U.S. equities slid sharply Thursday as geopolitical tensions in the Middle East reignited volatility across global markets. A renewed surge in crude oil prices, combined with uncertainty surrounding the expanding conflict involving Iran, pushed investors toward risk-off positioning and weighed heavily on major indices.

The Dow Jones Industrial Average fell more than 800 points, dropping roughly 1.8% in afternoon trading. The S&P 500 declined about 0.8%, while the Nasdaq Composite slipped approximately 0.6%, reflecting broad selling pressure across sectors as investors reassessed geopolitical and inflation risks.

At the center of the market’s concern is the escalating confrontation between the U.S.-Israel coalition and Iran. The conflict has now entered its sixth day, with reports indicating continued military strikes across the region. U.S. officials said more than 2,000 targets have been hit, while the White House indicated American forces are moving toward what it described as “complete and total control of Iranian airspace.”

For markets, the immediate concern is energy supply.

Iran is the fourth-largest producer in OPEC, and disruptions to its production capacity or shipping routes through the Strait of Hormuz could ripple through global oil markets. Even the perception of supply disruption has been enough to drive crude prices higher.

West Texas Intermediate crude futures rose toward $79 per barrel, while Brent crude climbed above $84, marking a renewed rally in energy prices after a brief pullback earlier this week.

Higher oil prices often feed directly into inflation expectations — a dynamic that has quickly caught the attention of investors already watching the Federal Reserve’s next policy moves. Rising energy costs can push transportation, manufacturing, and consumer prices higher, potentially complicating the Fed’s interest rate outlook if inflation proves sticky.

The ripple effects were visible across other asset classes Thursday.

Despite its reputation as a safe-haven asset, gold fell more than 1%, pressured by a stronger U.S. dollar. When the dollar strengthens, commodities priced in dollars become more expensive for international buyers, often weighing on prices.

Other precious metals followed suit. Silver, platinum, and palladium also declined, reflecting a broader commodities pullback outside of oil.

Meanwhile, Treasury markets also saw movement, with 10-year yields rising as bond prices fell. Higher yields can add another layer of pressure to equities by increasing borrowing costs and reducing the relative attractiveness of stocks compared with fixed income.

Energy costs are already filtering into the real economy.

According to AAA data, the national average gasoline price climbed to $3.25 per gallon, up $0.27 from a week ago. Diesel prices have risen even more sharply, jumping $0.41 to $4.16 per gallon, their highest level since 2023. Diesel plays a critical role in shipping, trucking, and industrial activity, meaning sustained increases could amplify inflation across supply chains.

Looking ahead, markets may remain sensitive to both geopolitical headlines and incoming economic data.

Friday’s U.S. monthly jobs report is expected to provide the next major signal about the health of the labor market and whether economic momentum remains strong despite mounting global uncertainty.

Investors will also watch corporate earnings releases after the closing bell Thursday from Costco and Marvell Technology, which could provide additional insight into consumer demand and technology spending trends.

For now, however, the primary driver of market sentiment remains geopolitical risk — and the unpredictable path of oil prices that often accompanies it.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Canadian government steps up with financial support. First Phosphate received conditional approval for up to C$16.7 million in non-repayable funding through Natural Resources Canada under the Global Partnerships Initiative. The contribution will fund the assessment of technical and engineering parameters, including processing circuits and equipment, needed to validate the company’s ability to produce battery-grade phosphate concentrate aligned with its definitive offtake agreement. The funding supports study activities through 2028. First Phosphate received US$523,017 under a long-term phosphate concentrate offtake agreement, reinforcing commercial validation and establishing initial cash flow tied to downstream demand.

Phosphate added to Canada’s critical minerals list. The Canadian federal government amended the 2025 budget to include phosphate as a critical mineral essential for clean technology. This designation makes First Phosphate eligible for the 30% Critical Mineral Exploration Tax Credit (CMETC) and the 30% Clean Technology Manufacturing Investment Tax Credit (CTM). The CMETC enhances the company’s ability to raise exploration capital, while the CTM offers the potential to materially reduce downstream capital intensity for the planned phosphoric acid and LFP cathode active material facilities.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

USA Rare Earth (NASDAQ: USAR) announced a definitive agreement to acquire Texas Mineral Resources Corp. (OTCQB: TMRC) in an all-stock transaction valued at approximately $73 million, a deal that would consolidate ownership of one of the most significant rare earth deposits in the United States. The transaction centers on the Round Top Heavy Rare Earth and Critical Minerals Project in West Texas, a large domestic resource that has drawn increasing attention amid global efforts to secure critical mineral supply chains.

Texas Mineral Resources currently holds an approximately 19% minority interest in the Round Top project, while USA Rare Earth operates the development through a joint venture structure. By acquiring Texas Mineral Resources, USA Rare Earth would effectively gain full ownership of the project, simplifying governance and aligning development strategy under a single operator. The companies said the transaction will be completed through the issuance of roughly 3.8 million shares of USA Rare Earth common stock to TMRC shareholders, with closing expected by the third quarter of 2026, subject to shareholder approval and customary closing conditions.

The Round Top deposit, located in Hudspeth County, Texas, roughly 85 miles southeast of El Paso, is considered one of the largest known deposits of heavy rare earth elements in North America. Heavy rare earths such as dysprosium and terbium are essential inputs for high-performance permanent magnets used in electric vehicles, defense technologies, robotics, and advanced electronics. As global demand for these materials continues to grow, governments and manufacturers have increasingly focused on developing domestic supply chains to reduce dependence on overseas processing and mining capacity.

USA Rare Earth has positioned Round Top as the cornerstone of its broader “mine-to-magnet” strategy, which aims to vertically integrate rare earth mining, processing, metal production, and magnet manufacturing within the United States. The company is advancing development of the deposit under an accelerated mining plan and has previously indicated that commercial production could begin later in the decade. At full scale, the operation is expected to process tens of thousands of metric tons of mineral feedstock per day by 2030, supporting the growing demand for critical materials used across high-technology and clean-energy industries.

The Round Top project also carries broader economic and strategic implications. Rare earth elements are widely considered critical to national security and advanced manufacturing, and the United States has prioritized domestic production after decades of reliance on foreign suppliers. China currently dominates global rare earth refining capacity, creating supply chain vulnerabilities that policymakers have increasingly sought to address through investment, policy initiatives, and support for domestic mining projects.

The consolidation of Round Top under a single owner may streamline project financing, engineering development, and permitting processes as the project moves toward the construction phase. USA Rare Earth has previously engaged engineering and infrastructure partners to support feasibility work and project planning tied to the future development of the mine and associated processing facilities.

For investors watching the rare earth and critical minerals sector, the acquisition underscores a broader trend of consolidation and vertical integration as companies seek to control strategic resources and build domestic supply chains. As demand for rare earth elements continues to expand across electric vehicles, renewable energy systems, and advanced electronics, projects like Round Top remain central to the evolving landscape of U.S. critical mineral development.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)—a high–grade Copper–PGE, Nickel, gold and silver system—toward Canada’s next polymetallic mine. On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~212.86 km² and roughly 50 km of prospective basin margins. Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs. Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025. It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s JabalSaid Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Expansion of Lion mineralization. Recent drilling at Lion East and Lion West resulted in a newly identified shallow eastward plunging structural trend that controls high grade copper mineralization and extends the Lion system beyond its previously defined limits. Step-out drilling expanded mineralization both east and west, and the emerging structural model may vector toward a larger nickel copper source at depth, enhancing the project’s long-term potential.

