Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Challenging Conditions. Continuing challenging macroeconomic and business conditions impacted ODP in Q4. ODP Business Solutions faced economic factors that caused enterprise spending constraints in the quarter, while Office Depot had more cautious consumer spending (along with 47 fewer stores). However, fiscal year figures were in-line with management guidance, and management is executing on initiatives to improve traction on both fronts.

4Q Results. Sales for the fourth quarter were $1.62 billion compared to $1.80 billion last year but were above our expectations at $1.55 billion and consensus at $1.61 billion. Net loss totaled $3 million, or $0.10/sh, compared to a loss of $37 million, or $0.96/sh, in the prior year. Adjusted EPS was $0.66 versus $1.13 last year. We were at $0.40 and $0.68, respectively. Adjusted EBITDA totaled $58 million, down from $83 million last year, and we were at $49 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Phase 2 Trial Tests THIO Against THIO With Libtayo. MAIA announced the design of the third stage of the THIO-101 Phase 2 trial, consisting of Expansion and Registration stages. Both stages will enroll patients with non-small cell lung cancer (NSCLC) receiving the regimens as third-line treatment, expected to begin in 1Q25. Following the conclusion of the trial around 4Q25, we expect MAIA to apply for Accelerated Approval from the FDA.

Expansion Stage Is Expected To Begin In 1Q25. The THIO-101 Expansion stage will have two arms to determine the contributions of each drug to patient outcomes. In the first arm, 30 patients will receive the THIO-Libtayo (cemiplimab) combination at the 180mg dose. The second arm will treat 7 patients who were treated with THIO monotherapy to determine its efficacy. If the outcomes of THIO alone are moderate, the treatment arm will be discontinued. If sufficient efficacy is seen, up to 8 more patients will be enrolled for a total maximum enrollment of 48 patients. The primary endpoint is Overall Response Rate (ORR).

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q Results. Revenue for the fourth quarter was $283.1 million, an increase from $273.8 million last year but slightly below our $290 million estimate. Gross margin was 24.7% compared to 26.3%. Net income was $3.9 million, or $0.03/sh, from $2.4 million, or $0.02/sh, last year. We estimated net income of $2.5 million or $0.02/sh. Adjusted EPS was $0.13 from $0.12 last year and our $0.10 estimate. Adjusted EBITDA was $25.2 million from $29.1 million last year and our $24 million estimate.

New Joint Venture. Alongside the results was the announcement of a new joint venture with the Company and RAFAEL. The roughly 50/50 partnership is to establish a U.S.-based merchant supplier of solid rocket motors (SRMs) and other energetics named Prometheus Energetics. Up to $175 million in capital is committed between the two companies, with the venture currently forecasted an annual base case revenue of several $100 million a year once at rate production. In our view, the venture can represent a substantial value-creation driver and could potentially drive top and bottom-line growth once up and running.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Kelly (Nasdaq: KELYA, KELYB) connects talented people to companies in need of their skills in areas including Science, Engineering, Education, Office, Contact Center, Light Industrial, and more. We’re always thinking about what’s next in the evolving world of work, and we help people ditch the script on old ways of thinking and embrace the value of all workstyles in the workplace. We directly employ nearly 350,000 people around the world and connect thousands more with work through our global network of talent suppliers and partners in our outsourcing and consulting practice. Revenue in 2021 was $4.9 billion. Visit kellyservices.com and let us help with what’s next for you.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

More Integration. As promised, Kelly continues to take steps to integrate the Motion Recruitment Partners offerings with Kelly’s offerings. Kelly announced the formation of an integrated permanent hiring solutions business line resulting from the combination of KellyOCG’s global recruitment process outsourcing (RPO) specialty and MRPs’ talent acquisition solutions brand, Sevenstep. The integrated business creates a leading talent solutions offering that ranks among the top five globally.

Detail. The integrated business will oversee a team supporting 71 countries with 33 in-country teams and 19 global hub locations. Sevenstep brings an industry-leading brand and attractive client base to KellyOCG, expanding its RPO scale and capabilities. We believe the KellyOCG and Sevenstep businesses are highly complementary and will deliver an unmatched breadth of service, a high delivery footprint, and innovative technology offerings to clients.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Apollo Global Management in talks to lead $35 billion financing package for Meta’s US data centers – Funding will support Meta’s planned $65 billion AI investment strategy announced by Zuckerberg – Deal represents growing private credit market for AI infrastructure as tech giants race to build capacity

Meta Platforms is pursuing a groundbreaking $35 billion financing package led by Apollo Global Management to accelerate the development of artificial intelligence data centers across the United States, according to sources familiar with the negotiations.

The Facebook parent company is engaging with the alternative asset manager to secure this substantial funding as part of its previously announced $65 billion investment in AI infrastructure planned for 2025. While discussions remain in early stages with no guarantee of completion, the deal represents one of the largest private financing arrangements for technology infrastructure to date.

“The race to build AI infrastructure is creating unprecedented investment opportunities,” said a market analyst who requested anonymity due to the sensitive nature of the ongoing negotiations. “Tech giants are competing for computing power, and Meta is positioning itself to avoid falling behind competitors like Microsoft.”

Meta CEO Mark Zuckerberg outlined the company’s aggressive AI strategy last month, emphasizing plans to construct massive new data centers and expand AI-focused teams. A key component of this vision includes bringing approximately one gigawatt of computing power online in 2025 – enough electricity to power roughly 750,000 homes.

The company has already announced a $10 billion data center in Louisiana and has been actively purchasing advanced computer chips to power its growing suite of AI products and services. This financing arrangement would provide Meta with the capital flexibility to accelerate these initiatives without compromising its balance sheet strength.

For Apollo, the deal aligns with its recent strategy of providing large-scale financing to investment-grade corporations while typically retaining a portion of the funding and syndicating the remainder to other investors. The firm has been expanding its capacity to write substantial checks as it pushes deeper into what it considers the next frontier of private credit markets.

The AI infrastructure boom is creating enormous demand for capital across the technology sector. Industry experts estimate hundreds of billions of dollars will be required to build the necessary data centers, power facilities, and networking infrastructure to support the computing demands of advanced AI systems.

Microsoft, one of Meta’s primary competitors in the AI space, recently announced plans to spend $80 billion on data centers in the current fiscal year. CEO Satya Nadella emphasized that sustaining this level of investment is essential to meet “exponentially more demand” for AI services.

Bankers and investors have been eager to participate in AI-related financing deals after witnessing stock markets heavily reward companies central to the AI ecosystem throughout the past year. Private credit providers like Apollo are increasingly stepping in to fill funding gaps as traditional banks face regulatory constraints on large-scale lending.

Neither Meta nor Apollo provided official comments regarding the potential financing arrangement, maintaining standard practice for deals at this preliminary stage. However, industry observers note that securing this funding would represent a significant strategic advantage for Meta as it competes for AI dominance against tech rivals including Microsoft, Google, and Amazon.

