Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updating estimates. While we are maintaining our 2025 rail car delivery estimate of 4,710, we have lowered our second quarter expectations to 850 from 950 and increased our third quarter estimate to 1,790 from 1,690. Our 2025 EBITDA and EPS estimates are unchanged at $45.9 million, and $0.47, respectively. However, our second and third quarter EPS estimates are $0.06 and $0.20, respectively, compared to our prior estimates of $0.07 and $0.19.

Flexible production schedule. With FreightCar’s asset-based lending facility, the company has greater flexibility to manage its production schedule, given that it can borrow against inventory. The company has the ability to produce rail cars associated with firm orders and hold them for delivery to suit customer needs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Bolsters its southern operations. On June 11, the company announced that it had acquired the assets of Pelicoin, a crypto ATM company with operations in the Gulf South (particularly MS, AL, TX, TN). The additional kiosks, which we believe to be roughly 50, are expected to be fully integrated within several weeks.

Industry consolidation. In our view, the acquisition demonstrates the attractive industry consolidation opportunity for the company. Notably, the Pelicoin acquisition marks the second time in the last 18 months that the company has opportunistically added to its kiosk fleet. In April 2024, the company acquired 2,300 kiosks at a 50% discount from a defunct operator. We believe, with its healthy cash balance of $35 million (as of 3/31/25), the company is well positioned to continue to consolidate the industry as opportunities arise.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Stripe’s acquisition of crypto wallet provider Privy represents far more than a simple technology purchase—it’s a calculated move to position the payments giant at the forefront of the digital currency revolution. This strategic acquisition, coming on the heels of Stripe’s massive $1.1 billion purchase of Bridge earlier this year, demonstrates the company’s commitment to building a comprehensive cryptocurrency infrastructure that could fundamentally reshape how businesses and consumers interact with digital assets.

Privy’s impressive scale provides immediate validation of the crypto wallet market’s maturity. With over 75 million accounts across more than 1,000 developer teams facilitating billions in transactions, the New York-based startup has proven that cryptocurrency wallets can achieve mainstream adoption when properly executed. Founded in 2021 by Henri Stern and Asta Li, Privy solved a critical problem in the crypto ecosystem by creating developer-friendly APIs that eliminate the technical barriers traditionally associated with wallet creation and blockchain integration.

The timing of this acquisition is particularly significant given the broader cryptocurrency market’s evolution toward practical utility rather than speculative trading. Privy’s technology spans multiple high-growth sectors including decentralized finance, gaming, artificial intelligence agents, and consumer applications, indicating that crypto infrastructure is becoming integral to diverse business models rather than remaining confined to niche financial applications.

Stripe’s strategic vision becomes clearer when considering how Privy’s capabilities complement the company’s existing strengths. The payments processor has built its reputation on simplifying complex financial operations for merchants, and cryptocurrency transactions represent the next logical frontier. By integrating Privy’s wallet technology with Bridge’s stablecoin infrastructure and Stripe’s global payment network, the company is creating a unified platform that could make cryptocurrency transactions as seamless as traditional card payments.

The acquisition’s structure reveals Stripe’s confidence in Privy’s independent value proposition. By allowing Privy to continue operating as an independent product, Stripe acknowledges that the crypto wallet market requires specialized expertise and dedicated focus. This approach mirrors successful technology acquisitions where the parent company provides resources and distribution while preserving the acquired company’s innovative culture and technical capabilities.

Patrick Collison’s statement about enabling “Internet-native financial services” hints at Stripe’s larger ambition to challenge traditional banking infrastructure. The combination of wallet technology, stablecoin capabilities, and global payment processing creates a powerful alternative to conventional financial systems, particularly for international transactions where traditional banking remains slow and expensive.

The undisclosed acquisition price, while notable, is less important than the strategic implications. Privy’s $40 million in raised capital from prominent investors including Ribbit Capital and Coinbase Ventures suggests a valuation multiple that reflects both current performance and future potential. For Stripe, which processes hundreds of billions in annual payment volume, the cost of this acquisition is minimal compared to the potential revenue from expanding into cryptocurrency infrastructure.

This acquisition positions Stripe to capture value from the inevitable growth in cryptocurrency adoption while maintaining its core business focus. As regulatory clarity improves and institutional adoption accelerates, companies with comprehensive crypto infrastructure will possess significant competitive advantages in the evolving digital economy.

LVAD patients face a high risk of bleeding events associated with oral anticoagulation alongside increased risk of cardiovascular (CV) events such as stroke

Hospitalization costs for patients following a major bleeding event associated with oral anticoagulation use averages $39,000 per event

Tecarfarin, with its novel metabolic pathway, potentially may offer an alternative to warfarin in this vulnerable population

PONTE VEDRA, Fla. – Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a biopharmaceutical company developing novel therapeutics for patients with cardiovascular disease, today announced new findings from third-party research on the economic and medical burdens faced by advanced heart failure patients with left ventricular assist devices (LVAD) requiring chronic anticoagulation.