Encouraging results at Lion West. Drilling intersected massive nickel-bearing sulphide within the UM zone, indicating the presence of a deeper nickel-palladium-copper system much like mineralization observed at Tiger. Follow-up drilling is underway to better define the geometry and relationship to the Lion geological stratigraphy.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VIRGINIA CITY, NEVADA, March 3, 2026 — Comstock Inc. (NYSE: LODE) (“Comstock” and the “Company”) and Comstock Metals LLC (“Comstock Metals”), a leader in the responsible recycling of end-of-life solar panels with the only certified, North American, zero-landfill solution, announced today that significant portions of the industry-scale facility precision equipment, manufactured on proprietary specifications, has arrived at our Silver Springs, Nevada location for installation, testing and ultimate integration of the 100,000 ton per year solar panel recycling production line. Commissioning will continue through March 2026, and into early April with operations planned during the second quarter of this year.

The manufacture of precision-machined equipment for Comstock Metals’ proprietary solar panel recycling begins with a highly engineered design process focused on durability, accuracy, speed, and maximizing throughput. Each system is modeled using advanced CAD platforms to ensure exact tolerances for shredding, conditioning, and ultimately, critical materials separation and recovery. The shredding systems are currently being assembled.

Shredding systems being installed at Comstock Metals’ new industry-scale facility in Silver Springs, NV.

“Our team is now fully deployed and engaged in every aspect of our facility upgrades, storage build out and the all of the work associated with commissioning our first industry-scale recycling process and we have now received the major front-end components of our proprietary shredding systems,” said Dr. Fortunato Villamagna, President of Comstock Metals. “Installation involves a plurality of activities, from complex tasks like the interconnection of the various unit operations, completing the communication interfaces between the various systems, to things as simple as precision leveling, anchoring to reinforced and epoxied flooring, operational and electrical integration with facility power infrastructure, and calibration of automated control systems. Our design allows us to commission and evaluate each unit operation independently as they are installed, effectively streamlining the process and accelerating the full start-up and eventual ongoing, continuous operations.”

Final receipt and integration of all major components will continue through March and into April when the Company will confirm operational efficiencies, safety compliance, and optimized workflows within the dedicated recycling platform. The Company remains on schedule for continuous operations during the second quarter.

The Company has also completed and submitted its first major operating permit application with the State of Nevada for our second, integrated, industry-scale facility located in Clark County, in southern Nevada and has also begun the engagement with the city, county, and surrounding industrial neighbors and community.

“Our disciplined approach with technology and systems readiness required a multi-year operation of the commercial demonstration facility, enabling this final, first of its kind design and ordering of the industrial-scale systems,” said Corrado De Gasperis, Executive Chairman and CEO of Comstock. “The ‘unit operation model’ deployed in the commercial demonstration facility is what enabled the Company to independently commission each part of the full scale plant independently, streamlining start-up. The project for readying, receiving, and commissioning this facility in Silver Springs is in full swing with frequent updates forthcoming on commissioning.”

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 [email protected]

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 [email protected]

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: future market conditions; future explorations or acquisitions; divestitures, spin-offs or similar distribution transactions, future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, divestitures, spin-offs or similar distribution transactions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; business opportunities, growth rates, future working capital, needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: adverse effects of climate changes or natural disasters; adverse effects of global or regional pandemic disease spread or other crises; global economic and capital market uncertainties; the speculative nature of gold or mineral exploration, and lithium, nickel and cobalt recycling, including risks of diminishing quantities or grades of qualified resources; operational or technical difficulties in connection with exploration, metal recycling, processing or mining activities; costs, hazards and uncertainties associated with precious and other metal based activities, including environmentally friendly and economically enhancing clean mining and processing technologies, precious metal exploration, resource development, economic feasibility assessment and cash generating mineral production; costs, hazards and uncertainties associated with metal recycling, processing or mining activities; contests over our title to properties; potential dilution to our stockholders from our stock issuances, recapitalization and balance sheet restructuring activities; potential inability to comply with applicable government regulations or law; adoption of or changes in legislation or regulations adversely affecting our businesses; permitting constraints or delays; challenges to, or potential inability to, achieve the benefits of business opportunities that may be presented to, or pursued by, us, including those involving battery technology and efficacy, quantum computing and generative artificial intelligence supported advanced materials development, development of cellulosic technology in bio-fuels and related material production; commercialization of cellulosic technology in bio-fuels and generative artificial intelligence development services; ability to successfully identify, finance, complete and integrate acquisitions, spin-offs or similar distribution transactions, joint ventures, strategic alliances, business combinations, asset sales, and investments that we may be party to in the future; changes in the United States or other monetary or fiscal policies or regulations; interruptions in our production capabilities due to capital constraints; equipment failures; fluctuation of prices for gold or certain other commodities (such as silver, zinc, lithium, nickel, cobalt, cyanide, water, diesel, gasoline and alternative fuels and electricity); changes in generally accepted accounting principles; adverse effects of war, mass shooting, terrorism and geopolitical events; potential inability to implement our business strategies; potential inability to grow revenues; potential inability to attract and retain key personnel; interruptions in delivery of critical supplies, equipment and raw materials due to credit or other limitations imposed by vendors; assertion of claims, lawsuits and proceedings against us; potential inability to satisfy debt and lease obligations; potential inability to maintain an effective system of internal controls over financial reporting; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to list our securities on any securities exchange or market or maintain the listing of our securities; and work stoppages or other labor difficulties. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Operational momentum continues. Nicola reported a significant increase in throughput of high-grade gold and silver mill feed from its partnership with Blue Lagoon Resources at the Dome Mountain Gold Project. Processing at the Merritt Mill has shifted from a gravity-and-flotation circuit to a flotation-only flowsheet, better aligning with the sulphide-hosted mineralization and enhancing recoveries, concentrate grades, and payable metal output. Ongoing plant upgrades are expected to improve efficiency and throughput. Underground development at Dome Mountain is progressing, with additional mining faces being prepared to support sustainable increases in mill feed tonnage.

Advancing the next phase of gold production at Dominion Creek. Dominion represents an additional driver of growth, targeting high-grade gold mineralization. Nicola is procuring needed mobile equipment and personnel ahead of the planned extraction in July 2026 under a bulk sample permit. The bulk sample program is intended to validate grade continuity, metallurgical performance, and mining selectivity, while also contributing incremental cash flow.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Recent assay results confirm strong nickel-cobalt grades. Aurania reported results from 28 new samples at the Balangero Nickel-Cobalt Project in northern Italy, returning nickel values between 1,560 and 2,015 parts per million (ppm) and averaging 1,763 ppm, along with 81.5 to 108 ppm cobalt and 16.2 to 146 ppm copper. These results align with more than 200 historical samples and validate the presence of awaruite, a nickel-iron alloy suitable to be used as a direct source of furnace feed for stainless steel production or processed downstream EV battery-grade nickel sulphate production. Notably, samples from development rock piles were confirmed to be asbestos-free, potentially expanding the resource base beyond tailings.

A differentiated alternative to greenfield peers. Unlike comparable awaruite-focused projects, which require full mine development, Balangero’s potential resource consists primarily of dry-stacked, pre-crushed tailings and surface rock already extracted from the ground. This eliminates the need for drilling, blasting, and underground haulage. The project benefits from electric power, rail access, highway connectivity, and an available skilled workforce, positioning it as a potentially accelerated development opportunity with significant cost advantages.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VANCOUVER, B.C, February 26, 2026, – Nicola Mining Inc. (the “Company” or “Nicola”) (TSXV: NIM) (OTCQB: HUSIF) (FSE: HLIA) (the “Company” or “Nicola Mining”) is pleased to report a material increase in throughput of high-grade gold and silver mill feed sourced from its partnership with Blue Lagoon Resources (CSE: BLLG) at the Dome Mountain Gold Project.