Key Points: – Patient small cap investors view market downturns as chances to acquire quality businesses at discounted prices. – Thorough analysis of small cap companies can uncover exceptional businesses with strong fundamentals before they attract mainstream attention. – The greatest advantage in small cap investing comes from maintaining conviction during periods of underperformance that drive away less patient investors.

In a market often dominated by mega-cap tech stocks and headline-grabbing trends, small cap investing remains a powerful avenue for those willing to embrace patience as their primary strategy. While these smaller companies may lack the immediate name recognition of their larger counterparts, they offer distinct advantages to investors who can weather short-term volatility in pursuit of long-term gains.

The Virtue of Patience in Small Cap Investing

The true edge in small cap investing isn’t found in rapid trading or timing market swings—it’s discovered through patient capital deployment and a steadfast focus on fundamentals. Small cap stocks, typically defined as companies with market capitalizations between $300 million and $2 billion, often experience greater price volatility than large caps. This volatility, rather than representing inherent risk, actually creates opportunities for patient investors.

When market sentiment shifts and institutional investors flee to perceived safety, small caps frequently bear the brunt of the selling pressure. This creates temporary dislocations between price and value that patient investors can explore. While others panic during downturns, disciplined small cap investors recognize these moments as rare opportunities to acquire ownership in quality businesses at discounted prices.

Filtering the Noise to Find Value

Today’s financial ecosystem bombards investors with constant commentary, predictions, and “expert” opinions. Patient small cap investors develop the crucial skill of filtering this noise to identify genuine value. They understand that short-term price movements often reflect temporary factors rather than fundamental business changes.

The ability to separate market noise from meaningful information allows these investors to maintain conviction in their small cap holdings through inevitable periods of underperformance. They recognize that small companies need time to execute their business plans, expand their market presence, and ultimately deliver value to shareholders.

The Power of Thorough Equity Research

In the small cap universe, thorough equity research becomes an invaluable competitive advantage. While large caps are constantly scrutinized by hundreds of analysts, dedicated research into smaller companies can uncover hidden gems before they appear on the institutional radar. Patient investors who commit to comprehensive due diligence often identify promising businesses with robust fundamentals that remain undervalued.

This research advantage becomes especially powerful when investors develop expertise in specific sectors or industries. By understanding the competitive landscape, technological trends, and regulatory environments that shape small cap businesses, patient investors can accurately assess both risks and growth catalysts that casual market participants might miss. This deep research foundation also provides the conviction necessary to hold positions through inevitable market fluctuations.

Embracing the Long View

The most successful small cap investors share a common trait: they evaluate investments through a multi-year lens rather than quarterly results. They understand that compound growth in small businesses can eventually translate into extraordinary investment returns. A company growing earnings at 15-20% annually will double its profits approximately every four years—a powerful driver of long-term stock performance that patient investors can capture.

The Psychological Challenge

Perhaps the greatest challenge in small cap investing isn’t analytical but psychological. It requires the fortitude to remain invested when markets turn negative, when positions move against you, and when the temptation to chase better-performing assets becomes strongest. Patient investors understand that their edge comes precisely from accepting short-term discomfort that others refuse to endure.

For those willing to cultivate patience, small cap investing continues to offer one of the most compelling risk-reward propositions in public markets. By focusing on long-term business value rather than short-term price fluctuations, investors can position themselves to achieve returns that make the occasional storms worth weathering.

SAN DIEGO, Feb. 26, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in the defense, national security and global markets, and RAFAEL Advanced Defense Systems Ltd., today announced an approximate 50/50 partnership for the establishment of a U.S.-based merchant supplier of solid rocket motors (SRMs) and other energetics. The new joint venture, named Prometheus Energetics (“Prometheus”), is set to be headquartered on an approximate 500-acre site near the United States Navy and Army facility in Crane, Indiana.

Kratos and RAFAEL (through its U.S. based subsidiary RAFAEL USA) have jointly committed up to $175 million in capital for the establishment of Prometheus and required property, plant, equipment and personnel needed for the new, state-of-the-art energetics manufacturing campus and facilities. After construction of the plant and once RAFAEL’s technology transfer is completed and certified for operations, Prometheus is projected to begin production in 2027 of SRMs.

RAFAEL is the developer and manufacturer of unique, world-renowned systems such as the Iron Dome and the TROPHY APS which are in service in the Israeli Defense Forces as well as the David’s Sling which provides the middle layer of air defense for the state of Israel. The company, originally established as the IDF Science Corps, has developed groundbreaking technologies like high energy laser solutions like the Iron Beam which are expected to be operational by the end of 2025. The company functions through a vertical integration structure that enables a unique ability to meet the demands and overcome the challenges of the global market and supply chain. RAFAEL offers a diverse portfolio from new space to the ground battlespace with battle-proven technologies.

Kratos is a leader in hypersonic or advanced systems, strategic systems, ballistic missile targets, sub-orbital research vehicles, sounding rockets, and solid rocket motors. Kratos has served the U.S. advanced systems and missile defense communities for decades, delivering numerous novel systems and vehicle flight tests. Kratos is the only company today delivering both propulsion and advanced flight systems, with Kratos advanced systems including the low-cost Erinyes Glide Vehicle, Dark Fury, Zeus and Oriole Solid Rocket Motors, and other Kratos systems and technologies. Kratos provides unmatched innovation, disruptive capabilities, mission responsiveness and affordability to our customers across our portfolio of systems.

Eric DeMarco, President and CEO of Kratos Defense, said, “We believe Prometheus, once up and running at full rate production, will be a step function catalyst in value creation for Kratos’ stakeholders and the U.S. defense industrial base, similar to Kratos’ recent MACH-TB contract award—the largest single-award contract in Kratos history. Like other major Kratos investments such as Oriole, Zeus, and Erinyes, Prometheus responds to a critical need to strengthen the U.S. Industrial Base and will also provide tens of thousands of SRMs and casted warheads supporting both America’s most reliable partner in the Middle East and United States national security related demand from a true SRM and energetics merchant supplier.”

Kratos will reflect Prometheus in its consolidated financial statements on the Equity Method of Accounting, under which Kratos will record approximately 50 percent of Prometheus Net Income on a single line “Net Income from Prometheus Energetics” in its income statement, and Kratos will annually receive approximately 50 percent of the Free Cash Flow generated from Prometheus. Kratos intends to continue to report Kratos Operating Income, Net Income, Adjusted EBITDA and other financial matrices separate from the Prometheus results, in order for all Kratos stakeholders to be able to follow the progress of each Company, the investment made in Prometheus and the future return on Kratos’ investment in Prometheus.