The research recently conducted by Guidehouse, an AI-led professional services firm delivering advisory, technology, and managed services to the commercial and government sectors, underscores the significant clinical and economic burden for LVAD patients who require chronic oral anticoagulation. Key findings include:

Major bleeds remain a primary cost driver, with average hospitalization costs (per event) of $54,100 for intracranial hemorrhage, $26,900 for gastrointestinal bleeds, and $36,600 for other major bleeds.

Guidehouse’s analysis also identified tecarfarin – a novel, Phase 3-ready oral anticoagulant being developed by Cadrenal – as a potential alternative to warfarin to address the current unmet need in this patient population. Tecarfarin is designed to provide more consistent anticoagulation control by avoiding the multiple metabolic pathways associated with warfarin. Its unique metabolism via a single enzyme (CES2) may reduce the risk of drug interactions, dietary complications, and adverse bleeding or thrombotic events.

“Despite decades of use, warfarin has significant limitations – especially in complex patients with LVADs,” said Quang X. Pham, Chairman and CEO of Cadrenal Therapeutics. “This research reinforces our conviction that tecarfarin has the potential to transform anticoagulation management for this high-risk population who currently has no alternative options.”

About Cadrenal Therapeutics, Inc.

Cadrenal Therapeutics, Inc. is a biopharmaceutical company developing therapeutics for patients with cardiovascular disease. Cadrenal’s lead investigational product is tecarfarin, a novel oral vitamin K antagonist anticoagulant that addresses unmet needs in anticoagulation therapy. Tecarfarin is a reversible anticoagulant (blood thinner) designed to prevent heart attacks, strokes, and deaths due to blood clots in patients requiring chronic anticoagulation. Although warfarin is widely used off-label for a number of indications, extensive clinical and real-world data have shown it can have significant, serious side effects. With tecarfarin, Cadrenal is advancing an innovative solution to address the unmet needs in anticoagulation therapy, aiming to reduce the clinical complexities of warfarin and capture value in a market with high demand for safer, more manageable treatment options.

Cadrenal is pursuing a pipeline-in-a-product approach with tecarfarin. Tecarfarin received Orphan Drug designation (ODD) for advanced heart failure patients with implanted mechanical circulatory support devices, including Left Ventricular Assisted Devices (LVADs). The Company also received ODD and fast-track status for tecarfarin in end-stage kidney disease and atrial fibrillation (ESKD+AFib).

Cadrenal is opportunistically pursuing business development initiatives with a longer-term focus on creating a pipeline of cardiovascular therapeutics. For more information, visit https://www.cadrenal.com/and connect with us on LinkedIn.

Safe Harbor

Any statements in this press release about future expectations, plans, and prospects, as well as any other statements regarding matters that are not historical facts, may constitute “forward-looking statements.” The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potentially,” “predict,” “project,” “should,” “target,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These statements include statements regarding Tecarfarin offering an alternative to warfarin for LVAD patients requiring chronic anticoagulation; providing more consistent anticoagulation control by avoiding the multiple metabolic pathways associated with warfarin; Tecarfarin’s metabolism via a single enzyme (CES2) reducing the risk of drug interactions, dietary complications, and adverse bleeding or thrombotic events; transforming anticoagulation management for LVAD patients who currently have no alternative options; preventing heart attacks, strokes, and deaths due to blood clots in patients requiring chronic anticoagulation; addressing the unmet needs in anticoagulation therapy; reducing the clinical complexities of warfarin; and capturing value in a market with high demand for safer, more manageable treatment options. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including the ability of tecarfarin to provide clinical benefits for LVAD patients who require anticoagulation; the ability to successfully complete clinical trials on time and achieve desired results and benefits as expected; the ability of Cadrenal to build a pipeline of specialized cardiovascular therapeutics and other assets and the other risk factors described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2024, and the Company’s subsequent filings with the Securities and Exchange Commission, including subsequent periodic reports on Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Any forward-looking statements contained in this press release speak only as of the date hereof and, except as required by federal securities laws, the Company specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events, or otherwise.

SAN DIEGO, June 12, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in Defense, National Security and Global Markets, today announced its participation in NATO’s At-Sea Demonstration (ASD)/Formidable Shield (FS) 25. This extensive live-fire exercise, the largest of its kind in the European theater, is hosted biennially by the U.S. 6th Fleet and executed by Naval Striking and Support Forces NATO.

This year’s exercise comprised a series of live-fire events against unmanned air and surface systems, subsonic, supersonic, and ballistic targets. It incorporated multiple Allied ships, multi-national/multi-service ground-based air defenses, and aviation forces, working cohesively across battlespaces to deliver lethal effects, accomplish exercise objectives, and hone warfighting skills.

Kratos’ Aegis Readiness Assessment Vehicle Type B (ARAV-B) medium range ballistic missile target participated during the exercise. Kratos launched the ARAV-B target on May 20, 2025, which flew a nominal trajectory and performed all planned events before being successfully engaged and intercepted by U.S. guided missile destroyers USS Bulkeley (DDG-84) and USS Thomas Hudner (DDG-116) using a Standard Missile 3 (SM-3).