High-grade gold and silver material is being processed at Nicola’s fully permitted Merritt Mill, where the Company has transitioned from gravity & flotation gold recovery to a flotation-only recovery circuit to suit the new mill feed and to streamline production. This optimization reflects the sulphide-hosted nature of the mineralization and is designed to enhance metallurgical recoveries, improve concentrate grades, and maximize payable metal content. The resulting high-grade gold-silver flotation concentrate is sold to Ocean Partners UK Limited[1] (“Ocean Partners”)., a globally recognized metals trading and finance group.

The transition from gravity-centric recovery to a flotation-focused flowsheet has been executed without operational disruption. Incremental plant upgrades and circuit refinements are being implemented concurrently with production to further improve recoveries, throughput stability, and operating efficiencies. Underground development at Dome Mountain continues, with additional mining faces being prepared to sustainably increase mill feed tonnage.

In parallel, Nicola has initiated procurement of key mobile equipment and personnel in preparation for planned extraction at its Dominion Gold Project. The Dominion project hosts structurally controlled, high-grade gold. which Nicola intends to commence extraction under a bulk sample permit in July 2026. Gold production will allow validation of grade continuity, metallurgical performance, and mining selectivity while further augment the Company’s cash flow.

Peter Espig, CEO of Nicola, stated, “Nicola continues to systematically advance its near-, mid-, and long-term development strategy. Our integrated milling infrastructure, coupled with high-grade feed sources in a premier mining jurisdiction, provides operating leverage to strengthening precious and base metal markets. Concurrently, we remain focused on achieving our planned Q1 2026 NASDAQ uplisting.”

Qualified Person

Cameron Lilly, P. Eng., the Company’s Mill Manager, is the Qualified Person as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects and supervised the preparation of, and has reviewed and approved, the technical information in this release.

About Nicola Mining

Nicola Mining Inc. is a junior mining company listed on the Exchange and Frankfurt Exchange that maintains a 100% owned mill and tailings facility, located near Merritt, British Columbia It has signed Mining and Milling Profit Share Agreements with high grade gold projects. Nicola’s fully permitted mill can process both gold and silver mill feed via gravity and flotation processes.

The Company owns 100% of the New Craigmont Project, a high-grade copper property, which covers an area of over 10,800 hectares along the southern end of the Guichon Batholith and is adjacent to Highland Valley Copper, Canada’s largest copper mine. The Company also owns 100% of the Treasure Mountain Property, which is a fully-permitted high grade silver mine and includes 30 mineral claims and a mineral lease, spanning an area exceeding 2,200 hectares.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

[1] Ocean Partners operates in several countries throughout the world. Ocean Partners maintains a strong global network of relationships and contacts in the base metal mining and smelting sector.

Saguenay, Quebec–(Newsfile Corp. – February 25, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the launch of its sponsored Level 1 American Depositary Receipt (“ADR“) program to increase exposure to American and international investors wishing direct access to Quebec igneous phosphate and the downstream lithium iron phosphate (“LFP“) battery supply chain.

The First Phosphate ADR is now available for trading in the United States on the OTCQX market under the symbol “FPHOY” (CUSIP: 33611D301; ISIN: US33611D3017).

The First Phosphate ADR is the first Canadian Level 1 company-sponsored ADR to trade on OTC Markets. The ADR ratio is set to ten (10) First Phosphate common shares for each (1) First Phosphate ADR.

Participants may issue ADRs at no cost during the first 6 months after the effectiveness date of the program (February 12, 2026) through The Bank of New York Mellon (“BNY“) which has been appointed as depositary bank for the First Phosphate ADR program.

The new First Phosphate ADR is complimentary to all other Company listings on all other stock exchanges and does not affect the Company’s current OTCQX listed common shares under symbol “FRSPF“.

BNY facilitates the issuance and cancellation of First Phosphate ADRs in accordance with instructions received from market participants. The First Phosphate ADR program operates in accordance with a deposit agreement, filed with the United States Securities and Exchange Commission (“SEC“) and available through https://www.sec.gov/Archives/edgar/data/2108542/000101915526000028/0001019155-26-000028-index.htm. The First Phosphate common shares underlying the First Phosphate ADRs are held in custody by BNY.

The establishment of the First Phosphate ADR program is not a new offering of securities and, therefore, no additional shares are being issued nor is any capital being raised in connection with the launch of the First Phosphate ADR program. Moreover, nothing herein shall be deemed to constitute an offer to sell or a solicitation of an offer to buy securities.

An ADR is a separate security denominated in US dollars that allows US investors to invest in shares of non-US companies without the need for cross-border or cross-currency transactions.

Initial Payment Received Under Long-term Offtake Agreement

The Company has now received the initial payment of USD $523,017.59 in respect of the existing, long-term phosphate concentrate offtake agreement with its existing offtake partner as announced on January 6, 2026 (https://firstphosphate.com/offtakepayment).

Options Exercise & RSU Grants

Z Six Financial Corporation, an entity controlled by Laurence W. Zeifman, Chaiman of the Board of First Phosphate, has exercised 300,000 options originally issued on September 14, 2022 and exercisable at $0.25 and 300,000 options originally issued on December 22, 2022 and exercisable at $0.35 per option.

Pursuant to an exemption granted by the Canadian Securities Exchange to Policy 6.5(7), the Company has issued 781,395 Restricted Share Units (“RSUs“) to ExpoWorld Ltd. (“ExpoWorld“), an entity controlled by John Passalacqua, CEO of First Phosphate, as consideration for the termination of 1,200,000 options held by ExpoWorld including 600,000 options originally issued on September 14, 2022 and exercisable at $0.25 per option, and 600,000 options originally issued on December 22, 2022 and exercisable at $0.35 per option (the “Options“). These vested RSUs represent the in-the-money value of the Options being terminated (calculated based on the closing price of First Phosphate shares on February 10, 2026) and serve to facilitate the cashless exercise of options while minimizing the impact that the transaction would have on the open market.

The Company also informs that Mr. Passalacqua, through ExpoWorld, made an open market purchase of 119,500 shares in the open market on January 30, 2026.

As a show of commitment to the business and alignment with shareholders, the Board and management will receive approximately 50% of their total compensation in the form of RSUs. As such, the Board has approved the grant of 1,975,000 RSUs to eligible directors, officers, consultants and employees of the Company for services to be provided for the 12-month period commencing March 1, 2026. One-half of these new RSUs will vest on August 31, 2026 and February 28, 2027, respectively. All of the common shares issuable on vesting of the RSUs will be subject to a hold period of four months plus one day from the date of vesting. The RSUs will be granted in accordance with and subject to the Company’s Omnibus Equity Incentive Plan.

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration, development and cleantech company dedicated to examining and ultimately building and onshoring a vertically integrated mine-to-market lithium iron phosphate (LFP) battery supply chain for North America. Target markets include energy storage, data centers, robotics, mobility and national security.

First Phosphate’s flagship Bégin-Lamarche Property in Saguenay–Lac-Saint-Jean, Quebec, Canada is a North American rare igneous phosphate resource yielding high-purity phosphate with minimal impurities.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2026 guidance. InPlay approved a C$66 to C$74 million capital program targeting average production of 18,600 to 19,200 boe/d (~61% light oil and NGLs), representing approximately 11% growth over the estimated 2025 production of ~17,000 boe/d. Management forecasts adjusted funds flow (AFF) of C$122 to C$129 million and free adjusted funds flow (FAFF) of C$48 to C$63 million, implying an 11% to 15% FAFF yield. Year-end net debt is guided to C$199 to C$206 million, reflecting continued deleveraging.

