Highly Regarded Analyst Tells Investors How to Position for the Upturn

Are recession worries fully baked into stock prices? At least one Wall Street analyst has publicly made her case this may be accurate. And she offers tips on what sectors may have more upside and on those that have factors working against them. While a recession still may occur before year-end, forward-looking stock investors may have fully priced that risk in – forward-looking investors may also be the reason the overall market is up on the year despite greater expectations of a recession. They are looking past any slowdown.

Stock market participants, many still down on last year’s price moves, have been extremely cautious in front of a Fed that is playing catch up in a fight against inflation. The rapid Fed Funds rate increases that began in March 2022, coupled with quantitative tightening, sank stocks, bonds, and even cryptocurrency holdings. While the economy did shrink for two consecutive quarters last year, there are many that expect a mild recession will begin at some point this year.

Those that do expect a bumpy economic ride and a rough landing point to high-interest rates, a weakening dollar, tech industry layoffs, and a Federal Reserve that is resolved to get inflation down as soon as possible.

Savita Subramanian, equity and quant strategist at Bank of America Securities, proposed to investors in a research note published on April 24, that these fears and recession worries have been in place for a while and may be largely baked into the market. She says, barring a sudden shock to the economy, it makes sense for investors to reintroduce riskier assets into their portfolios.

Her guidance on finding value is well thought out. Subramanian, proposes investors own stocks over bonds and cyclical stocks over defensive names. The reason given is that hedge funds and long-only funds are near maximum exposure in defensive industries such as health care, utilities, and consumer staples. The suggestion here is that the probabilities would lean toward a better risk-reward payoff for cyclical names.

Ms. Subramanian does not say an economic slowdown won’t occur; instead, her thinking seems to be that after raising the Federal Funds rate from near-zero to a range of 4.75% to 5%, there is more control should a downturn need to be dealt with by easing. When rates are at or near zero percent, there is less the Fed can do to stimulate growth. So far, we’ve made it through the first quarter, and now April with only a few disruptions in the banking sector.

“Even if a recession is imminent, the Fed has latitude to soften the impact after pushing rates up by 5%. And after the fastest hiking cycle ever, the only thing to ‘break’ so far is SVB,” Subramanian wrote.

In an article published in Barron’s this week the investment news publication wrote, “Some corners of Wall Street are feeling confident that there will be no recession and that the very things that make a recession appear likely–the inverted yield curve, inflation, and the recent banking crisis–actually guarantee that one won’t happen.”

This could be good news for investors that have been nervous about having money in a market that has been given much to be concerned about, and ver little to be jubilant about.

On Thursday, GDP (Gross Domestic Product) for the first quarter will be released. No one expects this to indicate a recession began then. Forecasters expect that the economy will show 2% growth, following growth of 3.2% and 2.6% in the third and fourth quarters of 2022. This is one of the cases where if the number surprises much higher, the market may expect the Fed to make bigger rate moves. If it surprises on the low side, markets may see it as a sign of an approaching recession.

Take Away

A highly regarded analyst joins others with thoughts that the market could be priced for a recession; this could be good for stocks. If true, investors may want to start looking past a recession. Those she is most positive on are riskier names. While funds and other investors are near maxed out in lower-risk holdings, there is far less upside for them. The bigger upswings can occur in the industries, market-cap sectors, and companies that have been given less attention due to recession fears.

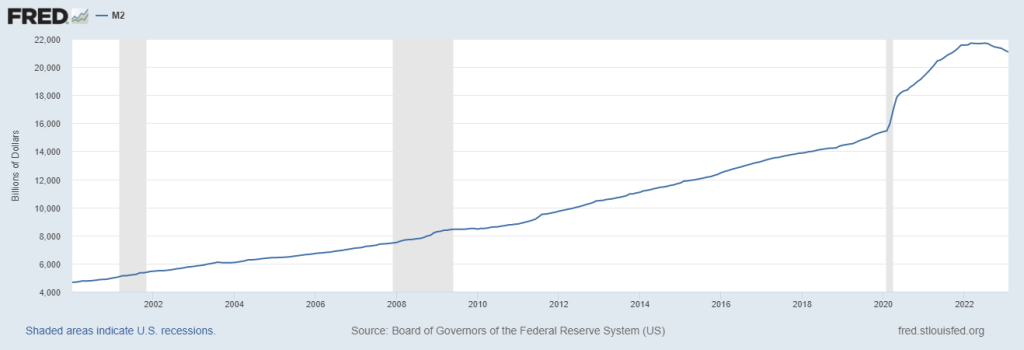

M2 is Fuel for Inflation, How Much Money Must the Fed Drain to Achieve 2 Percent?

U.S. Money Supply, measured as M2, is an important consideration when forecasting inflation. A decline in immediately available cash in the economy has a downward effect on price levels. At the same time, less cash available to consumers also cools economic growth. With the Federal Open Market Committee’s (FOMC) interest rate decision coming the first week in May, the updated report this week (for March) will give investors a look see at how successful the Fed has been draining funds from the system while trying to maintain some growth.

M2 Shrinking

The Federal Reserve will update stock and bond markets Tuesday afternoon on the total amount of currency, coins, bank savings deposits, and money-market funds held in March. This broader measure, officially M2SL, referred to as M2, gained renewed focus after contracting for the first time ever in December 2022, then contracting even further in January and February. January’s 1.75% decline and February’s 2.4% drop to $21.1 trillion, are the steepest drops so far in M2.

Image: M2 levels ramped up starting in 2020 in response to pandemic economic efforts

A fourth consecutive decline in M2 would provide more evidence that inflation can be expected to continue to come down and weigh into the FOMC decision when the Fed meets to adjust monetary policy at its May 2-3 meeting. While the chart above shows the recent declines are significant, it is still far higher than the trend line that was established decades ago. So while a decline of similar magnitude as the first two months would be welcome by inflation hawks, there is still a great deal more cash in the system than there was pre-pandemic. But it would be a huge positive and may cause the Fed to pause or slow draining money from the system.

Inflation

Consumer price inflation is well off its 8.6% average for all of 2022. Inflation since rose 5% in March 2023 (annual basis), decelerating from February’s 6% pace. While this slowdown in price increases is substantial, the Fed doesn’t want to declare “mission accomplished” until it is ranging near 2%. Its work is not yet finished.

How close is the Fed from finished is what investors will try to discern from M2. Highly regarded analysts and Fed watchers anticipate that there is a lag of about a year when the money supply shrinks. However, as indicated above, it has never come down on an annualized basis, and January and February were the largest declines to date. So even the best analysts have little history to point to.

Financial Sector

The data is for March, so it is the first look at M2 since the banking sector showed trouble early that month. A part of the difficulty banks are currently experiencing is that the reduction in cash has caused a need for them to liquidate U.S. Treasuries and other bonds to fund withdrawals. A further huge reduction in M2 could be shown to be challenging more banks as bonds and other interest rate-sensitive assets had lost considerable value as rates rose dramatically over the past year.

Using the most recent data, the Federal Reserve reported bank deposits were down 6% for the week ending April 12 versus a year ago. Deposits have been falling year-over-year since November, off slightly at $17.2 trillion compared to the highest-ever $18.2 trillion level seen in April last year.

Further declines in deposits should lead to fewer loans written, fewer loans slows economic growth. This in part, accounts for why there is a lag between when the Fed drains and when it has an impact on inflationary pressures.

Take Away

M2 is an important gauge of future inflation. Because of this, the release of data may cause economists to change their May FOMC meeting forecast. A large decline may cause the Fed to pause, if M2 resumed its path upward the Fed may become more hawkish. Efforts to help the banking system last month, may have reinflated money supply, this will be a very interesting report.

CULVER CITY, Calif., April 24, 2023 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail” or “the Company”), a leading, global independent developer and publisher of interactive digital entertainment, today announced ARK: Survival Ascended (“ASA”), the next-generation remaster of the beloved ARK: Survival Evolved, harnessing the power of Unreal Engine 5 (“UE5”), is expected to release on Xbox Series S/X, PC (Windows/Steam), and PlayStation 5 in August 2023.

ASA is expected to be available as a standalone package on all platforms at $59.99. This comprehensive package will contain the remastered and next-generation optimized content, including The Island, a revamped Survival of the Fittest, and other DLCs and maps (including Scorched Earth, Aberration, Extinction, Genesis Part 1 & Part 2, Fjordur, Ragnarok, The Center, Lost Island, Valguero, and Crystal Isles).

Upon launch, ASA players will gain access to The Island, Survival of the Fittest and Scorched Earth. The other DLCs will be added over time. The game will showcase significant improvements and enhancements and ongoing planned updates with new features, content drops, creatures, items, structures, and DLC. Survival of the Fittest will be integrated into ASA as a new fully-supported game mode, backed by a dedicated development team concentrating on gameplay changes and adjustments. Moreover, a new canonical-story expansion pack for ASA is expected to be available in Q4 2023, introducing four new creatures and more details to be revealed later this year.

Snail is committed to delivering the finest gaming experience and will continue to support the next generation of ARK with continuous updates and enhancements.

