Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 Results Reflect Commercialization Transition. Figure #1 Q1 Results highlight Xcel Brands’ transition from a portfolio development phase into active commercialization, as the company began rolling out several influencer-led brands across livestream commerce, retail, and digital channels. While near-term financial results remained pressured by launch timing, the quarter marked an important operational inflection point.

Mesa Mia Launch Served as Key Growth Driver: The debut of Mesa Mia by Jenny Martinez on HSN represented the quarter’s most important strategic development, validating Xcel’s creator-commerce model by leveraging Martinez’s large social following, culturally authentic content, and integrated omnichannel distribution strategy spanning HSN, social commerce, and retail expansion.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Retail distribution. On May 7, the company announced additional details regarding the initial phase of its retail distribution strategy for Shakeology, which is scheduled to launch in more than 80 Sprouts Farmers Market locations on May 18. Notably, the company secured a strategic partnership with KeHE Distributors, a national distributor specializing in organic, fresh, and specialty products, with distribution spanning more than 30,000 retail locations.

Details. For its initial rollout in the retail market, the company will be selling a convenient seven-serving bag of Shakeology for the first time. The seven-serving bag is priced at $34.99 and available in four flavors. Additionally, each Shakeology purchase also includes access to BODi’s digital fitness platform, supporting the company’s cross-over strategy. While Shakeology has never been sold in retail locations, it has generated more than $4 billion in direct-to-consumer sales and delivered more than 1 billion servings since its release in 2009.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 reflects cost discipline. Fiscal Q3 revenue declined 11.6% to $293.0 million, driven by disciplined marketing spend and traffic headwinds, particularly within Consumer Floral & Gifts. Despite the top-line decline, gross margin expanded 150 basis points to 33.2%, and adjusted EBITDA improved to a loss of $(31.2) million from $(34.9) million in the prior year period, reflecting early benefits from cost initiatives and pricing discipline

Underlying segment-level profitability. While demand remains pressured, profitability improved across key segments. Consumer Floral & Gifts delivered higher contribution margins despite revenue declines, and Gourmet Foods & Gift Baskets narrowed losses, reflecting better cost controls and operational efficiencies. These trends suggest that management’s focus on marketing efficiency, pricing discipline, and cost rationalization is beginning to gain traction.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Spirit Airlines is gone. In the early morning hours of May 2, 2026, the ultra-low-cost carrier that helped reshape American air travel for more than three decades ceased all global operations, effective immediately — becoming the first major U.S. airline to go out of business due to financial failure in 25 years.

The collapse came after a last-ditch effort to secure a $500 million government bailout fell apart. The Trump administration had proposed a rescue package that would have given the federal government a stake of up to 90% in the airline, but a key group of bondholders rejected the deal. With no financial lifeline and no runway left, Spirit pulled the plug overnight — canceling all flights, shutting down customer service, and leaving thousands of passengers stranded at airports across the country.

Spirit’s downfall wasn’t a single event — it was a slow unraveling. The airline had filed for bankruptcy twice since 2024, each time attempting to emerge leaner and more competitive. But the math stopped working. Soaring jet fuel costs driven by the U.S.-Iran conflict hit low-cost carriers hardest, and Spirit’s core competitive advantage — the ability to undercut legacy airlines on price — had been steadily eroded.

The bigger carriers had watched Spirit’s playbook for years and eventually adopted it themselves, rolling out their own basic economy fares and stripping down ticket prices on key routes. When the major airlines started playing Spirit’s game, Spirit had little left to differentiate itself. A proposed $3.8 billion merger with JetBlue in 2023 was blocked by the Department of Justice on antitrust grounds — a decision that, in hindsight, may have sealed the airline’s fate.

By February 2026, Spirit’s market share had already slipped to under 4% of U.S. passengers, and projections for May had it falling to 1.8%. The writing had been on the wall for some time.

The closure leaves a real void, and consumers are likely to feel it — whether they ever flew Spirit or not. At its peak, Spirit operated roughly 300 flights per day, serving price-sensitive travelers across the U.S., Caribbean, and Latin America. That capacity doesn’t simply disappear; it creates an opening for surviving carriers to fill — and price accordingly.

