quarters due primarily to lower volumes as discussed above and purchased coal.

Royalties

Segment Adjusted EBITDA for the Oil & Gas Royalties segment decreased to $31.0 million in the 2023 Quarter compared to $35.3 million and $31.4 million in the 2022 and Sequential Quarters, respectively. Compared to the 2022 Quarter, the decrease was due to lower price realizations, partially offset by record oil & gas volumes, which increased 13.1% to 809 MBOE sold in the 2023 Quarter. Higher volumes during the 2023 Quarter resulted from increased drilling and completion activities on our interests and acquisitions of additional oil & gas mineral interests.

Segment Adjusted EBITDA for the Coal Royalties segment increased to $10.2 million for the 2023 Quarter compared to $8.2 million and $9.9 million for the 2022 and Sequential Quarters, respectively. Compared to the 2022 Quarter, the increase resulted from higher average royalty rates per ton, partially offset by lower royalty tons sold and increased selling expenses. Sequentially, the increase in Segment Adjusted EBITDA for Coal Royalties primarily resulted from lower selling expenses.

Balance Sheet and Liquidity

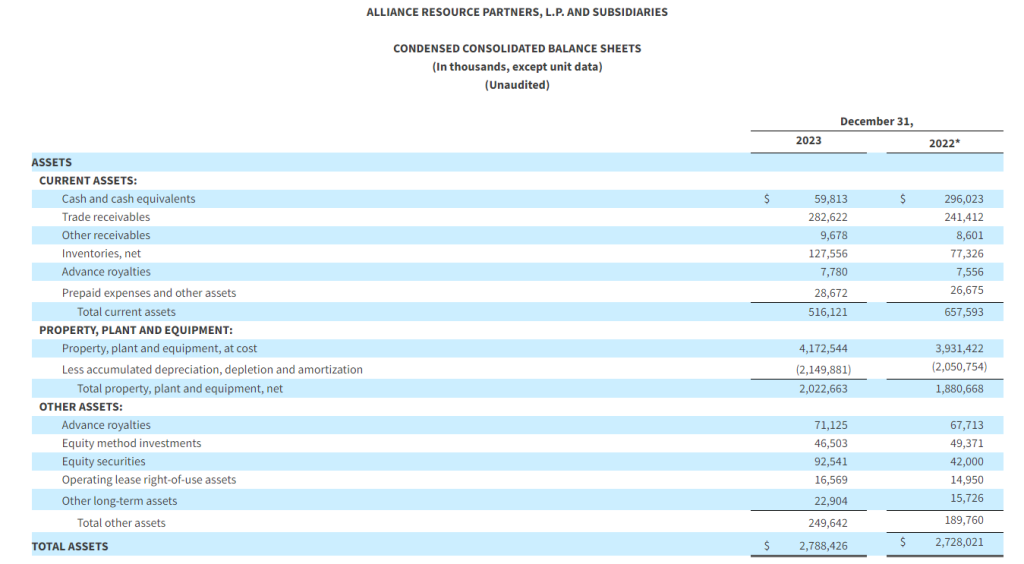

As of December 31, 2023, total debt and finance leases outstanding were $348.1 million, including $284.6 million in ARLP’s 2025 senior notes. During the 2023 Quarter, ARLP reduced its total debt and finance leases by $22.9 million. The Partnership’s total and net leverage ratios were 0.37 times and 0.31 times, respectively, as of December 31, 2023. ARLP ended the 2023 Quarter with total liquidity of $492.1 million, which included $59.8 million of cash and cash equivalents and $432.3 million of borrowings available under its revolving credit and accounts receivable securitization facilities.

Distributions

On January 26, 2024, the Board of Directors of ARLP’s general partner (the “Board”) approved a cash distribution to unitholders for the 2023 Quarter of $0.70 per unit (an annualized rate of $2.80 per unit), payable on February 14, 2024, to all unitholders of record as of the close of trading on February 7, 2024. The announced distribution is consistent with the cash distributions for the 2022 and Sequential Quarters.

Acquisition of Oil & Gas Mineral Interests

In December 2023, ARLP closed on an acquisition of mineral interests in approximately 2,372 oil & gas net royalty acres in the Anadarko, Williston and Delaware Basins for a purchase price of $14.5 million. During the 2023 Quarter, ARLP also separately purchased approximately 864 net royalty acres in the Permian Basin for $10.3 million.

Outlook

“As we look to 2024, our coal sales book is expected to be equally as strong as last year and be the anchor to deliver another record year of revenues,” commented Mr. Craft. “Our dependability and the reliability of our coal quality is highly valued by our customers, evidenced by the premium pricing we have received, relative to the spot market, on recent commitments with domestic customers for multi-year contracts. We are entering 2024 with over 90% of our coal sales volumes committed and priced at similar levels relative to 2023. We are expecting our production to be more consistent in 2024, believing we have moved beyond the several negative geological areas that we faced in 2023.”

“We expect to complete the major infrastructure projects at Tunnel Ridge, Hamilton, Warrior and the River View complex in 2024,” Mr. Craft continued. “ARLP will start to recognize the benefits from these strategic investments in 2025 as total capital expenditures will be significantly lower and these mines will be more productive, ensuring we maintain our position as one of the most reliable, low-cost producers in the eastern United States over the next decade. We are forecasting domestic natural gas prices to rise in 2025 as new LNG terminal capacity comes online, driving an increase in natural gas exports, benefitting both our Coal and Royalties segments.”