Estimate revisions. We have adjusted our 2026 estimates to average production of 18,900 boe/d, revenue of C$338.3 million, and AFF of C$125.2 million, or C$4.45 per share. For Q1 2026, we have assumed production of 18,605 boe/d, revenue of C$79.0 million, and AFF of C$26.6 million, or C$0.95 per share. The first quarter carries heavier drilling activity, with five wells drilled and completed, most coming onstream late in the period, marking Q1 as the lightest production quarter of the year. We forecast 2026 capital expenditures of C$70 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated feasibility study. Century released the results of its 2026 NI 43-101 feasibility study for the 100%-owned Angel Island Lithium Project in Esmeralda County, Nevada. The updated study reflects engineering optimization and improvements that materially strengthen the project’s economic profile and highlight Angel Island as one of the most significant and economically robust sedimentary lithium developments in the United States.

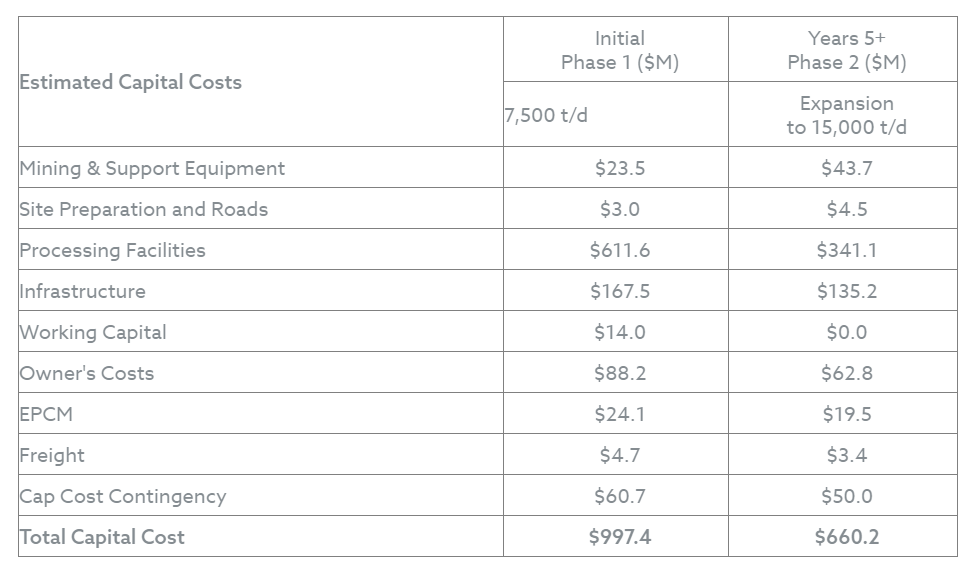

Lower initial capital expenditures. Phase I initial capital expenditures are estimated to be $997 million, a significant reduction from the $1.5 billion outlined in the 2024 Study. The updated study streamlines development into a two-phase approach. Phase I contemplates 7,500 tonnes per day (tpd) of mill feed, expanding to 15,000 tpd in Phase II beginning in Year 5. Phase II expansion capital is estimated at $660 million. A previously planned third expansion phase has been eliminated, lowering overall capital requirements. The economic analysis is based on a 40-year production schedule, with planned life-of-mine average production of 26,500 tonnes per annum of battery-grade lithium carbonate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

VIRGINIA CITY, NEVADA, February 23, 2026 – Comstock Inc. (NYSE: LODE) (“Comstock” or the “Company”) and its subsidiary, Comstock Metals LLC (“Comstock Metals”), a leader in the responsible recycling of end-of-life solar panels and the only certified, zero-landfill solar recycling solution in North America, today announced that following the opening of its facility in Kings County, CA, it has received approval from California’s Department of Toxic Substances Control (“DTSC”) and has been placed on a very select list of companies authorized as universal waste recyclers that can treat photovoltaic (“PV”) modules. The recently opened facility in combination with this new “certification” now avails California companies with a true “California solution” for recycling end of life PV solar panels that is authorized by the DTSC and supported by several strategic customers.

This new California facility, and recent certification, marks a regional expansion and optimization of Comstock Metals’ southwestern recycling network, reinforcing the company’s commitment to serving high-demand California-based renewable energy customers. Strategically located to optimize logistics and support customers across California—the single largest end-of-life U.S. solar panel market by far—the site will operate as a centralized hub for the collection, preparation, storage, and aggregation of decommissioned PV solar panels.

As increasing numbers of solar panels reach the end of their useful life across California, Arizona and Nevada, demand is rapidly growing for compliant, environmentally responsible recycling solutions. The California facility is purpose-built to meet this need, providing major utilities, developers, engineering and construction firms (EPCs), installers, decommissioning contractors, and asset owners with a dependable, locally based option for managing these environmental liabilities. Through advanced recovery processes, valuable materials—including aluminum, silver, copper, gallium, and other metals—can eventually be extracted and returned to the supply chain for reuse.

“Opening a facility in California positions us to better serve the region’s increasing demand for end-of-life solar panel disposal while delivering a streamlined, cost-effective logistics solution for our customers,” said Dr. Fortunato Villamagna, President of Comstock Metals. “Our mission is to close the loop on solar energy by ensuring the environmental liabilities associated with these retired panels are safely, cleanly and completed eliminated so they do not find their way into landfills and ultimately, our natural water and broader eco-systems.”

By delivering timely, efficient, and fully compliant decommissioning, transportation, and recycling services, Comstock’s zero-landfill solution minimizes waste, preserves natural resources, and advances the long-term sustainability of the solar industry. The Company is also completing permit applications and preparing submission plans for a second, integrated, industry-scale facility in Nevada, with final site selection expected later this month.

“As the number of end-of-life solar panels nationwide rises into the tens and eventually hundreds of millions, our ability to scale responsibly and efficiently ensures meaningful sustainability outcomes—and confidence—for our customers and partners,” said Corrado De Gasperis, Executive Chairman and CEO of Comstock. “Our team is establishing a new benchmark for solar panel recycling through a growing, fully integrated national network.”

About Comstock Inc.

Comstock Inc. (NYSE: LODE) innovates and commercializes technologies, systems and supply chains that enable, support and sustain clean energy systems by efficiently, effectively, and expediently extracting and converting under-utilized natural resources into reusable metals, like silver, aluminum, gold, and other critical minerals, primarily from end-of-life photovoltaics. To learn more, please visit www.comstock.inc.

Comstock Social Media Policy

Comstock Inc. has used, and intends to continue using, its investor relations link and main website at www.comstock.inc in addition to its X.com, LinkedIn and YouTube accounts, as means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD.

Contacts

For investor inquiries: Judd B. Merrill, Chief Financial Officer Tel (775) 413-6222 [email protected]

For media inquiries: Zach Spencer, Director of External Relations Tel (775) 847-7573 [email protected]