Jim Tsai, Chief Executive Officer of Snail, commented, “We are excited to bring ASA to our loyal players and new audiences alike. Leveraging the power of UE5, we aim to elevate the iconic ARK gaming experience to new heights, providing enhanced visuals, gameplay, and features that will engage the community for years to come.”

About Snail, Inc.

Snail is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs and mobile devices.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future plans and objectives related to the release of ASA, including but not limited to, the timing of the release, the pricing of ASA, the content and features of ASA, the release of the expansion pack for ASA. The statements Snail makes regarding the following matters are forward-looking by their nature: growth prospects and strategies; launching new games and additional functionality to games that are commercially successful; expansion of upcoming games; its ability to develop new video games and enhance existing games; its relationships with third-party platforms such as Xbox Live and Game Pass, PlayStation Network, Steam, Epic Games Store, Google Stadia, the Apple App Store, the Google Play Store and the Amazon Appstore; assumptions underlying any of the foregoing.

FLORHAM PARK, N.J., April 24, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease announced the Company received $1.4 million from the net sale of tax benefits to an unrelated, profitable New Jersey corporation pursuant to the Company’s participation in the New Jersey Technology Business Tax Certificate Transfer Net Operating Loss (NOL) program for State Fiscal Year 2021.

“We are pleased to receive funds from the New Jersey NOL program,” said Matthew Hill, Chief Financial Officer of PDS Biotech. “The funding will be beneficial to us as we transition our lead asset, PDS0101, into a registrational trial for the treatment of HPV16-positive metastatic or recurrent head and neck cancer.”

The New Jersey Technology Business Tax Certificate Transfer program enables qualified, unprofitable NJ-based technology or biotechnology companies with fewer than 225 US employees (including parent company and all subsidiaries) to sell a percentage of their NOL and research and development tax credits to unrelated profitable corporations. This allows qualifying technology and biotechnology companies with NOLs to turn tax losses and credits into cash proceeds to fund their growth and operations, including research and development or other allowable expenditures.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, Versamune® plus PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted immunotherapies have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials. and will be advancing into a Phase 3 clinical trial in combination with KEYTRUDA® for the treatment of recurrent/metastatic HPV16-positive head and neck cancer in 2023. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to the Company’s currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; to aid in the development of the Versamune® platform; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual, quarterly and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

Versamune® is a registered trademark and Infectimune™ is a trademark of PDS Biotechnology. KEYTRUDA® is a registered trademark of Merck Sharp and Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, N.J., USA.

SAN DIEGO, April 24, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a Technology Company in the Defense, National Security and Global Markets, announced today that it will publish financial results for the first quarter 2023 after the close of market on Wednesday, May 3rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS) is a Technology Company that develops and fields transformative, affordable systems, products and solutions for United States National Security, our allies and global commercial enterprises. At Kratos, Affordability is a Technology, and Kratos is changing the way breakthrough technology is rapidly brought to market – at a low cost – with actual products, systems, and technologies rather than slide decks or renderings. Through proven commercial and venture capital backed approaches, including proactive, internally funded research and streamlined development processes, Kratos is focused on being First to Market with our solutions, well in advance of competition. Kratos is the recognized Technology Disruptor in our core market areas, including Space and Satellite Communications, Cyber Security and Warfare, Unmanned Systems, Rocket and Hypersonic Systems, Next-Generation Jet Engines and Propulsion Systems, Microwave Electronics, C5ISR and Virtual and Augmented Reality Training Systems. For more information, visit www.KratosDefense.com.

BOTHELL, Wash., April 24, 2023 (GLOBE NEWSWIRE) — Cocrystal Pharma, Inc. (Nasdaq: COCP) (Cocrystal or the Company) announces the appointment of Fred Hassan to its Board of Directors, increasing its Board membership to six. Mr. Hassan’s distinguished 40-year career includes serving in senior executive and director positions at global pharmaceutical companies and leading investment firms. Earlier this month, Cocrystal announced Mr. Hassan’s $2 million investment in the Company through an at-the-market private placement.

“It’s an honor to attract such a highly accomplished industry veteran to our Board,” said Roger Kornberg, PhD, Cocrystal Chairman, Chief Scientist and Chairman of the Scientific Advisory Board. “We expect that Fred’s significant experience will strengthen our corporate governance and his guidance will be instrumental in advancing our antiviral pipeline. On behalf of my fellow Directors, I welcome Fred and look forward to working together.”

“I appreciate Cocrystal’s tremendous potential in developing safe and effective antiviral therapies in priority indications of global concern,” said Mr. Hassan. “I’m impressed with the ability of the company’s structure-based discovery platform technology to efficiently discover and develop novel drug candidates. I look forward to working closely with Cocrystal’s Board and executive leadership to advance our pipeline toward commercialization.”

Mr. Hassan is Chairman of the investment firm Caret Group and a Director of Warburg Pincus LLC, a global private equity firm. From 2003 to 2009 Mr. Hassan served as Chairman and Chief Executive Officer of Schering-Plough and from 2001 to 2003 he was Chairman and Chief Executive Officer of Pharmacia Corporation, a company via the merger of Monsanto Company and Pharmacia & Upjohn, Inc. He joined Pharmacia & Upjohn, Inc. as Chief Executive Officer in 1997. Earlier in his career Mr. Hassan held leadership positions with Wyeth, including serving as Executive Vice President and as a Director from 1995 to 1997, and with Sandoz Pharmaceuticals, including leading its U.S. pharmaceuticals business.

Mr. Hassan is a Director of Precigen, Inc., BridgeBio Pharma and Prometheus Biosciences, Inc., which earlier this month announced a definitive agreement to be acquired by Merck for approximately $10.8 billion. Previously he was a Director of Amgen, Inc. and Time Warner Inc. (now Warner Media, LLC). Over the course of his career, he has served on various other Boards including at Avon Products, Inc. and Bausch & Lomb, which was acquired by Valeant Pharmaceuticals International, Inc.

Mr. Hassan has chaired several prominent pharmaceutical industry organizations including The Pharmaceutical Research and Manufacturers of America (PhRMA) and The International Federation of Pharmaceutical Manufacturers Associations (IFPMA). He received a BS in chemical engineering from the Imperial College of Science and Technology at the University of London and an MBA from Harvard Business School.

About Cocrystal Pharma, Inc.

Cocrystal Pharma, Inc. is a clinical-stage biotechnology company discovering and developing novel antiviral therapeutics that target the replication process of influenza viruses, coronaviruses (including SARS-CoV-2), hepatitis C viruses and noroviruses. For further information about Cocrystal, please visit www.cocrystalpharma.com.

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements regarding the advancement of the Company’s pipeline toward commercialization and the Company’s potential for developing safe and effective antiviral therapies in priority indications of global concern. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events. Some or all of the events anticipated by these forward-looking statements may not occur. Important factors that could cause actual results to differ from those in the forward-looking statements include, but are not limited to, the risks and uncertainties arising from inflation, interest rate increases, the current banking crisis and the Ukraine war on our Company, our collaboration partners, and on the U.S., U.K., Australia and global economies, including manufacturing and research delays arising from raw materials and labor shortages, supply chain disruptions and other business interruptions including any adverse impacts on our ability to obtain raw materials and test animals as well as similar problems with our vendors and our current Contract Research Organization (CRO) and any future CROs and Contract Manufacturing Organizations, the results of the studies for CC-42344 and CDI-988, the ability of our CROs to recruit volunteers for, and to proceed with, clinical studies, our and our collaboration partners’ technology and software performing as expected, financial difficulties experienced by certain partners, the results of future preclinical and clinical trials, the impact of COVID-19 (including long-term and pervasive effects of the virus), general risks arising from clinical trials, receipt of regulatory approvals, regulatory changes, development of effective treatments and/or vaccines by competitors, including as part of the programs financed by the U.S. government. Further information on our risk factors is contained in our filings with the SEC, including our Annual Report on Form 10-K for the year ended December 31, 2022. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

SASKATOON, Saskatchewan, Canada, Apr. 24, 2023 – MustGrow Biologics Corp. (TSXV: MGRO) (OTC: MGROF) (FRA: 0C0) (the “Company” or “MustGrow”), announces that it will be hosting an investor webcast on Wednesday, April 26th at 4:00pm ET. MustGrow’s management team will be presenting on recent corporate progress, biological industry developments, and upcoming catalysts. The presentation will be followed by an audience Q&A session.

Live Webcast: Wednesday, April 26th at 4:00pm ET / 1:00pm PT Register/View Here Please join/register at least 5 minutes prior to the call.

Before April 26th, please email questions to info@mustgrow.ca to be addressed during the Q&A portion of the webcast.

Sustainbile Food Security

One significant industry catalyst to be discussed during the webcast is the demand for safe and sustainable food security solutions. The interest in natural crop protection, food preservation, and fertility products is increasing as farmers, consumers, regulators, and investors seek organic alternatives to synthetic chemicals and fertilizers. Safe and effective solutions will be needed for future food security and environmentally sustainable agriculture.

Throughout 2022, MustGrow engaged in extensive market research, formulation activities, and prospective partnership discussions, and has added Soil Amendment and Biofertility programs to its growing global intellectual property portfolio which now covers: Biocontrol applications (including preplant soil fumigation, postharvest food preservation, bioherbicide), and now Soil Amendment and Biofertility applications.