RAFAEL Advanced Defense Systems Ltd., one of Israel’s largest defense contractors, develops, manufactures, and sustains combat-proven technologies, products, and systems-of-systems for air, land, naval, space and digital applications. RAFAEL’s delivery of combat-proven systems is supported by vertically integrated facilities and engineering teams servicing the development and production of SRMs and warhead (WH) products that play a critical role in Israel’s Iron Dome, the world’s premier air defense system designed to intercept and destroy short-range rockets, artillery shells, UAVs, and other aerial threats. This vertical integration has made RAFAEL a leading expert in SRMs and WH development and production, allowing it to continuously expand capabilities and push the envelope in technology, performance, and fielding of effective systems. RAFAEL’s multi-dimensional portfolio and unique innovative capabilities have enabled the development of world-leading technologies across all spheres.

Yoav Tourgeman, President and CEO of RAFAEL Advanced Defense Systems Ltd., said: “The establishment of Prometheus Energetics is a strategic leap forward, reinforcing RAFAEL’s commitment to strengthening the U.S. defense industrial base while ensuring our allies and partners have access to the most advanced, combat-proven energetics solutions. This step constitutes a strategic vector that combines business considerations in the American market with the increasing demand for energetic products, while significantly enhancing our ability to deliver resilient and reliable supply solutions to our customers. Through this joint venture, we are deepening our longstanding partnership with the United States, strengthening supply chain independence, and bolstering the critical capabilities needed to address evolving national security challenges.”

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

About RAFAEL Advanced Defense Systems Ltd. Established in 1948, RAFAEL Advanced Defense Systems Ltd. develops, manufactures, and sustains combat-proven technologies, products, and systems-of-systems for air, land, naval, space and digital applications. As the developer of two integral layers of Israel’s multi-layered air defense array and the developer of the world’s only operation active protection system TROPHY APS, the company offers innovative and proven solutions for the global market. RAFAEL’s air defense portfolio has achieved international recognition from Iron Dome to David’s Sling and is expected to provide the first ever operational high-energy laser weapon system to the IDF by 2025. The company has bolstered its international standing as a top-tier defense manufacturer by through an innovative approach of vertical integration enabling seamless technology transfer and local production, making it a trusted partner for defense solutions in global markets, particularly in the U.S. where its systems strengthen national security priorities. Leveraging its technological ingenuity, operational experience, and unparalleled understanding of evolving combat requirements, RAFAEL provides global warfighters with today’s most advanced technologies and life-saving defense solutions that ensure operational superiority. RAFAEL’s strategy includes strategic international partnerships and localization to ensure customer sovereignty. For more information on RAFAEL, please visit https://www.rafael.co.il/

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

NEW ALBANY, Ohio, Feb. 26, 2025 (GLOBE NEWSWIRE) — Commercial Vehicle Group (the “Company” or “CVG”) (NASDAQ: CVGI) will hold its quarterly conference call on Tuesday, March 11, 2025, at 8:30 a.m. ET, to discuss fourth quarter and full year 2024 financial results. CVG will issue a press release and presentation prior to the conference call.

Toll-free participants dial (800) 549-8228 using conference code 45919. International participants dial (289) 819-1520 using conference code 45919. This call is being webcast and can be accessed through the “Investors” section of CVG’s website at ir.cvgrp.com where it will be archived for one year.

A telephonic replay of the conference call will be available until March 25, 2025. To access the replay, toll-free callers can dial (+1) 888 660 6264 using access code 45919#, and toll callers in North America and other locations can dial (+1) 289 819 1325.

About CVG

At CVG, we deliver real solutions to complex design, engineering and manufacturing problems while creating positive change for our customers, industries, and communities we serve. Information about the Company and its products is available on the internet at www.cvgrp.com.

Investor Relations Contact: Ross Collins or Stephen Poe Alpha IR Group CVGI@alpha-ir.com

Full Year 2024 Revenues of $1.136 Billion Reflect 9.6 Percent Growth and 9.1 Percent Organic Growth, Respectively, Over Full Year 2023 Revenues of $1.037 Billion

Full Year 2024 Unmanned Systems Revenues of $270.5 Million Reflect 27.5 Percent Growth and 25.1 Percent Organic Growth Over Full Year 2023 Revenues of $212.2 Million

Full Year 2024 KGS Revenues of $865.8 Million Reflect 5.0 Percent Organic Growth of $40.9 Million Over Full Year 2023 Revenues of $824.9 Million

Full Year 2024 Net Income of $16.3 Million and GAAP EPS of $0.11 Per Share

Fourth Quarter 2024 Revenues of $283.1 Million Reflect 3.4 Percent Growth Over Fourth Quarter 2023 Revenues of $273.8 Million

Fourth Quarter 2024 Cash Flow Generated from Operations and Free Cash Flow of $45.6 million and $32.0 million, Respectively

Fourth Quarter 2024 Consolidated Book to Bill Ratio of 1.5 to 1 and Bookings of $434.2 Million

Last Twelve Months Ended December 29, 2024 Consolidated Book to Bill Ratio of 1.2 to 1 and Bookings of $1.354 Billion

2025 Financial Forecast Includes 10 Percent Organic Revenue Growth and 2026 Initial Revenue Growth Forecast of 13 to 15 Percent over 2025 Forecast Based on Recent Program Awards

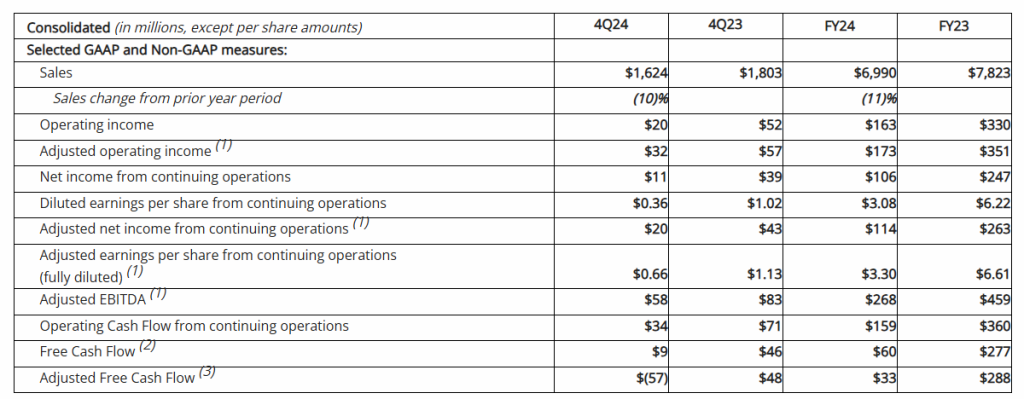

SAN DIEGO, Feb. 26, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a Technology Company in the Defense, National Security and Commercial Markets, today reported its fourth quarter 2024 financial results, including Revenues of $283.1 million, Operating Income of $3.0 million, Net Income attributable to Kratos of $3.9 million, Adjusted EBITDA of $25.2 million and a consolidated book to bill ratio of 1.5 to 1.0.