In the immediate aftermath, United, Delta, Southwest, JetBlue, and American all moved to cap fares at roughly $200 one-way to absorb stranded Spirit customers. That goodwill is likely short-lived. Once the dust settles, the removal of an aggressive low-fare competitor from key routes historically results in higher average ticket prices across the board. Consumers flying routes that Spirit served — particularly leisure-heavy markets in Florida, the Caribbean, and secondary cities — should expect less pricing pressure moving forward.

The airline’s shutdown also puts 17,000 direct and indirect jobs at risk, including 14,000 Spirit employees. While major carriers have opened hiring pipelines and extended travel benefits to displaced workers, the broader labor impact on aviation support industries at affected airports remains to be seen.

Spirit’s collapse creates a consolidation opportunity for surviving ultra-low-cost carriers. Frontier Airlines, Avelo, and Allegiant now stand to absorb market share on routes where Spirit had been the primary budget option. Fleet assets, airport gate slots, and route authorities will become valuable commodities as Spirit winds down through bankruptcy proceedings.

For the broader airline industry, this moment raises a pointed question about the long-term viability of the ultra-low-cost model in a post-pandemic, high-fuel-cost environment. When legacy carriers can effectively replicate your pricing strategy, and geopolitical shocks can wipe out your margin overnight, the business case becomes nearly impossible to sustain.

Spirit may have been the butt of every travel meme for years — but its presence kept prices honest. With those yellow planes grounded for good, budget-conscious travelers will be the ones paying the price.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results reflect steady growth with investment-driven earnings pressure. Revenue increased 5% year-over-year to $24.3 million, in line with our estimate, while adj. EBITDA beat our estimate ($3.5 million versus our estimate of $2.9 million). EPS declined modestly as the company continued to prioritize member acquisition, highlighting the trade-off between near-term profitability and long-term value creation.

Subscription growth and renewals drove the quarter. Record membership renewals and continued Club Member acquisition were key drivers, reinforcing the strength of the subscription model and improving underlying unit economics despite upfront marketing costs. Membership Fee revenue, which represented 19% of total company revenue, increased by a solid 91%.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

The University of Michigan’s final April Consumer Sentiment reading came in at 49.8 — beating the 48.5 economists anticipated, but landing in a place no one wanted to be: the lowest level ever recorded. That means Americans right now are more anxious about their economic futures than during the 2008 financial crisis, the depths of the COVID-19 pandemic, or the inflation surge that followed Russia’s invasion of Ukraine.

The data reflects the ongoing economic disruption triggered by the U.S.-Iran conflict, which has driven gas prices up by more than a dollar per gallon on average since hostilities began. A two-week ceasefire temporarily softened the blow, and sentiment did improve slightly as a result. But survey director Joanne Hsu made clear in the release that diplomatic moves which don’t translate into actual relief at the pump — or lower prices on store shelves — aren’t enough to meaningfully shift consumer confidence.

That’s the core challenge here. Stocks have hit record highs this week, and the ceasefire offered a moment of cautious optimism. Yet sentiment fell across every demographic measured — age, income, education level, and political affiliation. That kind of across-the-board deterioration signals something broader than partisan frustration or market volatility. It points to a deeply embedded anxiety about where prices are headed.

The inflation data reinforces that concern. Year-ahead inflation expectations jumped to 4.7% in April, up from 3.8% in March — the largest single-month increase since April 2025, when sweeping tariff announcements rattled markets. Long-term inflation expectations climbed to 3.5%, the highest mark since last October. For context, both of these figures were well below 3% during the relatively stable 2019–2020 period. Americans don’t just feel squeezed now — they expect to keep feeling squeezed.

This disconnect between a rallying stock market and cratering consumer confidence is worth paying close attention to. Equity valuations often price in future optimism, but consumer sentiment is a more direct measure of how households — the engine of U.S. consumer spending, which drives roughly 70% of GDP — are actually behaving and planning. When confidence erodes to record lows, it tends to translate into deferred purchases, tighter household budgets, and reduced risk-taking across the board.

For investors tracking small and microcap equities, the downstream effects of sustained consumer pessimism are real. Companies in discretionary spending categories, regional retail, and consumer services face headwinds that don’t disappear when the S&P 500 ticks higher. The gap between Wall Street’s mood and Main Street’s reality has rarely been this wide — and historically, one of them ends up being right.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Additional Agreement. Hot on the heels of last week’s strategic partnership agreement with Group OTT, SKYX signed an agreement with OTT Heritage Hospitality, a prominent European developer, to deploy and market SKYX’s technologies across the European hotel chains segment and buildings. The new agreement provides additional focus and opportunity for SKYX, in our view, marking another significant step in the Company’s global expansion.

