Meta is continuing its aggressive expansion into artificial intelligence with the acquisition of Manus, a fast-growing AI startup, signaling the company’s intent to strengthen its position in an increasingly competitive AI landscape. The Facebook and Instagram parent company confirmed the deal this week, though it did not disclose financial terms. Multiple reports estimate the transaction value at more than $2 billion.

Manus, now headquartered in Singapore, gained industry attention earlier this year after launching a general-purpose AI agent designed to assist users with research, coding, and productivity-driven tasks. The platform operates on a subscription model and has experienced rapid adoption across both individual users and businesses. Within just eight months of launch, Manus surpassed $100 million in annual recurring revenue, highlighting strong market demand for its AI capabilities.

Meta described the acquisition as a strategic fit for its broader AI ambitions. The company plans to scale Manus’ technology across its ecosystem, including integration into Meta AI for both consumer and enterprise use cases. Importantly, Meta indicated that Manus will continue operating its existing services independently, allowing current users to retain access through the startup’s app and website.

Leadership at Manus emphasized continuity following the acquisition. The company views the partnership as an opportunity to grow on a more stable foundation while preserving its operational autonomy and product direction. This approach reflects Meta’s recent strategy of acquiring specialized AI teams while allowing them to maintain their core innovation culture.

The deal also carries geopolitical implications. Manus previously received backing from several Chinese-linked investors and originated from a company founded in China before relocating to Singapore. Meta confirmed that, following the acquisition, there will be no remaining Chinese ownership interests in Manus. The startup will also discontinue operations in China while continuing to expand from its Singapore base, where the majority of its workforce is located.

Meta’s move comes as CEO Mark Zuckerberg intensifies efforts to position the company at the forefront of artificial intelligence development. Facing stiff competition from rivals such as Google and OpenAI, Meta has made AI a central pillar of its long-term growth strategy. Earlier this year, the company made a multibillion-dollar investment in AI data firm Scale and recruited its CEO to help lead advanced AI research initiatives.

By bringing Manus under its umbrella, Meta gains a commercially proven AI platform and a rapidly scaling technology team. The acquisition reinforces Meta’s commitment to embedding AI across its products while accelerating innovation in intelligent agents that could reshape how users interact with digital platforms in the years ahead.

SoftBank Group Corp. has agreed to acquire DigitalBridge Group Inc. in a cash deal valuing the digital infrastructure investor at approximately $4 billion, including debt. The transaction underscores SoftBank founder Masayoshi Son’s renewed push to dominate the backbone of the artificial intelligence economy: data centers, computing power, and the infrastructure required to scale AI globally.

Under the terms of the agreement, SoftBank will pay $16 per share for New York–listed DigitalBridge, representing a roughly 15% premium to the firm’s closing price on December 26. Shares of DigitalBridge jumped nearly 10% following the announcement, trading just below the offer price. The deal is expected to close in the second half of 2026, subject to regulatory approvals.

DigitalBridge is one of the largest global investors dedicated exclusively to digital infrastructure, managing roughly $108 billion in assets as of September. Its portfolio includes a roster of major data center and connectivity platforms such as Vantage Data Centers, Switch Inc., AtlasEdge, DataBank, Yondr Group, and AIMS. By acquiring DigitalBridge, SoftBank gains not only physical infrastructure exposure but also deep relationships with institutional investors actively deploying capital into data center development worldwide.

The acquisition comes amid an unprecedented surge in demand for data centers, driven by the rapid adoption of generative AI and cloud computing. Major players across finance and technology have poured capital into the sector. BlackRock’s $40 billion purchase of Aligned Data Centers and Oracle’s multiyear agreement to provide OpenAI with up to 4.5 gigawatts of computing power highlight the scale of investment reshaping the industry.

For SoftBank, the deal fits squarely into Son’s long-term vision of building an AI-centric ecosystem. Earlier this year, SoftBank announced the $500 billion “Stargate” initiative alongside OpenAI, Oracle, and Abu Dhabi-backed MGX, aiming to develop large-scale data centers across the United States. While the project’s rollout has been slower than initially promised due to financing challenges and site selection disputes, the DigitalBridge acquisition strengthens SoftBank’s strategic positioning in the infrastructure layer of AI.