Fourth quarter 2024 Net Income and Operating Income includes non-cash stock compensation expense of $6.8 million, Company-funded Research and Development (R&D) expense of $10.6 million, including efforts in our Space, Satellite, Unmanned Systems and Microwave Electronic businesses, and expense to accrue $3.2 million related to an employee benefit plan assumed by the Company in an acquisition completed in 2011.

Kratos reported fourth quarter 2024 GAAP Net Income attributable to Kratos of $3.9 million and GAAP Net Income per share of $0.03, compared to GAAP Net Income attributable to Kratos of $2.4 million and GAAP Net Income per share of $0.02, for the fourth quarter of 2023. Adjusted earnings per share (EPS) was $0.13 for the fourth quarter of 2024, compared to $0.12 for the fourth quarter of 2023.

Fourth quarter 2024 Revenues of $283.1 million increased $9.3 million, reflecting 3.4 percent organic growth from fourth quarter 2023 Revenues of $273.8 million. Organic revenue growth was reported in both our Unmanned Systems and KGS segments, with KGS growth including increased revenues in Kratos Turbine Technologies, Defense Rocket Systems, Microwave Products, and C5ISR, offset by the previously reported and expected decline of approximately $16.1 million in the Space and Satellite business, including the industry related impact from OEM delays in the manufacture and delivery of software defined satellites.

Fourth quarter 2024 Cash Flow Generated from Operations was $45.6 million, primarily reflecting the receipt of accelerated favorable customer milestone payments, and increases in deferred revenues or customer advanced payments to $76.3 million at the end of the fourth quarter of 2024, up from $61.9 million at the end of the third quarter of 2024. Free Cash Flow Generated from Operations for the Fourth Quarter of 2024 was $32.0 million after funding of $13.6 million of capital expenditures.

For the fourth quarter of 2024, Kratos’ Unmanned Systems (KUS) segment generated Revenues of $61.1 million and organic revenue growth of 10.3 percent, as compared to $55.4 million in the fourth quarter of 2023, primarily reflecting increased target drone sales. KUS’s Operating Loss was $0.7 million in the fourth quarter of 2024, compared to Operating Income of $1.0 million in the fourth quarter of 2023. KUS’s Adjusted EBITDA for the fourth quarter of 2024 was $2.6 million, compared to $4.0 million for the fourth quarter 2023, reflecting revenue mix, the impact of increased material and subcontractor costs on multi-year fixed price contracts and increased R&D costs.

KUS’s book-to-bill ratio for the fourth quarter of 2024 was 1.3 to 1.0 and 1.2 to 1.0 for the twelve months ended December 29, 2024, with bookings of $82.4 million for the three months ended December 29, 2024, and bookings of $326.8 million for the twelve months ended December 29, 2024. Total backlog for KUS at the end of the fourth quarter of 2024 was $295.2 million compared to $273.9 million at the end of the third quarter of 2024 and $239.0 million at the end of the fourth quarter of 2023.

For the fourth quarter of 2024, Kratos’ Government Solutions (KGS) segment Revenues of $222.0 million increased from Revenues of $218.4 million in the fourth quarter of 2023, reflecting a 1.6 percent growth and organic growth rate. The increased Revenues includes organic revenue growth in our Turbine Technologies, C5ISR, Defense Rocket Support and Microwave Products businesses of $19.7 million, offset by the previously reported and expected decline of approximately $16.1 million in the Space and Satellite business.

KGS reported Operating Income of $11.0 million in the fourth quarter of 2024 compared to $17.5 million in the fourth quarter of 2023, primarily reflecting the mix in revenues and resources as well as the expense to accrue $3.2 million in the fourth quarter of 2024 related to a benefit plan assumed by the Company in a previous acquisition. Fourth quarter 2024 KGS Adjusted EBITDA was $22.6 million, compared to fourth quarter 2023 KGS Adjusted EBITDA of $25.1 million, primarily reflecting the mix in revenues and resources.

KGS reported a book-to-bill ratio of 1.6 to 1.0 for the fourth quarter of 2024, a book to bill ratio of 1.2 to 1.0 for the last twelve months ended December 29, 2024 and bookings of $351.8 million and $1.028 billion for the three and last twelve months ended December 29, 2024, respectively. KGS’s total backlog at the end of the fourth quarter of 2024 was $1.150 billion, as compared to $1.020 billion at the end of the third quarter of 2024, and $988.0 million at the end of the fourth quarter of 2023.

Kratos reported consolidated bookings of $434.2 million and a book-to-bill ratio of 1.5 to 1.0 for the fourth quarter of 2024, and consolidated bookings of $1.354 billion and a book-to-bill ratio of 1.2 to 1.0 for the last twelve months ended December 29, 2024. Consolidated backlog was $1.445 billion on December 29, 2024, as compared to $1.294 billion at September 29, 2024 and $1.227 billion on December 31, 2023. Kratos’ bid and proposal pipeline was $12.4 billion at December 29, 2024, as compared to $11.0 billion at December 31, 2023. Backlog at December 29, 2024 included funded backlog of $1.090 billion and unfunded backlog of $355.0 million.

Full Year 2024 Results

Kratos reported its full year 2024 financial results, including Revenues of $1.136 billion, Operating Income of $29.0 million, Net Income attributable to Kratos of $16.3 million, Adjusted EBITDA of $105.7 million and a consolidated book to bill ratio of 1.2 to 1.0.

Included in the full year 2024 Net Income and Operating Income is non-cash stock compensation expense of $29.8 million, Company-funded Research and Development (R&D) expense of $40.3 million, including ongoing development efforts in our Space and Satellite Communications business to develop our first to market, virtual, software-based OpenSpace command & control (C2), telemetry tracking & control (TT&C) and other ground system solutions and ongoing development efforts in our Unmanned Systems and Microwave Products businesses, and an expense to accrue $3.2 million related to an employee benefit plan assumed by the Company in an acquisition completed in 2011.

Kratos reported full year 2024 GAAP Net Income of $16.3 million and GAAP Net Income per share of $0.11, compared to a GAAP Net Loss attributable to Kratos of $8.9 million and a GAAP Net Loss per share of $0.07, for the full year 2023. Adjusted earnings per share (EPS) was $0.49 for the full year 2024, compared to $0.42 for the full year 2023.

Full year 2024 Revenues of $1.136 billion increased $99.2 million, reflecting 9.6 percent growth and 9.1 percent organic growth, including the impact of the Sierra Technical Services, Inc. (STS) acquisition on a pro forma basis as if acquired at the beginning of 2023, respectively, from full year 2023 Revenues of $1.037 billion. Full year 2024 Cash Flow Generated from Operations was $49.7 million, including the receipt of accelerated favorable customer milestone payments, offset partially by working capital uses including increases in inventories, prepaid assets and investments in other assets and reduction of deferred revenues or advanced customer payments. Free Cash Flow Used in Operations was $8.5 million after funding of $58.2 million of capital expenditures. Full year 2024 capital expenditures were elevated due primarily to the manufacture of the two production lots of Valkyries prior to contract award to meet anticipated customer orders and requirements and due to investments related to the expansion and addition of production facilities.

