The Federal Reserve held its benchmark interest rate unchanged Wednesday, keeping the federal funds rate in the range of 3.5% to 3.75% as policymakers assess a shifting economic landscape shaped by elevated energy prices, a resilient growth outlook, and ongoing uncertainty tied to the conflict in the Middle East. The decision marks the second consecutive hold this year, with officials maintaining their projection of one rate cut in 2026 — consistent with guidance issued in December.

The vote was split. Fed Governor Stephen Miran dissented in favor of an immediate quarter-point reduction, reflecting the diversity of views inside the central bank as policymakers weigh competing signals from inflation data, labor markets, and geopolitical developments.

For the first time, the Fed formally acknowledged the war in Iran as an economic variable, stating that “the implications of developments in the Middle East for the U.S. economy are uncertain.” The acknowledgment signals that policymakers are actively monitoring the conflict’s impact on energy prices and supply chains as they assess the timing and pace of future policy adjustments.

Inflation forecasts were revised modestly higher as a result. Officials now see headline inflation at 2.7% for 2026, up from a prior estimate of 2.4%, and core inflation — which excludes food and energy — at 2.7% versus the previous 2.5% projection. While inflation remains above the Fed’s 2% target, the central bank’s updated projections also reflect a more optimistic view of overall economic growth, suggesting policymakers see the current environment as manageable rather than alarming.

In a constructive revision, the Fed raised its GDP growth forecast to 2.4% for 2026, up from 2.3% previously, reflecting continued economic momentum. The unemployment rate projection held steady at 4.4% — a level historically consistent with a healthy labor market.

Month-to-month payroll data has been choppy — January posted a gain of 126,000 jobs followed by a decline of 92,000 in February — but the unemployment rate has remained largely stable throughout the swing, which Fed officials noted as a point of continuity. Policymakers are watching incoming data closely before drawing conclusions about the labor market’s direction.

The Fed’s steady-hand approach offers a degree of predictability that markets and businesses can plan around. With one rate cut still projected for 2026, the path toward monetary easing remains intact — even if the timeline is data-dependent. For small and microcap companies, the key takeaway is that the cost of capital environment, while elevated, appears to be stabilizing rather than tightening further.

The breadth of opinion inside the Fed — ranging from no cuts to as many as four this year — reflects genuine debate rather than consensus pessimism, and leaves room for the policy outlook to shift as energy markets and labor data evolve through the year.

Adding another dimension to the Fed’s near-term story: Chair Jerome Powell’s term expires May 15, and his nominated successor Kevin Warsh awaits Senate confirmation. The transition is unfolding against a complex political backdrop, but the Fed’s institutional framework and data-driven decision-making process are expected to remain intact regardless of timing.

The direction of travel on rates is still lower. The question is when.

President Trump issued a 60-day waiver of the Jones Act on Wednesday in a bid to cool surging domestic energy prices as the Iran conflict continues to hammer global oil markets. The move, confirmed by White House press secretary Karoline Leavitt, opens U.S. ports to foreign-flagged vessels for the next two months — covering crude oil, refined products like gasoline and diesel, natural gas, coal, fertilizer, and other energy-derived commodities.

The decision comes as Brent crude crossed $109 per barrel Wednesday morning — up more than 7% on the day — while WTI traded above $97. Gas prices at the pump have climbed to a national average of $3.84 per gallon, up sharply from $2.92 just one month ago, according to AAA data. Diesel has already crossed $5 per gallon nationally. The administration is clearly feeling political pressure to act ahead of the midterm cycle, and the Jones Act waiver is the most tangible move it has made so far.

What the Jones Act Actually Does

The Jones Act — formally the Merchant Marine Act of 1920 — requires that any cargo transported between U.S. ports be carried by vessels that are U.S.-built, U.S.-owned, U.S.-flagged, and U.S.-crewed. The law was designed to protect the domestic shipping industry after World War I, but has long been criticized by economists as an inflationary form of protectionism that raises the cost of moving goods within the country. With fewer than 100 Jones Act-compliant vessels in existence, the waiver immediately opens the door to a much larger pool of international tankers to move fuel between domestic ports.

The Practical Impact — And Its Limits

In theory, the waiver should have its biggest effect on refined product shipments from Gulf Coast refinery complexes to the more isolated East Coast — a corridor that has historically been a bottleneck during supply disruptions. Cheaper, more accessible shipping capacity means fuel can theoretically move faster and at lower cost to the regions that need it most.

But experts are already tempering expectations. The core problem isn’t moving fuel — it’s refining it. Most U.S. refineries are configured to process heavier Middle Eastern crude grades, while domestic shale production yields lighter oil. That structural mismatch means the U.S. still cannot fully self-supply even with more flexible shipping rules. The waiver makes domestic logistics more efficient, but it does not solve the underlying supply equation.

The Broader Policy Picture

The Jones Act move is reportedly just one item on a broader White House menu of potential energy interventions being considered, including possible Treasury-led action in energy futures markets and export bans on crude and refined products. Any of those measures — if enacted — would carry significant market implications across the energy sector.