OTT Heritage Hospitality. Also founded by Jean-Francois Ott, OTT Heritage is a real estate company specializing in special situation real estate. The strategy consists of acquiring assets affordably in well-known cities, leveraging their underlying market value. With an investment pipeline of €150-250 million, current projects include a hotel consolidation strategy (objective: 2,000+ rooms) in Lourdes, luxury hospitality in Grasse and Prague, and redevelopment of the legendary Magny-Cours Formula 1 track, with the vision to turn the area into a premier destination for car and motorsport enthusiasts, including racing experiences, hotels, F&B, entertainment, and golf.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Apple (NASDAQ: AAPL) dropped one of the biggest corporate leadership announcements in years on Monday: Tim Cook will step down as CEO on September 1, 2026, transitioning to executive chairman, while John Ternus — currently Senior Vice President of Hardware Engineering — becomes the company’s eighth chief executive. The move was unanimously approved by Apple’s board of directors.

Ternus, 50, is a 25-year Apple veteran who joined the company in 2001 as a product design engineer and rose through the ranks overseeing hardware development for the iPhone, iPad, AirPods, and Mac product lines. His appointment continues Apple’s tradition of internal succession — the same approach used when Cook replaced Steve Jobs in 2011.

The transition is effective September 1, with Cook remaining in his CEO role through the summer to ensure continuity. Arthur Levinson, Apple’s non-executive chairman for the past 15 years, will shift to lead independent director at the same time Ternus joins the board.

For investors, the leadership change raises a question that goes beyond Apple’s $4 trillion market cap: what does a hardware-first CEO mean for the company’s strategic direction — and who benefits downstream?

Cook’s tenure was defined by operational excellence and margin expansion. Under his leadership, Apple’s profit more than quadrupled, and the company became the first to achieve a $1 trillion market cap. But the knock on Cook heading into his final years was the same one analysts have leveled at Apple broadly — a lagging AI strategy relative to peers.

Ternus inherits that problem directly. Apple has faced a bumpy rollout of its AI-enhanced Siri platform and relied on Google’s Gemini in January as a bridge while its own large language model development hit snags. The company is now accelerating development of AI-driven wearables — reportedly including smart glasses, a pendant device, and camera-equipped AirPods — along with a foldable iPhone that some analysts are calling the most significant hardware moment in years. Bloomberg has also reported Apple is eyeing deeper moves into robotics.

That product roadmap matters significantly for the small and microcap companies sitting inside Apple’s supply chain. Shifts in hardware strategy at the CEO level translate directly into procurement decisions, component specifications, and manufacturing volumes that flow through dozens of smaller, publicly traded suppliers. When Apple pivots toward new form factors — AI wearables, foldable displays, edge-computing hardware — it creates winners and losers across a web of suppliers many of which operate well below the $2 billion market cap threshold.

Wall Street’s initial read on the Ternus appointment has been cautiously positive. Morgan Stanley noted that promoting a product-centric engineer signals Apple’s core hardware flywheel will remain intact. Wedbush’s lead tech analyst characterized the move as an opportunity for Apple to shift from a defensive to offensive posture in the AI hardware race.

Whether Ternus can deliver on both sides of that mandate — preserving Cook’s operational discipline while channeling the kind of product innovation the market has been waiting for — will define not just Apple’s next chapter, but the trajectory of an entire ecosystem of smaller companies built around it.

Apple is scheduled to report fiscal second-quarter earnings next week, with Cook still at the helm for that call. Ternus, however, will almost certainly face pointed questions from investors about his vision from day one.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Shareholders approve CEO option grant. Travelzoo shareholders approved a 600,000-share non-qualified stock option grant to CEO Holger Bartel, formalizing a performance-based compensation structure tied directly to stock price appreciation and marking a clear inflection point in management incentives. The grant represents a significant 5.5% of the current total shares outstanding.

