Baudax Bio is a pharmaceutical company focused on innovative products for acute care settings. ANJESO is the first and only 24-hour, intravenous (IV) COX-2 preferential non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. In addition to ANJESO, Baudax Bio has a pipeline of other innovative pharmaceutical assets including two novel neuromuscular blocking agents (NMBs) and a proprietary chemical reversal agent specific to these NMBs. For more information, please visit www.baudaxbio.com.

Gregory Aurand, Senior Vice President, Equity Research Analyst, Healthcare Services & Medical Devices, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Key Opinion Leader Webinar. In conjunction with the full top line data release, yesterday Baudax Bio held a key opinion leader webinar to discuss the results in greater detail. Led by Gerri Henwood, President and CEO, and Stuart McCallum, Chief Medical Officer, the webinar featured Dr. Todd Bertoch, CEO of JBR Clinical Research, and Dr. Harold Minkowitz, Associate Director at MD Anderson Cancer Center Dept. of Anesthesiology and Perioperative Medicine.

BX1000 patient data was “spectacular”. Similar to the prior two interim analyses, the full 79-patient (of the four 20-patient cohorts one patient in the rocuronium arm was not evaluated due to issues with the endotracheal tube) trial showed that all BX1000 patients met Good or Excellent intubating conditions at 60 seconds. From a safety perspective, treatment emergent side effects like nausea were comparable to rocuronium (current standard) in all BX1000 cohorts. There will be 28-day patient safety follow-up and this data could be available in around four weeks.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

One popular meme stock, Bed Bath & Beyond (BBBY) is being delisted from the Nasdaq exchange, according to a company announcement. There are a number of reasons a public company can delist from an exchange. In BBBY’s case it is related to their recent bankruptcy filing, according to management. Below are examples of the many reasons a company would delist, what happened in BBBY’s case, and what delisting means for investors.

Many Reasons to Delist

Delisting from the stock exchange refers to the removal of a company’s shares from public trading on a particular exchange. It occurs by management choice or at the exchange’s request. The process can happen for various reasons, such as regulatory violations, bankruptcy, or a company’s decision to go private. Delisting can have significant consequences for the corporation and its investors, including decreased liquidity and visibility in the market.

A common reason for delisting is regulatory violations. For example, if a company fails to comply with the reporting requirements of the Securities and Exchange Commission (SEC), it may face delisting from the stock exchange. This was the case with Chinese tech giant Alibaba, which was delisted from the Hong Kong Stock Exchange in 2020 because of regulatory violations.

Sometimes, companies have a reason to take themselves private and delist as part of that process. Going private means that a corporation’s shares are no longer traded on public stock exchanges. In 2013, computer maker Dell was taken private in a deal worth $24.9 billion. The company’s delisted its shares from the NASDAQ exchange. Twitter was recently purchased and taken private.

As is the case with Bed Bath and Beyond, bankruptcy often causes shares not to meet the exchange’s criteria, forcing a delisting. Another retailing example is Toys R Us in 2018. It filed for bankruptcy and was subsequently delisted from the New York Stock Exchange (NYSE).

Delisting can have significant implications for a company and its shareholders. One of the main consequences is a decrease in liquidity. When a company is delisted, its shares are no longer traded on public stock exchanges, which means that investors may have a harder time finding buyers or sellers for their shares.

Additionally, delisting can impact a company’s visibility in the market. Without a public listing, a company may find it more difficult to attract investors and raise capital. This can be particularly challenging for small and mid-sized companies that rely on the stock market to raise funds.

Bed Bath and Beyond’s Delisting

Trading in BBBY common stock will cease at the opening of the trading day on May 3 – according to a filing with the Securities and Exchange Commission (SEC).

In its bankruptcy announcement, the company said trading of shares would halt on the Nasdaq exchange. Nasdaq and the NYSE have standards companies need to meet for their stocks to be listed and stay listed. This includes minimum levels of liquidity, market value, or price level.

Back in January, Nasdaq warned the company its shares would be delisted after it failed to report quarterly results in a timely manner. The company eventually filed the report and returned to compliance. This time Bed Bath and Beyond said it doesn’t intend to appeal.

Shareholders will still own the stock and fractional shares of the company after May 3. However, without the help of a major exchange, trading between stockholders and speculators is usually much more difficult. Some bankrupt companies’ stocks continues to trade in over-the-counter markets (OTC). They typically have the letter “Q” at the end of their stock symbol. It isn’t yet clear if BBBY will trade as BBBYQ.

