Net income of $22.8 million; adjusted net income1 of $49.3 million, up 16% year-over-year

Adjusted EBITDA1 of $88.7 million; adjusted EBITDA1 margin of 7.3%

Diluted EPS of $0.72; record adjusted diluted EPS1 of $1.56, up 17% year-over-year

Cash flow from operations of $209.5 million

Full-Year Highlights

Revenue of $4.48 billion, up 4% year-over-year

Net income of $77.9 million; adjusted net income1 of $166.8 million, up 20% year-over-year

Adjusted EBITDA1 of $323.3 million, with a margin of 7.2%

Diluted EPS of $2.45; adjusted diluted EPS1 of $5.24, up 21% year-over-year

Cash flow from operations of $182.0 million

Achieved net debt reduction of $116 million and 2.2x net leverage ratio1

2026 Guidance

Establishing full-year 2026 guidance with 6% revenue and adjusted EBITDA1 growth at mid-point

RESTON, Va., Feb. 23, 2026 /PRNewswire/ — V2X, Inc. (NYSE:VVX) today announced financial results for the fourth quarter and full-year 2025 ended December 31, 2025, and established guidance for full-year 2026.

“V2X ended 2025 with another quarter of strong performance, underscoring our team’s successful execution of our strategy,” said Jeremy C. Wensinger, President and Chief Executive Officer. “We are entering 2026 with significant momentum. Our recent awards and alignment to National Security priorities for readiness and modernization are creating tailwinds for continued growth. Additionally, we are continuing to prioritize investments and expand partnerships to deliver innovative solutions that anticipate and fulfill our customers’ requirements. These growth priorities are further supported by the strength of our capital structure. As we look ahead, V2X is well positioned to continue to deliver readiness enabling solutions to support our customers’ evolving requirements, while generating enhanced value for our shareholders.”

Fourth Quarter 2025 Results

In the fourth quarter, V2X reported record revenue of $1.22 billion, which represents 5% year-over-year growth. The Company reported solid topline growth and strong operating performance, yielding double-digit growth in adjusted net income1 and adjusted EPS1. Net income for the quarter was $22.8 million. Adjusted net income1 was $49.3 million, an increase of $6.6 million dollars, or 16%, year-over-year. Fourth quarter GAAP diluted EPS was $0.72. Adjusted diluted EPS1 for the quarter increased 17% year-over-year to $1.56.

V2X delivered record adjusted EBITDA1 of $88.7 million, with a margin of 7.3%, representing an increase of $2.6 million dollars, or 3%, from the prior year.

Fourth quarter net cash provided by operating activities was $209.5 million. Adjusted net cash provided by operating activities1 increased 3% year-over-year to $172.4 million.

At the end of the fourth quarter, net debt for V2X was $758 million, representing an improvement of $116 million year-over-year and achieving its 2.2x net leverage ratio1.

Total backlog as of December 31, 2025 was $11.1 billion. Funded backlog1 was $2.3 billion. Book-to-bill1 in the quarter was approximately 0.7x.

Full-Year 2025 Results

Full-year revenue was $4.48 billion, representing a 4% increase compared to the previous year.

Net income for the year was $77.9 million. Adjusted net income1 was $166.8 million, an increase of $27.9 million dollars, or 20%, year-over-year. Full-year GAAP diluted EPS was $2.45. Adjusted diluted EPS1 for 2025 was $5.24, increasing 21% year-over-year. Full-year adjusted EBITDA1 was $323.3 million with a margin of 7.2%.

Net cash provided by operating activities in 2025 was $182.0 million. Adjusted net cash provided by operating activities1 was $148.3 million.

2026 Guidance

Expectations for the Company’s full year 2026 financial results are as follows:

$ millions, except for per share amounts

2026 Guidance

2026 Mid-Point

Revenue

$4,675

$4,825

$4,750

Adjusted EBITDA1

$335

$350

$343

Adjusted Diluted Earnings Per Share1

$5.50

$5.90

$5.70

Adjusted Net Cash Provided by Operating Activities1

$150

$170

$160

The Company is not providing a quantitative reconciliation with respect to the foregoing forward-looking non-GAAP measures in reliance on the “unreasonable efforts” exception set forth in SEC rules because certain financial information, the probable significance of which cannot be determined, is not available and cannot be reasonably estimated. For example, unusual, one-time, non-ordinary, or non-recurring costs, which relate to M&A, integration and related activities cannot be reasonably estimated. Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Fourth Quarter Conference Call

Management will conduct a conference call with analysts and investors at 4:30 p.m. ET on Monday, February 23, 2026. U.S.-based participants may dial in to the conference call at 877-300-8521, while international participants may dial 412-317-6026. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/3do4py9pnRx

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through March 9, 2026, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 10195666.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the company’s website at https://gov2x.com. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

___________________________

1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X

V2X builds innovative solutions that integrate physical and digital environments by aligning people, actions, and technology. V2X is embedded in all elements of a critical mission’s lifecycle to enhance readiness, optimize resource management, and boost security. The company provides innovation spanning national security, defense, civilian, and international markets. With a global team of approximately 16,200 professionals, V2X enables mission success by injecting AI and machine learning capabilities to meet today’s toughest challenges across all operational domains.

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management. Forward-looking statements in this press release, include, but are not limited to our future performance and capabilities; all of the statements and items listed under “2026 Guidance” above and other assumptions contained therein for purposes of such guidance; our belief that prior performance provides substantial visibility for future performance; market trends; product development; capital deployment; statements about the benefits and expectations with respect to the strategic acquisition; and our belief that our innovation strategy, visibility, and targeted growth opportunities provide substantial opportunities for value creation.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

CERRITOS, Calif., Feb. 23, 2026 (GLOBE NEWSWIRE) — The Oncology Institute, Inc. (“TOI”) (NASDAQ: TOI), one of the largest value-based oncology groups in the United States, today announced the appointment of Kim Tzoumakas to its Board of Directors, effective February 23, 2026. Ms. Tzoumakas brings more than two decades of executive leadership experience across oncology, pharmacy services and healthcare operations. Notably, she is Chief Executive Officer for VytlOne National Pharmacy Services, and previously held the CEO role at 21st Century Oncology, where she successfully led the organization through a multi-year operational turnaround, culminating in its strategic sale. She also has served on the board of several private and public healthcare companies including SeaSpine, Coherus BioSciences, Ob Hospitalist Group and most recently, VytlOne.

“We are thrilled to welcome Kim to our Board of Directors,” said Daniel Virnich, MD, CEO of The Oncology Institute. “Her deep experience in both oncology and pharmacy services are particularly relevant at this point in TOI’s journey as we expand our care delivery model across employed and MSO networks and grow our pharmacy business. Kim’s proven track record of expanding access, improving cost management, and advancing integrated care delivery models, will be invaluable as to our company and further strengthen our already outstanding board of directors.”

“It’s an honor to have been selected as a Board member of The Oncology Institute,” said Ms. Tzoumakas. “I look forward to utilizing my background and experience in healthcare services to advise this dedicated team and help them accomplish their mission of improving cancer outcomes and streamlining the patient journey.”

