Jerome Powell’s tenure as Federal Reserve Chair officially ended Friday after more than seven years leading the central bank through a pandemic, the steepest rate hiking cycle in four decades, and a prolonged battle with post-pandemic inflation. His successor, Kevin Warsh, stepped into the role this week inheriting what may be the most complicated monetary policy environment since Paul Volcker confronted double-digit inflation in the early 1980s.

For small and microcap investors, the transition is not a ceremonial changing of the guard. It is a material shift in the direction of monetary policy at precisely the moment when the cost of capital is becoming the defining variable for smaller company valuations and earnings growth.

Who Warsh Is and Why It Matters

Kevin Warsh previously served as a Federal Reserve Governor from 2006 to 2011, a tenure that included navigating the 2008 financial crisis. He is widely characterized as a hawk — a policymaker with a structural preference for price stability over growth accommodation and a historically low tolerance for above-target inflation. His academic and professional profile suggests he is less likely than Powell to hold rates steady while inflation remains elevated and more willing to tighten further if price pressures persist.

He is stepping in at a moment when that disposition will be tested immediately.

The Macro Backdrop Warsh Inherits

The numbers Warsh walks into are unambiguous. The 30-year Treasury yield closed last week at 5.12% — its highest level since June 2007. The 10-year benchmark yield has breached 4.57%. The Consumer Price Index showed consumer inflation running at 3.8% year over year in April, driven heavily by energy costs tied to the ongoing US-Iran conflict. The Producer Price Index came in at 6% annually — a number that signals upstream cost pressures have not peaked. CME’s FedWatch tool currently prices in a near-certainty of a rate hold at June’s meeting, with traders assigning close to a 50% probability of at least one rate hike before year end.

That is the environment Warsh now owns. Federal Reserve Governor Stephen Miran submitted his resignation last week, effective upon Warsh’s swearing in, creating additional uncertainty around the composition and internal dynamics of the board at a critical juncture.

The Direct Small Cap Implication

The cost of capital story is where this transition becomes acutely relevant for investors in the sub-$2 billion market cap space. Small and microcap companies carry disproportionately more variable-rate debt relative to their large cap counterparts. When benchmark rates rise — or even when the probability of rate hikes increases — the interest expense on that debt rises in real time, compressing earnings directly and immediately.

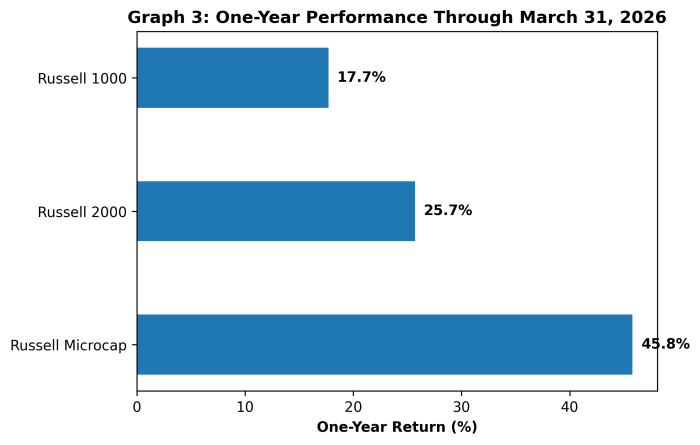

Beyond debt service costs, a hawkish Fed posture extends the timeline for rate relief that many smaller companies had been counting on to refinance obligations at more favorable terms. The Russell 2000 has already declined more than 1% today while the S&P 500 trades modestly higher — a divergence that reflects exactly this dynamic playing out in real time.

A Warsh-led Fed that prioritizes inflation control over growth accommodation will likely sustain higher rates longer than markets had previously anticipated. For companies with strong balance sheets and pricing power, that is manageable. For smaller companies operating on thin margins with floating rate exposure, it is a structural headwind that belongs in every portfolio risk assessment right now.

The Powell era is over. The Warsh era begins with inflation still elevated, yields near 20-year highs, and the smallest companies in the market most exposed to whatever comes next.