IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) announced today that it plans to report its third quarter 2023 financial results after the market closes on November 13, 2023.

The company also plans to host a teleconference to discuss its results on November 13, 2023, at 4:00 PM Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined to the Salem Media Group Third Quarter 2023 call or listen to the webcast.

A replay of the teleconference will be available through November 27, 2023, and can be heard by dialing (800) 770-2030 – replay pin number 2413416, or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

ABOUT SALEM MEDIA GROUP:

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com.

For more than 70 years, Vectrus has provided critical mission support for our customers’ toughest operational challenges. As a high-performing organization with exceptional talent, deep domain knowledge, a history of long-term customer relationships, and groundbreaking technical expertise, we deliver innovative, mission-matched solutions for our military and government customers worldwide. Whether it’s base operations support, supply chain and logistics, IT mission support, engineering and digital integration, security, or maintenance, repair and overhaul, our customers count on us for on-target solutions that increase efficiency, reduce costs, improve readiness, and strengthen national security. Vectrus is headquartered in Colorado Springs, Colo., and includes about 8,100 employees spanning 205 locations in 28 countries. In 2021, Vectrus generated sales of $1.8 billion. For more information, visit the company’s website at www.vectrus.com or connect with Vectrus on Facebook, Twitter, and LinkedIn.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

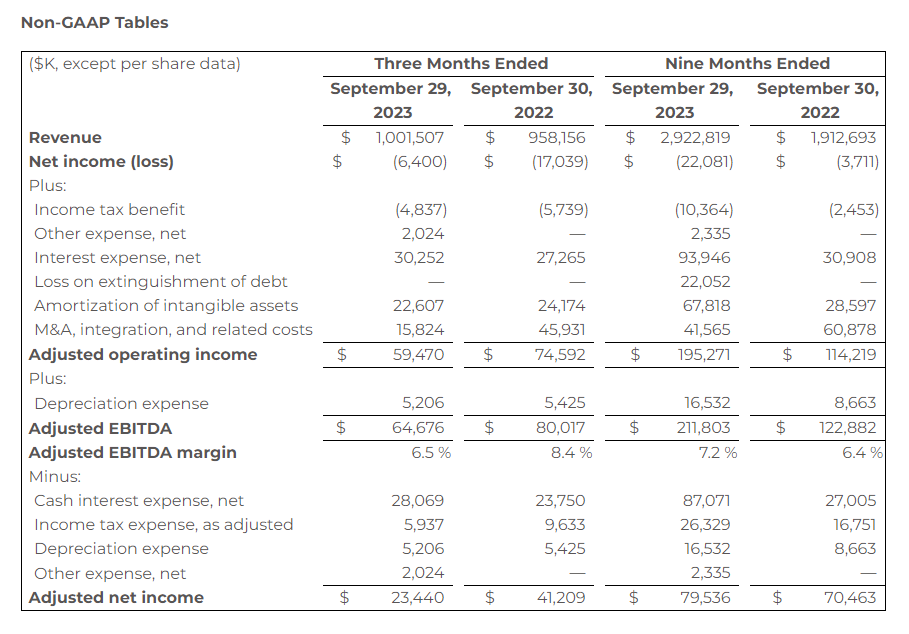

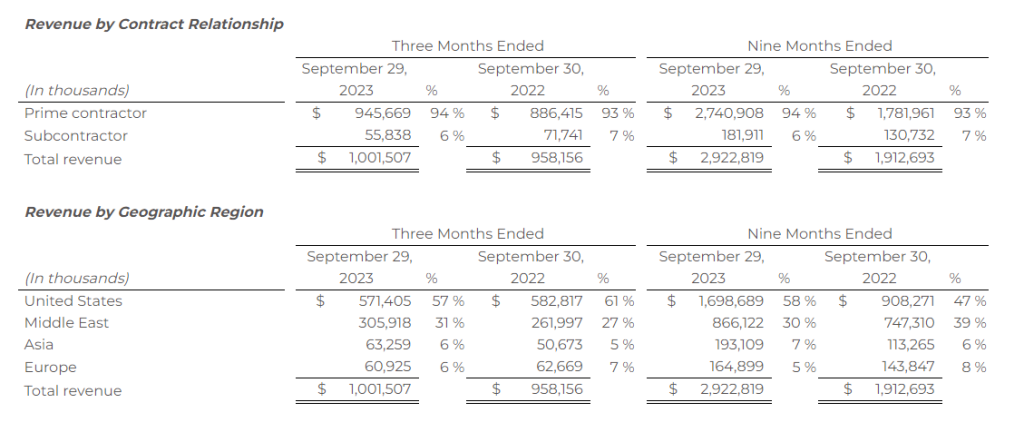

3Q23 Results. Record revenue of $1.0 billion was up 4.5% y-o-y, and above our $965 million forecast. Adjusted EBITDA came in at $64.7 million, versus $79 million in 3Q22 and our $64 million estimate. Adjusted diluted EPS was $0.73 compared to $1.33 last year and our $0.90 estimate.

Some Headwinds. 3Q23 results were impacted by a couple items, including contract mix and performance on certain integrated electronic security programs. In addition, the strong 2Q23 benefitted from the pull forward of some business that was expected to occur in the just completed quarter.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Energy Fuels is a leading U.S.-based uranium mining company, supplying U3O8 to major nuclear utilities. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is ramping up commercial-scale production of REE carbonate. Its corporate offices are in Lakewood, Colorado, near Denver, and all its assets and employees are in the United States. Energy Fuels holds three of America’s key uranium production centers: the White Mesa Mill in Utah, the Nichols Ranch in-situ recovery (“ISR”) Project in Wyoming, and the Alta Mesa ISR Project in Texas. The White Mesa Mill is the only conventional uranium mill operating in the U.S. today, has a licensed capacity of over 8 million pounds of U3O8 per year, has the ability to produce vanadium when market conditions warrant, as well as REE carbonate from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Alta Mesa ISR Project is also on standby and has a licensed capacity of 1.5 million pounds of U3O8 per year. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the U.S. and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development. The primary trading market for Energy Fuels’ common shares is the NYSE American under the trading symbol “UUUU,” and the Company’s common shares are also listed on the Toronto Stock Exchange under the trading symbol “EFR.” Energy Fuels’ website is www.energyfuels.com.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Higher uranium prices led to increased sales out of inventory. Uranium prices rose during the quarter with spot prices moving into the mid-seventies. While realized prices for Energy Fuel were only $58.18/lb. because of long-term contract pricing, it remains well above production costs, which management describes as “well below $50/lb.” Energy Fuels continues to meet its utility contracts through the sale of uranium out of inventory. Inventory levels (586,000 tonnes) are roughly half of the level at the start of the year (1,027,000 tonnes).

Financial results improve with uranium sales. 2023-3Q results were largely in line with expectations once nonrecurring gains are removed. Of course, the Energy Fuel story has never been about near-term results. Instead, the stock moves on corporate developments. And, while there have been some setbacks (REE supply issues, share dilution), the company has made steady progress. We look for the stock to do well as projections turn into cash flow, and as investors begin to realize the potential of rising uranium prices and the profitability of REE separation.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for nearly 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

3Q Results. Revenue totaled $483.7 million, up 4.2% year-over-year and up 4.3% sequentially, driven by higher populations and increased per diems. Net income was $13.9 million, or $0.12/sh versus $68.3 million, or $0.58 per share last year. Adjusted EPS was $0.14 for 3Q23 versus $0.08 for 3Q22. Adjusted EBITDA was $75.2 million, up from $68.4 million last year.