The deal may also pave the way for further consolidation. SoftBank has reportedly held discussions about acquiring Switch Inc., one of DigitalBridge’s portfolio companies, at a valuation approaching $50 billion including debt. If pursued, such a move would further cement SoftBank’s influence over critical AI infrastructure assets.

Despite its reputation for high-profile technology bets—such as Alibaba, Arm Holdings, and the ill-fated WeWork investment—SoftBank has prior experience in asset management. Its 2017 acquisition of Fortress Investment Group, later sold in 2024, demonstrated Son’s willingness to operate across both technology and investment platforms.

Funding the AI push has required difficult trade-offs. Son recently disclosed that SoftBank sold a $5.8 billion stake in Nvidia to reallocate capital toward broader AI investments. The DigitalBridge acquisition signals that SoftBank is betting heavily that control of digital infrastructure—not just software or chips—will define the next phase of the AI revolution.

ACCO Brands Corporation is one of the world’s largest designers, marketers and manufacturers of branded academic, consumer and business products. Our widely recognized brands include AT-A-GLANCE®, Esselte®, Five Star®, GBC®, Kensington®, Leitz®, Mead®, PowerA®, Quartet®, Rapid®, Rexel®, Swingline®, Tilibra®, and many others. Our products are sold in more than 100 countries around the world. More information about ACCO Brands, the Home of Great Brands Built by Great People, can be found at www.accobrands.com.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition. ACCO is acquiring EPOS, which provides a comprehensive range of premium enterprise wired and wireless headsets, and other audio solutions. The transaction enhances and broadens ACCO’s Kensington computer accessories portfolio into the large global enterprise headset category, estimated at $1.7 billion in size. We believe the acquisition aligns with management’s strategy to invest in markets with better growth profiles. The addition of EPOS will allow ACCO to deliver a more complete line of workspace technology accessory solutions to enterprise customers.

Details. The transaction is valued at $11.7 million, including up to $3.5 million in deferred payments, and will be funded by existing cash resources. The deal is expected to close in January 2026. EPOS generates approximately $80 million in annual revenue. ACCO expects to achieve cost synergies in the range of $10-$15 million over the next two years. ACCO expects to take approximately $7 million of restructuring charges. Management expects 2026 profit to be modestly positive.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

NEW YORK, December 22, 2025 /PRNewswire/ – Bit Digital, Inc. (Nasdaq: BTBT) (“Bit Digital” or the “Company”), a publicly traded digital asset platform focused on Ethereum-native treasury and staking strategies, today announced the appointment of Amanda Cassatt, founder and and Chief Executive Officer of Serotonin, to its Board of Directors effective January 1, 2026.

Cassatt previously served as Chief Marketing Officer at Consensys, the leading Ethereum software company, building the infrastructure, tools, and protocols that power the world’s largest decentralized ecosystem, where she helped shape early market narratives around Ethereum and its ecosystem. Serotonin is a services company for institutions and startups in the blockchain and crypto industry and has played a central role in introducing blockchain technologies to mainstream audiences.

The Company noted that Cassatt brings experience across digital assets, institutional adoption, and product strategy at a time when Bit Digital continues to expand its presence in Ethereum and AI infrastructure. Her perspective is expected to support the Company’s focus on productive digital asset strategies and compute-driven business models.

“I look forward to supporting the mission of making Ethereum and AI compute accessible to the public markets,” Cassat said. “I appreciate Bit Digital’s thoughtful, long-term approach to the assets and infrastructure that matter most for the future.”

”Amanda’s experience sits directly at the intersection of Bit Digital’s strategic priorities,“ said Sam Tabar, Chief Executive Officer of Bit Digital. “She brings a deep understanding of digital assets, infrastructure, and how emerging technologies are communicated to institutional audiences. As the market increasingly differentiates between speculative exposure and productive digital infrastructure, her perspective will be a valuable addition to the Board.”

With the addition of Cassatt, Bit Digital continues to strengthen its corporate governance and long-term strategic alignment as it executes on its Ethereum and AI-focused growth strategy.

