Cumulus Media (NASDAQ: CMLS) is an audio-first media company delivering premium content to over a quarter billion people every month — wherever and whenever they want it. Cumulus Media engages listeners with high-quality local programming through 406 owned-and-operated radio stations across 86 markets; delivers nationally-syndicated sports, news, talk, and entertainment programming from iconic brands including the NFL, the NCAA, the Masters, CNN, the AP, the Academy of Country Music Awards, and many other world-class partners across more than 9,500 affiliated stations through Westwood One, the largest audio network in America; and inspires listeners through the Cumulus Podcast Network, its rapidly growing network of original podcasts that are smart, entertaining and thought-provoking. Cumulus Media provides advertisers with personal connections, local impact and national reach through broadcast and on-demand digital, mobile, social, and voice-activated platforms, as well as integrated digital marketing services, powerful influencers, full-service audio solutions, industry-leading research and insights, and live event experiences. Cumulus Media is the only audio media company to provide marketers with local and national advertising performance guarantees. For more information visit www.cumulusmedia.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Tough comps ahead. The conventional investment scenario is to expect a weak first half of 2023 and a stronger second half. However, we believe the absence of high margin political advertising and the dissolution of the WynnBet partnership calls for a more conservative outlook for 2023. In our view, there are troubling near term signs for the company that have led us to take a more sober outlook for 2023.

Economic headwinds and National advertising. Weakness in National advertising continues to be prevalent as macroeconomic headwinds persist. Additionally, we believe Local advertising is starting to show weakness.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Axcella is a clinical-stage biotechnology company pioneering a new approach to treat complex diseases using compositions of endogenous metabolic modulators (EMMs). The company’s product candidates are comprised of EMMs and derivatives that are engineered in distinct combinations and ratios to restore cellular homeostasis in multiple key biological pathways and improve cellular energetic efficiency. Axcella’s pipeline includes lead therapeutic candidates in Phase 2 development for the treatment of Long COVID and non-alcoholic steatohepatitis (NASH), and the reduction in risk of overt hepatic encephalopathy (OHE) recurrence. The company’s unique model allows for the evaluation of its EMM compositions through non-IND clinical studies or IND clinical trials. For more information, please visit www.axcellatx.com.

Robert LeBoyer, Vice President, Research Analyst, Life Sciences , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Regulators Agree With Axcella’s Plan For A Phase 2b/3 Clinical Trial. Axcella Heath announced that US and UK regulators have agreed to a plan for a global Phase 2b/3 study of AXA1125 in Long COVID-19 patients. An IND has been submitted to the FDA for trials in the US, and agreement from the UK regulators has been received. The Phase 2b/3 trial will include other countries to support worldwide approvals. We see this as an important milestone for AXA1125 and the future of the company.

The Trial Announcement Reduces Uncertainty Around AXA1125. As discussed in our Research Note on August 3, results from the Phase 2a trial in Long COVID showed a significant improvement in the physical fatigue, mental fatigue, and the 6-minute walk test. In December 2022, the company restructured to preserve cash, raising uncertainty about further development for the drug. The announcement of the Phase 2b/3 IND submission provides a development plan, allowing investors to assess timeframes and progress toward the market.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

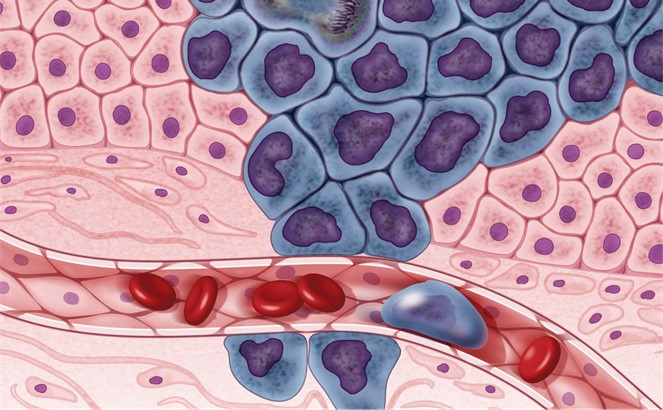

How Cancer Cells Move and Metastasize is Influenced by the Fluids Surrounding Them – Understanding How Tumors Migrate Can Help Stop Their Spread

Cell migration, or how cells move in the body, is essential to both normal body function and disease progression. Cell movement is what allows body parts to grow in the right place during early development, wounds to heal and tumors to become metastatic.