Dave Carter, President of the Kratos Defense & Rocket Support Services Division, said, “Kratos is immensely proud of our dedicated team of professionals who consistently contribute to the success of events like Formidable Shield for users worldwide. Our team continues to deliver affordable, responsive, and reliable threat representative targets to our government customers and their allies.”

Eric DeMarco, President and CEO of Kratos, said, “At Kratos, we deliver real, mission relevant products and systems to our customers, not powerpoints, renditions or imagination. We believe that affordability is a technology, and rather than pay dividends or buy back KTOS stock, we invest Kratos funds to rapidly develop and field National Security relevant hardware, innovating, and also saving our government customer and the U.S. taxpayer time and money compared to traditional approaches. Kratos’ participation in Formidable Shield 25 is a recent example of the success and value creation of Kratos’ strategy for our entire incredibly important stakeholder community.”

The exercise, which commenced on May 3, 2025, involved approximately 6,900 personnel from across NATO member states. Kratos has been supporting the biennial Formidable Shield Exercise with aerial drone and ballistic missile targets since its inception in 2017, continually offering NATO forces opportunities to test and improve interoperability in the integrated air and missile defense (IAMD) environment.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, systems, and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital, and other investments to rapidly develop, produce, and field solutions that address our customers’ mission-critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading-edge approaches and technology, not unproven, bleeding-edge approaches, with Kratos’ approach designed to reduce cost, schedule, and risk, enabling us to be first to market with cost-effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems upfront for successful rapid, large-quantity, low-cost future manufacturing, which is a value-add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles; jet-powered unmanned aerial drone systems; advanced vehicles and rocket systems; propulsion systems for drones, missiles, loitering munitions, supersonic systems, spacecraft, and launch systems; C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter-UAS, directed energy, communication, and other systems; and virtual and augmented reality training systems for the warfighter. For more information, visit http://www.kratosdefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q1 Results. The company reported Q1 revenue of $97.0 million and adj. EBITDA of $15.6 million, both of which easily surpassed our estimates of $87.0 million and a loss of $0.6 million, respectively. Notably, while revenue decreased 9% from last year, adj. EBITDA was up substantially from a loss of roughly $1.0 million. The improvement in adj. EBITDA was largely driven by the company’s efficient use of marketing spend and focus on profitability.

Key operating metrics. Bookings and monthly paying users decreased by 25% and 26%, respectively, compared to the prior year period, but the decrease was expected as the company is focused on improving the quality of gameplay and not over-monetizing its user base. For example, average bookings per paying user (ABPPU) increased from $88 in Q1’24 to $90 in Q1’25, despite a decrease in monthly paying users.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition. CoreCivic is expanding its Safety Segment with the proposed acquisition of The Farmville Detention Center in Farmville, Virginia, about 60 miles west of Richmond. Constructed in 2010, Farmville is a 736-bed facility that provides transportation, care, and civil detention services to adult male noncitizens through an Intergovernmental Service Agreement between Prince Edward County, Virginia, and U.S. Immigration & Customs Enforcement (“ICE”), which expires in March 2029.

Details. CoreCivic is paying $67 million for Farmville, or about $91,000 per bed. The transaction is expected to be funded with cash on hand and borrowings under the Company’s revolving credit facility. The acquisition is expected to close effective July 1st and will add approximately $40 million of incremental revenue on an annual basis. Using the Safety segment’s average 2024 operating margin, Farmville could add nearly $10 million of segment operating income on an annual basis.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Senior Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Demand for rare earth elements expected to grow. Demand for rare earth elements is expected to grow meaningfully through 2030 and beyond, driven by electric vehicles, wind turbines, grid upgrades, and advanced defense technologies. According to the IEA, global rare earth demand could double by 2050 under a net-zero scenario, underscoring the growing strategic relevance in the global energy transition.

China dominates the REE market. According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves, while accounting for most of the midstream and downstream capacity. While mining activity is gradually diversifying, the refining stage remains concentrated. This level of concentration poses a risk to both the U.S. supply chain and national security.

U.S. policymakers seek to reduce dependence on China. U.S. policymakers are increasingly focused on reducing dependence on China for rare earth elements, viewing it as a national security and industrial resilience issue. Recent actions include invoking the Defense Production Act, funding domestic processing projects, and expanding international partnerships through initiatives like the Minerals Security Partnership. Legislative efforts and strategic investments are aimed at reshoring supply chains and building alternative capacity in allied countries such as Canada and Australia.

Necessity is the mother of invention. While the Trump Administration is taking appropriate action and policy momentum is growing, the path to increasing rare earth supply chain independence is complex and will take time. Policymakers may need to work with allies, such as Canada, to promote a North American supply chain that encompasses all aspects of the REE value chain, including upstream, midstream, and downstream. In addition to supportive public policy, private industry will likely need financial support from governments to kick start the effort.