About Bit Digital Bit Digital is a publicly traded digital asset platform focused on Ethereum-native treasury and staking strategies. The Company began accumulating and staking ETH in 2022 and now operates one of the largest institutional Ethereum staking infrastructures globally. Bit Digital’s platform includes advanced validator operations, institutional-grade custody, active protocol governance, and yield optimization. Through strategic partnerships across the Ethereum ecosystem, Bit Digital aims to deliver exposure to secure, scalable, and compliant access to onchain yield. Bit Digital also holds a majority equity stake in WhiteFiber (Nasdaq: WYFI), a leading AI infrastructure provider and HPC solutions. For additional information, please contact ir@bit-digital.com or follow us on LinkedIn or X.

Alphabet is making a decisive move to secure the energy backbone of its artificial intelligence ambitions. The Google parent announced it will acquire clean energy developer Intersect in a $4.75 billion cash deal, including assumed debt, underscoring how access to power has become a strategic priority in the global AI race.

The acquisition comes as Big Tech companies pour billions into expanding computing capacity to support generative AI models, cloud services, and data centers — all of which require enormous and reliable amounts of electricity. As U.S. power grids strain to keep pace with surging demand, technology firms are increasingly turning upstream, investing directly in energy generation rather than relying solely on utilities.

Intersect brings scale that few developers can match. The company has roughly $15 billion in assets that are either operating or under construction, with projects expected to deliver about 10.8 gigawatts of power by 2028. That capacity is more than twenty times the electricity generated by the Hoover Dam, highlighting the magnitude of energy now required to sustain AI-driven growth.

Under the agreement, Alphabet will acquire Intersect’s energy and data center projects that are currently under development or construction. These assets are designed to support large-scale computing infrastructure, aligning closely with Google’s expanding network of U.S. data centers. Intersect’s operations will remain separate from Alphabet, preserving operational independence while strategically supporting Google’s long-term power needs.

Notably, Intersect’s existing operating assets in Texas and its operating and in-development projects in California will not be included in the deal. Those assets will continue as an independent business backed by existing investors. Among them is Quantum, a clean energy storage system in Texas built directly alongside a Google data center campus — a model increasingly favored by hyperscalers seeking to pair computing facilities with on-site or adjacent power sources.

The deal builds on Alphabet’s broader push into energy partnerships. Earlier this month, NextEra Energy expanded its collaboration with Google Cloud to develop new energy supplies across the U.S. Together, these moves signal a shift in how tech giants approach infrastructure: energy security is no longer a background consideration, but a core component of competitive advantage.

For Alphabet, the acquisition also reinforces its commitment to clean energy. As AI workloads expand, the environmental footprint of data centers has drawn scrutiny from regulators and investors alike. By investing directly in renewable generation and energy storage, Alphabet aims to mitigate emissions while insulating itself from grid bottlenecks, price volatility, and regulatory risk.

Intersect will also explore emerging energy technologies to diversify supply, according to Alphabet, positioning the company to adapt as AI-driven electricity demand continues to grow. This forward-looking approach reflects a broader industry trend, where control over power generation is becoming just as critical as control over chips, data, and algorithms.

Ultimately, Alphabet’s purchase of Intersect highlights a defining reality of the AI era: the battle for intelligence is also a battle for energy. As demand accelerates, companies that can secure scalable, reliable, and clean power may hold a decisive edge in shaping the future of technology.

Oracle (ORCL) shares jumped roughly 8% Friday after the cloud computing company confirmed it will join a group of investors set to lead TikTok’s U.S. operations, a move that eases national security concerns and removes a major overhang for the popular social media platform. The rally marked a sharp reversal for Oracle stock, which has faced heightened volatility in recent weeks amid broader uncertainty around artificial intelligence infrastructure spending.

According to an internal memo sent to employees, TikTok’s U.S. business will be operated through a new joint venture that includes Oracle, private equity firm Silver Lake, and Abu Dhabi-based investment group MGX. The deal is expected to close on January 22 and is designed to comply with U.S. legislation requiring ByteDance, TikTok’s China-based parent company, to divest control of the app’s U.S. operations.

The agreement effectively prevents a potential shutdown or ban of TikTok in the United States, which had loomed after President Joe Biden signed legislation mandating divestiture over national security concerns. President Donald Trump previously extended deadlines for a deal multiple times and approved a potential framework through an executive order earlier this year, setting the stage for the current agreement.