MustGrow believes its Soil Amendment and Biofertility initiative will complement existing Biocontrol programs, which are currently under development with four global partners: Janssen PMP, Bayer, Sumitomo Corporation, and NexusBioAg. These four partnered programs continue to achieve performance milestones and expand globally in scope and investment. MustGrow believes 2023 will be a pivotal year for commercial and strategic advancement in certain regions and crops.

———

About MustGrow

MustGrow is an agriculture biotech company developing organic biocontrol, soil amendment and biofertility products by harnessing the natural defense mechanism and organic materials of the mustard plant to sustainably protect the global food supply and help farmers feed the world. MustGrow and its leading global partners — Janssen PMP (pharmaceutical division of Johnson & Johnson), Bayer, Sumitomo Corporation, and Univar Solutions’ NexusBioAg — are developing mustard-based organic solutions to potentially replace harmful synthetic chemicals. Concurrenly, with new formulations derived from food-grade mustard, the Compmany is pursusing the adoption and use of it’s technology in the soil amendment and biofertily markets. Over 150 independent tests have been completed, validating MustGrow’s safe and effective approach to crop and food protection and yield enhancements. Pending regulatory approval, MustGrow’s patented liquid products could be applied through injection, standard drip or spray equipment, improving functionality and performance features. Now a platform technology, MustGrow and its global partners are pursuing applications in several different industries from preplant soil treatment and weed control, to postharvest disease control and food preservation, to soil amendment and biofertility. MustGrow has approximately 49.7 million basic common shares issued and outstanding and 55.6 million shares fully diluted. For further details, please visit www.mustgrow.ca.

Certain statements included in this news release constitute “forward-looking statements” which involve known and unknown risks, uncertainties and other factors that may affect the results, performance or achievements of MustGrow.

Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects”, “is expected”, “budget”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, “occur” or “be achieved”. Examples of forward-looking statements in this news release include, among others, statements MustGrow makes regarding: (i) the investor webcast to be held on April 26th 2023; (ii) the ability of MustGrow’s Soil Amendment and Biofertility initiative to complement existing Biocontrol programs currently under development; and (iii) the anticipated commercial and strategic advancement of MustGrow in certain regions and crops in 2023.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual results of MustGrow to differ materially from those discussed in such forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, MustGrow. Important factors that could cause MustGrow’s actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: (i) the preferences and choices of agricultural regulators with respect to product approval timelines; (ii) the ability of MustGrow’s partners to meet obligations under their respective agreements; and (iii) other risks described in more detail in MustGrow’s Annual Information Form for the year ended December 31, 2021 and other continuous disclosure documents filed by MustGrow with the applicable securities regulatory authorities which are available at www.sedar.com. Readers are referred to such documents for more detailed information about MustGrow, which is subject to the qualifications, assumptions and notes set forth therein.

This release does not constitute an offer for sale of, nor a solicitation for offers to buy, any securities in the United States.

Neither the TSXV, nor their Regulation Services Provider (as that term is defined in the policies of the TSXV), nor the OTC Markets has approved the contents of this release or accepts responsibility for the adequacy or accuracy of this release.

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of molecularly targeted cancer and infectious disease immunotherapies based on the Company’s proprietary Versamune® and Infectimune™ T-cell activating technology platforms. Our Versamune®-based products have demonstrated the potential to overcome the limitations of current immunotherapy by inducing in vivo, large quantities of high-quality, highly potent polyfunctional tumor specific CD4+ helper and CD8+ killer T-cells. PDS Biotech has developed multiple therapies, based on combinations of Versamune® and disease-specific antigens, designed to train the immune system to better recognize diseased cells and effectively attack and destroy them. The Company’s pipeline products address various cancers including HPV16-associated cancers (anal, cervical, head and neck, penile, vaginal, vulvar) and breast, colon, lung, prostate and ovarian cancers.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

KOL Discussion Of IL-12. PDL Biotechnology held a Roundtable Discussion on cancer therapy with IL-12 and its proprietary, tumor-seeking version, PDS0301. The panel was moderated by Dr. Lauren Wood, Chief Medical Officer, and featured two distinguished scientists from the National Cancer Institute. The presentations highlighted the distinctions between PDL0301 and recombinant IL-12, with clinical data from trials testing both drugs.

Comparisons Between IL-12 and PDS0301. The presentations pointed out the differences between IL-12 and PDS0301, the proprietary version developed by the NCI and licensed by PDS. One of the key points is that PDS0301 is an antibody linked to IL-12. The antibody domain targets and binds to cancer cell DNA that has been released from dead or dying cancer cells. This concentrates PDS0301 in the tumor, then the IL-12 portion stimulates an immune response. This differs from other trials that have used recombinant IL-12 to stimulate an immune response. In comparison, systemic rIL-12 delivery or targeting technologies have resulted in lack of efficacy, systemic side effects, or both.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Key takeaways from the NAB. Media investors are unpacking the information from the National Association of Broadcaster’s (NAB) convention. While there are promising new technologies that are sure to create shiny new objects to catch investor’s attention, particularly AI, the chatter is about the current advertising environment. Looking for the key takeaways? Sign up here for the virtual conference on April 27th.

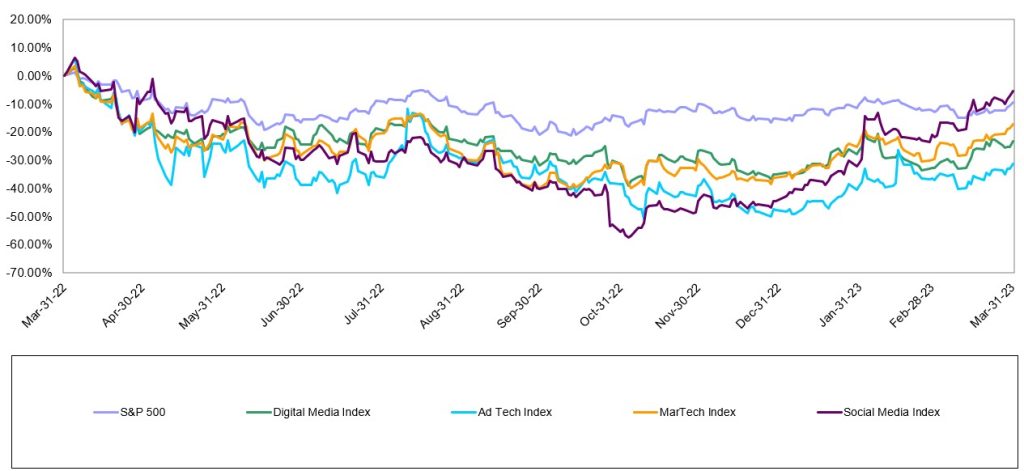

Digital Media & Technology:Head fake? Every one of Noble’s Internet and Digital Media Indices not only finished the quarter up, but significantly outperformed the S&P 500. The best performing index was Noble’s Social Media Index, which increased by 70% in the first quarter of 2023, followed by Noble’s Ad Tech Index (+31%), MarTech Index (+30%), and Digital Media Index (+18%).

Television Broadcasting: Weak current revenue trends.While auto advertising appears to be faring better, the weight of the economic challenges appear to be causing further moderation in advertising. Will auto and, potentially Political, carry the second half 2023 revenue performance?

Radio Broadcasting: All out of love.The industry is reeling from a Wall Street research downgrade to an underperform on iHeart Media, which sent all radio stocks tumbling. Some stocks performed better than others. What’s behind the downgrade and which stocks performed better?

Publishing:Advertising takes a hit. After a period of moderating revenue trends, Publishers reported a weakened advertising environment. The downturn was due to Print advertising which took a nose dive. As a result, publishing companies implemented another round of expense cuts to bolster cash flow. There is a bright spot as Digital continues to perform strongly.

Overview

The NAB Show Stopper

Media investors are unpacking all of the information from last week’s National Association of Broadcaster’s (NAB) convention. There is a lot to digest given that there were over 1,400 exhibits, 140 new exhibitors this year. Because of the overwhelming number of exhibitors, many that go to Vegas for this annual convention do not go to the convention floor. It is a shame. There was a lot to see and learn. As Noble’s Media & Entertainment Analyst I walked the convention floor, which covers 4.6 million square feet of exhibit halls and meeting rooms. I stopped by booths and taped presentations to explain the new technologies, the plan for implementation of new services, and the prospect for revenue monetization. One important demonstration focused on the new broadcast standard, ATSC 3.0, the hope for a bright future for the television industry. This new standard should allow the industry to become more contemporary in terms of how its audience consumes video and information. In addition, it offers the ability for the industry to participate in new revenue streams, including Datacasting, which may become bigger than Retransmission revenue in the future.

In addition to touring the floor, I attended NAB panel discussions and hosted meetings with media management teams in a fireside chat format to discuss current business trends, the new technologies (including Artificial Intelligence (AI) and the new broadcast standard). In addition, these C-suite management teams provided their key takeaways from the NAB convention and offered why they participated in the conference this year. These discussions are available to you for free on Channelchek.com on April 27th in a virtual conference. In this upcoming Channelchek Takeaway Series on the NAB Show, I offer my key takeaways, including the current advertising outlook, my take on the monetization of the new technologies and what media investors should do now given the current economic and advertising environment. Your free registration to this informative event is available here.

