FORT WORTH, Texas, March 31, 2026 /PRNewswire/ — AZZ Inc. (NYSE: AZZ), the leading independent provider of hot-dip galvanizing and coil coating solutions, today announced it will conduct a conference call to review the Company’s financial results for the fourth quarter and fiscal year 2026 at 11:00 a.m. ET on Thursday, April 23, 2026. The Company will issue a press release reporting fourth quarter and full fiscal year financial results after the market closes on Wednesday, April 22, 2026.

Conference Call Details Interested parties can access the conference call by dialing (844) 855-9499 or (412) 317-5497 (international). A webcast of the call will be available on the Company’s Investor Relations page at https://investor.azz.com/

A replay of the call will be available at (855) 669-9658 or (412) 317-0088 (international), replay access code: 5871094 through April 30, 2026, or by visiting https://investor.azz.com/ for the next 12 months.

About AZZ Inc.

AZZ Inc. is the leading independent provider of hot-dip galvanizing and coil coating solutions to a broad range of end-markets. Collectively, our business segments provide sustainable, unmatched metal coating solutions that enhance the longevity and appearance of buildings, products and infrastructure that are essential to everyday life. For more information, please refer to www.azz.com.

Safe Harbor Statement

Certain statementsherein about our expectations of future events or results constitute forward-looking statements for purposes of the safe harbor provisions of The Private Securities Litigation Reform Act of 1995. You can identify forward-looking statements by terminology such as “may,” “could,” “should,” “expects,” “plans,” “will,” “might,” “would,” “projects,” “currently,” “intends,” “outlook,” “forecasts,” “targets,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue,” or the negative of these terms or other comparable terminology. Such forward-looking statements are based on currently available competitive, financial, and economic data and management’s views and assumptions regarding future events. Such forward-looking statements are inherently uncertain, and investors must recognize that actual results may differ from those expressed or implied in the forward-looking statements. Forward-looking statements speak only as of the date they are made and are subject to risks that could cause them to differ materially from actual results. Certain factors could affect the outcome of the matters describedherein. This press release may contain forward-looking statements that involve risks and uncertainties including, but not limited to, changes in customer demand for our manufactured solutions, including demand by the construction markets, the industrial markets, and the metal coatings markets. We could also experience additional increases in labor costs, components and raw materials including zinc and natural gas, which are used in our hot-dip galvanizing process, paint used in our coil coating process; supply-chain vendor delays; customer requested delays of our manufactured solutions; delays in additional acquisition opportunities; an increase in our debt leverage and/or interest rates on our debt, of which a significant portion is tied to variable interest rates; availability of experienced management and employees to implement AZZ’s growth strategy; a downturn in market conditions in any industry relating to the manufactured solutions that we provide; economic volatility, including a prolonged economic downturn or macroeconomic conditions such as inflation or changes in the political stability in the United States and other foreign markets in which we operate; tariffs; acts of war or terrorism inside the United States or abroad; and other changes in economic and financial conditions. AZZ has provided additional information regarding risks associated with the business, including in Part I, Item 1A. Risk Factors, in AZZ’s Annual Report on Form 10-K for the fiscal year ended February28, 2026, and other filings with the SEC, available for viewing on AZZ’s website at www.azz.com and on the SEC’s website at www.sec.gov. You are urged to consider these factors carefully when evaluating the forward-looking statements herein and are cautioned not to place undue reliance on such forward-looking statements, which are qualified in their entirety by this cautionary statement. These statements are based on information as of the datehereof and AZZ assumes no obligation to update any forward-looking statements, whether as a result of new information, future events, or otherwise.

Company Contact: David Nark, Chief Marketing, Communications, and Investor Relations Officer AZZ Inc. (817) 810-0095 www.azz.com

Investor Contact: Sandy Martin or Phillip Kupper Three Part Advisors (214) 616-2207 or (817) 368-2556 www.threepa.com

ATLANTA, GA – March 31, 2026 (NEWMEDIAWIRE) – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing vaccines and immunotherapies against infectious diseases and cancer, today announced its entry into a warrant inducement agreement with existing healthcare-focused institutional investors of the Company for the immediate exercise of existing warrants (the “Existing Warrants”) to purchase up to 634,658 shares of the Company’s common stock, par value $0.001 per share (the “Common Stock”) at a reduced exercise price of $1.36 for gross cash proceeds of approximately $863,000, before deducting financial advisor fees and other transaction expenses. The Company intends to use the net proceeds from the offering for working capital and other general corporate purposes.

In consideration for the immediate exercise in full of the Existing Warrants, the investor will receive, in a private placement, new unregistered warrants to purchase up to 1,269,316 shares of Common Stock (the “New Warrants”). The New Warrants will have an exercise price of $1.36, will be initially exercisable on the date that shareholder approval of the issuance of the New Warrants is obtained (the “Approval Date”), and will expire five (5) years following the Approval Date. The closing of the warrant inducement transaction is expected to occur on or about April 1, 2026, subject to satisfaction of customary closing conditions.

The private placement of the New Warrants and the shares of Common Stock underlying the New Warrants offered to the institutional investor will be made in reliance on an exemption from registration under Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”) and Regulation D promulgated thereunder. Accordingly, the securities issued in the Concurrent Private Placement may not be offered or sold in the United States except pursuant to an effective registration statement or an applicable exemption from the registration requirements of the Securities Act and such applicable state securities laws.

This press release does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in this Offering, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company focused on the development of vaccines and immunotherapies addressing high-consequence infectious diseases and solid tumor cancers. GeoVax’s priority program is GEO-MVA, a Modified Vaccinia Ankara (MVA)–based vaccine targeting mpox and smallpox. The program is advancing under an expedited regulatory pathway, with plans to initiate a pivotal Phase 3 clinical trial in the second half of 2026, to address critical global needs for expanded orthopoxvirus vaccine supply and biodefense preparedness. In oncology, GeoVax is developing Gedeptin(R), a gene-directed enzyme prodrug therapy (GDEPT) designed to enhance immune checkpoint inhibitor activity. Gedeptin has completed a multicenter Phase 1/2 clinical trial in advanced head and neck cancer and is being advanced into combination strategies, including planned neoadjuvant and first-line settings. GeoVax’s broader pipeline includes the development of GEO-CM04S1, a next-generation COVID-19 vaccine candidate being evaluated in immunocompromised and other patient populations. GeoVax maintains a global intellectual property portfolio supporting its infectious disease and oncology programs and continues to evaluate strategic partnerships and funding opportunities aligned with its development priorities. For more information, visit www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Phase 1b norovirus challenge study is underway at Emory University School of Medicine

CDI-988 is the first oral antiviral candidate being developed for norovirus treatment and prevention

No approved treatments or vaccines are available for norovirus infection, posing a significant unmet need and contributing to a global economic burden of $60 billion annually

BOTHELL, Wash., March 31, 2026 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (“Cocrystal” or the “Company”) reports financial results for the year ended December 31, 2025, and provides updates on its antiviral product pipeline, upcoming milestones and business activities.

“We are delighted to report that our norovirus human challenge study evaluating efficacy and safety of CDI‑988 is underway at Emory University School of Medicine. In our first cohort, healthy subjects are being inoculated with the GII.2 (Snow Mountain Virus) strain under highly controlled conditions,” said Sam Lee, Ph.D., President and co‑CEO of Cocrystal.

“Norovirus remains a significant and underserved market. Developing an effective norovirus antiviral or vaccine has been challenging due to the high genetic and antigenic diversity of norovirus and lack of simple in vitro cell-based assays and animal model system,” Dr. Lee continued. “Using our proprietary structure‑based drug discovery platform technology, we developed CDI‑988 as a direct‑acting, oral antiviral that targets a highly conserved region of the viral 3CL protease found in all known norovirus strains. As a pan-viral 3CL protease inhibitor, CDI‑988 also holds potential as a broad‑spectrum antiviral effective against coronaviruses.”