Under the terms outlined in the memo, Oracle will play a critical role in ensuring compliance with U.S. national security requirements. The company will be responsible for auditing and validating that TikTok adheres to agreed-upon safeguards, including how sensitive U.S. user data is handled and stored. Oracle’s cloud infrastructure will house this data, reinforcing the company’s position as a trusted enterprise technology provider.

While China has not formally confirmed the transaction, reports from Chinese state media suggest the deal is expected to move forward. Commentary cited by CNBC indicates the structure aligns with Chinese regulations and does not constitute a sale of TikTok’s core recommendation algorithm, a key sticking point in past negotiations.

Investors responded positively to the announcement, viewing it as both a strategic win and a stabilizing development for Oracle. In a note to clients, Evercore ISI described the move as a “nice win” for the cloud provider, highlighting potential upside as the market reassesses Oracle’s longer-term growth outlook. The firm suggested that the recent pullback in shares may present an attractive entry point for investors with a six- to twelve-month time horizon.

The TikTok news arrives after a turbulent period for Oracle stock. Shares have been pressured by concerns over the sustainability of the artificial intelligence trade and the capital intensity required to build out large-scale AI data centers. Earlier this week, Oracle shares slid following reports that negotiations over a $10 billion data center deal with Blue Owl Capital had stalled, amplifying investor anxiety about funding risks tied to AI infrastructure expansion.

Despite Friday’s rally, Oracle stock remains down more than 20% over the past month, reflecting the market’s reassessment of high-multiple tech names. Year to date, however, shares are still up about 8%, underscoring the company’s ability to rebound when strategic clarity emerges.

Oracle’s involvement in TikTok’s U.S. operations reinforces its growing role at the intersection of cloud computing, data security, and large-scale digital platforms. While questions around AI spending persist, the TikTok partnership offers a timely boost to sentiment and highlights Oracle’s relevance in high-profile, mission-critical technology deals.

Management Anticipates Significant Growth in Target Channel During 2026

Driven by Strong Demand, SKYX Expects Additional Winter Launches at Several Other Leading U.S. Retailers and Big-Box Chains

Management Expects the Turbo Heater & Ceiling Fan to Generate Significant Revenue Beginning this Winter and Continuing throughout Fiscal Year 2026

The Company Anticipates that the Winter Launch Will Advance its Path to Cash-Flow Positivity

The Ceiling Fan and Space Heater Categories Represent a Multi-Billion-Dollar Annual Market, with Tens of Millions of Units Sold Each Year in North America

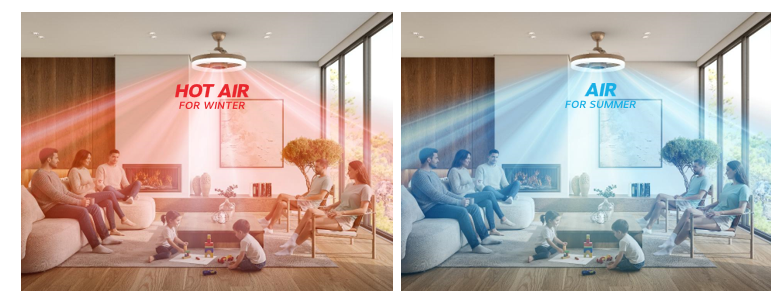

MIAMI, Dec. 18, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced it will launch its newly patented all-in-one ceiling plug & play SKYFAN & TURBO HEATER at U.S. leading retailer Target. Management anticipates significant growth in its Target business during 2026.

The innovative product—combining a ceiling fan with a built-in turbo heater—offers a safer, more efficient alternative to traditional space heaters and addresses a large year-round market opportunity across both winter and summer seasons. The combined ceiling fan and portable heater category is a multi-billion-dollar market, with tens of millions of units sold annually in North America.

In response to strong demand, SKYX intends to offer the product in six colors to serve both residential and commercial markets. Production is now underway with the Company’s manufacturing partners, and SKYX expects to continue its broad rollout in Q4 2025 and Q1 2026 to align with the winter season.

To view a video of SKYX’s turbo heater ceiling fan Click here

Rani Kohen, Founder and Executive Chairman of SKYX Platforms Corp., stated; “We are excited to begin launching our ceiling SKYFAN and Turbo Heater at a leading retailer such as Target, and we expect to continue expanding our presence across additional leading retailers and big-box chains. This product exemplifies our commitment to innovation, safety, and scalable global solutions. We believe this all-in-one offering will drive meaningful value for customers, partners, and shareholders.”