After a company files for Chapter 11, unsecured creditors—including suppliers and leaseholders—line up in an attempt to get repaid. How much creditors get paid back depends on how much money Bed Bath and Beyond can raise from the sale of either parts of its business or the chain itself.

Take Away

Delisting from major stock exchanges can happen for various reasons and can have significant consequences for investors. While regulatory violations and bankruptcy can lead to forced delisting, companies may choose to delist voluntarily to go private or for other strategic reasons. Regardless of the reason, delisting can impact a company’s liquidity and visibility in the market, making it important for investors to carefully consider the implications before investing in delisted companies or those facing delisting.

HOUSTON, April 25, 2023 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (NASDAQ: GLDD) today announced that it will release the financial results for its three months ended March 31, 2023 on Tuesday, May 2, 2023 at 7:00 a.m. C.D.T. A conference call with the Company will be held the same day at 9:00 a.m. C.D.T.

Investors and analysts are encouraged to pre-register for the conference call by using the link below. Participants who pre-register will be given a unique PIN to gain immediate access to the call. Pre-registration may be completed at any time up to the call start time.

The live call and replay can also be heard at https://edge.media-server.com/mmc/p/rse8awvj or on the Company’s website, www.gldd.com, under Events on the Investor Relations page. A copy of the press release will be available on the Company’s website.

The Company Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 133-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

VANCOUVER, BC, April 25, 2023 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce that further to the news release dated April 12, 2023, all assays for the hydrometallurgical pilot plant have been received and interpretation of the data is largely complete. Data from Phase I have been used to optimize the design conditions for Phase II of the pilot plant.

John Goode, P.Eng., Defense Metals’ Consulting Metallurgist, commented as follows:

“Phase I of the hydrometallurgical pilot plant operation went very well and gave us the opportunity to explore areas of the flowsheet where we could further improve the efficiency of the Wicheeda hydrometallurgical process. Changes have been incorporated in the Phase II pilot plant campaign which started yesterday and will run for about ten days. The importance of pilot plants like the one we are operating cannot be over-emphasized. It provides the opportunity to see if processes are stable and can be effectively controlled; to determine the effects of in-plant recirculation of solutions and solids; measure recoveries and reagent demands; and generates significant quantities of material that can be used for engineering design and environment-related tests. The data from the pilot plant will be used in the pre-feasibility study.”

Minor changes were made during Phase I of the pilot plant testing to investigate the impact on circuit operability, extraction, impurity removal and product quality. The specific changes that were made during Phase I of the pilot plant, and their impacts, are summarized below:

The acid bake kiln was operated at 350ºC for much of the run but 250ºC was tested in the latter part with no obvious impact on REE extraction which averaged 93% throughout.

Fresh water was used in the water leach circuit for the initial part of the pilot plant run but regenerated water was used for the last portion with no discernable adverse effect.

Industrial grade magnesia was initially used for neutralization and impurity removal in the water leach circuit and proved to be more effective than the regenerated magnesia.

Phase I of the pilot plant run used magnesia as the rare earth precipitant based on bench testwork, but at the pilot plant it was difficult to attain low magnesium content in the rare earth product. Oxalic acid will be used as the precipitant in the next phase of pilot testing.

Defense Metals has selected the engineering company Hatch to undertake parts of the PFS; Hatch will attend the pilot plant.

Qualified Person

The scientific and technical information contained in this news release, as it relates to the metallurgical aspects of the Wicheeda Rare-Earth Project, has been reviewed and approved by John Goode, P. Eng., metallurgical consultant to the Company and who is a Qualified Person as defined by National Instrument 43-101 and who has provided the technical information relating to metallurgy in this news release.

About the Wicheeda REE Property

Defense Metals 100% owned, 4,262-hectare (~10,532-acre) Wicheeda Light REE property is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda Project is readily accessible by all-weather gravel roads and is near infrastructure, including hydro power transmission lines and gas pipelines. The nearby Canadian National Railway and major highways allow easy access to the port facilities at Prince Rupert, the closest major North American port to Asia.

The 2021 Wicheeda Project Preliminary Economic Assessment technical report (“PEA”) outlined a robust after-tax net present value (NPV@8%) of $517 million and an 18% IRR1. This PEA contemplated an open pit mining operation with a 1.75:1 (waste:mill feed) strip ratio providing a 1.8 Mtpa (“million tonnes per year”) mill throughput producing an average of 25,423 tonnes REO annually over a 16 year mine life. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

About Defense Metals Corp.