ICE Populations. Since the ending of Title 42 on May 11th, overall ICE populations are up 66% through the end of September. CoreCivic ICE populations are up by 4,729, or 84% over the same time frame. We believe this has been driven by management’s foresight in adding staff in anticipation of higher population levels. Reportedly, ICE populations have continued to rise.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Mining Slightly Down. Bit Digital produced 111.6 BTC during the month, a 14% decrease from last month due to an increase in network difficulty, a power utility mandated maintenance outage that temporarily reduced operating hash rate at one location, and the relocation of miners from one hosting location following the conclusion of that hosting agreement. The Company had an active hash rate of 2.0 EH/s compared to 1.19 EH/s last month.

Staking Side. The Company had approximately 12,752 ETH actively staked in native and liquid staking protocols as of October 31, 2023, with 12,352 ETH natively staked and 400 ETH deployed in liquid staking protocols. Bit Digital earned a blended APY of approximately 4.25% on its staked ETH position for the month compared to roughly 4.1% last month, and earned aggregate staking rewards of approximately 46.08 ETH.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Alvopetro Energy Ltd.’s vision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Michael Heim, Senior Vice President, Equity Research Analyst, Energy & Transportation, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production in the month of October was 1,839 boe/d, up from 1,203 boe/d in September. Production has been anemic in recent months due to partner nomination issues in the Cabure field and demand issues by Bahia Gas. The production increase, and the fact that it largely came from the Cabure field, is a positive indication that Alvopetro’s growth plans are getting back on track. Management has set a near-term goal of reaching 3,000 boe/d and a long-term goal of 5,833 boe/d.

Speaking of growth, results from a new oil well look positive. Alvopetro completed the BL-6 well in the Bom Lugar field. The well is averaging 13 boe/d, more that all other existing oil production. The Bom Lugar field could be an important field for the company as it seeks to expand operations and reduce dependency upon natural gas sales to Bahia Gas. We believe the success of the BL-6 well will lead to management putting additional resources into the Bom Lugar field.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Securities regulators have leverage risks in the multi-trillion dollar US Treasuries market back under the microscope. Recent remarks by Securities and Exchange Commission (SEC) Chair Gary Gensler signaled renewed urgency around curtailing destabilizing trading practices in the world’s largest bond market.

In a speech to financial executives, Gensler emphasized the systemic dangers posed by excessive leverage use among institutional government bond traders. He pointed to stresses witnessed during this year’s regional banking turmoil as a reminder of such hazards manifesting and causing wider contagion.

Regulators worry traders combining high leverage with speculative strategies in Treasuries could trigger severe market dysfunction during times of volatility. This could then spill over to wreak havoc in the broader financial system given Treasuries’ status as a global haven asset class.

Gensler advocated for SEC proposals intended to impose tighter control over leverage and trading risks. These include requiring central clearing for Treasuries transactions and designating large proprietary trading institutions as broker-dealers subject to higher regulatory standards.

The SEC chief argues such reforms are vital to counterbalance the threat of destabilizing blowups in a foundational market underpinning global finance.

Among the riskier trading plays under scrutiny is the so-called basis trade where leverage magnifies bets exploiting slight pricing variations between Treasury futures and underlying bonds. While providing liquidity, regulators fret the strategy’s extensive borrowing leaves it vulnerable to violent unwinding in turbulent markets.

Warnings around the basis trade have intensified given concentration of risks among influential bond trading heavyweights. US regulators demand greater visibility into leverage levels across systemically-important markets to be able to detect emerging hazards.

Overseas authorities are also tightening oversight of leveraged strategies. The Bank of England recently floated measures to restrain risk-taking in British government bond markets that could destabilize the financial system.

However, Wall Street defenders argue the basis trade fulfills a valuable role in greasing trading and provides resilience during crises. They point to the strategy weathering last decade’s pandemic-induced mayhem in markets without mishap.

But SEC leadership remains unconvinced current patchwork regulation provides sufficient safeguards against excessive risk-taking. They emphasize the over-the-counter nature of Treasuries trading allows huge leverage buildup outside the purview of watchdogs.

Hence the regulatory push for greater transparency from large leveraged investors to facilitate continuous monitoring for dangers to system stability. Furthermore, shorter settlement timelines being phased in are meant to curb risk accumulation in the opaque Treasury secondary market.

While largely supportive of the abbreviated settlement schedule, Gensler noted challenges still abound on the foreign exchange side that demand close tracking.

Overall, the revived warnings from America’s top securities regulator underscore enduring concerns post-2008 crisis reforms did not fully address leverage-fueled excess in Treasury markets. Keeping a tight leash on potentially destabilizing trading practices remains a clear priority for policymakers focused on securing the financial system against shocks.

WeWork, once the most valuable startup in the United States with a peak valuation of $47 billion, filed for bankruptcy protection this week – a stunning collapse for a company that was the posterchild of the shared workspace industry.

Founded in 2010 by Adam Neumann and Miguel McKelvey, WeWork grew at breakneck speed by offering flexible office spaces for freelancers, startups and enterprises. At its peak in 2019, WeWork had 528 locations in 111 cities across 29 countries with 527,000 members.

The company was initially successful at attracting both customers and investors with its vision of creating communal workspaces. SoftBank, its biggest backer, poured in billions having bought into Neumann’s grand ambitions to revolutionize commercial real estate. WeWork was the cornerstone of SoftBank’s $100 billion Vision Fund aimed at taking big bets on tech companies that could be mold-breakers.

However, WeWork’s model of taking long-term leases and renting out spaces short-term led to persistent losses. The company lost $219,000 an hour in the 12 months prior to June 2023. Occupancy rates are down to 67% from 90% in late 2020. Yet WeWork had $4.1 billion in future lease payment obligations as of June.

Problematic corporate governance and mismanagement under Neumann also came under fire. Eyebrow-raising revelations around Neumann such as infusing the company with a hard-partying culture and cashing out over $700 million ahead of the planned IPO while retaining majority control further eroded confidence.

The lack of a path to profitability finally derailed the company’s prospects when it failed to launch its Initial Public Offering in 2019. The IPO was expected to raise $3 billion at a $47 billion valuation but got postponed after investors balked at buying shares. Neumann was forced to step down as CEO.

Since the failed IPO, WeWork has tried multiple strategies to right the ship. It has attempted to renegotiate leases, cut thousands of jobs, sold off non-core businesses, and reduced operating expenses significantly. For example, it got $1.5 billion in financing in exchange for control of its China unit in 2022.

WeWork also tried changing leadership to infuse more financial discipline. It brought in real estate veteran Sandeep Mathrani as CEO in 2020. Mathrani helped cut costs but could not fix the underlying business model. He was replaced in 2022 by David Tolley, an investment banker and private equity executive.

Additionally, WeWork tried merging with a special purpose acquisition company (SPAC) in 2021 that valued the company at $9 billion. But the co-working space leader continued struggling with low demand and high costs.