This report highlights the performance of the media sectors over the past 12 months and past quarter. Overall, media stocks struggled in the past year, but there has been some improved quarterly performance, particularly in Digital Media and Broadcast Television, discussed later. All media stocks are struggling to offset losses over the course of the past year with trailing 12 months stocks down in the range of 5% on the low end to down 68% on the high end. The best performing sector in the past 12 months were Social Media stocks, down 5% versus the general market decline of 9% over the comparable period.

In the first quarter, stock performance was mixed. The best performers in the traditional media sectors were Broadcast Television stocks, up nearly 10% versus the general market which increased 7% in the comparable period. But, the individual TV stock performance reflected a different story, explained later in this report. The worse performer for the quarter were the radio stocks, driven by a Wall Street downgrade of one of the leading radio broadcasters. The Digital Media stocks had another good performance. We believe that stock performance will be a roller coaster for at least another quarter or two as the weight of the Fed rate increases begin to adversely affect the economy.

While National advertising has remained weak, we believe that Local advertising is now beginning to moderate as well. The Local advertising weakness appears to be in the smaller markets as well as the larger markets. This is somewhat different than the most recent economic cycles whereby the smaller markets were somewhat resilient. It seems that the smaller markets are feeling the adverse affects from inflation, rising employment costs and tightening bank credit. In our view, the disappointing advertising outlook likely will cause second quarter revenue estimates to come down, creating a difficult environment for media stocks. As such, we encourage investors to be opportunistic and take an accumulation approach to building positions for the prospective economic and advertising improvement. Our favorites have digital media exposure, given that we expect Digital Advertising (while softening as well) will be more resilient than traditional advertising mediums. Our favorites include Travelzoo (TZOO), Townsquare Media (TSQ), Harte Hanks (HHS), E.W. Scripps (SSP), and Direct Digital (DRCT).

Digital Media

Head fake?

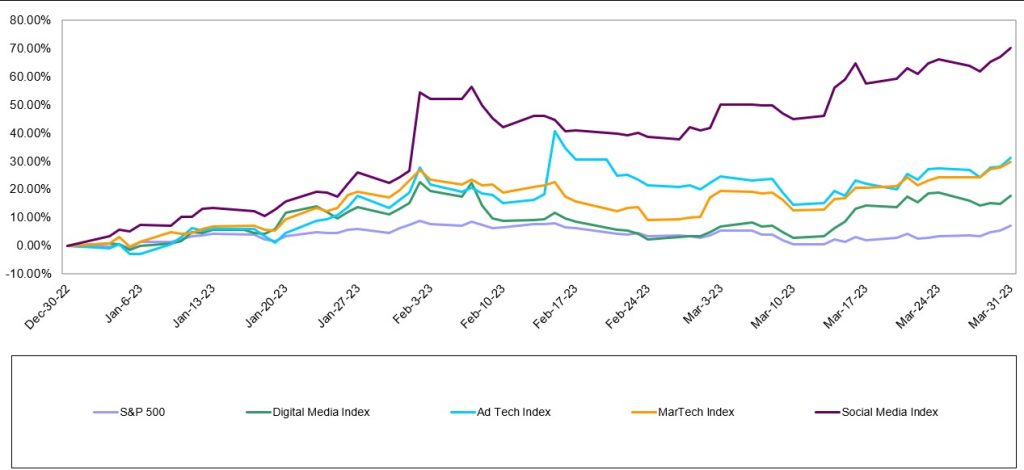

Last quarter we wrote that the S&P 500 increased for the first time since the fourth quarter of 2021 and that we were beginning to see signs of life in Noble’s Internet and Digital Media Indices as well. Those signs of life continued to bear fruit throughout the first quarter, as every one of Noble’s Internet and Digital Media Indices not only finished the quarter up, but significantly outperformed the S&P 500. Figure #1 LTM Digital Media Performance highlights that many of the Digital Media sectors are now approaching year earlier levels given the most recent favorable performance. The best performing index was Noble’s Social Media Index, which increased by 70% in the first quarter of 2023, followed by Noble’s Ad Tech Index (+31%), MarTech Index (+30%), and Digital Media Index (+18%).

Figure #1 LTM Digital Media Performance

Source: Capital IQ

Noble’s Indices are market cap weighted, and we attribute the strength of the Social Media Index to its largest constituent, Meta Platforms (META; a.k.a. Facebook) whose shares increased by 76% in the first quarter. Figure #2 Q1 Digital Media Performancehighlights the first quarter performance for the digital stocks.Meta’s management stirred interest in the shares from its 4Q 2022 earnings call when they spent most of their time talking about “efficiency”, which investors interpreted to mean that Meta was newly focused on profitability. After a relatively disastrous 3Q 2022 earnings call, after which shares fell by 25%, the company demonstrated on its 4Q 2022 earnings call that it clearly had gotten the message: investors were not enamored about the company’s plans in October 2022 to spend billions of dollars to develop its Metaverse initiatives. Rather, on its fourth quarter call, management focused on driving its short form video initiative, Reels (i.e., becoming more TikTok like), reducing its headcount by reducing layers of management, lowering its operating expenses and reducing its capital expenditures. Investors applauded this newfound focus on profitability and shares rebounded from a low of $88.90 per share in early November to $211.94 at the March quarter-end.

The next best performing index was Noble’s Ad Tech Index which increased by 31% during 1Q 2023. Fourteen of the 23 stocks in the index were up in the first quarter. Standouts during the quarter were Integral Ad Science (IAS; +62%) and Perion Networks (PERI; +56%). Integral Ad Science exceeded expectations in its fourth quarter results and guided to better-than-expected results in 1Q 2023. The company continues to expand its product suite, scale its social media offerings (i.e., for TikTok) and is well positioned to continue to benefit from the shift from linear TV to connected TV (CTV). Perion shares continued their winning: Perion was the only ad tech stock whose shares were up in 2022. Perion’s 56% increase in 1Q 2023 reflected beat on both revenues (by 2%) and EBITDA (by 10%) as well as improved guidance for 1Q 2023. Perion’s profitability increased significantly in 2022, with EBITDA nearly doubling (+90%) from 2021 ($70M) to 2022 ($132M).

Noble’s MarTech Index increased by 30% with 14 of the 22 stocks in the index posting increases in 1Q 2023. The best performing stocks were Qualtrics (XM; +70%) Sprinklr (CXM; +59%), Salesforce (CRM; +51%), Hubspot (HUBS; +48%) and Yext (YEXT; +47%). Qualtrics agreed to be acquired for $12.5 billion by Silver Lake and the Canadian Pension Plan Investment Board, which came at a 73% premium to its 30-day volume weighted stock price. Sprinklr beat revenue expectations and significantly beat EBITDA expectations (doubling the Street expectations) and guided to a current year forecast that focuses more on efficiency and profitability.

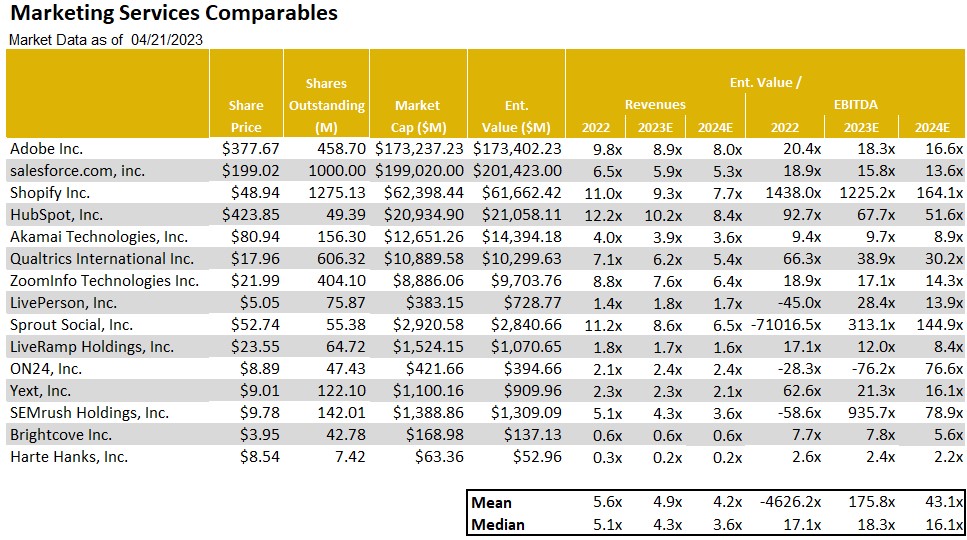

MarTech stocks have been victims of their own success. Two years ago at this time the sector was trading at 11.3x forward revenue estimates, and a year ago the group was trading at 6.5x forward revenues. Today the group trades at 4x forward revenues and investors appear to be wading back into the sector. Figure #3 Marketing Tech Comparables highlights the compelling stock valuations.One of the laggards in the sector has been Harte Hanks (HHS), which declined 20% in the first quarter. We believe that the shares have not gained traction following the successful rebound toward profitability in 2022. The shares advanced a powerful 136% in 2022 from lows in May to highs achieved in August 2022. Since that time, investors appear to be taking chips off the table. In our view, the HHS shares appear to be oversold. Its business appears to be resilient. Given the recent weakness in the shares, the shares appear to be undervalued and offer a favorable risk reward relationship. As such, the HHS shares are among our favorites in the sector.