Mr. Craft added, “As we think about the outlook for the coal industry and the markets we serve, we should all take notice that grid planners have nearly doubled five-year load growth forecasts in support of ongoing investments in U.S. industrial and manufacturing sectors, as well as rising energy needs associated with datacenters and artificial intelligence. While the speed of electrifying the transportation sector may have slowed, the enthusiasm for AI has accelerated.”

Mr. Craft concluded, “We remain confident in our projections for sustained coal demand for ARLP and the likelihood that the pre-mature closures of coal-fired power plants in the eastern U.S. will be delayed.”

ARLP is providing the following updated guidance for the full year ended December 31, 2024 (the “2024 Full Year”):

Conference Call

A conference call regarding ARLP’s 2023 Quarter and Full Year financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “Investors” section of ARLP’s website at www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13743714.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States, supplying reliable, affordable energy domestically and internationally to major utilities, metallurgical and industrial users. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is evolving and positioning itself as a reliable energy partner for the future by pursuing opportunities that support the advancement of energy and related infrastructure.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7673 or via e-mail at investorrelations@arlp.com.

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, and our future repurchases of units and senior notes, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion, the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels and the planned retirement of coal-fired power plants in the U.S.; changes in macroeconomic and market conditions and market volatility, and the impact of such changes and volatility on our financial position; changes in global economic and geo-political conditions or changes in industries in which our customers operate; changes in commodity prices, demand and availability which could affect our operating results and cash flows; the outcome or escalation of current hostilities in Ukraine and the Israel-Gaza conflict; the severity, magnitude and duration of any future pandemics and impacts of such pandemics and of businesses’ and governments’ responses to such pandemics on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold oil & gas mineral interests due to low commodity prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions and to successfully integrate such acquisitions into our business and achieve the anticipated benefits therefrom; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws; central bank policy actions including interest rates, bank failures and associated liquidity risks; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social, and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortage of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these, and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2022, filed on February 24, 2023,and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2023, June 30, 2023 and September 30, 2023, filed on May 9, 2023, August 8, 2023 and November 8, 2023, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of Non-GAAP Financial Measures

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding equity method investment earnings, interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures and adding distributions from equity method investments. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e., public reporting versus computation under financing agreements).

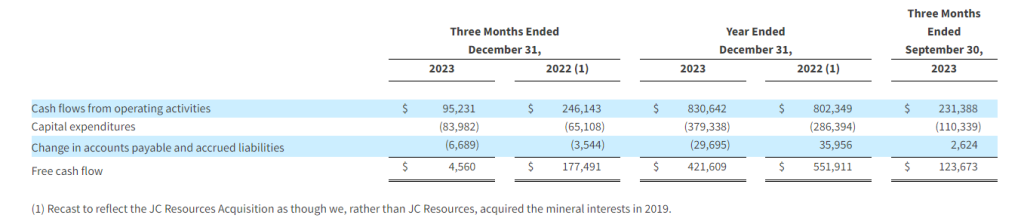

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property, plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

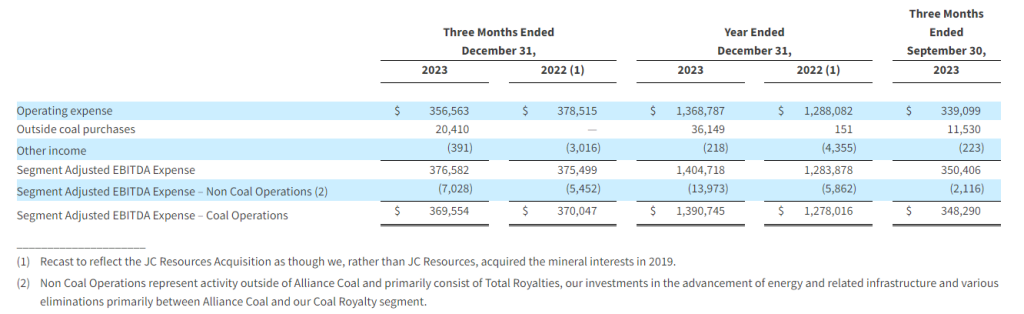

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases, if applicable, and other income or expense. Transportation expenses are excluded as these expenses are passed on to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations represents Segment Adjusted EBITDA Expense from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities.

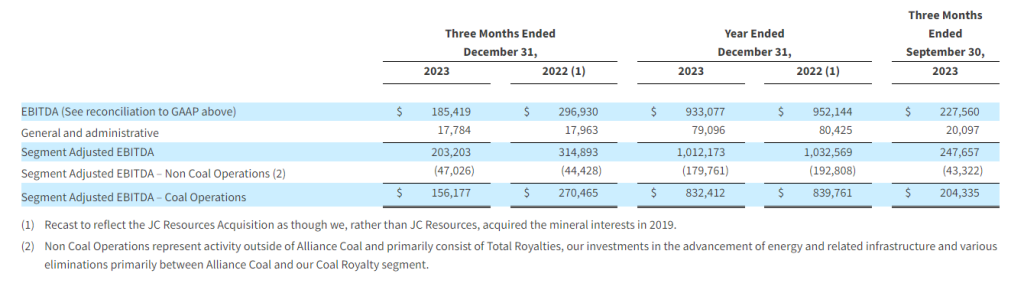

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization and general and administrative expenses. Segment Adjusted EBITDA – Coal Operations represents Segment Adjusted EBITDA from our wholly-owned subsidiary, Alliance Coal, which holds our coal mining operations and related support activities and allows management to focus primarily on the operating performance of our Illinois Basin and Appalachia segments.