For small and microcap investors, the read-through is layered. Domestic shippers and Jones Act operators could see near-term pricing pressure as foreign competition enters the market. Refiners with Gulf Coast exposure and East Coast distribution capability may benefit from improved logistics economics. And any company with meaningful fuel cost exposure — from regional truckers to agricultural operators to industrial manufacturers — should be watching this space closely as the administration continues to improvise policy responses to a crisis with no clear end date.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Gyre Receives Priority Review. Hydronidone has been awarded Priority Review Status by the Center for Drug Evaluation (CDE) of China’s National Medical Products Administration (NMPA). This is consistent with our expectations for an accelerated NDA review and late FY2026 approval for Hydronidone.

Meeting With The CMPA Was Positive. In early January, Gyre Pharmaceuticals (China) held a Pre-New Drug Application meeting with the CDE. At that time, the CDE agreed that data from the Hydronidone Phase 3 trial for treating chronic hepatitis B (CHB)-associated liver-fibrosis supported an application for conditional approval. It also met the criteria for Priority Review.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

New Analysis Shows Less Than 1% Recurrance Rate. Greenwich Pharmaceuticals announced a preliminary update from its FLAMINGO-01 trial. The data from the open-label arm of the trial showed a recurrence rate of less than 1% per year compared to a recurrence rate of 4% per year for patients treated with Kadcyla (ado-trastuzumab emtansine or T-DM1, from Genentech) in the Phase 3 KATHERINE Study. This is a 70% to 80% reduction in the historical recurrence rate for these patients.

Background On The Phase 3 FLAMINGO-01 Trial. The trial tests GLSI-100, an immunotherapy to prevent recurrence of HER2-positive breast cancer. Its design has a double-blind portion that enrolls patients with the immune marker HLA-A*02 to receive either GLSI-100 or placebo, and an open-label arm that enrolls patients that have other HLA types (non-HLA-A*02). The new data is from the open-label arm of the trial.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Double E Pipeline growth. Summit recently signed two new long-term take-or-pay agreements totaling 540 MMcf/d of incremental firm capacity on the Double E Pipeline, an 11-year, 210 MMcf/d contract with a large investment-grade shipper and an 11-year, 230 MMcf/d agreement with an undisclosed shipper, alongside the previously announced 100 MMcf/d Producers Midstream II commitment, which received an affirmative FID during the quarter. These contracts are expected to grow the Permian Segment Adj. EBITDA from ~$34 million in 2025 to ~$60 million by 2029.

2026 guidance. Summit expects full-year 2026 Adj. EBITDA of $225 million to $265 million, with total capital expenditures of $85 million to $105 million, including approximately $35 million attributable to Double E. The outlook assumes WTI at approximately $64 per barrel and Henry Hub at approximately $3.40 per MMBtu, both materially below current strip prices, suggesting meaningful upside if the commodity environment is sustained. The company expects 116 to 126 well connections supported by seven active rigs and approximately 90 DUCs.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strategic updates ahead of Q4 Earnings Call. At the Game Developers Conference (GDC) in San Francisco last week, the company provided updates across its game portfolio, outlining a steady pipeline of ARK franchise releases, expansions for existing titles, and new indie projects. The announcements were delivered ahead of the company’s Q4 and full-year 2025 earnings call scheduled for March 19, 2026, at 4:30 p.m. ET, providing a preview of its strategic product developments.

Strong Early Access sales. Notably, Bellwright has surpassed 1 million units sold on Steam during Early Access, demonstrating strong player engagement ahead of its 1.0 launch and planned expansion to Xbox and PlayStation. As a reminder, development is now fully in-house following the acquisition and integration of Donkey Crew, the Poland-based studio behind Bellwright, strengthening the franchise’s long-term potential.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Updated feasibility study. Century recently filed its updated 2026 NI 43-101 feasibility study for its 100%-owned Angel Island Lithium Project in Nevada. The updated study reflects engineering optimization and improvements that materially strengthen the project’s economic profile and highlight Angel Island as one of the most significant and economically robust sedimentary lithium developments in the United States.

Lower initial capital expenditures. Phase I initial capital expenditures are estimated to be $997 million, a significant reduction from the $1.5 billion outlined in the 2024 Study. The updated study streamlines development into a two-phase approach. Phase I contemplates 7,500 tonnes per day (tpd) of mill feed, expanding to 15,000 tpd in Phase II beginning in Year 5. Phase II expansion capital is estimated at $660 million. A previously planned third expansion phase was eliminated, lowering overall capital requirements. The economic analysis is based on a 40-year production schedule, with planned life-of-mine average production of 26,500 tonnes per annum of battery-grade lithium carbonate.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Jensen Huang doesn’t do small numbers. But the figure he dropped this week at Nvidia’s annual GTC conference in San Jose may be the most consequential projection in the history of the semiconductor industry — and the ripple effects extend well beyond one company’s balance sheet.