Over the last century, how researchers understood cell migration was limited to the effects of biochemical signals, or chemotaxis, that direct a cell to move from one place to another. For example, a type of immune cell called a neutrophil migrates toward areas in the body that have a higher concentration of a protein called IL-8, which increases during infection.

In the past two or three decades, however, scientists have started to recognize the importance of the mechanical, or physical, factors that play a role in cell migration. For example, human mammary epithelial cells – the cells lining the milk ducts in the breast – migrate toward areas of increasing stiffness when placed on a surface with a stiffness gradient.

This article was republished with permission from The Conversation, a news site dedicated to sharing ideas from academic experts. It represents the research-based findings and thoughts of, Yizeng Li, Assistant Professor of Biomedical Engineering, Binghamton University, State University of New York.

And now, instead of focusing on just the effect of the “solid” environment of cells, researchers are turning toward their “fluid” environment. As a theoretician trained in applied mathematics, I use mathematical models to understand the physics behind cell biology. My colleagues Sean X. Sun and Konstantinos Konstantopoulos and I were among the pioneering scientists who discovered how water and hydraulic pressure influence cell migration through theoretical models and lab experiments. In our recently published research, we found that human breast cancer cell migration is enhanced by the flow and viscosity of the fluids surrounding them, clarifying one of the factors influencing how tumors metastasize.

How Fluids Affect Cell Migration

Cells in the human body are constantly exposed to fluids of different physical properties. Water is one such fluid that can direct cell migration. For example, we found that how water flows across the membranes of breast cancer cells influences how they move and metastasize. This is because the amount of water traveling in and out of a cell causes it to shrink or swell, inducing movement by translocating different parts of the cell.

The viscosity, or thickness, of body fluids varies from organ to organ, and from health to disease, and this can also affect cell migration. For example, the fluid between cancer cells in tumors is more viscous than the fluid between normal cells in healthy tissues. When we compared how quickly breast cancer cells move in confined channels filled with fluid of normal viscosity versus fluid of high viscosity, we found that cells in high viscosity channels counterintuitively sped up by a significant 40%. This discovery was unexpected because the fundamental laws of physics tell us that inert particles should slow down in high viscosity fluids due to increased resistance.

We wanted to figure out the mechanism behind this surprising result. So we identified what molecules were involved in this process, discovering a cascade of events that allow high viscosity environments to enhance cell motility.

We found that high viscosity fluids first promote the growth of protein filaments called actin, which open channels in the cell’s membrane and increase water intake. The cell expands from the water, activating another channel that takes in calcium ions. These calcium ions activate another type of protein filament called myosin that induces the cell to move. This cascade of events induces cells to change their structure and generate more force to overcome the resistance imposed by high viscosity fluid, meaning the cells aren’t inert at all.

We also discovered that cells retained “memory” after exposure to a high viscosity medium. This meant that if we put cells in a high viscosity medium for several days and then returned them to a normal viscosity medium, they would still move at a faster speed. How cells retain this memory is still an open question.

We then wondered whether our findings on viscous memory would remain true in animals, not just in Petri dishes. So we exposed human breast cancer cells to a high viscosity medium for six days, then placed them in a normal viscosity medium. We then injected the cells into chicken embryos and mice.

Our results were consistent: Cells pre-exposed to a high viscosity medium had an increased ability to leak into surrounding tissues and metastasize compared to cells that were not pre-exposed. This result demonstrates that the viscosity of the fluids in a cell’s surrounding environment is a mechanobiological cue that promotes cancer cells to metastasize.

Implications for Cancer Treatment

Cancer patients usually don’t die from the original source of the tumor, but from its spread to other parts of the body.

When cancer cells travel through the body, they move into spaces that will have varying fluid viscosity. Understanding how fluid viscosity affects the movement of tumor cells could help researchers figure out ways to better treat and detect cancer before it metastasizes.

The next step is to build imaging and analysis techniques to precisely examine how cells from various types of lab animals respond to changes in fluid viscosity. Identifying the molecules that regulate how cells respond to changes in viscosity could help researchers identify potential drug targets to reduce the spread of cancer.

When it comes to hand-selecting companies for investment, a critical ingredient for success is information. This ingredient becomes even more critical with biotech companies. Each year, many companies have been involved in medicine, medical equipment, genetics, and wellness that take off and provide investors with double or triple-digit gains. During the same years, there are stocks in the sector that, on the surface seem to have just as much going for them, yet a diligent peak below the surface demonstrates their success is less probable.