Metals and Mining Spotlight: Rare Earth Elements

Rare earth elements (REEs) are comprised of 15 elements in the lanthanum series, along with scandium and yttrium. While not lanthanides, scandium and yttrium are classified as rare earth elements because they occur within the same ore deposits and share similar chemical properties. While the actual elements may not be rare, it is often difficult to find them in sufficient concentrations for economic extraction, and they require extensive processing. Cerium, lanthanum, neodymium, praseodymium, and promethium are considered light rare earth elements. Europium, gadolinium, and samarium are often referred to as medium rare earth elements, while dysprosium, erbium, holmium, lutetium, terbium, thulium, and ytterbium are considered heavy rare earth elements. We do not classify scandium (Sc) or yttrium (Y) as light, medium, or heavy. Below is a table summarizing the elements and their symbols.

Figure 1: Rare Earth Elements and Atomic Number and Symbol

Source: Noble Capital Markets, Inc.

One of the many uses of rare earth elements is in the production of permanent magnets which are critical components in electric vehicles, wind turbines, and other communication and defense technologies. Neodymium and praseodymium are critical materials in the manufacturing of neodymium-iron-boron (NdFeB) magnets, which have among the highest magnetic strength among commercially available magnets and promote high energy density and efficiency in energy technologies. They are often referred to as NdPr magnets because they generally contain about one-third neodymium, of which some of that can be replaced by praseodymium. While REEs are used for a variety of applications, the highest value REEs are neodymium and praseodymium, which currently drive the value of mixed rare earth concentrates and precipitates. By economic value, neodymium-praseodymium (NdPr) is the largest segment of the REE market. NdPr is primarily used in neodymium-iron-boron (NdFeB) permanent magnets for electric machines, such as electric vehicle (EV) traction motors, wind power generators, drones, robotics, electronics, and other applications. Given the wide-ranging uses of these component materials in critical infrastructure essential for national security and economic growth, the U.S. government has taken an interest in industry concentration.

Figure 2: Rare Earth Applications

Source: National Energy Technology Laboratory

According to the 2024 edition of the Energy Institute Statistical Review of World Energy, China accounted for 67.9% of rare earth mineral production in 2023 and 38.1% of rare earth mineral reserves. Conversely, the United States accounted for 12.2% of rare earth mineral production in 2023 and 1.6% of rare earth mineral reserves.

Figure 3: Rare Earth Metals Production and Reserves

Source: Energy Institute Statistical Review of World Energy 2024

Supply Chain and Pricing Overview

The supply chain for rare earths includes upstream, midstream, and downstream components.

Figure 4: Rare Earth Element Supply Chain

Source: Critical Materials Rare Earths Supply Chain: A Situational White Paper, U.S. Department of Energy, Office of Energy Efficiency & Renewable Energy, April 2020

As illustrated in Figure 4, concentration or beneficiation is an extractive metallurgy process that upgrades the value of mineral ores that contain raw REEs by removing low value minerals and resulting in a higher-grade product such as rare-earth concentrate.

Separation is the process of separating individual REEs from one another in the rare earth oxide (REO) concentrates. Separation of REEs is chemically intensive because the REEs are chemically similar. Processing refers to the conversion of REOs to rare earth metals, such as neodymium metal which can then be used to form alloys. China controls most of the midstream separating and processing capacity.

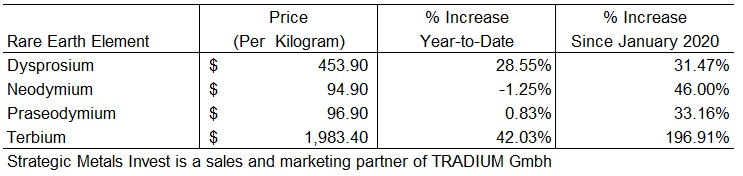

There is no single price for REEs collectively, but numerous prices for REE oxides and compounds individually. Pricing information for rare earths is opaque and generally available by paid subscription. Public information is generally not comprehensive and generally does not provide detailed information as to quality and origin, which makes comparisons difficult. Below we have provided a pricing sample of the most valuable elements as of June 11, 2025.

Figure 5: Pricing Data for Select Rare Earth Elements (REE)

Source: Strategic Metals Invest

U.S. Rare Earth Element Market

According to the U.S. Department of the Interior, the estimated value of rare-earth compounds and metals imported by the United States in 2023 was $190 million, down 7% from $208 million in 2022. Catalysts represented the leading domestic end use for rare earths, followed by applications in ceramics and glass, metallurgical alloys, polishing, and embedded permanent magnets in finished goods. While rare earth recycling is expected to grow in the coming years, current recovery rates from sources such as batteries and permanent magnets remain limited. The table below provides some statistics associated with the rare earths market in the United States.

Figure 6: United States REE Market Statistics

Source: Mineral Commodity Summaries 2024, U.S. Department of the Interior, U.S. Geological Survey

Given the United States’ reliance on imports, we think Canadian producers stand to benefit from a shift away from sources in China. As processing capabilities are developed, the U.S. could be an important destination for Canada sourced materials.

Key REE Market Participants

The global rare earth industry remains defined by a limited number of dominant players, most of which are concentrated in China. China Northern Rare Earth Group (SHH: 600111), and China Minmetals are the largest vertically integrated producers, with strong government alignment and control over both upstream mining and midstream separation capacity. These firms benefit from large-scale infrastructure, domestic demand, and preferential access to processing technology that remains restricted from foreign use.

