Research News and Market Data on GOVX

- Last updated: 08 November 2023 21:03

- Created: 08 November 2023 15:32

- Hits: 505

Significant Progress towards data milestones in Phase 2 Program of GEO-CM04S1, Next-generation COVID-19 vaccine

Gedeptin® clinical data from Phase 1/2 study presented at AACR-AHNS Head and Neck Cancer Conference showing safe administration and tumor reduction

Multi-Product License Secured for ProBioGen’s AGE1.CR.pIX® suspension cell line to enhance manufacturing capabilities of MVA-based vaccine portfolio

Company to host conference call and webcast today at 4:30 p.m. ET

ATLANTA, GA, November 8, 2023 – GeoVax Labs, Inc. (Nasdaq: GOVX), a biotechnology company developing immunotherapies and vaccines against cancers and infectious diseases, today announced financial results for the third quarter ended September 30, 2023 and provided a business update.

“We are thrilled to see material advancements across all aspects of our business. Through the third quarter, we are delivering on our promise to bring transformative change to the treatment of COVID-19 by completing enrollment in our healthy volunteer Phase 2 clinical trial evaluating GEO-CM04S1 as a potentially more robust, more durable booster vaccine. In addition, with two additional Phase 2 trials ongoing in immunocompromised population, and recent publication of positive safety and potent immunogenicity data in this population, we have strengthened our conviction in the potential of our next-generation COVID-19 vaccine (GEO-CM04S1) for immunocompromised patients. We believe the need for new treatment options for immunocompromised patients in the fight against COVID-19 is significant, particularly as we begin to enter the winter surges of this diseases, where these patients will be left most vulnerable,” said David Dodd, Chief Executive Officer of GeoVax.

“We are preparing to announce initial data readouts from two of our Phase 2 GEO-CM04S1 trials as well as updates from our Gedeptin® clinical trial against head and neck cancer in the coming months. Earlier this summer, we were delighted to present clinical data which revealed the safe and feasible administration of Gedeptin®. We believe the Gedeptin mechanism of action to be solid tumor agnostic, and therefore offers the potential as a therapeutic option for multiple cancer types and positions the product for long-term growth. The third quarter of 2023 also saw new patents issued for our Ebola, Marburg, Malaria, and HIV vaccines, demonstrating the strength of our team’s ability to execute on our broader strategy. In addition, we advanced our manufacturing process through the signing of a landmark multi-product commercial license agreement with ProBioGen for the use of their AGE1.CR.PIX®suspension cell line. We believe that these catalysts altogether will have a profound impact on patients in need and all our stakeholders.”

Recent Business Achievements

GEO-CM04S1

- Enrollment completed for Phase 2 clinical trial evaluating GEO-CM04S1 as a booster for healthy patients who have previously received the Pfizer or Moderna mRNA vaccine in September of 2023. An initial data readout is expected soon.

- GEO-CM04S1 demonstrated potent antibody and cellular immunity in immunocompromised patients in a recent publication in the journal, Vaccines, in August 2023. GeoVax’s Phase 2 clinical trial evaluated the safety and immunogenicity of GEO-CM04S1, compared to either the Pfizer/BioNTech or Moderna mRNA-based vaccine in patients who have previously received an allogeneic hematopoietic cell transplant, an autologous hematopoietic cell transplant or CAR-T cell therapy. Most promising in the results published was the demonstration of the potential of GEO-CM04S1 as a variant agnostic COVID-19 vaccine, providing potent immunity from the Wuhan through Delta and Omicron strains.

- In October 2023, GeoVax commenced the planned site expansion for this trial to accelerate patient enrollment. In addition to study enrollments completed at the City of Hope Medical Center (Duarte, California), the trial is now open at Wake Forest Baptist Medical Center (Winston Salem, North Carolina), the University of Massachusetts Medical Center (Worcester, Massachusetts), and Fred Hutchinson Cancer Center (Seattle, Washington).

- Commenced investigator-initiated randomized observer-blinded Phase 2 clinical trial of COVID-19 boosters with GEO-CM04S1 or Pfizer-BioNTech bivalent vaccines in patients with chronic lymphocytic leukemia (CLL) in July of 2023. The trial is rapidly enrolling patients and progressing towards an interim data review.