For full year 2024, KUS generated Revenues of $270.5 million, as compared to $212.2 million in the full year 2023, reflecting 27.5 percent growth and 25.1 percent organic growth, including the impact of the STS acquisition on a pro forma basis as if acquired at the beginning of 2023, primarily reflecting increased domestic and international drone activity. KUS’s Operating Income was $2.9 million in full year 2024 compared to $4.2 million in full year 2023. KUS’s Adjusted EBITDA for full year 2024 was $16.3 million, compared to full year 2023 Adjusted EBITDA of $14.8 million, reflecting the increased volume partially offset by increased material and subcontractor costs on multi-year fixed price contracts and increased R&D costs.

For full year 2024, KGS Revenues of $865.8 million increased $40.9 million, reflecting 5.0 percent organic growth from Revenues of $824.9 million in full year 2023. The increased Revenues includes organic revenue growth in our Turbine Technologies, C5ISR, Microwave Products, Defense Rocket Support and Training Solutions businesses aggregating $88.7 million, offset by a reduction of $47.8 million in offset by the Space and Satellite business described previously.

KGS reported operating income of $56.6 million in full year 2024 compared to $52.7 million in full year 2023, primarily reflecting the increased revenue volume. Full year 2024 KGS Adjusted EBITDA was $89.4 million, compared to full year 2023 KGS Adjusted EBITDA of $80.6 million, primarily reflecting the increased revenue.

Eric DeMarco, Kratos’ President and CEO, said, “Kratos’ full year 2024 and fourth quarter demonstrated once again that we can significantly organically grow the business, and make sizable internally funded investments, positioning the Company for accelerating future growth, while also generating significant, positive operating cash flow. We have recently received several large new program and contract awards, including in the hypersonic, target drone, jet engine, rocket, and satellite system areas, enabling us to increase our expected revenue growth rate for 2026 to a range of 13 percent to 15 percent above our current 2025 financial forecast that we provided today, which includes 10 percent growth over 2024. Kratos’ fourth quarter 1.5 to 1.0 book to bill ratio and our $12.4 Billion opportunity pipeline also provides confidence in our expected accelerating future growth trajectory, with increased margins.”

Mr. DeMarco continued, “The Trump Administration has increased emphasis on reducing cost, rapidly fielding new technology and systems and getting more for less, all which are and have been pillars of Kratos’ Mission. At Kratos, “Affordability is a Technology” and “Better is the Enemy of Good Enough Ready to Field Today”, as represented in our Erinyes, Dark Fury and other hypersonic vehicles, our Zeus, Oriole and other rocket systems, and our jet drones, jet engines and propulsion systems. We believe Kratos’ alignment with the new Administration’s objectives will be recognized in increased bookings, increased expected future growth rates and increased future profitability, including as based on recent meetings and discussions with certain of our customers.”

Mr. DeMarco concluded, “After decades of focus on fighting terrorism and asymmetric warfare, the United States has begun a generational rebuild of its industrial base and the ability to deter and defeat Nation State adversaries. The Axis of Resistance and the threat to the U.S. and its Allies is real, and Kratos is a key element of the proven Peace through Overwhelming Strength approach to Global Security and stability. As a result, we expect a future, multiyear, up and to the right organic growth trajectory with increased margins and profitability, and Kratos making the necessary investments in, among other things, property, plant, and equipment, to successfully execute for our customers and country.”

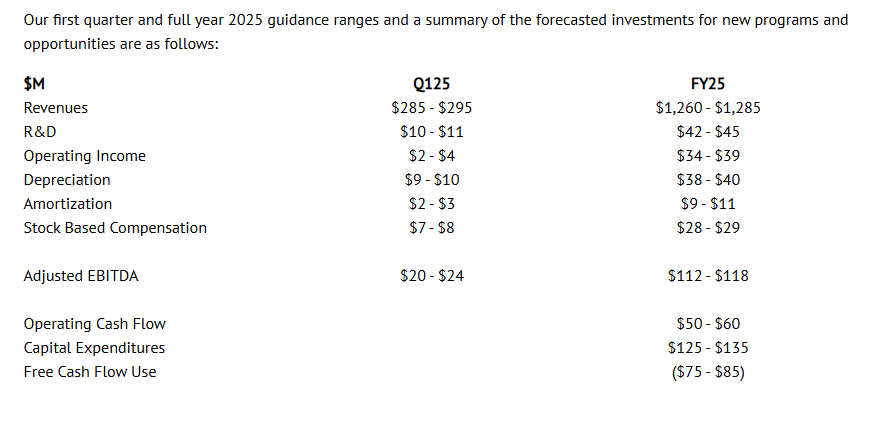

Financial Guidance

We are providing our initial 2025 first quarter and full year 2025 financial guidance range, which includes our assumptions, including as related to: current forecasted business mix, employee sourcing, hiring and retention; manufacturing, production and supply chain disruptions; parts shortages and related continued significant cost and price increases in each of these areas, that are impacting the industry and Kratos. Additionally, a U.S. Government budget was not passed by October 1, 2024, the beginning of Federal Fiscal Year 2025, and as a result, Kratos and others in our industry are operating under a Continuing Resolution Authorization (CRA), which currently expires March 14, 2025, under which no new contracts and no increases in existing contracts production or funding, among other stipulations, is permitted. If the current CRA is not resolved by March 14, 2025, the industry and Kratos will have operated under CRAs, without a DoD Budget, for approximately 12 of the previous 18 months. Kratos has a number of new and existing programs and contracts which are directly being impacted by the current CRA. Kratos’ 2025 financial forecast and guidance provided today assumes that the current CRA will be resolved by March 14, 2025, and that a U.S. Federal and DoD budget which includes no unexpected funding cuts impacting our business occurs. If the current CRA goes substantially beyond the existing March 14, 2025 date, or if there are significant reductions or changes to programs, contracts or initiatives that Kratos is or expects to be involved with, we will evaluate Kratos’ 2025 and future financial forecasts at that time, based on the existing facts, circumstances and expectations and make any adjustments required.