Outside China, Lynas Rare Earths (ASX: LYC, OTC: LYSDY), in Australia is the largest fully integrated producer, with upstream operations at Mount Weld and a separation plant in Malaysia. Lynas is expanding into heavy rare earth processing in Texas through a strategic partnership with the U.S. Department of Defense.

MP Materials, the most significant rare earth materials producer in the United States, completed a business combination with Fortress Value Acquisition Corp., a special purpose acquisition company and began trading on the New York Stock Exchange on November 18, 2020, under the ticker MP. MP Materials owns and operates the Mountain Pass rare earth mine and processing facility in California which opened in 1952 as a uranium producer, pivoted to one of the largest suppliers of rare earth minerals, but closed in 2002 as environmental restrictions and imports made it difficult to compete. The facility underwent various ownership changes and reopened in 2017 under MP Materials’ ownership. It is North America’s only active and scaled rare earth production site and now has a market capitalization of $4.1 billion as of June 11, 2025.

The Mountain Pass mine in California and is the only active rare-earth mine in the United States. The company has restarted oxide production and is building refining and alloying capacity in Texas. MP has signed multi-year offtake agreements with original equipment manufacturers (OEMs), including General Motors, aimed at creating a vertically integrated domestic supply chain. However, the company still relies on China to assist in the separation process for some of its output, underscoring the current U.S. capabilities gap.

Additional participants working to expand non-Chinese supply chains include Iluka Resources (ASX: ILU, OTC: ILKAF) and Arafura Rare Earths (ASX: ARU, OTC: ARAFF), both based in Australia. Iluka is building a new facility with support from the Australian government, aimed at handling all stages of rare earth production. Arafura is also developing a new project with backing from international lenders, focused on supplying materials used in magnets for electric motors and other technologies. On the downstream side, magnet production is dominated by firms such as Shin-Etsu (TSE: 4063, OTC: SHECY), Hitachi Metals, and JL MAG (SZSC: 300748, OTC: JMREY), with capacity heavily skewed toward Asia. Efforts among U.S. and allied countries to establish domestic magnet manufacturing are progressing but remain in the early stages.

China dominates the production of many critical minerals, including rare earth elements. There appears to be an awakening among U.S. policy makers of the dangers of dependence on foreign sources for critical minerals, especially those that are adversarial to the United States. We believe a shift is underway to source REEs from countries that are friendly to the United States, including Canada. As part of its strategy to ensure secure and reliable supplies of critical minerals, the U.S. Department of the Interior identified 35 critical minerals, including the rare earth elements group. The U.S. Government is planning to fund rare earths projects to reduce reliance on China. In January 2022, bipartisan legislation was introduced, the Restoring Essential Energy and Security Holdings Onshore for Rare Earths Act, to protect the U.S. from the threat of rare-earth element supply disruptions, encourage domestic production, and reduce reliance on China. REEs are found in mineral deposits such as bastnaesite and monazite, the two largest sources of REEs. Bastnaesite, a carbonate-fluoride mineral, typically contains cerium, lanthanum, neodymium, and praseodymium. Monazite, a phosphate mineral, typically contains cerium, lanthanum, neodymium, and samarium. Rare earths are mined domestically in the United States. Bastnaesite is extracted at the mine in Mountain Pass, California.

Since January 2025, the Trump administration has significantly expanded its strategic focus on rare earth supply chain security. In April, an executive order initiated an investigation into whether U.S. dependence on foreign sources of rare earths constitutes a national security threat. An additional order opened up new offshore exploration zones for critical minerals, including seabed areas believed to contain rare earth and battery metals.

Furthermore, the administration has invoked the Defense Production Act to allocate capital and permit support to midstream and downstream segments of the rare earth supply chain. MP Materials began producing rare earth metals at its Texas facility, while Lynas advanced its U.S. processing plant with support from the Department of Defense. These efforts are part of a broader strategy to rebuild U.S. capabilities across the rare earth value chain.

International partnerships have also gained momentum. The U.S. is advancing cooperation with Australia, Canada, and Ukraine to secure alternative sources of supply and coordinate project financing through the Minerals Security Partnership. A bilateral agreement with Ukraine is expected to facilitate exploration and development of new deposits, while Australia remains a primary ally for both upstream mining and technical collaboration.

Outlook

The rare earth industry is entering a period of strong growth and growing strategic relevance. According to the International Energy Agency (IEA), magnet-grade rare earth demand could double by 2050, and mining projects could rise by 52% by 2040, under current policy (IEA, Critical Minerals Report, 2024). These forecasts are driven by growth in electric vehicle drivetrains, offshore wind development, and precision defense systems, all of which rely heavily on rare earth magnets for performance, efficiency, and miniaturization. As a result, rare earths have transitioned from niche industrial inputs to core strategic resources.