Forward-Looking Statements

This press release and any related calls or discussions may include forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of historical facts, are forward-looking statements. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” “plan,” “forecast,” “seek,” “target,” “should,” “intend,” “may,” “will,” “would,” “potential” and similar expressions identify forward-looking statements but are not the exclusive means of doing so. Forward-looking statements include statements about matters such as: expectations regarding the completion of the proposed securities offering, future market conditions; future explorations or acquisitions, divestitures, spin-offs or similar distribution transactions; future changes in our research, development and exploration activities; future financial, natural, and social gains; future prices and sales of, and demand for, our products and services; land entitlements and uses; permits; production capacity and operations; operating and overhead costs; future capital expenditures and their impact on us; operational and management changes (including changes in the Board of Directors); changes in business strategies, planning and tactics; future employment and contributions of personnel, including consultants; future land and asset sales; investments, acquisitions, joint ventures, strategic alliances, business combinations, operational, tax, financial and restructuring initiatives, including the nature, timing and accounting for restructuring charges, derivative assets and liabilities and the impact thereof; contingencies; litigation, administrative or arbitration proceedings; environmental compliance and changes in the regulatory environment; offerings, limitations on sales or offering of equity or debt securities, including asset sales and associated costs; and future working capital needs, revenues, variable costs, throughput rates, operating expenses, debt levels, cash flows, margins, taxes and earnings. These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical and current trends, current conditions, possible future developments and other factors they believe to be appropriate. Forward-looking statements are not guarantees, representations or warranties and are subject to risks and uncertainties, many of which are unforeseeable and beyond our control and could cause actual results, developments and business decisions to differ materially from those contemplated by such forward-looking statements. Some of those risks and uncertainties include the risk factors set forth in our filings with the SEC and the following: sales of, and demand for, our products, services, and/or properties; industry market conditions, including the volatility and uncertainty of commodity prices; the speculative nature, costs, regulatory requirements, and hazards of natural waste resource identification, exploration, development, availability, recycling, extraction, processing, and refining activities, including operational or technical difficulties, and risks of diminishing quantities or insufficiency of grades of qualified resources;; changes in our planning, exploration, research and development, production, and operating activities; research and development, exploration, production, operating, and other variable and fixed costs; throughput rates, margins, earnings, debt levels, contingencies, taxes, capital expenditures, net cash flows, and growth; restructuring activities, including the nature and timing of restructuring charges and the impact thereof; employment and contributions of personnel, including our reliance on key management personnel; the costs and risks associated with developing new technologies; our ability to commercialize existing and new technologies; the impact of new, emerging, and competing technologies on our business; the possibility of one or more of the markets in which we compete being impacted by political, legal, and regulatory changes, or other external factors over which we have little or no control; the effects of mergers, consolidations, and unexpected announcements or developments from others; the impact of laws and regulations, including permitting and remediation requirements and costs; changes in or elimination of laws, regulations, tariffs, trade, or other controls or enforcement practices, including the potential that we may not be able to comply with applicable regulations; changes in generally accepted accounting principles; adverse effects of climate changes, natural disasters, and health epidemics, such as the COVID-19 outbreak; global economic and market uncertainties, changes in monetary or fiscal policies or regulations, the impact of terrorism and geopolitical events, volatility in commodity and/or other market prices, and interruptions in delivery of critical supplies, equipment and/or raw materials; assertion of claims, lawsuits, and proceedings against us; potential inability to satisfy debt and lease obligations, including because of limitations and restrictions contained in the instruments and agreements governing our indebtedness; our ability to raise additional capital and secure additional financing; interruptions in our production capabilities due to equipment failures or capital constraints; potential dilution from stock issuances, recapitalization, and balance sheet restructuring activities; potential inability or failure to timely file periodic reports with the Securities and Exchange Commission; potential inability to maintain the listing of our securities on any securities exchange or market; and our ability to implement additional financial and management controls, reporting systems and procedures and comply with Section 404 of the Sarbanes-Oxley Act, as amended. Occurrence of such events or circumstances could have a material adverse effect on our business, financial condition, results of operations or cash flows, or the market price of our securities. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as may be required by securities or other law, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Neither this press release nor any related calls or discussions constitutes an offer to sell, the solicitation of an offer to buy or a recommendation with respect to any securities of the Company, the fund, or any other issuer.

After-tax NPV (using 8% discount rate) of $4.01 billion based on price assumptions of $24,000 per tonne (“/t”) for lithium carbonate (“Li2CO3”) and $750/dry metric tonne (“dmt”) for Sodium Hydroxide (“NaOH”)

After-tax internal rate of return (“IRR”) of 27.4%

Integrated patent-pending processing flowsheet, incorporating hydrochloric acid leaching, Direct Lithium Extraction (“DLE”), chlor-alkali processing, and on-site production of battery-grade lithium carbonate, validated through four years of pilot plant operations in Nevada

Large, long-life U.S.-based lithium development project, with Proven and Probable Reserves supporting a mine life exceeding 60 years

Economic analysis based on a 40-year production schedule, with planned life-of-mine average production of approximately 26,500 tonnes per annum (“tpa”) of battery-grade lithium carbonate

Initial Phase 1 throughput of 7,500 tonnes per day (“tpd”), expanding to 15,000 tpd in Year 5 (Phase 2)

Capital and Operating Costs

Phase I capital cost of $997 million compared to $1.537 billion in the 2024 Study

Phase 2 expansion capital of $660 million compared to $651 million in the 2024 Study

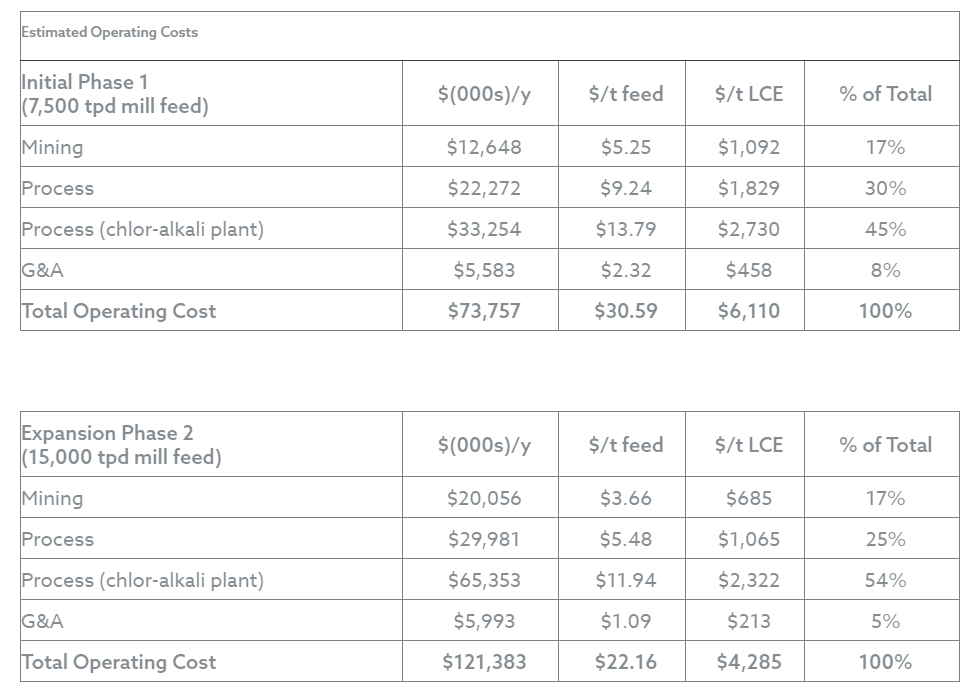

Average operating cost of $22.45 per tonne of mill feed, equivalent to $4,389 per tonne of lithium carbonate, compared to $8,223 per tonne in the 2024 Study

Project revenues from surplus sodium hydroxide equivalent to $5,393/t of lithium carbonate produced. When treated as a co-product credit, this would result in a net operating cost below zero