Cary P. Marshall Senior Vice President and Chief Financial Officer 918-295-7673 investorrelations@arlp.com

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

ID/IQ Award. According to the daily Department of Defense contract award release, on Friday, Kratos Space & Missile Defense Systems Inc. was one of three firms awarded a multiple-award, indefinite-delivery/indefinite-quantity, cost-plus-incentive-fee, cost-plus-fixed-fee, and firm-fixed-price contract with a combined maximum ceiling of $877 million with a nine-year ordering period for Sounding Rocket Program-4.

Sounding Rocket. Sounding Rocket is a multiyear contract where companies compete for orders to launch small rockets used to carry scientific instruments and experiments into suborbital space. Started in 2018, the original awardees for the seven year $424 million ID/IQ were Northrop Grumman and Space Vector. With the three new awardees announced Friday, the program has been extended until 2029 and the total projected value increased to $877 million. SRP-4 is run by the Space Systems Command’s small rocket program office.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Addition Of Rodriguez Will Shift Representation Of Women On Board To 78%

FORT WAYNE, Ind., Jan. 26, 2024 (GLOBE NEWSWIRE) — Vera Bradley, Inc. (Nasdaq: VRA) (the “Company”) today announced that Jessica Rodriguez, media business executive and former President of Entertainment and Chief Brand Officer for Univision Communications, Inc., has been elected to join its Board of Directors. With this appointment, representation of women on the Vera Bradley, Inc. Board of Directors will be 78%.

“Jessica Rodriguez brings a wealth of experience, supported by an exceptional record of driving innovation and executing future-focused, transformational strategies that deliver value and profitability in a rapidly changing business environment,” commented Jackie Ardrey, Chief Executive Officer of Vera Bradley, Inc. “Jessica’s unique perspective will be an excellent addition to the Vera Bradley, Inc. Board of Directors as we continue to focus on driving long-term, profitable growth for the Company and delivering value to our shareholders.”

Rodriguez is a visionary, results-driven leader and award-winning media business executive with a keen focus on creating, leading, and motivating high-performing, diverse, purpose-driven organizations. Rodriguez began her 20+ year career in media as Vice President and Station Manager for Univision Puerto Rico. From there, she successfully progressed through the organization in roles of increasing responsibility, including Vice President and Special Assistant to the President for Univision Networks, Inc.; Senior Vice President, Univision Cable Networks; Executive Vice President and Chief Marketing Officer, Univision; and Chief Operating Officer, Univision Networks. In 2018, Rodriguez was named President of Entertainment and Chief Brand Officer for Univision Communications, Inc., a post she held until 2022.

Rodriguez holds a bachelor’s degree in finance and economics from Fordham University and an MBA from the Stanford University Graduate School of Business. She currently serves as a member of the Burlington Stores, Inc. Board of Directors.

Rodriguez will join Vera Bradley Inc.’s eight other board members: Jackie Ardrey, CEO; Barbara Bradley Baekgaard, Co-Founder of Vera Bradley; Kristina Cashman, former Chief Financial Officer of P.F. Chang’s; Robert J. Hall, Chairman of the Vera Bradley Board of Directors and President of Green Gables Partners; Mary Lou Kelley, former President, E-Commerce for Best Buy; Frances P. Philip, Lead Independent Director of the Vera Bradley Board of Directors and former Chief Merchandising Officer of L.L. Bean, Inc.; Carrie Tharp, Vice President of Strategic Industries for Google Cloud; and recently appointed member Bradley Weston, former Chief Executive Officer of Party City Holdings, Inc.

About Vera Bradley, Inc. Vera Bradley, Inc. operates two unique lifestyle brands – Vera Bradley and Pura Vida. Vera Bradley and Pura Vida are complementary businesses, both with devoted, emotionally-connected, and multi-generational female customer bases; alignment as casual, comfortable, affordable, and fun brands; positioning as “gifting” and socially-connected brands; strong, entrepreneurial cultures; a keen focus on community, charity, and social consciousness; multi-channel distribution strategies; and talented leadership teams aligned and committed to the long-term success of their brands.

Vera Bradley, based in Fort Wayne, Indiana, is a leading designer of women’s handbags, luggage and other travel items, fashion and home accessories, and unique gifts. Founded in 1982 by friends Barbara Bradley Baekgaard and Patricia R. Miller, the brand is known for its innovative designs, iconic patterns, and brilliant colors that inspire and connect women unlike any other brand in the global marketplace.

In July 2019, Vera Bradley, Inc. acquired a 75% interest in Creative Genius, Inc., which also operates under the name Pura Vida Bracelets (“Pura Vida”). Pura Vida, based in La Jolla, California, is a digitally native, highly-engaging lifestyle brand founded in 2010 by friends Paul Goodman and Griffin Thall. Pura Vida has a differentiated and expanding offering of bracelets, jewelry, and other lifestyle accessories. The Company acquired the remaining 25% of Pura Vida in January 2023.

The Company has three reportable segments: Vera Bradley Direct (“VB Direct”), Vera Bradley Indirect (“VB Indirect”), and Pura Vida. The VB Direct business consists of sales of Vera Bradley products through Vera Bradley Full-Line and Factory Outlet stores in the United States, www.verabradley.com, Vera Bradley’s online outlet site, and the Vera Bradley annual outlet sale in Fort Wayne, Indiana. The VB Indirect business consists of sales of Vera Bradley products to approximately 1,600 specialty retail locations throughout the United States, as well as select department stores, national accounts, third party e-commerce sites, and third-party inventory liquidators, and royalties recognized through licensing agreements related to the Vera Bradley brand. The Pura Vida segment consists of sales of Pura Vida products through the Pura Vida websites, www.puravidabracelets.com, www.puravidabracelets.ca, and www.puravidabracelets.eu; through the distribution of its products to wholesale retailers and department stores; and through its Pura Vida retail stores.