On Monday, Huang forecast that Nvidia’s flagship AI processors would generate $1 trillion in sales through 2027, citing computing demand that has increased “by 1 million times in the last two years.” Then on Tuesday he raised the stakes further, clarifying that the $1 trillion figure doesn’t even capture Nvidia’s full product portfolio. The company has “strong confidence of $1 trillion-plus,” Huang told an audience of analysts and investors, adding that Nvidia expects to close, book and ship more than $1 trillion in total business.

For context, Nvidia had previously forecast $500 billion in data center sales through the end of 2026. The new projection doubles that cumulative figure and extends the window another year — a signal that Huang sees no near-term ceiling on AI infrastructure demand.

Wall Street’s immediate reaction was measured. Nvidia shares jumped as much as 4.8% on Monday before leveling off, trading virtually unchanged by Tuesday afternoon. Some analysts flagged that extending the timeline to 2027 to reach $1 trillion doesn’t necessarily signal accelerating growth — it could simply mean a longer runway to the same destination.

But the more interesting story for small and microcap investors isn’t what happens to Nvidia’s stock. It’s what a $1 trillion AI buildout means for the hundreds of smaller companies that sit inside that ecosystem.

Huang used the conference to announce a significant expansion of Nvidia’s addressable market. The company is pushing deeper into central processing units — territory long dominated by Intel — and introduced semiconductors incorporating technology acquired from chip startup Groq. Nvidia also revealed it is developing chips designed specifically for data centers in outer space, opening an entirely new frontier for AI compute infrastructure.

Each of these moves creates downstream opportunities. CPU expansion pressures Intel and AMD but simultaneously creates openings for smaller, specialized chip designers and manufacturers. The Groq acquisition signals that Nvidia is willing to buy rather than build when speed to market demands it — a dynamic that historically elevates valuations across the small cap semiconductor and AI hardware landscape as larger players scout for targets.

On the capital allocation front, Nvidia’s CFO Colette Kress announced the company plans to direct approximately 50% of free cash flow toward buybacks and dividends in the second half of 2026, once current investment commitments are fulfilled. That shift from aggressive reinvestment toward shareholder returns is a maturity signal — one that typically pushes institutional capital to look further down the market cap spectrum for the growth rates that Nvidia itself once offered.

The AI infrastructure buildout is still in its early innings. A $1 trillion demand signal from the dominant player in the space is not just a headline — it is a directional marker for where capital, talent and M&A activity will flow for the next several years. Small cap investors who understand the supply chain beneath Nvidia stand to benefit most.