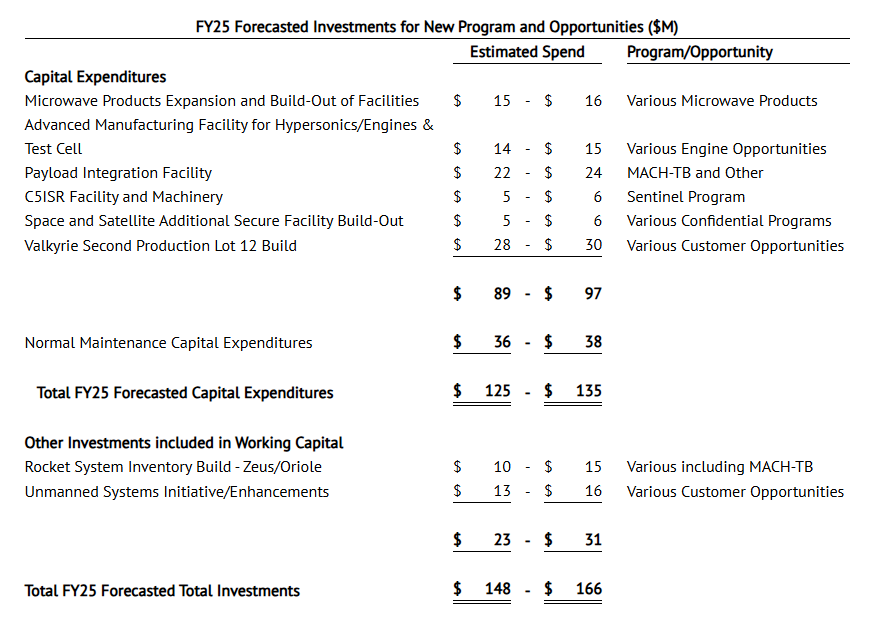

Kratos’ 2025 financial forecast and guidance includes elevated investments for capital expenditures for property, plant and equipment, including the expansion of our manufacturing and production facilities and related inventory builds in our Rocket Systems and Hypersonic businesses, primarily related to the recent MACH-TB 2.0 contract award, the continued manufacture of two production lots of Valkyries prior to contract award, to meet anticipated customer orders and requirements, the expansion and build-out of the Company’s Microwave Products production facilities, the expansion and build-out of our small jet engine production and test cell facilities, and the build-out of additional secure facilities for our federal secured space communications business, in accordance with contract and customer requirements. Kratos’ operating cash flow guidance also assumes certain investments in our rocket systems and unmanned systems businesses.

Management will discuss the Company’s financial results, on a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern) today. The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions

Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com

Notice RegardingForward–LookingStatements This news release contains certain forward-looking statements that involve risks and uncertainties, including, without limitation, express or implied statements concerning the Company’s expectations regarding its future financial performance, including the Company’s expectations for its first quarter and full year 2025 revenues, 2026 revenue growth rates and expected contributors to 2026 projected revenue growth, organic revenue growth rates, R&D, operating income (loss), depreciation, amortization, stock based compensation expense, and Adjusted EBITDA, and full year 2025 operating cash flow, capital expenditures and other investments, and free cash flow, the Company’s future growth trajectory and ability to achieve improved revenue mix and profit in certain of its business segments and the expected timing of such improved revenue mix and profit, including the Company’s ability to achieve sustained year over year increasing revenues, profitability and cash flow, the Company’s expectation of ramp on projects and that investments in its business, including Company funded R&D expenses and ongoing development efforts, will result in an increase in the Company’s market share and total addressable market and position the Company for significant future organic growth, profitability, cash flow and an increase in shareholder value, the Company’s bid and proposal pipeline and backlog, including the Company’s ability to timely execute on its backlog, demand for its products and services, including the Company’s alignment with today’s National Security requirements and the positioning of its C5ISR and other businesses, planned 2025 investments, including in the tactical drone and satellite areas, and the related potential for additional growth in 2025 and beyond, ability to successfully compete and expected new customer awards, including the magnitude and timing of funding and the future opportunity associated with such awards, including in the target and tactical drone and satellite communication areas, performance of key contracts and programs, including the timing of production and demonstration related to certain of the Company’s contracts and control (TT&C) product offerings, the impact of the Company’s restructuring efforts and cost reduction measures, including its ability to improve profitability and cash flow in certain business units as a result of these actions and to achieve financial leverage on fixed administrative costs, the ability of the Company’s advanced purchases of inventory to mitigate supply chain disruptions and the timing of converting these investments to cash through the sales process, benefits to be realized from the Company’s net operating loss carry forwards, the availability and timing of government funding for the Company’s offerings, including the strength of the future funding environment, the short-term delays that may occur as a result of Continuing Resolutions or delays in U.S. Department of Defense (DoD) budget approvals, timing of LRIP and full rate production related to the Company’s unmanned aerial target system offerings, as well as the level of recurring revenues expected to be generated by these programs once they achieve full rate production, market and industry developments, and any unforeseen risks associated with any public health crisis, supply chain disruptions, availability of an experienced skilled workforce, inflation and increased costs, risks related to potential cybersecurity events or disruptions of our information technology systems, and delays in our financial projections, industry, business and operations, including projected growth. Such statements are only predictions, and the Company’s actual results may differ materially from the results expressed or implied by these statements. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Factors that may cause the Company’s results to differ include, but are not limited to: risks to our business and financial results related to the reductions and other spending constraints imposed on the U.S. Government and our other customers, including as a result of sequestration and extended continuing resolutions, the Federal budget deficit and Federal government shut-downs; risks of adverse regulatory action or litigation; risks associated with debt leverage; risks that our cost-cutting initiatives will not provide the anticipated benefits; risks that changes, cutbacks or delays in spending by the DoD may occur, which could cause delays or cancellations of key government contracts; risks of delays to or the cancellation of our projects as a result of protest actions submitted by our competitors; risks that changes may occur in Federal government (or other applicable) procurement laws, regulations, policies and budgets; risks of the availability of government funding for the Company’s products and services due to performance, cost growth, or other factors, changes in government and customer priorities and requirements (including cost-cutting initiatives, the potential deferral of awards, terminations or reduction of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts resulting from Congressional committee recommendations or automatic sequestration under the Budget Control Act of 2011, as amended); risks that the unmanned aerial systems and unmanned ground sensor markets do not experience significant growth; risks that products we have developed or will develop will become programs of record; risks that we cannot expand our customer base or that our products do not achieve broad acceptance which could impact our ability to achieve our anticipated level of growth; risks of increases in the Federal government initiatives related to in-sourcing; risks related to security breaches, including cyber security attacks and threats or other significant disruptions of our information systems, facilities and infrastructures; risks related to our compliance with applicable contracting and procurement laws, regulations and standards; risks related to the new DoD Cybersecurity Maturity Model Certification; risks relating to the ongoing conflict in Ukraine and the Israeli-Palestinian military conflict; risks to our business in Israel; risks related to contract performance; risks related to failure of our products or services; risks associated with our subcontractors’ or suppliers’ failure to perform their contractual obligations, including the appearance of counterfeit or corrupt parts in our products; changes in the competitive environment (including as a result of bid protests); failure to successfully integrate acquired operations and compete in the marketplace, which could reduce revenues and profit margins; risks that potential future goodwill impairments will adversely affect our operating results; risks that anticipated tax benefits will not be realized in accordance with our expectations; risks that a change in ownership of our stock could cause further limitation to the future utilization of our net operating losses; risks that we may be required to record valuation allowances on our net operating losses which could adversely impact our profitability and financial condition; risks that the current economic environment will adversely impact our business, including with respect to our ability to recruit and retain sufficient numbers of qualified personnel to execute on our programs and contracts, as well as expected contract awards and risks related to increasing interest rates and risks related to the interest rate swap contract to hedge Term SOFR associated with the Company’s Term Loan A; currently unforeseen risks associated with any public health crisis, and risks related to natural disasters or severe weather. These and other risk factors are more fully discussed in the Company’s Annual Report on Form 10-K for the period ended December 29, 2024, and in our other filings made with the Securities and Exchange Commission.