Vera Bradley Safe Harbor Statement Certain statements in this release are “forward-looking statements” made pursuant to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the Company’s current expectations or beliefs concerning future events and are subject to various risks and uncertainties that may cause actual results to differ materially from those that we expected, including: possible adverse changes in general economic conditions and their impact on consumer confidence and spending; possible inability to predict and respond in a timely manner to changes in consumer demand; possible loss of key management or design associates or inability to attract and retain the talent required for our business; possible inability to maintain and enhance our brands; possible inability to successfully implement the Company’s long-term strategic plans; possible inability to successfully open new stores, close targeted stores, and/or operate current stores as planned; incremental tariffs or adverse changes in the cost of raw materials and labor used to manufacture our products; possible adverse effects resulting from a significant disruption in our distribution facilities; or business disruption caused by pandemics. More information on potential factors that could affect the Company’s financial results is included from time to time in the “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections of the Company’s public reports filed with the SEC, including the Company’s Form 10-K for the fiscal year ended January 28, 2023. We undertake no obligation to publicly update or revise any forward-looking statement.

The latest inflation reading is providing critical evidence that the Federal Reserve’s interest rate hikes through 2023 have begun to achieve their intended effect of cooling down excessively high inflation. However, the timing of future Fed rate cuts remains up in the air despite growing optimism among investors.

On Friday, the Commerce Department reported that the Fed’s preferred inflation gauge, the core personal consumption expenditures (PCE) index, rose 2.9% in December from a year earlier. This marked the first time since March 2021 that core PCE dipped below 3%, a major milestone in the fight against inflation.

Even more encouraging is that on a 3-month annualized basis, core PCE hit 1.5%, dropping below the Fed’s 2% target for the first time since 2020. The deceleration of price increases across categories like housing, goods, and services indicates that tighter monetary policy has started rebalancing demand and supply.

As inflation falls from 40-year highs, pressure on the Fed to maintain its restrictive stance also eases. Markets now see the central bank initiating rate cuts at some point in 2024 to stave off excess weakness in the economy.

However, policymakers have been pushing back on expectations of cuts as early as March, emphasizing the need for more consistent data before declaring victory over inflation. Several have suggested rate reductions may not occur until the second half of 2024.

This caution stems from the still-hot economy, with Q4 2023 GDP growth hitting a better-than-expected 3.3% annualized. If consumer spending, business activity, and the job market stay resilient, the Fed may keep rates elevated through the spring or summer.

Still, traders are currently pricing in around a 50/50 chance of a small 0.25% rate cut by the May Fed meeting. Just a month ago, markets were far more confident in a March cut.

While the inflation data provides breathing room for the Fed to relax its hawkish stance, the timing of actual rate cuts depends on the path of the economy. An imminent recession could force quicker action to shore up growth.

Meanwhile, stock markets cheered the evidence of peaking inflation, sending the S&P 500 up 1.9% on Friday. Lower inflation paves the way for the Fed to stop raising rates, eliminating a major headwind for markets and risk assets like equities.

However, some analysts caution that celebratory stock rallies may be premature. Inflation remains well above the Fed’s comfort zone despite the recent progress. Corporate earnings growth is also expected to slow in 2024, especially if the economy cools faster than expected.

Markets are betting that Fed rate cuts can spur a “soft landing” where growth moderates but avoids recession. Yet predicting the economy’s path is highly challenging, especially when it has proven more resilient than anticipated so far.

If upcoming data on jobs, consumer spending, manufacturing, and GDP point to persistent economic strength, markets may have to readjust their optimistic outlook for both growth and Fed policy. A pause in further Fed tightening could be the best-case scenario for 2024.

While lower inflation indicates the Fed’s policies are working, determining the appropriate pace of reversing course will require delicate judgment. Moving too fast risks re-igniting inflation later on.

The détente between inflation and the Fed sets the stage for a pivotal 2024. With core PCE finally moving decisively in the right direction, Fed Chair Jerome Powell has some latitude to nurse the economy toward a soft landing. But stability hinges on inflation continuing to cool amid resilient growth and spending.

For investors, caution and flexibility will be key in navigating potentially increased market volatility around Fed policy. While lower inflation is unambiguously good news, its impact on growth, corporate profits, and asset prices may remain murky until more economic tea leaves emerge through the year.

Earnings Release Scheduled for Thursday, February 15, 2024 Before the Market Opens

Conference Call Scheduled for Thursday, February 15, 2024 at 11:00 AM (Eastern Time)

BOCA RATON, Fla.–(BUSINESS WIRE)–Jan. 25, 2024– The GEO Group, Inc. (NYSE:GEO) (“GEO”) will release its fourth quarter 2023 financial results on Thursday, February 15, 2024 before the market opens. GEO has scheduled a conference call and simultaneous webcast for 11:00 AM (Eastern Time) on Thursday, February 15, 2024.

Hosting the call for GEO will be George C. Zoley, Executive Chairman of the Board, Brian R. Evans, Chief Executive Officer, Shayn March, Acting Chief Financial Officer, Wayne Calabrese, President and Chief Operating Officer, and James Black, President, GEO Secure Services.