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target,” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

Office Depot, Inc., together with its subsidiaries, supplies a range of office products and services. It offers merchandise, such as general office supplies, computer supplies, business machines and related supplies, and office furniture through its chain of office supply stores under the Office Depot, Foray, Ativa, Break Escapes, Worklife, and Christopher Lowell brand names. The company also provides graphic design, printing, reproduction, mailing, shipping, and other services through design, print, and ship centers. It has operations throughout North America, Europe, Asia, and Central America. The company also sells its products and services through direct mail catalogs, contract sales force, Internet sites, and retail stores, through a mix of company-owned operations, joint ventures, licensing and franchise agreements, alliances, and other arrangements. As of December 31, 2008, Office Depot operated 1,267 North American retail division office supply stores and 162 international division retail stores, as well as participated under licensing and merchandise arrangements in 98 stores. The company was founded in 1986 and is based in Boca Raton, Florida.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Acquisition Approved. On December 5th, The ODP Corporation held a special meeting of stockholders at which holders of ODP’s common stock approved the acquisition of ODP by an affiliate of Atlas Holdings for $28 per share. With shareholder approval, the acquisition is expected to be completed on December 10th, at which time ODP common shares will cease to trade.

Details. Of the 30,117,856 shares of ODP Common Stock issued and outstanding at the close of business on October 21, 2025, the record date for the ODP Special Meeting, 22,656,187 shares were present or represented by proxy at the ODP Special Meeting. A total of 22,540,259 shares voted in favor of the acquisition.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Driven by Strong Demand, the Company Expects Additional Winter Launches with Several Leading U.S. Retailers, Including Big-Box Chains

Management Expects the Turbo Heater & Ceiling Fan to Generate Significant Revenue Beginning this Winter and Continuing through Fiscal Year 2026

The Company Anticipates that the Winter Launch Will Help Advance its Path to Cash-Flow Positivity

Ceiling Fan and Space Heater Categories Represent a Multi-Billion-Dollar Annual Market, with Tens of Millions of Units Sold Each Year in the U.S.

MIAMI, Dec. 03, 2025 (GLOBE NEWSWIRE) — SKYX Platforms Corp. (NASDAQ: SKYX) (d/b/a SKYX Technologies) (the “Company” or “SKYX”), a highly disruptive platform technology company with over 100 pending and issued patents globally and over 60 lighting and home décor websites, with a mission to make homes and buildings become safe and smart as the new standard, today announced the launch of its newly patented all-in-one ceiling plug & play SKYFAN & TURBO HEATER on its U.S. e-commerce website platform.

The innovative product—combining a ceiling fan with a built-in turbo heater—offers a safer, more efficient alternative to traditional space heaters and addresses a large year-round market opportunity across both winter and summer seasons. The combined ceiling fan and portable heater category is a multi-billion-dollar market, with tens of millions of units sold annually in the U.S. alone.

In response to strong demand, SKYX will offer the product in six colors to serve both residential and commercial markets. Production is now underway with the Company’s manufacturing partners, and SKYX expects a broad rollout in Q4 2025 and Q1 2026 to align with the winter season.

Huey Long, CEO of SKYX’s eCommerce Platform Belami,stated: “We’re excited to introduce the SkyFan Turbo Heater, a breakthrough product that launches an entirely new category of heater-fans for our customers. This innovation brings year-round comfort and design together in a single solution, expanding the possibilities for how people heat, cool, and light their indoor and outdoor spaces.”

Rani Kohen, Founder and Executive Chairman of SKYX Platforms Corp., stated: “We are experiencing great interest in our turbo heater and ceiling fan from both U.S. and global markets. This product exemplifies our commitment to innovation, safety, and global market products. As we prepare for our upcoming launch, we believe this all-in-one solution will drive significant value for our customers, partners, and shareholders.”

To view a video of SKYX’s turbo heater ceiling fan Click here.

About SKYX Platforms Corp.