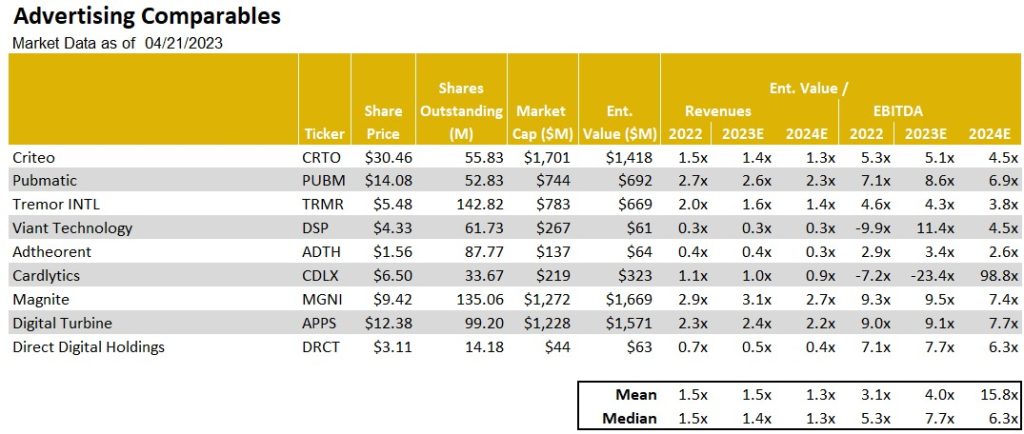

Another one of our current favorites is Direct Digital Holdings (DRCT). As Figure #4 Advertising Tech Comparables illustrates, the DRCT shares trade in line with the averages for the group at roughly 5.4 times 2024 adj. EBITDA. Notably, the company recently restated upward its 2022 full year revenue and adj. EBITDA results. Given the favorable operating momentum, we raised our full year 2023 and 2024 revenue and adj. EBITDA estimates, keeping our previous growth estimates. With the higher 2024 adj. EBITDA, we tweaked upward our price target from $5.50 to $6.00. Given a favorable fundamental outlook and compelling stock valuation, we view the shares as among our favorites.

Finally, Noble’s Digital Media Index, while lagging that of its digital peers at an 18% increase, significantly outperformed the S&P 500 (+7%), with a broad based recovery in which 9 of the sector’s 11 stocks increased during 1Q 2023. The best performing stock was Spotify (SPOT; +69%), whose revenues fell short of expectations by less than 1%, significantly beat consensus Street EBITDA expectations by $58M and more importantly pivoted towards demonstrating operating leverage. Spotify, which posted an EBITDA loss of nearly $500 billion in 2022, is expected to generate $650 billion in EBITDA in 2024, according to Street estimates. A deteriorating ad market in 2022 combined with higher interest rates likely prompted the company to shift its priorities to running a profitable company and doing it more quickly and with some urgency. The second best performing stock was Travelzoo (TZOO; +36%), as the company’s 4Q 2022 revenues and EBITDA increased by 31% and 328%, respectively. Notably, Travelzoo’s EBITDA came in 58% higher than Street consensus. The company appears to be benefiting from pent up travel demand for travel and management highlighted the opportunity for margin expansion in the coming quarters. Given the favorable outlook, we raised our price target to $10. Near current levels, the TZOO shares appear to offer above average returns and we reiterate our Outperform rating.

Figure #2 Q1 Digital Media Performance

Source: Capital IQ

Figure #3 Marketing Tech Comparables

Source: Eikon, Company filings & Noble estimates

Figure #4 Advertising Tech Comparables

Source: Eikon, Company filings & Noble estimates

Traditional Media

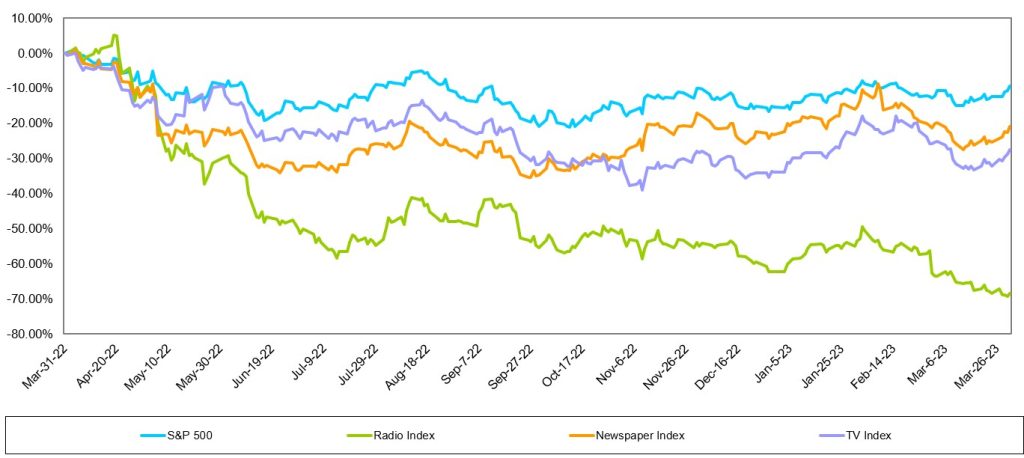

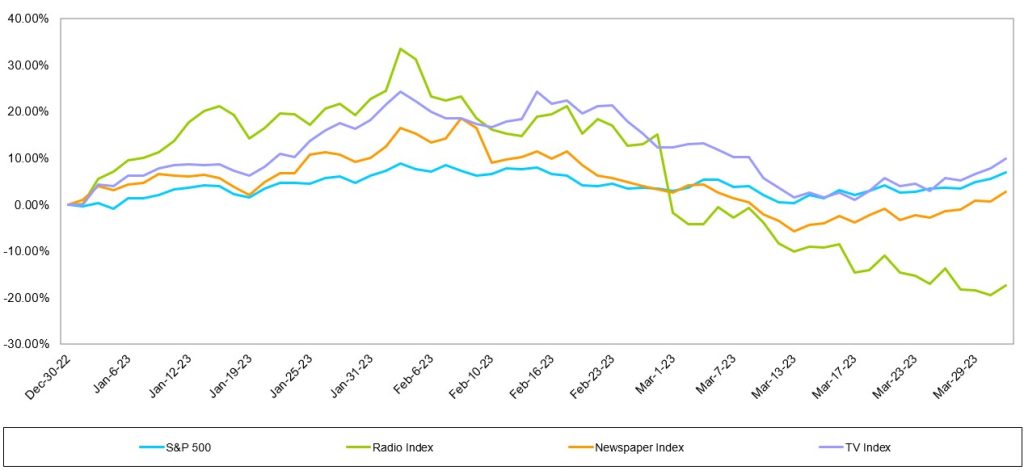

As Figure #5 LTM Traditional Media Performance illustrates, these stocks have struggled to gain sea legs, trending lower over the course of the past year. All traditional media sectors have underperformed over the past year, with Radio the poorest performing group. As Figure #6 Q1 Traditional Media Performance illustrates, only the TV Broadcast stocks edged out the general market performance in the latest quarter.