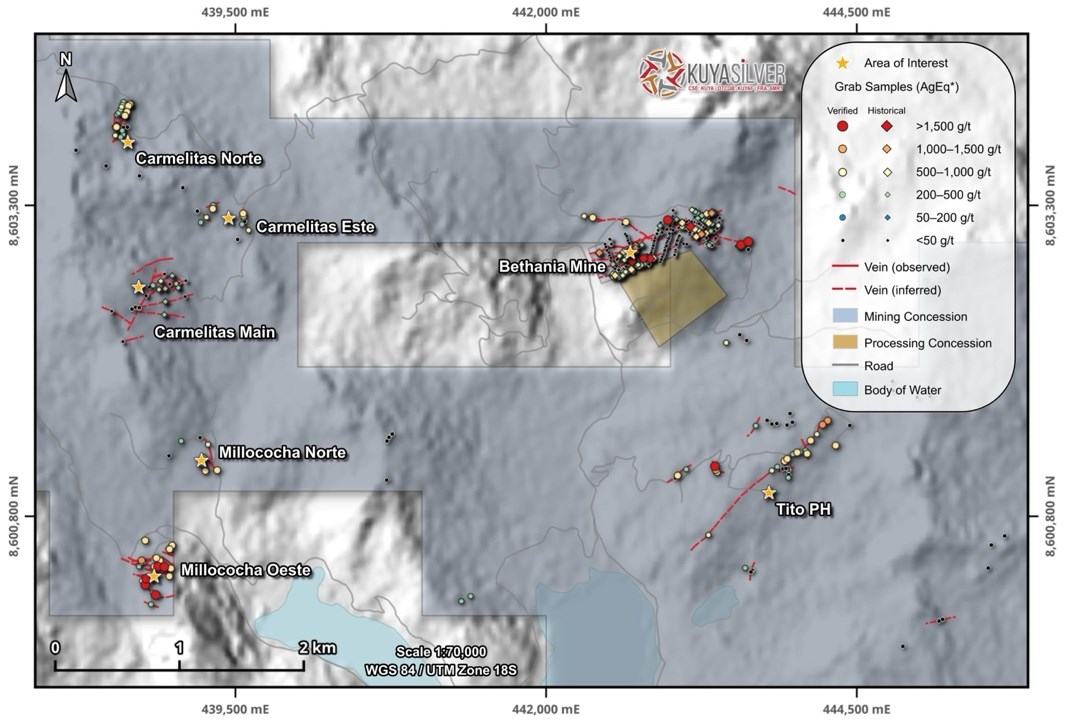

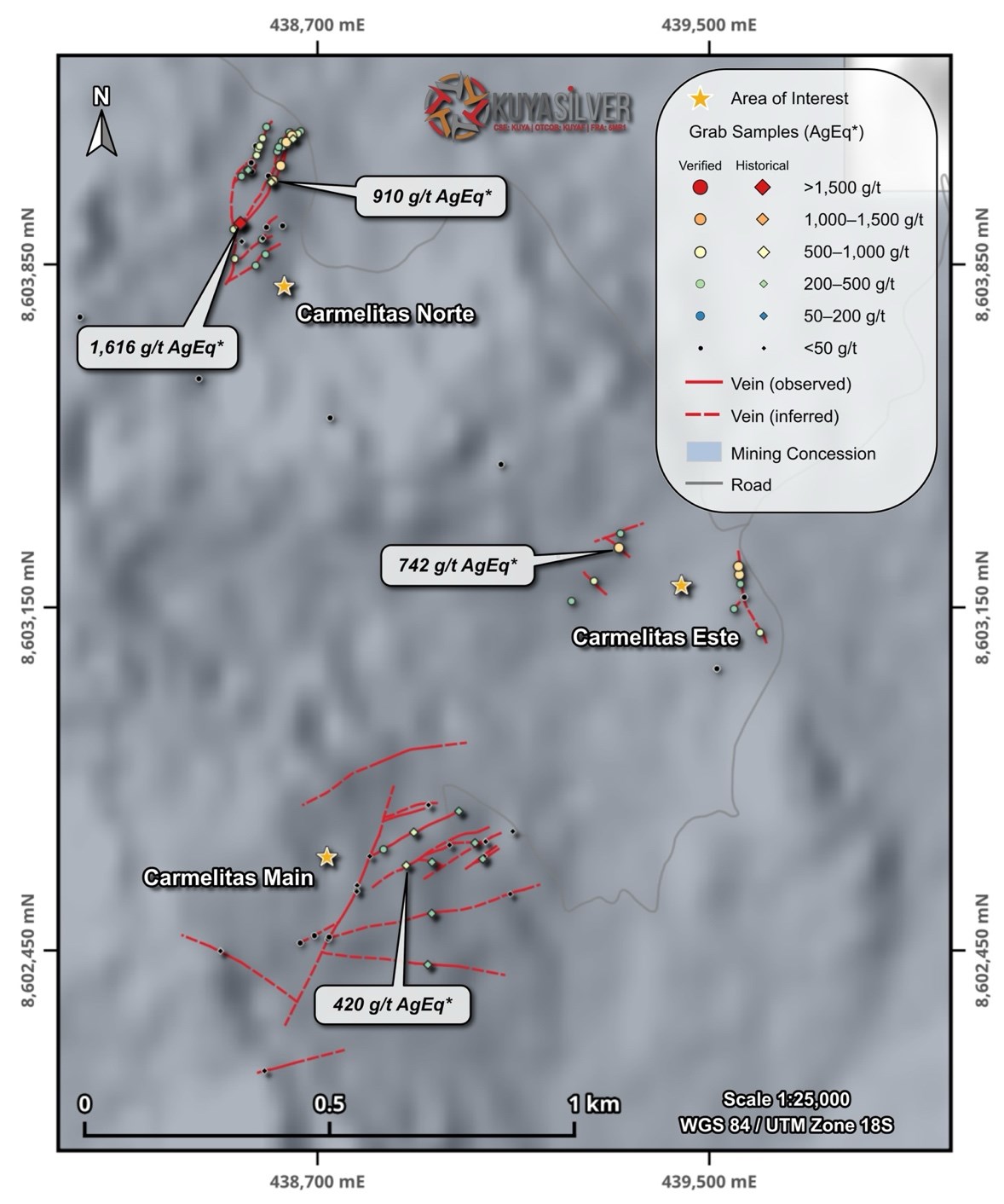

Toronto, Ontario–(Newsfile Corp. – March 17, 2026) – Kuya Silver Corporation (CSE: KUYA) (OTCQB: KUYAF) (FSE: 6MR1) (the “Company” or “KuyaSilver“) is pleased to announce an expansion of its fully-funded 2026 drill program at the Bethania Silver Project in central Peru designed to unlock value by focusing on delineating mineralized silver vein systems which have been historically underexplored. The program, expected to total approximately 20,000 metres combined underground and surface diamond drilling, would represent the largest drill program ever at the Bethania project.

The surface drill program is planned for approximately 10,000 metres and will focus on priority targets associated with historical artisanal mining areas identified during the Company’s recent regional exploration work, located outside the immediate Bethania mine area (Figure 1 below). These targets represent potential additions to the district-scale mineralized system and may also have potential for future production. Over the coming months Kuya Silver plans to conduct additional work to prioritize targets for the 2026 drill program which may include any of the six previously identified regional silver vein systems (e.g. Carmelitas, Tito PH, Millococha)

The Company also plans to expand on its previously announced underground drilling program to approximately 10,000 metres in 2026 (from 5,000 metres announced previously). Drilling will be conducted from established mine levels and is designed to test extensions of known mineralized structures that remain open along strike and at depth. This approach allows the Company to expand resources adjacent to current mine infrastructure while testing high-priority targets at relatively low cost and improving the geological continuity of the known vein system.