Commercial real estate landlords also pose an existential threat by offering their own flexible workspaces. Large property owners like CBRE and JLL now provide custom office spaces. With recession looming, demand for flexible office space has waned further.

As part of the Chapter 11 bankruptcy filing, WeWork aims to restructure its debt and shed expensive leases. However, it faces an uphill battle to rebuild its brand and regain customers’ trust. The flexible workspace model also faces an uncertain future given hybrid work arrangements are becoming permanent for many companies.

WeWork upended the commercial real estate industry and had a meteoric rise fueled by stellar growth and lofty ambitions. But poor management and lack of profitability finally brought down a quintessential startup unicorn valued at $47 billion at its peak. The dramatic saga serves as a cautionary tale for unproven, cash-burning companies and overzealous investors fueling their growth.

Shein, the Chinese fast fashion juggernaut, is aiming to achieve a massive $80-90 billion valuation in its eventual US stock market debut according to sources familiar with the company’s IPO plans.

The online fashion retailer has quickly become one of the largest in the world on the back of its ultra-fast production cycles and rock bottom pricing. Shein boasts a selection of over 5,000 fashion items with over 1,000 new products added daily. This rapid launch cadence along with AI-driven fashion designs and targeted social media marketing have supercharged Shein’s popularity among Gen Z consumers.

Shein’s meteoric rise has made it one of the most valuable private companies in the world. The company hit a $100 billion valuation in its last funding round in 2021. However, subsequent secondary market trades of Shein shares revealed erosion in its value, with estimates between $50-60 billion earlier this year.

The firm is looking to capitalize on the growth in online shopping with its planned US stock exchange listing. Shein is aiming to raise around $2 billion from public market investors as it continues its quest for global fashion industry dominance.

Shein has not officially confirmed its IPO plans yet, but is said to be targeting the second half of 2023 for its market debut. The timing remains in flux given the recent stock market volatility and economic uncertainty.

Unlike most ecommerce firms, Shein has claimed profitability since its inception. The company boasts strong margins partly derived from minimal advertising spend. Shein instead relies extensively on social media influencers and word-of-mouth among its primarily Gen Z fanbase.

The Chinese company does not disclose its financials publicly, but reportedly generated over $16 billion in sales in 2021. It has also expanded aggressively in Europe, the US and other international markets. Shein’s app was the second most downloaded shopping app globally on iOS last year after Amazon.

However, Shein faces controversies around alleged labor rights violations, plagiarized designs, and environmental concerns related to its fast fashion model. Critics also argue the opacity around its operations and finances warrant closer regulatory scrutiny especially as it plans to go public.

Shein’s US IPO will be a key test of investor appetite for cash-burning technology unicorns in the current market. Chinese companies listing in the US also face tighter regulations now. A number of them have opted instead for Hong Kong and domestic China exchanges more recently.

Nonetheless, the online fashion giant has its sights set firmly on tapping into public markets to fuel its next wave of worldwide expansion. Shein aims to leverage its digital-first model and supply chain agility to continue eating market share from struggling traditional retailers.

If Shein manages to pull off a $90 billion IPO, it would rank as one of the largest US listings ever for a foreign company. The blockbuster offering could set the stage for Shein to disrupt the global fashion hierarchy dominated by H&M, Zara and other legacy incumbents.

Despite decades of effective environmental policy and improved air quality in the US, air pollution remains the greatest environmental health risk factor, contributing to 100,000 to 200,000 incremental deaths annually, primarily from fine particulate matter (PM2.5) derived from pollutants including vehicle and industrial emissions from fuel and biomasscombustion, cigarette smoke, volcanos, fires, and desert dust.

PM2.5 is inhaled into the lungs, spreading through the bloodstream to other organs, especially the kidney, which accumulates it during glomerular filtration, where it triggers NLRP3 inflammasome activation resulting in damaging inflammation and cell death (pyroptosis) leading to chronic kidney disease and its progression.

ZyVersa is developing Inflammasome ASC Inhibitor IC 100 which can inhibit up to 12 different inflammasomes (including NLRP3 inflammasomes) and their associated ASC specks which perpetuate damaging inflammation.

WESTON, Fla., Nov. 06, 2023 (GLOBE NEWSWIRE) — ZyVersa Therapeutics, Inc. (Nasdaq: ZVSA, or “ZyVersa”), a clinical stage specialty biopharmaceutical company developing first-in-class drugs for treatment of inflammatory and renal diseases, announces publication of an article in the peer-reviewed journal, Ecotoxicology and Environmental Safety, demonstrating that inhibiting NLRP3 inflammasomes can attenuate kidney damage and dysfunction associated with the environmental pollutant, PM2.5.

In the paper titled, “PM2.5 induces renal tubular injury by activating NLRP3-mediated pyroptosis,” the authors conducted studies in a mouse model exposed to high concentrations of ambient PM2.5 for 12 weeks, and in a mouse kidney cell line. Following are key findings reported in the paper:

PM2.5 exposure leads to kidney structural changes and functional impairment.

Inflammasome NLRP3-induced Inflammation and pyroptosis were increased in PM2.5-exposed kidney tissues.

Inhibiting the inflammasome NLRP3 pathway, including downstream caspase-1, rescued the kidneys from PM2.5-induced cell death.

The authors stated, “We further provided evidence that NLRP3-mediated pyroptosis plays critical roles in the progression of kidney injury induced by PM2.5 exposure. Inhibiting the activation of NLRP3 inflammasome can remarkably protect the renal tubular epithelial cells from PM2.5-induced proptosis.” To read the article, Click Here.

“The research published in the Journal,Ecotoxicology and Environmental Safety, reinforces other published data demonstrating that inhibiting NLRP3 inflammasomes can attenuate kidney damage and dysfunction of multiple causes, now including kidney damage associated with the environmental pollutant, PM2.5,” commented Stephen C. Glover, ZyVersa’s Co-founder, Chairman, CEO and President. “This research provides increasing support for inflammasome inhibition as a promising treatment option for kidney disease, a major health problem affecting over 35 million adults in the United States. ZyVersa is developing Inflammasome ASC inhibitor IC 100. Unlike NLRP3 inhibitors, designed to inhibit formation of one inflammasome to block initiation of the inflammatory cascade, IC 100 was designed to inhibit multiple types of inflammasomes and their associated ASC specks to uniquely block both initiation and perpetuation of damaging inflammation.” To review a white paper summarizing the mechanism of action and preclinical data for IC 100, Click Here.

About Inflammasome ASC Inhibitor IC 100

IC 100 is a novel humanized IgG4 monoclonal antibody that inhibits the inflammasome adaptor protein ASC. IC 100 was designed to attenuate both initiation and perpetuation of the inflammatory response. It does so by binding to a specific region of the ASC component of multiple types of inflammasomes, including NLRP1, NLRP2, NLRP3, NLRC4, AIM2, Pyrin. Intracellularly, IC 100 binds to ASC monomers, inhibiting inflammasome formation, thereby blocking activation of IL-1β early in the inflammatory cascade. IC 100 also binds to ASC in ASC Specks, both intracellularly and extracellularly, further blocking activation of IL-1β and the perpetuation of the inflammatory response that is pathogenic in inflammatory diseases. Because active cytokines amplify adaptive immunity through various mechanisms, IC 100, by attenuating cytokine activation, also attenuates the adaptive immune response.