Figure 7: REE Demand Outlook and Mining Requirements (kt REE)

Source: Global Critical Minerals Outlook 2024, International Energy Agency (IEA)

We note that the IEA’s forecasts are based on three scenarios. These include: 1) the Stated Policies Scenario (STEPS), 2) the Announced Pledges Scenario (APS), and 3) the Net Zero Emissions by 2050 Scenario (NZE). The Stated Policies Scenario is based on current policy settings. The Announced Pledges Scenario assumes that governments will meet all climate-related commitments they have announced, including net zero emissions targets. The Net Zero Emissions by 2050 Scenario represents a pathway for the global energy sector to achieve net zero carbon dioxide emissions by 2050. These are summarized, of course, and readers may consult the IEA’s report for a more detailed description.

In the short term, challenges will continue to shape how supply chains evolve outside of China. Most new projects in Western countries face long approval timelines due to environmental reviews, local opposition, and infrastructure gaps. While government funding and procurement support are improving, the limited availability of midstream processing remains a key constraint.

In our view, rare earths are evolving from niche industrial inputs to foundational resources for advanced economies. Although the industry currently operates at a scale that lags its growing strategic importance, recent policy momentum and expanded investment across allied nations are setting the stage for meaningful transformation. Looking ahead, we expect a more balanced and resilient global supply chain to emerge—anchored by deepening cooperation between the United States, Canada, Australia, and European partners. While China will remain a major player in the near term, the diversification of supply chains is gaining traction, signaling a shift toward greater self-sufficiency and long-term security among like-minded nations.

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest

In a major step forward for the future of mRNA-based medicine, BioNTech SE has announced it will acquire fellow German biotech firm CureVac N.V. in an all-stock deal valued at approximately $1.25 billion. The transaction is set to bolster BioNTech’s capabilities in cancer immunotherapy and mRNA research, positioning the company for deeper innovation and broader commercialization in oncology.

Under the terms of the agreement, CureVac shareholders will receive approximately $5.46 in BioNTech American Depositary Shares (ADSs) for each CureVac share—representing a 55% premium over CureVac’s three-month average trading price. The exchange ratio will be adjusted depending on the 10-day average trading price of BioNTech stock leading up to the deal’s closure. Upon completion, CureVac shareholders are expected to own between 4% and 6% of BioNTech’s outstanding shares.

Both companies are pioneers in mRNA-based technologies, with BioNTech gaining international prominence for its COVID-19 vaccine co-developed with Pfizer. CureVac has long focused on developing mRNA therapeutics for cancer and infectious diseases. The deal unites two complementary platforms, merging BioNTech’s commercial success and oncology pipeline with CureVac’s expertise in mRNA design and lipid nanoparticle (LNP) delivery systems.

“This transaction is another building block in BioNTech’s oncology strategy and an investment in the future of cancer medicine,” said Prof. Ugur Sahin, CEO and Co-Founder of BioNTech. “By combining our strengths, we aim to accelerate the development of innovative and transformative cancer treatments that could become new standards of care.”

CureVac CEO Dr. Alexander Zehnder echoed Sahin’s sentiment, describing the acquisition as a shared mission rather than just a financial deal. “For more than 20 years, both companies have worked toward unlocking the potential of mRNA. This union represents a powerful convergence of technologies, cultures, and visions to push the boundaries of what’s possible in medicine,” Zehnder said.

The acquisition will integrate CureVac’s advanced R&D and manufacturing site in Tübingen into BioNTech’s broader operations. CureVac will become a wholly owned subsidiary of BioNTech, and a full corporate reorganization will follow the completion of the exchange offer, expected later this year.

The deal already has substantial shareholder backing. CureVac’s largest investor, dievini Hopp BioTech, and its affiliates—which collectively hold over 36% of CureVac shares—have agreed to support the transaction. Including other key stakeholders and the German government’s investment arm, BioNTech expects support from shareholders holding more than 50% of CureVac’s shares, positioning the company well to meet the 80% acceptance threshold required to finalize the transaction.

The boards of both companies have unanimously approved the deal, which now awaits regulatory approval and final shareholder votes. Legal and financial advisors for the deal include Covington & Burling LLP and PJT Partners for BioNTech, and Goldman Sachs and Skadden for CureVac.

This acquisition cements BioNTech’s strategy to lead the next generation of cancer therapies, leveraging the full power of mRNA science in the fight against some of the world’s most challenging diseases.

Key Points: – Air India Boeing 787-8 crashes after takeoff, killing all 242 passengers and crew. – Boeing shares drop over 4% as safety concerns resurface following the incident. – Supplier stocks also fall amid fears of regulatory delays and scrutiny.

Boeing’s stock took a sharp hit Thursday after a devastating crash involving an Air India Boeing 787-8 Dreamliner claimed the lives of over 200 people. The aircraft went down shortly after takeoff from Ahmedabad, India, en route to London’s Gatwick Airport, and is believed to have left no survivors among the 242 passengers and crew on board.

The Boeing 787-8 involved in the crash was delivered to Air India in 2014. While investigations into the cause of the incident are still underway, city officials confirmed that more than 200 bodies have already been recovered from the wreckage.

Shares of Boeing (NYSE: BA) dropped more than 4% by midday Thursday, trading around $204.88 — a sharp reversal for the aerospace giant, which had gained nearly 18% year-to-date thanks to a series of high-profile aircraft orders and what had been seen as a successful turnaround strategy under new CEO Kelly Ortberg.