Defense Metals Corp. is focused on the development of its 100% owned Wicheeda Project that contains Rare Earth Elements that are commonly used in the defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles.

Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB, and in Germany on the Frankfurt Exchange under “35D”.

Defense Metals is a proud member of Discovery Group. For more information please visit: http://www.discoverygroup.ca/

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the expected benefits and outcomes of the hydrometallurgical pilot plant, the expected completion of the hydrometallurgical pilot plant and the expected timelines, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration and metallurgical results, risks related to the inherent uncertainty of exploration and development and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological, metallurgical and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

____________

1 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

BRENTWOOD, Tenn., April 25, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (CoreCivic or the Company) announced today it received notice from the Oklahoma Department of Corrections (ODC) of its intent to terminate the lease agreement for the company-owned, 2,400-bed North Fork Correctional Facility (NFCF) upon the lease expiration on June 30, 2023.

The ODC was facing the impact of staffing challenges at the NFCF that limited the facility’s utilization and were exacerbated by the difficult employment market since the beginning of the COVID-19 pandemic. The Company was also aware that since commencing the lease of the NFCF in 2016, other privately owned correctional capacity became available to the state of Oklahoma and impacted the competitive landscape for renewal of the Company’s lease agreement. Rental revenue generated from the ODC at the NFCF for year ended December 31, 2022, was $12.2 million and is reported in the CoreCivic Properties business segment.

The Company is also actively renegotiating the terms of its contract with the state of Oklahoma at the company owned-and-operated 1,670-bed Davis Correctional Facility, which is also set to expire on June 30, 2023. The terms for a contract extension were being negotiated along with the lease agreement for the NFCF, and the Company will only renew the contract or enter into a similar lease agreement with the state of Oklahoma if the arrangement produces a satisfactory return on a stand-alone basis. The Company can provide no assurance that it will be successful in entering into an agreement with the state of Oklahoma for the continued use of the Davis Correctional Facility.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. CoreCivic provides a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. CoreCivic is the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. CoreCivic has been a flexible and dependable partner for government for 40 years. CoreCivic’s employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to CoreCivic’s beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the impact on the Company’s financial guidance resulting from the non-renewal of the lease agreement for the North Fork Correctional Facility and the probability of, and potential returns on, the renewal of the contract to manage or lease the Company’s Davis Correctional Facility. The Company expects to update its financial guidance in connection with is quarterly earnings announcement currently scheduled for May 3, 2023.

CoreCivic takes no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

Announced Acquisition to Increase Schwazze’s New Mexico Retail Store Count to 32

Transaction Provides Expanded Coverage Throughout State

DENVER, April 25, 2023 /CNW/ – Medicine Man Technologies, Inc., operating as Schwazze, (OTCQX: SHWZ) (NEO: SHWZ) (“Schwazze” or the “Company”), announced that it has signed definitive documents to acquire certain assets of Sucellus, LLC, pursuant to which the Company will manage Everest Apothecary, Inc., a New Mexico not-for-profit corporation (“Everest“). The proposed transaction includes retail dispensaries, cultivation, and manufacturing facilities.

The consideration for the proposed acquisition is US$38M and will be paid in a combination of cash, a four-year seller note and Company common stock. The acquisition is expected to close in the second quarter of 2023, upon receipt of approval from the New Mexico Regulation and Licensing Department.

Established in 2016, Everest is a New-Mexico-based licensed medical and recreational cannabis provider that consists of 14 dispensaries, one cultivation facility and one manufacturing plant. The dispensaries are located in Albuquerque, Santa Fe, Las Cruces, Los Lunas, Sunland Park, Belen, and Texico. Everest’s approximately 16,000 square feet of cultivation and 8,500 square foot manufacturing facility are located in Albuquerque.

This acquisition increases the Company’s retail consumer base and furthers Schwazze’s growth efforts in the New Mexico market, which upon transaction closing will bring the Company’s total number of New Mexico dispensaries to 32 with over 450 Schwazze employees. https://everestnm.com/products/

“This planned acquisition shows our commitment to the Company’s super-regional cannabis growth strategy to go deep in select markets,” said Nirup Krishnamurthy, President of Schwazze. “The Everest brand is a perfect complement to our existing retail brand in New Mexico, R. Greenleaf. Each serves a unique demographic, and we will continue to operate both retail banners in the state. By utilizing Schwazze’s operating playbook, we fully intend to support the Everest team and its customers by delivering outstanding service, great selection and quality products throughout the state of New Mexico.”