“Norovirus outbreaks can strike at any time of year in semi-closed environments such as cruise ships, military settings, and healthcare and assisted-living facilities,” said James Martin, Cocrystal’s CFO and co-CEO. “This constant threat underscores the need for an effective oral treatment and preventive that can be deployed whenever and wherever norovirus infections emerge. With CDI-988, our goal is to provide an easy-to-administer, safe and effective drug to combat these unpredictable outbreaks. We believe CDI‑988 represents a key value-creating opportunity for our Company and our investors.”

The Phase 1b randomized, double-blind, placebo-controlled study will enroll up to 40 subjects. The study’s primary endpoint is efficacy in reducing the incidence of clinical symptoms; secondary endpoints include reduction of viral shedding and disease severity, and safety and pharmacokinetic profiles.

Antiviral Product Pipeline Overview

We leverage our innovative structure-based drug discovery platform technology to develop next-generation, broad-spectrum antivirals that effectively block viral replication. Unlike other drug discovery approaches, our technology identifies compounds that bind to highly conserved regions of viral drug targets, including proteases and replication enzymes. By specifically targeting these essential viral functions, our drug candidates maintain efficacy even as viruses mutate, while simultaneously minimizing off-target interactions that typically lead to adverse side effects. This dual advantage represents a significant breakthrough in antiviral drug development. In addition, our innovative methodology fundamentally transforms the conventional drug discovery paradigm by eliminating the inefficient, resource-intensive cycles of high-throughput compound screening and prolonged hit-to-lead optimization. The result is faster identification of promising candidates with superior resistance profiles and safety characteristics.

Norovirus Program Norovirus is a common, highly contagious virus that afflicts people of all ages and causes symptoms of acute gastroenteritis including nausea, vomiting, stomach pain and diarrhea, as well as fatigue, fever and dehydration. There are currently no effective treatments or vaccines for norovirus, and the ability to curtail outbreaks is inadequate.

Oral protease inhibitor CDI-988 for the treatment of noroviruses and coronaviruses: Our novel, broad-spectrum 3CL protease inhibitor CDI-988 is designed as a potential treatment for noroviruses and coronaviruses. CDI-988 has shown in vitro activity against multiple norovirus strains.

In April 2025 we announced that CDI-988 showed superior broad-spectrum antiviral activity against the norovirus GII.17 strain, the most prevalent strain in the U.S. and Europe in 2024-2025.

In August 2025 we presented favorable Phase 1 safety and tolerability data from all CDI-988 doses, including a high-dose 1200 mg cohort, at the 2025 Military Health System Research Symposium (MHSRS).

In September 2025 we discussed CDI-988’s scientific foundation and clinical progress in an oral presentation at the 9th International Calicivirus Conference, the leading calicivirus scientific meeting.

In September 2025 we received a Study May Proceed Letter from the FDA to conduct a Phase 1b challenge study in the U.S. evaluating CDI-988 as a norovirus preventive and treatment.

In March 2026 we enrolled the first subjects in our Phase 1b challenge study with the initial cohort evaluating the infectivity rate of the GII.2 challenge inoculum, and subsequent cohorts to be orally administered CDI-988 or placebo.

Influenza Programs Influenza is a major global health threat that may become more challenging to treat due to the emergence of highly pathogenic avian influenza viruses and resistance to approved influenza antivirals. Currently approved antiviral treatments for influenza are effective but are burdened with significant viral resistance.

CC-42344 is our novel PB2 inhibitor that showed excellent in vitro activity against pandemic and seasonal influenza A strains, as well as against strains that are resistant to Tamiflu® and Xofluza®.

Oral CC-42344 as a treatment for pandemic and seasonal influenza A

In December 2022 we reported favorable Phase 1 safety and tolerability results.

In December 2023 we began a randomized, double-blind, placebo-controlled Phase 2a human challenge study to evaluate the safety, tolerability, and viral and clinical measurements of CC-42344 in influenza A-infected subjects in the United Kingdom, following authorization from the UK Medicines and Healthcare Products Regulatory Agency.

In May 2025 we reported that CC-42344 was shown to be active against the highly pathogenic 2024 Texas H5N1 avian influenza strain.

In November 2025 an initial Phase 2a study was completed, with CC-42344 showing a favorable safety and tolerability profile with no serious adverse events and no drug-related discontinuations by study participants. Efficacy analyses were not reported due to issues with trial conduct.

We plan to continue development of oral CC-42344 as a treatment for pandemic and seasonal influenza A with an additional Phase 2a study.

Inhaled CC-42344 as prophylaxis and treatment for pandemic and seasonal influenza A

Our preclinical testing showed superior pulmonary pharmacology with CC-42344, including high exposure to drug and a long half-life.

We have developed a dry powder inhalation formulation and have completed toxicology studies.

Influenza A/B program

In October 2025 we received a $500,000 Small Business Innovation Research Phase I award from the NIH’s National Institute of Allergy and Infectious Diseases to support the development of a novel, broad-spectrum lead candidate targeting the influenza A/B polymerase complex.

SARS-CoV-2 and Other Coronavirus Program By targeting viral replication enzymes and proteases, we believe it is possible to develop effective treatments for all diseases caused by coronaviruses including SARS-CoV-2 and its variants, Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome. CDI-988 showed potent in vitro pan-viral activity against common human coronaviruses, rhinoviruses and respiratory enteroviruses, as well as against noroviruses. By the end of 2031, the global COVID-19 therapeutics market is estimated to exceed $16 billion annually.

Oral protease inhibitor CDI-988 for the treatment of coronaviruses and noroviruses: CDI-988 exhibited superior in vitro potency against SARS-CoV-2 and demonstrated a favorable safety profile and pharmacokinetic properties.

In August 2025 we presented favorable safety and tolerability Phase 1 data from all CDI-988 doses, including a high-dose 1200 mg cohort, at the MHSRS.

We are currently pursuing further development of CDI-988 as a prophylaxis and treatment for norovirus and remain optimistic about its viability as a treatment for coronaviruses.

2025 Financial Results

Research and development expenses for 2025 were $5.1 million compared with $12.5 million for 2024, with the decrease primarily due to lower costs with the winddown of the Phase 2a influenza study and reduction in employee-related expenses. General and administrative expenses for 2025 were $4.0 million compared with $5.3 million for 2024, with the decrease primarily due to a reduction in compensation, insurance and corporate expenses.

Net loss for 2025 was $8.8 million, or $0.78 per share, compared with a net loss for 2024 of $17.5 million, or $1.72 per share.

Cocrystal reported unrestricted cash as of December 31, 2025, of $7.7 million compared with $9.9 million as of December 31, 2024. Net cash used in operating activities for 2025 was $8.2 million compared with $16.5 million for 2024. The Company had working capital of $5.9 million and 11.3 million common shares outstanding as of December 31, 2025.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of noroviruses, influenza viruses, coronaviruses (including SARS-CoV-2) and hepatitis C viruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create viable antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Cautionary Note Regarding Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding our plans for the future development of preclinical and clinical product candidates, the and the potential characteristics and benefits of and market for our product candidates. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from inflation, affordability, a deteriorating labor market, the possibility of recession, increases or other developments with respect to interest rates, uncertainty surrounding the impacts arising from imposed and threatened tariffs and developments with respect thereto, and wars and geopolitical conflicts including those in the Middle East and Ukraine on our Company, our collaboration partners, and on the U.S. and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions including any adverse impacts on our ability to obtain raw materials and test animals as well as similar problems with our vendors and our current and any future CROs and CMOs, the progress and results of the studies for CC-42344 and CDI-988 including issues with the initial Phase 2a study for CC-42344 which will prolong the development timeline of such product candidate, the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of future preclinical and clinical trials, general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes including based on initiatives and actions taken by the Trump Administration which could, among other things, result in delays in regulatory approvals or limit access to federal funding for our programs, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government, and potential mutations in a virus we are targeting which may result in variants that are resistant to a product candidate we develop. Further information on our risk factors is contained in our filings with the SEC, including the “Risk Factors” in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2025. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

Investor Contact: Alliance Advisors IR Jody Cain 310-691-7100 [email protected]

Nutriband has selected the commercial worldwide brand name for its lead product, an abuse deterrent fentanyl transdermal system, and will submit to the FDA for approval per FDA Guidance.

Nutriband partnered with Brand Institute, Inc, the global leader in pharmaceutical and healthcare-related brand name and identity development.

ORLANDO, Fla., March 30, 2026 (GLOBE NEWSWIRE) — Nutriband Inc. (NASDAQ:NTRB)(NASDAQ:NTRBW), a company engaged in the development of prescription transdermal pharmaceutical products, today announced that it has selected the commercial worldwide brand name candidate for its lead product, an abuse deterrent fentanyl transdermal system. The proposed brand name and product labeling will be submitted to the FDA and other international regulatory agencies for review and approval. In addition, the selected name is being submitted to the United States Patent and Trademark Office for trademark registration and to secure full intellectual property rights in the United States and internationally.

The company engaged Brand Institute, Inc, the global leader in pharmaceutical and healthcare-related brand name and identity development services to develop the worldwide commercial brand name and visual identity for the product. This product utilizes Nutriband’s AVERSA™ abuse deterrent transdermal technology and has the potential to be the world’s first abuse-deterrent patch designed to deter the abuse and misuse and reduce the risk of accidental exposure of transdermal fentanyl.

Nutriband’s abuse deterrent fentanyl transdermal system has the potential to reach peak annual US sales of $80 million to $200 million.1 While initially concentrating on the US market, the unmet medical need for adequate pain management is a global problem, and the product is in development for all major medical markets worldwide.

Developing a proprietary brand name for a prescription drug product is a critical element in drug product development because the end users (doctors, pharmacists, patients) must be able to easily distinguish a proprietary name from other drug names that are phonetically similar (sound-alike names) or similar in their spelling or appearance (look-alike names). In addition, if the drug name is otherwise confusing or misleading, the patient might receive the wrong product and the subsequent medication error could lead to significant harm to the patient.

Brand Institute has been leading the market for over 20 years with a 75% share of drug name approvals globally, including 87% of FDA approved names in 2024. In addition, Brand Institute has been responsible for many of the opioid chronic pain product brand names and specifically a majority of the abuse deterrent opioid product brand names approved by FDA for sale in the United States.

Drug Safety Institute (DSI), a wholly owned regulatory subsidiary of Brand Institute, will provide regulatory services, solutions and support on the project. DSI is led by former officials from US Food & Drug Administration (FDA), European Medicines Agency (EMA), Health Canada (HC), United States Adopted Name Council (USAN), and World Health Organization (WHO) who co-authored the naming guidance documents while with their former respective agencies.

Nutriband’s AVERSA™ abuse-deterrent technology is utilized to incorporate aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential including opioids and stimulants. The AVERSA™ abuse deterrent technology is protected by a broad international intellectual property portfolio with patents issued in 46 countries including the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

1 Health Advances Aversa Fentanyl market analysis report 2022

About AVERSA™ Abuse-Deterrent Transdermal Technology

Nutriband’s AVERSA™ abuse-deterrent transdermal technology incorporates aversive agents into transdermal patches to prevent the abuse, diversion, misuse, and accidental exposure of drugs with abuse potential. The AVERSA™ abuse-deterrent technology has the potential to improve the safety profile of transdermal drugs susceptible to abuse, such as fentanyl, while making sure that these drugs remain accessible to those patients who really need them. The technology is covered by a broad intellectual property portfolio with patents granted in the United States, Europe, Japan, Korea, Russia, China, Canada, Mexico, and Australia.

About Nutriband, Inc.

We are primarily engaged in the development of a portfolio of transdermal pharmaceutical products. Our lead product under development is an abuse-deterrent fentanyl patch incorporating our AVERSA™ abuse-deterrent technology. AVERSA™ technology can be incorporated into any transdermal patch to prevent the abuse, misuse, diversion, and accidental exposure of drugs with abuse potential.

The Company’s website is www.nutriband.com. Any material contained in or derived from the Company’s websites or any other website is not part of this press release.

About Brand Institute, Inc., and wholly owned regulatory subsidiary, Drug Safety Institute

Brand Institute is the global leader in pharmaceutical and healthcare-related name development, with a portfolio of over 5,000 marketed healthcare brand names and 1,800 USAN/INN nonproprietary names for nearly 1,600 clients. The company partners on over 75% of pharmaceutical brand and nonproprietary name approvals globally every year with healthcare manufacturers. Drug Safety Institute is composed of former naming regulatory officials from global government health agencies, including Food and Drug Administration (FDA), European Medicines Agency (EMA), Health Canada (HC), American Medical Association (AMA), and the World Health Organization (WHO). These regulatory experts co-authored the name review guidelines while with their former respective agencies, with many responsible for ultimately approving (or rejecting) brand name applications to ensure safety and prevent medication errors. To learn more about Brand Institute’s capabilities and experience, please visit www.brandinstitute.com and contact your local Brand Institute representative.

Forward-Looking Statements

Certain statements contained in this press release, including, without limitation, statements containing the words “believes,” “anticipates,” “expects” and words of similar import, constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve both known and unknown risks and uncertainties. The Company’s actual results may differ materially from those anticipated in its forward-looking statements as a result of a number of factors, including those including the Company’s ability to develop its proposed abuse-deterrent fentanyl transdermal system and other proposed products, its ability to obtain patent protection for its abuse technology, its ability to obtain the necessary financing to develop products and conduct the necessary clinical testing, its ability to obtain Federal Food and Drug Administration approval to market any product it may develop in the United States and to obtain any other regulatory approval necessary to market any product in other countries, including countries in Europe, its ability to market any product it may develop, its ability to create, sustain, manage or forecast its growth; its ability to attract and retain key personnel; changes in the Company’s business strategy or development plans; competition; business disruptions; adverse publicity and international, national and local general economic and market conditions and risks generally associated with an undercapitalized developing company, as well as the risks contained under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the Company’s Form S-1, Forms 10-K’s and Forms 10-Q’s, and the Company’s other filings with the Securities and Exchange Commission. Except as required by applicable law, we undertake no obligation to revise or update any forward-looking statements to reflect any event or circumstance that may arise after the date hereof.

Nutriband is a registered trademark of Nutriband, Inc. AVERSA is a trademark of Nutriband, Inc.

Brand Institute and Drug Safety Institute are registered trademarks of Brand Institute, Inc.

2025 marked transition of PrimeC into a late-stage clinical asset with FDA-cleared Phase 3 program in ALS

Statistically significant survival benefit demonstrated, including 65% reduction in risk of death and >14-month median survival advantage

Results published in JAMA Neurology, providing high-level peer-reviewed validation of clinical and biological activity

Advancing toward key regulatory milestones with planned pre-NDS meeting in Canada and near-term Alzheimer’s readout

CAMBRIDGE, Mass., March 31, 2026 /PRNewswire/ — NeuroSense Therapeutics Ltd. (Nasdaq: NRSN) (“NeuroSense” or the “Company”), a late-stage clinical biotechnology company developing treatments for severe neurodegenerative diseases, today reported its financial results for the year ended December 31, 2025 and provided a business update.

“2025 was a transformational year for NeuroSense, as we advanced PrimeC from a successful Phase 2b program into a late-stage clinical asset with a clear regulatory path forward,” said Alon Ben-Noon, Chief Executive Officer of NeuroSense. “As we entered 2026, we further strengthened our clinical and scientific foundation with statistically significant survival data and publication of our results in JAMA Neurology. Together, these milestones position PrimeC as a differentiated therapeutic candidate with the potential to meaningfully impact people with ALS and potentially other neurodegenerative diseases.”

Business Highlights from 2025

2025 marked a transformative year for NeuroSense, as the Company advanced PrimeC from a successful Phase 2b program into a late-stage clinical asset with a clearly defined regulatory and development pathway. Results from the Phase 2b PARADIGM study demonstrated approximately 33% slowing in disease progression over 18 months, alongside a substantial reduction in ALS-related complications. During the year, NeuroSense further strengthened its data package through additional biomarker analyses, including microRNA data, supporting the biological activity of PrimeC, supporting PrimeC’s potential as a disease-modifying therapy.

The Company also completed commercial-scale manufacturing and advanced its regulatory strategy, including engagement with Health Canada and ongoing partnership discussions.

Importantly, in November 2025, NeuroSense received FDA clearance to initiate the PARAGON Phase 3 trial in ALS, marking a key inflection point in the Company’s development trajectory.

NeuroSense also reported early signals of biological activity and statistically significant reductions in key biomarkers associated with Alzheimer’s disease, supporting broader potential across neurodegenerative diseases.

Recent Developments and First Quarter 2026 Highlights

Since the beginning of 2026, NeuroSense has continued to strengthen PrimeC’s position through significant clinical and scientific milestones. The Company reported statistically significant survival data from its Phase 2b study, demonstrating a 65% reduction in the risk of death and a greater than 14-month median survival benefit.

Further reinforcing the strength of its clinical package, results from the PARADIGM trial were published in JAMA Neurology, highlighting meaningful clinical outcomes and biological activity, including biomarker changes consistent with the proposed mechanism of action.

NeuroSense also expanded its scientific visibility through presentations at leading international conferences and strengthened its intellectual property portfolio with newly granted patents in the United States and internationally. In addition, the Company enhanced its Scientific Advisory Board with leading experts to support continued development in ALS and Alzheimer’s disease.

Upcoming Expected Milestones

Additional biomarkers readouts from PARADIGM

Readouts from the Phase 2 Alzheimer’s study

Planned pre-NDS meeting with Health Canada in May 2026

Potential NDS submission in Canada, subject to regulatory feedback

Continued preparation for initiation of the Phase 3 PARAGON trial in ALS

Financial Results

Research and development expenses for the years ended December 31, 2025 and 2024 were $6.2 million and $5.7 million, respectively. The increase of $0.5 million, or 8.8%, was mainly attributed to an increase in share-based payment expenses and increase in our salaries and social benefits expenses which were partly offset by a decrease of our expenses to subcontractors and consultants.

General and administrative expenses for the years ended December 31, 2025 and 2024 were $4.9 million and $4.2 million, respectively. The increase of $0.7 million, or 16.6%, was mainly attributed to an increase in share-based compensation.

As of December 31, 2025, NeuroSense had cash of approximately $0.2 million.

A summary of NeuroSense’s consolidated financial results is included in the tables below.

A copy of the Company’s annual report on Form 20-F for the year ended December 31, 2025 has been filed with the U.S. Securities and Exchange Commission at https://www.sec.gov/ and posted on the Company’s investor relations website at https://neurosense.investorroom.com/sec-filings. The Company will deliver a hard copy of its annual report, including its complete audited financial statements, free of charge, to its shareholders upon request at [email protected].

About NeuroSense

NeuroSense Therapeutics, Ltd. is a clinical-stage biotechnology company focused on discovering and developing treatments for patients suffering from debilitating neurodegenerative diseases. NeuroSense believes that these diseases, which include amyotrophic lateral sclerosis (ALS), Alzheimer’s disease and Parkinson’s disease, among others, represent one of the most significant unmet medical needs of our time, with limited effective therapeutic options available for patients to date. Due to the complexity of neurodegenerative diseases and based on strong scientific research on a large panel of related biomarkers, NeuroSense’s strategy is to develop combined therapies targeting multiple pathways associated with these diseases.

For additional information, we invite you to visit our website and follow us on LinkedIn, YouTube and X. Information that may be important to investors may be routinely posted on our website and these social media channels.

About PrimeC

PrimeC, NeuroSense’s lead drug candidate, is a novel extended-release oral formulation composed of a unique fixed-dose combination of two FDA-approved drugs: ciprofloxacin and celecoxib. PrimeC is designed to synergistically target several key mechanisms of ALS and AD, that contribute to neuron degeneration, inflammation, iron accumulation and impaired ribonucleic acid (“RNA”) regulation to potentially inhibit the progression of ALS and AD.

About ALS

Amyotrophic lateral sclerosis (“ALS”) is an incurable neurodegenerative disease that causes complete paralysis and death within 2-5 years from diagnosis. Every year, more than 5,000 people are diagnosed with ALS in the U.S. alone, with an annual disease burden of $1 billion. The number of people living with ALS is expected to grow by 24% by 2040 in the U.S. and EU.

Forward-Looking Statements

This press release contains “forward-looking statements” that are subject to substantial risks and uncertainties. All statements, other than statements of historical fact, contained in this press release are forward-looking statements. Forward-looking statements contained in this press release may be identified by the use of words such as “anticipate,” “believe,” “contemplate,” “could,” “estimate,” “expect,” “intend,” “seek,” “may,” “might,” “plan,” “potential,” “predict,” “project,” “target,” “aim,” “should,” “will” “would,” or the negative of these words or other similar expressions, although not all forward-looking statements contain these words. Forward-looking statements are based on NeuroSense Therapeutics’ current expectations and are subject to inherent uncertainties, risks and assumptions that are difficult to predict and include statements regarding the timing of regulatory filings, reporting of data, meetings and regulatory decisions. Further, certain forward-looking statements, including statements regarding future development of PrimeC, are based on assumptions as to future events that may not prove to be accurate. The future events and trends may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward looking statements. These risks include the uncertainty regarding the timing of regulatory filings, meetings and regulatory decisions; outcomes and the timing of current and future clinical trials; the risk the PrimeC will not advance towards later-stage development, timing for reporting data, including from the study of PrimeC in Alzheimer’s disease; that the study will not be successful; the ability of NeuroSense to remain listed on Nasdaq; and other risks and uncertainties set forth in NeuroSense’s filings with the Securities and Exchange Commission (SEC). You should not rely on these statements as representing our views in the future. More information about the risks and uncertainties affecting NeuroSense is contained under the heading “Risk Factors” in the Annual Report on Form 20-F filed with the Securities and Exchange Commission on March 31, 2026 and NeuroSense’s subsequent filings with the SEC. Forward-looking statements contained in this announcement are made as of this date, and NeuroSense undertakes no duty to update such information except as required under applicable law.

Potential breakthrough therapeutic targets $50B+ global immunotherapy market1

CHICAGO, March 31, 2026 (GLOBE NEWSWIRE) — MAIA Biotechnology, Inc. (NYSE American: MAIA) (“MAIA”, the “Company”), a clinical-stage biopharmaceutical company focused on developing targeted immunotherapies for cancer, today announced highlights from a poster presented on March 27, 2026, at the European Lung Cancer Congress 2026 (ELCC), a premier thoracic oncology forum held March 25-28, 2026, in Copenhagen, Denmark.

MAIA reports overall survival (OS) beyond two years for eight patients treated with ateganosine sequenced with cemiplimab in Parts A and B of its ongoing Phase 2 THIO-101 clinical trial in non-small cell lung cancer (NSCLC). The patients did not receive subsequent lines of therapy.

The eight patients featured in the poster include:

1 patient in third-line (3L) therapy with survival of 33 months. Expected survival in this heavily pre-treated population is 5.8 months.2

4 patients in 2L therapy with survival over 30 months. Documented OS for standard of care treatment (chemotherapy or checkpoint inhibitors alone) in second-line (2L) therapy is 10.5 months.3

All patients have failed previous treatment (prior to THIO-101) with a checkpoint inhibitor (CPI) alone.

All patients completed 29-34 cycles of therapy, except for 1 patient who completed 2 cycles of therapy with survival follow-up of 725 off therapy.

5 of the 8 patients have survival follow-up ongoing.

“It’s very encouraging to see such outstanding survival from these patients extending beyond our 24-month trial protocol and without any subsequent treatment. OS surpassing two-years bodes well as we continue to monitor patients in our ongoing Phase 3 pivotal trial and in THIO-101 Part C,” said Vlad Vitoc, M.D., Founder and Chief Executive Officer of MAIA. “These results illuminate ateganosine’s valuable role in targeting telomeres to eliminate NSCLC tumor cells and support this treatment—ateganosine sequenced by a CPI—as a potential breakthrough therapeutic option for NSCLC.”

THIO-101 treated 79 patients in Parts A and B of the trial. The Part C expansion is currently enrolling up to 48 participants in Asia and Europe. Treatment with ateganosine followed by cemiplimab (Libtayo®) has shown an acceptable safety profile to date in a heavily pre-treated population.

Ateganosine (THIO, 6-thio-dG or 6-thio-2’-deoxyguanosine) is a first-in-class investigational telomere-targeting agent currently in clinical development to evaluate its activity in non-small cell lung cancer (NSCLC). Telomeres, along with the enzyme telomerase, play a fundamental role in the survival of cancer cells and their resistance to current therapies. The modified nucleotide 6-thio-2’-deoxyguanosine induces telomerase-dependent telomeric DNA modification, DNA damage responses, and selective cancer cell death. Ateganosine-damaged telomeric fragments accumulate in cytosolic micronuclei and activates both innate (cGAS/STING) and adaptive (T-cell) immune responses. The sequential treatment of ateganosine followed by PD-(L)1 inhibitors resulted in profound and persistent tumor regression in advanced, in vivo cancer models by induction of cancer type–specific immune memory. Ateganosine is presently developed as a second or later line of treatment for NSCLC for patients that have progressed beyond the standard-of-care regimen of existing checkpoint inhibitors.

About THIO-101 Phase 2 Clinical Trial

THIO-101 is a multicenter, open-label, dose finding Phase 2 clinical trial. It is the first trial designed to evaluate ateganosine’s anti-tumor activity when followed by PD-(L)1 inhibition. The trial is testing the hypothesis that low doses of ateganosine administered prior to cemiplimab (Libtayo®) will enhance and prolong immune response in patients with advanced NSCLC who previously did not respond or developed resistance and progressed after first-line treatment regimen containing another checkpoint inhibitor. The trial design has two primary objectives: (1) to evaluate the safety and tolerability of ateganosine administered as an anticancer compound and a priming immune activator (2) to assess the clinical efficacy of ateganosine using Overall Response Rate (ORR) as the primary clinical endpoint. The expansion of the study will assess overall response rates (ORR) in advanced NSCLC patients receiving third line (3L) therapy who were resistant to previous checkpoint inhibitor treatments (CPI) and chemotherapy. Treatment with ateganosine followed by cemiplimab (Libtayo®) has shown an acceptable safety profile to date in a heavily pre-treated population. For more information on this Phase II trial, please visit ClinicalTrials.gov using the identifier NCT05208944.

About MAIA Biotechnology, Inc.

MAIA is a targeted therapy, immuno-oncology company focused on the development and commercialization of potential first-in-class drugs with novel mechanisms of action that are intended to meaningfully improve and extend the lives of people with cancer. Our lead program is ateganosine (THIO), a potential first-in-class cancer telomere targeting agent in clinical development for the treatment of NSCLC patients with telomerase-positive cancer cells. For more information, please visit www.maiabiotech.com.

Forward Looking Statements

MAIA cautions that all statements, other than statements of historical facts contained in this press release, are forward-looking statements. Forward-looking statements are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels or activity, performance or achievements to be materially different from those anticipated by such statements. The use of words such as “may,” “might,” “will,” “should,” “could,” “expect,” “plan,” “anticipate,” “believe,” “estimate,” “project,” “intend,” “future,” “potential,” or “continue,” and other similar expressions are intended to identify forward looking statements. However, the absence of these words does not mean that statements are not forward-looking. For example, all statements we make regarding (i) the initiation, timing, cost, progress and results of our preclinical and clinical studies and our research and development programs, (ii) our ability to advance product candidates into, and successfully complete, clinical studies, (iii) the timing or likelihood of regulatory filings and approvals, (iv) our ability to develop, manufacture and commercialize our product candidates and to improve the manufacturing process, (v) the rate and degree of market acceptance of our product candidates, (vi) the size and growth potential of the markets for our product candidates and our ability to serve those markets, and (vii) our expectations regarding our ability to obtain and maintain intellectual property protection for our product candidates, are forward looking. All forward-looking statements are based on current estimates, assumptions and expectations by our management that, although we believe to be reasonable, are inherently uncertain. Any forward-looking statement expressing an expectation or belief as to future events is expressed in good faith and believed to be reasonable at the time such forward-looking statement is made. However, these statements are not guarantees of future events and are subject to risks and uncertainties and other factors beyond our control that may cause actual results to differ materially from those expressed in any forward-looking statement. Any forward-looking statement speaks only as of the date on which it was made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as required by law. In this release, unless the context requires otherwise, “MAIA,” “Company,” “we,” “our,” and “us” refers to MAIA Biotechnology, Inc. and its subsidiaries.

Encouraging Phase 2 HIT data and recent FDA feedback support continued advancement of CAD-1005 as Cadrenal’s near-term development priority; broader 12-LOX platform remains a longer-term opportunity

PONTE VEDRA, Fla., March 31, 2026 (GLOBE NEWSWIRE) — Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a late-stage biopharmaceutical company advancing novel therapies for life-threatening immune and thrombotic conditions, today reported its financial results for the fourth quarter and full year ended December 31, 2025, and provided a corporate update highlighting recent progress across its CAD-1005 program for HIT and broader 12-LOX inhibitor platform. The update reflects continued progress for CAD-1005, Cadrenal’s first-in-class 12-LOX inhibitor for suspected heparin-induced thrombocytopenia (HIT), including completion of its End-of-Phase 2 (EOP2) meeting with the U.S. Food and Drug Administration (FDA) on March 26, 2026, to align on the proposed Phase 3 pivotal trial of CAD-1005 in patients with HIT.

Recent Highlights

Reported encouraging results from a randomized, blinded, placebo-controlled Phase 2 study of CAD-1005 in HIT, with fewer new or worsening thrombotic events observed in patients treated with CAD-1005 on a background of standard anticoagulant therapy.

Observed a greater than 25% absolute reduction in thrombotic events in the CAD-1005 treatment arm versus placebo, while also gaining important insight that platelet count recovery may not be an appropriate surrogate endpoint for clinical efficacy in HIT.

On March 26, 2026, the Company completed its End-of-Phase 2 meeting with the FDA and clarified a potential registrational path for its planned Phase 3 pivotal trial.

Incorporation of FDA feedback into Phase 3 protocol is currently underway.

Continued to position CAD-1005 as the only selective 12-LOX inhibitor currently in clinical development, supported by Orphan Drug and Fast Track designations from the FDA and orphan drug status from the European Medicines Agency.

While HIT remains the Company’s near-term development priority, it continues to see additional scientific support for 12-LOX inhibition beyond HIT, including research in obesity and type 2 diabetes showing potential improvements in glycemic control, pancreatic beta-cell preservation, and inflammatory signaling.

“CAD-1005 continues to reinforce our conviction that selective 12-LOX inhibition may offer a differentiated approach for patients with HIT, a life-threatening, immune-mediated prothrombotic disorder, and a serious condition with substantial unmet need,” commented Quang X. Pham, Chairman & CEO. “Despite modern care, mortality remains high (up to 18-20% in some groups), with many survivors facing limb amputations. The encouraging Phase 2 results, including the reduction in thrombotic events observed on top of standard anticoagulant therapy, further strengthen our confidence in the program and in the decision to make CAD-1005 our lead development priority.”

“The recent End-of-Phase 2 meeting with the FDA is an important milestone in clarifying the regulatory path forward for CAD-1005. As we incorporate FDA feedback and prepare for the next stage of development, we remain focused on advancing CAD-1005 as our lead priority in HIT. At the same time, we continue to evaluate longer-term opportunities across our broader 12-LOX platform and other pipeline assets to support future value creation.”

Fourth Quarter 2025 Financial Highlights Research and development expenses for the quarter ended December 31, 2025, were $0.7 million compared to $1.5 million for the same period in 2024. General and administrative expenses for the quarter ended December 31, 2025, were $2.4 million compared to $2.7 million for the same period in 2024. Cadrenal reported a net loss of $3.0 million for the quarter ending December 31, 2025, compared to $4.2 million for the same period in 2024.

On December 31, 2025, Cadrenal had cash and cash equivalents of $4.0 million. The Company is evaluating financing and strategic alternatives to support its planned clinical development activities. The Company had approximately 2.3 million shares of common stock outstanding as of December 31, 2025.

About Cadrenal Therapeutics, Inc.

Cadrenal Therapeutics, Inc. (Nasdaq: CVKD) is a late-stage biopharmaceutical company advancing novel therapies for life-threatening immune and thrombotic conditions. Its lead program, CAD-1005, is a first-in-class 12-LOX inhibitor for the treatment of heparin-induced thrombocytopenia (HIT), a deadly immune-mediated thrombotic disorder. CAD-1005 has received Orphan Drug and Fast Track designations from the U.S. Food and Drug Administration and orphan drug status from the European Medicines Agency. Second-generation 12-LOX oral therapeutics are also under development for chronic indications.

The Company’s broader pipeline features tecarfarin, a late-stage oral vitamin K antagonist designed to prevent heart attacks, strokes, and deaths due to blood clots in patients requiring chronic anticoagulation, including for patients with end-stage kidney disease and left ventricular assist devices, and frunexian, a parenteral Factor XIa inhibitor intended for use in acute hospital settings.

Any statements in this press release about future expectations, plans, and prospects, as well as any other statements regarding matters that are not historical facts, may constitute “forward-looking statements.” The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potentially,” “predict,” “project,” “should,” “target,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. These statements include, without limitation, statements regarding the continued progress for CAD-1005 for suspected heparin-induced thrombocytopenia; a potential registrational path for the Company’s planned Phase 3 pivotal trial; additional scientific support for 12-LOX inhibition beyond HIT; research in obesity and type 2 diabetes showing potential improvements in glycemic control, pancreatic beta-cell preservation, and inflammatory signaling; selective 12-LOX inhibition offering a differentiated approach for patients with HIT, a serious condition with substantial unmet need; continuing to evaluate longer-term opportunities across the Company’s broader 12-LOX platform and other pipeline assets to support future value creation; the Company’s clinical development plans and timing, regulatory pathway and potential registration strategy for CAD-1005; the design and initiation of its planned Phase 3 trial, the potential therapeutic and commercial opportunity for CAD-1005 and the Company’s broader pipeline, and the Company’s capital requirements and potential financing or strategic alternatives. Actual results may differ materially from those indicated by such forward-looking statements as a result of various important factors, including the ability to continue progress CAD-1005; the ability to successfully plan a registrational path for the Company’s planned Phase 3 pivotal trial; the ability for 12-LOX inhibition to provide improvements in obesity and type 2 diabetes in glycemic control, pancreatic beta-cell preservation, and inflammatory signaling and support future value creation; the Company’s ability to raise sufficient funding to commence and complete its planned Phase 3 trial, and the other risk factors described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, and the Company’s subsequent filings with the Securities and Exchange Commission, including subsequent periodic reports on Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. Any forward-looking statements contained in this press release speak only as of the date hereof and, except as required by federal securities laws, the Company specifically disclaims any obligation to update any forward-looking statement, whether as a result of new information, future events, or otherwise.

For more information, please contact:

Lytham Partners, LLC Robert Blum, Managing Partner 602-889-9700 [email protected]

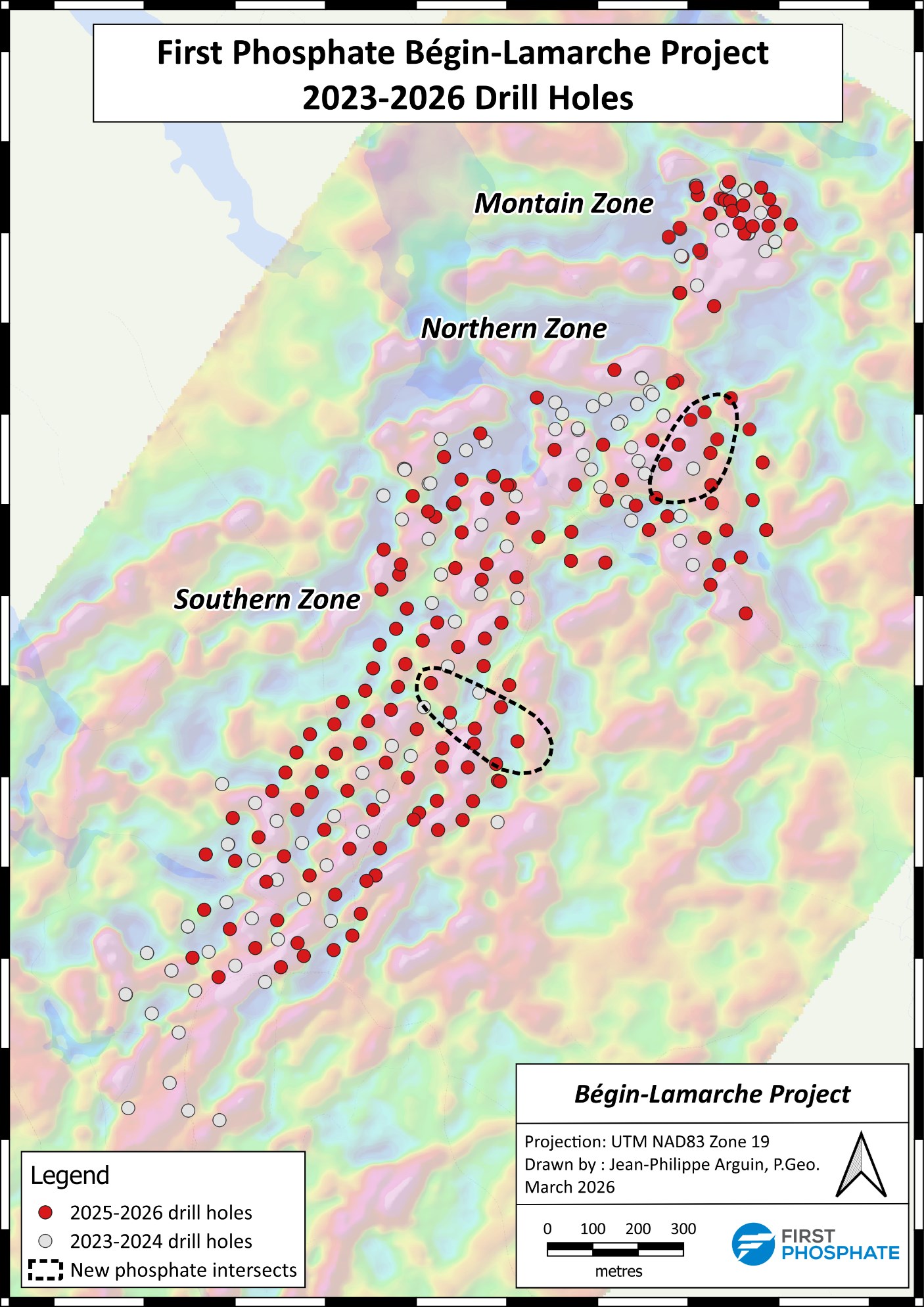

Saguenay-Lac-Saint-Jean, Quebec–(Newsfile Corp. – March 31, 2026) – First Phosphate Corp. (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) (“First Phosphate” or the “Company“) is pleased to announce the completion of its infill drill program launched on October 21, 2025 at its Bégin-Lamarche property in Saguenay-Lac-St-Jean, Quebec.

The drilling campaign has confirmed extensive, continuous mineralization across the existing horizon of the initial resource estimate. The drill program has also discovered two new phosphate intersects located in the Northern Zone and in the Southern Zone on the eastern side of the existing mineralized zone. An additional 10,000 meters of targeted drilling was added to the initial drill program of 30,000 meters to solidify an understanding of these new intersects as well as to test additional mineralization located at depth in various areas across the Northern and Southern Zones.

The Company is currently processing the full set of drill results from its original and expanded drill campaign which totalled about 40,000 m with the goal of upgrading the geological model for the Bégin-Lamarche property in the coming weeks.

“We were able to discover, drill and create a significant geological model for the Bégin-Lamarche property all within about 3.5 years,” commented Gilles Laverdiere, Chief Geologist of First Phosphate. “Such rapid progression from initial discovery reflects the exceptional continuity of the phosphate mineralization and the efficiency of our exploration approach.”

The Company also announces that Gilles Laverdiere will be retiring as Chief Geologist following 48 years of dedicated service to the mining industry. Existing team member, Steeve Lavoie, PGeo., will assume the role of Chief Geologist. Steeve has over 20 years of experience in the mineral exploration industry, having worked most recently with Agnico Eagle Mines prior to joining First Phosphate in November 2025.

“I’d like to thank Gilles Laverdière for his dedication to First Phosphate and the Bégin-Lamarche project since its early discovery and for building our strong exploration foundation,” says First Phosphate CEO, John Passalacqua. “Most importantly, we would like to thank Gilles for delaying his retirement until he could see through Bégin-Lamarche to its resource definition and geological modelling. Gilles is a man of remarkable dedication and a true role model for the industry.”

The Company also announces today a grant of 300,000 incentive stock options (the “Options”) to Steeve Lavoie in accordance with the terms of the Company’s Omnibus Equity Incentive Plan. Each Option has an exercise price of $0.98 and expires on December 29, 2028 with 25% vesting every 6 months for two years following the date of grant. All securities issued in accordance with the Option grant are subject to a hold period of four months plus one day.

First Phosphate Bégin-Lamarche Project 2023-2026 Drill Holes

The scientific and technical information relating to First Phosphate contained in this press release has been reviewed and approved by Gilles Laverdière, P.Geo., Chief Geologist of First Phosphate and Steeve Lavoie, P,Geo., Geology Manager of First Phosphate who are qualified persons within the meaning of National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”).

About First Phosphate Corp.

First Phosphate (CSE: PHOS) (OTCQX: FRSPF) (OTCQX ADR: FPHOY) (FSE: KD0) is a mineral exploration and development and clean technology company dedicated to building and reshoring a vertically integrated mine-to-market supply chain for the production of LFP batteries in North America. Target markets include energy storage, data centers, robotics, mobility, and national security.

First Phosphate’s flagship Bégin-Lamarche property, located in Saguenay-Lac-Saint-Jean, Québec, Canada, represents a rare North American igneous phosphate resource producing high-purity phosphate characterized by very low levels of impurities.

Forward-Looking Information and Cautionary Statement

This release includes certain statements that may be deemed “forward-looking information”. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking information. In particular, of the GPI funding award under the contribution agreement with NRCan and the project funded thereby including the Company’s plans for building and onshoring a vertically integrated mine-to-market LFP battery supply chain for North America. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those forward-looking statements. Factors that could cause actual results to differ materially from those in forward-looking statements include development and exploration successes, continued availability of capital and financing, and general economic, market or business conditions. These statements are based on a number of assumptions including, among other things, assumptions regarding general business and economic conditions; there being no significant disruptions affecting the activities of the Company or inability to access required project inputs; permitting and development of the projects being consistent with the Company’s expectations; the accuracy of the current mineral resource estimates for the Company and results of metallurgical testing; certain price assumptions for P2O5 and Fe2O3; inflation and prices for Company project inputs being approximately consistent with anticipated levels; the Company’s relationship with First Nations and other Indigenous parties remaining consistent with the Company’s expectations; the Company’s relationship with other third party partners and suppliers remaining consistent with the Company’s expectations; and government relations and actions being consistent with Company expectations. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Accordingly, readers should not place undue reliance on the forward-looking information contained in this press release. The Company does not assume any obligation to update or revise its forward-looking statements, whether because of new information, future events or otherwise, except as required by applicable law. All forward-looking information contained in this release is qualified by these cautionary statements.

TNX-4800 is a long-acting anti-Borrelia burgdorferi OspA human monoclonal antibody in development as a single-dose Lyme prophylactic

Phase 1 study of TNX-4800 demonstrated safety, tolerability, and pharmacokinetics supportive of approximately four months protection

Company expects to initiate a randomized, double-blind, placebo-controlled, adaptive Phase 2 field study in the first half of 2027, pending FDA clearance

BERKELEY HEIGHTS, N.J., March 31, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully integrated, commercial biotechnology company, announced Phase 1 data of TNX-4800 (formerly known as mAb 2217LS)1,2 was presented by Mark S. Klempner, MD, professor of medicine at UMass Chan Medical School, an inventor of TNX-4800 and principal investigator of the study, on March 30, 2026, at the World Vaccine Congress Washington 2026. Tonix also announced its planned strategy for an adaptive Phase 2 field study expected to initiate in the first half of 2027, pending FDA clearance.

TNX-4800 is a long-acting borreliacidal (or bactericidal), human monoclonal antibody (mAb) with an engineered crystallizable fragment (Fc) domain for an extended half-life that targets the outer surface protein A (OspA) of Borrelia burgdorferi, which causes 99.9% of Lyme disease cases in the U.S.3,4 Tonix is developing TNX-4800, which the Company in-licensed from UMass Chan Medical School in 2025, as a prophylactic that is administered in a single subcutaneous (SC) dose expected to provide approximately four months protection to people in endemic areas during the U.S. tick season. There are currently no marketed U.S. Food and Drug Administration (FDA)-approved vaccines or prophylactics to protect against Lyme disease.

“TNX-4800 is expected to provide a preventative option to the 87 million5 people in the United States who are at high risk of contracting the disease because they live, work, or vacation in a tick-endemic area,” said Seth Lederman, MD, Chief Executive Officer of Tonix Pharmaceuticals. “As a monoclonal antibody, we believe TNX-4800 offers significant advantages over vaccines in development. Lyme disease vaccines that elicit antibodies to OspA currently in development take more than six months to offer protection and require complex immunization schedules. A previously approved anti-OspA vaccine was withdrawn due to poor uptake,6 potentially relating to its complex immunization schedule.”

Dr. Lederman continued, “TNX-4800, targeting Borrelia burgdorferi, the serotype that causes 99.9% of Lyme disease in the U.S., is a single dose subcutaneous administration that potentially offers immunity within two days for a duration of approximately four months. We believe TNX-4800’s differentiating characteristics could offer meaningful improvements for people seeking protection from Lyme disease. We believe the Phase 1 pharmacokinetic (PK) data support our plan to conduct an adaptive field study in the first half of 2027, pending FDA clearance, in which protection at four months is the primary endpoint, and protection at six months is a key secondary endpoint.”

Phase 1 Results

“Our study demonstrated potentially protective blood levels of TNX-4800 at two days, with protective blood levels sustained for at least four months due to its extended half-life design,” said Dr. Klempner. “Additionally, with its differentiated mechanism of action, TNX-4800 has the potential to provide passive immunity by directly supplying neutralizing antibodies, bypassing the need for a vaccine to induce a patient’s immune system to generate its own antibodies, which can be associated with other issues. We look forward to further clinical investigation of TNX-4800 as we strive to overcome this major public health challenge.”

The primary objective of the Phase 1 study was to evaluate the safety and tolerability of a SC injection of TNX-4800 when administered to healthy male and female subjects ages 19-65 years old. The secondary objective was to evaluate the PK of a SC dose of TNX-4800 when administered to healthy subjects. 44 subjects were enrolled, with 41 subjects completing the study. Subjects received a single SC administration of placebo or TNX-4800 at 0.5, 1.5, 5, or 10 mg/kg.

Results showed no significant clinical or laboratory safety signals, with most adverse events mild or moderate. Peak serum concentration (Cmax) increased by ~25-fold for a 20-times increase in dose. Serum TNX-4800 was measurable at earliest sampling time of two days, indicating rapid systemic absorption. TNX-4800 levels remained quantifiable for >200 days in 80% of subjects at the lowest dose, and for up to 350 days in the majority of subjects at higher doses (i.e., ≥ 1.5 mg/kg). The mean half-life ranged from 62-69 days across TNX-4800 cohorts. Serum concentrations were quantifiable for up to 12 months in most subjects.

Mean exposure for the 10 mg/kg cohort had <17% of the highest exposures in a nonclinical toxicology study.

The maximum half-life ranged from 81-104 days, with the 10mg/kg cohort at 97 days and 5mg/kg cohort at 87 days.

In the 5mg/kg dose cohort, mean serum TNX-4800 concentration was approximately 10 μg/ml at four months, which was approximately twice the minimum effective concentration, or MEC, calculated from in vitro bactericidal activity, and approximately the MEC from in vitro tick-feeding experiments. These data support Tonix’s planned evaluation of protection at four months as the proposed primary endpoint.

Adaptive Phase 2 Field Study Plans

Pending FDA clearance, the Company plans to initiate an adaptive field study in the first half of 2027. TNX-4800 will be studied in a randomized, double-blind, placebo-controlled, adaptive Phase 2 field study to evaluate the efficacy of a single SC dose of TNX-4800, 350 mg, in preventing the first occurrence of confirmed Lyme disease during the primary efficacy surveillance period (Day 3 through Month 4 following administration). Based on the Phase 1 PK data, a fixed dose of 350 mg was selected for the Phase 2 field study, which is expected to provide exposures comparable to the 5 mg/kg dose evaluated in Phase 1. Participants will include adolescents and adults 16 to 65 years of age in Lyme-endemic areas in the U.S. The primary endpoint will be the prevention of Lyme disease at four months (comparison of TNX-4800 group and placebo group). A key secondary endpoint will be the prevention of Lyme disease at six months (comparison of TNX-4800 and placebo).

The Company expects to have GMP investigational product available for clinical testing in early 2027. Additionally, if necessary and pending FDA clearance, the Company plans to initiate a controlled human infection model (CHIM) study in 2028.

A copy of Dr. Klempner’s World Vaccine Congress Washington 2026 presentation is available under the Scientific Presentations tab on the Tonix website at https://www.tonixpharma.com/scientific-presentations. The Company’s TNX-4800 specific presentation can be found under the Presentations tab on the Investors section of the Tonix website at https://ir.tonixpharma.com/presentations.

About TNX-4800 TNX-4800 (formerly known as mAb 2217LS) is a long-acting borreliacidal (or bactericidal), human monoclonal antibody with an engineered extended half-life that targets the outer-surface protein A (OspA) on Lyme-causing Borrelia bacteria. When TNX-4800-containing blood is ingested by the tick, TNX-4800 kills and blocks the maturation of Borrelia burgdorferi in the mid-gut of infected deer ticks. The Company in-licensed TNX-4800 from UMass Chan Medical School in 2025. Published work in animals showed that TNX-4800 was 95% effective at preventing infection of non-human primates after six days of exposure to ticks infected with Borrelia burgdorferi.1 TNX-4800 was derived from mAb 2217 by amino acid substitutions in its Fc domain, which serve to prolong the serum half-life. A single administration is designed to potentially provide immunity against Lyme disease within two days and maintain protective antibody levels for approximately four months, without relying on the recipient’s immune system to generate antibodies. TNX-4800 also avoids the multidose priming schedules required for OspA vaccines in development7 and the FDA-approved vaccine that was withdrawn from the market.8

About the TNX-4800 Phase 1 Study TNX-4800 was studied in a randomized, double-blind, sequential dose-escalation study (NCT04863287) that evaluated safety, tolerability, PK, and immunogenicity of TNX-4800 in healthy adults. 44 subjects were randomized, and 41 completed the study. Subjects received a single SC administration of placebo or TNX-4800 at 0.5, 1.5, 5, or 10 mg/kg. Safety was assessed via clinical and lab evaluations. Drug exposure increased by approximately 25 times for a 20-times increase in dose. Serum TNX-4800 was measurable at the earliest sampling time of two days, indicating rapid systemic absorption. TNX-4800 concentrations remained quantifiable for >200 days in 80% of volunteers at the lowest dose and for up to 350 days in the majority of volunteers at higher doses (i.e., ≥ 1.5 mg/kg). Mean half-life ranged from 62-69 days across groups. Serum concentrations remained quantifiable for up to 12 months in most subjects. Mean exposure for the 10 mg/kg cohort was less than 17% of the highest exposures in a rat toxicology study. Anti-drug antibodies were detected in <10% of treated subjects, with no impact on PK. Most adverse events were mild or moderate. TNX-4800 was determined to be generally safe and well tolerated.

About Lyme Disease In the United States, Lyme disease is caused by the bacterium Borrelia burgdorferi. Lyme disease remains the most common vector-borne infection in the United States, and its incidence is climbing each year, due in part to global changes in climate expanding the habitat range for ticks.9 It occurs most commonly in the Northeast, mid-Atlantic, and upper-Midwest regions. Lyme disease bacteria are transmitted through the bite of infected Ixodes ticks. Typical symptoms include fever, headache, fatigue, and a characteristic skin rash called erythema migrans. If left untreated, infection can spread to joints, heart, and nervous system. Laboratory testing is helpful if used correctly and performed with FDA-cleared tests. Although many cases of Lyme disease can be treated successfully with antibiotics, diagnosis and treatment are often delayed or missed. Chronic Lyme is considered an Infection Associated Chronic Illness (IACI), and is a chronic, debilitating disease state characterized by joint and muscle pain, fatigue, and other symptoms.10

Citations 1Schiller ZA, et al. J Clin Invest. 2021 131(11):e144843. 2Wang Y, et al. J Infect Dis. 2016. 214(2):205-11. 3Marques AR, et al. Emerg Infect Dis. 2021. 27(8):2017-2024. 4Pritt BS, et al. Lancet Infect Dis. 2016. 6(5):556-564. 5Kugeler KJ, et al. Emerg Infect Dis. 2021. 27(2):616-619. 6 Nigrovic LE, et al. Epidemiol Infect. 2006. Aug 8;135(1):1-8. 7Comstedt P, et al. Vaccine. 2015 33(44):5982-8. 8Connaught’s (ImuLyme™) and SmithKline Beecham’s (LYMErix™) Lyme disease vaccines were withdrawn. Nigrovic LE, et al. Epidemiol Infect. 2007 135(1):1-8. 9Gomes-Solecki M, et. al. Clin Infect Dis. 2020 70(8):1768-1773. 10National Academies of Sciences, Engineering, and Medicine. 2025. Charting a Path Toward New Treatments for Lyme Infection-Associated Chronic Illnesses. Washington, DC: The National Academies Press. https://doi.org/10.17226/28578.

Tonix Pharmaceuticals Holding Corp. Tonix Pharmaceuticals* is a fully-integrated, commercial-stage biotechnology company focused on central nervous system (CNS) and immunology treatments in areas of high unmet medical need. TONMYA® (cyclobenzaprine HCl sublingual tablets 2.8 mg), is the first new treatment for fibromyalgia in adults in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® (sumatriptan injection 3 mg) and Tosymra® (sumatriptan nasal spray 10 mg). Tonix is investigating TONMYA® in Phase 2 clinical trials to evaluate its potential in major depressive disorder and acute stress disorder/acute stress reaction. In addition, the Company’s CNS portfolio includes TNX-2900 (intranasal oxytocin), which is Phase 2 ready for the treatment of Prader-Willi syndrome, a rare disease. Tonix is also advancing a pipeline of immunology programs, including TNX-4800, a Phase 2 ready long-acting human anti-Borrelia OspA monoclonal antibody (mAb) for the prevention of Lyme disease in the U.S., and TNX-1500, a Phase 2 ready third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. To learn more, visit www.tonixpharma.com and follow the Company on LinkedIn and X.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.