Structure emphasizes near-term performance and meaningful upside. The options carry a $5.05 exercise price, vest semi-annually over two years, and have a five-year term, creating a relatively short execution window in which management must deliver results to realize value.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Strong Q4 caps solid year. Vince delivered Q4 revenue growth of 4.7% to $83.7 million, with DTC up over 10%, and profitability exceeding the high end of guidance despite a ~$2M Saks-related headwind. Adj. EBITDA exceeded our expectations at $4.5 million versus our $2.0 million estimate. This performance underscores the company’s ability to execute effectively even amid wholesale channel disruption and macro uncertainty.

DTC strength and pricing power drive results. Growth was fueled by robust full-price demand, improved customer experience, and successful pricing actions that offset tariff and freight pressures while maintaining unit volumes. Importantly, this signals a structurally higher-quality revenue base with less reliance on promotions.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Q4 Net Sales Increased 4.7% to $83.7M Q4 Net Loss of $3.6M, includes $6M charge related to Saks reorganization; Q4 Adjusted EBITDA of $4.5M

FY2025 Net Sales Increased 2.2% to $300.0M FY2025 Net Income of $6.4M; FY2025 Adjusted EBITDA of $15.1M

NEW YORK–(BUSINESS WIRE)– Vince Holding Corp. (Nasdaq: VNCE) (“VNCE” or the “Company”), a global retail platform, today reported its financial results for the fourth quarter and fiscal year ended January 31, 2026.

Brendan Hoffman, Chief Executive Officer of VNCE said, “I am incredibly proud of the strong operating results we delivered in the fourth quarter reflecting the powerful momentum we built throughout fiscal 2025. Our team executed across all areas of the business, delivering nearly 5% sales growth with profitability exceeding the high end of our guidance ranges. The strength we saw in our direct-to-consumer business, with approximately 10% growth, demonstrates the power of our strategic initiatives as well as the quality of our product offering which continues to resonate with customers.”

Mr. Hoffman continued, “Our teams have done a tremendous job navigating the current environment while advancing key initiatives – from expanding our e-commerce capabilities and drop-ship program to scaling our men’s business and driving a full-price store business. The momentum we built throughout fiscal 2025 has carried seamlessly into the new year. We enter fiscal 2026 operating from a position of strength with a clear roadmap for profitable growth ahead.”

In this press release, the Company is presenting its financial results in conformity with U.S. generally accepted accounting principles (“GAAP”) as well as on an “adjusted” basis. Adjusted results presented in this press release are non-GAAP financial measures. See “Non-GAAP Financial Measures” below for more information about the Company’s use of non-GAAP financial measures and Exhibit 3 and Exhibit 4 to this press release for reconciliations of GAAP measures to such non-GAAP measures.

For the fourth quarter ended January 31, 2026:

Total Company net sales increased 4.7% to $83.7 million compared to $80.0 million in the fourth quarter of fiscal 2024. The year-over-year increase was driven by a 10.4% increase in the direct-to-consumer segment which offset a 1.2% decline in the wholesale segment.

Gross profit was $41.1 million, or 49.1% of net sales, compared to gross profit of $40.1 million, or 50.1% of net sales, in the fourth quarter of fiscal 2024. The decrease in gross margin rate was primarily driven by approximately 300 basis points due to the unfavorable impact of tariffs, 160 basis points due to higher promotional activity, and approximately 125 basis points due to increased freight costs, partially offset by a favorable impact of approximately 380 basis points primarily due to higher pricing.

Selling, general, and administrative expenses were $44.0 million, or 52.6% of sales, compared to $37.8 million, or 47.2% of sales, in the fourth quarter of fiscal 2024. The increase in SG&A dollars was primarily driven by a $6.0 million bad debt expense related to the Saks reorganization.

Loss from operations was ($2.9) million compared to a loss from operations of ($29.7) million in the same period last year. The year over year decrease in loss from operations is primarily driven by $32.0 million non-cash goodwill impairment charge (the “Goodwill Impairment Charge”) recorded in the prior comparative quarter, offset by the bad debt expense of $6.0 million related to the Saks reorganization. For fiscal 2025, excluding the impact of the bad debt expense, adjusted income from operations* was $3.1 million. For the prior year, excluding the Goodwill Impairment Charge and the transaction expenses (“P180 Transaction Expenses”) related to the acquisition of the Company’s majority stake by a wholly owned subsidiary of P180, Inc., adjusted income from operations* was $2.5 million.