Since April 2020, Schwazze has acquired, opened, or announced the planned acquisition of 60 cannabis retail dispensaries (bannered as Star Buds, Emerald Fields, R. Greenleaf, Standing Akimbo, and Everest) as well as eight cultivation facilities and three manufacturing plants across Colorado and New Mexico. In May 2021, Schwazze announced its Biosciences division, and in August 2021, it commenced home delivery services in Colorado.

About Schwazze

Schwazze (OTCQX: SHWZ) (NEO: SHWZ) is building a premier vertically integrated regional cannabis company with assets in Colorado and New Mexico and will continue to take its operating system to other states where it can develop a differentiated regional leadership position. Schwazze is the parent company of a portfolio of leading cannabis businesses and brands spanning seed to sale. The Company is committed to unlocking the full potential of the cannabis plant to improve the human condition.

Schwazze is anchored by a high-performance culture that combines customer-centric thinking and data science to test, measure, and drive decisions and outcomes. The Company’s leadership team has deep expertise in retailing, wholesaling, and building consumer brands at Fortune 500 companies as well as in the cannabis sector. Schwazze is passionate about making a difference in our communities, promoting diversity and inclusion, and doing our part to incorporate climate-conscious best practices.

Medicine Man Technologies, Inc. was Schwazze’s former operating trade name. The corporate entity continues to be named Medicine Man Technologies, Inc. Schwazze derives its name from the pruning technique of a cannabis plant to enhance plant structure and promote healthy growth. To learn more about Schwazze, visit www.Schwazze.com.

Forward-Looking Statements

This press release contains “forward-looking statements.” Such statements may be preceded by the words “may,” “will,” “could,” “would,” “should,” “expect,” “intends,” “plans,” “strategy,” “prospects,” “anticipate,” “believe,” “approximately,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” or the negative of these terms or other words of similar meaning in connection with a discussion of future events or future operating or financial performance, although the absence of these words does not necessarily mean that a statement is not forward-looking. Forward-looking statements are not guarantees of future events or performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which are beyond the Company’s control and cannot be predicted or quantified. Consequently, actual events and results may differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, without limitation, risks and uncertainties associated with (i) regulatory limitations on our products and services and the uncertainty in the application of federal, state, and local laws to our business, and any changes in such laws; (ii) our ability to manufacture our products and product candidates on a commercial scale on our own or in collaboration with third parties; (iii) our ability to identify, consummate, and integrate anticipated acquisitions; (iv) general industry and economic conditions; (v) our ability to access adequate capital upon terms and conditions that are acceptable to us; (vi) our ability to pay interest and principal on outstanding debt when due; (vii) volatility in credit and market conditions; (viii) the loss of one or more key executives or other key employees; and (ix) other risks and uncertainties related to the cannabis market and our business strategy. More detailed information about the Company and the risk factors that may affect the realization of forward-looking statements is set forth in the Company’s filings with the Securities and Exchange Commission (SEC), including the Company’s Annual Report on Form 10-K and its Quarterly Reports on Form 10-Q. Investors and security holders are urged to read these documents free of charge on the SEC’s website at http://www.sec.gov. The Company assumes no obligation to publicly update or revise its forward-looking statements as a result of new information, future events or otherwise except as required by law.

Highly Regarded Analyst Tells Investors How to Position for the Upturn

Are recession worries fully baked into stock prices? At least one Wall Street analyst has publicly made her case this may be accurate. And she offers tips on what sectors may have more upside and on those that have factors working against them. While a recession still may occur before year-end, forward-looking stock investors may have fully priced that risk in – forward-looking investors may also be the reason the overall market is up on the year despite greater expectations of a recession. They are looking past any slowdown.

Stock market participants, many still down on last year’s price moves, have been extremely cautious in front of a Fed that is playing catch up in a fight against inflation. The rapid Fed Funds rate increases that began in March 2022, coupled with quantitative tightening, sank stocks, bonds, and even cryptocurrency holdings. While the economy did shrink for two consecutive quarters last year, there are many that expect a mild recession will begin at some point this year.

Those that do expect a bumpy economic ride and a rough landing point to high-interest rates, a weakening dollar, tech industry layoffs, and a Federal Reserve that is resolved to get inflation down as soon as possible.

Savita Subramanian, equity and quant strategist at Bank of America Securities, proposed to investors in a research note published on April 24, that these fears and recession worries have been in place for a while and may be largely baked into the market. She says, barring a sudden shock to the economy, it makes sense for investors to reintroduce riskier assets into their portfolios.