About The Oncology Institute (www.theoncologyinstitute.com): Founded in 2007, The Oncology Institute (NASDAQ: TOI) is advancing oncology by delivering highly specialized, value-based cancer care in the community setting. TOI offers cutting-edge, evidence-based cancer care to a population of approximately 1.9 million patients, including clinical trials, transfusions, and other care delivery models traditionally associated with the most advanced care delivery organizations. With over 180 employed and affiliate clinicians and over 100 clinics and affiliate locations of care across five states and growing, TOI is changing oncology for the better.

PDF VersionJoint team will complete preliminary design of the GEK1500 engine to meet high performance and aggressive cost targets, leveraging GEK800 maturation to accelerate delivery

SAN DIEGO, Feb. 23, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, and GE Aerospace (NYSE: GE), today announced a joint U.S. Air Force contract for $12.4M to design a next generation engine for small Collaborative Combat Aircraft (CCA). The initial phase of the program will complete the preliminary design of the GEK1500 engine to meet demanding performance requirements while achieving aggressive cost targets for affordable mass.

Stacey Rock, President of Kratos Turbine Technologies Division, said, “Building on the success of our GEK800 engine program, the development of the GEK1500 further demonstrates our team’s ability and commitment to deliver high-performance, affordable, jet engines that can be rapidly produced to meet the demands of our defense customers.”

“Lessons learned from recent GEK800 altitude testing are directly informing GEK1500 —improving thrust, power generation, and lifecycle cost — so we can meet CCA requirements without compromising affordability or schedule,” said Steve “Doogie” Russell, Vice President and General Manager of Edison Works at GE Aerospace.

The GEK1500 is a 1,500-lb thrust jet engine that could potentially power unmanned aerial systems (UAS), collaborative combat aircraft (CCAs), and missiles. The design of the GEK1500 leverages the GEK800 cruise missile engine architecture which is successfully completing technical maturation. An additional option on the contract, if exercised, would enable the team to assess key design risks and characterize engine performance under relevant flight and installation conditions for the GEK1500 engine. The Air Force has prioritized the development of high performing and low-cost engines to enable the disruptive capabilities of small CCAs.

GEK1500 Engine (Concept Rendition: Kratos and GE Aerospace)

Recent altitude testing of the GEK800 engine demonstrated critical technologies that will provide future systems increased range, increased thrust, decreased life cycle cost, and increased electrical power. The investments and progress made to date on the GEK800 will reduce the cost and schedule timelines for the GEK1500 and provide enhanced performance for small CCAs.

In June, Kratos and GE Aerospace announced the signing of a formal teaming agreement to advance propulsion technologies for the next generation of affordable unmanned aerial systems and CCA-type aircraft, covering the GEK800 and a framework for partnering on additional engines. The result is another formal teaming agreement covering the GEK1500. This collaboration strengthens the companies’ ongoing partnership and builds on a 2024 Memorandum of Understanding (MOU) to advance the development and production of small, cost-effective engines for unmanned platforms. The teaming agreement expanded on that MOU and provided the framework for the two companies to develop, manufacture, test, and field the GEK800 and additional GEK engines in higher thrust classes.

Kratos brings more than 25 years of experience developing and producing small, affordable engines for UAS, drones, and missile platforms. GE Aerospace adds a century of expertise in propulsion technology and the ability to scale advanced designs into high-rate production, helping bridge the gap from prototype to deployment.

About GE Aerospace GE Aerospace is a global aerospace propulsion, services, and systems leader with an installed base of approximately 49,000 commercial and 29,000 military aircraft engines. With a global team of approximately 53,000 employees building on more than a century of innovation and learning, GE Aerospace is committed to inventing the future of flight, lifting people up, and bringing them home safely. Learn more about how GE Aerospace and its partners are defining flight for today, tomorrow and the future at www.geaerospace.com.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

LAKE ZURICH, Ill.–(BUSINESS WIRE)– ACCO Brands Corporation (NYSE: ACCO) today announced that it will release its fourth quarter and full year 2025 earnings before the market opens on March 9, 2026. The Company will host a conference call and webcast to discuss the results on March 9 at 8:30 a.m. EST. The webcast can be accessed through the Investor Relations section of www.accobrands.com and will be available for replay.

About ACCO Brands Corporation

ACCO Brands is the leader in branded consumer products that enable productivity, confidence and enjoyment while working, when learning and while playing. Our widely recognized brands include AT-A-GLANCE®, Five Star®, Kensington®, Leitz®, Mead®, PowerA®, Swingline®, Tilibra® and many others. More information about ACCO Brands Corporation (NYSE: ACCO) can be found at www.accobrands.com.

VIRGINIA CITY, NEVADA, February 23, 2026 – Comstock Inc. (NYSE: LODE) (“Comstock” or the “Company”) and its subsidiary, Comstock Metals LLC (“Comstock Metals”), a leader in the responsible recycling of end-of-life solar panels and the only certified, zero-landfill solar recycling solution in North America, today announced that following the opening of its facility in Kings County, CA, it has received approval from California’s Department of Toxic Substances Control (“DTSC”) and has been placed on a very select list of companies authorized as universal waste recyclers that can treat photovoltaic (“PV”) modules. The recently opened facility in combination with this new “certification” now avails California companies with a true “California solution” for recycling end of life PV solar panels that is authorized by the DTSC and supported by several strategic customers.

This new California facility, and recent certification, marks a regional expansion and optimization of Comstock Metals’ southwestern recycling network, reinforcing the company’s commitment to serving high-demand California-based renewable energy customers. Strategically located to optimize logistics and support customers across California—the single largest end-of-life U.S. solar panel market by far—the site will operate as a centralized hub for the collection, preparation, storage, and aggregation of decommissioned PV solar panels.

As increasing numbers of solar panels reach the end of their useful life across California, Arizona and Nevada, demand is rapidly growing for compliant, environmentally responsible recycling solutions. The California facility is purpose-built to meet this need, providing major utilities, developers, engineering and construction firms (EPCs), installers, decommissioning contractors, and asset owners with a dependable, locally based option for managing these environmental liabilities. Through advanced recovery processes, valuable materials—including aluminum, silver, copper, gallium, and other metals—can eventually be extracted and returned to the supply chain for reuse.

“Opening a facility in California positions us to better serve the region’s increasing demand for end-of-life solar panel disposal while delivering a streamlined, cost-effective logistics solution for our customers,” said Dr. Fortunato Villamagna, President of Comstock Metals. “Our mission is to close the loop on solar energy by ensuring the environmental liabilities associated with these retired panels are safely, cleanly and completed eliminated so they do not find their way into landfills and ultimately, our natural water and broader eco-systems.”

By delivering timely, efficient, and fully compliant decommissioning, transportation, and recycling services, Comstock’s zero-landfill solution minimizes waste, preserves natural resources, and advances the long-term sustainability of the solar industry. The Company is also completing permit applications and preparing submission plans for a second, integrated, industry-scale facility in Nevada, with final site selection expected later this month.

“As the number of end-of-life solar panels nationwide rises into the tens and eventually hundreds of millions, our ability to scale responsibly and efficiently ensures meaningful sustainability outcomes—and confidence—for our customers and partners,” said Corrado De Gasperis, Executive Chairman and CEO of Comstock. “Our team is establishing a new benchmark for solar panel recycling through a growing, fully integrated national network.”