Income tax provision was $0.5 million compared to an income tax benefit of $2.0 million in the same period last year. The year over year change is primarily driven by a tax benefit taken in the prior comparative quarter due to the reversal of the non-cash deferred tax liability associated with the goodwill impairment, which previously could not be used as a source of income to support the realization of certain deferred tax assets related to the Company’s net operating losses.

Net loss was ($3.6) million or $(0.28) per share compared to a net loss of ($28.3) million or $(2.24) per share in the same period last year. Excluding the impact of bad debt expense in the fourth quarter of fiscal 2025, adjusted net income* for the period was $2.4 million or $0.18 per share. This compares to adjusted net income* in the prior year period of $0.8 million or $0.06 per share which excludes the Goodwill Impairment Charge and the transaction expenses previously defined.

Adjusted EBITDA* was $4.5 million compared to $5.4 million in the same period last year.

The Company ended the quarter with 55 company-operated Vince stores, a net decrease of 2 stores since the fourth quarter of fiscal 2024.

For the fiscal year ended January 31, 2026:

Total Company net sales increased 2.2% to $300.0 million compared to $293.5 million in fiscal 2024. The year-over-year increase was driven by a 4.8% increase in the direct-to-consumer segment and a 0.2% increase in the wholesale segment.

Gross profit was $149.1 million, or 49.7% of net sales, compared to gross profit of $145.2 million, or 49.5% of net sales, in fiscal 2024. The increase in gross margin rate was driven by approximately 340 basis points related to higher pricing and 70 basis points due primarily to lower discounting. These increases were partially offset by approximately 250 basis points resulting from higher tariffs and 130 basis points due to the unfavorable impact of increased freight and distribution and handling costs.

Selling, general, and administrative expenses were $139.9 million, or 46.6% of sales, compared to $138.0 million, or 47.0% of sales, in fiscal 2024. The increase in SG&A dollars was primarily driven by $6.5 million of bad debt expense related to the Saks reorganization, increased marketing and advertising costs of approximately $1.9 million, and increased legal fees of approximately $1.4 million. These increased SG&A costs were partially offset by a decrease primarily driven by the receipt of payroll tax credit payments from the U.S. Department of the Treasury under the Employee Retention Credit program (the “ERC benefit”). The ERC benefit was approximately $7.2 million, of which $5.6 million related to the original payroll tax credit claims and was recorded in SG&A as an offset to compensation expenses, with the remaining $1.6 million of interest payments recorded as Other income. In addition, there was a decrease in professional fees.

Income from operations was $9.2 million compared to loss from operations of $17.2 million in the same period last year. Adjusted income from operations* in fiscal 2025 was $10.1 million compared to adjusted income from operations* of $7.3 million in the same period last year.

Income tax provision was $2.6 million. Our effective tax rate for fiscal 2025 and fiscal 2024 was 35.1% and 15.6%, respectively. The effective tax rate for fiscal 2025 differed from the U.S. statutory rate of 21% primarily due to state taxes and changes in our valuation allowance, partially offset by nontaxable ERC benefits. The tax provision in fiscal 2025 compares to an income tax benefit of $3.6 million in the same period last year.

Net income was $6.4 million or $0.49 per share compared to net loss of $19.0 million or $(1.51) per share in the same period last year. Adjusted net income* for fiscal 2025 was $5.8 million or $0.44 per share compared to adjusted net income* of $2.4 million or $0.19 per share in the same period last year.

Adjusted EBITDA* was $15.1 million compared to $14.0 million last year.