The ability to get below the surface is one reason the JPMorgan Health Symposium draws between 8,000 and 10,000 attendees each year. Attending is an expensive commitment, but firsthand information, insights from others that are in-the-know, and exposure to scientific paths, trends and research that barely existed a few years earlier, can pay off.

If you were not among the 8,000 counted as attending at the 2023 JP Morgan Health Symposium, you’ll want to know, Noble Capital Markets, teamed with Channelchek to provide a video recap with insights and key takeaways on some of the biotech trends that may be worth exploring. This takeaway, coupled with select company presentations and questions from two top equity analysts in the field is sure to build on your current health sector knowledge. Go Here For More Information (and free access).

Trends Worth Exploring

Molecular diagnostics, involves taking DNA or RNA which is our unique and easily obtainable genetic code, and analyzing the sequences for red flags. These markers can pinpoint the chance for emergence of specific diseases. This field has expanded rapidly in recent years, with some products now being used regularly. But the potential is for far more to be developed and approved for use. This provides for tremendous profit potential.

Alternative pain relief, non-opioid and non-NAISD pain medications for chronic sufferers, could benefit millions who suffer eah day. The potential runs the gamut from chronic headaches or back pain to situations where one is recovering from surgery, sports injuries, or accidents. Millions of prescriptions are written each year for pain medications. This has, in part fed into the opioid crisis in the U.S. It has prompted an almost emergency-level need for replacing older addictive medications with effective alternatives. There are a number of companies making gains in this area of great need.

Gene therapy is a technique to treat or cure disease by modifying one’s genes. In many cases, the hope is that it leads to a permanent cure. New gene therapies are being developed for a wide swath of ailments including life-threatening disease. It is expected to be in many cases the next generation of cure. The methods for gene therapy include replacing a disease-causing gene with a healthy copy, or inactivating the disease-causing gene. In other cases a modified gene may be introduced to help treat the disease. The research and development include cancers, infectious disease, organ failures, and autoimmune problems. Many of these companies will be opening the door to welcome life improvements for the some people, and curing what are now incurable diseases for others.

Drilling Down at the Company Level

It may feel uncomfortable to suggest that investing in and backing the right companies that resolve health issues can be profitable to you. But, the truth is, without investments and interest in stock ownership, tomorrow’s miracle drugs would never come to exist.

Watch the Takeaway from the JP Morgan conference with an eye toward what the company presenters deem important, and then listen to the analysts that also drill deeper beyond concept and stage of development, they discuss finances, which for many less experienced biotech investors, isn’t focused on enough. The companies selected for the Noble Capital Markets Takeaway all fall within one the fields mentioned above. Register Here.

Possible Side-Effects

The J.P. Morgan Healthcare Symposium was held in mid-January. It is one of life science’s largest and most frenzied sharing of information related to the industry. Not everyone gets to go. We’re enthusiastic to be bringing you a slice of the excitement in hopes that you deepen your understanding of not just these companies, but what to look for in others as well.

MALVERN, Pa., Jan. 24, 2023 (GLOBE NEWSWIRE) — Baudax Bio, Inc. (NASDAQ:BXRX) a pharmaceutical company focused on innovative products for hospital and related settings, today announced the successful outcome of its first interim analysis in a Phase II trial of BX1000 for neuromuscular blockade (NMB) in patients undergoing elective surgery.

“We are encouraged by the results of the first interim analysis of the BX1000 Phase II surgery trial,” said Gerri Henwood, Baudax Bio’s President and Chief Executive Officer. “We believe the use of BX1000, combined with our reversal agent, BX3000, could make for precise control of timing under neuromuscular paralysis for surgical patients, which could result in time and cost savings for patients and hospitals alike. We look forward to completing enrollment in the study in Q1 and sharing topline results for the study in April 2023.”

This randomized, double-blind, active-controlled clinical trial comparing three different doses of BX1000 to a standard dose of rocuronium is planned to enroll a total of 80 adult patients undergoing elective surgery utilizing total intravenous anesthesia. The primary efficacy endpoint is the proportion of patients meeting criteria for Good or Excellent intubating conditions using a standardized scale. Additionally, the trial is evaluating the safety and tolerability profile of BX1000 and rocuronium in this patient population.

This pre-planned interim analysis evaluated the intubating conditions for each patient after administration of study drug in a blinded fashion. In the 20-patient cohort, 5 patients per group received one of the study medications. All 20 patients were observed to have met the criteria for Good or Excellent intubating conditions at 60 seconds. Nineteen of the subjects were successfully intubated following the assessment at 60 seconds, and the one remaining subject following the assessment at 90 seconds. Study treatments were generally well tolerated with no occurrence of severe or serious adverse events.