About ZyVersa Therapeutics, Inc.

ZyVersa (Nasdaq: ZVSA) is a clinical stage specialty biopharmaceutical company leveraging advanced, proprietary technologies to develop first-in-class drugs for patients with renal and inflammatory diseases who have significant unmet medical needs. The Company is currently advancing a therapeutic development pipeline with multiple programs built around its two proprietary technologies – Cholesterol Efflux Mediator™ VAR 200 for treatment of kidney diseases, and Inflammasome ASC Inhibitor IC 100, targeting damaging inflammation associated with numerous CNS and other inflammatory diseases. For more information, please visit www.zyversa.com.

Certain statements contained in this press release regarding matters that are not historical facts, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. These include statements regarding management’s intentions, plans, beliefs, expectations, or forecasts for the future, and, therefore, you are cautioned not to place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. ZyVersa Therapeutics, Inc (“ZyVersa”) uses words such as “anticipates,” “believes,” “plans,” “expects,” “projects,” “future,” “intends,” “may,” “will,” “should,” “could,” “estimates,” “predicts,” “potential,” “continue,” “guidance,” and similar expressions to identify these forward-looking statements that are intended to be covered by the safe-harbor provisions. Such forward-looking statements are based on ZyVersa’s expectations and involve risks and uncertainties; consequently, actual results may differ materially from those expressed or implied in the statements due to a number of factors, including ZyVersa’s plans to develop and commercialize its product candidates, the timing of initiation of ZyVersa’s planned preclinical and clinical trials; the timing of the availability of data from ZyVersa’s preclinical and clinical trials; the timing of any planned investigational new drug application or new drug application; ZyVersa’s plans to research, develop, and commercialize its current and future product candidates; the clinical utility, potential benefits and market acceptance of ZyVersa’s product candidates; ZyVersa’s commercialization, marketing and manufacturing capabilities and strategy; ZyVersa’s ability to protect its intellectual property position; and ZyVersa’s estimates regarding future revenue, expenses, capital requirements and need for additional financing.

New factors emerge from time-to-time, and it is not possible for ZyVersa to predict all such factors, nor can ZyVersa assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Forward-looking statements included in this press release are based on information available to ZyVersa as of the date of this press release. ZyVersa disclaims any obligation to update such forward-looking statements to reflect events or circumstances after the date of this press release, except as required by applicable law.

This press release does not constitute an offer to sell, or the solicitation of an offer to buy, any securities.

Corporate and IR Contact: Karen Cashmere Chief Commercial Officer kcashmere@zyversa.com 786-251-9641

Amazon founder Jeff Bezos announced he is moving from Seattle to Miami in an emotional Instagram post on Thursday. The billionaire said that while the move is exciting, leaving Seattle is bittersweet.

“Seattle, you will always have a place in my heart,” Bezos wrote.

Bezos established Amazon in Seattle back in 1994, starting out in his garage in the suburb of Bellevue. Over the decades, Amazon transformed Seattle into a major tech hub and is the city’s largest private employer. Bezos stepped down as Amazon CEO last year to become executive chairman, with Andy Jassy succeeding him in the top role.

The billionaire recently purchased two luxury homes in Miami for $79 million and $68 million. He said the move brings him closer to his parents, his partner Lauren Sanchez, and operations for his space company Blue Origin which are increasingly shifting to Cape Canaveral.

Miami has been attracting more of the ultra-wealthy and their companies, luring them with a combination of lifestyle, business opportunities, and low taxes. Finance moguls like Ken Griffin, Dan Loeb and Josh Harris have also bought multi-million dollar Miami Beach mansions during the pandemic.

Griffin notably moved the headquarters of his hedge fund Citadel from Chicago to Miami last year. He is also planning to build a new $1 billion headquarters for Citadel in the city. Inter Miami CF, the Florida soccer club owned by David Beckham, recently signed superstar Lionel Messi who purchased his own lavish home in the area.

While being closer to family and friends is likely a factor, the tax benefits of moving to Florida also can’t be ignored. Jeff Bezos currently resides in Washington State which passed a 7% tax on capital gains that could cost wealthy individuals like Bezos millions when they sell stock.

Meanwhile, Florida is one of nine U.S. states without personal income or capital gains taxes. This tax haven status has drawn more billionaires to make Florida their primary residence. By moving from Seattle to Miami, Bezos could avoid Washington’s new capital gains tax and save huge amounts of money when he eventually sells his Amazon shares.

Why Florida is a Hotspot for Investors

In addition to its tax advantages, Florida offers an appealing climate and business-friendly environment that makes it attractive for investors and investment funds. The state has no personal income tax and no estate tax, allowing investors and funds to grow their capital faster.

Miami has also established itself as a hub for venture capital, with VC funding to Florida startups increasing year over year. Several high-profile investors have already established offices in Miami, and the city is actively trying to recruit more VC funds and angels.

With no state capital gains tax and rising startup activity, Florida provides an optimal environment for investors looking to maximize returns. The influx of investment funds and business incentives continue to make the state more appealing for entrepreneurs as well.

Jeff Bezos is the world’s third richest man according to Bloomberg’s Billionaire Index, with a current net worth of around $139 billion. Nearly all of his wealth comes from the 16% stake he still holds in Amazon stock.

By leaving Washington for Florida, Bezos joins other tech billionaires and investors like PayPal co-founder Peter Thiel and hedge fund manager Paul Tudor Jones who have relocated to the Sunshine State. Miami Mayor Francis Suarez has specifically been trying to court more tech entrepreneurs, investors and venture capital to Miami.

While Bezos did not mention taxes as a reason for his move, the massive savings he will enjoy underscores why Florida has become increasingly popular with the mega-rich. Fellow billionaire Elon Musk also moved himself to Texas in 2020 which does not collect personal income tax.

With no state income tax and a low cost of living relative to coastal cities like New York and San Francisco, Florida provides financial incentives for the wealthy to establish residency. For Jeff Bezos, the hundreds of millions he could save in taxes make relocating to Miami well worth leaving Seattle, the place that birthed his legendary company Amazon.