The combined surface and underground programs are expected to improve the geological understanding of the mineralized systems and support the Company’s ongoing efforts to grow resources within the broader Bethania district. Initial results from the underground drilling campaign are expected in Q2 2026 and additional drill results from underground and initial surface drilling results are expected over the second half of 2026.

“Following encouraging surface exploration results across the Bethania property, we are excited to begin the next phase of drilling,” stated Osbaldo Zamora, VP Exploration of Kuya Silver. “By combining surface drilling with underground drilling from existing workings, we are able to efficiently test both district-scale targets and near-mine extensions that could meaningfully expand the project’s resource base.”

David Stein, Kuya Silver’s President and CEO also remarked, “The Company is excited to embark on a much larger drill campaign covering multiple targets across the Bethania district. Given our significant cash position in excess of USD $25 million and expected cash flow from the Bethania mine, this more aggressive exploration strategy should be fully funded from internal sources and can be maintained and expanded over the coming years as we grow our silver mining operations.”

Figure 1: Bethania historical surface exploration results up to February 2026 showing all sample locations.

Surface drilling is expected to commence in the coming months following final permitting and logistical preparations. Over the past five plus years, Kuya Silver has consolidated in excess of 4,500 ha surrounding the Bethania mine. Various surface prospecting campaigns over the past several years has identified six different silver vein systems characterized by historical evidence of artisanal mining and outcropping veins with silver-polymetallic mineralization which have been mapped and sampled by Kuya Silver’s geologists. These additional vein systems can be subdivided into three areas located south (Tito PH), west (Carmelitas) and southwest (Millococha) of the Bethania silver mine.