This blinded interim analysis did not result in the decision to drop any of the four study groups nor any decision to adjust planned study enrollment numbers.

About Baudax Bio’s Neuromuscular Blocking Agents (NMBs)

Baudax Bio holds exclusive global rights to two novel NMBs, BX1000, an intermediate duration, clinical stage blocking agent, and BX2000, an ultra-short duration, clinical stage blocking agent, as well as a proprietary chemical reversal agent, BX3000, undergoing nonclinical studies intended to support an IND filing in 2023. BX3000 is a specific reversal agent that rapidly reverses BX1000 and BX2000. All three agents are licensed from Cornell University. We believe these agents allow for a very rapid induction of neuromuscular blockade for surgical settings, followed by a rapid reversal of the neuromuscular blockade. These novel agents have the potential to meaningfully reduce time to onset of blocking and of reversal of blockade, reducing time in operating rooms or post-acute care settings, resulting in potential clinical and cost advantages, as well as time-related valuable cost savings for hospitals and ambulatory surgical centers.

About Baudax Bio

Baudax Bio is a pharmaceutical company focused on innovative products for hospital and related settings. The Company has a pipeline of innovative pharmaceutical assets including two clinical-stage, novel neuromuscular blocking (NMBs) agents, one in a Phase II study and an additional unique NMB in a dose escalation Phase I study, as well as a proprietary chemical reversal agent specific to these NMBs. Baudax Bio has received approval for and marketed ANJESO®, the first and only 24-hour, intravenous (IV) COX-2 preferential non-opioid, non-steroidal anti-inflammatory (NSAID) for the management of moderate to severe pain. For more information, please visit www.baudaxbio.com.

Forward-Looking Statements

This press release contains forward-looking statements that involve risks and uncertainties. Such forward-looking statements reflect Baudax Bio’s expectations about its future performance and opportunities that involve substantial risks and uncertainties. When used herein, the words “anticipate,” “believe,” “estimate,” “may,” “upcoming,” “plan,” “target,” “goal,” “intend” and “expect” and similar expressions, as they relate to Baudax Bio or its management, are intended to identify such forward-looking statements. These forward-looking statements, which include statements relating to the development of each of BX1000 and BX3000, are based on information available to Baudax Bio as of the date of this press release and are subject to a number of risks, uncertainties, and other factors that could cause actual results to differ materially from those expressed in, or implied by, these forward-looking statements. These risks and uncertainties include, among other things, risks related to market, economic and other conditions, the ongoing economic and social consequences of the COVID-19 pandemic, Baudax Bio’s ability to advance its current product candidate pipeline through pre-clinical studies and clinical trials, Baudax Bio’s ability to raise future financing for continued development of its product candidates such as BX1000, BX2000 and BX3000, Baudax Bio’s ability to pay its debt and satisfy conditions necessary to access future tranches of debt, Baudax Bio’s ability to comply with the financial and other covenants under its credit facility, Baudax Bio’s ability to manage costs and execute on its operational and budget plans, Baudax Bio’s ability to achieve its financial goals; Baudax Bio’s ability to comply with all listing requirements of the Nasdaq Capital Market; and Baudax Bio’s ability to obtain, maintain and successfully enforce adequate patent and other intellectual property protection. These forward-looking statements should be considered together with the risks and uncertainties that may affect Baudax Bio’s business and future results included in Baudax Bio’s filings with the Securities and Exchange Commission at www.sec.gov. These forward-looking statements are based on information currently available to Baudax Bio, and Baudax Bio assumes no obligation to update any forward-looking statements except as required by applicable law.