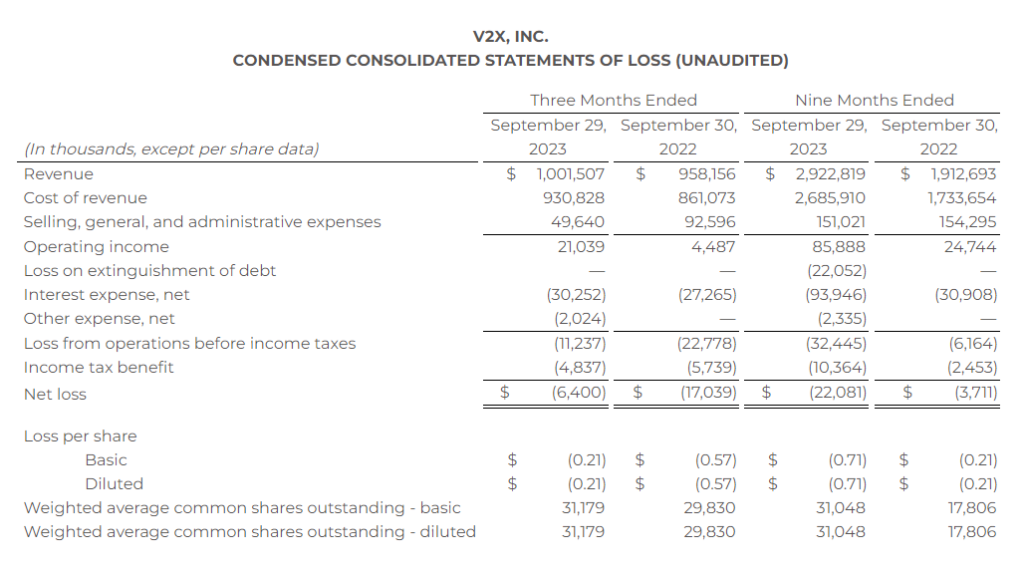

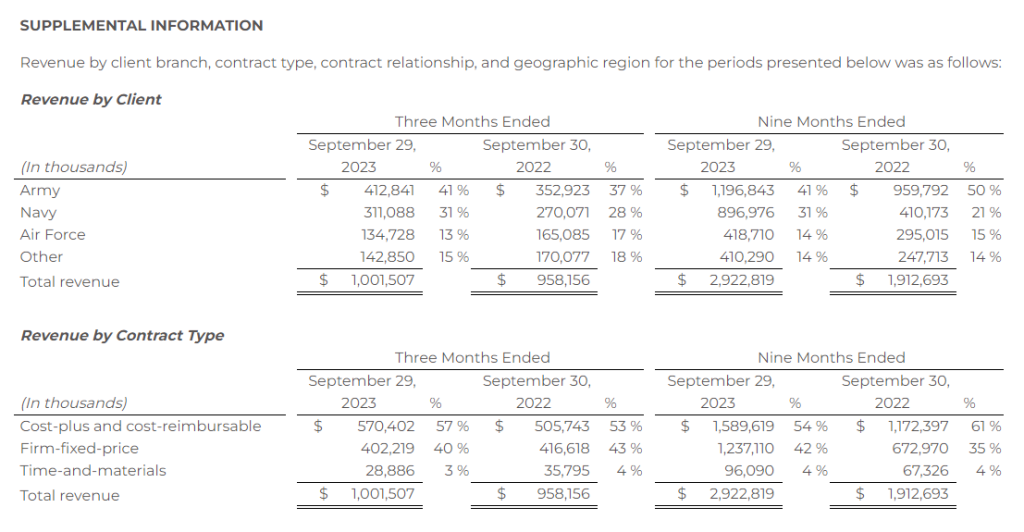

Reported record revenues of $1.0 billion, up 5% y/y

Awarded bookings of $1.3 billion, increasing backlog to a record high of $13.3 billion

Reported operating income of $21.0 million; adjusted operating income1 of $59.5 million

Adjusted EBITDA1 of $64.7 million with a margin1 of 6.5%

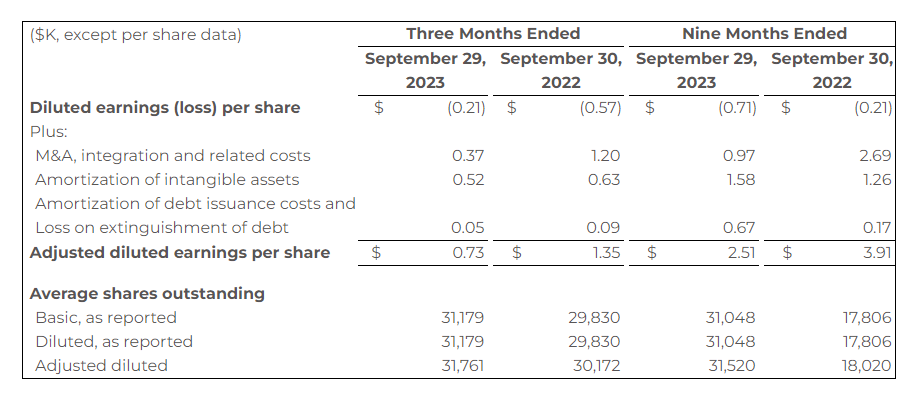

Diluted EPS1 of ($0.21); Adjusted diluted EPS1 of $0.73

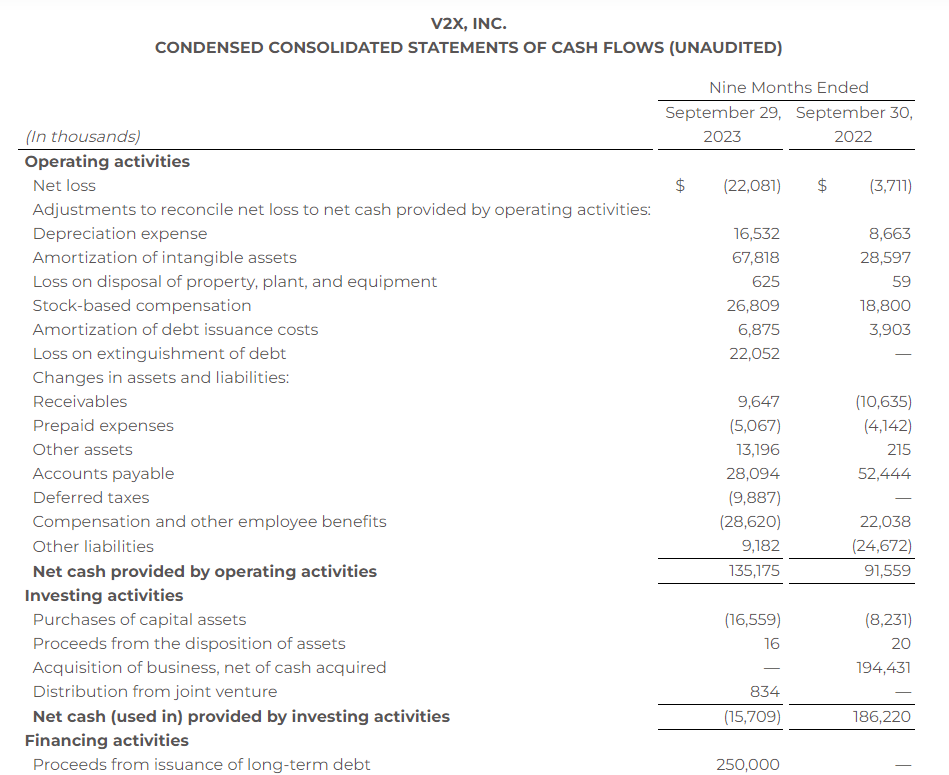

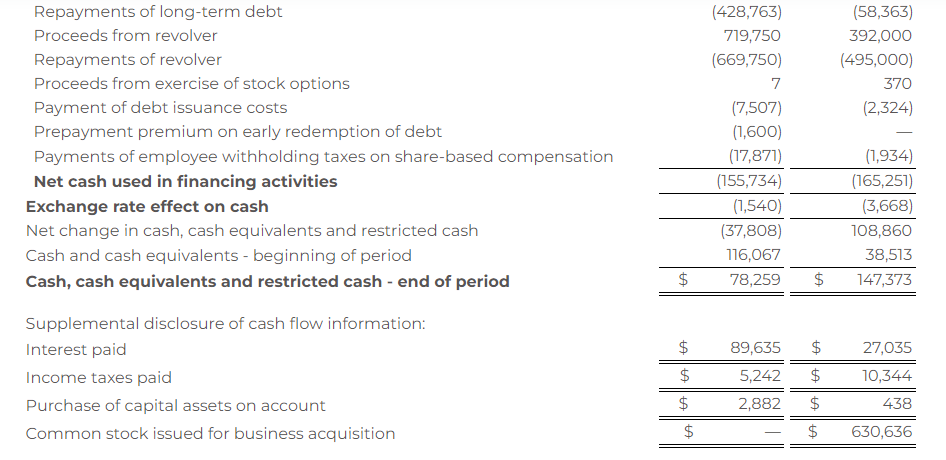

Reported year-to-date cash flow from operations of $135.2 million, and reduced net debt $88.9 million