Figure #5 LTM Traditional Media Performance

Source: Capital IQ

Figure #6 Q1 Traditional Media Performance

Source: Capital IQ

Television Broadcast

Weak current revenue trends

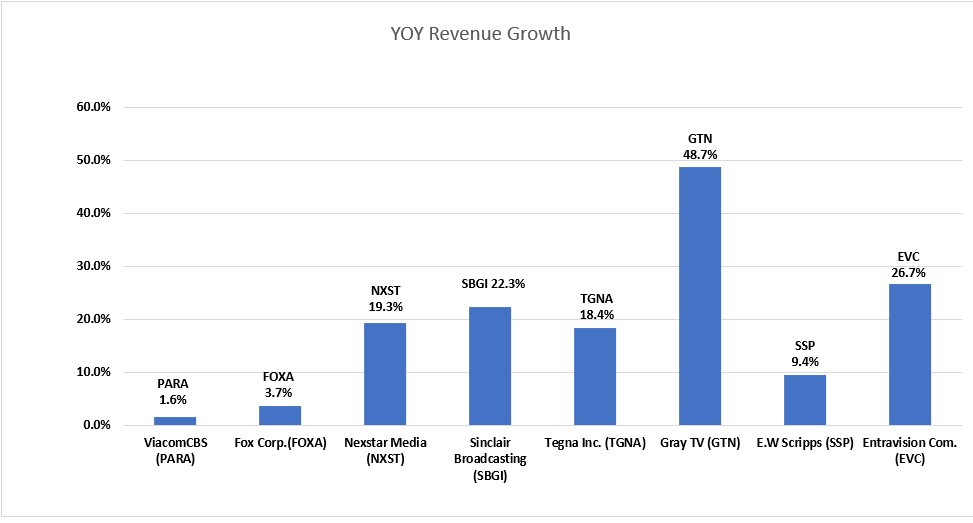

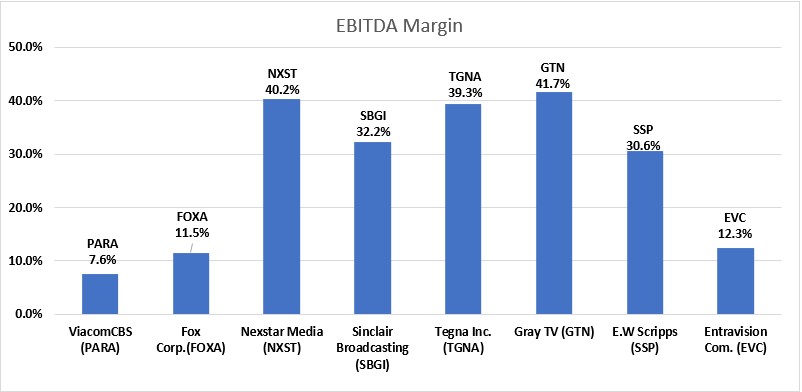

As illustrated in the previous chart, the TV stocks outperformed the general market in the first quarter. This market cap weighted index masked the performance of many poor performing stocks in the quarter. Sinclair Broadcasting (SBGI; up 10%), Entravision (EVC; up a strong 26%), and Fox (FOX; up 12%) were among the best performing stocks and favorably influenced the TV index in the quarter. But, there were many poor performing stocks including E.W. Scripps (SSP; down 29%), Gray Television (GTN; down 22%) and Tegna (TGNA; down 20%). We believe that there was heightened interest in Entravision given its favorable Q1 results which was fueled by its fast growing Digital business. Figure #7 TV Q4 YoY Revenue Growth illustrates the Entravision’s Q4 revenue performance was among the best in the industry. While Entravision was among the best revenue performers, its margins are below that of its peer group as illustrated in Figure #8 TV Q4 EBITDA Margins. This is due to the accounting treatment of its Digital revenues given that it is an agency business. Given that Digital represents roughly 80% of the company’s total company revenue, we plan to put the EVC shares into the Digital Media sector to more accurately reflect its business. The poorer performing stocks are among the higher debt levered in the industry. As such, we believe the underperformance reflects concern of a slowing economy and investors flight to quality in the sector.

We do not believe that we are out of the woods with the TV stocks and the market is expected to be volatile. The advertising environment appears to be deteriorating given weakening economic conditions. There are bright spots which include some improvement in the Auto category. Dealerships appear to be stepping up advertising given higher inventory levels. In addition, broadcasters appear optimistic about Political advertising, which could begin in the third quarter 2023. There is a planned Republican presidential candidate debate scheduled in August. As such, there is some promise that candidates will advertise in advance of that debate and into the fourth quarter given the early primary season. We do not believe that Political and Auto will be enough to offset the weakness in National and in the weakening Local category. In our view, Q2 and full year 2023 estimates are likely to come down. Furthermore, we believe that broadcasters will be shy about predicting Political advertising even into 2024 given the past disappointments in management forecasts in the last Political cycle.

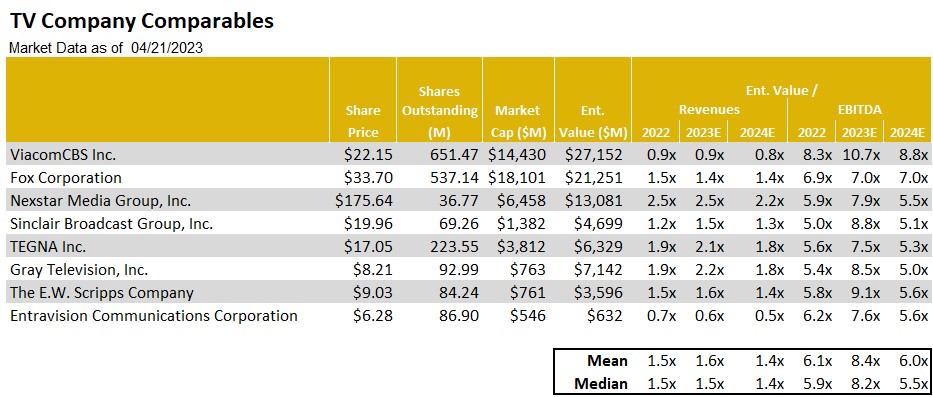

We encourage investors to take an accumulation approach to the sector. Notably, as Figure #9 TV Comparables highlights, nearly all of the stocks are trading near each other, with the exception of the larger media stocks. In our view, the valuations are near recession type valuations and appear to have limited downside risk. Our current favorite is E.W. Scripps (SSP). While the company is not immune to the current weak advertising environment, we believe that there is a favorable Retransmission revenue opportunity as 75% of its subscribers are due in the next 12 months. In addition, we believe that Retransmission margins will improve. Given the relatively small float for the shares, the SSP shares tend to underperform when the industry is out of favor, but then outperform when the industry is back in favor. In our view, the SSP shares offer a favorable risk/reward relationship and top our favorites in the sector.

Figure #7 TV Q4 YoY Revenue Growth

Source: Eikon & Company filings

Figure #8 TV Q4 EBITDA Margins

Source: Eikon & Company filings

Figure #9 TV Comparables

Source: Noble Estimates & Eikon

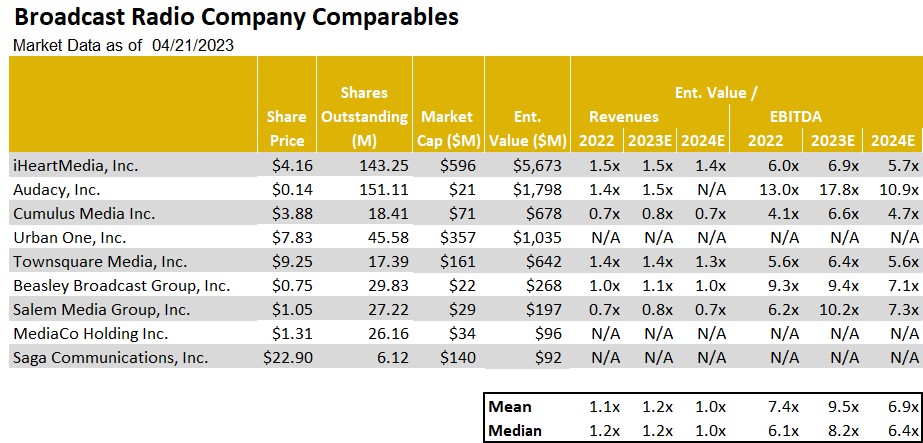

Radio Broadcasting

All out of love

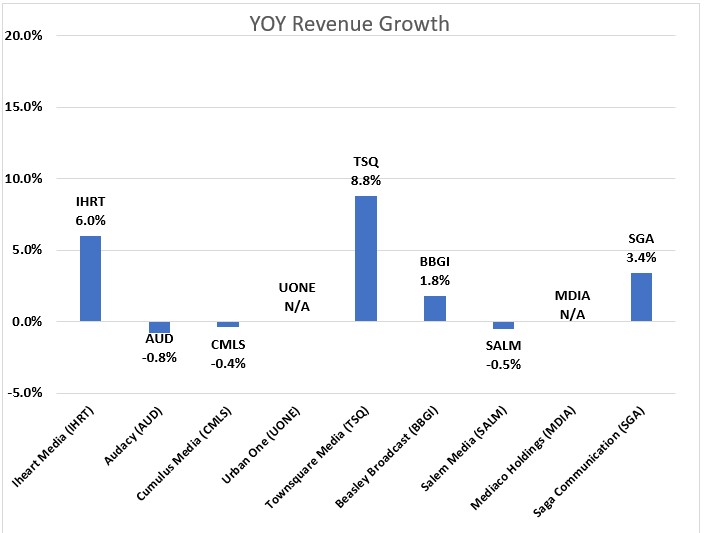

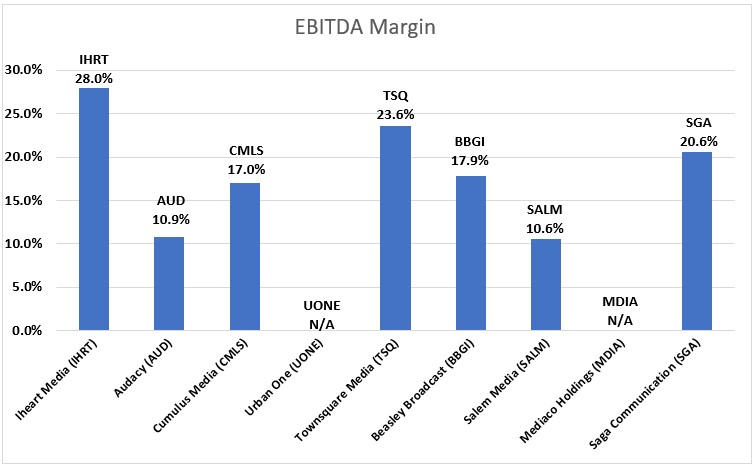

The Radio stocks had another tough quarter, down 17% versus a 7% gain for the general market. Notably, there was a wide variance in the individual stock performance, with the largest stocks in the group having the worst performance in the quarter, including Audacy (AUD; down 40%), Cumulus Media (CMLS; down 41%) and iHeart Media (IHRT; down 36%). The first quarter stock performance did not appear to reflect the fourth quarter results. As Figure #10 Radio Industry Q4 YoY Revenue Growth illustrates, revenues were relatively okay, with some exceptions. Some of the larger Radio companies which have a large percentage of National advertising, underperformed relative to the more diversified Radio companies, especially those with a strong Digital segment presence. Figure #11 Radio Industry Q4 YoY EBITDA Margins illustrate that the margins for the industry remain relatively healthy.