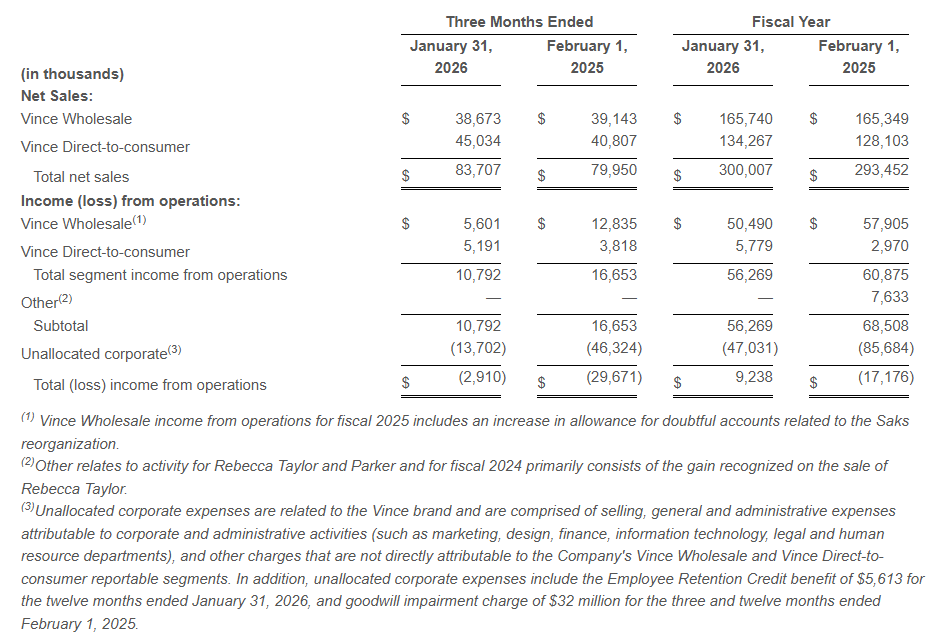

Fourth Quarter Review

Net sales increased 4.7% to $83.7 million as compared to the fourth quarter of fiscal 2024.

Wholesale segment sales decreased 1.2% to $38.7 million compared to the fourth quarter of fiscal 2024.

Direct-to-consumer segment sales increased 10.4% to $45.0 million compared to the fourth quarter of fiscal 2024.

Income from operations excluding unallocated corporate expenses was $10.8 million compared to income from operations of $16.7 million in the same period last year. The decline compared to the prior year period was primarily driven by a $6.0 million bad debt expense related to the Saks reorganization.

Net Sales and Operating Results by Segment:

Balance Sheet

At the end of fiscal 2025, total borrowings under the Company’s debt agreements totaled $19.5 million and the Company had $40.8 million of excess availability under its revolving credit facility.

Net inventory at the end of fiscal 2025 was $66.2 million compared to $59.1 million at the end of fiscal 2024. The year-over-year increase in inventory includes approximately $4.8 million of higher inventory carrying value due to tariffs.

During the year ended January 31, 2026, the Company issued and sold 578,041 shares of common stock under the Virtu At-the-Market offering for aggregate net proceeds of $2,023 at an average price of $3.57 per share. At January 31, 2026, $861 was available under Virtu At-the-Market Offering.

Outlook

For the first quarter of fiscal 2026 the Company expects the following:

Net sales to increase approximately 8.5% to 10.5% compared to the prior year period.

Adjusted operating loss as a percentage of net sales to be approximately (3.5)% to (4.5)%.

Adjusted EBITDA as a percentage of net sales to be approximately (1.5)% to (2.5)%.

For fiscal 2026 the Company expects the following:

Net sales to increase approximately 3% to 6% compared to the prior year.

Adjusted operating income as a percentage of net sales to be approximately 3.5% to 4%.

Adjusted EBITDA as a percentage of net sales to be approximately 5% to 5.5%.

Following the Supreme Court’s decision striking down certain tariffs imposed under the International Emergency Economic Powers Act, (“IEEPA”), the Company’s outlook assumes a 15 percent rate for applicable inventory receipts under Section 122 of the Trade Act of 1974. The Company’s outlook does not consider potential tariff refunds resulting from the Supreme Court’s decision on the IEEPA tariffs.

*Non-GAAP Financial Measures

In addition to reporting financial results in accordance with GAAP, the Company has provided, with respect to the financial results relating to the three and twelve months ended January 31, 2026 and February 1, 2025, adjusted EBITDA, which is a non-GAAP measure. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation and amortization, share-based compensation, capitalized cloud computing amortization, goodwill impairment, P180 transaction expenses, bad debt expense related to the Saks reorganization (“Bad debt expense”), ERC benefit, and gain on sale of Rebecca Taylor, Inc. and its wholly owned subsidiary (“Gain on Sale of Subsidiary”). For the three and twelve months ended January 31, 2026 and February 1, 2025, the Company has provided adjusted income from operations, adjusted income before income taxes and equity in net income of equity method investment, adjusted provision (benefit) for income taxes, adjusted income before equity in net income of equity method investment, adjusted net income, and adjusted earnings per share, which are non-GAAP measures, in order to eliminate the effect of the Bad Debt Expense, ERC benefit, Discrete Tax Effect associated with ERC benefit, Gain on sale of Subsidiary, Impairment of Goodwill, the P180 Transaction Expenses, and the associated income tax impacts.