As electricity is a standard in every home and building, our mission is to make homes and buildings become safe-advanced and smart as the new standard. SKYX has a series of highly disruptive advanced-safe-smart platform technologies, with over 100 U.S. and global patents and patent pending applications. Additionally, the Company owns over 60 lighting and home decor websites for both retail and commercial segments. Our technologies place an emphasis on high quality and ease of use, while significantly enhancing both safety and lifestyle in homes and buildings. We believe that our products are a necessity in every room in both homes and other buildings in the U.S. and globally. For more information, please visit our website at https://skyplug.com/ or follow us on LinkedIn.

Forward-Looking Statements

Certain statements made in this press release are not based on historical facts but are forward-looking statements. These statements can be identified by the use of forward-looking terminology such as “aim,” “anticipate,” “believe,” “can,” “could,” “continue,” “estimate,” “expect,” “evaluate,” “forecast,” “guidance,” “intend,” “likely,” “may,” “might,” “objective,” “ongoing,” “outlook,” “plan,” “potential,” “predict,” “probable,” “project,” “seek,” “should,” “target” “view,” “will,” or “would,” or the negative thereof or other variations thereon or comparable terminology, although not all forward-looking statements contain these words. These statements reflect the Company’s reasonable judgment with respect to future events and are subject to risks, uncertainties and other factors, many of which have outcomes difficult to predict and may be outside our control, that could cause actual results or outcomes to differ materially from those in the forward-looking statements. Such risks and uncertainties include statements relating to the Company’s ability to successfully launch, commercialize, develop additional features and achieve market acceptance of its products and technologies and integrate its products and technologies with third-party platforms or technologies; the Company’s efforts and ability to drive the adoption of its products and technologies as a standard feature, including their use in homes, hotels, offices and cruise ships; the Company’s ability to capture market share; the Company’s estimates of its potential addressable market and demand for its products and technologies; the Company’s ability to raise additional capital to support its operations as needed, which may not be available on acceptable terms or at all; the Company’s ability to continue as a going concern; the Company’s ability to execute on any sales and licensing or other strategic opportunities; the possibility that any of the Company’s products will become National Electrical Code (NEC)-code or otherwise code mandatory in any jurisdiction, or that any of the Company’s current or future products or technologies will be adopted by any state, country, or municipality, within any specific timeframe or at all; risks arising from mergers, acquisitions, joint ventures and other collaborations; the Company’s ability to attract and retain key executives and qualified personnel; guidance provided by management, which may differ from the Company’s actual operating results; the potential impact of unstable market and economic conditions on the Company’s business, financial condition, and stock price; and other risks and uncertainties described in the Company’s filings with the Securities and Exchange Commission, including its periodic reports on Form 10-K and Form 10-Q. There can be no assurance as to any of the foregoing matters. Any forward-looking statement speaks only as of the date of this press release, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by U.S. federal securities laws.

STAMFORD, Conn.–(BUSINESS WIRE)– Information Services Group (ISG) (Nasdaq: III), a global AI-centered technology research and advisory firm, has launched a research study examining provider capabilities within the fast-growing Snowflake services ecosystem.

The study results will be published in a comprehensive ISG Provider Lens® report, called Snowflake Ecosystem Partners, scheduled to be released in June 2026. The report will cover companies offering Snowflake-focused modernization and AI and ML enablement capabilities, along with ongoing managed data and optimization services.

Enterprise buyers will be able to use information from the report to evaluate their current vendor relationships, potential new engagements and available offerings, while ISG advisors use the information to recommend providers to the firm’s buy-side clients.

Snowflake has emerged as a critical data platform that redefines how enterprises store, process and activate data for analytics and AI. Its cloud-native architecture offers improved scalability, flexibility and cost efficiency, helping enterprises move beyond the constraints of traditional data warehouses. Globally, enterprises are increasingly adopting this platform to unify structured, semi-structured and unstructured data under a single governance and security model. This approach streamlines complex data operations while enabling faster insights and AI-driven innovation.

“Enterprises are prioritizing providers that offer automation maturity, FinOps discipline and robust governance,” said Aman Munglani, senior director and principal analyst at ISG. “Using Snowflake-native tools such as Snowpark, Cortex AI and Native Apps enables them to achieve meaningful, measurable improvements in data management.”

ISG has distributed surveys to more than 100 Snowflake ecosystem partners. Working in collaboration with ISG’s global advisors, the research team will produce two quadrants representing the Snowflake offerings the typical enterprise is buying, based on ISG’s experience working with its clients. The two quadrants are:

Modernization and AI/ML Enablement Services, evaluating providers that deliver end-to-end strategy, advisory and implementation support to help enterprises get the most from their Snowflake investments. These providers are assessed on their ability to guide data modernization efforts and facilitate integration of AI and ML into operations.