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 ir@comstockinc.com

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 media@comstockinc.com

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “forecast,” “seek,” “target,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: expectations regarding the completion of the proposed securities offering, future market conditions; future explorations or acquisitions, divestitures, spin-offs or similar distribution transactions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: sales of, and demand for, our products, services, and/or properties; industry market conditions, including the volatility and uncertainty of commodity prices; the speculative nature, costs, regulatory requirements, and hazards of natural waste resource identification, exploration, development, availability, recycling, extraction, processing, and refining activities, including operational or technical difficulties, and risks of diminishing quantities or insufficiency of grades of qualified resources;; changes in our planning, exploration, research and development, production, and operating activities; research and development, exploration, production, operating, and other variable and fixed costs; throughput rates, margins, earnings, debt levels, contingencies, taxes, capital expenditures, net cash flows, and growth; restructuring activities, including the nature and timing of restructuring charges and the impact thereof; employment and contributions of personnel, including our reliance on key management personnel; the costs and risks associated with developing new technologies; our ability to commercialize existing and new technologies; the impact of new, emerging, and competing technologies on our business; the possibility of one or more of the markets in which we compete being impacted by political, legal, and regulatory changes, or other external factors over which we have little or no control; the effects of mergers, consolidations, and unexpected announcements or developments from others; the impact of laws and regulations, including permitting and remediation requirements and costs; changes in or elimination of laws, regulations, tariffs, trade, or other controls or enforcement practices, including the potential that we may not be able to comply with applicable regulations; changes in generally accepted accounting principles; adverse effects of climate changes, natural disasters, and health epidemics, such as the COVID-19 outbreak; global economic and market uncertainties, changes in monetary or fiscal policies or regulations, the impact of terrorism and geopolitical events, volatility in commodity and/or other market prices, and interruptions in delivery of critical supplies, equipment and/or raw materials; assertion of claims, lawsuits, and proceedings against us; potential inability to satisfy debt and lease obligations, including because of limitations and restrictions contained in the instruments and agreements governing our indebtedness; our ability to raise additional capital and secure additional financing; interruptions in our production capabilities due to equipment failures or capital constraints; potential dilution from stock issuances, recapitalization, and balance sheet restructuring activities; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to maintain the listing of our securities on any securities exchange or market; and our ability to implement additional financial and management controls, reporting systems and procedures and comply with Section 404 of the Sarbanes-Oxley Act, as amended. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

After-tax NPV (using 8% discount rate) of $4.01 billion based on price assumptions of $24,000 per tonne (“/t”) for lithium carbonate (“Li2CO3”) and $750/dry metric tonne (“dmt”) for Sodium Hydroxide (“NaOH”)

After-tax internal rate of return (“IRR”) of 27.4%

Integrated patent-pending processing flowsheet, incorporating hydrochloric acid leaching, Direct Lithium Extraction (“DLE”), chlor-alkali processing, and on-site production of battery-grade lithium carbonate, validated through four years of pilot plant operations in Nevada

Large, long-life U.S.-based lithium development project, with Proven and Probable Reserves supporting a mine life exceeding 60 years

Economic analysis based on a 40-year production schedule, with planned life-of-mine average production of approximately 26,500 tonnes per annum (“tpa”) of battery-grade lithium carbonate

Initial Phase 1 throughput of 7,500 tonnes per day (“tpd”), expanding to 15,000 tpd in Year 5 (Phase 2)

Capital and Operating Costs

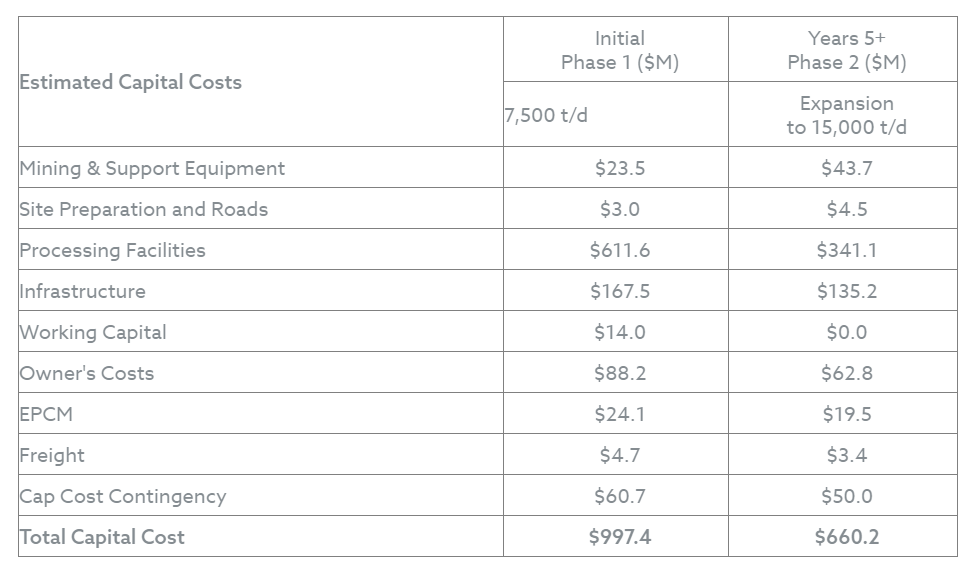

Phase I capital cost of $997 million compared to $1.537 billion in the 2024 Study

Phase 2 expansion capital of $660 million compared to $651 million in the 2024 Study

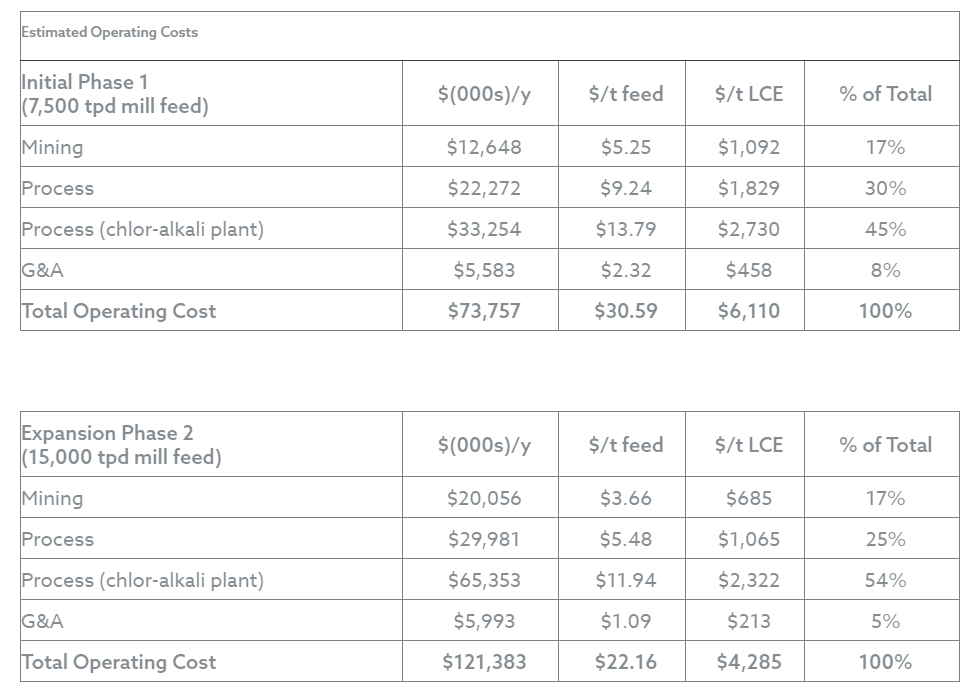

Average operating cost of $22.45 per tonne of mill feed, equivalent to $4,389 per tonne of lithium carbonate, compared to $8,223 per tonne in the 2024 Study

