Research News and Market Data on GLDD

Mar 18, 2026

Tender Offer Made in Connection with Parties’ Pending Business Combination Expected to Close Early in the Second Quarter

HOUSTON and SEATTLE, March 18, 2026 (GLOBE NEWSWIRE) — Saltchuk Resources, Inc. (the “Offeror”) and Great Lakes Dredge & Dock Corporation (NASDAQ:GLDD) (the “Company”) announced that the Offeror has commenced a cash tender offer (the “Tender Offer”) for any and all of the Company’s 5.25% Senior Notes due 2029 (the “Notes”).

In conjunction with the Tender Offer, the Offeror is soliciting (the “Consent Solicitation”) consents (each, a “Consent” and, collectively, the “Consents”) from holders of the Notes (each, a “Holder” and, collectively, the “Holders”) to amend certain provisions (the “Proposed Amendments”) of the indenture, dated as of May 25, 2021 (as supplemented from time to time prior to the date hereof, the “Indenture”), between Computershare Trust Company, N.A., as successor to Wells Fargo Bank, National Association, as trustee (the “Trustee”), the Company and the subsidiary guarantors party thereto, under which the Notes were issued. In order for the Proposed Amendments to be approved with respect to the Notes, Holders of a majority in principal amount of the outstanding Notes must consent to the Proposed Amendments (the “Requisite Consents”). If the Requisite Consents with respect to the Notes are received, the Proposed Amendments would, among other things, eliminate substantially all of the restrictive covenants, eliminate certain events of default and modify certain redemption notice requirements with respect to the Notes.

Holders may not tender their Notes without delivering their Consents pursuant to the Consent Solicitation and may not deliver Consents without tendering their Notes pursuant to the Tender Offer. The terms and conditions of the Tender Offer and Consent Solicitation are described in an Offer to Purchase and Consent Solicitation Statement, dated March 18, 2026 (the “Offer to Purchase and Consent Solicitation Statement”). Capitalized terms used herein, but not otherwise defined, have the meanings ascribed to such terms in the Offer to Purchase and Consent Solicitation Statement.

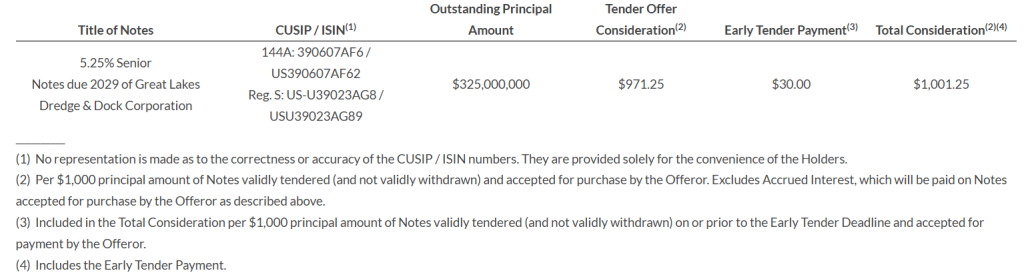

Upon the terms and subject to the conditions set forth in the Offer to Purchase and Consent Solicitation Statement, the Offeror will pay to each Holder who validly tenders (and does not validly withdraw) their Notes and validly delivers (and does not validly revoke) Consents on or prior to 5:00 P.M., New York City time, on March 31, 2026, unless extended or earlier terminated (such date and time, as the same may be extended, the “Early Tender Deadline”), an amount in cash equal to the Tender Offer Consideration, plus the Early Tender Payment for the Notes (as described in the table below and in the Offer to Purchase and Consent Solicitation Statement) on the Early Settlement Date or Final Settlement Date, as applicable (each of which is defined below and either of which may be referred to herein as a “Settlement Date”), if such Notes are accepted for purchase by the Offeror. Tendered Notes may be withdrawn any time on or prior to 5:00 P.M., New York City time, on March 31, 2026 (such date and time, as the same may be extended, the “Withdrawal Deadline”) but not thereafter. Holders who validly tender their Notes and validly deliver Consents after the Early Tender Deadline but on or prior to the Expiration Time (as defined below) will be entitled to receive the Tender Offer Consideration (as described in the table below and in the Offer to Purchase and Consent Solicitation Statement) but not the Early Tender Payment on the Final Settlement Date, if such Notes are accepted for purchase.

In addition to the Tender Offer Consideration or the Total Consideration (as described in the table below), as applicable, such Holders will also receive accrued and unpaid interest on the Notes that the Offeror accepts for purchase in the Tender Offer up to, but excluding, the applicable Settlement Date (“Accrued Interest”).

The following table summarizes the material pricing terms of the Tender Offer.

The Tender Offer and Consent Solicitation are scheduled to expire at 5:00 P.M., New York City time, on April 15, 2026, unless extended or earlier terminated by the Offeror in its sole discretion (such date and time, as the same may be extended, the “Expiration Time”). If, as anticipated, the Offeror’s pending Equity Offer (as defined below) is consummated prior to the Expiration Time, the Offeror may, in its sole discretion, accept for purchase the Notes that have been validly tendered and not validly withdrawn on or prior to the Early Tender Deadline at or promptly following the consummation of the Equity Offer (the “Early Settlement Date”). If the Offeror elects to schedule an Early Settlement Date, the Offeror will provide a notice of such date by press release or other public announcement. If the Equity Offer is not consummated prior to the Expiration Time, there will be no Early Settlement Date. The Offeror expects to accept for purchase the Notes validly tendered and not validly withdrawn on or prior to the Expiration Time promptly following the Expiration Time (the “Final Settlement Date”), subject to the satisfaction of all conditions to the Tender Offer and Consent Solicitation. In the event that the Equity Offer is not consummated prior to the Expiration Time, the Offeror intends to extend the Expiration Time.

Pending Business Combination and Financing Transactions

The Tender Offer and the Consent Solicitation are being made in connection with, and are expressly conditioned upon the closing of, the acquisition of the Company pursuant to the Agreement and Plan of Merger, dated February 10, 2026 (as it may be amended, supplemented or otherwise modified from time to time, the “Merger Agreement”), by and among the Company, the Offeror, and Huron MergeCo., Inc., a Delaware corporation and wholly owned subsidiary of the Offeror (the “Acquisition Sub”). Pursuant to the terms and conditions of the Merger Agreement, Acquisition Sub commenced a tender offer (the “Equity Offer”) on March 4, 2026 to purchase all of the outstanding shares of common stock, par value $0.0001 per share, of the Company (“Company Common Stock”), for $17.00 per share of Company Common Stock, net to the seller thereof in cash, without interest, subject to any required tax withholdings (subject to the conditions described in the offer to purchase filed with the U.S. Securities and Exchange Commission (the “SEC”) on March 4, 2026, by the Offeror and Acquisition Sub (together with any amendments or supplements thereto, the “Equity Offer to Purchase”). The Merger Agreement also provides that, as soon as practicable on the same business day that Acquisition Sub irrevocably accepts for payment all shares of Company Common Stock that are validly tendered (and not validly withdrawn) pursuant to the Equity Offer, or at another date mutually agreed upon by the Company, the Offeror and Acquisition Sub, upon the terms and subject to the conditions set forth in the Merger Agreement, Acquisition Sub will be merged with and into the Company (the “Merger” and, collectively with the Equity Offer, the “Acquisition Transactions”), with the Company continuing as the surviving corporation and a wholly owned subsidiary of the Offeror.

The Offeror and the Company expect (i) to close the Acquisition Transactions early in the second quarter of 2026, subject to the satisfaction (or, to the extent permitted, waiver) of the conditions set forth in the Merger Agreement, and (ii) the Early Settlement Date to occur on or about the closing date of the Acquisition Transactions, as more fully described in the Offer to Purchase and Consent Solicitation Statement. Assuming the satisfaction or waiver of the conditions to the Equity Offer and the Merger Agreement, the Acquisition Transactions are currently scheduled to close on April 1, 2026. The closing of the Acquisition Transactions is not conditioned on (i) any minimum amount of Notes being tendered, (ii) the receipt of the Requisite Consents or (iii) the closing of the Tender Offer or the Consent Solicitation.

The Offeror intends to finance the cash consideration for the Acquisition Transactions, the refinancing of certain of its existing indebtedness, the discharge of the Notes, and certain related transaction expenses using available cash and either the proceeds of borrowings under the New Credit Agreement (as defined below) or a combination of the Offeror’s existing credit facilities and the proceeds from borrowings under the Bridge Facility (as defined below).

Certain lenders, including an affiliate of the Dealer Manager, have agreed to enter into new senior unsecured credit facilities, which are expected to be provided in the form of either (i) a fully committed, senior unsecured bridge term loan facility (the “Bridge Facility”) or (ii) a new senior unsecured credit agreement (the “New Credit Agreement” and, together with the Bridge Facility, the “New Senior Credit Facilities”) providing for (x) a five-year $1.5 billion revolving credit facility and (y) a five-year $1.25 billion term loan facility.

General Information

The Offeror’s obligation to accept for purchase, and to pay for, Notes validly tendered and not validly withdrawn and to accept accompanying Consents validly delivered and not validly revoked pursuant to the Tender Offer and Consent Solicitation is conditioned upon the following having occurred or having been waived by the Offeror: (1) the consummation of the Equity Offer on the terms and conditions set forth in the Merger Agreement and Equity Offer to Purchase, and (2) the satisfaction of the General Conditions described in the Offer to Purchase and Consent Solicitation Statement. In addition, our obligation to accept Consents that have been validly delivered and not validly revoked pursuant to the Consent Solicitation is further conditioned upon supplemental conditions described in the Offer to Purchase and Consent Solicitation Statement. There can be no assurance that the Tender Offer or the Consent Solicitation will be consummated. The Offeror may amend, extend or terminate the Tender Offer and the Consent Solicitation, in its sole discretion. The Tender Offer is not conditioned on any minimum amount of Notes being tendered or the receipt of the Requisite Consents.

The Offeror intends to fund the Total Consideration and the Tender Offer Consideration (including, in each case, the Accrued Interest), plus all related fees and expenses, using available cash and the borrowings described above under Pending Business Combination and Financing Transactions.

Any Notes not tendered and purchased pursuant to the Tender Offer will remain outstanding. If the Requisite Consents are received with respect to the Notes, and the Proposed Amendments become operative with respect to the Indenture, then the Notes that are not purchased pursuant to the Tender Offer will be subject to the Proposed Amendments as set forth in a supplemental indenture with respect to the Indenture.

To the extent any Notes remain outstanding following the consummation of the Tender Offer and Consent Solicitation, the Offeror intends, but is not obligated, to redeem such remaining Notes at par on or after June 1, 2026 and satisfy and discharge the Company’s obligations under the Indenture pursuant to the terms thereof. Alternatively, the Offeror may cause the Company to leave any such remaining Notes outstanding or effect any of the alternative transactions described in the Offer to Purchase and Consent Solicitation Statement.

BofA Securities has been retained as the Dealer Manager in connection with the Tender Offer and as the Solicitation Agent in connection with the Consent Solicitation. In such capacities, they may contact Holders regarding the Tender Offer and the Consent Solicitation and may request brokers, dealers, banks, trust companies and other nominees or intermediaries to forward the Offer to Purchase and Consent Solicitation Statement and related materials to beneficial owners of Notes. Questions and requests for assistance regarding the terms of the Tender Offer and the Consent Solicitation should be directed to the Dealer Manager at (888) 292-0070 (toll-free) or (980) 388-3646 (collect). Questions regarding the procedures for tendering Notes and delivering Consents relating to the Tender Offer and the Consent Solicitation or requests for additional copies of the Offer to Purchase and Consent Solicitation Statement may be directed to Global Bondholder Services Corporation, the Tender and Information Agent for the Tender Offer, at (212) 430-3774 (for banks and brokers only) or (855) 654-2014 (toll-free) (for all others) or [email protected].

This press release is for informational purposes only. The Tender Offer and the Consent Solicitation are being made solely pursuant to the Offer to Purchase and Consent Solicitation Statement. This press release does not constitute an offer to purchase or the solicitation of an offer to sell any securities. Full details of the terms and conditions of the Tender Offer and the Consent Solicitation are described in the Offer to Purchase and Consent Solicitation Statement, which is being furnished by the Offeror to Holders of the Notes. Holders of the Notes are encouraged to read the Offer to Purchase and Consent Solicitation Statement and the information incorporated therein by reference, as they contain important information regarding the Tender Offer and the Consent Solicitation. The Tender Offer and the Consent Solicitation are not being made to Holders in any jurisdiction in which the making or acceptance thereof would not be in compliance with the securities, blue sky or other laws of such jurisdiction. In any jurisdiction in which the securities laws or blue sky laws require the Tender Offer or the Consent Solicitation to be made by a licensed broker or dealer, the Tender Offer and the Consent Solicitation will be deemed to be made on behalf of the Offeror by the Dealer Manager, or one or more registered brokers or dealers that are licensed under the laws of such jurisdiction.

This press release is for information purposes only and does not constitute an offer to buy or the solicitation of an offer to sell any securities. The Offeror’s solicitation and offer to buy shares of Company Common Stock is being made only pursuant to the Equity Offer to Purchase and related materials that the Offeror and Acquisition Sub have filed with the SEC. In connection with the Equity Offer, the Offeror and Acquisition Sub have filed a Tender Offer Statement on Schedule TO with the SEC and the Company has filed a Solicitation/Recommendation Statement on Schedule 14D-9. Before making any investment decision with respect to the Equity Offer, investors and security holders of the Company are urged to read the tender offer materials, the solicitation/recommendation statement and any other relevant documents filed with the SEC. In addition, all of these materials (and all other tender offer documents filed with the SEC) are available at no charge from the SEC through its website at www.sec.gov and upon request to MacKenzie Partners, Inc., the information agent for the Equity Offer, at 7 Penn Plaza, New York, New York 10001, by calling toll free (800) 322-2885. Broadridge Corporate Issuer Solutions, LLC is acting as depositary and paying agent for the Equity Offer.

None of the Offeror, the Company, the Trustee, the Dealer Manager, the Tender and Information Agent, or any of their respective affiliates makes any recommendation as to whether Holders should tender or refrain from tendering their Notes in response to the Tender Offer or delivering Consents pursuant to the Consent Solicitation, and no person or entity has been authorized by any of them to make such a recommendation. Holders must make their own independent decision as to whether to tender Notes and deliver accompanying Consents and, if so, the principal amount of the Notes as to which action is to be taken.

Nothing contained herein shall constitute a notice of redemption of the Notes or an obligation to issue a notice of redemption or satisfy or discharge the Indenture.

About Saltchuk Resources, Inc.

Saltchuk is a privately owned family of diversified freight transportation, marine service, and energy distribution companies, with consolidated annual revenue of approximately $5.5 billion and 8,800 employees. We make multi-generational investments, championing our companies’ individual brands while providing strategic leadership and resources through our Corporate Home. Our companies maintain independent operations guided by shared values: safety comes first, reliability defines our customer relationships, and integrity shapes how we conduct business. We’re committed to each other, to environmental stewardship, and to contributing to our communities, fostering places where anyone would be proud for their children to work. Headquartered in Seattle, additional information is available at www.saltchuk.com.

About Great Lakes Dredge & Dock Corporation

Great Lakes Dredge & Dock Corporation is the largest provider of dredging services in the United States, which is complemented with a long history of performing significant international projects. In addition, Great Lakes is fully engaged in expanding its core business into the offshore energy industry. GLDD employs experienced civil, ocean and mechanical engineering staff in its estimating, production, and project management functions. In its over 136-year history, GLDD has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experience-based performance as they advance through GLDD operations. GLDD’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the GLDD’s culture. GLDD’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Cautionary Note Regarding Forward-Looking Statements

Forward-looking statements made herein with respect to the Tender Offer and Consent Solicitation and related transactions, including, for example, the timing of the completion of the Tender Offer and Consent Solicitation, Equity Offer and the Merger or the potential benefits of any such transactions, reflect the current analysis of existing information and are subject to various risks and uncertainties. As a result, caution must be exercised in relying on forward-looking statements. Due to known and unknown risks, the Company and the Offeror’s actual results may differ materially from its expectations or projections. All statements other than statements of historical fact are statements that could be deemed forward-looking statements. Forward-looking statements can be identified by, among other things, the use of forward-looking language, such as the words “plan,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “target,” “project,” “contemplate,” “predict,” “potential,” “continue,” “may,” “would,” “could,” “should,” “seeks,” “scheduled to,” or other similar words, or the negative of these terms or other variations of these terms or comparable language.

The following factors, among others, could cause actual plans and results to differ materially from those described in forward-looking statements. Such factors include, but are not limited to, the effect of the announcement of the Acquisition Transactions and the Tender Offer and Consent Solicitation on the Company and the Offeror’s relationships with employees, governmental entities and other business relationships, operating results and business generally; the occurrence of any event, change or other circumstances that could give rise to the termination of the Merger Agreement, and the risk that the Merger Agreement may be terminated in circumstances that require the Company to pay a termination fee; the possibility that competing offers will be made; the outcome of any legal proceedings that may be instituted against the Company and the Offeror related to the transactions contemplated by the Merger Agreement, including the Acquisition Transactions; uncertainties as to the timing of the consummation of the Tender Offer and Consent Solicitation and the Acquisition Transactions; uncertainties as to the number of stockholders of the Company who may tender their stock in the Equity Offer and number of Holders who may tender their Notes and deliver accompanying Consents in the Tender Offer and Consent Solicitation; the failure to satisfy other conditions to consummate the Acquisition Transactions on the anticipated timeframe or at all; risks that the Tender Offer and Consent Solicitation and the Acquisition Transactions disrupt current plans and operations and the potential difficulties in employee retention as a result of the proposed transactions; the effects of local and national economic, credit and capital market conditions on the economy in general, and other risks and uncertainties; and those risks and uncertainties discussed from time to time in the reports or other public filings of the Company, the Offeror or the Acquisition Sub with the SEC.

Additional information concerning these and other factors that may impact the Company’s expectations and projections can be found in its periodic filings with the SEC, including its Annual Report on Form 10-K for the year ended December 31, 2025. GLDD’s SEC filings are available publicly on the SEC’s website at www.sec.gov, on GLDD’s website at gldd.com under “Investors—Financials & Filings—SEC filings” or upon request via email to [email protected]. All forward-looking statements contained in this communication are based on information available to the Company and the Offeror as of the date hereof and are made only as of the date of this communication. The Company and the Offeror disclaim any obligation or undertaking to update or revise the forward-looking statements contained herein, whether as a result of new information, future events or otherwise, except as required under applicable law. These forward-looking statements should not be relied upon as representing the Company and the Offeror’s views as of any date subsequent to the date of this communication. Furthermore, any information about our intentions contained in any of our forward-looking statements reflects our intentions as of the date of such forward-looking statement, and is based upon, among other things, existing regulatory, industry, competitive, economic and market conditions, and our assumptions as of such date. We may change our intentions, strategies or plans (including our plans expressed herein) without notice at any time and for any reason. In light of the foregoing, investors are urged not to rely on any forward-looking statement in reaching any conclusion or making any investment decision about any securities of the Company and the Offeror.

Contact:

Eric Birge,

Vice President of Investor Relations of the Company,

313-220-3053