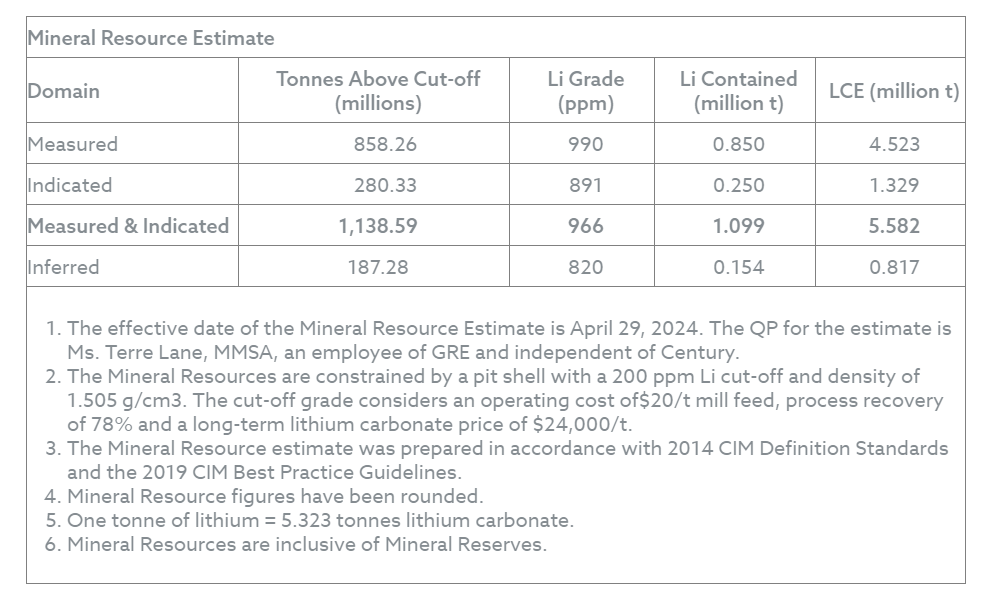

Mineral Resource and Reserve

Measured and Indicated Mineral Resources of 1.138 billion tonnes at 966 parts per million (“ppm”) lithium, containing 5.582 million tonnes lithium carbonate equivalent (“LCE”)

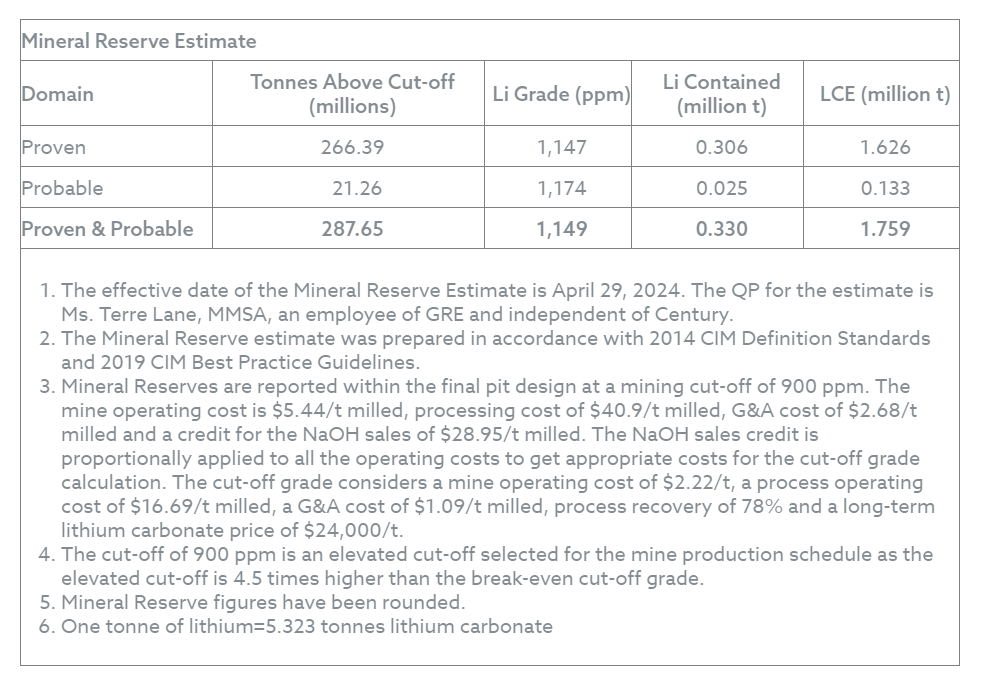

Proven and Probable Mineral Reserves of 287.65 million tonnes at 1,149 ppm lithium, containing 1.759 million tonnes LCE

February 23, 2026 – Vancouver, Canada – Century Lithium Corp. (TSXV: LCE) (OTCQX: CYDVF) (Frankfurt: C1Z) (“Century Lithium” or “the Company”) is pleased to announce the results of an updated National Instrument 43-101 (“NI 43-101”) compliant Feasibility Study (“2026 Feasibility Study”) for its 100%-owned Angel Island Lithium Project (“Angel Island”) located in Esmeralda County, Nevada, USA.

The 2026 Feasibility Study incorporates the results of continued metallurgical testing, engineering optimization, refinement of the mine plan, and updated capital and operating cost estimates for Angel Island. The study demonstrates strong project economics, including an after-tax net present value (“NPV”) of $4.01 billion.

No material changes were made to the Mineral Resource or Mineral Reserve estimates used in the “NI 43-101 Technical Report on the Feasibility Study of the Clayton Valley Lithium Project, Esmeralda County, Nevada, USA”, dated April 29, 2024 (“2024 Study”) and are used in their entirety in the 2026 Feasibility Study.

All currency amounts in this news release are expressed in U.S. dollars.

2026 FEASIBILITY STUDY SUMMARY

The 2026 Feasibility Study confirms the technical and economic viability of developing the Angel Island project as a significant domestic source of battery-grade lithium carbonate in the United States.

Mining is planned as a conventional open-pit operation extracting lithium-bearing claystone mineralization. Mined material will be processed on-site using hydrochloric acid leaching, solid-liquid separation, Direct Lithium Extraction (“DLE”), lithium carbonate precipitation, and an integrated chlor-alkali plant, resulting in on-site production of battery-grade lithium carbonate.

The 2026 Feasibility Study reconfigures Angel Island into a two-phase development plan, consisting of an initial 7,500 tpd operation with expansion to 15,000 tpd. The third expansion phase contemplated in the 2024 Study was removed, simplifying project execution and reducing overall capital requirements.

Bill Willoughby, President and CEO of Century Lithium commented:

“The results of the 2026 Feasibility Study represent a material improvement. These results were made possible by Century Lithium’s team who, through many steps of optimization including those at the Company’s pilot plant, have delivered a more efficient development plan for the Project. In the 2026 Feasibility Study, this streamlined process is reflected in equipment and related infrastructure, importantly in electrical demand, and is seen in the resulting capital and operating cost estimates.”

CAPITAL AND OPERATING COSTS

A Class 3 capital cost estimate was prepared in accordance with AACE guidelines, and Canadian Institute of Mining Metallurgy and Petroleum (“CIM”) Best Practices. The updated costs were developed using second-quarter 2025 data.

Phase 1 (7,500 tpd) initial capital cost: $997 million

Phase 2 (15,000 tpd) expansion capital cost: $660 million

Reductions to estimated capital costs in the 2026 Feasibility Study relative to the 2024 Study are attributable to:

Elimination of a previously planned third production phase

Simplification of project scope and installed capacity

Refinement of the mine scheduling and equipment selection

Processing flowsheet optimization informed by pilot plant operations

Updated vendor pricing and construction cost inputs

Operating costs benefit materially from Angel Island’s planned vertically integrated chlor-alkali facility, which generates hydrochloric acid and produces surplus sodium hydroxide for sale.

Average operating cost – Phase 1: estimated $30.58/t of mill feed

Average operating cost – Phase 2: estimated $22.16/t of mill feed

MINERAL RESOURCES AND MINERAL RESERVES

Mineral Resource and Mineral Reserve estimates used in the 2026 Feasibility Study are unchanged from the prepared in accordance with NI 43-101 and CIM Definition Standards.