The weakness in the Radio stocks was fueled in the quarter from a downgrade to under perform on the shares of iHeart by a Wall Street firm. Many radio stocks were down in sympathy. The analyst attributed the downgrade to the current macro environment and its heavy floating rate debt burden. The company is not expected to generate enough free cash flow to de-lever its balance sheet. We believe the downgrade as well as the excessive debt profile of Audacy, another industry leader which likely will need to restructure, sent all radio stocks tumbling. Some stocks performed better than others. While Cumulus Media’s debt profile is not as levered as iHeart or Audacy, the shares were caught in the net of a weak advertising outlook. Cumulus is among the most sensitive to National advertising, which currently continues to be weak.

Some of our favorite stocks which are diversified and have developing digital businesses performed better. Those stocks included Townsquare Media (TSQ; up 10%), and Salem Media (SALM; up 4%). Notably, while the shares of Beasley Broadcasting (BBGI) were down 10%, the shares performed better than the 17% decline for the industry in the quarter. Importantly, Beasley recently provided favorable updated Q1 guidance for the first quarter. Q1 revenues are expected to increase 1% to 2.5% and EBITDA growth is expected to be in the range of 40% to 50%, significantly better than our estimates. Furthermore, management provided a sanguine outlook for 2023 and 2024. Digital revenue is expected to reach 20% to 30% of total revenue with a goal of reaching 40% in 2024. By comparison, Digital revenue was 17% of total revenue in the fourth quarter 2022. Furthermore, the company is sitting on roughly $35 million in cash. It has opportunistically repurchased $10 million of its bonds at a significant discount. We believe that it is likely to maintain a strong cash position given the economic uncertainty.

We view Townsquare Media (TSQ), Salem Media (SALM) and Beasley Broadcast (BBGI) as among our favorites in the industry given the diverse revenue streams. While these companies are not immune to the economic headwinds, we believe that its Digital businesses should offer some ballast to its more sensitive Radio business. In the case of Salem, 30% of its revenues are relatively stable with block programming. As Figure #12 Broadcast Radio Comparables illustrates, the shares of Townsquare are among the cheapest in the industry, trading below peer group averages. Notably, the company instituted a hefty dividend. As a result, investors get paid while we await a favorable upturn in fundamentals. As such, the shares of TSQ tops our list of favorites.

Figure #10 Radio Industry Q4 YoY Revenue Growth

Source: Eikon & Company filings

Figure #11 Radio Industry Q4 YoY EBITDA Margins

Source: Eikon & Company filings

Figure #12 Broadcast Radio Comparables

Source: Noble estimates & Eikon

Publishing

Advertising takes a hit

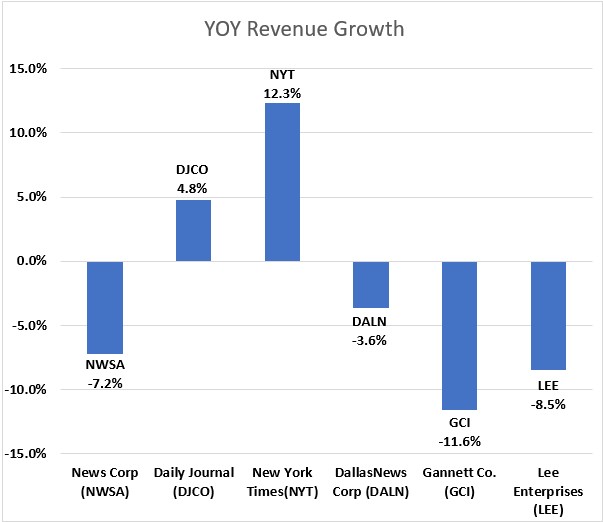

After a period of moderating revenue trends, Publishers reported a weakened advertising environment. As illustrated in Figure #13 Publishing Industry YOY Revenue Growth, illustrates that revenue trends deteriorated with Print advertising taking a nose dive. This trend was illustrative in the results from Lee Enterprises, one of our current favorites in the sector. After a fiscal fourth quarter flat revenue performance, the company reported a 8.5% decline in its fiscal first quarter. The Q1 revenue performance reflected an 18.5% decrease in Print advertising, an acceleration in the rate of the 11% decline in the previous quarter.

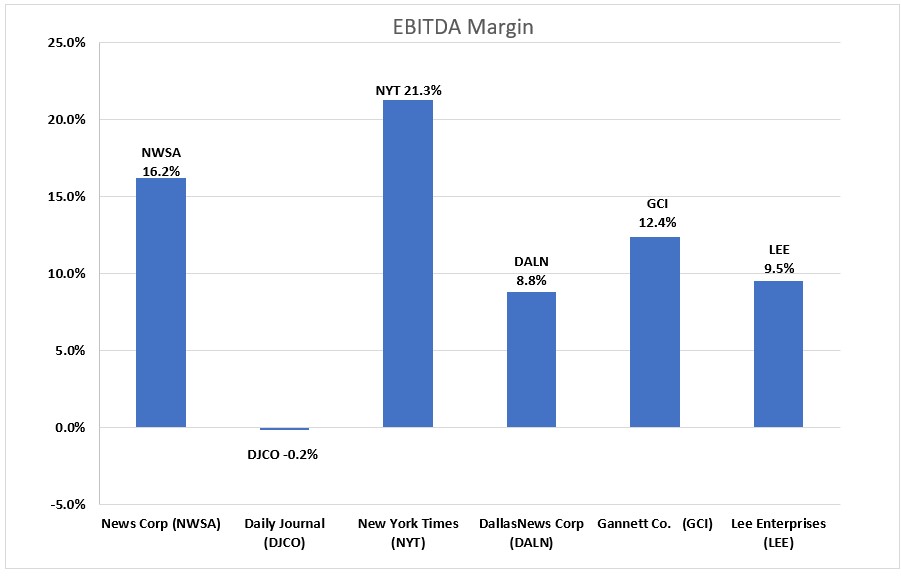

The surprisingly weak quarter hit the company’s adj. EBITDA margins. Traditionally, Lee maintained some of the best margins in the industry. As Figure #14 Q4 Publishing Industry EBITDA Margins illustrates, the company fell in ranking to among the lowest in the sector. Importantly, in spite of the revenue weakness, the company maintains its previous adj. EBITDA guidance of $94 million to $100 million. To achieve its cash flow target in light of the soft revenue outlook, Lee implemented a round of expense cuts to bolster cash flow. Cost reductions are expected to result in $40 million of savings in FY23, and $60 million in annualized savings going forward. While we are disappointed that the company’s Print business is not moderating as previously expected, the company’s Digital businesses remain favorably robust. In addition, its Digital business is turning toward contributing margins. As such, we remain sanguine about the company’s digital transition.

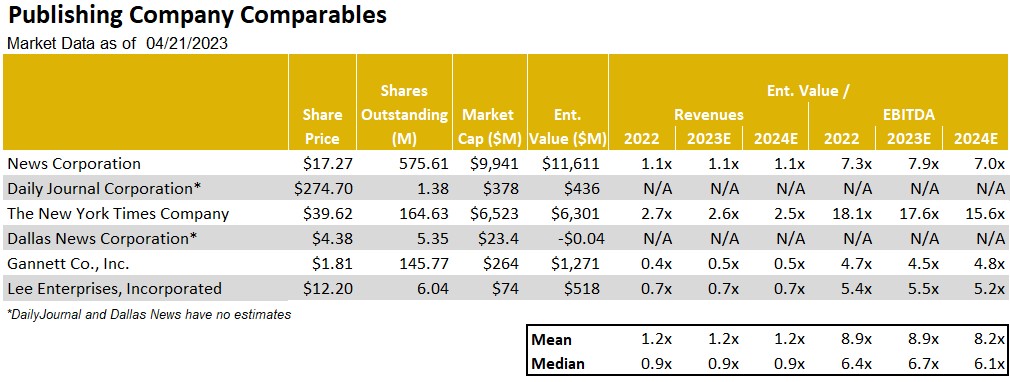

As Figure #15 Publishing Comparables highlights, there is a wide gap between the valuation of the New York Times (NYT) and the rest of the industry, including Lee. While the highly debt levered shares of Gannett appear cheaper, we believe that Lee has a more favorable debt profile with a fixed 9% annual rate, no fixed principal payments, no performance covenants and a 25 year maturity. With the shares trading at 5.3 times our 2024 adj. EBITDA estimate compared with 15.4 times at the New York Times, we believe that there is limited downside risk in the LEE shares. Furthermore, we believe that the company is well positioned as economic and advertising prospects improve. Given the company’s favorable outlook for its Digital transition, we believe that the shares should close the gap in valuations with the leadership stock in the group. Consequently, the shares of LEE are among our favorite play for an improving economic outlook.