To participate in the teleconference, please contact one of the following numbers 5 minutes prior to the scheduled start time:

In addition, a live audio webcast of the conference call may be accessed on the Webcasts section of GEO’s investor relations home page at investors.geogroup.com. A webcast replay will remain available on the website for one year.

A telephonic replay will also be available through February 22, 2024. The replay numbers are 1-877-344-7529 (U.S.) and 1-412-317-0088 (International). The passcode for the telephonic replay is 5397718. If you have any questions, please contact GEO at 1-866-301-4436.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

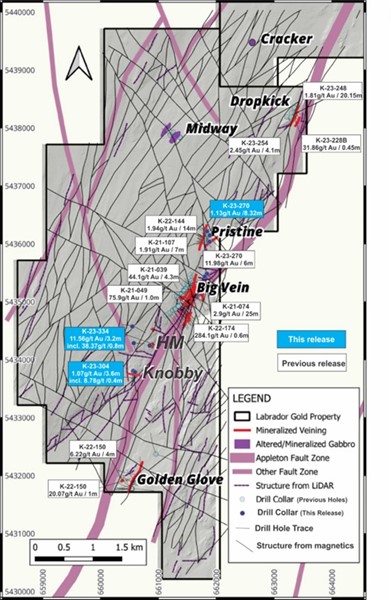

Recent drilling results. Labrador Gold released results from recent drilling targeting the Appleton Fault Zone. The drilling is part of the company’s 100,000-meter diamond drilling program at its 100%-owned Kingsway project. The most recent results are for holes drilled at Pristine, the northeast extension of Big Vein, initial holes at Knobby and Peter Easton, and the first hole in the recently identified HM occurrence.

A new discovery at HM. The HM occurrence was discovered by prospecting and is roughly 570 meters along strike to the southwest of Big Vein. Hole K-23-334 tested for gold mineralization at depth below the quartz vein at surface. The hole returned gold grading 0.87 grams of gold per tonne over 55.9 meters, including a zone with visible gold that graded 38.37 grams of gold per tonne over 0.8 meters. Hole K-23-334 is the only hole drilled into this occurrence to date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Hemisphere Energy reported 2024-4Q production results. Hemisphere Energy reported production of 3,375 boe/d, a 16% increase over the same period in 2022 and an 11% increase over 2023-3Q results. Production for the most recent quarter surpassed the 3,325 boe/d rate we had been using in our models.

Management gives initial 2024 production, pricing, and cost guidance. Management gave initial 2024 production, cash flow and capital expenditure guidance. Guidance was largely in line with our expectations.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Healthcare technology firm HEALWELL AI is starting 2024 off strong with the strategic acquisition of Intrahealth Systems, a global provider of electronic health record (EHR) software. This $24 million deal provides HEALWELL with a platform to showcase and scale up its impressive AI capabilities within the massive EHR solutions market.

For investors focused on healthcare tech and AI, this is an exciting play on some of the most promising trends reshaping the industry. As digital health and telemedicine expand rapidly, there is surging demand for next-gen EHR systems equipped with cutting-edge analytics and AI.

HEALWELL is aiming to be at the forefront of this movement by uniting its physician-designed AI with Intrahealth’s established EHR solutions and multi-national customer base.

With over 15,000 clinicians and millions of patients served across Canada, Australia, and New Zealand, Intrahealth boasts an impressive footprint and high-margin recurring revenue exceeding $12 million annually.

HEALWELL plans to turbocharge Intrahealth’s offerings by embedding its own AI-powered clinical decision support software. This technology has already demonstrated major promise in preventative care by enabling earlier disease detection and personalized interventions.

Integrating these AI capabilities into a widely adopted EHR platform like Intrahealth opens up tremendous possibilities to amplify outcomes and lower costs for healthcare providers globally. This direction aligns perfectly with growing adoption of value-based care models that prioritize proactive, tech-enabled, and patient-centric treatment.

For HEALWELL specifically, the benefits of acquiring Intrahealth extend well beyond the technology integration upside. This established player provides HEALWELL with a stable source of profitable SaaS revenue to complement its R&D pipeline. And Intrahealth’s international reach significantly expands HEALWELL’s total addressable market.

The deal also furthers HEALWELL’s broader acquisition-driven strategy focused on consolidating AI, data science, and digital health assets. Intrahealth delivers an ideal platform to demonstrate the power of HEALWELL’s innovations to a large audience of potential customers and partners.

With healthcare spending continuing to spiral globally, there is tremendous appetite for tools that can optimize care and reduce waste. This thematic tailwind, combined with Intrahealth’s impressive financials and HEALWELL’s tech prowess, makes the acquisition look like a savvy move.

The opportunity in AI-enhanced software platforms like EHR looks especially strong when considering the sheer size of the healthcare IT market. According to Grand View Research, this sector is projected to reach $230 billion by 2028, expanding at nearly 12% annually.

Within this landscape, EHR systems are a central focus, with MarketsandMarkets forecasting this specific niche to be worth $48 billion globally by 2027. First movers with differentiated offerings stand to grab significant market share as adoption of next-gen EHR accelerates.

By snapping up Intrahealth, HEALWELL is positioning itself as a frontrunner in this race to redefine the EHR status quo. Investors interested healthcare technology and AI should keep a close eye on how successfully HEALWELL leverages this strategic acquisition. The company’s progress integrating its robust AI into Intrahealth’s solutions will be an important proof point.