MCLEAN, Va., Nov. 6, 2023 /PRNewswire/ — V2X, Inc. (NYSE:VVX) announced third quarter 2023 financial results.

“We achieved record revenue in the third quarter of approximately $1 billion, which demonstrates our unwavering commitment to our clients and the missions we support,” said Chuck Prow, President and Chief Executive Officer of V2X. “Bookings activity in the quarter was strong at $1.3 billion in awards. This yielded total backlog of $13.3 billion, an all-time high for the company and provides solid revenue visibility moving into 2024. Importantly, we are executing the “Expand the Base” component of our strategic framework and were successful in achieving extended scope through client engagement initiatives on existing business, which has yielded $332 million of awards in the quarter and $1.2 billion year-to-date. We are also leveraging our converged capabilities to pursue new business and currently have a robust pipeline of opportunities, which includes ~$19 billion of bids we plan to submit over the next twelve months and over $6 billion submitted and in evaluation.”

Mr. Prow continued, “During the quarter, we had notable success capturing several key pursuits that are representative of V2X’s differentiated ability to deliver technology and operational solutions across the mission lifecycle. For example, we secured a $190 million five-year, fixed price contract to continue providing training and range operations services to the U.S. Army in the Middle East. Our team will provide training support services as well as instruction, operation, and maintenance of training aids, devices, simulators, and simulations; fixed ranges; deployable ranges; and numerous training facilities. This successful capture leverages our decades of experience providing high consequence training as well as our global scale and will allow V2X to bring our Army client unparalleled service delivery in support of enhancing the warfighting skills via the use of live and virtual training. We continue to invest in the future and are developing the next generation of training capabilities, techniques, and enablers.”

“We have also made remarkable progress organically growing V2X’s environmental capabilities and were recently awarded an $85 million two-year contract to support the recovery and remediation of drinking water. This win builds on V2X’s original work to support the Department of Defense with the establishment of a water supply system for military housing at Red Hill, Hawaii. Our ability to deliver solutions that generate tangible results and public health benefits have led to incremental work and are now helping to deliver safe drinking water to the local communities. We have also successfully leveraged this capability to win similar work in Japan. We are proud to be supporting such an important environmental mission and believe there is significant opportunity to expand our efforts to other geographic areas both within and outside of the Pacific region.”

“Finally, subsequent to the end of the quarter, we were awarded a $458 million five-year, fixed price program to provide depot site standup as well as organizational, selected intermediate and limited depot level maintenance, and logistics support for the F-5 Adversary aircraft with the Navy and Marine Corps. The F-5 contract, combined with our Naval Test Wing Pacific and Atlantic awards, equates to over $1.7 billion in new work V2X has won with the U.S. Navy over the past ~18 months. I’d like to thank our teams for their commitment to delivering unique and value-added solutions that provide differentiation and enhanced client outcomes.”

Mr. Prow concluded, “We are pleased with our continued revenue growth and record backlog which is supported by the momentum generated through our efforts to converge solutions across our clients’ mission lifecycle. V2X is differentiating its capability offerings through the intersection of technology and operations, which we believe will continue to create value for our shareholders.”

Third Quarter 2023 Results

Revenue of $1.0 billion, up 4.5% y/y

Operating income of $21.0 million, including merger and integration related costs of $15.8 million, and amortization of acquired intangible assets of $22.6 million

Adjusted operating income1 of $59.5 million

Adjusted EBITDA1 of $64.7 million with a 6.5% adjusted EBITDA margin1

Diluted EPS1 of ($0.21); Adjusted Diluted EPS1 of $0.73

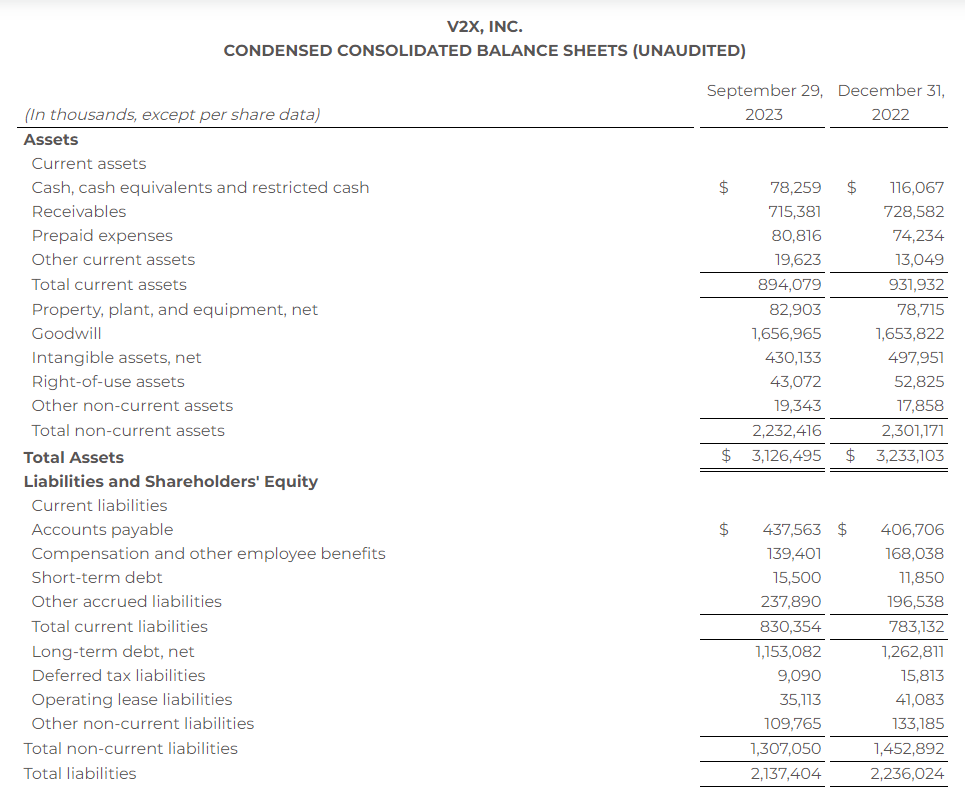

Net debt as of September 29, 2023 of $1.1 billion

Total backlog as of September 29, 2023 of $13.3 billion

“V2X reported revenue of $1.0 billion in the quarter, which represents 4.5% year-over-year growth,” said Shawn Mural, Senior Vice President and Chief Financial Officer. “Revenue growth in the quarter was achieved through continued program execution on existing programs, plus the phase-in of recent awards, including our first task order win with the Department of State, which reached full operational capability approximately two weeks ahead of schedule and has since expanded in size. We were also successful in continuing to defend our core and have won over $1 billion in recompete programs year to date.”