Figure #13 Publishing Industry YoY Revenue Growth

Source: Eikon & Company filings

Figure #14 Q4 Publishing Industry EBITDA Margins

Source: Eikon & Company filings

Figure #15 Publishing Comparables

Source: Noble estimates & Eikon

For more information on companies mentioned in this report click on the following:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

AI-Generated Spam May Soon Be Flooding Your Inbox – It Will Be Personalized to Be Especially Persuasive

Each day, messages from Nigerian princes, peddlers of wonder drugs and promoters of can’t-miss investments choke email inboxes. Improvements to spam filters only seem to inspire new techniques to break through the protections.

Now, the arms race between spam blockers and spam senders is about to escalate with the emergence of a new weapon: generative artificial intelligence. With recent advances in AI made famous by ChatGPT, spammers could have new tools to evade filters, grab people’s attention and convince them to click, buy or give up personal information.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of John Licato, Assistant Professor of Computer Science and Director of AMHR Lab, University of South Florida.

As director of the Advancing Human and Machine Reasoning lab at the University of South Florida, I research the intersection of artificial intelligence, natural language processing and human reasoning. I have studied how AI can learn the individual preferences, beliefs and personality quirks of people.

This can be used to better understand how to interact with people, help them learn or provide them with helpful suggestions. But this also means you should brace for smarter spam that knows your weak spots – and can use them against you.

Spam, Spam, Spam

So, what is spam?

Spam is defined as unsolicited commercial emails sent by an unknown entity. The term is sometimes extended to text messages, direct messages on social media and fake reviews on products. Spammers want to nudge you toward action: buying something, clicking on phishing links, installing malware or changing views.

Spam is profitable. One email blast can make US$1,000 in only a few hours, costing spammers only a few dollars – excluding initial setup. An online pharmaceutical spam campaign might generate around $7,000 per day.

Legitimate advertisers also want to nudge you to action – buying their products, taking their surveys, signing up for newsletters – but whereas a marketer email may link to an established company website and contain an unsubscribe option in accordance with federal regulations, a spam email may not.

Spammers also lack access to mailing lists that users signed up for. Instead, spammers utilize counter-intuitive strategies such as the “Nigerian prince” scam, in which a Nigerian prince claims to need your help to unlock an absurd amount of money, promising to reward you nicely. Savvy digital natives immediately dismiss such pleas, but the absurdity of the request may actually select for naïveté or advanced age, filtering for those most likely to fall for the scams.

Advances in AI, however, mean spammers might not have to rely on such hit-or-miss approaches. AI could allow them to target individuals and make their messages more persuasive based on easily accessible information, such as social media posts.

Future of Spam

Chances are you’ve heard about the advances in generative large language models like ChatGPT. The task these generative LLMs perform is deceptively simple: given a text sequence, predict which token – think of this as a part of a word – comes next. Then, predict which token comes after that. And so on, over and over.

Somehow, training on that task alone, when done with enough text on a large enough LLM, seems to be enough to imbue these models with the ability to perform surprisingly well on a lot of other tasks.

Multiple ways to use the technology have already emerged, showcasing the technology’s ability to quickly adapt to, and learn about, individuals. For example, LLMs can write full emails in your writing style, given only a few examples of how you write. And there’s the classic example – now over a decade old – of Target figuring out a customer was pregnant before her father knew.

Spammers and marketers alike would benefit from being able to predict more about individuals with less data. Given your LinkedIn page, a few posts and a profile image or two, LLM-armed spammers might make reasonably accurate guesses about your political leanings, marital status or life priorities.

Our research showed that LLMs could be used to predict which word an individual will say next with a degree of accuracy far surpassing other AI approaches, in a word-generation task called the semantic fluency task. We also showed that LLMs can take certain types of questions from tests of reasoning abilities and predict how people will respond to that question. This suggests that LLMs already have some knowledge of what typical human reasoning ability looks like.

If spammers make it past initial filters and get you to read an email, click a link or even engage in conversation, their ability to apply customized persuasion increases dramatically. Here again, LLMs can change the game. Early results suggest that LLMs can be used to argue persuasively on topics ranging from politics to public health policy.

Good for the Gander

AI, however, doesn’t favor one side or the other. Spam filters also should benefit from advances in AI, allowing them to erect new barriers to unwanted emails.

Spammers often try to trick filters with special characters, misspelled words or hidden text, relying on the human propensity to forgive small text anomalies – for example, “c1îck h.ere n0w.” But as AI gets better at understanding spam messages, filters could get better at identifying and blocking unwanted spam – and maybe even letting through wanted spam, such as marketing email you’ve explicitly signed up for. Imagine a filter that predicts whether you’d want to read an email before you even read it.

Despite growing concerns about AI – as evidenced by Tesla, SpaceX and Twitter CEO Elon Musk, Apple founder Steve Wozniak and other tech leaders calling for a pause in AI development – a lot of good could come from advances in the technology. AI can help us understand how weaknesses in human reasoning might be exploited by bad actors and come up with ways to counter malevolent activities.

All new technologies can result in both wonder and danger. The difference lies in who creates and controls the tools, and how they are used.

The amount of investment in initial public offerings (IPOs) during March-April has jumped from January-February levels. Globally, the pick-up in IPOs is linked to the uptick in stock prices, which has allowed companies to tap into investor appetite for newer listings. A sizeable percentage of the offerings are in Asia, but Europe and the U.S. have experienced a surge as well. Activity during the first two months of 2023 had ground to a halt; new data compiled by Bloomberg demonstrates a much faster trend.

To date, there has been $25 billion worth of IPOs worldwide in March and April; this is nearly twice the amount transacted during the prior two months of the year. Companies headquartered from Hong Kong to Milan have put up their “Going Public” signs up as market volatility declined. The uptick in IPOs in Asia substantially moved the needle as non-U.S. exchanges accounted for nearly 80% of new share sales during April.

The uptick in Europe can’t be ignored either; European listings are higher by a wide margin compared to earlier in the year. The activity in the U.S. is not as robust but also noteworthy, as concern about a recession had been creating caution among potential U.S. issuers.

In a quote published by Bloomberg News, Jason Manketo global co-head of the law firm Linklaters’ equities practice said, “We are beginning to see green shoots of activity with companies restarting processes that were on hold, but there is still a fair degree of uncertainty in the market.” Mankel added, “The buy side is keen to see results for a couple of quarters before committing to an IPO. This means the potential pipeline of some 2023 deals has been moved out to 2024.”

Leaders

Statistically, Asia is where a great deal of the action is in the world today. But the activity is different, perhaps more appealing, than last year. In 2022 the vast majority of large deals were concentrated in mainland China; over the past two months, issuance is coming from a broader representation of Asia.

“The IPO market is coming back gradually and slowly. It is not 100% back yet, but there are signs of life and renewed vigor,” said James Wang, co-head of equity capital markets at Goldman Sachs Group Inc. in Asia ex-Japan.

A couple of nickel producers from Indonesia surged as they went public. And in Japan, as part of the country’s largest IPO since 2018, Rakuten Bank Ltd. soared after it raised 83.3 billion yen ($623 million). And KKR & Co.-backed Chinese liquor company ZJLD Group Inc. as recently as April 20th, priced Hong Kong’s largest offering in 2023.

Europe Wakes Up

Europe’s IPO market had been dragging, with activity in 2023 down about 12% from the same period last year as Russia’s invasion of Ukraine brought new listings to a screeching halt.

Also weighing on the market, poor IPO returns have been a deterrent for investors. Portfolio managers had been in the drivers seat insisting on bargains for less proven companies. In March the sudden meltdown of financial firm Credit Suisse, ignited a global market rout, this added to investor worries about interest rates and inflation; the event also made it less attractive for companies to try and attract a favorable price.

But there are growing signs of fear lifting. Most notably, Lottomatica SpA, the Italian gambling company backed by Apollo Global Management Inc., opened the books last week for a €600 million ($657 million) IPO, becoming the third large firm to tap European exchanges this year. Additionally, German web-hosting company Ionos SE and electric motor component maker EuroGroup Laminations SpA have managed to raise more than $400 million in the region, though both stocks have struggled after debuting.

U.S. Uptick

While IPO activity in the U.S. is not as robust, there has been a huge uptick as well. The IPO calendar for U.S. exchanges shows 20 priced deals totalling $751.5 billion, and 29 new filings. This is an acceleration after only $4.1 billion had been raised for companies listing on U.S. exchanges during the first two months of 2023.

Take Away

Globally companies are finding it more worthwhile to tap capital from the equity markets via IPO. While the most growth is greater Asia, Europe and the U.S. see a significant uptick as well. Whether this trend continues and represents, a buying opportunity seems to hinge on recession concerns. Many forecasters are now calling for a much more mild recession than previously expected.

A Focus on Profitability Drives A Strong Start to the Year