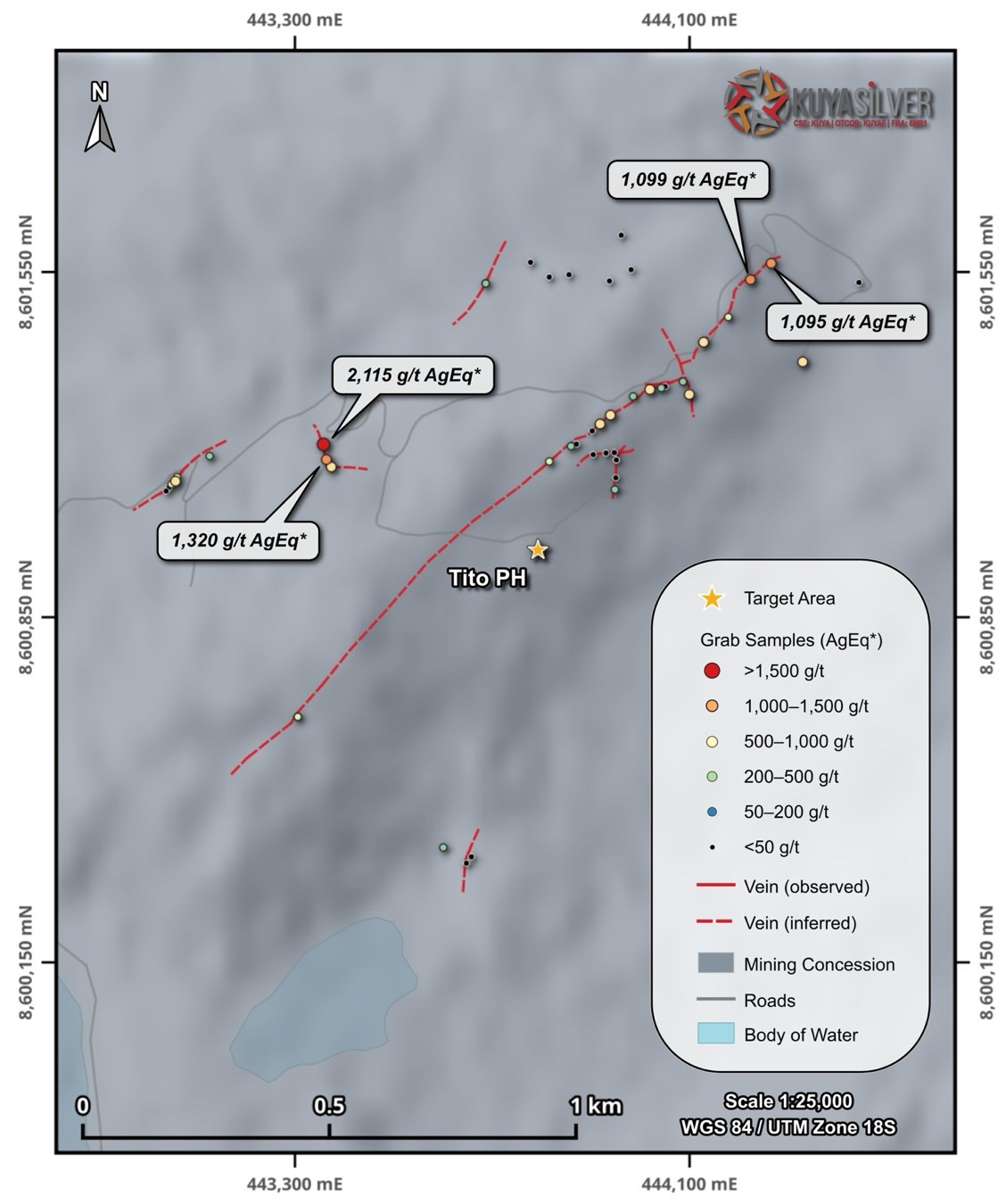

Tito PH

Tito PH is a priority exploration target consisting of one main vein and at least seven additional subparallel veins (Figure 2 below). The main vein has been mapped over approximately 600 metresof strike and may extend up to 1,500 metres, although a 700 metres gap in surface exposure remains to be tested by drilling.

Minor artisanal workings, including two shallow adits and an open stope, occur along the vein cluster. A total of 55grab samples collected by Kuya Silver geologists returned an arithmetic average grade of 285.7 g/t AgEq* and a maximum value of 2,114.7 g/t AgEq*. The interpreted strike length and high-grade surface samples suggest the system could be comparable in scale to the veins currently mined at Bethania.

Figure 2. Detailed map showing interpreted veins, grab sample locations, and assays at the Tito PH prospect.

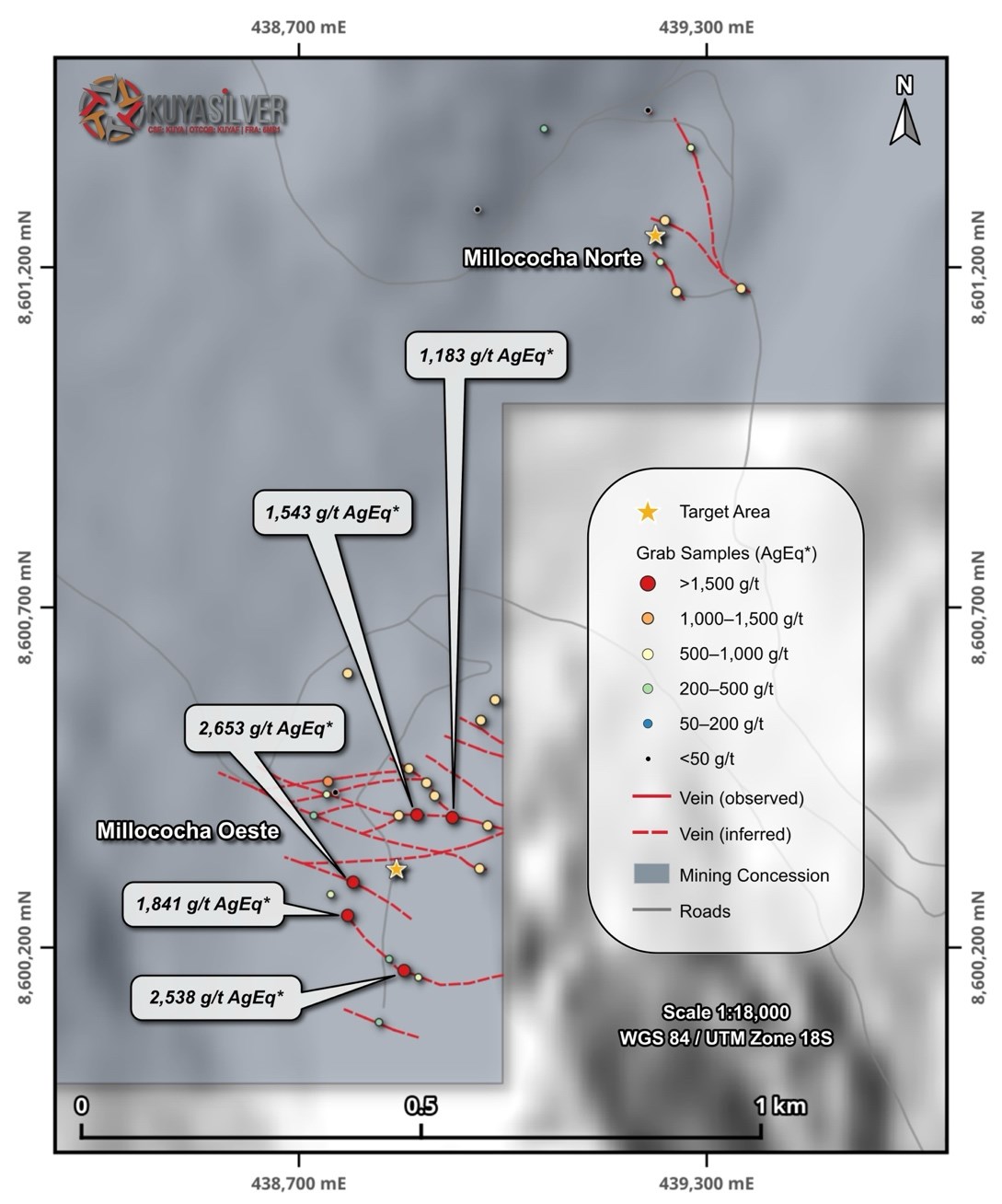

Millococha Oeste is one of the most prospective targets identified within the Bethania land package due to the presence of more than 10 mapped veins with consistently high grades. A total of 40 grab samples collected by Kuya Silver geologists returned an arithmetic average grade of 690.4 g/t AgEq* and a maximum value of 2,652.7 g/t AgEq* (Figure 3 below).