Her guidance on finding value is well thought out. Subramanian, proposes investors own stocks over bonds and cyclical stocks over defensive names. The reason given is that hedge funds and long-only funds are near maximum exposure in defensive industries such as health care, utilities, and consumer staples. The suggestion here is that the probabilities would lean toward a better risk-reward payoff for cyclical names.

Ms. Subramanian does not say an economic slowdown won’t occur; instead, her thinking seems to be that after raising the Federal Funds rate from near-zero to a range of 4.75% to 5%, there is more control should a downturn need to be dealt with by easing. When rates are at or near zero percent, there is less the Fed can do to stimulate growth. So far, we’ve made it through the first quarter, and now April with only a few disruptions in the banking sector.

“Even if a recession is imminent, the Fed has latitude to soften the impact after pushing rates up by 5%. And after the fastest hiking cycle ever, the only thing to ‘break’ so far is SVB,” Subramanian wrote.

In an article published in Barron’s this week the investment news publication wrote, “Some corners of Wall Street are feeling confident that there will be no recession and that the very things that make a recession appear likely–the inverted yield curve, inflation, and the recent banking crisis–actually guarantee that one won’t happen.”

This could be good news for investors that have been nervous about having money in a market that has been given much to be concerned about, and ver little to be jubilant about.

On Thursday, GDP (Gross Domestic Product) for the first quarter will be released. No one expects this to indicate a recession began then. Forecasters expect that the economy will show 2% growth, following growth of 3.2% and 2.6% in the third and fourth quarters of 2022. This is one of the cases where if the number surprises much higher, the market may expect the Fed to make bigger rate moves. If it surprises on the low side, markets may see it as a sign of an approaching recession.

Take Away

A highly regarded analyst joins others with thoughts that the market could be priced for a recession; this could be good for stocks. If true, investors may want to start looking past a recession. Those she is most positive on are riskier names. While funds and other investors are near maxed out in lower-risk holdings, there is far less upside for them. The bigger upswings can occur in the industries, market-cap sectors, and companies that have been given less attention due to recession fears.

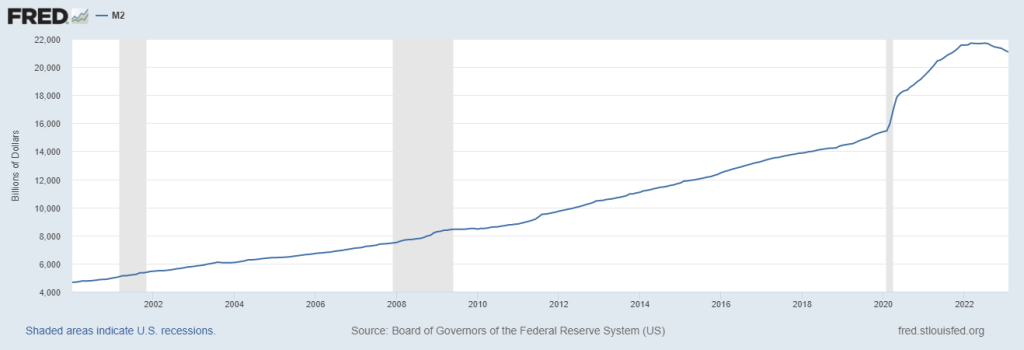

M2 is Fuel for Inflation, How Much Money Must the Fed Drain to Achieve 2 Percent?

U.S. Money Supply, measured as M2, is an important consideration when forecasting inflation. A decline in immediately available cash in the economy has a downward effect on price levels. At the same time, less cash available to consumers also cools economic growth. With the Federal Open Market Committee’s (FOMC) interest rate decision coming the first week in May, the updated report this week (for March) will give investors a look see at how successful the Fed has been draining funds from the system while trying to maintain some growth.

M2 Shrinking

The Federal Reserve will update stock and bond markets Tuesday afternoon on the total amount of currency, coins, bank savings deposits, and money-market funds held in March. This broader measure, officially M2SL, referred to as M2, gained renewed focus after contracting for the first time ever in December 2022, then contracting even further in January and February. January’s 1.75% decline and February’s 2.4% drop to $21.1 trillion, are the steepest drops so far in M2.

Image: M2 levels ramped up starting in 2020 in response to pandemic economic efforts

A fourth consecutive decline in M2 would provide more evidence that inflation can be expected to continue to come down and weigh into the FOMC decision when the Fed meets to adjust monetary policy at its May 2-3 meeting. While the chart above shows the recent declines are significant, it is still far higher than the trend line that was established decades ago. So while a decline of similar magnitude as the first two months would be welcome by inflation hawks, there is still a great deal more cash in the system than there was pre-pandemic. But it would be a huge positive and may cause the Fed to pause or slow draining money from the system.