Overall, the Intrahealth deal provides HEALWELL with both an immediate boost in revenue and profitability, plus a long-term growth driver if the combined EHR/AI offering gains traction. This is exactly the sort of calculated, opportunistic move investors should want to see in an emerging healthcare technology leader like HEALWELL.

The New Year has kicked off with a bang in biotech, as CG Oncology has completed the first initial public offering in the space for 2024. The cancer-focused biotech raised a whopping $380 million in its IPO on the Nasdaq, sailing past its initial target range of $181 million.

CG Oncology priced its shares at $19 apiece, above the $16-18 range it had set ahead of the IPO. The impressive deal is being viewed by many analysts and investors as a positive indicator that the biotech IPO market is rebounding in 2024 after a relatively slow 2023.

The robust demand for CG Oncology stock reflects renewed optimism and openness to investing in early-stage biotech companies, especially those with innovative science and strong leadership teams.

CG Oncology is developing a novel oncolytic virus therapy known as cretostimogene grenadenorepvec for the treatment of non-muscle invasive bladder cancer. Oncolytic viruses represent an exciting new approach in cancer treatment, wherein specially engineered viruses are able to infect and destroy cancer cells directly while also stimulating anti-tumor immune responses.

Cretostimogene grenadenorepvec is an adenovirus that has been engineered to replicate selectively in bladder cancer cells and stimulate the immune system by expressing granulocyte-macrophage colony-stimulating factor (GM-CSF). Early stage clinical data have shown promising signs of efficacy.

The company plans to use the IPO proceeds to fund a Phase 3 clinical trial of its lead candidate as well as earlier stage pipeline programs. Success in the Phase 3 study could support regulatory approval and commercialization.

CG Oncology was founded in 2018 by a veteran team of biotech entrepreneurs and scientists. The company pursued a pre-IPO crossover financing round in 2022, enabling it to build momentum heading into its public debut.

The IPO success places CG Oncology in a strong position to advance its pipeline. With the influx of capital, the company will be able to aggressively pursue its clinical development plans without relying heavily on external partners.

Moreover, the validation and visibility provided by being a public company can potentially help CG Oncology forge productive collaborations and access additional funding in the future.

Looking ahead, the positive investor response to CG Oncology seems likely to pave the way for more biotech IPOs in 2024. A robust IPO market provides fuel for innovation and discoveries that can transform patient lives.

The biotech sector sputtered in 2022, with only around 20 IPOs completed versus more than 50 in 2021. However, sentiment appears to be shifting, perhaps signaling sunnier days ahead.

In addition to favorable market conditions, biotech companies pursuing IPOs seem to be taking valuable lessons from 2022 by tightening focus on fundamentals like drug efficacy and visibility on clinical milestones.

Other than CG Oncology, a host of biotechs have already filed with SEC intentions to go public in 2024, spanning exciting areas like gene therapy, neurology, and synthetic biology.

With fresh capital and investor enthusiasm, the next generation of biotech companies can pursue ambitious goals to develop innovative medicines. More early-stage companies may also gain the funding needed to initiate or advance clinical trials.

CG Oncology’s big IPO pop reflects the right combination of cutting-edge science, unmet medical need, and strong leadership. This formula will likely be replicated by other emerging biotech stars in the making.

In all, the successful CG Oncology IPO kicks off 2024 as a promising year for biotech funding, innovation, and progress against once intractable diseases. Investors and industry observers will be tracking the IPO market closely through the year for signs of sustained momentum. If the appetite for compelling biotech stories persists, it could drive a much-needed renaissance helping to unlock new medical frontiers.

Mark your calendars! Don’t miss Noble Capital Markets’ Emerging Growth Virtual Healthcare Equity Conference April 17-18. This exclusive virtual event connects investors with 50 leading public biotech, healthcare services, and medical device companies. Presenting company slots are available.

ORME was created to reward customers for interacting with brands and retailers

NEW YORK, Jan. 24, 2024 (GLOBE NEWSWIRE) — Xcel Brands, Inc. (NASDAQ: XELB) (“Xcel” or the “Company”), a media and consumer products company with expertise in livestream shopping and social commerce, today announced its 30% investment in ORME, a groundbreaking short-form video (SFV) marketplace designed to revolutionize social commerce.

“ORME is an opportunity with unicorn potential,” said Robert W. D’Loren, Chairman and Chief Executive Officer of Xcel. “ORME is redefining how consumers interact with brands and products, creating a seamless and engaging shopping experience that provides a nearly infinite return on ad spend for brands and gives all shoppers an opportunity to participate in the retail commerce flywheel.”

Faisal Ahmed, CEO of ORME, Inc., highlighted, “ORME is more than a marketplace; it is a community where social sharing and referral incentives include and reward shoppers and influencers. This feature not only amplifies brand content but also offers fee earning potential through referrals, leveraging the power of social networks and word-of-mouth marketing.”

ORME is set to transform the retail model from a one-to-many to a many-to-many experience. Combining the best aspects of affiliate, influencer, and digital marketing into a performance-based model, ORME presents a whole new experience for shoppers, influencers, brands, and retailers.

For shoppers and influencers, ORME creates a unique environment where they can create fun content, tell inspiring stories, learn from authentic people, explore an array of products in fashion, beauty, home, pet, and wellness sectors, and even earn performance-based cash fees for sharing content. For brands and retailers, ORME offers free, simple, and fast integration with all e-commerce platforms and an easy, efficient, and controlled content creation process. The platform also boasts a personalized AI-powered content and product recommendation engine, a style chatbot, and a content editor filter.