- Presented data for GEO-CM02 at the Keystone Symposia Conference in an abstract titled, MVA-vector multi-antigen COVID-19 vaccines induce protective immunity against SARS-CoV-2 variants spanning Alpha to Omicron in preclinical animal models in September of 2023. The data revealed that the GEO-CM02 vaccine induced immune responses that were efficacious against the original Wuhan strain and Omicron variants with a single dose. This effort expands upon GeoVax’s hypothesis that vaccines designed to induce both antibodies and T-cell responses to multiple viral structural proteins can address the issue of viral variation and escape from the immune system without the need for repeated seasonal adjustments.

Gedeptin®

- Gedeptin® clinical data presented at the AACR-AHNS Head and Neck Cancer Conference in an abstract titled, Phase 1/2 study of Ad/PNB with Fludarabine for the Treatment of Head and Neck Squamous Cell Carcinoma (HNSCC) in July 2023. The FDA-funded study revealed that the administration of Gedeptin® is safe and feasible.

Advanced Vaccine Manufacturing Process

- GeoVax and ProBioGen announced the signing of a landmark multi-product commercial license agreement for ProBioGen’s groundbreaking AGE1.CR.PIX® suspension cell line in September 2023. The agreement enhances the manufacturing capabilities of GeoVax’s entire Modified Vaccinia Ankara (MVA)-based vaccine portfolio with respect to both scale and flexibility. This follows the May 2023 agreement with Advanced Bioscience Laboratories, Inc. (ABL) to support current Good Manufacturing Practices (cGMP) production of the Company’s vaccine candidates. These agreements move the Company toward fully implementing a continuous cell line manufacturing system that will provide lower-cost, scalable versatility for our entire MVA-based vaccine portfolio.

Intellectual Property Developments

- GeoVax recently secured multiple positive patent decisions covering notice of allowances for Ebola, Marburg, Malaria and HIV vaccines.

- GeoVax announced that the U.S. Patent and Trademark Office has issued a Notice of Allowance for Patent Application No. 17/584,231 titled patent titled “Replication Deficient Modified Vaccina Ankara (MVA) Expressing Marburg Virus Glycoprotein (GP) and Matrix Protein (VP40).”

- GeoVax announced that the U.S Patent and Trademark Office has issued a Notice of Allowance for Patent Application No. 17/409,574 titled “Multivalent HIV Vaccine Boost Compositions and Methods of Use.”

- GeoVax announced that the U.S. Patent and Trademark Office has issued a Notice of Allowance for Patent Application No. 17/726,254 titled “Compositions and Methods for Generating an Immune Response to Treat or Prevent Malaria.”

- GeoVax announced that the U.S. Patent and Trademark Office has issued Patent No. 11,701,418 B2 to GeoVax, pursuant to the Company’s patent application No. 15/543,139 titled “Replication-Deficient Modified Vaccinia Ankara (MVA) and Matrix Protein (VP40).”

Upcoming Events

- GeoVax will participate in upcoming conferences and industry events:

- Vaccines Summit 2023, November 13-15, 2023, Boston, MA

- World Vaccine Congress, West Coast, November 27-30, 2023, Santa Clara, CA

- NobleCon19, December 3-5, Boca Raton, FL

- Emerging Growth Conference, December 6-7, Virtual

Third Quarter 2023 Financial Results

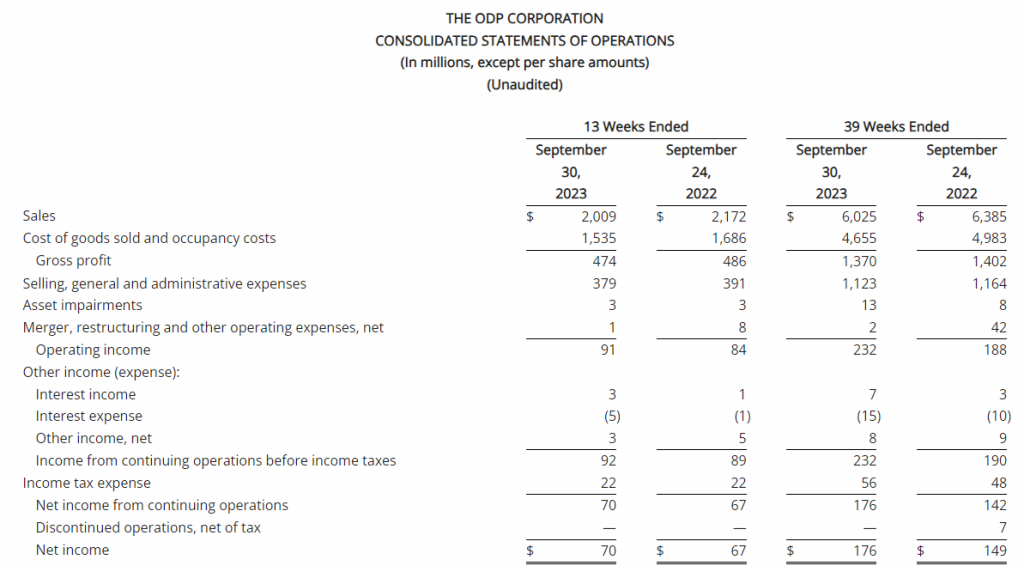

Net Loss: Net loss for the three months ended September 30, 2023, was $8,408,818 ($0.32 per share) as compared to $3,968,102 ($0.17 per share) for the comparable period in 2022. For the nine months ended September 30, 2023, the Company’s net loss was $18,374,354 ($0.69 per share) as compared to a net loss of $8,637,316 ($0.63 per share) in 2022.

R&D Expenses: Research and development expenses were $6,947,979 and $14,486,896 for the three-month and nine-month periods ended September 30, 2023, compared to $2,721,196 and $5,358,917 for the comparable periods in 2022, with the increase primarily due to the cost of conducting clinical trials for GEO-CM04S1 and Gedeptin, costs of manufacturing materials for use in our clinical trials, additional personnel costs, technology license fees, costs of preclinical research activities and a generally higher level of activity.

G&A Expenses: General and administrative expenses were $1,651,775 and $4,562,293 for the three-month and nine-month periods ended September 30, 2023, compared to $1,249,337 and $3,363,672 for the comparable periods in 2022, with the increase primarily due to higher personnel costs, investor relations consulting costs, patent costs and other expenses supportive of a higher level of activity.

Cash Position: GeoVax reported cash balances of $12,687,041 at September 30, 2023, as compared to $27,612,732 at December 31, 2023.

Further information is included in the Company’s Quarterly Report on Form 10-Q filed with the Securities and Exchange Commission.

Conference Call Details

Management will host a conference call scheduled to begin at 4:30 p.m. ET today, November 8, 2023, to review financial results and provide an update on corporate developments. A question-and-answer session will follow management’s formal remarks.

Domestic: +1-800-715-9871

International: +1-646-307-1963

Conference ID: 7519986

Webcast: https://edge.media-server.com/mmc/p/r4i9d5j7

A webcast replay of the call will be available for three months via the same link as the live webcast approximately two hours after the end of the call.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company developing novel therapies and vaccines for solid tumor cancers and many of the world’s most threatening infectious diseases. The company’s lead program in oncology is a novel oncolytic solid tumor gene-directed therapy, Gedeptin®, presently in a multicenter Phase 1/2 clinical trial for advanced head and neck cancers. GeoVax’s lead infectious disease candidate is GEO-CM04S1, a next-generation COVID-19 vaccine targeting high-risk immunocompromised patient populations. Currently in three Phase 2 clinical trials, GEO-CM04S1 is being evaluated as a primary vaccine for immunocompromised patients such as those suffering from hematologic cancers and other patient populations for whom the current authorized COVID-19 vaccines are insufficient, and as a booster vaccine in patients with chronic lymphocytic leukemia (CLL). In addition, GEO-CM04S1 is in a Phase 2 clinical trial evaluating the vaccine as a more robust, durable COVID-19 booster among healthy patients who previously received the mRNA vaccines. GeoVax has a leadership team who have driven significant value creation across multiple life science companies over the past several decades. For more information, visit our website: www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

| Company Contact: | Investor Relations Contact: | Media Contact: | ||

| info@geovax.com | paige.kelly@sternir.com | sr@roberts-communications.com | ||

| 678-384-7220 | 212-698-8699 | 202-779-0929 |