Mineral Resources (inclusive of Mineral Reserves):

Measured and Indicated: 1.138 billion tonnes at 966 ppm lithium, containing 5.582 million tonnes LCE

Inferred: 187.28 million tonnes at 820 ppm lithium

Mineral Reserves:

Proven and Probable: 287.65 million tonnes at 1,149 ppm lithium, containing 1.759 million tonnes LCE

Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability

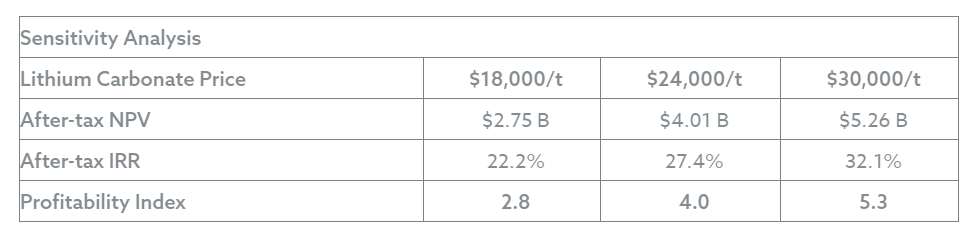

ECONOMIC ANALYSIS indicates Angel Island remains economically attractive across a wide range of commodity price and cost assumptions, with lithium price representing the most significant driver of Angel Island’s value.

Using a base-case lithium carbonate price of $24,000/t and an 8% discount rate, Angel Island generates:

After-tax NPV: $4.01 billion

After-tax IRR: 27.4%

Profitability Index: 4.0

Sensitivity analysis indicates Angel Island remains economically attractive across a wide range of commodity price and cost assumptions, with lithium price representing the most significant driver of Angel Island’s value.

NEXT STEPS

Century Lithium will continue to advance Angel Island toward development through submission of plan of operations, permitting, detailed engineering, and engagement with interested parties as the Project progresses toward a construction decision. Integral to these key steps are:

Recent appointment of Cormac O’Laoire, PhD to advise the Company in discussions with potential downstream partners and offtake interests. The Company continues to make inroads in Washington DC and Nevada to convey the importance of Angel Island for a secure North American supply chain.

Further evaluation of the economic potential for rare earth elements (“REE”) recovery at Angel Island.

Engagement of BMO Capital Markets to assist the Company in its efforts towards securing strategic interests and development funding.

Addition, in 2025 to the US Federal Permitting Dashboard for FAST-41 transparency status. Inclusion to FAST-41 increases the Project’s exposure to federal agencies and stakeholders to accelerate the permitting process.

SUMMARY OF 2026 NI 43-101 FEASIBILITY STUDY

This summary forms an integral part of this news release.

An NI 43-101 Feasibility Study on the Angel Island Lithium Project was prepared to update metallurgical results, mine planning assumptions, and capital and operating cost estimates relative to the 2024 Study.

Unless otherwise stated herein, Mineral Resource and Mineral Reserve estimates, geological interpretations, and environmental and permitting assumptions remain materially unchanged from the 2024 Study.

Property Description, Location, and Tenure

Angel Island is located in Esmeralda County, Nevada, USA, approximately 354 km southeast of Reno. Angel Island comprises 503 unpatented mining claims (276 placer and 227 lode claims) covering approximately 2,286 hectares, held 100% by Cypress Holdings (Nevada) Ltd., a wholly owned subsidiary of Century Lithium Corp. Existing royalty arrangements remain unchanged.

Geology, Mineralization, and Deposit Type

Angel Island hosts a large, flat-lying sedimentary lithium claystone deposit within the Esmeralda Formation. Lithium mineralization occurs primarily within claystone, tuffaceous mudstone, and siltstone units. No material changes were made to the geological model, mineralization interpretation, or deposit classification from the 2024 Study.

Exploration, Drilling, Sampling, and Data Verification

The Mineral Resource and Mineral Reserve estimates are supported by 45 drill holes totaling approximately 3,955 meters, completed between 2017 and 2022. Drilling includes conventional core and sonic drilling. Sample preparation, analytical methods, QA/QC protocols, and data verification procedures remain unchanged from the 2024 Study and meet CIM and NI 43-101 standards.

Mineral Resource Estimate (Unchanged from 2024 Study)

The Mineral Resource estimate has an effective date of April 29, 2024, and remains unchanged in the 2026 Feasibility Study.

Measured and Indicated Mineral Resources:

1.138 billion tonnes at an average grade of 966 ppm lithium, containing 5.582 million tonnes LCE

Inferred Mineral Resources:

187.28 million tonnes at an average grade of 820 ppm lithium, containing 0.817 million tonnes LCE

Mineral Resources are constrained by a pit shell using a 200 ppm lithium cut-off grade and assume a bulk density of approximately 1.5 tonnes per cubic meter (“t/m³”). Mineral Resources are inclusive of Mineral Reserves. Higher recoveries demonstrated through pilot-scale testing were determined to not materially affect the selected cut-off grade or the reported Mineral Resource tonnage or grade.

Mineral Reserve Estimate (Unchanged from 2024 Study)

The Mineral Reserve estimate also has an effective date of April 29, 2024, and remains unchanged.

Proven and Probable Mineral Reserves:

287.65 million tonnes at an average grade of 1,149 ppm lithium, containing 1.759 million tonnes LCE

Mineral Reserves are reported at a 900 ppm lithium cut-off grade, which is approximately 4.5 times the calculated break-even cut-off grade, and support a mine life exceeding 60 years, with a 40-year production schedule used in the economic analysis.

Mining Methods and Production Schedule

Mining will be conducted as a conventional open-pit operation using free-digging equipment, including dozers, shovels, and haul trucks. No drilling or blasting is required.

The mine plan reflects a two-phase development strategy:

Phase 1: 7,500 tpd of mill feed

Phase 2: expansion to 15,000 tpd

A previously planned third expansion phase was eliminated. The production schedule prioritizes near-surface, higher-grade mineralization in the early years, reducing waste movement and improving capital efficiency.

Mineral Processing and Metallurgy

The processing flowsheet consists of:

High-pH attrition scrubbing

Hydrochloric acid leaching

Neutralization and pressure filtration with dry-stack tailings

Direct Lithium Extraction

Lithium carbonate precipitation, drying, and packaging

Reagent generation via on-site chlor-alkali plant

Metallurgical assumptions are supported by multi-year pilot plant operations through mid-2025. Leach extraction of approximately 90% was demonstrated, resulting in an overall lithium recovery of approximately 84%. A final lithium carbonate product grading >99.9% purity was consistently achieved.

Angel Island facilities include an integrated chlor-alkali plant producing hydrochloric acid and sodium hydroxide. Surplus sodium hydroxide, as produced in excess in conjunction with the design production of hydrochloric acid, is expected to be sold, contributing substantial additional revenue and thereby reducing effective operating cost.

Capital Costs

A Class 3 capital cost estimate was prepared in accordance with AACE International guidelines. The updated costs were developed using second-quarter 2025 data:

Phase 1 (7,500 tpd) initial capital cost: estimated $997.4 million

Phase 2 (15,000 tpd) expansion capital cost: estimated $660.2 million

Reductions to estimated capital costs relative to the 2024 Study are attributable to the elimination of a third production phase, simplification of installed capacity, processing flowsheet optimization, and updated vendor and construction cost inputs.

The chlor-alkali plant cost is $481.5 million in Phase 1 and $256.8 million in Phase 2, included in Processing Facilities, and is vendor all-in turn-key constructed costs, inclusive of indirect costs, owners’ costs and contingency.

Operating Costs

Average operating cost estimates were updated based on refined mine scheduling, updated reagent consumption, and pilot-validated process parameters.

Average operating cost: approximately $22.45/t of mill feed, or $4,389/t of lithium carbonate.

Sodium hydroxide by-product revenue is equivalent to $5,393/t of lithium carbonate. If credited against operating costs (which was not done in the average operating cost above), base operating costs would be negative.

Economic Analysis

The economic analysis of Angel Island was done using a discounted cash flow (“DCF”) model using only the first 40 years of project life. Cash flows in the model were based on second-quarter 2025 U.S. dollars with no escalation of costs or revenues. The DCF model uses a base-case discount rate of 8%. Financing costs were excluded from the valuation.