ORME aims to solve the issues with low conversion rates with affiliate, influencer and digital marketing, and the lack of an end-to-end SFV platform in the US. According to McKinsey & Company, on average, 28% of video shopping leads are converted into sales, a statistic that ORME plans to capitalize on.

The SFV and social commerce market is growing rapidly. Affiliate and banner marketing is a $12 billion market globally, with video shopping projected to be a $35 billion market in the US in 2024. Social media influencer marketing spend by brands was around $16.4 billion in 2022 and is increasing at a rate of 18.8% per annum.

About Xcel Brands

Xcel Brands, Inc. (NASDAQ: XELB) is a media and consumer products company engaged in the design, marketing, live streaming, social commerce sales of branded apparel, footwear, accessories, fine jewelry, home goods and other consumer products, and the acquisition of dynamic consumer lifestyle brands. Xcel was founded in 2011 with a vision to reimagine shopping, entertainment, and social media as one thing. Xcel owns the Judith Ripka, Halston, LOGO by Lori Goldstein, and C. Wonder by Christian Siriano brands and a minority stake in the Isaac Mizrahi brand. It also owns and manages the Longaberger brand through its controlling interest in Longaberger Licensing LLC and a 50% interest in a JV in TWRHLL (“Tower Hill”) by Christie Brinkley. Xcel is pioneering a true modern consumer products sales strategy which includes the promotion and sale of products under its brands through interactive television, digital live-stream shopping, social commerce, brick-and-mortar retail, and e-commerce channels to be everywhere its customer’s shop. The company’s brands have generated in excess of $4 billion in retail sales via livestreaming in interactive television and digital channels alone. Headquartered in New York City, Xcel Brands is led by an executive team with significant live streaming, production, merchandising, design, marketing, retailing, and licensing experience, and a proven track record of success in elevating branded consumer products companies. www.xcelbrands.com.

About ORME

ORME is based in New York and is a next generation short form video marketplace inspiring our users through honest and authentic content created by shoppers, creators, influencers and brands wherever they create, watch, listen, connect and socialize in the digital universe. ORME was cofounded by Xcel Brands and KonnectBio, Inc.

ORME is committed to evolving through innovations in technology including the major application of AI, making deep connections with our users and community and providing opportunity to all in the retail commerce flywheel. ORME makes the everyday shopper a paid influencer. www.ormelive.com

Forward Looking Statements

This press release contains forward-looking statements. All statements other than statements of historical fact contained in this press release, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “ongoing,” “could,” “estimates,” “expects,” “intends,” “may,” “appears,” “suggests,” “future,” “likely,” “goal,” “plans,” “potential,” “projects,” “predicts,” “seeks,” “should,” “would,” “guidance,” “confident” or “will” or the negative of these terms or other comparable terminology. These forward-looking statements include, but are not limited to, statements regarding our anticipated revenue, expenses, profitability, strategic plans and capital needs. These statements are based on information available to us on the date hereof and our current expectations, estimates and projections and are not guarantees of future performance. Forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors, including, without limitation, the risks discussed in the “Risk Factors” section and elsewhere in the Company’s Annual Report on form 10-K for the year ended December 31, 2022 and its other filings with the SEC, which may cause our or our industry’s actual results, levels of activity, performance or achievements to differ materially from those expressed or implied by these forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time, and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements. You should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, we undertake no obligation to update any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason.

For further information please contact:

Dave Gentry, CEO RedChip Companies Inc. 407-491-4498 XELB@redchip.com

Vancouver, British Columbia–(Newsfile Corp. – January 25, 2024) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) is pleased to provide a corporate update, announce the declaration of a quarterly dividend payment to shareholders, and deliver guidance for 2024.

Corporate Update

Hemisphere realized another successful year in 2023, balancing production growth with balance sheet strength and shareholder return. During the year, $17.5 million was returned to shareholders in the form of dividends ($13.1 million) and share buybacks ($4.4 million), representing an approximate 14% yield to shareholders based on the market capitalization of Hemisphere at year-end.

The Company achieved record average production in the fourth quarter of 3,375 boe/d (99% heavy oil), which represents a 16% increase over the same period in 2022. This growth in production year-over-year is the combined result of Hemisphere’s successful third quarter drilling program with the Company’s effective enhanced oil recovery (“EOR”) polymer flood projects. Hemisphere’s annual average production for 2023 was approximately 3,100 boe/d (99% heavy oil), representing 10% growth as compared to 2022.

Balance sheet strength continued to be a priority in 2023, with Hemisphere exiting the year in a cash position. Hemisphere funded all of its shareholder returns and entire $16 million capital expenditure1 program on 2023 cash flow. In addition to drilling 8 successful Atlee Buffalo wells and upgrading some of its facilities, the Company acquired over 2,500 hectares of new land in Saskatchewan and Alberta. Hemisphere has plans to drill a new prospect on some of these Saskatchewan lands in the first half of 2024, and believes it to be prospective for EOR polymer flooding.

Given the significant free cash flow generated by Hemisphere’s ultra-low production decline and long-life reserve asset base, the Company was able to complement its $0.025 per share quarterly base dividend with a $0.03 per share special dividend paid in the fourth quarter of 2023. This brought total shareholder returns last year to $0.13 per share in dividends. Hemisphere also invested $4.4 million into its normal course issuer bid (“NCIB”) share buyback program to purchase and cancel 3.5 million shares in 2023.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on February 23, 2024 to shareholders of record as of the close of business on February 9, 2024. The dividend is designated as an eligible dividend for income tax purposes.