Inflation

Consumer price inflation is well off its 8.6% average for all of 2022. Inflation since rose 5% in March 2023 (annual basis), decelerating from February’s 6% pace. While this slowdown in price increases is substantial, the Fed doesn’t want to declare “mission accomplished” until it is ranging near 2%. Its work is not yet finished.

How close is the Fed from finished is what investors will try to discern from M2. Highly regarded analysts and Fed watchers anticipate that there is a lag of about a year when the money supply shrinks. However, as indicated above, it has never come down on an annualized basis, and January and February were the largest declines to date. So even the best analysts have little history to point to.

Financial Sector

The data is for March, so it is the first look at M2 since the banking sector showed trouble early that month. A part of the difficulty banks are currently experiencing is that the reduction in cash has caused a need for them to liquidate U.S. Treasuries and other bonds to fund withdrawals. A further huge reduction in M2 could be shown to be challenging more banks as bonds and other interest rate-sensitive assets had lost considerable value as rates rose dramatically over the past year.

Using the most recent data, the Federal Reserve reported bank deposits were down 6% for the week ending April 12 versus a year ago. Deposits have been falling year-over-year since November, off slightly at $17.2 trillion compared to the highest-ever $18.2 trillion level seen in April last year.

Further declines in deposits should lead to fewer loans written, fewer loans slows economic growth. This in part, accounts for why there is a lag between when the Fed drains and when it has an impact on inflationary pressures.

Take Away

M2 is an important gauge of future inflation. Because of this, the release of data may cause economists to change their May FOMC meeting forecast. A large decline may cause the Fed to pause, if M2 resumed its path upward the Fed may become more hawkish. Efforts to help the banking system last month, may have reinflated money supply, this will be a very interesting report.

CULVER CITY, Calif., April 24, 2023 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, today announced ARK: Survival Ascended (“ASA”), the next-generation remaster of the beloved ARK: Survival Evolved, harnessing the power of Unreal Engine 5 (“UE5”), is expected to release on Xbox Series S/X, PC (Windows/Steam), and PlayStation 5 in August 2023.

ASA is expected to be available as a standalone package on all platforms at $59.99. This comprehensive package will contain the remastered and next-generation optimized content, including The Island, a revamped Survival of the Fittest, and other DLCs and maps (including Scorched Earth, Aberration, Extinction, Genesis Part 1 & Part 2, Fjordur, Ragnarok, The Center, Lost Island, Valguero, and Crystal Isles).

Upon launch, ASA players will gain access to The Island, Survival of the Fittest and Scorched Earth. The other DLCs will be added over time. The game will showcase significant improvements and enhancements and ongoing planned updates with new features, content drops, creatures, items, structures, and DLC. Survival of the Fittest will be integrated into ASA as a new fully-supported game mode, backed by a dedicated development team concentrating on gameplay changes and adjustments. Moreover, a new canonical-story expansion pack for ASA is expected to be available in Q4 2023, introducing four new creatures and more details to be revealed later this year.

Snail is committed to delivering the finest gaming experience and will continue to support the next generation of ARK with continuous updates and enhancements.

Jim Tsai, Chief Executive Officer of Snail, commented, “We are excited to bring ASA to our loyal players and new audiences alike. Leveraging the power of UE5, we aim to elevate the iconic ARK gaming experience to new heights, providing enhanced visuals, gameplay, and features that will engage the community for years to come.”

About Snail, Inc.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future plans and objectives related to the release of ASA, including but not limited to, the timing of the release, the pricing of ASA, the content and features of ASA, the release of the expansion pack for ASA. The statements Snail makes regarding the following matters are forward-looking by their nature: growth prospects and strategies; launching new games and additional functionality to games that are commercially successful; expansion of upcoming games; its ability to develop new video games and enhance existing games; its relationships with third-party platforms such as Xbox Live and Game Pass, PlayStation Network, Steam, Epic Games Store, Google Stadia, the Apple App Store, the Google Play Store and the Amazon Appstore; assumptions underlying any of the foregoing.

FLORHAM PARK, N.J., April 24, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease announced the Company received $1.4 million from the net sale of tax benefits to an unrelated, profitable New Jersey corporation pursuant to the Company’s participation in the New Jersey Technology Business Tax Certificate Transfer Net Operating Loss (NOL) program for State Fiscal Year 2021.