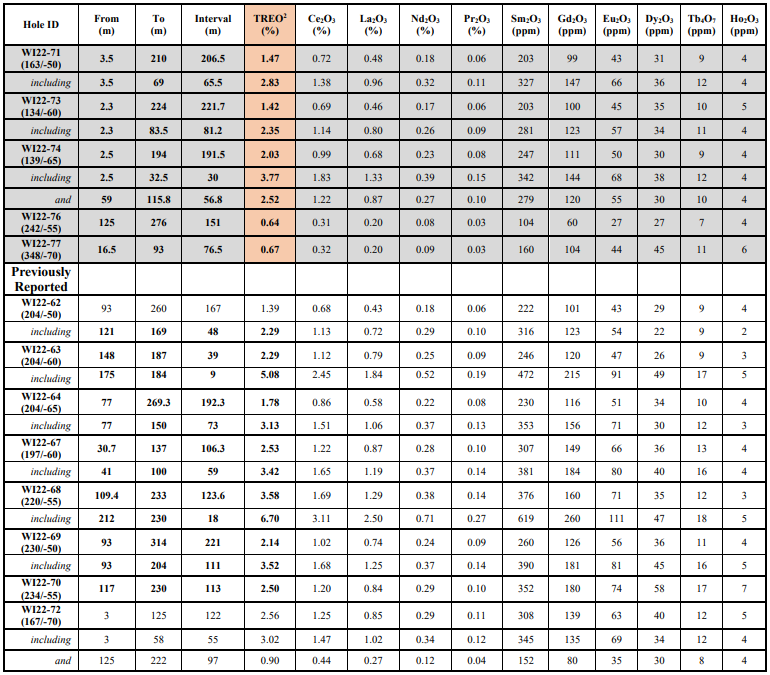

VANCOUVER, BC, Jan. 24, 2023 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company”; (TSXV: DEFN) (OTCQB: DFMTF) (FSE: 35D) is pleased to announce Rare Earth Element (“REE”) assay results from the final two core drill holes, totalling 295 metres (“m”), completed during 2022 at its 100% owned Wicheeda REE Deposit. These assay results are from two exploration geotechnical core drill holes. The final drill hole (WI22-79) returned the best drill intercept on a grade-times-width basis of the entire 18-hole 5,510 m (~18,077 feet) 2022 campaign.

Pit slope geotechnical drill hole WI22-78 (-60o dip at azimuth 200o) drilled into the west pit wall intersected well mineralized dolomite carbonatite that assayed 2.63% total rare earth oxide (“TREO”) over 97 metres (“m”) from surface within a broader mineralized one returning 2.03% TREO over 168 m (see Table 1 and Figure 1).

The final drill hole, WI22-79 (-65o dip at 095o azimuth), drilled within the central area of the Wicheeda Deposit and into the east pit wall intersected an upper high-grade mineralized dolomite-carbonatite interval from surface assaying3.66% TREO over 138m; and lower interval grading 0.50% TREO over 43 m (see Table 1Figure 1, and Image 1).

The upper interval in WI22-79 represents the best mineralized intercept returned of all 2022 holes and ranks among the top 10 reported drill intercepts of the more than 10,000 m drilled in 47 holes Defense Metals has completed post-PEA (see “About the Wicheeda REE Project“).

Luisa Moreno, President, and Director of Defense Metals stated:

“The economic significance of the Wicheeda REE Project is underscored by the fact that the final drill hole yielded the best drill intercept of the 2022 campaign. Since the release of our positive PEA based on drilling completed up to the end of 2019, the last two years of exploration at Wicheeda has focused on resource expansion, delineation, and detailed pit slope geotechnical drilling designed to place us solidly on the path towards initiation of a Preliminary Feasibility Study (PFS). With critical minerals and particularly rare earth elements coming into sharper focus as part the rapidly accelerating transition to electric vehicles, Defense Metals looks forward to continuing to advance the social-environmental, metallurgical, engineering, and geotechnical aspects of the Wicheeda REE Project during 2023.”

Table 1. Final Wicheeda REE Deposit 2022 Diamond Drill Intercepts1

1 The true width of REE mineralization is estimated to be 70-100% of the drilled interval.

2 TREO % sum of CeO2, La2O3, Nd2O3, Pr6O11, Sm2O3, Eu2O3, Gd2O3, Tb4O7, Dy2O3 and Ho2O3.

About the Wicheeda REE Project

The 100% owned, 4,262-hectare (~10,532-acre) Wicheeda REE Project is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda project is readily accessible by all-weather gravel roads and is near infrastructure, including power transmission lines, gas pipelines, the Canadian National Railway, and major highways.

The 2021 Wicheeda REE Project Preliminary Economic Assessment technical report (“PEA”) outlined a robust after-tax net present value (NPV@8%) of $517 million and an 18% IRR3. This PEA contemplated an open pit mining operation with a 1.75:1 (waste:mill feed) strip ratio providing a 1.8 Mtpa (“million tonnes per year”) mill throughout producing an average of 25,423 tonnes REO annually over a 16 year mine life. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