2024 Corporate Guidance

Hemisphere’s Board of Directors has approved a 2024 capital expenditure program of $21 million, which is planned to be entirely funded by Hemisphere’s estimated 2024 adjusted funds flow1 (“AFF”) of $40 million and is anticipated to provide 10% annual production growth. The majority of capital will be allocated to drilling and facility work, with approximately 10% allotted to exploration and land acquisition. Over half of the planned capital expenditures are scheduled for the third quarter, providing Hemisphere with the flexibility to adjust plans subject to the commodity price environment.

The start of 2024 brought with it some extreme cold weather which has substantially affected corporate production during the month of January. The failure of an electrical panel at Hemisphere’s G pool facility resulted in the loss of power to its operations. Subsequent sustained -40°C weather led to freezing of most of the G pool wells and facility, which experienced 5 days of complete downtime and an additional few days of lower production as equipment was repaired and wells were brought back online. All impacts of this production disruption have been accounted for in the guidance set out below, and the team has now restored operations back to normal levels.

After capital expenditures and asset retirement obligations (“ARO”), 2024 free funds flow1 (“FFF”) is estimated to be $19 million, of which approximately 50% is planned to be paid in quarterly dividends as shown in the table below. The balance of cash will be used for discretionary purposes, which may include potential acceleration of other development or exploration projects, acquisitions, and additional return of capital to shareholders through Hemisphere’s NCIB program and/or special dividends.

Management believes that the 2024 development plan provides stable production growth and consistent shareholder returns, while still allowing for modest investment in a new EOR play with exciting growth potential for the Company.

Highlights and assumptions of Hemisphere’s guidance at US$75/bbl WTI are as follows:

Average annual production of 3,400 boe/d (99% heavy oil), a 10% increase as compared to 2023

Average WTI price of US$75/bbl, with sensitivities shown at US$65/bbl and US$85/bbl

WCS differential of US$15.50/bbl and quality adjustment of $7.50/bbl

CAD/US FX of 1.35

Operating and transportation costs of $14.85/boe

Royalties and GORRs on gross revenue of 20% at US$75/bbl WTI, 18% at US$65/bbl WTI, and 22% at US$85/bbl WTI

Net G&A of $3.65/boe

Tax Costs of $7.29/boe at US$75/bbl WTI, $4.91/boe at US$65/bbl WTI, and $9.53/boe at US$85/bbl WTI

2024 Corporate Guidance(2)

US$65 WTI

US$75 WTI

US$85 WTI

Adjusted Funds Flow (AFF)

$ million

31

40

49

AFF per Basic Share(1,3)

$/share

0.32

0.41

0.49

Capital Expenditures& ARO

$ million

21

21

21

Free Funds Flow (FFF)

$ million

10

19

28

FFF per Basic Share(1,3)

$ million

0.10

0.19

0.28

Dividend per Basic Share(3)

$ million

0.10

0.10

0.10

Notes:

(1) AFF, Capital Expenditures, and FFF are non-IFRS financial measures that are forward looking and do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. AFF per basic share and FFF per basic share are non-IFRS financial ratios that are forward looking and do not have any standardized meaning under IFRS and therefore may not be comparable to similar ratios presented by other entities and include non-IFRS financial measure components of AFF and FFF. See “Non-IFRS Measures“. (2) See assumptions noted above within “2024 Corporate Guidance”. (3) Using a 2024 weighted average of 98,988,539 basic shares issued and outstanding. (4) The amounts above do not include potential future purchases through the Company’s NCIB program or other discretionary uses of available funds.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through EOR polymer flood projects. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-Looking statements are typically identified by words such as anticipate, continue, estimate, expect, forecast, may, will, project, could, plan, intend, should, believe, outlook, potential, target, and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements regarding the Company’s plans to drill its new Saskatchewan prospect in early 2024 and its belief that it is prospective for EOR polymer flooding; the record date and payment date for Hemisphere’s quarterly dividend; that Hemisphere’s 2024 capital budget is planned to be entirely funded by Hemisphere’s estimated 2024 AFF and is anticipated to provide 10% annual production growth, including that the majority of capital will be allocated to drilling and facility work, with approximately 10% of it allotted to exploration and land acquisition as well as expectations for the timing of such expenditures; Hemisphere’s anticipation that approximately 50% of estimated $19 million in free funds flow will be paid in quarterly dividends with the balance of cash being used for discretionary purposes, which may include potential acceleration of other development or exploration projects, acquisitions, and additional return of capital to shareholders through Hemisphere’s NCIB program and/or special dividends; the expected manner in which the Company’s 2024 capital budget will be spent, including the timing of such expenditures and any discretionary amounts, which may include potential acceleration of other development or exploration projects, acquisitions, and return of capital to shareholders through Hemisphere’s NCIB program and/or dividends, and the anticipated effects thereof, including as set forth under “2024 Corporate Guidance” and the Company’s dividend policy and the other matters and guidance set forth under “2024 Corporate Guidance”.

Forward‐Looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information, but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein (including the assumptions noted in respect of “2024 Corporate Guidance”), assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; inflationary pressure and related costs; that the Company’s dividend policy will remain the same and the Company will continue to be able to declare dividends; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the accuracy of the Company’s reservoir modelling; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; regulatory risks, including penalties or other remedial actions, the ability of the Company to maintain legal title to its properties; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; results of Hemisphere’s waterflood operations; the ability of Hemisphere to, pending future events, return capital to shareholders as a result of any required third party approvals; changes in budgets; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s most recent Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

Forward-Looking Financial Information