Managed Data and Optimization Services,assessing providers offering management, monitoring and optimization services for Snowflake environments. These providers should specialize in managing Snowflake infrastructure across cloud platforms and offer training and change management initiatives.

Geographically focused reports from the study will cover the global Snowflake ecosystem and examine products and services available worldwide. ISG analysts Gowtham Kumar Sampath and Hemangi Patel will serve as authors of the report.

A list of identified providers and vendors and further details on the study are available in this digital brochure. Companies not listed as Snowflake ecosystem partners can contact ISG and ask to be included in the study.

All 2025 ISG Provider Lens® evaluations feature expanded customer experience (CX) data that measures actual enterprise experience with specific provider services and solutions, based on ISG’s continuous CX research.

About ISG Provider Lens® Research

The ISG Provider Lens® Quadrant research series is the only service provider evaluation of its kind to combine empirical, data-driven research and market analysis with the real-world experience and observations of ISG’s global advisory team. Enterprises will find a wealth of detailed data and market analysis to help guide their selection of appropriate sourcing partners, while ISG advisors use the reports to validate their own market knowledge and make recommendations to ISG’s enterprise clients. The research currently covers providers offering their services globally, across Europe, as well as in the U.S., Canada, Mexico, Brazil, the U.K., France, Benelux, Germany, Switzerland, the Nordics, Australia and Singapore/Malaysia, with additional markets to be added in the future. For more information about ISG Provider Lens research, please visit this webpage.

About ISG

ISG (Nasdaq: III) is a global AI-centered technology research and advisory firm. A trusted partner to more than 900 clients, including 75 of the world’s top 100 enterprises, ISG is a long-time leader in technology and business services that is now at the forefront of leveraging AI to help organizations achieve operational excellence and faster growth. The firm, founded in 2006, is known for its proprietary market data, in-depth knowledge of provider ecosystems, and the expertise of its 1,600 professionals worldwide working together to help clients maximize the value of their technology investments.

French artificial intelligence startup Mistral has introduced a new suite of advanced AI models, marking its most ambitious step yet as it races to remain competitive with global heavyweights like OpenAI, Google, and DeepSeek. The release comes at a pivotal moment in the AI ecosystem, where rapid innovation cycles and aggressive commercialization strategies are reshaping the landscape.

Mistral’s updated portfolio includes a new large multimodal model, which the company describes as the “world’s best open-weight multimodal and multilingual.” Designed for enterprise-grade performance, this model targets use cases such as AI assistants, scientific workloads, retrieval-augmented generation (RAG) systems, and complex agentic workflows. By pushing for open-weight access, Mistral continues to position itself as a key proponent of transparent and customizable AI—an increasingly important stance among European enterprises wary of closed-source dominance from U.S. labs.

Alongside the flagship model, the company launched Ministral 3, a compact, highly efficient model engineered for robotics, autonomous drones, consumer devices, and on-device intelligence. Its smaller footprint allows it to run on a single GPU, reducing operational costs and making it attractive for companies seeking scalable, low-latency AI without heavy cloud dependency. According to Mistral, smaller models offer major advantages in real-world applications, where speed, cost efficiency, and domain-specific tuning outperform size alone.

The launches build on a year of rapid growth for the Paris-based startup. Founded in 2023, Mistral raised 1.7 billion euros in September, reaching a valuation of 11.7 billion euros. The round was led by global semiconductor leader ASML, which invested 1.3 billion euros, with additional backing from Nvidia, Microsoft, and Andreessen Horowitz. This massive inflow of capital reflects Europe’s mounting urgency to develop AI champions capable of competing with U.S. and Chinese giants.

Mistral’s momentum extends beyond research. On Monday, the company announced a major commercial agreement with HSBC, granting the global bank access to its models for tasks such as financial forecasting, language translation, and automation. The startup has already secured additional enterprise contracts worth hundreds of millions of dollars, signaling growing trust from large organizations seeking alternatives to entrenched U.S. players.