Artisanal workings on Kuya Silver’s claims represent the most significant historic activity outside the Santa Elena concession, but remain relatively shallow and poorly explored, highlighting the potential for additional mineralization at depth.

Figure 3. Detailed map showing interpreted veins, grab sample locations, and assays at the Millococha prospect.

The Carmelitas prospect includes three vein clusters within an area of approximately 800 metres, comprising the main Carmelitas artisanal mine as well as the Carmelitas Norte and Carmelitas Este showings (Figure 4 below). A total of 125 grab samples collected by Kuya Silver returned grades up to 1,771.5 g/t Ag and an arithmetic average of 145.2g/t AgEq*.

Although vein density is lower than at other targets, the prospect remains attractive due to the presence of high-grade mineralization and potential structural connections between the three vein clusters.

*Silver Equivalency (AgEq) was calculated using silver ($85.74 USD/troy oz), gold ($5,177.70 USD/troy oz), copper ($12,815.48 USD/tonne), lead ($1,892.0 USD/tonne) and zinc ($3,286.76 USD/tonne) values, obtained on March 3, 2026 from Kitco, and do not consider metal recovery.

Figure 4. Detailed map showing interpreted veins, grab sample locations, and assays at the Carmelitas prospect.

A total of 940 grab samples (plus QA/QC) were collected in different exploration campaigns from 2021 to 2026. Only 192 samples collected from 2024 to 2026 count with proper QA/QC assessment. The coordinates of the locations of each sample were measured by handheld GPS and the samples dispatched to the ALS Peru S.A. laboratory in Lima for geochemical analysis. The analyses were carried out using the following methods:

ME-OG61a – Multi-acid digestion with ICP-AES detection for 33 elements

Au-AA23 – Fire assay for gold

Ag-OG62 – Four-acid digestion with ICP-AES detection for overlimit silver

All QA/QC standards were acceptable and within two standard deviations of certified values.

As these samples include a mix of early-stage grab, chip, and channel samples and do not include details on vein width, they are not fully representative of total vein mineralization.

National Instrument 43-101 Disclosure

The technical content of this news release has been reviewed and approved by Osbaldo Zamora, PhD., P.Geo., Vice President Exploration with Kuya Silver Corp. and a Qualified Person as defined by National Instrument 43-101.

About Kuya Silver Corporation

Kuya Silver is a Canadian‐based, growth-oriented mining company with a focus on silver. Kuya Silver operates the Bethania silver mine in Peru, while developing district-scale silver projects in mining-friendly jurisdictions including Peru and Canada.

This news release contains statements that constitute “forward-looking information,” including statements regarding the plans, intentions, beliefs, and current expectations of the Company, its directors, or its officers with respect to the future business activities of the Company. The words “may,” “would,” “could,” “will,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “expect,” “must,” “next,” “propose,” “new,” “potential,” “prospective,” “target,” “future,” “verge,” “favorable,” “implications,” and “ongoing,” and similar expressions, as they relate to the Company or its management, are intended to identify such forward-looking information. Investors are cautioned that statements including forward-looking information are not guarantees of future business activities and involve risks and uncertainties, and that the Company’s future business activities may differ materially from those described in the forward-looking information as a result of various factors, including but not limited to fluctuations in market prices, successes of the operations of the Company, continued availability of capital and financing, and general economic, market, and business conditions. There can be no assurances that such forward-looking information will prove accurate, and therefore, readers are advised to rely on their own evaluation of the risks and uncertainties. The Company does not assume any obligation to update any forward-looking information except as required under the applicable securities laws.

Neither the Canadian Securities Exchange nor the Investment Industry Regulatory Organization of Canada accepts responsibility for the adequacy or accuracy of this release.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Presigious Journal Publishes The Phase 2b PARDIGM Study. JAMA Neurology has published an article dissussing the Phase 2b PARDIGM clinical trial. This peer-reviewed journal is published by the American Medical Association and regarded as one of the most prestigious journals in the field of neurology. We see this as a validation the clinical results and an acknowledgement of the impact PrimeC had on the amyotrophic lateral sclerosis (ALS) patients in the study.

PrimeC Addresses Important Mechanisms Of Neuron Degeneration. PrimeC is a proprietary fixed-dose oral combination of celecoxib and ciprofloxacin. These drugs target pathways of neuronal cell death, including regulation of microRNA synthesis, reduction in neuroinflammation, and modulation of iron accumulation. Additional testing by NeuroSense determined the optimal dosage combination of the two drugs for human studies and the extended releaase formulaton.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 results. Bitcoin Depot reported Q4 revenue of $116.0 million, above our estimate of $112.0 million, reflecting somewhat stronger transaction activity than anticipated despite emerging regulatory headwinds. Adj. EBITDA of $1.6 million was below our forecast of $2.5 million due to higher operating expenses during the quarter.