Project revenues from surplus sodium hydroxide equivalent to $5,393/t of lithium carbonate produced. When treated as a co-product credit, this would result in a net operating cost below zero

Mineral Resource and Reserve

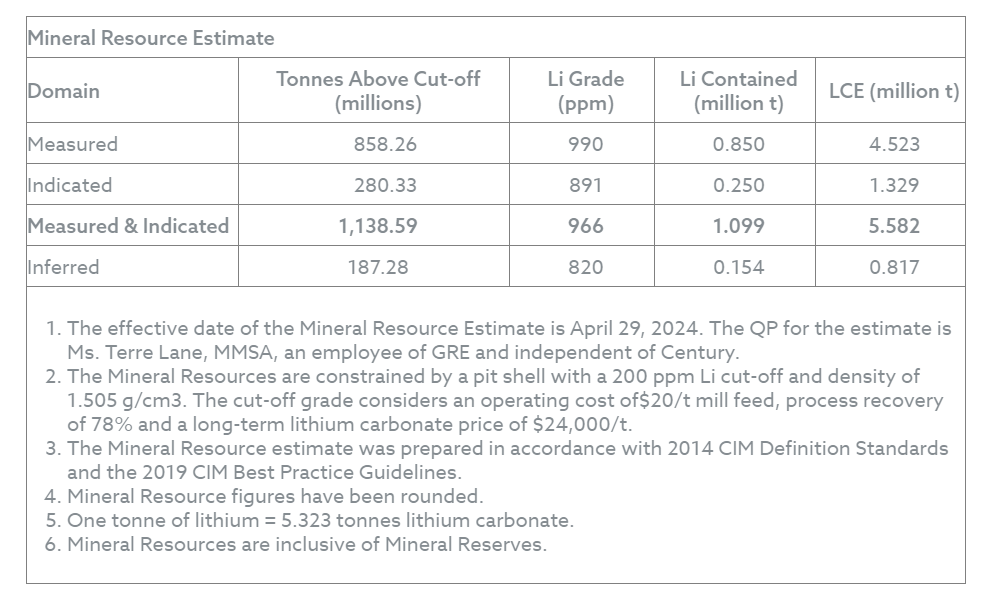

Measured and Indicated Mineral Resources of 1.138 billion tonnes at 966 parts per million (“ppm”) lithium, containing 5.582 million tonnes lithium carbonate equivalent (“LCE”)

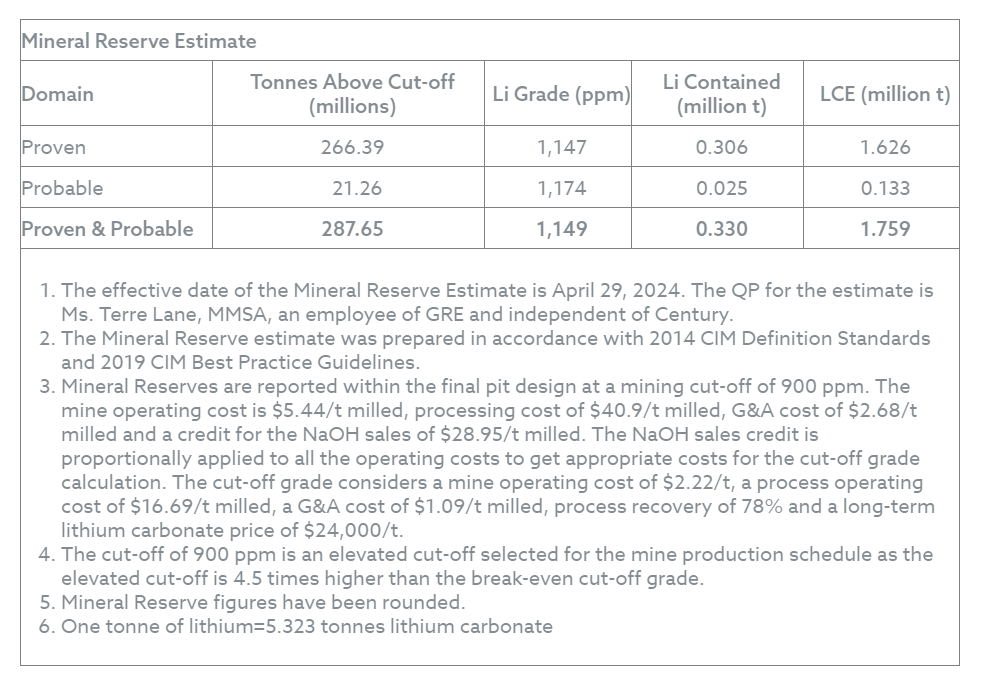

Proven and Probable Mineral Reserves of 287.65 million tonnes at 1,149 ppm lithium, containing 1.759 million tonnes LCE

February 23, 2026 – Vancouver, Canada – Century Lithium Corp. (TSXV: LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or “the Company”) is pleased to announce the results of an updated National Instrument 43-101 (“NI 43-101”) compliant Feasibility Study (“2026 Feasibility Study”) for its 100%-owned Angel Island Lithium Project (“Angel Island”) located in Esmeralda County, Nevada, USA.

The 2026 Feasibility Study incorporates the results of continued metallurgical testing, engineering optimization, refinement of the mine plan, and updated capital and operating cost estimates for Angel Island. The study demonstrates strong project economics, including an after-tax net present value (“NPV”) of $4.01 billion.

No material changes were made to the Mineral Resource or Mineral Reserve estimates used in the “NI 43-101 Technical Report on the Feasibility Study of the Clayton Valley Lithium Project, Esmeralda County, Nevada, USA”, dated April 29, 2024 (“2024 Study”) and are used in their entirety in the 2026 Feasibility Study.

All currency amounts in this news release are expressed in U.S. dollars.

2026 FEASIBILITY STUDY SUMMARY

The 2026 Feasibility Study confirms the technical and economic viability of developing the Angel Island project as a significant domestic source of battery-grade lithium carbonate in the United States.

Mining is planned as a conventional open-pit operation extracting lithium-bearing claystone mineralization. Mined material will be processed on-site using hydrochloric acid leaching, solid-liquid separation, Direct Lithium Extraction (“DLE”), lithium carbonate precipitation, and an integrated chlor-alkali plant, resulting in on-site production of battery-grade lithium carbonate.

The 2026 Feasibility Study reconfigures Angel Island into a two-phase development plan, consisting of an initial 7,500 tpd operation with expansion to 15,000 tpd. The third expansion phase contemplated in the 2024 Study was removed, simplifying project execution and reducing overall capital requirements.

Bill Willoughby, President and CEO of Century Lithium commented:

“The results of the 2026 Feasibility Study represent a material improvement. These results were made possible by Century Lithium’s team who, through many steps of optimization including those at the Company’s pilot plant, have delivered a more efficient development plan for the Project. In the 2026 Feasibility Study, this streamlined process is reflected in equipment and related infrastructure, importantly in electrical demand, and is seen in the resulting capital and operating cost estimates.”

