Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. For the full year 2025, MariMed reported record revenue as well as the sixth consecutive year of positive adjusted EBITDA. Wholesale was once again the star performer, with sales increasing 11% y-o-y. MariMed increased its distribution footprint penetration to 85% of the dispensaries in its core markets.

4Q25 Results. Revenue of $41.7 million rose 7.2% y-o-y and exceeded our $40.5 million estimate. Better than expected retail sales drove the results. Adjusted gross margin came in at 39.9% versus 43.2% last year. Adjusted EBITDA totaled $4.4 million, down from $5.9 million in 4Q24. MariMed reported adjusted net income of $2.2 million, compared to a net loss of $3.1 million in 4Q24.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gold is heading into the weekend with back-to-back weekly losses — a signal that something unusual is happening in commodity markets. The metal that investors typically rush to during geopolitical crises is being undercut by the very crisis driving its usual tailwinds.

Spot gold is trading around $5,084 per ounce on Friday, down nearly 1% from Thursday’s close and on pace for a 2.4% weekly decline. That would mark the first consecutive weekly drop since November, pulling gold further from its all-time high of $5,595 set on January 29. Despite the retreat, the metal remains roughly 17% higher year-to-date — a figure that should not be lost on investors trying to contextualize the current pullback.

The Oil-Inflation Paradox

The culprit is crude. Oil prices near $100 a barrel — sustained by the ongoing US-Israeli military campaign against Iran — are creating an inflation feedback loop that is actually working against gold in the near term. Here’s the mechanism: rising oil strengthens the U.S. dollar, since the U.S. is a net energy exporter. A stronger dollar makes dollar-denominated gold more expensive for global buyers, compressing demand. At the same time, oil-driven inflation is forcing markets to price out Federal Reserve rate cuts, and gold doesn’t pay interest — so higher-for-longer rates make yield-bearing assets comparatively more attractive.

The U.S. Dollar Index has gained about 1% over the past five trading sessions and is up 3.3% over the past month. That’s a meaningful headwind for bullion.

Fed Watch Dominates

Markets now assign just a 4.4% probability to a rate cut at next week’s Fed meeting, with 95.6% of participants expecting rates to hold at 3.50%–3.75%. Earlier this year, the consensus expectation was two cuts in 2026. That view has collapsed as energy prices reignite inflationary pressure — and fresh consumer spending data released Friday showed spending barely moved in January, adding to concerns that a stagflationary dynamic could be forming ahead of the conflict’s economic ripple effects.

U.S. consumer sentiment has also declined to a three-month low as gasoline prices climb. This matters for the Fed: a consumer-led slowdown paired with sticky inflation removes the policy flexibility that gold bulls were counting on.

Where Does Gold Go From Here?

The longer-term picture remains constructive. Wall Street’s major banks haven’t flinched — J.P. Morgan holds a $6,300 price target for gold in 2026, and Deutsche Bank is at $6,000. Central bank buying, persistent inflation above the Fed’s 2% target, and geopolitical uncertainty all underpin a structurally bullish case. The current weakness appears to be a recalibration, not a reversal.

For small and microcap investors, the gold pullback carries downstream implications worth watching. Junior miners and gold royalty companies — many of which trade well below the $2 billion market cap threshold — tend to amplify gold’s moves in both directions. A sustained drop from current levels would compress margins and valuations across that segment. Conversely, if conflict escalation or a dollar reversal sends gold back toward $5,500, smaller producers could see outsized recoveries.

The market is being asked a simple question right now: is $100 oil a headwind or a catalyst for gold? The answer, at least this week, is headwind.

Strategic Portfolio Optimization Creating Long-Term Value

Cost Management Drives Restaurant Margin Improvement in Fourth Quarter

Full Year 2026 Financial Targets Introduced

DENVER–(BUSINESS WIRE)– The ONE Group Hospitality, Inc. (“The ONE Group” or the “Company”) (Nasdaq: STKS) today reported its financial results for the fourth quarter and full year ended December 28, 2025.

Effective January 1, 2025, the Company adopted a new fiscal calendar structure using four 13-week quarters, with a 53rd week added when necessary. The 2025 fiscal year ran from January 1, 2025, to December 28, 2025.

This fiscal calendar change created timing differences that impacted quarterly comparisons: the fourth quarter of 2025 had 91 days versus 92 days in the fourth quarter of 2024. Additionally, the New Year’s Eve holiday shifted from fiscal 2025 to fiscal 2026. The exclusion of New Year’s Eve in the current year impacted total GAAP revenues by approximately 2.5%, representing 37% of the total GAAP revenue decline for the quarter.

Highlights for the fourth quarter 2025 compared to the same quarter in 2024 are as follows:

Total GAAP revenues decreased 6.7% to $207 million from $222 million;

Consolidated comparable sales*decreased 1.8%;

GAAP net loss attributable to The ONE Group Hospitality, Inc. increased to $6 million from a net income of $2 million primarily related to a non-cash loss on impairment of $7 million related to the Grill optimization strategy;

Restaurant Operating Profit**increased by 10 basis points to 19.5% of owned restaurant net revenue, excluding Grill Concepts restaurants closed or to be closed, from 19.4%; and,

Adjusted EBITDA*** attributable to The ONE Group Hospitality, Inc. decreased to $28 million from $31 million, with approximately $3 million of the decrease attributable to the New Year’s Eve holiday shift from fiscal 2025 to fiscal 2026.

Highlights for the full year 2025 compared to the full year 2024 are as follows:

Total GAAP revenues increased 19.7% to $806 million from $673 million;

Consolidated comparable sales*decreased 3.7%;

GAAP net loss attributable to The ONE Group Hospitality, Inc. increased to $92 million from a net loss of $17 million due primarily to an increase in the income tax expenses of $69 million, primarily related to the establishment of a non-cash tax valuation allowance, and non-cash lease termination and exits costs of $7 million coupled with a non-cash impairment of $11 million related to the Grill optimization strategy;

Adjusted Operating Income**** increased 15.2% to $38 million from $33 million; and,

Adjusted EBITDA*** attributable to The ONE Group Hospitality, Inc. increased 16.3% to $89 million, excluding approximately $4 million attributable to two days in fiscal year 2025 versus fiscal year 2024, from $76 million.

“Guests continue to choose our differentiated Vibe Dining concepts when they want memorable experiences. In the fourth quarter, consolidated comparable sales improved by four percentage points sequentially from the third quarter, with every brand contributing. So far in the first quarter, we are delivering positive consolidated comparable sales. These results confirm that our strategy is working, even in a challenging consumer environment,” said Emanuel “Manny” Hilario, President and CEO of The ONE Group.

“Our disciplined cost management initiatives continue to drive results. In the fourth quarter, we expanded our restaurant operating margins, even while facing sales deleveraging. Looking ahead, our operational foundation remains strong, supported by beef supply and pricing secured through September 2026 and significant cost synergies from the Benihana acquisition that we believe we have yet to fully capture,” Hilario continued.

“In 2025, we took decisive action to optimize our portfolio and position the company for sustained long-term growth. We closed six underperforming Grill locations and identified up to five additional units for conversion to our higher-performing Benihana or STK formats through 2026. Our first RA Sushi to STK conversion in Scottsdale, Arizona has exceeded expectations, operating at a run rate of approximately $7 million in annualized sales on an approximate $1 million capital investment. This validates the strength of this repositioning strategy. Additionally, we advanced our asset-light growth strategy by securing development rights for ten Benihana and Benihana Express locations in the San Francisco Bay Area, representing the largest franchise agreement in our Company’s history. We have also secured a commitment for an additional franchised Benihana location and a licensed Benihana Express location in the Florida Keys,” Hilario concluded.

Strategic Portfolio Optimization

Grill Concepts Rationalization:

Closed six underperforming Grill locations in 2025 and one in 2026;

Identified up to five additional Grill units for conversion to Benihana or STK formats through 2026;

Conversion economics: approximately $1.0 to $1.5 million per conversion with a one-year payback; and

Expected outcome: 100% profitable Grill portfolio with enhanced margins.

Capital Efficiency Focus:

Prioritizing asset-light and conversion-driven growth;

Targeting new company-owned openings averaging $1.5 million or less in build-out costs;

Significant reduction in discretionary capital expenditures to strengthen balance sheet; and

Advancing existing pipeline of approximately 12 signed leases with limited new signings.

2025 Restaurant Development

Restaurant

Location

Opening Date

Owned Benihana

San Mateo, California

March 2025

Owned STK

Topanga, California

April 2025

Owned STK (relocation)

Los Angeles, California

May 2025

Franchised Benihana Express

Miami, Florida

June 2025

Owned STK (RA Sushi conversion)

Scottsdale, Arizona

October 2025

Sports Arena Benihana

UBS Arena in Elmont, New York

December 2025

Owned STK

Oak Brook, Illinois

December 2025

2026 Restaurant Development and Pipeline

Quarter-to-date Activity:

January 2026: Opened Company-owned Kona Grill in San Antonio, Texas (relocation)

February 2026: Converted franchised Benihana to owned in Monterey, California

Currently Under Construction (4 locations):

Owned STK in Phoenix, Arizona

Owned STK in New York, New York (relocation of an existing STK restaurant)

Owned Benihana in San Jose, California

Owned Benihana in Seattle, Washington

Asset-Light Expansion Highlights:

Ten-restaurant franchise development agreement for Benihana/Benihana Express in Greater San Francisco Bay Area, California

Accelerates West Coast expansion while maintaining capital discipline

Two-restaurant commitment for a franchised Benihana and a licensed Benihana Express in the Florida Keys

Partnership with experienced operator ensures quality execution

Liquidity

As of December 28, 2025, the Company held $24 million in cash and short-term credit card receivables and had $27 million available under our revolving credit facility, or a total of $51 million in short term liquidity. Under the current conditions, the Company’s credit facility does not have any financial covenants.

2026 Financial Targets

The Company is introducing the following financial targets, reflecting the benefits of portfolio optimization, operational improvements, and continued Benihana integration synergies.

Financial Results and Other Select DataUS$s in millions

Q1 2026 GuidanceMarch 29, 2026

2026 GuidanceDecember 27, 2026

Total GAAP revenues

$217 to $221

$840 to $855

Consolidated comparable sales

0% to 1%

1% to 3%

Managed, license and franchise fee revenues

$3.5 to $4.0

$14 to $15

Total owned operating expenses as a percentage of owned restaurant net revenue

82% to 83%

82% to 83%

Consolidated total G&A, excluding stock-based compensation

$13 to $14

Approx. $53

Consolidated Adjusted EBITDA(1)

$28 to $29

$100 to $110

Consolidated restaurant pre-opening expenses

$1 to $2

$5 to $6

Consolidated effective income tax rate

Approx. 10%

Consolidated total capital expenditures, net of allowances received by landlords

$38 to $42

Consolidated number of new system-wide venues

6 to 10 new venues

Note: As of January 1, 2025, we began reporting financial information on a fiscal quarter basis using four 13-week quarters with the addition of a 53rd week when necessary. Our fourth quarter of 2025 had 91 days. For 2026, our fiscal calendar began on December 29, 2025 and ends on December 27, 2026.

(1) We have not reconciled guidance for Consolidated Adjusted EBITDA to the corresponding GAAP financial measure because we do not provide guidance for the various reconciling items. We are unable to provide guidance for these reconciling items because we cannot determine their probable significance, as certain items are outside of our control and cannot be reasonably predicted since these items could vary significantly from period to period. Accordingly, reconciliations to the corresponding GAAP financial measure are not available without unreasonable effort.

Conference Call and Webcast

Emanuel “Manny” Hilario, President and Chief Executive Officer, and Nicole Thaung, Chief Financial Officer, will host a conference call and webcast today at 8:30 AM Eastern Time.

The conference call can be accessed live over the phone by dialing 412-542-4186. A replay will be available after the call and can be accessed by dialing 412-317-6671; the passcode is 10206228. The replay will be available until Friday, March 27, 2026.

The webcast can be accessed from the Investor Relations tab of The ONE Group’s website at www.togrp.com under “News / Events.”

About The ONE Group

The ONE Group Hospitality, Inc. (Nasdaq: STKS) is an international restaurant company that develops and operates upscale and polished casual, high-energy restaurants and lounges and provides hospitality management services for hotels, casinos and other high-end venues both in the U.S. and internationally. The ONE Group is recognized as one of “America’s Greatest Companies” (Newsweek, 2025), and Benihana is honored as one of ”America’s Best Brands for Value” (Forbes, 2025). The ONE Group’s focus is to be the global leader in Vibe Dining, and its primary restaurant brands and operations are:

STK, a modern twist on the American steakhouse concept with restaurants in major metropolitan cities in the U.S., Europe and the Middle East, featuring premium steaks, seafood and specialty cocktails in an energetic upscale atmosphere.

Benihana, an interactive dining destination with highly skilled chefs preparing food right in front of guests and served in an energetic atmosphere alongside fresh sushi and innovative cocktails. The Company franchises Benihanas in the U.S., Caribbean, Central America, and South America.

Samurai, an interactive dining experience located in sunny Miami, FL, provides a distinctive dining experience where skilled personal chefs masterfully perform the ancient art of teppanyaki right before your eyes.

Kona Grill, a polished casual, bar-centric Grill concept with restaurants in the U.S., featuring American favorites, award-winning sushi, and specialty cocktails in an upscale casual atmosphere.

Salt Water Social is your gateway to the seven seas, featuring an array of signature and unique fresh seafood items, complemented by the highest quality beef dishes and elegant, delicious cocktails.

Benihana Express, a small footprint casual concept showcasing the best of Benihana but without teppanyaki tables or bar.

RA Sushi, a Japanese cuisine concept that offers a fun-filled, bar-forward, upbeat, and vibrant dining atmosphere with restaurants in the U.S. anchored by creative sushi, inventive drinks, and outstanding service.

ONE Hospitality, The ONE Group’s food and beverage hospitality services business develops, manages and operates premier restaurants and turnkey food and beverage services within high-end hotels and casinos currently operating venues in the U.S. and Europe.

Additional information about The ONE Group can be found at www.togrp.com.

Non-GAAP Definitions

We have evolved our definition of non-GAAP financial measures starting in Q4 2025. We use certain non-GAAP measures in analyzing operating performance and believe that the presentation of these measures provides investors and analysts with information that is beneficial to gaining an understanding of the Company’s financial results. Non-GAAP disclosures should not be viewed as a substitute for financial results determined in accordance with GAAP.

We exclude items management does not consider in the evaluation of its ongoing core operating performance from Adjusted EBITDA. Starting in Q4 2025, the Adjusted EBITDA attributable to closed Grill Concepts restaurants is excluded from Adjusted EBITDA. Reconciliations of these non-GAAP measures are included under “Reconciliation of Non-GAAP Measures” in this press release.

*Comparable sales represent total U.S. food and beverage sales at owned and managed units, a non-GAAP financial measure, opened for at least a full 24-months. This measure includes total revenue from our owned and managed locations. The Company monitors sales growth at its established restaurant base in addition to growth that results from restaurant acquisitions and new restaurant openings. Refer to the reconciliation of GAAP revenue to total food and beverage sales at owned and managed units in this press release.

**We define Adjusted EBITDA as net income (loss) before interest expense, provision for income taxes, depreciation and amortization, stock-based compensation, transition and integration expenses, loss on impairment of non-current assets, lease termination and exit expenses, transaction and exit costs, loss on early debt extinguishment, non-cash rent and the Adjusted EBITDA attributable to the closed Grill Concepts restaurants. Adjusted EBITDA has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of Net income (loss) to Adjusted EBITDA in this press release.

*** We define Restaurant Operating Profit as owned restaurant net revenue minus owned restaurant cost of sales and owned restaurant operating expenses. Restaurant Operating Profit has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of operating income to Restaurant Operating Profit in this press release.

**** We define Adjusted Operating Income as operating income (loss) before transition and integration expenses, loss on impairment of non-current assets, lease termination and exit expenses and transaction and exit costs. Not all the aforementioned items defining Adjusted Operating Income occur in each reporting period but have been included in our definitions of terms based on our historical activity. Adjusted Operating Income has been presented in this press release and is a supplemental measure of financial performance that is not required by, or presented in accordance with, GAAP. Refer to the reconciliation of operating income to Adjusted Operating Income in this press release.

Cautionary Statement on Forward-Looking Statements

This press release includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995, including with respect to 2025 results, the impact of the Benihana Inc. acquisition, portfolio optimization, restaurant openings and 2026 financial targets. Forward-looking statements may be identified by the use of words such as “target,” “intend,” “anticipate,” “believe,” “expect,” “estimate,” “plan,” “outlook,” and “project” and other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. A number of factors could cause actual results or outcomes to differ materially from those indicated by such forward-looking statements, including but not limited to: (1) our ability to integrate the new or acquired restaurants into our operations without disruptions to operations; (2) our ability to capture anticipated synergies; (3) our ability to open new restaurants and food and beverage locations in current and additional markets, grow and manage growth profitably, maintain relationships with suppliers and obtain adequate supply of products and retain employees; (4) factors beyond our control that affect the number and timing of new restaurant openings, including weather conditions and factors under the control of landlords, contractors and regulatory and/or licensing authorities; (5) our ability to successfully improve performance and cost, realize the benefits of our marketing efforts and achieve improved results as we focus on developing new management and license deals; (6) changes in applicable laws or regulations; (7) the possibility that The ONE Group may be adversely affected by other economic, business, and/or competitive factors, including economic downturns; (8) the impact of actual and potential changes in immigration policies, including potential labor shortages; (9) the potential impact of the imposition of tariffs, including increases in food prices and inflation and any resulting negative impacts on the macro-economic environment; (10) risks related to our development and franchise partners; (11) risks related to geopolitical events; and (12) other risks and uncertainties indicated from time to time in our filings with the Securities and Exchange Commission, including our Annual Report on Form 10-K filed for the year ended December 31, 2024 and Quarterly Reports on Form 10-Q.

Investors are referred to the most recent reports filed with the Securities and Exchange Commission by The ONE Group Hospitality, Inc. Investors are cautioned not to place undue reliance upon any forward-looking statements, which speak only as of the date made, and we undertake no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Joint Team Continues to Progress Towards Completing an Integrated Uncrewed Collaborative Combat Aircraft (UCCA) System for the German Air Force

SAN DIEGO, March 13, 2026 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leader in defense, national security and global markets, and its partner Airbus announced today that the joint team continues to take steps towards completing an integrated Uncrewed Collaborative Combat Aircraft (UCCA) offering for the German Air Force and towards a maiden flight with a sovereign European mission system, the Multiplatform Autonomous Reconfigurable and Secure (MARS) system.

The two companies are bringing their respective industry-leading capabilities to integrate, missionize, and ultimately produce and deliver the Airbus UCCA System and are scheduled to fly later this year.

“By combining the Kratos Valkyrie with our MARS mission system, we are offering the German customer exactly what Germany and Europe urgently need in the current geopolitical situation: a proven flying uncrewed combat aircraft with a sovereign European mission system that does not have to be developed from scratch in a time-consuming and costly manner”, said Marco Gumbrecht, Head of Key Account Germany at Airbus Defence and Space. “Our objective is to deliver credible combat capability in time of relevance, while assuring key sovereign aspects. And we are confident that we can do this at a very affordable price – which is a key driver for UCCAs.”

Steve Fendley, President of Kratos Unmanned Systems Division, said, “We could not be more excited about the opportunity, the capability we’re providing, and the teaming relationship with Airbus. By taking the flight-proven and in-production Valkyrie and integrating the Airbus MARS mission system, the Airbus-missionized Valkyrie UCCA is a multi-mission, affordable system that can operate independently, in teams of UAS, or in Manned-Unmanned-Teaming operations. Along with the technical and production backing Airbus and Kratos bring, we are realizing an optimal capability system that can be bought and deployed as ‘affordable mass’; the consistent discriminator identified in today’s peer to peer wargames.”

The Kratos Valkyrie is a high-performance, runway-flexible tactical unmanned aerial vehicle capable of long-range flights at high-subsonic speeds. Combining affordability, survivability, long-range, high-subsonic speeds, maneuverability and ability to carry flexible mission kit configurations and mix of lethal weapons from its internal weapons bay and wing stations, the Valkyrie provides unmatched operational flexibility at an affordable price for both Department of War (DoW) and international customers.

With a length of 9.1 m, a wingspan of 8.2 m, range of over 5,000 kilometres, maximum take-off weight (MTOW) of around three tons, the Valkyrie can fly at an altitude of up to 45,000 feet. The maiden flight of the Valkyrie already took place in the USA in 2019; and additional aircraft have been flying regularly since that time. The maiden flight of the Airbus variant is scheduled for 2026.

Fully autonomous or commanded by a Eurofighter, the Valkyrie is designed to be able to take on sensitive mission tasks that would pose too great a danger to the pilot. The UCCA can service kinetic and non-kinetic mission sets in several roles. For the German customer, Airbus and Kratos are initially focusing on a specific role to deliver credible combat air power on time and on target.

In Manching, Germany, Airbus is currently preparing two Kratos Valkyries for their first flight with its European mission system.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a technology, products, system and software company addressing the defense, national security, and commercial markets. Kratos makes true internally funded research, development, capital and other investments, to rapidly develop, produce and field solutions that address our customers’ mission critical needs and requirements. At Kratos, affordability is a technology, and we seek to utilize proven, leading edge approaches and technology, not unproven bleeding edge approaches or technology, with Kratos’ approach designed to reduce cost, schedule and risk, enabling us to be first to market with cost effective solutions. We believe that Kratos is known as an innovative disruptive change agent in the industry, a company that is an expert in designing products and systems up front for successful rapid, large quantity, low-cost future manufacturing which is a value add competitive differentiator for our large traditional prime system integrator partners and also to our government and commercial customers. Kratos intends to pursue program and contract opportunities as the prime or lead contractor when we believe that our probability of win (PWin) is high and any investment required by Kratos is within our capital resource comfort level. We intend to partner and team with a large, traditional system integrator when our assessment of PWin is greater or required investment is beyond Kratos’ comfort level. Kratos’ primary business areas include virtualized ground systems for satellites and space vehicles including software for command & control (C2) and telemetry, tracking and control (TT&C), jet powered unmanned aerial drone systems, advanced vehicles and rocket systems, propulsion systems for drones, missiles, loitering munitions, supersonic systems, space craft and launch systems, C5ISR and microwave electronic products for missile, radar, missile defense, space, satellite, counter UAS, directed energy, communication and other systems, and virtual & augmented reality training systems for the warfighter. For more information, visit www.KratosDefense.com.

Notice Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are made on the basis of the current beliefs, expectations and assumptions of the management of Kratos and are subject to significant risks and uncertainty. Investors are cautioned not to place undue reliance on any such forward-looking statements. All such forward-looking statements speak only as of the date they are made, and Kratos undertakes no obligation to update or revise these statements, whether as a result of new information, future events or otherwise. Although Kratos believes that the expectations reflected in these forward-looking statements are reasonable, these statements involve many risks and uncertainties that may cause actual results to differ materially from what may be expressed or implied in these forward-looking statements. For a further discussion of risks and uncertainties that could cause actual results to differ from those expressed in these forward-looking statements, as well as risks relating to the business of Kratos in general, see the risk disclosures in the Annual Report on Form 10-K of Kratos for the year ended December 28, 2025, and in subsequent reports on Forms 10-Q and 8-K and other filings made with the SEC by Kratos.

NEW YORK–(BUSINESS WIRE)– Perfect Corp. (NYSE: PERF) (“Perfect” or the “Company”), a global leader in providing augmented reality (“AR”) and artificial intelligence (“AI”) Software-as-a-Service (“SaaS”) solutions to beauty and fashion industries, today announced that it filed its annual report on Form 20-F for the fiscal year ended December 31, 2025. The annual report can be accessed under the SEC Filing section on the Company’s investor relations website at https://ir.perfectcorp.com.

The Company will provide a hard copy of its annual report containing the audited consolidated financial statements, free of charge, to its shareholders upon request. Requests should be directed to 14F, No. 98 Minquan Road, Xindian District, New Taipei City 231, Taiwan, or via email at Investor_Relations@PerfectCorp.com.

About Perfect Corp.

Perfect Corp. (NYSE: PERF) leverages ‘Beautiful AI’ innovations to make our world more beautiful. As a pioneer and leader in the space, Perfect Corp. works with over 650 partners around the globe to empower brands to embrace the digital-first world by transforming shopping journeys through digital tech innovations. Perfect Corp.’s suite of enterprise solutions delivers synergistic, technology-driven experiences that facilitate sustainable, ultra-personalized, and engaging shopping journeys through hyper-realistic virtual try-ons, AI-powered skin analyses, personalized product recommendation tools and many more Beautiful AI innovations. For more information, visit https://ir.perfectcorp.com.

TONMYA™ (cyclobenzaprine HCl sublingual tablets) launched November 17, 2025, for the treatment of fibromyalgia; through February 27, 2026, more than 1,500 healthcare providers have prescribed TONMYA to patients, approximately 2,500 patients have initiated treatment with TONMYA, and cumulative prescriptions totaled approximately 4,200

Expect to initiate U.S. field study in 2027 for TNX-4800 for seasonal prevention of Lyme disease pending FDA clearance

Completed $20.0 million registered direct offering with Point72 on December 29, 2025

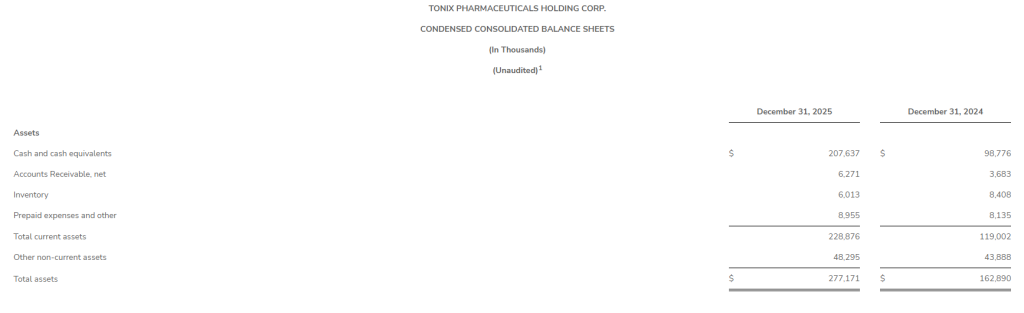

Approximately $207.6 million in cash and cash equivalents as of December 31, 2025

BERKELEY HEIGHTS, N.J., March 12, 2026 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (“Tonix” or the “Company”), a fully integrated, commercial biotechnology company, today announced financial results for the fourth quarter and full year ended December 31, 2025, and provided an overview of recent operational highlights.

“2025 was transformational for Tonix as we achieved FDA approval and began the U.S. commercial launch of TONMYA, our first fully in-house developed product and the first new medicine approved for fibromyalgia in more than 15 years,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “TONMYA is a non-opioid analgesic designed for long-term, once-daily bedtime dosing. We believe TONMYA now provides an alternative medicine for the approximately 10 million adults in the U.S. who suffer from fibromyalgia. We have the capabilities to engage healthcare providers and patients, having launched the product and an approximately 90-member salesforce. Early prescription trends reflect favorable prescriber uptake and repeat utilization consistent with our internal launch expectations. Our experienced commercial team is committed to growing awareness and adoption, facilitating patient access, and obtaining payer coverage as we strive to improve the fibromyalgia journey for patients and healthcare providers.”

Dr. Lederman continued, “We also meaningfully advanced our robust clinical pipeline in 2025. Tonix in-licensed TNX-4800, a long-acting human monoclonal antibody for the seasonal prevention of Lyme disease, for which there are no FDA-approved vaccines or prophylactics. This program, developed by researchers at UMass Chan Medical School, anchors our clinical-stage infectious disease pipeline, and we plan to discuss Phase 2/3 development with the FDA this year. An additional highlight includes FDA clearance of the Investigational New Drug application (IND) for HORIZON, a potentially pivotal Phase 2 study of TNX-102 SL (cyclobenzaprine HCl sublingual tablets) in major depressive disorder, which is expected to initiate enrollment in mid-2026. Looking ahead, our priorities are clear. We are driven to continue our momentum in 2026 as we focus on the successful commercialization of TONMYA, pipeline progress, and sustainable long-term value for patients and shareholders.”

Commercial Updates

TONMYA (cyclobenzaprine HCl sublingual tablets): a centrally acting, non-opioid analgesic for the treatment of fibromyalgia in adults

In August 2025, the U.S. FDA approved TONMYA for the treatment of fibromyalgia in adults, making it the first new prescription medicine approved for this indication in more than 15 years. The approval was based on two double-blind, randomized, placebo-controlled Phase 3 clinical trials of nearly 1,000 patients that demonstrated statistically significant reduction in daily pain scores compared to placebo.

On November 17, 2025, TONMYA became commercially available at pharmacies by prescription in the U.S. Approximately 90 sales representatives were deployed in the field in advance of the launch. Early prescription trends reflect favorable adoption rates by prescribers and patients, with prescription volumes increasing each full month post launch. Launch metrics for the period November 17, 2025–February 27, 2026 (launch-to-date), are as follows:

More than 1,500 healthcare providers have prescribed TONMYA to patients.

Approximately 2,500 patients have initiated treatment with TONMYA.

Cumulative prescriptions totaled approximately 4,200. This includes bridge prescriptions that are facilitated through the Company’s specialty pharmacy channel. Bridge prescriptions represent initial patient fills provided while coverage determinations are pending and do not immediately generate net product revenue.

The Company has contracted with existing wholesalers and specialty pharmacies for distribution and with companies to assist with prescription fulfillment and patient access. Tonix also has a robust patient access program and support services in place, including TONMYA savings card, copay assistance, and prior authorization support, intended to reduce access barriers during early commercialization.

The Company is prioritizing expanding payer engagement and establishing contracts with commercial payers, while also progressing discussions with Medicare and Medicaid.

Infectious Disease Pipeline TNX-4800 (anti-OspA mAb): long-acting human monoclonal antibody in development for the seasonal prevention of Lyme disease, which has no FDA-approved vaccines or prophylactics

In December 2025, Tonix announced plans to meet with the FDA in 2026 to explore Phase 2/3 development options, including a Phase 2 field study and a Phase 2 controlled human infection model (CHIM) study, which is also called a human challenge study. The Company expects to have GMP investigational product available for clinical testing in early 2027. Pending FDA clearances, the field study is expected to initiate enrollment in 2027 and the CHIM study in 2028.

Central Nervous System (CNS) Pipeline TNX-102 SL (cyclobenzaprine HCl sublingual tablets): in development for major depressive disorder (MDD)

In November 2025, the FDA cleared the IND for TNX-102 SL 5.6 mg for the treatment of MDD in adults. The IND clearance enables Tonix to proceed with the HORIZON study, a potentially pivotal Phase 2, 6-week, randomized, double-blind, placebo-controlled study of TNX-102 SL as a first-line monotherapy in adults with MDD. About 360 patients will be enrolled at approximately 30 U.S. sites, with the primary endpoint being the MADRS total score change from baseline at Week 6. Tonix plans to initiate enrollment in mid-2026.

Prior studies of TNX-102 SL in fibromyalgia and post-traumatic stress disorder (PTSD) showed promising signals for improvement of depressive symptoms. TNX-102 SL treatment has been associated with a low incidence of side effects common with traditional antidepressants, including weight gain, blood pressure changes, sexual dysfunction, and cognitive issues.

TNX-102 SL for the treatment of acute stress reaction (ASR) and acute stress disorder (ASD), and prophylaxis against development of PTSD

The U.S. Department of Defense-funded Optimizing Acute Stress Reaction Interventions (OASIS) trial is being conducted by the University of North Carolina under an investigator-initiated IND application. The OASIS trial examines the safety and efficacy of TNX-102 SL to reduce adverse posttraumatic neuropsychiatric sequelae among patients in the emergency department after a motor vehicle collision. Topline data is expected to be reported in the second half of 2026.

Immunology Pipeline TNX-1500 (dimeric Fc modified anti-CD40L, humanized monoclonal antibody): third generation anti-CD40L for prophylaxis of kidney transplant rejection and treatment of autoimmune disorders

In November 2025, Tonix announced a collaboration with Massachusetts General Hospital to advance a Phase 2 open-label, investigator-initiated clinical trial of TNX-1500 in kidney transplant recipients, planned for initiation mid-year 2026 pending FDA clearance of the IND. The study is expected to enroll five adult kidney transplant recipients.

In October 2025, Tonix presented an update at the Japan Society for Transplantation annual congress, highlighting Phase 1 safety and pharmacokinetic and pharmacodynamic results and outlining next steps toward Phase 2 evaluation in allogenic kidney transplantation.

Rare Disease Pipeline TNX-2900 (intranasal potentiated oxytocin): in development for Prader-Willi syndrome, with Orphan Drug designation as well as Rare Pediatric Disease designation that could make Tonix eligible for a Priority Review Voucher upon approval

In September 2025, Tonix announced plans to initiate a Phase 2, randomized, double-blind, placebo-controlled trial in children and adolescents with Prader-Willi syndrome. The study is expected to initiate in the first quarter of 2027.

Financial: Recent Highlights

Tonix had approximately $207.6 million of cash and cash equivalents as of December 31, 2025, compared to approximately $98.8 million as of December 31, 2024. Net cash used in operations was approximately $99.8 million for the full year ended December 31, 2025, compared to $60.9 million for the same period in 2024. Cash paid for capital expenditures for the full year ended December 31, 2025, were approximately $3.4 million compared to $0.1 million for the same period in 2024.

In December 2025, Tonix completed a $20.0 million registered direct offering with Point72 Asset Management. The net proceeds are being used to fund commercialization of marketed products, pipeline development, and general working capital. TD Cowen acted as sole placement agent for the offering. A.G.P./Alliance Global Partners acted as a financial advisor.

Subsequent to year-end, the Company has raised $8.6 million proceeds using its at-the-market (ATM) facility.

The Company believes that its cash resources at December 31, 2025, will meet its planned operating and capital expenditure requirements into the first quarter of 2027.

As of March 11, 2026, the Company had 13,405,401 shares of common stock outstanding.

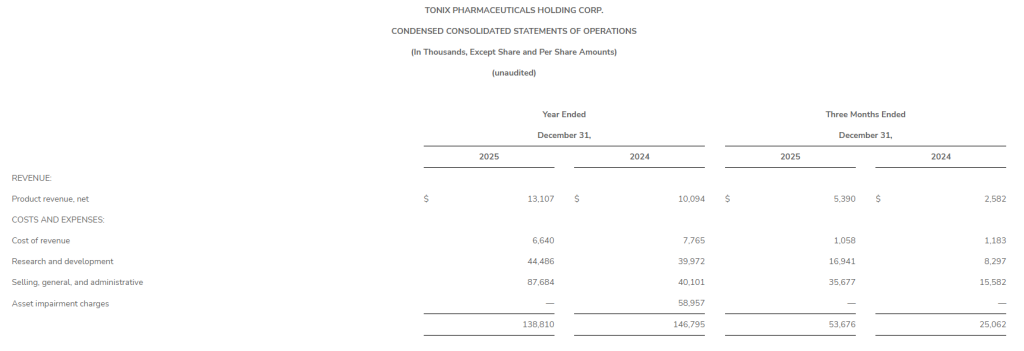

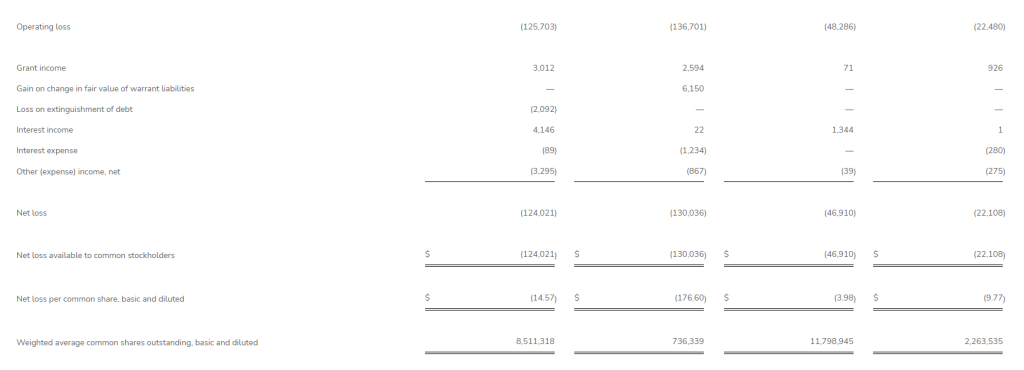

Full Year 2025 Financial Results

Net product revenue for the full year 2025 was approximately $13.1 million, compared to $10.1 million in 2024. Net revenue from sales of Zembrace®, SymTouch®, and Tosymra® for the full year 2025 was approximately $11.7 million, compared to $10.1 million in 2024. Net revenue from sales of TONMYA for the period from launch on November 17, 2025, to December 31, 2025, was approximately $1.4 million. Cost of sales for the full year 2025 was approximately $6.6 million, compared to $7.8 million in 2024.

Research and development expenses for the full year 2025 were approximately $44.5 million, compared to $40.0 million in 2024. This increase is predominately due to pipeline prioritization period over period, and increased headcount.

Selling, general, and administrative expenses for the full year 2025 were $87.7 million, compared to $40.1 million in 2024. The increase is predominately due to spending on sales and marketing related to TONMYA as well as increased headcount.

Net loss available to common stockholders was approximately $124.0 million, or $14.57 per basic and diluted share, for the full year 2025, compared to net loss available to common stockholders of $130.0 million, or $176.60 per basic and diluted share, in 2024. The basic and diluted weighted average common shares outstanding for the full year 2025 was 8,511,318 compared to 736,339 shares for 2024.

Fourth Quarter 2025 Financial Results

Net product revenue for the fourth quarter 2025 was approximately $5.4 million, compared to $2.6 million for the same period in 2024, and consisted of combined net sales of TONMYA™, Zembrace® SymTouch®, and Tosymra®. Cost of sales for the fourth quarter 2025 was approximately $1.1 million, compared to $1.2 million for the same period in 2024.

Research and development expenses for the fourth quarter 2025 were approximately $16.9 million, compared to $8.3 million for the same period in 2024. This increase is predominately due to pipeline prioritization period over period and increased headcount.

Selling, general, and administrative expenses for the fourth quarter 2025 were $35.7 million, compared to $15.6 million for the same period in 2024. The increase is predominately due to spending on sales and marketing related to TONMYA and increased headcount.

Net loss available to common stockholders was $46.9 million, or $3.98 per basic and diluted share, for the fourth quarter 2025, compared to net loss available to common stockholders of $22.1 million, or $9.77 per basic and diluted share, for the same period in 2024. The basic and diluted weighted average common shares outstanding for the fourth quarter 2025 was 11,798,945 compared to 2,263,535 shares for the same period in 2024.

Tonix Pharmaceuticals Holding Corp. Tonix Pharmaceuticals* is a fully-integrated, commercial-stage biotechnology company focused on central nervous system (CNS) and immunology treatments in areas of high unmet medical need. TONMYATM (cyclobenzaprine HCl sublingual tablets 2.8mg), the Company’s recently approved flagship medicine, is the first new treatment for fibromyalgia in more than 15 years. Tonix’s CNS commercial infrastructure supports its marketed products, including its acute migraine products, Zembrace® SymTouch® and Tosymra®. Tonix is maximizing the science behind TONMYA in Phase 2 clinical trials to evaluate its potential in major depressive disorder and acute stress disorder. In addition, the Company’s CNS portfolio includes TNX-2900, which is Phase 2 ready for the treatment of Prader-Willi syndrome, a rare disease. Tonix is also advancing a pipeline of immunology programs, including monoclonal antibody TNX-4800 for Lyme disease prophylaxis and TNX-1500, a third-generation CD40 ligand inhibitor for the prevention of kidney transplant rejection. To learn more, visit www.tonixpharma.com and follow the Company on LinkedIn and X.

*Tonix’s product development candidates are investigational new drugs or biologics; their efficacy and safety have not been established and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. TONMYA is a trademark of Tonix Pharma Limited. All other marks are property of their respective owners.

Forward Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995 including those relating to the completion of the offering, the satisfaction of customary closing conditions, the intended use of proceeds from the offering and other statements that are predictive in nature. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially as a result of a number of factors, including the ability of the Company to satisfy the conditions to the closing of the offering and the timing thereof, as well as those described in the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on March 12, 2026, and periodic reports filed with the SEC on or after the date thereof. Tonix does not undertake an obligation to update or revise any forward-looking statement. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

INDICATION TONMYA is indicated for the treatment of fibromyalgia in adults.

CONTRAINDICATIONS TONMYA is contraindicated: In patients with hypersensitivity to cyclobenzaprine or any inactive ingredient in TONMYA. Hypersensitivity reactions may manifest as an anaphylactic reaction, urticaria, facial and/or tongue swelling, or pruritus. Discontinue TONMYA if a hypersensitivity reaction is suspected. With concomitant use of monoamine oxidase (MAO) inhibitors or within 14 days after discontinuation of an MAO inhibitor. Hyperpyretic crisis seizures and deaths have occurred in patients who received cyclobenzaprine (or structurally similar tricyclic antidepressants) concomitantly with MAO inhibitors drugs. During the acute recovery phase of myocardial infarction, and in patients with arrhythmias, heart block or conduction disturbances, or congestive heart failure. In patients with hyperthyroidism.

WARNINGS AND PRECAUTIONS Embryofetal toxicity: Based on animal data, TONMYA may cause neural tube defects when used two weeks prior to conception and during the first trimester of pregnancy. Advise females of reproductive potential of the potential risk and to use effective contraception during treatment and for two weeks after the final dose. Perform a pregnancy test prior to initiation of treatment with TONMYA to exclude use of TONMYA during the first trimester of pregnancy.

Serotonin syndrome: Concomitant use of TONMYA with selective serotonin reuptake inhibitors (SSRIs), serotonin norepinephrine reuptake inhibitors (SNRIs), tricyclic antidepressants, tramadol, bupropion, meperidine, verapamil, or MAO inhibitors increases the risk of serotonin syndrome, a potentially life-threatening condition. Serotonin syndrome symptoms may include mental status changes, autonomic instability, neuromuscular abnormalities, and/or gastrointestinal symptoms. Treatment with TONMYA and any concomitant serotonergic agent should be discontinued immediately if serotonin syndrome symptoms occur and supportive symptomatic treatment should be initiated. If concomitant treatment with TONMYA and other serotonergic drugs is clinically warranted, careful observation is advised, particularly during treatment initiation or dosage increases.

Tricyclic antidepressant-like adverse reactions: Cyclobenzaprine is structurally related to TCAs. TCAs have been reported to produce arrhythmias, sinus tachycardia, prolongation of the conduction time leading to myocardial infarction and stroke. If clinically significant central nervous system (CNS) symptoms develop, consider discontinuation of TONMYA. Caution should be used when TCAs are given to patients with a history of seizure disorder, because TCAs may lower the seizure threshold. Patients with a history of seizures should be monitored during TCA use to identify recurrence of seizures or an increase in the frequency of seizures.

Atropine-like effects: Use with caution in patients with a history of urinary retention, angle-closure glaucoma, increased intraocular pressure, and in patients taking anticholinergic drugs.

CNS depression and risk of operating a motor vehicle or hazardous machinery: TONMYA monotherapy may cause CNS depression. Concomitant use of TONMYA with alcohol, barbiturates, or other CNS depressants may increase the risk of CNS depression. Advise patients not to operate a motor vehicle or dangerous machinery until they are reasonably certain that TONMYA therapy will not adversely affect their ability to engage in such activities. Oral mucosal adverse reactions: In clinical studies with TONMYA, oral mucosal adverse reactions occurred more frequently in patients treated with TONMYA compared to placebo. Advise patients to moisten the mouth with sips of water before administration of TONMYA to reduce the risk of oral sensory changes (hypoesthesia). Consider discontinuation of TONMYA if severe reactions occur.

ADVERSE REACTIONS The most common adverse reactions (incidence ≥2% and at a higher incidence in TONMYA-treated patients compared to placebo-treated patients) were oral hypoesthesia, oral discomfort, abnormal product taste, somnolence, oral paresthesia, oral pain, fatigue, dry mouth, and aphthous ulcer.

DRUG INTERACTIONS MAO inhibitors: Life-threatening interactions may occur.

Other serotonergic drugs: Serotonin syndrome has been reported.

CNS depressants: CNS depressant effects of alcohol, barbiturates, and other CNS depressants may be enhanced.

Tramadol: Seizure risk may be enhanced. Guanethidine or other similar acting drugs: The antihypertensive action of these drugs may be blocked.

USE IN SPECIFIC POPULATIONS Pregnancy: Based on animal data, TONMYA may cause fetal harm when administered to a pregnant woman. The limited amount of available observational data on oral cyclobenzaprine use in pregnancy is of insufficient quality to inform a TONMYA-associated risk of major birth defects, miscarriage, or adverse maternal or fetal outcomes. Advise pregnant women about the potential risk to the fetus with maternal exposure to TONMYA and to avoid use of TONMYA two weeks prior to conception and through the first trimester of pregnancy. Report pregnancies to the Tonix Medicines, Inc., adverse-event reporting line at 1-888-869-7633 (1-888-TNXPMED).

Lactation: A small number of published cases report the transfer of cyclobenzaprine into human milk in low amounts, but these data cannot be confirmed. There are no data on the effects of cyclobenzaprine on a breastfed infant, or the effects on milk production. The developmental and health benefits of breastfeeding should be considered along with the mother’s clinical need for TONMYA and any potential adverse effects on the breastfed child from TONMYA or from the underlying maternal condition.

Pediatric use: The safety and effectiveness of TONMYA have not been established.

Geriatric patients: Of the total number of TONMYA-treated patients in the clinical trials in adult patients with fibromyalgia, none were 65 years of age and older. Clinical trials of TONMYA did not include sufficient numbers of patients 65 years of age and older to determine whether they respond differently from younger adult patients.

Hepatic impairment: The recommended dosage of TONMYA in patients with mild hepatic impairment (HI) (Child Pugh A) is 2.8 mg once daily at bedtime, lower than the recommended dosage in patients with normal hepatic function. The use of TONMYA is not recommended in patients with moderate HI (Child Pugh B) or severe HI (Child Pugh C). Cyclobenzaprine exposure (AUC) was increased in patients with mild HI and moderate HI compared to subjects with normal hepatic function, which may increase the risk of TONMYA-associated adverse reactions.

Please see additional safety information in the full Prescribing Information. To report suspected adverse reactions, contact Tonix Medicines, Inc. at 1-888-869-7633, or the FDA at 1-800-FDA-1088 or www.fda.gov/medwatch.

Indication and Usage Zembrace® SymTouch® (sumatriptan succinate) injection (Zembrace) and Tosymra® (sumatriptan) nasal spray are prescription medicines used to treat acute migraine headaches with or without aura in adults who have been diagnosed with migraine.

Zembrace and Tosymra are not used to prevent migraines. It is not known if Zembrace or Tosymra are safe and effective in children under 18 years of age.

Important Safety Information Zembrace and Tosymra can cause serious side effects, including heart attack and other heart problems, which may lead to death. Stop use and get emergency help if you have any signs of a heart attack:

discomfort in the center of your chest that lasts for more than a few minutes or goes away and comes back

severe tightness, pain, pressure, or heaviness in your chest, throat, neck, or jaw

pain or discomfort in your arms, back, neck, jaw or stomach

shortness of breath with or without chest discomfort

breaking out in a cold sweat

nausea or vomiting

feeling lightheaded

Zembrace and Tosymra are not for people with risk factors for heart disease (high blood pressure or cholesterol, smoking, overweight, diabetes, family history of heart disease) unless a heart exam shows no problem.

Do not use Zembrace or Tosymra if you have:

history of heart problems

narrowing of blood vessels to your legs, arms, stomach, or kidney (peripheral vascular disease)

uncontrolled high blood pressure

hemiplegic or basilar migraines. If you are not sure if you have these, ask your provider.

had a stroke, transient ischemic attacks (TIAs), or problems with blood circulation

severe liver problems

taken any of the following medicines in the last 24 hours: almotriptan, eletriptan, frovatriptan, naratriptan, rizatriptan, ergotamines, or dihydroergotamine. Ask your provider for a list of these medicines if you are not sure.

are taking certain antidepressants, known as monoamine oxidase (MAO)-A inhibitors or it has been 2 weeks or less since you stopped taking a MAO-A inhibitor. Ask your provider for a list of these medicines if you are not sure.

an allergy to sumatriptan or any of the components of Zembrace or Tosymra

Tell your provider about all of your medical conditions and medicines you take, including vitamins and supplements.

Zembrace and Tosymra can cause dizziness, weakness, or drowsiness. If so, do not drive a car, use machinery, or do anything where you need to be alert.

Zembrace and Tosymra may cause serious side effects including:

changes in color or sensation in your fingers and toes

sudden or severe stomach pain, stomach pain after meals, weight loss, nausea or vomiting, constipation or diarrhea, bloody diarrhea, fever

cramping and pain in your legs or hips; feeling of heaviness or tightness in your leg muscles; burning or aching pain in your feet or toes while resting; numbness, tingling, or weakness in your legs; cold feeling or color changes in one or both legs or feet

increased blood pressure including a sudden severe increase even if you have no history of high blood pressure

medication overuse headaches from using migraine medicine for 10 or more days each month. If your headaches get worse, call your provider.

serotonin syndrome, a rare but serious problem that can happen in people using Zembrace or Tosymra, especially when used with anti-depressant medicines called SSRIs or SNRIs. Call your provider right away if you have: mental changes such as seeing things that are not there (hallucinations), agitation, or coma; fast heartbeat; changes in blood pressure; high body temperature; tight muscles; or trouble walking.

hives (itchy bumps); swelling of your tongue, mouth, or throat

seizures even in people who have never had seizures before

The most common side effects of Zembrace and Tosymra include: pain and redness at injection site (Zembrace only); tingling or numbness in your fingers or toes; dizziness; warm, hot, burning feeling to your face (flushing); discomfort or stiffness in your neck; feeling weak, drowsy, or tired; application site (nasal) reactions (Tosymra only) and throat irritation (Tosymra only).

Tell your provider if you have any side effect that bothers you or does not go away. These are not all the possible side effects of Zembrace and Tosymra. For more information, ask your provider.

This is the most important information to know about Zembrace and Tosymra but is not comprehensive. For more information, talk to your provider and read the Patient Information and Instructions for Use. You can also visit https://www.tonixpharma.com or call 1-888-869-7633.

You are encouraged to report adverse effects of prescription drugs to the FDA. Visit www.fda.gov/medwatch, or call 1-800-FDA-1088.

The S&P 500 is closing out its third consecutive losing week — the longest such streak in nearly a year — and the forces behind the selloff are not the kind that resolve quickly. A geopolitical shock, deteriorating economic data, and a Federal Reserve with no room to maneuver have converged into a triple threat that is reshaping how investors should be positioning right now.

The index hit an all-time high of 7,002 on January 27, 2026. It has since fallen approximately 4.5%, trading near 6,684 as of Thursday’s close — its lowest level since mid-December. The Dow Jones Industrial Average is tracking for a 1.8% weekly loss, and the Nasdaq Composite has declined roughly 0.9% week-to-date. The S&P 500 is now down 1.54% on the year.

Threat #1: Iran and the Oil Shock

The U.S.-Israeli military conflict with Iran has disrupted Persian Gulf shipping lanes, sending Brent crude above $100 per barrel for the first time since August 2022 and pushing WTI crude near $96. With Iran’s new Supreme Leader signaling the Strait of Hormuz closure should continue as leverage against the West, there is no near-term resolution in sight. Energy costs at these levels feed directly into consumer prices, complicating an inflation fight the Fed had not yet won.

Threat #2: Stagflation Is No Longer a Tail Risk

This morning’s Q4 2025 GDP revision delivered a gut punch to the soft-landing narrative. Economic growth came in at just 0.7% annualized — down sharply from the prior estimate of 1.4% and well below the consensus forecast of 1.5%. That is the weakest quarterly growth reading in years, outside of the pandemic. Meanwhile, core PCE rose 0.4% month-over-month and February CPI held at 2.4% year-over-year. Slow growth paired with rising prices is the textbook definition of stagflation — historically one of the most punishing environments for equity markets. The 1973 OPEC oil crisis offers an uncomfortable parallel, when the S&P 500 fell more than 40% as recession and energy shock collided.

Threat #3: The Fed Has No Good Options

The Federal Open Market Committee meets March 17–18, and futures markets are pricing in just a 4.7% probability of a rate cut, according to CME FedWatch data. The Fed cannot cut into rising inflation driven by an oil shock, and it cannot hike into slowing growth. The result is policy paralysis — and markets hate uncertainty more than bad news. Rate-sensitive equities, particularly high-multiple tech names, are absorbing the most damage.

What the Headline Number Isn’t Telling You

While the cap-weighted S&P 500 is down 1.54% year-to-date, the S&P 500 Equal Weight Index is up 3.16% over the same period. That divergence reveals the selloff for what it is — a concentrated repricing of mega-cap technology, not a broad market collapse. The Russell 2000 small cap index outperformed Thursday, climbing over 1% on a day the Nasdaq posted losses. Energy, defense, financials, and domestically focused small cap names are holding ground while Big Tech reprices.

The macro environment is undeniably difficult. But for investors willing to look past the headline index, the rotation already underway may prove to be one of 2026’s most important opportunities.

TOI is an oncology practice management company that provides administrative services to oncology clinics. These clinics provide cancer care to a population of approximately 1.9 million patients. Services include cancer care, pharmacy and dispensary services, clinical trials, and services associated with oncology care. The company employs nearly 120 clinicians and over 700 teammates at over 70 clinic locations.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q25 Had Strong Revenue Growth. The Oncology Institute reported a 4Q25 loss of $7.5 million or $(0.06) per share and a FY2026 loss of $60.6 million or $(0.54) per share. Importantly, 4Q25 Revenues of $142.0 million were up 41.6% over 4Q24, close to our estimate of $142.4 million, with a slightly different mix from Patient Services and Dispensary Revenues. EBITDA in 4Q25 was $0.15 million, turning positive for the first time, and compares with $(7.8) million in 4Q24. Cash balance on December 31, 2025 was $33.6 million.

Margins Improved During 4Q and For FY2025. Overall Gross Margin for 4Q2025 improved to 16.0% of revenues compared with 14.6% in 4Q2024. This reflects margins improvements in Patient Services of 11.9% compared with 8.9% in 4Q24, and Dispensary margins of 18.1% compared with 16.9% in 4Q24. FY2025 Overall Gross Margin was 15.2% compared with 13.7% for FY2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Fourth quarter and FY2025 financial results. Summit will report operating and financial results after the market close on Monday, March 16. Management will host a teleconference at 10 am ET on Tuesday, March 17. We anticipate management will provide its outlook and corporate guidance for 2026.

Noble estimates. We forecasted fourth quarter and FY2025 EBITDA of $62.5 million and $246.6 million, respectively, and net losses of $0.4 million, or $(0.00) per share, and $11.5 million, or $(0.95) per share. Our fourth quarter and full year revenue estimates are $146.7 million and $566.5 million, respectively. Recall management previously communicated that it expected adjusted EBITDA to be at the low end of its $245 million to $280 million 2025 guidance range. For 2026, we are projecting revenue, EBITDA, net income and EPS of $591.3 million, $265.7 million, $12.7 million, and $1.03, respectively.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Seanergy Maritime Holdings Corp. is a prominent pure-play Capesize shipping company listed in the U.S. capital markets. Seanergy provides marine dry bulk transportation services through a modern fleet of Capesize vessels. The Company’s operating fleet consists of 18 vessels (1 Newcastlemax and 17 Capesize) with an average age of approximately 13.4 years and an aggregate cargo carrying capacity of approximately 3,236,212 dwt. Upon completion of the delivery of the previously announced Capesize vessel acquisition, the Company’s operating fleet will consist of 19 vessels (1 Newcastlemax and 18 Capesize) with an aggregate cargo carrying capacity of approximately 3,417,608 dwt. The Company is incorporated in the Marshall Islands and has executive offices in Glyfada, Greece. The Company’s common shares trade on the Nasdaq Capital Market under the symbol “SHIP”.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Newbuild program expands to five vessels. Seanergy announced the acquisition of two Japanese newbuild scrubber-fitted 181,500 dwt Capesize vessels, expanding the total newbuild program to five vessels, including four Capesize vessels and one Newcastlemax, with a combined contract value of approximately $384 million. The first Japanese vessel is a direct purchase with delivery expected between Q2 and Q3 2027, while the second is structured as a 10-year bareboat-in contract with a Q1 2029 delivery and a purchase option beginning at year five. The combined cost of both Japanese vessels is approximately $158 million.

Sale of M/V Squireship. Seanergyagreed to sell the 2010-built, 170,018 dwt M/V Squireship to a related party for $29.5 million with delivery expected between late April and early June 2026. The transaction is expected to generate net proceeds of approximately $13.5 million after debt repayment and produce an accounting gain of roughly $4 million. The sale is consistent with management’s capital recycling strategy, monetizing an older vessel at an attractive valuation while funding the newbuilding program and reducing average fleet age.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Saga Communications, Inc. is a broadcast company whose business is primarily devoted to acquiring, developing and operating radio stations. Saga currently owns or operates broadcast properties in 27 markets, including 79 FM and 33 AM radio stations. Saga’s strategy is to operate top billing radio stations in mid sized markets, defined as markets ranked (by market revenues) from 20 to 200. Saga’s radio stations employ a myriad of programming formats, including Active Rock, Adult Album Alternative, Adult Contemporary, Country, Classic Country, Classic Hits, Classic Rock, Contemporary Hits Radio, News/Talk, Oldies and Urban Contemporary. In operating its stations, Saga concentrates on the development of strong decentralized local management, which is responsible for the day-to-day operations of the stations in their market area and is compensated based on their financial performance as well as other performance factors that are deemed to effect the long-term ability of the stations to achieve financial objectives. Saga began operations in 1986 and became a publicly traded company in December 1992. The stock trades on NASDAQ under the ticker symbol “SGA”.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 Results. The company reported Q4 revenue and adj. EBITDA of $26.5 million and $0.8 million, respectively, modestly below our estimates of $27.7 million and $2.0 million, as illustrated in Figure #1 Q4 Results. Results were impacted by softness in traditional broadcast revenue, while digital Interactive revenue remained a bright spot, increasing 25.8% y-o-y.

Strong digital results. The company continued to implement its blended digital-radio strategy, integrating broadcast and digital solutions to enhance advertiser engagement and retention. Total Interactive revenue reached $4.3 million, an increase of 25.8% year over year, with full year growth reaching 19.1%. Furthermore, the growth was driven by several verticals, including search advertising, targeted display, and e-commerce platforms, reflecting growing adoption of integrated radio and digital advertising campaigns.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

4Q25 Revenues Showed Modest Increase. Gyre reported a 4Q loss of $1.7 million or $(0.02) per share and profit of $5.0 million or $0.06 per basic share and $0.02 per fully diluted share. Revenues of $116.6 million increased 10.2% over the $105.8 million in FY2024. These results are consistent with our view that FY2026 is a transition year, as the company focuses on approval and launch of Hydronidone plus the acquisition of Cullgen, Inc, adding its degrading protein technology platform (discussed in our Research Note on March 3).

Product Sales and Financials. FY2025 revenue of $116.6 million was driven by continued sales of Etuary and new product launches. Etuary sales of $106.1 million for FY2026 compare with $105.0 million in 4Q25. During the year, Gyre launched Contiva (avatrombopag maleate tablet) in March 2025 and Etorel (nintedanib ethanesulfonate capsules) in June 2025. Contiva sales were $5.5 million and Etorel sales were $4.6 million for the full year. The company expects the National Drug Procurement Program in China and market conditions to lower sales of $100.5 million to $111.0 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

In the most significant emergency energy intervention since the IEA was founded in 1974, the world’s wealthiest nations just deployed their biggest weapon against soaring oil prices — and crude kept climbing anyway. For investors tracking energy markets and small cap stocks in 2026, the implications are impossible to ignore.

On Wednesday, the International Energy Agency announced that all 32 of its member countries unanimously agreed to release 400 million barrels of oil from emergency reserves, the largest coordinated strategic petroleum reserve release in history. The move more than doubles the 182 million barrels deployed in 2022 following Russia’s invasion of Ukraine. The United States committed 172 million barrels from its Strategic Petroleum Reserve alone. Oil prices briefly dipped — then climbed straight back above $90 a barrel before the day was out.

Why the IEA’s Record Oil Reserve Release Failed to Move Markets

The math exposes the problem quickly. Macquarie analysts estimated the 400 million barrel release equates to roughly four days of global oil production and about 16 days of the volume that normally transits through the Strait of Hormuz. As the analysts noted — if that doesn’t sound like much, it isn’t.

Export volumes through the Strait of Hormuz are currently at less than 10% of pre-conflict levels, as shippers continue to avoid the waterway amid active threats and confirmed vessel attacks. The reserve release addresses the symptom. The Strait of Hormuz closure is the disease — and no amount of barrels from emergency stockpiles fixes a shipping lane that remains effectively shut.

There is also a delivery gap that markets priced in immediately. Once a presidential order is issued to deploy oil from the U.S. Strategic Petroleum Reserve, deliveries typically don’t begin for about 13 days, with additional shipping time before volumes reach end consumers. The supply disruption is happening in real time. The relief is weeks away at best. JPMorgan Chase analysts noted that policy measures may have limited impact on oil prices unless safe passage through the Strait of Hormuz is assured.

How the Iran War Oil Price Surge Is Reshaping the Fed’s Path in 2026

This morning’s February CPI report came in at 2.4% year-over-year, with core inflation cooling to 0.2% month-over-month — the softest monthly reading since last summer. Under normal conditions, that data would be a clear runway for continued Federal Reserve rate cuts in 2026. The Iran war has changed those conditions entirely.

February CPI captures none of the oil shock that began when the conflict escalated on February 28. The real inflation print — the one that reflects $87-plus crude flowing into gasoline, airfares, and freight costs — hasn’t landed yet. Futures markets now imply only one full rate cut in 2026 and roughly a 50% probability of a second, a dramatic collapse from the three or four cuts investors were pricing in just weeks ago. The Iran war oil price surge is doing what no economic data had managed to do — it is freezing the Fed.

What Rising Oil Prices Mean for Small Cap and Microcap Stocks

Energy is the only sector trading higher today, and that creates a direct opportunity set in the small and microcap universe. Domestic energy producers, oilfield services companies, and energy infrastructure plays are clear beneficiaries of sustained high crude prices and the global push to source supply outside the Middle East. These are precisely the kinds of under-the-radar names that populate the small cap space and rarely attract attention until a macro event forces investors to find them.

The rate picture is the countervailing risk. The small cap rotation thesis that pushed the Russell 2000 to nearly 9% year-to-date gains was built on continued Fed easing. A prolonged Iran war, sustained crude oil prices above $90, and a Fed on pause separates quality small cap companies from the leveraged names that were simply riding the rate-cut trade.

The IEA’s record oil reserve release in 2026 is not evidence that the crisis is under control. It is evidence of how severe the disruption actually is. When the largest emergency intervention in energy market history fails to bring prices down, the market is sending a signal — and the investors who act on it early are the ones who tend to come out ahead.