Initial steps toward revenue diversification. The company is beginning to expand beyond the core Bitcoin ATM network through new fintech initiatives. It recently acquired Kutt, a peer-to-peer social betting platform, and launched ReadyBucks, a merchant cash advance platform targeting small businesses and gig workers. Management indicated that both initiative are starting small and not expected to materially impact near-term revenue.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Townsquare is a community-focused digital media and digital marketing solutions company with market leading local radio stations, principally focused outside the top 50 markets in the U.S. Our assets include a subscription digital marketing services business, Townsquare Interactive, providing website design, creation and hosting, search engine optimization, social media and online reputation management as well as other digital monthly services for approximately 26,800 SMBs; a robust digital advertising division, Townsquare IGNITE, a powerful combination of a) an owned and operated portfolio of more than 330 local news and entertainment websites and mobile apps along with a network of leading national music and entertainment brands, collecting valuable first party data, and b) a proprietary digital programmatic advertising technology stack with an in-house demand and data management platform; and a portfolio of 321 local terrestrial radio stations in 67 U.S. markets strategically situated outside the Top 50 markets in the United States. Our portfolio includes local media brands such as WYRK.com, WJON.com, and NJ101.5.com and premier national music brands such as XXLmag.com, TasteofCountry.com, UltimateClassicRock.com and Loudwire.com.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

In-line Q4 results. The company reported Q4 revenue and adj. EBITDA of $106.5 million and $21.5 million, both of which were in line with our estimates of $106.1 million and $22.0 million, respectively. Notably, the company continued to face headwinds in its digital businesses, which have been its primary growth engine.

Advertising trends appear to be improving. Digital revenues remained the company’s largest contributor and primary growth engine, representing approximately 55% of total revenue in 2025, up from 52% in 2024, and generated 56% of segment profit, compared with 50% a year earlier. Despite the stronger mix, fourth quarter Digital Advertising revenue declined 1%, as weakness in remnant advertising offset growth in direct-sold and programmatic digital advertising.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The pharmaceutical industry is facing a revenue crisis of its own making, and the fallout is quietly creating one of the most compelling acquisition environments for small-cap biotech investors in recent memory. The catalyst is straightforward: patent expirations on some of the world’s best-selling drugs are set to eliminate hundreds of billions in annual revenue from major drugmakers’ balance sheets, and the only viable path to replacing that income runs directly through the small-cap biotech sector.

An estimated $236 billion in annual Big Pharma revenue is at risk as blockbuster drugs lose exclusivity in the 2026–2030 window. Flagship products from AbbVie, Merck, Bristol Myers Squibb, and Pfizer are all exposed. Pfizer alone faces a revenue shortfall that analysts project could reach $17–18 billion by 2030 as key drugs lose patent protection. These are not minor headwinds — they represent structural holes in revenue models that took decades to build.

Acquisition Is the Only Realistic Fix

Internal R&D pipelines, no matter how well-funded, cannot reliably produce late-stage, de-risked assets fast enough to offset losses of this scale. That reality is driving an acceleration of M&A activity at a pace not seen in years. Biopharma dealmaking surged to $43.2 billion in value in Q3 2025 alone — a 36.7% jump quarter-over-quarter — and analysts broadly expect 2026 and 2027 to see even more aggressive activity as patent deadlines loom closer.

The targets of choice are small-cap biotechs with proven or near-proven assets, particularly those with late-stage clinical data in high-value therapeutic areas like oncology, rare disease, and immunology. These companies represent an increasingly attractive proposition: they carry significantly lower valuation multiples than large-cap pharma — many trading around 6x revenue — while offering precisely the pipeline depth that major acquirers need most.

What This Means for Small-Cap Investors

For investors paying attention to the small and microcap biotech space, this dynamic creates a clear opportunity structure. Companies advancing late-stage assets in therapeutic categories where major drug patents are expiring are sitting at the intersection of scientific value and urgent corporate need. That combination has historically produced acquisition premiums that significantly reward early investors.

Novartis’s $12 billion acquisition of Avidity Biosciences stands as one of the most cited recent examples — a deal that illustrated how quickly a credible pipeline can attract top-tier buyers willing to pay a substantial premium. It will not be the last. With private equity also sitting on an estimated $440 billion in dry powder earmarked for smaller enterprises, competition for the highest-quality small-cap biotech targets is intensifying from both strategic and financial buyers simultaneously.

The Floor Has Shifted

What makes this M&A wave structurally different from prior cycles is the urgency driving it. This is not opportunistic dealmaking — it is defensive necessity for some of the most capitalized companies in the world. That urgency creates a pricing floor for quality small-cap biotech assets that did not exist five years ago.

For investors willing to do the fundamental work of identifying companies with credible late-stage pipelines, strong IP positions, and exposure to the therapeutic categories where patent cliffs are most acute, the current environment may represent one of the better entry windows of the decade. The deals are coming. The question is whether investors are positioned ahead of them.