CAPITAL AND OPERATING COSTS

A Class 3 capital cost estimate was prepared in accordance with AACE guidelines, and Canadian Institute of Mining Metallurgy and Petroleum (“CIM”) Best Practices. The updated costs were developed using second-quarter 2025 data.

Phase 1 (7,500 tpd) initial capital cost: $997 million

Phase 2 (15,000 tpd) expansion capital cost: $660 million

Reductions to estimated capital costs in the 2026 Feasibility Study relative to the 2024 Study are attributable to:

Elimination of a previously planned third production phase

Simplification of project scope and installed capacity

Refinement of the mine scheduling and equipment selection

Processing flowsheet optimization informed by pilot plant operations

Updated vendor pricing and construction cost inputs

Operating costs benefit materially from Angel Island’s planned vertically integrated chlor-alkali facility, which generates hydrochloric acid and produces surplus sodium hydroxide for sale.

Average operating cost – Phase 1: estimated $30.58/t of mill feed

Average operating cost – Phase 2: estimated $22.16/t of mill feed

MINERAL RESOURCES AND MINERAL RESERVES

Mineral Resource and Mineral Reserve estimates used in the 2026 Feasibility Study are unchanged from the prepared in accordance with NI 43-101 and CIM Definition Standards.

Mineral Resources (inclusive of Mineral Reserves):

Measured and Indicated: 1.138 billion tonnes at 966 ppm lithium, containing 5.582 million tonnes LCE

Inferred: 187.28 million tonnes at 820 ppm lithium

Mineral Reserves:

Proven and Probable: 287.65 million tonnes at 1,149 ppm lithium, containing 1.759 million tonnes LCE

Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability

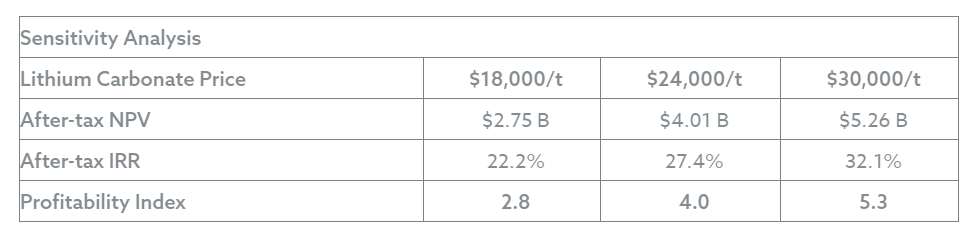

ECONOMIC ANALYSIS indicates Angel Island remains economically attractive across a wide range of commodity price and cost assumptions, with lithium price representing the most significant driver of Angel Island’s value.

Using a base-case lithium carbonate price of $24,000/t and an 8% discount rate, Angel Island generates:

After-tax NPV: $4.01 billion

After-tax IRR: 27.4%

Profitability Index: 4.0

Sensitivity analysis indicates Angel Island remains economically attractive across a wide range of commodity price and cost assumptions, with lithium price representing the most significant driver of Angel Island’s value.

NEXT STEPS

Century Lithium will continue to advance Angel Island toward development through submission of plan of operations, permitting, detailed engineering, and engagement with interested parties as the Project progresses toward a construction decision. Integral to these key steps are:

Recent appointment of Cormac O’Laoire, PhD to advise the Company in discussions with potential downstream partners and offtake interests. The Company continues to make inroads in Washington DC and Nevada to convey the importance of Angel Island for a secure North American supply chain.

Further evaluation of the economic potential for rare earth elements (“REE”) recovery at Angel Island.

Engagement of BMO Capital Markets to assist the Company in its efforts towards securing strategic interests and development funding.

Addition, in 2025 to the US Federal Permitting Dashboard for FAST-41 transparency status. Inclusion to FAST-41 increases the Project’s exposure to federal agencies and stakeholders to accelerate the permitting process.

SUMMARY OF 2026 NI 43-101 FEASIBILITY STUDY

This summary forms an integral part of this news release.

An NI 43-101 Feasibility Study on the Angel Island Lithium Project was prepared to update metallurgical results, mine planning assumptions, and capital and operating cost estimates relative to the 2024 Study.

Unless otherwise stated herein, Mineral Resource and Mineral Reserve estimates, geological interpretations, and environmental and permitting assumptions remain materially unchanged from the 2024 Study.

Property Description, Location, and Tenure

Angel Island is located in Esmeralda County, Nevada, USA, approximately 354 km southeast of Reno. Angel Island comprises 503 unpatented mining claims (276 placer and 227 lode claims) covering approximately 2,286 hectares, held 100% by Cypress Holdings (Nevada) Ltd., a wholly owned subsidiary of Century Lithium Corp. Existing royalty arrangements remain unchanged.

Geology, Mineralization, and Deposit Type

Angel Island hosts a large, flat-lying sedimentary lithium claystone deposit within the Esmeralda Formation. Lithium mineralization occurs primarily within claystone, tuffaceous mudstone, and siltstone units. No material changes were made to the geological model, mineralization interpretation, or deposit classification from the 2024 Study.

Exploration, Drilling, Sampling, and Data Verification

The Mineral Resource and Mineral Reserve estimates are supported by 45 drill holes totaling approximately 3,955 meters, completed between 2017 and 2022. Drilling includes conventional core and sonic drilling. Sample preparation, analytical methods, QA/QC protocols, and data verification procedures remain unchanged from the 2024 Study and meet CIM and NI 43-101 standards.

Mineral Resource Estimate (Unchanged from 2024 Study)

The Mineral Resource estimate has an effective date of April 29, 2024, and remains unchanged in the 2026 Feasibility Study.

Measured and Indicated Mineral Resources:

1.138 billion tonnes at an average grade of 966 ppm lithium, containing 5.582 million tonnes LCE

Inferred Mineral Resources:

187.28 million tonnes at an average grade of 820 ppm lithium, containing 0.817 million tonnes LCE

Mineral Resources are constrained by a pit shell using a 200 ppm lithium cut-off grade and assume a bulk density of approximately 1.5 tonnes per cubic meter (“t/m³”). Mineral Resources are inclusive of Mineral Reserves. Higher recoveries demonstrated through pilot-scale testing were determined to not materially affect the selected cut-off grade or the reported Mineral Resource tonnage or grade.

Mineral Reserve Estimate (Unchanged from 2024 Study)

The Mineral Reserve estimate also has an effective date of April 29, 2024, and remains unchanged.

Proven and Probable Mineral Reserves:

287.65 million tonnes at an average grade of 1,149 ppm lithium, containing 1.759 million tonnes LCE

Mineral Reserves are reported at a 900 ppm lithium cut-off grade, which is approximately 4.5 times the calculated break-even cut-off grade, and support a mine life exceeding 60 years, with a 40-year production schedule used in the economic analysis.

Mining Methods and Production Schedule

Mining will be conducted as a conventional open-pit operation using free-digging equipment, including dozers, shovels, and haul trucks. No drilling or blasting is required.

The mine plan reflects a two-phase development strategy:

Phase 1: 7,500 tpd of mill feed

Phase 2: expansion to 15,000 tpd

A previously planned third expansion phase was eliminated. The production schedule prioritizes near-surface, higher-grade mineralization in the early years, reducing waste movement and improving capital efficiency.