The Company believes that the presentation of these non-GAAP measures facilitates an understanding of the Company’s continuing operations without the impact associated with the aforementioned items. While these types of events can and do recur periodically, they are excluded from the indicated financial information due to their impact on the comparability of earnings across periods. Non-GAAP financial measures should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. A reconciliation of GAAP to non-GAAP results has been provided in Exhibit 3 and Exhibit 4 to this press release.

Conference Call

A conference call to discuss the fourth quarter results will be held today, April 15, 2026, at 8:30 a.m. ET, hosted by Vince Holding Corp. Chief Executive Officer, Brendan Hoffman, and Chief Financial Officer, Yuji Okumura. During the conference call, the Company may make comments concerning business and financial developments, trends and other business or financial matters. The Company’s comments, as well as other matters discussed during the conference call, may contain or constitute information that has not been previously disclosed.

Those who wish to participate in the call may do so by dialing (800) 715-9871, conference ID 8749496. Any interested party will also have the opportunity to access the call via the Internet at http://investors.vince.com/. To listen to the live call, please go to the website at least 15 minutes early to register and download any necessary audio software. For those who cannot listen to the live broadcast, a recording will be available for 12 months after the date of the event. Recordings may be accessed at http://investors.vince.com.

ABOUT VINCE HOLDING CORP.

Vince Holding Corp. is a global retail platform that operates the Vince brand women’s and men’s ready to wear business. Vince, established in 2002, is a leading global luxury apparel and accessories brand best known for creating elevated yet understated pieces for every day effortless style. Vince Holding Corp. operates the Vince brand under a long-term license agreement with Authentic Brands Group, including 43 full-price retail stores, 12 outlet stores, and its e-commerce site, vince.com, as well as through premium wholesale channels globally. Please visit www.vince.com for more information.

Forward-Looking Statements: This document, and any statements incorporated by reference herein contain forward-looking statements under the Private Securities Litigation Reform Act of 1995. Forward-looking statements include the statements under “Transformation Program & Fiscal 2024 Outlook” above as well as statements regarding, among other things, our current expectations about possible or assumed future results of operations of the Company and are indicated by words or phrases such as “may,” “will,” “should,” “believe,” “expect,” “seek,” “anticipate,” “intend,” “estimate,” “plan,” “target,” “project,” “forecast,” “envision” and other similar phrases. Although we believe the assumptions and expectations reflected in these forward-looking statements are reasonable, these assumptions and expectations may not prove to be correct and we may not achieve the results or benefits anticipated. These forward-looking statements are not guarantees of actual results, and our actual results may differ materially from those suggested in the forward-looking statements. These forward-looking statements involve a number of risks and uncertainties, some of which are beyond our control, including, without limitation: changes to and unpredictability in the trade policies and tariffs imposed by the U.S. and the governments of other nations; general economic conditions; our ability to maintain adequate cash flow from operations or availability under our revolving credit facility to meet our liquidity needs; restrictions on our operations under our credit facilities; our ability to improve our profitability; our ability to maintain our larger wholesale partners; our ability to accurately forecast customer demand for our products; our ability to maintain the license agreement relating to the Vince brand with ABG Vince; ABG Vince’s expansion of the Vince brand into other categories and territories; ABG Vince’s approval rights and other actions; our ability to realize the benefits of our strategic initiatives; our ability to make lease payments when due; our ability to open retail stores under favorable lease terms and operate and maintain new and existing retail stores successfully; our operating experience and brand recognition in international markets; our ability to remediate the identified material weakness in our internal control over financial reporting; our ability to comply with domestic and international laws, regulations and orders; increased scrutiny regarding our approach to sustainability matters and environmental, social and governance practices; competition in the apparel and fashion industry; our ability to attract and retain key personnel; seasonal and quarterly variations in our revenue and income; the protection and enforcement of intellectual property rights relating to the Vince brand; the extent of our foreign sourcing; our reliance on independent manufacturers; our ability to ensure the proper operation of the distribution facilities by third-party logistics providers; fluctuations in the price, availability and quality of raw materials; the ethical business and compliance practices of our independent manufacturers; our ability to mitigate system or data security issues, such as cyber or malware attacks, as well as other major system failures; our ability to adopt, optimize and improve our information technology systems, processes and functions; our ability to comply with privacy-related obligations; our status as a “controlled company”; our status as a “smaller reporting company”; and other factors as set forth from time to time in our Securities and Exchange Commission filings, including those described under “Item 1A—Risk Factors” in our Annual Report on Form 10-K and Quarterly Reports on Form 10-Q. We intend these forward-looking statements to speak only as of the time of this release and do not undertake to update or revise them as more information becomes available, except as required by law.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid holiday performance. For the nine-week period ended January 3, 2026, total company net sales increased 5.3% year over year, supported primarily by steady demand and continued strength in the Direct-to-Consumer segment. Furthermore, management attributed the improvement to ongoing investments in customer experience, digital capabilities, and omnichannel engagement.