Still, the competitive backdrop is intense. Rivals such as Anthropic and OpenAI are aggressively expanding into Europe, opening new offices and securing colossal funding rounds that dwarf those of European firms. With Anthropic now valued at $183 billion and OpenAI reportedly priced at nearly $500 billion through secondary sales, Mistral faces an uphill battle to match the scale of global rivals.

Nonetheless, the company maintains that the next era of AI will be defined not only by size, but by speed, adaptability, on-device intelligence, and openness. With its new models, Mistral aims to position itself at the forefront of this shift—advancing its vision of a globally distributed AI ecosystem that blends cutting-edge research with practical enterprise deployment.

Amazon has introduced its newest AI semiconductor, Trainium3, signaling another major push by tech giants to loosen Nvidia’s grip on the rapidly growing artificial intelligence hardware market. Announced Tuesday during Amazon Web Services’ annual re:Invent conference, the chip represents a significant leap in the company’s strategy to build affordable, high-performance computing infrastructure tailored for AI training and inference.

According to AWS, servers outfitted with Trainium3 deliver four times the speed and energy efficiency of the previous generation. For enterprises racing to scale large language models and multimodal systems, this improvement translates to faster development cycles and noticeably lower operational costs—an increasingly critical advantage as AI workloads explode.

“Trainium already represents a multibillion-dollar business today and continues to grow really rapidly,” said AWS CEO Matt Garman, underscoring Amazon’s deepening investment in custom silicon. Once primarily dependent on Nvidia for its cloud AI capacity, AWS now sees homegrown hardware as essential both for performance control and long-term cost stability.

Amazon is far from alone. The industry has entered a new era in which Nvidia’s largest customers—Google, Microsoft, Meta, and Amazon itself—are designing their own AI chips to reduce reliance on the GPU leader. In early November, Google debuted its Ironwood TPU v7, and reports suggest the company is negotiating a multibillion-dollar deal to supply TPUs to Meta. Meanwhile, Microsoft continues to develop its in-house silicon despite encountering delays.

AWS executives view this diversification as healthy for the broader ecosystem. “Diversity of chips in the AI market is a good thing,” said Dave Brown, AWS vice president of compute and machine learning, in an interview with Yahoo Finance. Brown emphasized that the rising demand for AI infrastructure is creating room for multiple architectures to coexist, each optimized for different workloads.

Cost remains one of Amazon’s sharpest competitive angles. Brown noted that developers using Trainium-based instances typically see 30% to 40% savings compared to Nvidia GPU clusters. At a time when AI model training can reach hundreds of millions—or even billions—of dollars, these savings could shift market dynamics.

Amazon is also expanding its AI infrastructure at massive scale. The company recently completed Project Rainier, a colossal data center initiative built specifically for AI workloads. OpenAI competitor Anthropic is expected to use one million of Amazon’s custom chips across Rainier and other AWS data centers by the end of 2025. Anthropic has reportedly played a hands-on role in guiding the chip’s design.

Still, Nvidia remains unmatched in both raw performance and software ecosystem maturity. CEO Jensen Huang has argued that developers would choose Nvidia chips “even if alternatives were free,” citing CUDA and the extensive tools built around Nvidia hardware. Amazon itself remains one of Nvidia’s biggest customers, accounting for 7.5% of Nvidia’s revenue, and OpenAI recently signed a $38 billion agreement to access Nvidia GPUs through AWS.

Yet Amazon is preparing for a future where its chips coexist seamlessly with Nvidia’s. The company revealed that its upcoming Trainium4 processors will support NVLink Fusion, Nvidia’s advanced networking technology that links chips across server racks. That compatibility signals a hybrid future—one where Amazon tightens control over its hardware roadmap while still acknowledging Nvidia as the industry’s gold standard.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Review. In the third quarter, Bit Digital continued its transformation into an ETH focused treasury firm. Management continued its orderly wind-down of the bitcoin mining business, while the WhiteFiber holding has significant upside potential, in our view. Management has successfully guided the Company through past periods of volatility, and we believe they will be successful once again.

ETH. ETH prices remain volatile, currently trading just above $3,000, down from the $4,800 level at the end of the summer. However, as the backbone of decentralized finance (DeFi), NFTs (non-fungible tokens), and numerous blockchain-based platforms, industry experts expect the demand for ETH to grow over time, positively impacting the long-term price.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.