Mineral Processing and Metallurgy

The processing flowsheet consists of:

High-pH attrition scrubbing

Hydrochloric acid leaching

Neutralization and pressure filtration with dry-stack tailings

Direct Lithium Extraction

Lithium carbonate precipitation, drying, and packaging

Reagent generation via on-site chlor-alkali plant

Metallurgical assumptions are supported by multi-year pilot plant operations through mid-2025. Leach extraction of approximately 90% was demonstrated, resulting in an overall lithium recovery of approximately 84%. A final lithium carbonate product grading >99.9% purity was consistently achieved.

Angel Island facilities include an integrated chlor-alkali plant producing hydrochloric acid and sodium hydroxide. Surplus sodium hydroxide, as produced in excess in conjunction with the design production of hydrochloric acid, is expected to be sold, contributing substantial additional revenue and thereby reducing effective operating cost.

Capital Costs

A Class 3 capital cost estimate was prepared in accordance with AACE International guidelines. The updated costs were developed using second-quarter 2025 data:

Phase 1 (7,500 tpd) initial capital cost: estimated $997.4 million

Phase 2 (15,000 tpd) expansion capital cost: estimated $660.2 million

Reductions to estimated capital costs relative to the 2024 Study are attributable to the elimination of a third production phase, simplification of installed capacity, processing flowsheet optimization, and updated vendor and construction cost inputs.

The chlor-alkali plant cost is $481.5 million in Phase 1 and $256.8 million in Phase 2, included in Processing Facilities, and is vendor all-in turn-key constructed costs, inclusive of indirect costs, owners’ costs and contingency.

Operating Costs

Average operating cost estimates were updated based on refined mine scheduling, updated reagent consumption, and pilot-validated process parameters.

Average operating cost: approximately $22.45/t of mill feed, or $4,389/t of lithium carbonate.

Sodium hydroxide by-product revenue is equivalent to $5,393/t of lithium carbonate. If credited against operating costs (which was not done in the average operating cost above), base operating costs would be negative.

Economic Analysis

The economic analysis of Angel Island was done using a discounted cash flow (“DCF”) model using only the first 40 years of project life. Cash flows in the model were based on second-quarter 2025 U.S. dollars with no escalation of costs or revenues. The DCF model uses a base-case discount rate of 8%. Financing costs were excluded from the valuation.

The analysis includes generating gross sales from lithium carbonate and sodium hydroxide, before-tax cash flow, which is gross sales minus operating costs, and after-tax cash flow, which is before-tax cash flow minus taxes and capital costs. The NPV and IRR were calculated from the DCF.

The economic analysis uses a base-case lithium carbonate price of $24,000/t and an 8% discount rate.

After-tax NPV: $4.01 billion

After-tax IRR: 27.4%

Profitability Index: 4.0

Sensitivity to Lithium Carbonate Price

Sensitivity analyses demonstrate Angel Island economics are most sensitive to lithium price and remain robust across a wide range of cost and price assumptions.

Environmental, Permitting, and Social Considerations

Baseline environmental studies are complete. Permitting is expected to proceed under the National Environmental Policy Act (“NEPA”) through the US Bureau of Land Management. Angel Island is currently in the permitting stage, with no material changes to the permitting pathway outlined in the 2024 Study.

Interpretation and Conclusions

The 2026 Feasibility Study concludes that the Angel Island project is technically and economically viable, with improved capital efficiency, reduced execution risk, and robust long-term economics. The simplified two-phase development plan, extensive metallurgical validation, and integrated chlor-alkali process support Angel Island’s competitiveness as a domestic US. source of battery-grade lithium carbonate.

In addition, the integrated chlor-alkali process also provides environmental and operational advantages relative to sulfuric acid-based systems, including on-site reagent production.

Recommendations

Work recommended to advance Angel Island and continue project development is as follows:

A Plan of Operations (“PoO”) should be completed and filed with the BLM to initiate the National Environmental Policy Act (“NEPA”) process; and begin the permitting process with the State of Nevada to work concurrently with the federal process.

Additional geotechnical data should be collected to supplement the existing characterization data and further support the tailings storage facility (TSF) design and foundation, foundation infrastructure requirements for the processing plant, and traffic management and load bearing capacity of materials in the pit during mining.

Additional pilot testing should be completed on deeper material from claystone zones 1 and 2 collected previously, to further confirm the metallurgy of these materials.

Infrastructure work should be completed as follows: 1) initiate preliminary engineering studies with NV Energy for the interconnection of the Project to the electrical grid, 2) define a water source for the Project with a drilling program using piezometers and other pumping tests to be developed under the Company’s water rights permit, and 3) locate local sources of barrow material for construction use at the Project.

Detailed engineering should begin when the NEPA process commences and be completed in appropriate phases to develop the Project design to a level sufficient to support procurement, construction planning, and financing.

A supplemental infill drilling program is recommended, though not required, with the following goals: 1) collect additional data for the Project’s Phase 1 economic and mining models, 2) material for additional density test work, and 3) material for geotechnical test work.

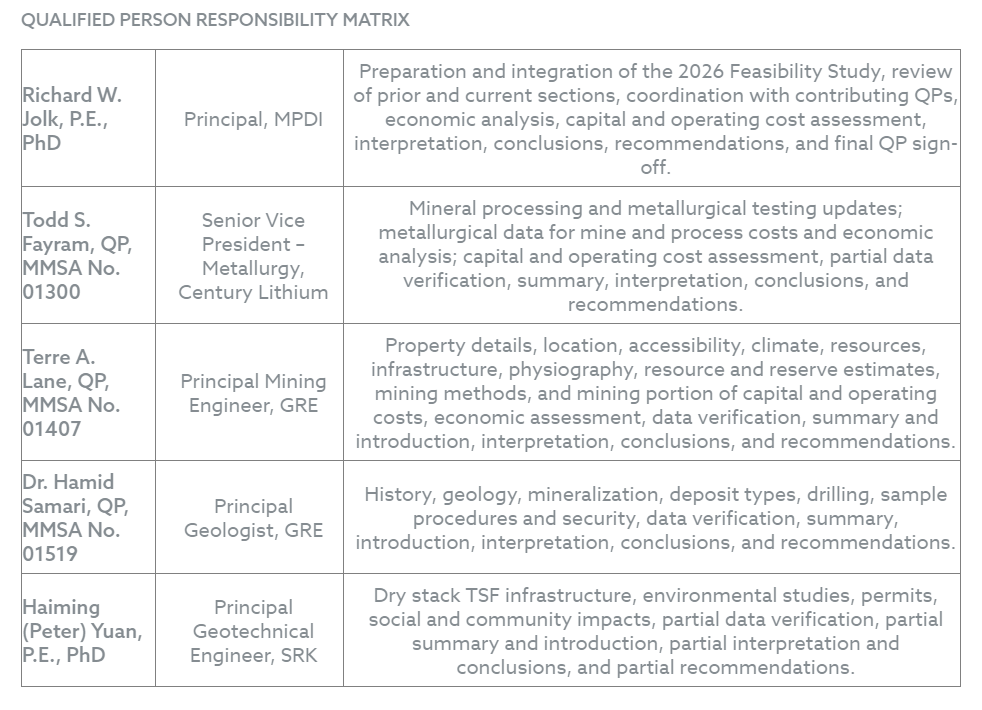

QUALIFIED PERSON

The technical information contained in this news release has been reviewed and approved by Richard W. Jolk, P.E., an independent Qualified Person as defined under National Instrument 43-101.

Further information about Angel Island, including a description of the key assumptions, parameters, description of sampling methods, data verification and quality assurance/quality control programs, methods relating to Mineral Resources and Mineral Reserves and factors that may affect those estimates will be contained in a NI 43-101 Technical Report on the Feasibility Study of the Angel Island Lithium Project. Following Section 3.4 of NI 43-101 the report will be available on SEDAR+ and on the Company’s website within 45 days of the date of this news release.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced-stage lithium development company focused on its 100%-owned Angel Island lithium project in Esmeralda County, Nevada. Angel Island hosts one of the largest known sedimentary lithium deposits in the United States and is designed with an integrated, end-to-end process for the on-site production of battery-grade lithium carbonate to support the electric vehicle and battery storage markets.

The Company has developed a patent-pending process that incorporates hydrochloric acid leaching combined with direct lithium extraction to produce battery-grade lithium carbonate. As part of the integrated chlor-alkali process, Angel Island is designed to produce sodium hydroxide as a co-product, with planned surplus sales expected to lower operating costs, reduce reliance on externally sourced reagents, and minimize environmental impacts.

The Angel Island Project is currently advancing through the permitting process.

Century Lithium trades on the TSX Venture Exchange under the symbol “LCE” the OTCQX under the symbol “CYDVF”, and on the Frankfurt Stock Exchange under the symbol “C1Z”.

WILLIAM WILLOUGHBY, PhD., PE President & Chief Executive Officer For further information, please contact: Spiros Cacos | Vice President, Investor Relations Direct: +1 604 764 1851 Toll Free: 1 800 567 8181 scacos@centurylithium.com centurylithium.com

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition. In a 424B3 filing, Kratos disclosed that it acquired Nomad Global Communication Solutions, Incorporated, for an initial amount of 972,136 KTOS shares or approximately $100 million. Nomad provides mobile command, control, and communications systems for space and satellite systems, UAVs, counter UAVs, and other systems, with clients including all branches of the U.S. armed forces, Homeland Security, and other Agencies, among others. We expect management to provide additional detail and color on the earnings call.

Drone Dominance. Kratos has been selected to participate in the initial Phase 1 Gauntlet for the Office of the Secretary of War’s Drone Dominance Program. This opportunity seeks to identify and evaluate platforms capable of demonstrating multiple one-way attack missions through a live competition. Upon successful completion of the Gauntlet, participants will be ranked and extended a prototype delivery award based on their performance and placement. The Drone Dominance Program represents a $1.1 billion investment in groundbreaking unmanned systems technologies. The program aims to procure approximately 350,000 units.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and full year results. EuroDry reported fourth-quarter net revenues of $17.4 million, exceeding our estimate of $16.5 million, driven by a stronger average TCE rate of $16,262 per day versus our $15,900 estimate and lighter drydocking of 13.7 days against our 22-day assumption. Adjusted EBITDA of $7.5 million and adjusted EPS of $0.88 came in ahead of our estimates of $6.7 million and $0.78, respectively. For the full year, net revenues of $52.3 million, adjusted EBITDA of $12.5 million, and an adjusted net loss of $2.50 per share all modestly surpassed our estimates of $51.4 million, $11.7 million, and a loss of $2.57.

Market update. Dry-bulk fundamentals strengthened in the fourth quarter, with average TCE rates rising to the highest levels in approximately two years. The global order book remains near historically low levels, at approximately 13.4% of the existing fleet, providing structural support. Near-term demand tailwinds include growing bauxite trade from West Africa, continued grain flows following the U.S.–China trade truce, and longer voyage distances due to Red Sea disruptions, though geopolitical uncertainty and tariff-related volatility remain risks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Tidewater Inc. (NYSE: TDW) is expanding its global offshore footprint with a $500 million all-cash acquisition of Wilson Sons Ultratug Participações S.A. and its affiliate Atlantic Offshore Services S.A. (collectively, “WSUT”). The transaction, which includes the assumption of approximately $261 million in existing debt, significantly scales Tidewater’s presence in Brazil—one of the world’s most active offshore energy markets.

The deal adds 22 platform supply vessels (PSVs) to Tidewater’s fleet. Pro forma for the acquisition, Tidewater will own 213 offshore support vessels (OSVs) and 231 total vessels globally, including crew boats, tug boats, and maintenance vessels.

The most immediate impact is geographic. Tidewater’s fleet in Brazil will expand from six vessels to 28, creating meaningful operating scale in a market widely viewed as structurally attractive due to sustained offshore development activity.

Notably, 19 of WSUT’s 22 PSVs are Brazilian-built. That distinction carries strategic weight. Brazilian-built vessels receive priority in local tenders and also provide access to Brazilian Special Registry (REB) tonnage rights. Through REB, Tidewater may import certain international-flagged vessels into Brazil while enjoying similar status to locally built ships.

In effect, the transaction provides both domestic positioning and optionality for additional fleet deployment.

WSUT brings approximately $441 million in existing backlog. According to Tidewater, many of those contracts are priced at day rates below current market levels, creating potential earnings leverage as contracts roll over.

Assuming a late second-quarter 2026 close, Tidewater expects the acquired business to generate roughly $220 million in revenue over the first twelve months, with gross margins around 58%. Annual G&A expenses are projected at approximately $14 million.

Management also characterized the deal as immediately accretive to 2026 and 2027 estimated earnings and free cash flow per share, though final outcomes will depend on closing timing, integration, and market conditions.

The acquisition will be funded with cash on hand. Tidewater intends to novate WSUT’s existing long-duration amortizing debt, provided by BNDES and Banco do Brasil, preserving what management describes as low-cost financing already embedded in the capital structure.

Following refinancing transactions in 2025 and this acquisition, Tidewater expects pro forma net leverage below 1.0x at closing, assuming a June 30, 2026 completion. A lower leverage profile could provide flexibility for future capital allocation decisions, subject to market conditions.

Brazil’s offshore sector remains one of the largest globally, with sustained activity in deepwater and pre-salt developments. Vessel supply dynamics, local content requirements, and regulatory structures create a market where scale and local tonnage matter.

For investors tracking the offshore services cycle, this transaction underscores a broader theme: operators are positioning for sustained utilization and disciplined fleet growth rather than speculative expansion. Consolidation also remains a key lever for improving operating leverage in a capital-intensive industry.

The transaction has been unanimously approved by Tidewater’s board and is expected to close late in the second quarter of 2026, pending regulatory approvals, including from Brazil’s antitrust authority (CADE).

As the offshore support vessel market continues to recalibrate following years of volatility, Tidewater’s Brazil-focused expansion signals confidence in long-term regional fundamentals—while also highlighting how capital structure discipline is shaping today’s consolidation playbook.

The US trade landscape shifted abruptly Friday after the Supreme Court struck down the centerpiece of President Trump’s second-term tariff program, ruling 6–3 that the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose sweeping blanket tariffs. The decision immediately halts a massive portion of the tariffs announced last year on “Liberation Day,” dealing a significant blow to the administration’s trade strategy and sending stocks higher as investors recalibrated expectations for costs, inflation, and corporate margins.