DTC leads the way. Notably, Direct-to-Consumer revenue increased 9.7% versus the prior-year holiday period, underscoring strong traffic conversion across e-commerce and retail locations. In contrast, the Wholesale segment declined 2.7% year over year, reflecting disruption in receipt flow related to its partner Saks Global. Despite this pressure, management indicated that strong point-of-sale performance with key partners partially offset the disruption.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

February’s Personal Consumption Expenditures (PCE) report, released Thursday, confirmed what many on Wall Street suspected but hoped wasn’t true: inflation remains stubbornly entrenched, and the Federal Reserve has no clear path to cutting interest rates anytime soon. For small and microcap investors, this isn’t just a macro headline — it’s a direct input into valuations, borrowing costs, and growth timelines.

The Fed’s preferred inflation gauge rose 2.8% in February on a headline basis. Core PCE, which strips out food and energy and is the number the Fed actually weighs policy decisions against, came in at 3.0% — exactly where it has been parked for three consecutive months. On a 3-month annualized basis, core inflation is running at 3.7%, nearly double the Fed’s 2% target. The report was delayed from its original March 27 release date due to the government shutdown last fall, making today’s release the first clean read the market has had in months.

The timing is particularly complicated. This data reflects economic conditions that existed before the Iran conflict escalated, before oil prices surged, and before the Strait of Hormuz disruptions began compressing global supply chains. In other words, the inflation picture captured in February’s numbers is arguably the best it’s going to look for a while — and it still isn’t good enough for the Fed to act.

Goods inflation clocked in at 0.84% for the month, a figure economists point to as evidence that tariff pass-throughs are still working their way into consumer prices. That’s the sticky problem: even if geopolitical tensions ease, tariff-driven inflation has its own timeline, and the Fed can’t cut its way around it.

The one silver lining in the report was services inflation, which showed meaningful improvement in February. Services prices have been a persistent headache for central bankers because they typically reflect wage pressures and domestic demand — both harder to control than goods prices. The improvement suggests that underlying inflation may not be structurally broken, even as energy shocks pile on.

The practical read for small and microcap companies is this: the higher-for-longer rate environment is not lifting anytime soon. Small companies carry a disproportionate share of variable-rate debt and are more sensitive to the cost of capital than their large-cap counterparts. When borrowing costs stay elevated, growth initiatives slow, refinancing gets expensive, and M&A activity tightens — all headwinds for the small and microcap universe.

That said, today’s Iran ceasefire news introduces a meaningful counterweight. Oil prices have already begun pulling back, which relieves some of the near-term inflationary pressure the Fed has been bracing for. If the ceasefire holds and energy prices stabilize, the Fed may not need to hike — it just may not be in position to cut either.

Futures market participants have already absorbed this reality, with nearly 90% now expecting the Fed’s target rate to hold at 3.50%–3.75% through September 2026.

For investors focused on smaller companies, the message is clear: fundamentals matter more than ever in this environment. Companies with strong cash flows, manageable debt loads, and pricing power are best positioned to navigate a world where rate relief isn’t coming on anyone’s preferred schedule.