In a brief statement, Boeing acknowledged the tragedy: “We are in contact with Air India regarding Flight 171 and stand ready to support them. Our thoughts are with the passengers, crew, first responders and all affected.” The company has yet to release any technical details or assessments regarding the crash.

This marks the first fatal incident involving the Boeing 787 Dreamliner since its introduction in 2011, according to Boeing’s aircraft safety records. The Dreamliner line has been considered one of Boeing’s flagship wide-body jets and was widely touted for its fuel efficiency, lightweight composite materials, and advanced onboard systems.

The crash adds to the list of major aviation tragedies tied to Boeing aircraft in recent years. The company is still recovering from the fallout of two deadly crashes involving its 737 Max 8 jets in 2018 and 2019. Those incidents, caused by software flaws, led to a 20-month worldwide grounding of the 737 Max and triggered numerous lawsuits, regulatory reforms, and a complete overhaul of Boeing’s safety and development processes.

Earlier this year, Boeing faced another crisis after a door panel on an Alaska Airlines 737 Max blew off mid-flight. That incident renewed safety concerns and prompted the resignation of former CEO Dave Calhoun, paving the way for Ortberg’s leadership. The company has since focused on rebuilding its reputation, tightening manufacturing oversight, and securing new contracts.

Thursday’s crash threatens to undo much of that progress. Analysts at Edward Jones warned that heightened regulatory scrutiny could delay future aircraft deliveries, potentially reducing Boeing’s cash flow. However, they noted that the company still retains a strong order backlog.

“While a delay in deliveries is possible, Boeing maintains a strong order book, and we think significant cancellations are unlikely given the lengthy wait times at Boeing’s primary competitor,” wrote Jeff Windau, senior industrials analyst at Edward Jones.

The tragedy also rippled through the broader aerospace sector. GE Aerospace, which manufactures engines for the 787, saw its shares fall more than 2%, while Spirit AeroSystems, a major supplier of fuselage components for Boeing aircraft, declined nearly 3%.

Investigators are expected to examine black box data, flight maintenance records, and crew communications to determine the cause of the crash. Both Boeing and global aviation authorities are closely watching developments as the company once again faces difficult questions about safety and accountability.

Key Points: – Oil prices jumped over 4% after reports of a partial U.S. embassy evacuation in Iraq raised geopolitical concerns. – Additional support came from President Trump’s doubts over a nuclear deal with Iran, potentially limiting future oil supply. – A breakthrough in U.S.-China trade talks also boosted sentiment, helping crude extend its recent rally.

Crude oil prices soared on Wednesday, climbing more than 4% amid escalating geopolitical tensions and renewed concerns over global supply disruptions. The sharp move followed reports that the U.S. embassy in Baghdad is preparing for a partial evacuation due to rising security threats.

West Texas Intermediate (WTI) crude futures closed at $68.15 per barrel, up 4.5%, while Brent crude, the global benchmark, settled at $69.77, a gain of 4%. The rally reflects growing unease in energy markets over the stability of the Middle East, a region critical to global oil production and transportation.

The price spike was triggered by a Reuters report indicating that U.S. and Iraqi officials are coordinating plans for an “ordered departure” of embassy personnel in Iraq. The development comes amid mounting threats in the region, raising fears that oil infrastructure or transportation routes could be impacted if tensions escalate further.

In addition to the embassy-related concerns, oil prices were also supported by comments from President Donald Trump, who expressed skepticism over the prospects of reaching a new nuclear agreement with Iran — a major oil-producing nation. Speaking during a podcast, Trump said his confidence in a deal had “diminished,” casting doubt on the potential return of sanctioned Iranian barrels to the market.

Oil prices found further support from signs of easing trade tensions between the U.S. and China. Following high-level discussions in London, both nations reportedly agreed to a framework aimed at reducing tariffs and improving trade flows. President Trump hinted that a formal agreement could be imminent, pending final approval from Chinese President Xi Jinping.

The latest surge adds to a month-long recovery in oil prices, which have rebounded from a sharp sell-off in April driven by global economic concerns and softer demand projections. Despite the rebound, both WTI and Brent remain down year-to-date, reflecting the broader market’s caution around demand durability and geopolitical risk.

Analysts are closely watching developments in the Middle East and diplomatic signals from Washington and Beijing, noting that any further escalation or policy shifts could significantly impact global supply dynamics in the weeks ahead

Key Points: – Quantum computing stocks surged after Nvidia’s CEO said the field is nearing an “inflection point.” – IBM’s announcement of a fault-tolerant quantum computer by 2029 marks a breakthrough toward real-world applications. – Big Tech and investors alike are ramping up bets on quantum as its commercial potential begins to materialize.

Shares of quantum computing companies soared midweek following a wave of renewed optimism about the sector’s near-term potential. The rally was sparked by remarks from Nvidia CEO Jensen Huang, who highlighted the accelerating pace of progress in quantum technology during the company’s developer conference in Paris.