The analysis includes generating gross sales from lithium carbonate and sodium hydroxide, before-tax cash flow, which is gross sales minus operating costs, and after-tax cash flow, which is before-tax cash flow minus taxes and capital costs. The NPV and IRR were calculated from the DCF.

The economic analysis uses a base-case lithium carbonate price of $24,000/t and an 8% discount rate.

After-tax NPV: $4.01 billion

After-tax IRR: 27.4%

Profitability Index: 4.0

Sensitivity to Lithium Carbonate Price

Sensitivity analyses demonstrate Angel Island economics are most sensitive to lithium price and remain robust across a wide range of cost and price assumptions.

Environmental, Permitting, and Social Considerations

Baseline environmental studies are complete. Permitting is expected to proceed under the National Environmental Policy Act (“NEPA”) through the US Bureau of Land Management. Angel Island is currently in the permitting stage, with no material changes to the permitting pathway outlined in the 2024 Study.

Interpretation and Conclusions

The 2026 Feasibility Study concludes that the Angel Island project is technically and economically viable, with improved capital efficiency, reduced execution risk, and robust long-term economics. The simplified two-phase development plan, extensive metallurgical validation, and integrated chlor-alkali process support Angel Island’s competitiveness as a domestic US. source of battery-grade lithium carbonate.

In addition, the integrated chlor-alkali process also provides environmental and operational advantages relative to sulfuric acid-based systems, including on-site reagent production.

Recommendations

Work recommended to advance Angel Island and continue project development is as follows:

A Plan of Operations (“PoO”) should be completed and filed with the BLM to initiate the National Environmental Policy Act (“NEPA”) process; and begin the permitting process with the State of Nevada to work concurrently with the federal process.

Additional geotechnical data should be collected to supplement the existing characterization data and further support the tailings storage facility (TSF) design and foundation, foundation infrastructure requirements for the processing plant, and traffic management and load bearing capacity of materials in the pit during mining.

Additional pilot testing should be completed on deeper material from claystone zones 1 and 2 collected previously, to further confirm the metallurgy of these materials.

Infrastructure work should be completed as follows: 1) initiate preliminary engineering studies with NV Energy for the interconnection of the Project to the electrical grid, 2) define a water source for the Project with a drilling program using piezometers and other pumping tests to be developed under the Company’s water rights permit, and 3) locate local sources of barrow material for construction use at the Project.

Detailed engineering should begin when the NEPA process commences and be completed in appropriate phases to develop the Project design to a level sufficient to support procurement, construction planning, and financing.

A supplemental infill drilling program is recommended, though not required, with the following goals: 1) collect additional data for the Project’s Phase 1 economic and mining models, 2) material for additional density test work, and 3) material for geotechnical test work.

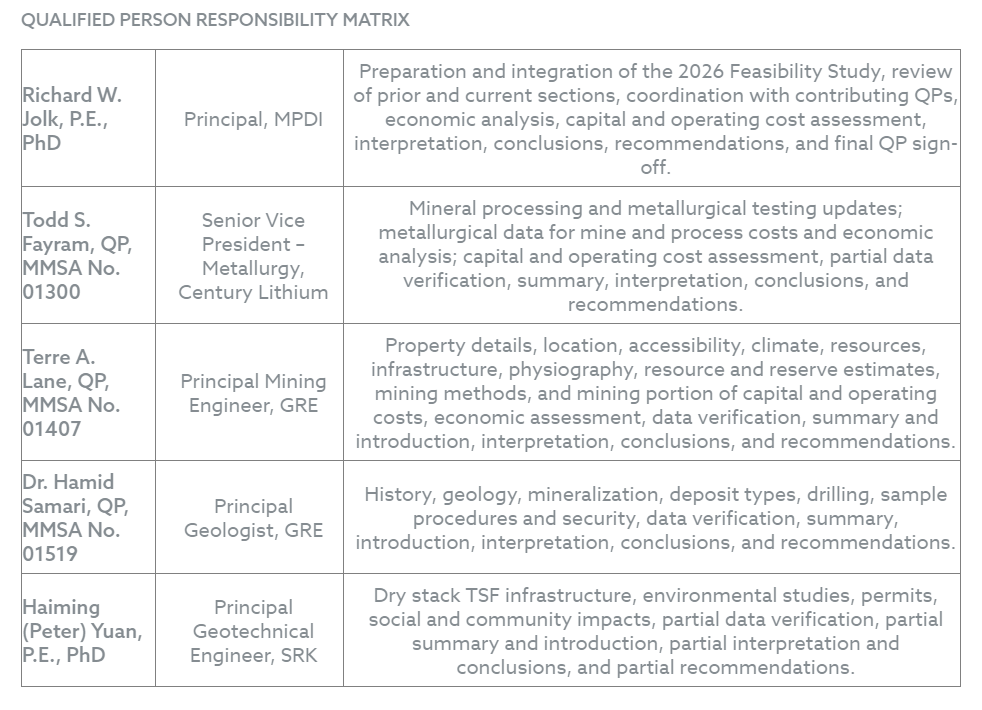

QUALIFIED PERSON

The technical information contained in this news release has been reviewed and approved by Richard W. Jolk, P.E., an independent Qualified Person as defined under National Instrument 43-101.

Further information about Angel Island, including a description of the key assumptions, parameters, description of sampling methods, data verification and quality assurance/quality control programs, methods relating to Mineral Resources and Mineral Reserves and factors that may affect those estimates will be contained in a NI 43-101 Technical Report on the Feasibility Study of the Angel Island Lithium Project. Following Section 3.4 of NI 43-101 the report will be available on SEDAR+ and on the Company’s website within 45 days of the date of this news release.

ABOUT CENTURY LITHIUM CORP.

Century Lithium Corp. is an advanced-stage lithium development company focused on its 100%-owned Angel Island lithium project in Esmeralda County, Nevada. Angel Island hosts one of the largest known sedimentary lithium deposits in the United States and is designed with an integrated, end-to-end process for the on-site production of battery-grade lithium carbonate to support the electric vehicle and battery storage markets.

The Company has developed a patent-pending process that incorporates hydrochloric acid leaching combined with direct lithium extraction to produce battery-grade lithium carbonate. As part of the integrated chlor-alkali process, Angel Island is designed to produce sodium hydroxide as a co-product, with planned surplus sales expected to lower operating costs, reduce reliance on externally sourced reagents, and minimize environmental impacts.

The Angel Island Project is currently advancing through the permitting process.

Century Lithium trades on the TSX Venture Exchange under the symbol “LCE” the OTCQX under the symbol “CYDVF”, and on the Frankfurt Stock Exchange under the symbol “C1Z”.

WILLIAM WILLOUGHBY, PhD., PE President & Chief Executive Officer For further information, please contact: Spiros Cacos | Vice President, Investor Relations Direct: +1 604 764 1851 Toll Free: 1 800 567 8181 [email protected] centurylithium.com

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

This release contains certain forward-looking statements within the meaning of applicable Canadian securities legislation. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” and similar expressions suggesting future outcomes or statements regarding an outlook.

Forward-looking statements relate to any matters that are not historical facts and statements of our beliefs, intentions and expectations about developments, results and events which will or may occur in the future, without limitation, statements with respect to the potential development and value of the Project and benefits associated therewith, statements with respect to the expected project economics for the Project, such as estimates of life of mine, lithium prices, production and recoveries, capital and operating costs, IRR, NPV and cash flows, any projections outlined in the Feasibility Study in respect of the Project, the permitting status of the Project and the Company’s future development plans.These and other forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause their actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein.These risks include those described under the heading “Risk Factors” in the Company’s most recent annual information form and its other public filings, copies of which can be under the Company’s profile at www.sedarplus.com. The Company expressly disclaims any obligation to update-forward-looking information except as required by applicable law. No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place reliance on forward-looking statements or information. Furthermore, Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability