Why S&P Global Ratings Dropped Its Alphanumeric ESG Ratings

As evidence that new concepts need to go through a cycle and find their place, S&P Global Ratings has stopped including environmental, social, and governance (ESG) ratings on its reports. S&P Global Ratings is the credit ratings division of Standard & Poor’s. The division specializes in providing company-sponsored research, analysis, credit ratings, and data to assist investors in evaluating the creditworthiness and risk associated with financial instruments and entities.

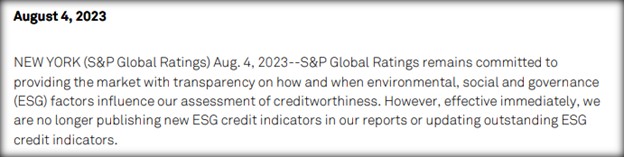

In an official press release titled, S&P Global Ratings Update On ESG Credit Indicators released this month. The prominent and perhaps best-known Nationally Recognized Statistical Ratings Organization (NRSRO) revealed its decision to discontinue the publication of new ESG credit indicators, and will not be updating those ESG scores previously determined.

Source: S&P Global Ratings, Dated August 4, 2023

S&P defines ESG credit indicators as “those ESG factors that can materially influence the creditworthiness of a rated entity or issue.” The rating agency said in the release that it had initially begun publishing alphanumeric ESG credit indicators for publicly rated entities in some sectors and asset classes in 2021. “These indicators were intended to illustrate and summarize the relevance of ESG credit factors on our rating analysis through the use of an alphanumerical scale,” the agency added, “They supplemented the narrative paragraphs in our credit rating reports where we describe the impact of ESG credit factors on creditworthiness.”

It has been just two years, and S&P has changed its reporting, if not its methodology. The release explained that after further review the “dedicated analytical narrative paragraphs in our credit rating reports are most effective at providing detail and transparency on ESG credit factors material to our rating analysis, and these will remain integral to our reports.” So there is no separate breakout rating, but to the extent that an ESG related factor could impact creditworthiness, S&P will include the discussion in its write-ups, and it will be reflected when appropriate in an institutions’ security ranking.

S&P Global was clear that the immediately implemented policy does not affect its ESG principles criteria or its research and commentary on ESG-related topics, including the influence that ESG factors may have on a companies ability to pay interest and return principal.

Fitch Ratings, chief credit officer, Richard Hunter told Pension and Investments that: “Fitch believes that there are profound limits to what text disclosures can do for investors monitoring an entire portfolio of hundreds of serviced issuers and bonds. This is the second time in less than amonth that the two NRSROs demonstrated very different methodologies. After Fitch Ratings downgraded U.S. backed Treasuries and other obligations, S&P said they would not unless the U.S. was going to miss a payment.

To round out the big three institutional rating agencies, Moody’s said in a statement that it “incorporates all risks, including those related to ESG, into its credit ratings when they are material, and also publishes ESG scores on a 1 to 5 scale.”

Take Away

The definitions, overall landscape, and actions taken to support sustainability are evolving. S&P Global Ratings’ decision to not separately rank obligors is a strategic recalibration in its presentation of ESG factors that may impact an entities ability to pay. It believes the credit factors don’t warrant a separate carve-out within their reports – and that clarity and assessing creditworthiness is best discussed and not boiled down to an alphanumeric rating for use by investors.

For the Third Time This Year, Investors Get to Peak Behind the “Smart Money” Curtain

What’s smart money doing?

If retail investors weren’t always eager to know what hedge fund managers, corporate insiders, and others building positions in a stock have been doing, shows like CNBC’s Closing Bell, news sources like Investors Business Daily, and communities like Seeking Alpha would get far less attention. Next week, the most followed institutional investors are expected to make their quarter-end holdings public. This will usher in a lot of buzz around the surprise changes in holdings and even short positions in celebrity investor portfolios.

Popular SEC Filings

The most popular SEC filings from the supposed “smart money” that small investors look to for ideas are:

Form 13D – This is a filing that is required to be made by any person or group that acquires 5% or more of a company’s voting securities. The filing must disclose the person’s or group’s intentions with respect to the company, such as whether they plan to take control of the company or simply invest in it.

Investors may recall Elon Musk’s accumulation of Twitter shares was incorrectly filed on form 13-G which is for passive investors. He later had to amend his filing on 13D as his accumulation of shares was discovered to be predatory.

Form 4 – This is a filing that is required to be made by any officer, director, or 10% shareholder of a company when they buy or sell shares of the company’s stock. The filing must disclose the number of shares bought or sold, the price per share, and the date of the transaction.

This is the filing that the public used to discover that in 2021, Mark Zuckerberg sold Meta (META) shares (Facebook) almost daily for a total of $4.1 billion. The same year Jeff Bezos sold $8.8 billion worth of Amazon (AMZN) stock, mostly during the month of November.

Both of the filing types mentioned above are as needed, they don’t have a recurring season. However, another popular filing is form 13-F, these much anticipated filings occur four times each year.

Form 13F – This is a quarterly report that is required to be filed by institutional investment managers with at least $100 million in assets under management. The report discloses the manager’s equity and other public securities, including the number of shares held, the CUSIP number, and the market value.

Investors will pour over the quarter-end snapshot of the account and measure changes from the prior quarter, especially from investors like Warren Buffett, Bill Ackman, and Cathie Wood for insights. When Michael Burry filed his 13-F in mid May 2022, he had a position showing that he was short Apple (AAPL). Headlines erupted across news sources, and this certainly had an impact on the tech company’s stock price as other investors questioned its high valuation against any positions they may have had.

The Consistency of the 13-F

The SEC 13-F is a regular filing for large funds. Interested investors can generally mark their calendars for when a funds 13-F will be released. The SEC requires a quarterly report filed no later than 45 days from the calendar quarter’s ends. Most popular managers wait until the last minute, as they may not be so eager to share their funds positions any sooner than needed. This means that most 13-F filings are on February 15 (or before), May 15 (or before), August 15 (or before), and November 15 (or before). In 2023, August 15th is next Tuesday. During the second quarter of 2023 there seemed to have been significant sector rotation, and a reduction in short positions among large funds. This will make for above average interest.

Famous Investors that file a Form 13F

The legendary investor Warren Buffett is the CEO of Berkshire Hathaway. His company’s Form 13F filings are closely watched by investors around the world.

Warren Buffett, last filed a 13-F on May 15, 2023

Ray Dalio is the founder of Bridgewater Associates, one of the world’s largest hedge funds. His company’s Form 13F filings are also very popular with investors.

Ray Dalio, founder of Bridgewater Associates, last filed a 13-F on May 15, 2023

Michael Burry is the investor who famously bet against the housing market in the lead-up to the 2008 financial crisis. His company’s Form 13F filings are often seen as positions of a highly regarded contrarian.

Dr. Michael Burry, last filed a 13-F on May 15, 2023

Cathie Wood is the CEO of ARK Invest, a firm that invests in disruptive technologies. Her company’s Form 13F filings are often seen as a bellwether for the future of technology. Wood is always open and transparent about her funds holdings. This may explain why she is among the earliest filers after each quarter-end.

Cathie Wood, last filed a 13-F on July 10, 2023 for the second quarter ended June 31, 2023

Drawbacks to Using Form 13F

While Form 13F filings can be a valuable source of information for investors, it isn’t magic. And if it is going to weigh heavily as part of an investor’s selection process, some drawbacks should be considered.

The information is delayed: Form 13F filings are not real-time information. They are usually filed 45 days after the end of the quarter, so the information is already outdated by the time it is available to the public.

The information is not complete: Form 13F filings only disclose the top 10 holdings of each fund. This means that investors do not have a complete picture of the fund’s portfolio.

It is not always clear if a position is based on expectations for the one holding, or should be viewed in light of the full portfolio, balancing risk and potential reward. For example, an investment manager may be bullish on tech and long a tech megacap with a lower than average P/E ratio and as of the same filing, short a similar amount of a tech megacap with a higher P/E ratio. The fund manager may be bullish on both, and the nature of the positions may indicate an expectation that the P/E ratios are likely to move toward a similar ratio. If there is just a focus on one side (long or short), the investor may read the intentions or expectations wrong.

Take Away

As earnings season fades, the third week in August will provide a mountain of information on what institutional investors were doing during the second quarter. This is a great place to find ideas and understand any changes in flows.

Investors should be cautioned that this is only a June 30th snap shot, and these holdings may have changed days later.’

Company-Owned Cookie Dough FacilityNow Serving Fatburgerand Johnny Rockets

LOS ANGELES, Aug. 08, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Fatburger, Johnny Rockets and 15 other restaurant concepts, today announces the rollout of cookie offerings at burger portfolio restaurants nationwide – Fatburger, Johnny Rockets and Elevation Burger.

The sweet menu rollout is a strategic optimization that leverages FAT Brands’ company-owned manufacturing facility, which produces cookie dough and pretzel mix for sister portfolio brands Great American Cookies and Pretzelmaker. Elevation Burger completed its cookie roll-out earlier in April of this year.

“For both Fatburger and Johnny Rockets, we see these additions as a way to further build and enhance our dessert programs,” said Taylor Fischer, Vice President of Marketing of FAT Brands’ Fast Casual Division. “Playing into synergies is at the core of FAT Brands’ DNA. We are thrilled to be able to tap into our cookie dough facility to provide more delicious offerings for our fans.”

For more information or to find a Fatburger near you, please visit www.Fatburger.com. For more information or to find a Johnny Rockets near you, please visit www.JohnnyRockets.com.

About FAT (Fresh. Authentic. Tasty.) Brands

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast-casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Fatburger

An all-American, Hollywood favorite, Fatburger is a fast-casual restaurant serving big, juicy, tasty burgers, crafted specifically to each customer’s liking. With a legacy spanning 70 years, Fatburger’s extraordinary quality and taste inspire fierce loyalty amongst its fan base, which includes a number of A-list celebrities and athletes. Featuring a contemporary design and ambience, Fatburger offers an unparalleled dining experience, demonstrating the same dedication to serving gourmet, homemade, custom-built burgers as it has since 1952 – The Last Great Hamburger Stand™.

About Johnny Rockets

Founded in 1986 on iconic Melrose Avenue in Los Angeles, Johnny Rockets is a world-renowned, international restaurant franchise that offers high quality, innovative menu items including Certified Angus Beef® cooked-to-order hamburgers, veggie burgers, chicken sandwiches, crispy fries and rich, delicious hand-spun shakes and malts. With over 325 locations in over 25 countries around the globe, this dynamic lifestyle brand offers friendly service and upbeat music contributing to the chain’s signature atmosphere of relaxed, casual fun. For more information, visit www.johnnyrockets.com.

TORONTO, ON / ACCESSWIRE / August 8, 2023 / GameSquare Holdings, Inc. (“GameSquare“, or the “Company“) (NASDAQ:GAME)(TSXV:GAME) announced today that it expects to release its second quarter 2023 financial results after the close of business on Monday, August 14, 2023. A copy of the news release will be available on the investor website.

Shareholders, investors, interested parties, and media are encouraged to join the Company’s earnings call via webcast on Monday, August 14, 2023, at 5:00 pm ET. The call will be hosted by Justin Kenna, GameSquare’s CEO and will be joined by other members of GameSquare’s management team. Please join the call at https://services.choruscall.ca/links/gamesquare2023q2.html.

About GameSquare Holdings, Inc.

GameSquare Holdings, Inc. (NASDAQ:GAME | TSXV:GAME) is a vertically integrated, digital media, entertainment and technology company that connects global brands with gaming and youth culture audiences. GameSquare’s end-to-end platform includes GCN, a digital media company focused on gaming and esports audiences, Cut+Sew (Zoned), a gaming and lifestyle marketing agency, USA, Code Red Esports Ltd., a UK based esports talent agency, Complexity Gaming, a leading esports organization, Fourth Frame Studios, a creative production studio, Mission Supply, a merchandise and consumer products business, Frankly Media, programmatic advertising, Stream Hatchet, live streaming analytics, and Sideqik a social influencer marketing platform. www.gamesquare.com

Media and Investor Relations Andrew Berger Phone: (216) 464-6400 Email: IR@gamesquare.com

Forward-Looking Information This news release contains “forward-looking information” and “forward-looking statements” (collectively, “forward-looking statements”) within the meaning of the applicable securities legislation. All statements, other than statements of historical fact, are forward-looking statements and are based on expectations, estimates and projections as at the date of this news release. Any statement that involves discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking statements. In this news release, forward-looking statements relate, among other things, to: the Company’s future performance and revenue; continued growth and profitability; the Company’s ability to execute its business plan; and the proposed use of net proceeds of the Offering. These forward-looking statements are provided only to provide information currently available to us and are not intended to serve as and must not be relied on by any investor as, a guarantee, assurance or definitive statement of fact or probability. Forward-looking statements are necessarily based upon a number of estimates and assumptions which include, but are not limited to: the Company being able to grow its business and being able to execute on its business plan, the Company being able to complete and successfully integrate acquisitions, the Company being able to recognize and capitalize on opportunities and the Company continuing to attract qualified personnel to supports its development requirements. These assumptions, while considered reasonable, are subject to known and unknown risks, uncertainties, and other factors which may cause the actual results and future events to differ materially from those expressed or implied by such forward-looking statements. Such factors include, but are not limited to: the Company’s ability to achieve its objectives, the Company successfully executing its growth strategy, the ability of the Company to obtain future financings or complete offerings on acceptable terms, failure to leverage the Company’s portfolio across entertainment and media platforms, dependence on the Company’s key personnel and general business, economic, competitive, political and social uncertainties including impact of the COVID-19 pandemic and any variants. These risk factors are not intended to represent a complete list of the factors that could affect the Company which are discussed in the Company’s most recent MD&A. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on the forward-looking statements and information contained in this news release. GameSquare assumes no obligation to update the forward-looking statements of beliefs, opinions, projections, or other factors, should they change, except as required by law.

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

First dual coronavirus-norovirus oral antiviral isscheduledfor Phase 1 in healthy volunteers

In vitro studies show broad-spectrum activity against noroviruses including GII.4 pandemic strains

No approved treatments or vaccines for norovirus infection

BOTHELL, Wash., Aug. 08, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (“Cocrystal” or the “Company”), a clinical-stage biopharmaceutical company dedicated to developing novel small molecule antiviral therapeutics, announces the selection of its novel, oral, broad-spectrum 3CL protease inhibitor CDI-988 as a potential oral therapy for norovirus. The randomized, double-blind, placebo-controlled Phase 1 study of CDI-988 is approved by Australia Human Research Ethics Committees (HREC). The study is designed to access the safety, tolerability and pharmacokinetics of CDI-988.

With no approved treatments or vaccines, norovirus represents a significant unmet medical need. It is a highly contagious infection and is the most common cause of acute gastroenteritis, accounting for nearly one in five cases. According to the Centers for Disease Control and Prevention (CDC), an estimated 685 million cases and an estimated 200,000 deaths are attributed to norovirus each year worldwide with an estimated societal cost of $60 billion. About 200 million cases are reported among children under five years of age, leading to an estimated 50,000 child deaths every year. Among 30 known genotypes of human norovirus, nearly 60% of outbreaks are attributable to genogroup II, genotype 4 (GII.4) strains, which have caused periodic human pandemics since 1996.

CDI-988 was specifically designed and developed as a broad-spectrum antiviral inhibitor using Cocrystal’s proprietary structure-based drug discovery platform technology. It targets a highly conserved region in the active site of coronaviruses, noroviruses and other 3CL viral proteases. Cocrystal previously selected CDI-988 to investigate as an oral treatment for COVID-19 and is approved to conduct a Phase 1 study in Australia, following approval by that country’s Human Research Ethics Committee (HREC). In recent preclinical in vitro studies, CDI-988 showed potent broad-spectrum antiviral activity against a panel of pandemic GII.4 norovirus proteases and a favorable pharmacokinetic property targeting the gastrointestinal tract.

“In preclinical testing CDI-988 showed significant activity against seven different pandemic strains of norovirus, and we are enthusiastic about developing this compound as a dual broad-spectrum antiviral inhibitor,” said Sam Lee, PhD, Cocrystal President and co-CEO. “CDI-988 further validates our proprietary structure-based drug-discovery platform technology and contributes to our robust product pipeline. Our approach is to develop an effective targeted oral treatment for acute and chronic gastroenteritis caused by norovirus, as well as for potential use in addressing future pandemic norovirus outbreaks.”

“Given the recent increase in norovirus cases and the lack of approved treatments or vaccines, we continue to see a significant opportunity for our broad-spectrum antiviral CDI-988,” said James Martin, Cocrystal CFO and co-CEO. “There has been a sharp rise in norovirus outbreaks worldwide since 1996 with the emergence of the GII.4 strain. Already in 2023, 13 outbreaks on cruise ships have been reported, the largest number of such infections in a decade.”

About Norovirus Human noroviruses are highly contagious, constantly evolving, extremely stable in the environment and associated with debilitating illness. Symptoms include vomiting and diarrhea, with or without nausea and abdominal cramps. Norovirus infection can be much more severe and prolonged in specific risk groups including infants, children and people with immunodeficiency. In the United States alone, noroviruses are responsible for an estimated 21 million cases of acute gastroenteritis annually, including 109,000 hospitalizations, 465,000 emergency department visits and nearly 900 deaths, according to the CDC. The National Institutes of Health (NIH) estimates the annual burden to the U.S. at $10.6 billion. Outbreaks occur most commonly in semi-closed communities such as nursing homes, hospitals, cruise ships, schools, disaster relief sites and military settings.

About Cocrystal Pharma, Inc. Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2 and noroviruses) and hepatitis C viruses. Cocrystal employs unique structure-based technologies and Nobel Prize-winning expertise to create first- and best-in-class antiviral drugs. For further information about Cocrystal, please visit www.cocrystalpharma.com.

Cautionary Note Regarding Forward-Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the initiation and characteristics of a Phase 1 study for CDI-988 and the potential efficacy and clinical benefits of such product candidate. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, regulatory approval to commence the planned trial, risks relating to the Australian economy, manufacturing and research delays arising labor shortages and other factors, the ability of our Clinical Research Organization partner to recruit volunteers for, and to proceed with, the Phase 1 clinical study for CDI-988, and general risks arising from conducting a clinical trial. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

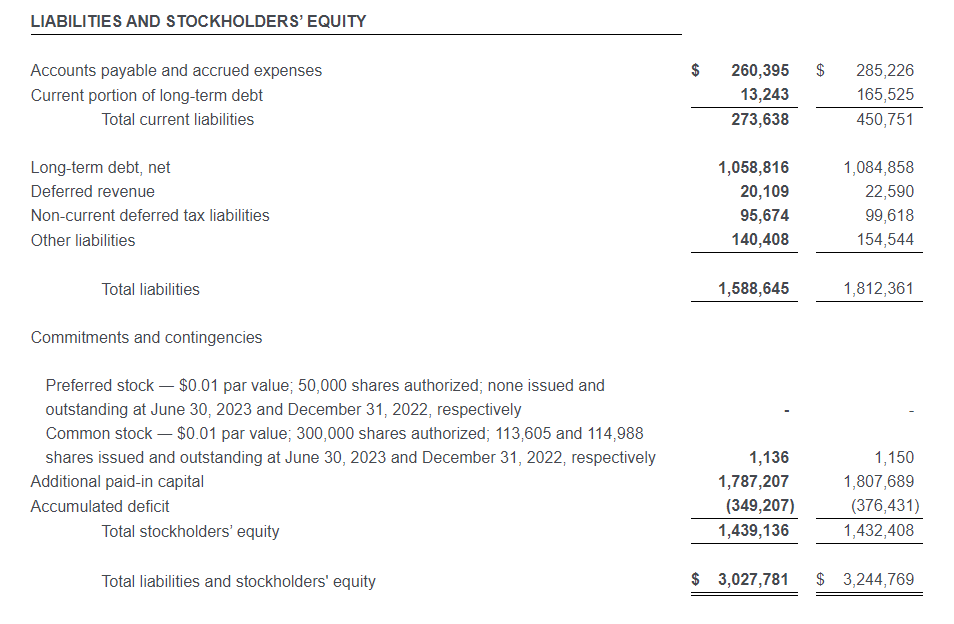

REDUCES TOTAL DEBT BY $34.1 MILLION INCREASES 2023 FULL YEAR GUIDANCE

Reduces Total Debt by $34.1 Million

Increases 2023 Full Year Guidance

BRENTWOOD, Tenn., Aug. 07, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today its financial results for the second quarter of 2023.

Damon T. Hininger, CoreCivic’s President and Chief Executive Officer, said, “Our second quarter financial results were better than our forecast and we are increasing our financial outlook for the year. We are increasing our financial outlook despite the challenging labor market, above average inflation and a higher interest rate environment. During the second quarter, we continued to execute on our long-term capital allocation strategy of reducing debt by repurchasing $21.0 million of our 8.25% Senior Notes that are scheduled to mature on April 15, 2026, through open market purchases.”

Hininger continued, “The post-pandemic environment is creating new challenges for a number of our government partners, particularly as a result of the expiration of the Public Health Emergency for COVID-19 that occurred in May, which ended the Title 42 closure of the southern border. Specifically, certain government agencies are experiencing an increase in the need for correctional and detention capacity. We believe the significant investments we have made in our workforce have positioned us well to meet these emerging needs.”

Financial Highlights – Second Quarter 2023

Total revenue of $463.7 million

CoreCivic Safety revenue of $421.7 million

CoreCivic Community revenue of $28.4 million

CoreCivic Properties revenue of $13.6 million

Net Income of $14.8 million

Diluted earnings per share of $0.13

Adjusted Diluted EPS of $0.12

Normalized Funds From Operations per diluted share of $0.33

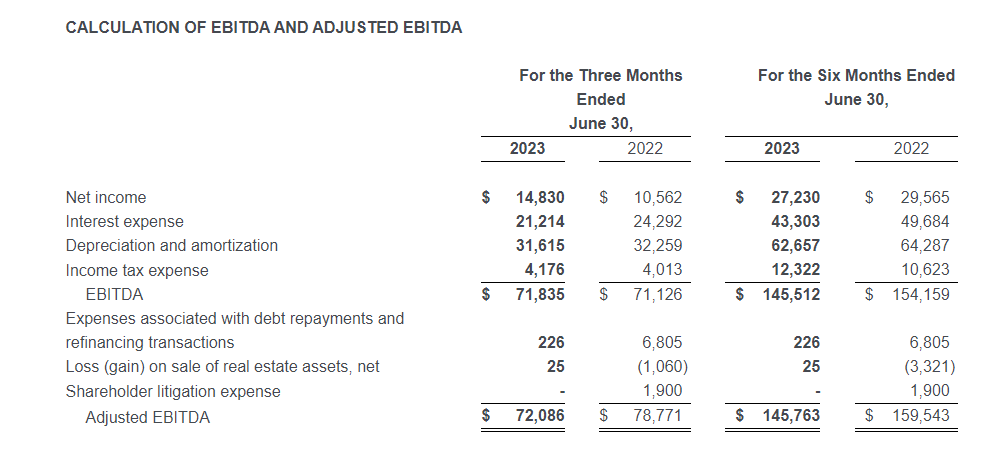

Adjusted EBITDA of $72.1 million

Second Quarter 2023 Financial Results Compared With Second Quarter 2022

Net income in the second quarter of 2023 totaled $14.8 million, or $0.13 per diluted share, compared with net income in the second quarter of 2022 of $10.6 million, or $0.09 per diluted share. Adjusted for special items, adjusted net income in the second quarter of 2023 was $13.6 million, or $0.12 per diluted share (Adjusted Diluted EPS), compared with adjusted net income in the second quarter of 2022 of $16.2 million, or $0.13 per diluted share. Special items for each period are presented in detail in the calculation of Adjusted Net Income and Adjusted Diluted EPS in the Supplemental Financial Information following the financial statements presented herein.

The special items in the prior year quarter contributed to the increase in net income per share of $0.04. The $0.01 per share decline in Adjusted Diluted EPS occurred in part due to the expiration of our contract with the Federal Bureau of Prisons (BOP) at the McRae Correctional Facility on November 30, 2022, and ongoing labor market pressures, including above average wage inflation, and higher staffing levels. Despite the expiration of the contract with the BOP at the McRae facility, a facility we sold to the state of Georgia in 2022, our renewal rate on owned and controlled facilities remains high at 94% over the previous five years. We believe our renewal rate on existing contracts remains high due to a variety of reasons including the aged and constrained supply of available beds within the U.S. correctional system, our ownership of the majority of the beds we operate, the value our government partners place in the wide range of recidivism-reducing programs we offer to those in our care, and the cost effectiveness of the services we provide.

Earnings before interest, taxes, depreciation and amortization (EBITDA) was $71.8 million in the second quarter of 2023, compared with $71.1 million in the second quarter of 2022. Adjusted EBITDA was $72.1 million in the second quarter of 2023, compared with $78.8 million in the second quarter of 2022. Adjusted EBITDA decreased from the prior year quarter primarily due to the previously mentioned labor market pressures across our facility portfolio, including above average wage inflation and higher staffing levels in anticipation of increased occupancy, and the expiration of our BOP contract at the McRae Correctional Facility in November 2022. EBITDA at the McRae Correctional Facility was $2.4 million during the second quarter of 2022.

Although labor market pressures continue to be more difficult than historical norms, we have experienced improvements in the number of applicants at many of our facilities which has allowed us to achieve higher staffing levels in the second quarter of 2023 than in the prior year quarter. We believe the investments in staffing we made during the pandemic have positioned us to manage the increased number of residents we began to experience in the second quarter of 2023. On May 11, 2023, all remaining COVID-19 related health policies expired, most notably occupancy restrictions on our facilities and Title 42, a policy that denied entry at the United States border to asylum-seekers and anyone crossing the border without proper documentation or authority in an effort to contain the spread of COVID-19. Since the end of Title 42, the number of individuals in the custody of U.S. Immigration and Customs Enforcement (ICE) has increased 43%. We have experienced a similar increase within our facilities under contract with ICE, which we believe was possible because of our investments in staffing. Since May 11, 2023, through July 31, 2023, ICE detention populations within our facilities have increased by 2,573, or 45%. Despite the difficult labor market, we have been able to reduce certain labor-related expenses, such as registry nursing, temporary wage incentives, and travel, each of which moderated during the second quarter of 2023. We believe we can further reduce these expenses as the tight labor market continues to alleviate, which we expect will take additional time.

Funds From Operations (FFO) was $39.0 million, or $0.34 per diluted share, in the second quarter of 2023, compared to $34.3 million, or $0.28 per diluted share, in the second quarter of 2022. Normalized FFO, which excludes special items, was $37.8 million, or $0.33 per diluted share, in the second quarter of 2023, compared with $40.7 million, or $0.34 per diluted share, in the second quarter of 2022. Normalized FFO was impacted by the same factors that affected Adjusted EBITDA.

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share amounts, are measures calculated and presented on the basis of methodologies other than in accordance with generally accepted accounting principles (GAAP). Please refer to the Supplemental Financial Information and the note following the financial statements herein for further discussion and reconciliations of these measures to net income, the most directly comparable GAAP measure.

Business Update

New Lease Agreement with the State of Oklahoma at the Davis Correctional Facility. On June 14, 2023, we announced that we entered into a lease agreement with the Oklahoma Department of Corrections (ODOC) for the company-owned 1,670-bed Davis Correctional Facility, which we currently report in our CoreCivic Safety segment and operate under a management contract with the ODOC. The management contract was scheduled to expire on June 30, 2023. However, effective July 1, 2023, the Company entered into a 90-day contract extension for the management contract, after which time operations of the Davis facility will transfer from CoreCivic to the ODOC in accordance with the new lease agreement. We incurred a facility net operating loss of $0.9 million and $1.5 million for the three and six months ended June 30, 2023, respectively. Annual lease revenue under the new lease agreement will be $7.5 million during the base term, which we expect will generate margins consistent with the average margin we report in our Properties segment. The new lease agreement includes a base term commencing October 1, 2023, with a scheduled expiration date of June 30, 2029, and unlimited two-year renewal options. Upon commencement of the new lease agreement, the Davis facility will be reported in our CoreCivic Properties segment.

Share Repurchases

On May 12, 2022, our Board of Directors approved a share repurchase program authorizing the Company to repurchase up to $150.0 million of our common stock. On August 2, 2022, our Board of Directors authorized an increase in our share repurchase program of up to an additional $75.0 million in shares of our common stock, or a total of up to $225.0 million. During the three and six months ended June 30, 2023, we repurchased 0.1 million and 2.6 million shares of our common stock, respectively, at an aggregate purchase price of $0.7 million and $25.6 million, respectively, and in each case excluding fees, commissions and other costs related to the repurchases. Since the share repurchase program was authorized, through June 30, 2023, we have repurchased a total of 9.2 million shares at an aggregate price of $100.1 million under this share repurchase program, excluding fees, commissions and other costs related to the repurchases.

As of June 30, 2023, we had $124.9 million remaining under the share repurchase program authorized by the Board of Directors. Additional repurchases of common stock will be made in accordance with applicable securities laws and may be made at management’s discretion within parameters set by the Board of Directors from time to time in the open market, through privately negotiated transactions, or otherwise. The share repurchase program has no time limit and does not obligate us to purchase any particular amount of our common stock. The authorization for the share repurchase program may be terminated, suspended, increased or decreased by our Board of Directors in its discretion at any time.

Debt Repayments

During the second quarter of 2023, we reduced our total debt balance by $34.1 million, or $24.5 million, net of the change in cash, increasing out total debt repaid for the six months ended June 30, 2023, to $72.7 million, net of the change in cash. During the second quarter of 2023, we purchased $21.0 million of our 8.25% Senior Notes in open market purchases, reducing the outstanding balance of the 8.25% Senior Notes to $593.1 million. We have no debt maturities until the 8.25% Senior Notes mature in April 2026.

During 2023, we expect to invest $68.0 million to $71.0 million in capital expenditures, consisting of $36.0 million to $37.0 million in maintenance capital expenditures on real estate assets, $25.0 million to $26.0 million for maintenance capital expenditures on other assets and information technology, and $7.0 million to $8.0 million for other capital investments.

Supplemental Financial Information and Investor Presentations

We have made available on our website supplemental financial information and other data for the second quarter of 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Financial Information” of the Investors section. We do not undertake any obligation and disclaim any duties to update any of the information disclosed in this report.

Management may meet with investors from time to time during the third quarter of 2023. Written materials used in the investor presentations will also be available on our website beginning on or about August 28, 2023. Interested parties may access this information through our website at http://ir.corecivic.com/ under “Events & Presentations” of the Investors section.

Conference Call, Webcast and Replay Information

We will host a webcast conference call at 10:00 a.m. central time (11:00 a.m. eastern time) on Tuesday, August 8, 2023, which will be accessible through the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BI245ce05fd4c64a6ead7845124358177d. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and one of the largest prison operators in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Forward-Looking Statements

This press release contains statements as to our beliefs and expectations of the outcome of future events that are “forward-looking” statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from the statements made. These include, but are not limited to, the risks and uncertainties associated with: (i) changes in government policy, legislation and regulations that affect utilization of the private sector for corrections, detention, and residential reentry services, in general, or our business, in particular, including, but not limited to, the continued utilization of our correctional and detention facilities by the federal government, including as a consequence of the United States Department of Justice, or DOJ, not renewing contracts as a result of President Biden’s Executive Order on Reforming Our Incarceration System to Eliminate the Use of Privately Operated Criminal Detention Facilities, or the Private Prison EO, impacting utilization primarily by the BOP and the United States Marshals Service, and the impact of any changes to immigration reform and sentencing laws (we do not, under longstanding policy, lobby for or against policies or legislation that would determine the basis for, or duration of, an individual’s incarceration or detention); (ii) our ability to obtain and maintain correctional, detention, and residential reentry facility management contracts because of reasons including, but not limited to, sufficient governmental appropriations, contract compliance, negative publicity and effects of inmate disturbances; (iii) changes in the privatization of the corrections and detention industry, the acceptance of our services, the timing of the opening of new facilities and the commencement of new management contracts (including the extent and pace at which new contracts are utilized), as well as our ability to utilize available beds; (iv) general economic and market conditions, including, but not limited to, the impact governmental budgets can have on our contract renewals and renegotiations, per diem rates, and occupancy; (v) fluctuations in our operating results because of, among other things, changes in occupancy levels; competition; contract renegotiations or terminations; inflation and other increases in costs of operations, including a continuing rise in labor costs; fluctuations in interest rates and risks of operations; (vi) the impact resulting from the termination of Title 42, the federal government’s policy to deny entry at the United States southern border to asylum-seekers and anyone crossing the southern border without proper documentation or authority in an effort to contain the spread of the coronavirus and related variants, or COVID-19; (vii) our ability to successfully identify and consummate future development and acquisition opportunities and realize projected returns resulting therefrom; (viii) our ability to have met and maintained qualification for taxation as a real estate investment trust, or REIT, for the years we elected REIT status; and (ix) the availability of debt and equity financing on terms that are favorable to us, or at all. Other factors that could cause operating and financial results to differ are described in the filings we make from time to time with the Securities and Exchange Commission.

We take no responsibility for updating the information contained in this press release following the date hereof to reflect events or circumstances occurring after the date hereof or the occurrence of unanticipated events or for any changes or modifications made to this press release or the information contained herein by any third-parties, including, but not limited to, any wire or internet services.

NOTE TO SUPPLEMENTAL FINANCIAL INFORMATION

Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO, and, where appropriate, their corresponding per share metrics are non-GAAP financial measures. The Company believes that these measures are important operating measures that supplement discussion and analysis of the Company’s results of operations and are used to review and assess operating performance of the Company and its properties and their management teams. The Company believes that it is useful to provide investors, lenders and securities analysts disclosures of its results of operations on the same basis that is used by management.

FFO, in particular, is a widely accepted non-GAAP supplemental measure of performance of real estate companies, grounded in the standards for FFO established by the National Association of Real Estate Investment Trusts (NAREIT). NAREIT defines FFO as net income computed in accordance with GAAP, excluding gains (or losses) from sales of property and extraordinary items, plus depreciation and amortization of real estate and impairment of depreciable real estate and after adjustments for unconsolidated partnerships and joint ventures calculated to reflect funds from operations on the same basis. As a company with extensive real estate holdings, we believe FFO and FFO per share are important supplemental measures of our operating performance and believe they are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs and other real estate operating companies, many of which present FFO and FFO per share when reporting results. EBITDA, Adjusted EBITDA, and FFO are useful as supplemental measures of performance of the Company’s properties because such measures do not take into account depreciation and amortization, or with respect to EBITDA, the impact of the Company’s tax provision and financing strategies. Because the historical cost accounting convention used for real estate assets requires depreciation (except on land), this accounting presentation assumes that the value of real estate assets diminishes at a level rate over time. Because of the unique structure, design and use of the Company’s properties, management believes that assessing performance of the Company’s properties without the impact of depreciation or amortization is useful. The Company may make adjustments to FFO from time to time for certain other income and expenses that it considers non-recurring, infrequent or unusual, even though such items may require cash settlement, because such items do not reflect a necessary or ordinary component of the ongoing operations of the Company. Normalized FFO excludes the effects of such items. The Company calculates Adjusted Net Income by adding to GAAP Net Income expenses associated with the Company’s debt repayments and refinancing transactions, and certain impairments and other charges that the Company believes are unusual or non-recurring to provide an alternative measure of comparing operating performance for the periods presented.

Other companies may calculate Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO differently than the Company does, or adjust for other items, and therefore comparability may be limited. Adjusted Net Income, EBITDA, Adjusted EBITDA, FFO, and Normalized FFO and, where appropriate, their corresponding per share measures are not measures of performance under GAAP, and should not be considered as an alternative to cash flows from operating activities, a measure of liquidity or an alternative to net income as indicators of the Company’s operating performance or any other measure of performance derived in accordance with GAAP. This data should be read in conjunction with the Company’s consolidated financial statements and related notes included in its filings with the Securities and Exchange Commission.

Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms, and systems for United States National Security related customers, allies, and commercial enterprises. Kratos is changing the way breakthrough technologies for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research, and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training and combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.kratosdefense.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

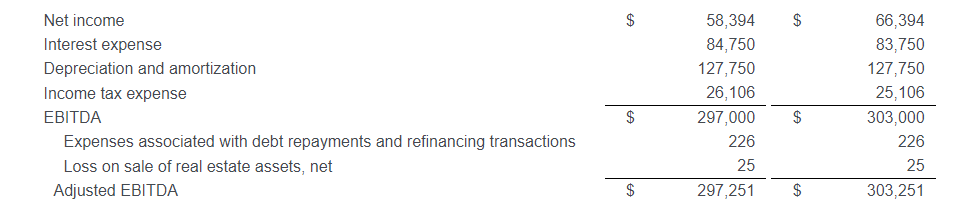

2Q23 Results. Results came in above expectations. Revenue totaled $256.9 million, up 14.6% y-o-y. Adjusted EBITDA came in at $21.6 million, up from $17.7 million in 2Q22. GAAP EPS loss was $0.02 and adjusted EPS was $0.09, compared to a EPS loss of $0.04 and adjusted EPS of $0.07, respectively, a year ago. We had forecasted $235 million, $16.5 million, $(0.03), and $0.06, respectively.

Solid Organic Growth In KGS. The Government Solutions Segment saw overall revenue increase 22.1% to $204.8 million. Organic growth for KGS grew 17.1% in the quarter, with organic growth across all businesses within KGS and notable increases in the Space and Satellite, Turbine Technologies, Microwave products, and C5ISR units.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Gray Television is a multimedia company headquartered in Atlanta, Georgia. We are the nation’s largest owner of top-rated local television stations and digital assets in the United States. Our television stations serve 113 television markets that collectively reach approximately 36 percent of US television households. This portfolio includes 80 markets with the top-rated television station and 100 markets with the first and/or second highest rated television station. We also own video program companies Raycom Sports, Tupelo Honey, PowerNation Studios and Third Rail Studios.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Patrick McCann, CFA, Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q2 results. The company reported Q2 revenue of $813 million, better than our estimate of $802 million; adj. EBITDA in the quarter was $225 million, beating our estimate of $187 million by 20%. Notably, Local and National core advertising revenues performed strongly, increasing in the low single-digits from the prior year period.

Positive momentum. In our view, the company’s Local and National core advertising growth was impressive, with many industry peers reporting declines. Notably, management highlighted that National and Local advertising are pacing up in Q3 as well. We believe the company has favorable operating momentum, given its resilient advertising revenues and expected influx of political revenue later this year and in 2024.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Energy Fuels reported 2023-2Q results in line with expectations as rare earth element carbonite sales expand. Uranium sales to a major nuclear utility kicked in and rare earth carbonate sales accelerated. Of note, uranium sales were done at an operating cost of $26.40/lb. below the price in our models. Also notable was an increase in REE sales after several quarters of sales being limited by monzanite supply issues.

With sales still in the early stages, operating line items were fairly predictable. Of course, the Energy Fuel story has never been about near-term results. Instead, the stock moves on corporate developments. And, while there have been some setbacks (REE supply issues, share dilution, foreign uranium supply competition), the company has made steady progress in recent quarters towards its goals.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

2Q23 Results. Total revenue of $463.7 million, better than our $463.1 million estimate, and up from $456.7 million last year. Adjusted EBITDA of $72.1 million compared to $78.8 million last year and our $73.2 million projection. Net income of $14.8 million, or EPS of $0.13, compared to $10.6 million, or EPS of $0.09, last year. We had forecast net income of $14.4 million, or $0.13 per share.

ICE, ICE Baby. The expiration of COVID related regulations in May has resulted in a 45% increase in ICE populations at CoreCivic facilities through July 31st. We would anticipate ICE populations to increase further as the border situations remains volatile, although politics make predictions challenging.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

For a small percentage of cancer patients, doctors are unable to determine where their cancer originated. This makes it much more difficult to choose a treatment for those patients, because many cancer drugs are typically developed for specific cancer types.

A new approach developed by researchers at MIT and Dana-Farber Cancer Institute may make it easier to identify the sites of origin for those enigmatic cancers. Using machine learning, the researchers created a computational model that can analyze the sequence of about 400 genes and use that information to predict where a given tumor originated in the body.

Using this model, the researchers showed that they could accurately classify at least 40 percent of tumors of unknown origin with high confidence, in a dataset of about 900 patients. This approach enabled a 2.2-fold increase in the number of patients who could have been eligible for a genomically guided, targeted treatment, based on where their cancer originated.

“That was the most important finding in our paper, that this model could be potentially used to aid treatment decisions, guiding doctors toward personalized treatments for patients with cancers of unknown primary origin,” says Intae Moon, an MIT graduate student in electrical engineering and computer science who is the lead author of the new study.

Mysterious Origins

In 3 to 5 percent of cancer patients, particularly in cases where tumors have metastasized throughout the body, oncologists don’t have an easy way to determine where the cancer originated. These tumors are classified as cancers of unknown primary (CUP).

This lack of knowledge often prevents doctors from being able to give patients “precision” drugs, which are typically approved for specific cancer types where they are known to work. These targeted treatments tend to be more effective and have fewer side effects than treatments that are used for a broad spectrum of cancers, which are commonly prescribed to CUP patients.

“A sizeable number of individuals develop these cancers of unknown primary every year, and because most therapies are approved in a site-specific way, where you have to know the primary site to deploy them, they have very limited treatment options,” Gusev says.

Moon, an affiliate of the Computer Science and Artificial Intelligence Laboratory who is co-advised by Gusev, decided to analyze genetic data that is routinely collected at Dana-Farber to see if it could be used to predict cancer type. The data consist of genetic sequences for about 400 genes that are often mutated in cancer. The researchers trained a machine-learning model on data from nearly 30,000 patients who had been diagnosed with one of 22 known cancer types. That set of data included patients from Memorial Sloan Kettering Cancer Center and Vanderbilt-Ingram Cancer Center, as well as Dana-Farber.

The researchers then tested the resulting model on about 7,000 tumors that it hadn’t seen before, but whose site of origin was known. The model, which the researchers named OncoNPC, was able to predict their origins with about 80 percent accuracy. For tumors with high-confidence predictions, which constituted about 65 percent of the total, its accuracy rose to roughly 95 percent.

After those encouraging results, the researchers used the model to analyze a set of about 900 tumors from patients with CUP, which were all from Dana-Farber. They found that for 40 percent of these tumors, the model was able to make high-confidence predictions.

The researchers then compared the model’s predictions with an analysis of the germline, or inherited, mutations in a subset of tumors with available data, which can reveal whether the patients have a genetic predisposition to develop a particular type of cancer. The researchers found that the model’s predictions were much more likely to match the type of cancer most strongly predicted by the germline mutations than any other type of cancer.

Guiding Drug Decisions

To further validate the model’s predictions, the researchers compared data on the CUP patients’ survival time with the typical prognosis for the type of cancer that the model predicted. They found that CUP patients who were predicted to have cancer with a poor prognosis, such as pancreatic cancer, showed correspondingly shorter survival times. Meanwhile, CUP patients who were predicted to have cancers that typically have better prognoses, such as neuroendocrine tumors, had longer survival times.

Another indication that the model’s predictions could be useful came from looking at the types of treatments that CUP patients analyzed in the study had received. About 10 percent of these patients had received a targeted treatment, based on their oncologists’ best guess about where their cancer had originated. Among those patients, those who received a treatment consistent with the type of cancer that the model predicted for them fared better than patients who received a treatment typically given for a different type of cancer than what the model predicted for them.

Using this model, the researchers also identified an additional 15 percent of patients (2.2-fold increase) who could have received an existing targeted treatment, if their cancer type had been known. Instead, those patients ended up receiving more general chemotherapy drugs.

“That potentially makes these findings more clinically actionable because we’re not requiring a new drug to be approved. What we’re saying is that this population can now be eligible for precision treatments that already exist,” Gusev says.

The researchers now hope to expand their model to include other types of data, such as pathology images and radiology images, to provide a more comprehensive prediction using multiple data modalities. This would also provide the model with a comprehensive perspective of tumors, enabling it to predict not just the type of tumor and patient outcome, but potentially even the optimal treatment.

Alexander Gusev, an associate professor of medicine at Harvard Medical School and Dana-Farber Cancer Institute, is the senior author of the paper, which appeared on August 7, 2023, in Nature Medicine.

Equity Research Allows Investors to More Confidently Step Away from the Growing Index Valuations

Hedge Fund Managers Michael Burry and Bill Ackman have expressed deep concern over indexed funds for a years and for different reasons. Burry primarily fears a bubble growing, and Ackman agrees but also fears investors are giving away control to parties that may not have their best interests at heart. Both make understandable cases. Below we discuss the overall concerns and how an individual investor who shares their concerns may “hedge” their portfolio against these risks.

Michael Burry

“The bubble in passive investing through ETFs and index funds as well as the trend to very large size among asset managers has orphaned smaller value-type securities globally,” Michael Burry told Bloomberg News in August of 2019. “Orphaned” presumably refers to a lack of attention now paid to this market segment.

Burry’s concerns centered around the idea that the rise of passive investing could lead to distortions in the stock market. He believed that as more and more investors put their money into indexed funds, the valuations of the companies included in those indices might become disconnected from their underlying fundamentals as fund managers were required to own the index at the established weighting. In his view, this could create a bubble-like situation where certain stocks are overvalued due to indiscriminate buying driven by the popularity of index funds.

While many view this hedge fund manager, made most famous by the movie The Big Short, as a pessimist, it is easy to think of him as an optimist finding opportunity, even where there could be trouble.

As he discussed then, the rush into indexed funds has punished small cap value stocks. Burry also highlighted, “There is all this opportunity, but so few active managers.”

Bill Ackman

“We believe that it is axiomatic that while capital flows will drive market values in the short term, valuations will drive market values over the long term. As a result, large and growing inflows to index funds, coupled with their market-cap driven allocation policies, drive index component valuations upwards and reduce their potential long-term rates of return,” according to Bill Ackman in a statement which agrees with Burry’s thoughts. Bull Bill Ackman also sees another risk.

In a letter to shareholders earlier this year, the activist investor, and big boss at Pershing Square Capital, made the point that the passive funds not only follow indexes but encourage active managers to stay close to the index where investors pay for active management, but get index-like results because the fund company fears shareholder reaction if returns deviates sharply from the index benchmark.

More telling is Ackaman’s fear of proxy votes and other governance taken out the hands of the masses and bestowed on so few. Ackman believes that passive managers like Vanguard, BlackRock, and State Street hurt investors by concentrating corporate power in a small group of players “who get larger by the minute.” With 20% or more of fund flows headed to an indexed fund or ETF, Ackman wonders who will “look out for one another’s interests?”

Actively Managed and Self-Directed Investing

The Nasdaq 100 index just reorganized in order to lessen potential risks to being overweighted in a few stocks. Surrounding this event and through the years there has been no shortage of discussion around index bubbles and why some see indexes as an eventual train wreck:

“Is There an Index Fund Bubble?” (Bloomberg, September 4, 2019)

“The Index Fund Bubble Is Coming” (The Motley Fool, January 23, 2020)

“Is the Index Fund Bubble About to Burst?” (Investopedia, March 11, 2021)

“The Index Fund Bubble Is Real, and It’s Going to Burst” (MarketWatch, April 20, 2022)

“The Index Fund Bubble Is Even Bigger Than You Think” (Barron’s, May 23, 2023)

And there is also fear in the consolidation of power into the hands of a few fund companies that could impact all of us more subtly.

While index fund investing is growing in popularity and has been rewarding, investors can prepare by scaling down these investments and making their own selections, weighting their portfolio in a way that makes more sense in light of the risks to them. This could include seeking managed funds with a manager that has a good track record over the years, but it also may mean adding stocks that are not well represented in major indexes. Investors like to use Morningstar for fund selection, for stocks information including excellent research on what Burry termed “small-cap value stocks,” and other small and microcap offerings is likely found on Channelchek.

Informed Decision-Making: Equity research reports provide detailed analysis and insights about a company’s financial performance, industry trends, competitive landscape, and growth prospects. Investors may save weeks putting together enough information to believe they understand an opportunity enough to make a decision.

Valuation Insights: Research reports will include valuation models that estimate a company’s intrinsic value. This can help investors understand whether a stock is overvalued, undervalued, or fairly priced, guiding their buy, sell, or hold decisions. Some research will actually provide an analyst’s price target.

Risk Assessment: Equity research reports assess the risks associated with an investment. This could include factors like regulatory changes, industry volatility, management quality, and financial stability. Understanding these risks helps investors manage their portfolios effectively.

Industry and Market Trends: Research reports not only focus on individual companies but also provide insights into broader industry trends and market dynamics. Investors can gain a better understanding of how macroeconomic factors might impact their investments.

Company Performance Analysis: Detailed financial analysis in these reports helps investors understand a company’s revenue streams, profit margins, debt levels, and growth potential. This information is crucial for evaluating a company’s overall financial health.

Competitive Landscape: Equity research reports often compare a company’s performance to its competitors. This analysis helps investors gauge a company’s competitive position within its industry.

Long-Term Investment Strategy: Investors with a long-term perspective can benefit from equity research by identifying companies with strong growth potential, sustainable competitive advantages, and solid management teams.

Industry Diversification: Research reports can make it easier for investors to diversify holdings by defining the category the company is in and even highlighting opportunities in various sectors or industries.

News Interpretation: Equity research reports can provide context and interpretation for press releases and other news including, earnings releases, and developments related to the company. This helps investors understand the potential impact on the stock price.

Investor Growth: For novice investors, equity research reports can provide valuable insights into how professionals analyze stocks and make investment decisions, enhancing their investment knowledge over time.

It’s important to note that equity research reports are typically produced by financial analysts working for brokerage firms, investment banks, or independent research firms. Investors should exercise critical thinking and compare and contrast multiple sources of information.

Take Away

Credible professional investors make the case that the surging assets in index funds are leading to a bubble. There is also concern that control is taken out of the hands of individuals and placed in the hands of a few large companies whose corporate interests may not match individual investor interests.

Taking back control of the management of one’s portfolio may seem daunting, but quality equity research is a tool that can serve to help the selection process while at the same time increasing the self-directed investors’ understanding of what is important to watch. Channelchek is a no-cost platform leading the way in North America, providing company-sponsored research on small and microcap stocks.

Individual stock investors may also wish to consider attending NobleCon19, in December. This investment conference is widely recognized as the place investors go to discover small emerging companies that they may act upon through their traditional brokerage account. Discover more about about NobleCon19 here.

Iconic Burger Chain to Triple State’s Footprint By 2033

LOS ANGELES, Aug. 07, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Johnny Rockets and 16 other restaurant concepts, announces a new development deal set to bring 20 new franchised Johnny Rockets locations to Texas in the next 10 years with the first unit set to open in 2024.

The brand currently operates a number of restaurants in the Lone Star State. The new locations will open in partnership with Brame Holdings LLC, featuring the classic fare that put the brand on the map over 35 years ago, including juicy, made-to-order burgers and hand-spun shakes.

“Brame Holdings LLC continues to be a great growth partner in Texas across the FAT Brands portfolio,” said Taylor Wiederhorn, Chief Development Officer of FAT Brands. “They are quickly developing many Fatburger and Buffalo’s Express locations in addition to Round Table Pizza locations which is part of an 80-store development deal for the state, the first of these stores are set to open soon in San Antonio. We are thrilled to extend our relationship with an experienced operator like Brame Holdings LLC, driving further domestic growth in Texas for another beloved, iconic brand of ours, Johnny Rockets.”

The first Johnny Rockets restaurant opened June 6, 1986 on Melrose Avenue in Los Angeles. Since that time, the chain’s timeless all-American brand has connected with customers across the U.S. and in 25 other countries around the globe.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets and develops fast casual, quick-service, casual and polished casual dining restaurant concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide. For more information on FAT Brands, please visit www.fatbrands.com.

About Johnny Rockets Founded in 1986 on Melrose Avenue in Los Angeles, Johnny Rockets is a world-renowned international franchise that offers high-quality, innovative menu items including Certified Angus Beef® cooked-to-order hamburgers, veggie burgers, chicken sandwiches, crispy fries, and rich, delicious hand-spun shakes and malts. With over 325 locations in over 25 countries around the globe, this dynamic lifestyle brand offers friendly service and upbeat music contributing to the chain’s signature atmosphere of relaxed, casual fun. For more information, visit www.johnnyrockets.com.

Forward Looking Statements This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings. Forward-looking statements reflect expectations of FAT Brands Inc. (“we”, “our” or the “Company”) concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that we file from time to time with the Securities and Exchange Commission, such as our reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.