Huang told attendees that quantum computing is approaching a pivotal stage in its development — a shift from theoretical promise to tangible application. His statements mark a notable departure from his more conservative estimates earlier this year, when he suggested commercially viable quantum machines could be decades away. This change in tone sent investor sentiment surging.

As a result, several companies in the space saw their stock prices jump significantly. Quantum Computing Inc. gained over 30% in early trading Wednesday, while Rigetti Computing and IonQ also posted strong single- and double-digit gains. The moves stand out against a largely flat broader market, reflecting growing confidence in the industry’s progress and future revenue potential.

The renewed excitement comes just one day after IBM revealed plans to launch the world’s first large-scale quantum computer designed to run without the common errors that have plagued existing systems. That machine is expected to debut by 2029, representing what analysts view as a meaningful advance toward practical, scalable quantum computing.

Unlike traditional computers, which process information in binary form, quantum computers harness the principles of quantum mechanics to perform calculations at exponentially faster speeds. Their unique architecture holds the potential to revolutionize fields that require complex computation, such as cryptography, materials science, drug discovery, and optimization problems in logistics.

However, the path to that reality has been hindered by a major obstacle: quantum systems are notoriously sensitive to external interference, often producing inaccurate results. IBM’s announcement, alongside accelerated efforts from major players like Google, Amazon, and Microsoft, signals a growing industry-wide push to solve these reliability challenges.

Nvidia’s increasing involvement in the sector further underscores the growing convergence between quantum and classical computing. In March, the company hosted its first-ever “Quantum Day” and announced plans to establish a quantum research hub in Boston. The move reflects Nvidia’s strategy to remain at the forefront of next-generation computing platforms as it expands beyond AI chips into quantum-ready infrastructure.

While fully fault-tolerant quantum systems may still be years away, the latest developments suggest progress is unfolding faster than many previously expected. If the momentum continues, quantum computing could become one of the most disruptive technologies of the next decade.

Kratos’ OpenSpace® Platform will be employed to support capabilities for Nuclear Command, Control, and Communication

SAN DIEGO, June 11, 2025 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (Nasdaq: KTOS), a technology company in defense, national security and global markets, announced today that it was awarded a task order under the Command and Control System-Consolidated (CCS-C) Sustainment and Resiliency (C-SAR) contract with the U.S. Space Force (USSF) Space Systems Command (SSC) to support ground system capabilities for Evolved Strategic Satellite Communications (SATCOM) (ESS). The ESS system will provide the survivable and endurable satellite communications capability for the Nuclear Command, Control, and Communications (NC3) mission in all operational environments.

First, the task order will begin to lay the CCS-C infrastructure groundwork to eventually support an out-of-band (OOB) ESS telemetry, tracking, and command capability as part of the larger SSC Military Communications & Positioning, Navigation and Timing Program Executive Office (PEO) mission. Second, it will create the necessary infrastructure to link the ground system solutions as required for operations. Third, through a pair of study efforts, it will facilitate the development of a road map for implementation of ESS Mission Unique Software and CCS-C micro-services implementation. Finally, the effort will facilitate a prototyping effort to allow CCS-C users to utilize new enterprise architecture.

The task order has a contract value of $25 million with a 34-month period of performance, beginning 14 March 2025 and concluding on 30 November 2027. This was accomplished under the C-SAR single-award indefinite delivery/indefinite quantity (IDIQ) contract awarded to Kratos on 15 November 2023. The C-SAR IDIQ contract has a maximum value of $579 million to cover task/delivery orders to support operations, sustainment, enhancements, and constellation capacity.

The C-SAR contract supports sustainment and operations of CCS-C which provides secure and integrated communications for Military SATCOM (MILSATCOM) requirements across Wideband and Strategic systems. CCS-C delivers OOB command and control (C2) for MILSATCOM systems currently including the Defense Satellite Communications System (DSCS), Milstar, Wideband Global SATCOM (WGS), and Advanced Extremely High Frequency (AEHF) satellites. CCS-C may eventually play a pivotal role in OOB C2 for the ESS constellation.

According to Phil Carrai, President of Kratos’ Space, Training & Cybersecurity Division, “One of the primary CCS-C infrastructure changes associated with this task order is the implementation of Kratos’ OpenSpace Platform to support the specified needs of the program. OpenSpace employs a modern, containerized and orchestrated architecture enabling the Space Force to select only the OpenSpace capabilities needed as missions evolve, providing a pathway for enterprise ground services for MILSATCOM constellations to effectively scale for future space vehicles while improving availability and resiliency.”

About Kratos OpenSpace Kratos’ OpenSpace family of solutions enables the digital transformation of satellite ground systems to become a more dynamic and powerful part of the space network. The family consists of three product lines: OpenSpace SpectralNet for converting satellite RF signals to be used in digital environments; OpenSpace quantum products, which are virtual versions of traditional hardware components; and the OpenSpace Platform, the first commercially available, fully orchestrated, software-defined ground system. These three OpenSpace lines enable satellite operators and other service providers to implement digital operations at their own pace and in ways that meet their unique mission goals. For more information about the OpenSpace family visit www.KratosDefense.com/OpenSpace.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, hypersonic vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 29, 2024, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.