Note Regarding Use of Non-GAAP Financial Measures and Other Performance Metrics This news release contains non-GAAP financial measures, including organic revenue growth rates, Adjusted EPS (computed using income from continuing operations before income taxes, excluding income (loss) from discontinued operations, excluding income (loss) attributable to non-controlling interest, excluding depreciation, amortization of intangible assets, amortization of capitalized contract and development costs, stock-based compensation expense, acquisition and restructuring related items and other, which includes, but is not limited to, legal related items, non-recoverable rates and costs, and foreign transaction gains and losses, less the estimated impact to income taxes) and Adjusted EBITDA (which includes net income (loss) attributable to noncontrolling interest and excludes, among other things, losses and gains from discontinued operations, acquisition and restructuring related items, stock compensation expense, foreign transaction gains and losses, and the associated margin rates). Additional non-GAAP financial measures include Free Cash Flow from Operations computed as Cash Flow from Operations less Capital Expenditures plus proceeds from sale of assets and Adjusted EBITDA related to our KUS and KGS businesses. Kratos believes this information is useful to investors because it provides a basis for measuring the Company’s available capital resources, the actual and forecasted operating performance of the Company’s business and the Company’s cash flow, excluding non-recurring items and non-cash items that would normally be included in the most directly comparable measures calculated and presented in accordance with GAAP. The Company’s management uses these non-GAAP financial measures, along with the most directly comparable GAAP financial measures, in evaluating the Company’s actual and forecasted operating performance, capital resources and cash flow. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information presented in compliance with GAAP, and investors should carefully evaluate the Company’s financial results calculated in accordance with GAAP and reconciliations to those financial results. In addition, non-GAAP financial measures as reported by the Company may not be comparable to similarly titled amounts reported by other companies. As appropriate, the most directly comparable GAAP financial measures and information reconciling these non-GAAP financial measures to the Company’s financial results prepared in accordance with GAAP are included in this news release.

Another Performance Metric the Company believes is a key performance indicator in our industry is our Book to Bill Ratio as it provides investors with a measure of the amount of bookings or contract awards as compared to the amount of revenues that have been recorded during the period and provides an indicator of how much of the Company’s backlog is being burned or utilized in a certain period. The Book to Bill Ratio is computed as the number of bookings or contract awards in the period divided by the revenues recorded for the same period. The Company believes that the rolling or last twelve months’ Book to Bill Ratio is meaningful since the timing of quarter-to-quarter bookings can vary.

Expansion study to enroll patients in the U.S. and select countries in Europe and Asia

Multiple milestones attainable for 2025

CHICAGO–(BUSINESS WIRE)– MAIA Biotechnology, Inc., (NYSE American: MAIA) (“MAIA,” the “Company”), a clinical-stage biopharmaceutical company developing targeted immunotherapies for cancer, today announced the trial design for the expansion of its THIO-101 pivotal Phase 2 trial in non-small cell lung cancer (NSCLC). Following successful outcomes to date in THIO-101, the expansion of the study will assess overall response rates (ORR) in advanced NSCLC patients receiving third line (3L) therapy who were resistant to previous checkpoint inhibitor treatments (CPI) and chemotherapy.

The THIO-101 study in 3L will enroll up to 48 patients with two arms: Arm 1, continuing the evaluation of THIO sequenced with Libtayo® (cemiplimab); and Arm 2, evaluating THIO as a monotherapy, to further gain experience of THIO in the contribution of components. Treatment cycles for patients in both arms will administer THIO on 3 consecutive days, followed by immune activation on day 4. Arm 1 will administer Libtayo on day 5. The Company plans to enroll an additional 100 patients for the registration phase of the trial. MAIA expects to conduct the trials in the U.S. and select countries in Europe and Asia.

MAIA recently announced an amended clinical supply agreement with Regeneron to include the expansion portion of THIO-101. Under terms of the amended agreement, MAIA continues to sponsor THIO-101 and Regeneron will provide Libtayo for the treatment of all patients including the additional patients in the expansion and potentially, the registration studies.

“We are excited to start the expansion arm of our THIO-101 trial which is designed to determine overall response rates in third line NSCLC. We expect to have new patients enrolled in the coming weeks,” said Vlad Vitoc, M.D., CEO of MAIA. “Through THIO-101 to date, THIO has delivered unprecedented disease control, response, and survival results. Continued efficacy and safety data generated by our study could support an FDA NDA submission directly, particularly as we plan to seek an accelerated approval of THIO in the U.S.

“We have multiple milestones that we believe are attainable for 2025 and we look forward to keeping our shareholders and investors well informed of our progress on value creation,” Dr. Vitoc added.

As of January 15, 2025, data indicated that Median Overall Survival (OS) in third-line treatment was reached at 16.9 months, with a 95% confidence interval (CI) lower bound of 12.5 months and a 99% CI lower bound of 10.8 months). The treatment has been generally well-tolerated to date in this heavily pre-treated population1.

________________________________

1

Details on safety can be found on the previously announced SITC 2024 presentation available on MAIA’s website.

About THIO THIO (6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in Non-Small Cell Lung Cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleotide 6-thio-2’-deoxyguanosine (THIO) induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. THIO-damaged telomeric fragments accumulate in cytosolic micronuclei and activates both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment with THIO followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. THIO is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About THIO-101, a Phase 2 Clinical Trial THIO-101 is a multicenter, open-label, dose finding Phase 2 clinical trial. It is the first trial designed to evaluate THIO’s anti-tumor activity when followed by PD-(L)1 inhibition. The trial is testing the hypothesis that low doses of THIO administered prior to cemiplimab (Libtayo®) will enhance and prolong immune response in patients with advanced NSCLC who previously did not respond or developed resistance and progressed after first-line treatment regimen containing another checkpoint inhibitor. The trial design has two primary objectives: (1) to evaluate the safety and tolerability of THIO administered as an anticancer compound and a priming immune activator (2) to assess the clinical efficacy of THIO using Overall Response Rate (ORR) as the primary clinical endpoint. Treatment with THIO followed by cemiplimab (Libtayo) has been generally well-tolerated to date in a heavily pre-treated population. For more information on this Phase II trial, please visit ClinicalTrials.gov using the identifier NCT05208944.

About MAIA Biotechnology, Inc. MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is THIO, a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

RESTON, Va., Feb. 26, 2025 /PRNewswire/ — V2X (NYSE: VVX) Inc., announces its award of a $100 million contract to provide aviation maintenance and support services for the Federal Bureau of Investigation’s (FBI) Critical Incident Response Group. Under this contract, V2X will deliver mission-critical aviation resources that enable the FBI to conduct intelligence gathering, investigate operations, and law-enforcement activities.