“We are pleased to receive funds from the New Jersey NOL program,” said Matthew Hill, Chief Financial Officer of PDS Biotech. “The funding will be beneficial to us as we transition our lead asset, PDS0101, into a registrational trial for the treatment of HPV16-positive metastatic or recurrent head and neck cancer.”

The New Jersey Technology Business Tax Certificate Transfer program enables qualified, unprofitable NJ-based technology or biotechnology companies with fewer than 225 US employees (including parent company and all subsidiaries) to sell a percentage of their NOL and research and development tax credits to unrelated profitable corporations. This allows qualifying technology and biotechnology companies with NOLs to turn tax losses and credits into cash proceeds to fund their growth and operations, including research and development or other allowable expenditures.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials. and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; to aid in the development of the Versamune® platform; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual, quarterly and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology. KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

SAN DIEGO, April 24, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the first quarter 2023 after the close of market on Wednesday, May 3rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a Technology Company that develops and fields transformative, affordable systems, products and solutions for United States National Security, our allies and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems, and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, visit www.KratosDefense.com.

BOTHELL, Wash., April 24, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (Cocrystal or the Company) announces the appointment of Fred Hassan to its Board of Directors, increasing its Board membership to six. Mr. Hassan’s distinguished 40-year career includes serving in senior executive and director positions at global pharmaceutical companies and leading investment firms. Earlier this month, Cocrystal announced Mr. Hassan’s $2 million investment in the Company through an at-the-market private placement.

“It’s an honor to attract such a highly accomplished industry veteran to our Board,” said Roger Kornberg, PhD, Cocrystal Chairman, Chief Scientist and Chairman of the Scientific Advisory Board. “We expect that Fred’s significant experience will strengthen our corporate governance and his guidance will be instrumental in advancing our antiviral pipeline. On behalf of my fellow Directors, I welcome Fred and look forward to working together.”

“I appreciate Cocrystal’s tremendous potential in developing safe and effective antiviral therapies in priority indications of global concern,” said Mr. Hassan. “I’m impressed with the ability of the company’s structure-based discovery platform technology to efficiently discover and develop novel drug candidates. I look forward to working closely with Cocrystal’s Board and executive leadership to advance our pipeline toward commercialization.”

Mr. Hassan is Chairman of the investment firm Caret Group and a Director of Warburg Pincus LLC, a global private equity firm. From 2003 to 2009 Mr. Hassan served as Chairman and Chief Executive Officer of Schering-Plough and from 2001 to 2003 he was Chairman and Chief Executive Officer of Pharmacia Corporation, a company via the merger of Monsanto Company and Pharmacia & Upjohn, Inc. He joined Pharmacia & Upjohn, Inc. as Chief Executive Officer in 1997. Earlier in his career Mr. Hassan held leadership positions with Wyeth, including serving as Executive Vice President and as a Director from 1995 to 1997, and with Sandoz Pharmaceuticals, including leading its U.S. pharmaceuticals business.

Mr. Hassan is a Director of Precigen, Inc., BridgeBio Pharma and Prometheus Biosciences, Inc., which earlier this month announced a definitive agreement to be acquired by Merck for approximately $10.8 billion. Previously he was a Director of Amgen, Inc. and Time Warner Inc. (now Warner Media, LLC). Over the course of his career, he has served on various other Boards including at Avon Products, Inc. and Bausch & Lomb, which was acquired by Valeant Pharmaceuticals International, Inc.

Mr. Hassan has chaired several prominent pharmaceutical industry organizations including The Pharmaceutical Research and Manufacturers of America (PhRMA) and The International Federation of Pharmaceutical Manufacturers Associations (IFPMA). He received a BS in chemical engineering from the Imperial College of Science and Technology at the University of London and an MBA from Harvard Business School.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the advancement of the Company’s pipeline toward commercialization and the Company’s potential for developing safe and effective antiviral therapies in priority indications of global concern. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from inflation, interest rate increases, the current banking crisis and the Ukraine war on our Company, our collaboration partners, and on the U.S., U.K., Australia and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions including any adverse impacts on our ability to obtain raw materials and test animals as well as similar problems with our vendors and our current Contract Research Organization (CRO) and any future CROs and Contract Manufacturing Organizations, the results of the studies for CC-42344 and CDI-988, the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of future preclinical and clinical trials, the impact of COVID-19 (including long-term and pervasive effects of the virus), general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

SASKATOON, Saskatchewan, Canada, Apr. 24, 2023 – MustGrow Biologics Corp. (TSXV: MGRO) (OTC: MGROF) (FRA: 0C0) (the “Company” or “MustGrow”), announces that it will be hosting an investor webcast on Wednesday, April 26th at 4:00pm ET. MustGrow’s management team will be presenting on recent corporate progress, biological industry developments, and upcoming catalysts. The presentation will be followed by an audience Q&A session.