“IEEPA does not authorize the President to impose tariffs,” Chief Justice John Roberts wrote in the majority opinion, rejecting the administration’s claim that the 1977 law granted broad authority to impose tariffs under a declared economic emergency. Roberts added that had Congress intended to grant such extraordinary tariff powers, it would have done so explicitly. The ruling upholds prior lower court decisions, including from the US Court of International Trade, that found the tariffs unlawful under that statute.

Markets responded swiftly. According to analysis from the Yale Budget Lab, the effective US tariff rate could now fall to 9.1%, down from 16.9% before the ruling. Investors interpreted the decision as reducing near-term cost pressures for companies that rely on imported goods and components. President Trump, however, quickly pushed back, calling the ruling “deeply disappointing” and criticizing members of the Court. Within hours, he announced plans to impose a 10% “global tariff” under Section 122 of the Trade Act of 1974, a provision that allows temporary tariffs of up to 15% for 150 days to address trade deficits. That authority has never previously been used to implement tariffs of this scale, and the administration signaled additional trade investigations under Section 301 may follow.

Notably, tariffs enacted under other legal authorities remain in place. Section 232 national security tariffs on steel, aluminum, semiconductors, and automobiles are unaffected, meaning a range of sector-specific import duties will continue. This layered approach underscores that while the Court invalidated one mechanism, trade tensions and tariff policy remain firmly in play.

An unresolved issue now looms over potential refunds. More than $100 billion — and possibly as much as $175 billion — in tariff revenue has been collected under IEEPA. The Court did not directly address refund eligibility, opening the door to further litigation and administrative action. Business groups, including the US Chamber of Commerce, are calling for swift refunds, arguing that repayment would meaningfully support small businesses and importers. Others caution that returning such sums could carry serious fiscal implications.

For small- and micro-cap investors, the ruling introduces both relief and renewed uncertainty. Smaller companies often operate with thinner margins and less pricing power than large multinational peers, making them particularly sensitive to import costs. A lower effective tariff rate could ease pressure on retailers, specialty manufacturers, and niche industrial firms that rely heavily on overseas inputs. At the same time, policy volatility remains elevated as the administration pivots to alternative tariff authorities, suggesting the trade environment may remain fluid.

The broader macro implications are equally significant. Reduced tariff pressure could temper inflation expectations, potentially influencing Federal Reserve policy — a key driver for small-cap performance given their sensitivity to financing conditions and domestic economic momentum.

Friday’s decision marks a major legal setback for the administration’s trade framework, but it does not signal an end to tariff-driven policy shifts. For small-cap investors, the near-term narrative may improve on cost relief, yet the longer-term trade outlook remains unsettled as Washington prepares its next move.

The US economy ended 2025 on a weaker-than-expected note.

New data from the Bureau of Economic Analysis showed GDP grew at an annualized rate of just 1.4% in the fourth quarter, well below economist expectations for 2.9% growth. The miss marks a notable slowdown from earlier in the year and caps full-year 2025 growth at 2.2%, down from 2.8% in 2024.

A key culprit: government spending.

Federal outlays fell sharply during the quarter, reflecting the impact of the 43-day government shutdown that spanned October and November. Overall government spending declined at a 5.1% annualized rate, subtracting 0.9 percentage points from headline GDP. Federal spending alone plunged 16.6%, shaving 1.15 percentage points off growth.

President Trump, posting on Truth Social ahead of the release, argued the shutdown cost the economy “at least two points in GDP” and renewed calls for lower interest rates.

Under the Surface: Not All Weakness

Despite the headline disappointment, underlying private-sector demand remained more resilient.

Real final sales to private domestic purchasers — a key gauge of core demand — rose 2.4%, only slightly below the prior quarter’s 2.9% pace. Private fixed investment increased 2.6%, supported by continued spending on intellectual property and information processing equipment.

The AI build-out remains a meaningful contributor to growth. Spending on information processing equipment added 0.65 percentage points to GDP in the quarter, while investment in intellectual property products rose at a 7.4% pace.

However, consumer behavior showed signs of divergence. Services spending grew 3.4%, while goods spending fell 0.1%, underscoring a continued rotation away from physical goods.

What This Means for Small-Cap Stocks

For small- and micro-cap investors, the implications are layered.

First, government spending volatility tends to disproportionately impact smaller companies with federal exposure. Contractors, niche defense suppliers, and specialized service providers may have felt the brunt of delayed payments or paused contracts during the shutdown.

Second, slower headline GDP growth can pressure investor sentiment toward riskier asset classes — and small caps often sit at the front of that risk spectrum. The Russell 2000 historically reacts more sharply to growth scares than large-cap indices.

But there’s another side.

If economists are correct that shutdown-related drag reverses in the first quarter — with some forecasts calling for 3% growth in early 2026 — small caps could benefit from a rebound narrative. Lower rates, which the administration continues to push for, would also ease capital constraints for smaller companies that rely more heavily on credit markets.

And the ongoing AI investment cycle may continue to support smaller industrial, semiconductor-adjacent, and specialty tech names tied to infrastructure build-outs.

Bottom Line

The Q4 GDP miss highlights how policy disruptions can ripple through the broader economy. While headline growth slowed, core private demand and investment remain intact.

For small-cap investors, volatility may persist in the near term — but a rebound in government activity and continued capital investment could shift the narrative quickly in early 2026.

Travelzoo® provides its 30 million members with exclusive offers and one-of-a-kind experiences personally reviewed by our deal experts around the globe. We have our finger on the pulse of outstanding travel, entertainment, and lifestyle experiences. We work in partnership with more than 5,000 top travel suppliers—our long-standing relationships give Travelzoo members access to irresistible deals.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Softer than expected Q4 Results. The company reported Q4 revenue of $22.5 million, an increase of 9%, and adj. EBITDA of $1.0 million, both of which were below our estimates of $23.0 million and $3.3 million, respectively. Importantly, the modestly softer than expected results were largely driven by weakness in advertising and commerce revenue. Increased marketing spend and elevated G&A expenses due to a non-recurring corporate event adversely affected EBITDA.

Customer acquisition efficiency. Customer acquisition costs averaged $34 per member in Q4, compared to $28 in Q1, $38 in Q2, and $40 in Q3, reflecting continued investment in subscriber growth. Management highlighted rapid payback economics, with annual membership fees collected upfront and supplemented by transaction revenue. Acquisition costs are expensed immediately, impacting near-term profitability, though the strategy is intended to expand recurring revenue and strengthen the advertising platform over time.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

CDI-988 Data Selected For Presentation At ICAR. Cocrystal announced that it has been selected to present data from its Phase 1 clinical trial and updates from the ongoing Phase 1b challenge study testing CDI-988 against norovirus infection at the 38th International Conference on Antiviral Research, to be held April 27 to May 1 in Prague, Czech Republic. We see the presentation at this important conference as recognition of the potential of CDI-988 for an indication that has serious medical and economic consequences.

Phase 1 and 1b Data Expected. We expect Dr. Sam Lee, President and Co-CEO, to present initial Phase 1 safety and tolerability data. Previously announced data from the single ascending dose (SAD) and multiple ascending dose (MAD) study showed safety and tolerability across all dose cohorts tested. Additional data from the ongoing Phase 1b norovirus challenge study testing CDI-988 as both a prophylactic and therapeutic may also be included.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.