“For the quarter, the Company reported operating income of $21.0 million and adjusted operating income1 of $59.5 million. Adjusted EBITDA1 was $64.7 million with a margin of 6.5%, which was influenced by contract mix and performance on certain integrated electronic security programs. Third quarter diluted EPS was ($0.21), due primarily to merger and integration related costs, amortization of acquired intangible assets, and interest expense. Adjusted diluted EPS1 for the quarter was $0.73.”

“Cash generation was strong and net cash provided by operating activities was $135.2 million year to date. Adjusted net cash provided by operating activities1 year to date was $83.6 million, adding back $20.9 million of M&A and integration costs with $13.4 million of CARES act payments, and removing the contribution of the master accounts receivable purchase or MARPA facility of $85.8 million.”

“At the end of the quarter, net debt for V2X was $1,131.8 million. Our solid cash generation has enabled V2X to reduce its total debt by $88.9 million year to date. Net consolidated indebtedness to EBITDA1 (net leverage ratio) was 3.46x. Additionally, our strong fundamentals and cash flow profile allowed us to reprice our Term Loan B shortly after the quarter close. We expect the new pricing to reduce annual interest expense by $2 million,” said Mr. Mural.

Total backlog as of September 29, 2023, was $13.3 billion. Funded backlog was $3.2 billion. Bookings in the quarter were $1.3 billion, resulting in a book-to-bill of 1.3x. The trailing twelve-month book-to-bill was 1.1x.

2023 Guidance Mr. Mural concluded, “Based on what we are seeing in the business we are raising the low end and mid-point of our full year revenue projections. Given third-quarter results and our outlook, we are lowering the ranges for adjusted EBITDA and adjusted diluted EPS. This change incorporates year-to-date results, including the program performance mentioned earlier and timing of activities associated with national security support. We are reaffirming guidance for adjusted net cash provided by operating activities.” The Company is adjusting its 2023 guidance and is as follows:

$ millions, except for per share amounts

2023 Guidance (Updated)

2023 Mid-Point (Updated)

Revenue

$3,900

$3,950

$3,925

Adjusted EBITDA1

$285

$295

$290

Adjusted Diluted Earnings Per Share1

$3.50

$3.75

$3.62

Adjusted Net Cash Provided by Operating Activities 1

$115

$135

$125

Forward-looking statements are based upon current expectations and are subject to factors that could cause actual results to differ materially from those suggested here, including those factors set forth in the Safe Harbor Statement below.

Third Quarter 2023 Conference Call

Management will conduct a conference call with analysts and investors at 8:00 a.m. ET on Monday, November 6, 2023. U.S.-based participants may dial in to the conference call at 877-407-3982, while international participants may dial 201-493-6780. A live webcast of the conference call as well as an accompanying slide presentation will be available here: https://app.webinar.net/gAed3AVKra2

A replay of the conference call will be posted on the V2X website shortly after completion of the call and will be available for one year. A telephonic replay will also be available through November 20, 2023, at 844-512-2921 (domestic) or 412-317-6671 (international) with passcode 13742132.

Presentation slides that will be used in conjunction with the conference call will also be made available online in advance on the “investors” section of the company’s website at https://gov2x.com/. V2X recognizes its website as a key channel of distribution to reach public investors and as a means of disclosing material non-public information to comply with its obligations under the U.S. Securities and Exchange Commission (“SEC”) Regulation FD.

Footnotes: 1 See “Key Performance Indicators and Non-GAAP Financial Measures” for descriptions and reconciliations.

About V2X V2X builds smart solutions designed to integrate physical and digital infrastructure – from base to battlefield – by aligning people, actions, and outputs. Formed by the merger of Vectrus and Vertex, we bring a combined 120 years of successful mission support. Our lifecycle solutions improve security, streamline logistics, and enhance readiness.

The Company delivers a comprehensive suite of integrated solutions across the operations and logistics, aerospace, training, and technology markets to national security, defense, civilian and international clients. Our global team of approximately 15,000 employees brings innovation to every point in the mission lifecycle, from preparation to operations, to sustainment, as it tackles the most complex challenges with agility, grit, and dedication.

Safe Harbor Statement

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 (the “Act”): Certain material presented herein includes forward-looking statements intended to qualify for the safe harbor from liability established by the Act. These forward-looking statements include, but are not limited to, all the statements and items listed under “2023 Guidance” above and other assumptions contained therein for purposes of such guidance, other statements about our 2023 performance outlook, revenue, contract opportunities, and any discussion of future operating or financial performance.

Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “could,” “potential,” “continue” or similar terminology. These statements are based on the beliefs and assumptions of the management of the Company based on information currently available to management.

These forward-looking statements are not guarantees of future performance, conditions, or results, and involve a number of known and unknown risks, uncertainties, assumptions, and other important factors, many of which are outside our management’s control, which could cause actual results to differ materially from the results discussed in the forward-looking statements. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from the Company’s historical experience and our present expectations or projections. For a discussion of some of the risks and uncertainties that could cause actual results to differ from such forward-looking statements, see the risks and other factors detailed from time to time our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, and other filings with the SEC.

We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Key Performance Indicators and Non-GAAP Measures

The primary financial performance measures we use to manage our business and monitor results of operations are revenue trends and operating income trends. Management believes that these financial performance measures are the primary drivers for our earnings and net cash from operating activities. Management evaluates its contracts and business performance by focusing on revenue, operating income, and operating margin. Operating income represents revenue less both cost of revenue and selling, general and administrative (SG&A) expenses. Cost of revenue consists of labor, subcontracting costs, materials, and an allocation of indirect costs, which includes service center transaction costs. SG&A expenses consist of indirect labor costs (including wages and salaries for executives and administrative personnel), bid and proposal expenses and other general and administrative expenses not allocated to cost of revenue. We define operating margin as operating income divided by revenue.

We manage the nature and amount of costs at the program level, which forms the basis for estimating our total costs and profitability. This is consistent with our approach for managing our business, which begins with management’s assessing the bidding opportunity for each contract and then managing contract profitability throughout the performance period.

In addition to the key performance measures discussed above, we consider adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted operating cash flow, and pro forma revenue to be useful to management and investors in evaluating our operating performance, and to provide a tool for evaluating our ongoing operations. This information can assist investors in assessing our financial performance and measures our ability to generate capital for deployment among competing strategic alternatives and initiatives. We provide this information to our investors in our earnings releases, presentations, and other disclosures.

Adjusted net income, adjusted diluted earnings per share, adjusted operating income, adjusted EBITDA, adjusted EBITDA margin, adjusted net cash provided by (used in) operating activities, and pro forma revenue, however, are not measures of financial performance under GAAP and should not be considered a substitute for financial measures determined in accordance with GAAP. Definitions and reconciliations of these items are provided below.