V2X will support the FBI’s specialized aviation fleet by providing field-level maintenance, special mission equipment sustainment, training, and administrative services. These capabilities ensure that FBI aircraft remain fully mission-ready to meet evolving operational demands.

“This contract underscores V2X’s expertise in delivering agile aviation solutions in support of national security,” said Vinny Caputo, Senior Vice President of Aerospace Systems at V2X. “We are proud to provide the FBI with the aviation resources needed to execute their mission anytime, anywhere—ensuring operational readiness when it matters most.”

The indefinite-delivery, indefinite-quantity contract includes a five-year ordering period, with four 12-month options. V2X will operate at multiple locations across the United States, reinforcing the company’s commitment to delivering agile, global aviation support in service of national security.

About V2X V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,000 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Investor Contact Mike Smith, CFA Vice President, Treasury, Corporate Development and Investor Relations IR@goV2X.com 719-637-5773

Media Contact Angelica Spanos Deoudes Senior Director, Marketing and Communications Angelica.Deoudes@goV2X.com 571-338-5195

Fourth Quarter Revenue of $1.6 Billion with GAAP EPS of $0.36; Adjusted EPS of $0.66

Announced Milestone Agreement with Leading Hospitality Management Company Becoming Key Supplier and Distribution Partner — A Key Step in Expanding Beyond Office Supplies

Launches “Optimize for Growth” Plan to Accelerate Revenue Growth in B2B Industry Segments

BOCA RATON, Fla.–(BUSINESS WIRE)–Feb. 26, 2025– The ODP Corporation (“ODP,” or the “Company”) (NASDAQ:ODP), a leading provider of products, services, and technology solutions to businesses and consumers, today announced results for the fourth quarter and full year ended December 28, 2024.

Fourth Quarter 2024 Summary(1)(3)

Total reported sales of $1.6 billion, down 10% versus the prior year period on a reported basis. The decrease in reported sales is largely related to lower sales in its Office Depot Division, primarily due to 47 fewer retail locations in service compared to the previous year and reduced retail and online consumer traffic, as well as lower sales in its ODP Business Solutions Division

GAAP operating income of $20 million and net income from continuing operations of $11 million, or $0.36 per diluted share, versus $52 million and $39 million, respectively, or $1.02 per diluted share, in the prior year period

Adjusted operating income of $32 million, compared to $57 million in the fourth quarter of 2023; adjusted EBITDA of $58 million, compared to $83 million in the fourth quarter of 2023

Adjusted net income from continuing operations of $20 million, or adjusted diluted earnings per share from continuing operations of $0.66, versus $43 million or $1.13, respectively, in the prior year period

Operating cash flow from continuing operations of $34 million and adjusted free cash flow of $(57) million, versus $71 million and $48 million, respectively, in the prior year period

Repurchased 1.4 million shares at a cost of $43 million in the fourth quarter of 2024

$644 million of total available liquidity including $166 million in cash and cash equivalents at quarter end

Full Year 2024 Summary

Total reported sales of $7.0 billion, versus $7.8 billion in the prior year

GAAP operating income of $163 million and net income from continuing operations of $106 million, or $3.08 per diluted share, versus $330 million and net income from continuing operations of $247 million, or $6.22 per diluted share, respectively, in the prior year

Adjusted operating income of $173 million, compared to $351 million in 2023; adjusted EBITDA of $268 million, compared to $459 million in 2023. Adjusted operating income in 2024 excludes $70 million of income related to legal matter monetization where the Company is engaged in legal proceedings as a plaintiff

Adjusted net income from continuing operations of $114 million, or adjusted diluted earnings per share from continuing operations of $3.30, versus $263 million or $6.61, respectively, in the prior year. Adjusted net income from continuing operations in 2024 excludes $70 million of income or $51 million of income, net of tax related to legal matter monetization where the Company is engaged in legal proceedings as a plaintiff

Operating cash flow from continuing operations of $159 million and adjusted free cash flow of $33 million, versus $360 million and $288 million, respectively in the prior year

Repurchased 8 million shares for $300 million in 2024

“We made significant progress in our B2B pivot during the year, strengthening ODP’s position to drive sustainable profitable growth in the future,” said Gerry Smith, chief executive officer of The ODP Corporation. “Our core strengths in supply chain, procurement, and distribution have continued to provide a meaningful competitive advantage, resulting in recent major new business wins across both our traditional market segments and in new higher-growth industry sectors. Building on our recent success and our core competencies, we are intensifying our focus on the growing potential within the B2B marketplace.”

“We’re now positioned to pursue growth in a new industry segment, recently signing a transformative contract with a major hotel management company that establishes ODP as a preferred supplier in the expanding $16 billion hospitality industry. This landmark agreement is a key step in expanding beyond office supplies and represents a true inflection point in our business, enabling us to strategically expand into growing industry segments where our core competencies resonate. When combined with adjacent industry segments, this represents a compelling $60 billion market opportunity for ODP to showcase its next-day delivery capabilities, exceptional customer service, and extensive national supply chain network to a growing customer base,” Smith continued.

“Our recent progress has the potential to reshape our business trajectory in the future after what has been a challenging period for our industry,” said Smith. “While we achieved our revised guidance for the year, our performance in 2024 was impacted by weak macroeconomic trends, subdued business and consumer activity, and effects from severe weather in the second half of the year. However, we remain competitively strong and, in addition to the landmark hospitality agreement, we continue to secure major new business wins, including signing one of the largest multi-year B2B contracts in our history and successfully launching strategic warehousing and fulfillment services to support one of the world’s leading social media-driven e-commerce platforms.”

“Building on these accomplishments, we are announcing our ‘Optimize for Growth’ plan,” Smith continued. “This plan capitalizes on our core strengths—including a robust B2B infrastructure, supply chain assets, strong distribution network, and loyal customer base—to expand and accelerate growth in the B2B distribution and 3PL market segments while reducing our retail exposure and associated obligations. Supporting our strategy, we are realigning our organization, refining product assortments, and reallocating capital to prioritize growth in the B2B marketplace. At the same time, we will suspend growth investments in our retail segment and continue to optimize our store footprint to better align with our long-term strategy. That said, we remain committed to supporting and providing an exceptional service experience at our active retail locations.”

“As we look ahead to 2025, our strategic priority remains centered on capturing the numerous opportunities in the B2B marketplace and pursuing growth in new industry segments. Although transformational progress takes time to fully materialize and macroeconomic conditions continue to present near-term challenges, we are confident in the strength of our strategy and steadfast in our commitment to delivering sustained, long-term value for our shareholders. We look forward to providing updates on our progress and offering deeper insights into our long-term growth plans in the quarters ahead,” Smith concluded.

Consolidated Results

Reported (GAAP) Results