Live Webcast: Wednesday, April 26th at 4:00pm ET / 1:00pm PT Register/View Here Please join/register at least 5 minutes prior to the call.

Before April 26th, please email questions to info@mustgrow.ca to be addressed during the Q&A portion of the webcast.

Sustainbile Food Security

One significant industry catalyst to be discussed during the webcast is the demand for safe and sustainable food security solutions. The interest in natural crop protection, food preservation, and fertility products is increasing as farmers, consumers, regulators, and investors seek organic alternatives to synthetic chemicals and fertilizers. Safe and effective solutions will be needed for future food security and environmentally sustainable agriculture.

Throughout 2022, MustGrow engaged in extensive market research, formulation activities, and prospective partnership discussions, and has added Soil Amendment and Biofertility programs to its growing global intellectual property portfolio which now covers: Biocontrol applications (including preplant soil fumigation, postharvest food preservation, bioherbicide), and now Soil Amendment and Biofertility applications.

MustGrow believes its Soil Amendment and Biofertility initiative will complement existing Biocontrol programs, which are currently under development with four global partners: Janssen PMP, Bayer, Sumitomo Corporation, and NexusBioAg. These four partnered programs continue to achieve performance milestones and expand globally in scope and investment. MustGrow believes 2023 will be a pivotal year for commercial and strategic advancement in certain regions and crops.

———

About MustGrow

MustGrow is an agriculture biotech company developing organic biocontrol, soil amendment and biofertility products by harnessing the natural defense mechanism and organic materials of the mustard plant to sustainably protect the global food supply and help farmers feed the world. MustGrow and its leading global partners — Janssen PMP (pharmaceutical division of Johnson & Johnson), Bayer, Sumitomo Corporation, and Univar Solutions’ NexusBioAg — are developing mustard-based organic solutions to potentially replace harmful synthetic chemicals. Concurrenly, with new formulations derived from food-grade mustard, the Compmany is pursusing the adoption and use of it’s technology in the soil amendment and biofertily markets. Over 150 independent tests have been completed, validating MustGrow’s safe and effective approach to crop and food protection and yield enhancements. Pending regulatory approval, MustGrow’s patented liquid products could be applied through injection, standard drip or spray equipment, improving functionality and performance features. Now a platform technology, MustGrow and its global partners are pursuing applications in several different industries from preplant soil treatment and weed control, to postharvest disease control and food preservation, to soil amendment and biofertility. MustGrow has approximately 49.7 million basic common shares issued and outstanding and 55.6 million shares fully diluted. For further details, please visit www.mustgrow.ca.

Certain statements included in this news release constitute “forward-looking statements” which involve known and unknown risks, uncertainties and other factors that may affect the results, performance or achievements of MustGrow.

Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects”, “is expected”, “budget”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved”. Examples of forward-looking statements in this news release include, among others, statements MustGrow makes regarding: (i) the investor webcast to be held on April 26th 2023; (ii) the ability of MustGrow’s Soil Amendment and Biofertility initiative to complement existing Biocontrol programs currently under development; and (iii) the anticipated commercial and strategic advancement of MustGrow in certain regions and crops in 2023.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual results of MustGrow to differ materially from those discussed in such forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, MustGrow. Important factors that could cause MustGrow’s actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: (i) the preferences and choices of agricultural regulators with respect to product approval timelines; (ii) the ability of MustGrow’s partners to meet obligations under their respective agreements; and (iii) other risks described in more detail in MustGrow’s Annual Information Form for the year ended December 31, 2021 and other continuous disclosure documents filed by MustGrow with the applicable securities regulatory authorities which are available at www.sedar.com. Readers are referred to such documents for more detailed information about MustGrow, which is subject to the qualifications, assumptions and notes set forth therein.

This release does not constitute an offer for sale of, nor a solicitation for offers to buy, any securities in the United States.

Neither the TSXV, nor their Regulation Services Provider (as that term is defined in the policies of the TSXV), nor the OTC Markets has approved the contents of this release or accepts responsibility for the adequacy or accuracy of this release.