Pro forma revenue is defined as the combined results of our operations as if the Merger had occurred on January 1, 2021.

Adjusted operating income is defined as operating income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA is defined as operating income, adjusted to exclude depreciation and amortization of intangible assets, and items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration, and related costs.

Adjusted EBITDA margin is defined as adjusted EBITDA divided by revenue.

Adjusted net income is defined as net income, adjusted to exclude items that may include, but are not limited to, significant charges or credits, and unusual and infrequent non-operating items that impact current results but are not related to our ongoing operations, such as M&A, integration and related costs, amortization of acquired intangible assets, amortization of debt issuance costs, and loss on extinguishment of debt.

Adjusted diluted earnings per share is defined as adjusted net income divided by the weighted average diluted common shares outstanding.

Cash interest, net is defined as interest expense, net adjusted to exclude amortization of debt issuance costs.

Adjusted net cash provided by (used in) operating activities is defined as net cash provided by (or used in) operating activities adjusted to exclude infrequent non-operating items, such as M&A payments and related costs.

Net leverage ratio is defined as net debt (or total debt less unrestricted cash) divided by trailing twelve-month (TTM) bank EBITDA.

In this document, the Company presents certain forward-looking non-GAAP metrics. The Company does not provide outlook on a GAAP basis because the items that the Company excludes from GAAP to calculate the comparable non-GAAP measure can be dependent on future events that are less capable of being controlled or reliably predicted by management and are not part of the Company’s routine operating activities. Additionally, management does not forecast many of the excluded items for internal use and therefore cannot create or rely on outlook done on a GAAP basis. The occurrence, timing, and amount of any of the items excluded from GAAP to calculate non-GAAP could significantly impact the Company’s fiscal 2023 GAAP results.

CONTACT:

V2X, Inc. Mike Smith, CFA 719-637-5773 ir@gov2x.com

CHELMSFORD, MA / ACCESSWIRE / November 6, 2023 / Harte Hanks, Inc. (NASDAQ:HHS), a leading global customer experience company focused on bringing companies closer to customers for 100 years, today announced that Ron Lee, an experienced executive with a proven track record of driving revenue growth and operational improvement by developing talent, leveraging analytics and innovating through technology modernization, has joined Harte Hanks as Senior Vice President of Sales Services. Mr. Lee will lead Harte Hanks’ sales offering, which includes inside sales outsourcing, sales transformation and optimization, and sales play development.

Lee joins Harte Hanks from Procore Technologies, a leading SaaS provider specializing in the construction industry, where he served as the Head of Revenue Planning and Productivity. Previously, he spent 10 years at ADP developing and executing the global inside sales strategy, transforming the sales & marketing tech stack and implementing predictive analytics within GTM processes. Mr. Lee started his career at PwC and has also served in sales operations and finance leadership roles at Lucent Technologies, D&B and Merck. He holds a Bachelor’s degree in Accounting from Villanova University and a MBA in Marketing, Finance and International Business from New York University.

Kirk Davis, Chief Executive Officer, commented: “We continue to recruit top sales talent to revitalize our growth engine. Ron, along with Kelly Waller, our new Corporate SVP for Sales and Marketing, are both accomplished leaders with a deep understanding of how to create solutions for enterprise clients. Ron takes the helm of Harte Hanks’ Sales Services division, which originated through our acquisition of InsideOut last December. Ron is a critical hire at a pivotal time. Inside sales is a valuable offering for our clients, and an area in which we expect to achieve a strong rebound, accelerating growth and higher profitability in 2024.”

“Inside sales is essential for the growth and transformation of sales through digital technology, cost savings, and the ability to meet the changing preferences of buyers,” commented Mr. Lee. “Harte Hanks has built powerful tools to streamline this process for clients, and this offering provides a quantifiable return on investment. I look forward to bringing this value proposition to new logos and expanding our relationships with existing customers.”

About Harte Hanks:

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract and engage their customers.

Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands, including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony and IBM among others. Headquartered in Chelmsford, Massachusetts, Harte Hanks has over 2,500 employees in offices across the Americas, Europe, and Asia Pacific.

As used herein, “Harte Hanks” or “the Company” refers to Harte Hanks, Inc. and/or its applicable operating subsidiaries, as the context may require. Harte Hanks’ logo and name are trademarks of Harte Hanks.

Our press release and related earnings conference call contain “forward-looking statements” within the meaning of U.S. federal securities laws. All such statements are qualified by this cautionary note, provided pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Statements other than historical facts are forward-looking and may be identified by words such as “may,” “will,” “expects,” “believes,” “anticipates,” “plans,” “estimates,” “seeks,” “could,” “intends,” or words of similar meaning. These forward-looking statements are based on current information, expectations and estimates and involve risks, uncertainties, assumptions and other factors that are difficult to predict and that could cause actual results to vary materially from what is expressed in or indicated by the forward-looking statements. In that event, our business, financial condition, results of operations or liquidity could be materially adversely affected and investors in our securities could lose part or all of their investments. These risks, uncertainties, assumptions and other factors include: (a) local, national and international economic and business conditions, including (i) the outbreak of diseases, such as the COVID-19 coronavirus, which has curtailed travel to and from certain countries and geographic regions, created supply chain disruption and shortages, disrupted business operations and reduced consumer spending, (ii) market conditions that may adversely impact marketing expenditures, (iii) the impact of the Russia/Ukraine conflict on the global economy and our business, including impacts from related sanctions and export controls and (iv) the impact of economic environments and competitive pressures on the financial condition, marketing expenditures and activities of our clients and prospects; (b) the demand for our products and services by clients and prospective clients, including (i) the willingness of existing clients to maintain or increase their spending on products and services that are or remain profitable for us, and (ii) our ability to predict changes in client needs and preferences; (c) economic and other business factors that impact the industry verticals we serve, including competition and consolidation of current and prospective clients, vendors and partners in these verticals; (d) our ability to manage and timely adjust our facilities, capacity, workforce and cost structure to effectively serve our clients; (e) our ability to improve our processes and to provide new products and services in a timely and cost-effective manner though development, license, partnership or acquisition; (f) our ability to protect our facilities against security breaches and other interruptions and to protect sensitive personal information of our clients and their customers; (g) our ability to respond to increasing concern, regulation and legal action over consumer privacy issues, including changing requirements for collection, processing and use of information; (h) the impact of privacy and other regulations, including restrictions on unsolicited marketing communications and other consumer protection laws; (i) fluctuations in fuel prices, paper prices, postal rates and postal delivery schedules; (j) the number of shares, if any, that we may repurchase in connection with our repurchase program; (k) unanticipated developments regarding litigation or other contingent liabilities; (l) our ability to complete anticipated divestitures and reorganizations, including cost-saving initiatives; (m) our ability to realize the expected tax refunds; and (n) other factors discussed from time to time in our filings with the Securities and Exchange Commission, including under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022 which was filed on March 31, 2023. The forward-looking statements in this press release and our related earnings conference call are made only as of the date hereof, and we undertake no obligation to update publicly any forward-looking statement, even if new information becomes available or other events occur in the future.

Investor Relations Contact:

Rob Fink or Tom Baumann 646.809.4048 / 646.349.6641 FNK IR HHS@fnkir.com