Methodology and Quality Assurance/Quality Control

The analytical work reported on herein was performed by ALS Canada Ltd. (“ALS”) at their Langley (sample preparation) and Vancouver (ICP-MS fusion), B.C. facilities. ALS is an ISO-IEC 17025:2017 and ISO 9001:2015 accredited geoanalytical laboratory and is independent of the Defense Metals and the QP. Drill core samples were subject to crushing at a minimum of 70% passing 2 mm, followed by pulverizing of a 250-gram split to 85% passing 75 microns. A 0.1-gram sample pulp was then subject to multi-element ICP-MS analysis via lithium-borate fusion to determine individual REE content (ME-MS81h). Defense Metals follows industry standard procedures for the work carried out on the Wicheeda Project, with a quality assurance/quality control (“QA/QC”) program. Blank, duplicate, and standard samples were inserted into the sample sequence sent to the laboratory for analysis. Defense Metals detected no significant QA/QC issues during review of the data.

Qualified Person

The scientific and technical information contained in this news release as it relates to the Wicheeda REE Project has been reviewed and approved by Kristopher J. Raffle, P.Geo. (B.C.), Principal and Consultant of APEX Geoscience Ltd. of Edmonton, Alberta, who is a director of Defense Metals and a “Qualified Person” (“QP”) as defined in NI 43-101. Mr. Raffle has verified the data, which included a review of the sampling, analytical and test methods underlying the data, information and opinions disclosed herein.

__________________________

3 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

About Defense Metals Corp.

Defense Metals Corp. is a company focused on the development of its 100% owned Wicheeda Rare Earth Element mineral deposit, located near Prince George, British Columbia, Canada, that contains metals and elements commonly used in in green energy, aerospace, automotive and defense technologies. Rare earth elements are especially important in the production of magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the Company’s plans for its Wicheeda REE Project, expanded resource and scale of expanded resource, expected results and outcomes, plans to complete a PFS, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

January 24, 2023 – Vancouver, Canada – Cypress Development Corp. (TSXV:CYP) (OTCQX: CYDVF) (Frankfurt: C1Z1) ( “Cypress” or “the Company”) announces that the Board of Directors has approved a name change of the Company from Cypress Development Corp. to Century Lithium Corp.

The Company will also change the ticker symbol upon which it trades on the TSX Venture Exchange (“TSXV”). The Company will issue a further news release announcing the date that trading under the new name, symbol and CUSIP number will commence. The name change remains subject to TSXV approval.

About Cypress Development Corp Cypress Development Corp. is a Canadian based advanced stage lithium company, focused on developing its 100%-owned Clayton Valley Lithium Project in Nevada, USA. Cypress is in the pilot stage of testing on material from its lithium-bearing claystone deposit and progressing towards completing a Feasibility Study and permitting, with the goal of becoming a domestic producer of lithium for the growing electric vehicle and battery storage market.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THE CONTENT OF THIS NEWS RELEASE.

Data Represent Research and Development Work Being Conducted at Tonix’s Infectious Disease R&D Center (RDC) in Frederick, Md.

CHATHAM, N.J., Jan. 24, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a clinical-stage biopharmaceutical company, today announced the publication of a paper entitled, “Development of a rapid image-based high-content imaging screening assay to evaluate therapeutic antibodies against the monkeypox virus,” in the journal Antiviral Research. The publication describes the development and optimization of two high-content image-based assays that were employed to screen for potential therapeutic antibodies against the monkeypox virus using surrogate poxviruses such as vaccinia virus. The article highlights Tonix’s TNX-3400 platform, which includes antibodies to potentially prevent or treat monkeypox and smallpox. The article can be accessed online at https://pubmed.ncbi.nlm.nih.gov/36592670/.

“These data represent the first wave of research and development conducted at our Infectious Disease R&D Center (RDC) in Frederick, Md,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “The RDC greatly enhances our ability to advance development of our pipeline of vaccines and therapeutics for infectious diseases. The TNX-3400 platform has promise for preventative and therapeutic monoclonal antibodies to treat monkeypox and smallpox.”

“The article describes how we optimized and standardized two high-content high-throughput image-based assays. The first assay was a neutralizing assay which detected viral proteins of vaccinia virus and used the assay to screen a large library of antibodies made against pox viruses. The second assay specifically detected phenotype changes in cells, called syncytia, after infection and protection by therapeutics.” said Sina Bavari, Ph.D., Executive Vice President of Tonix Pharmaceuticals and site director of the RDC. A critical component in assessing antibodies during pandemics requires the development of rapid but detailed methods to detect and quantitate the neutralization activity. “The neutralizing assay identified several antibodies with the capacity to protect against vaccinia virus infection. We believe this technology will allow us to identify combination therapies for monkeypox and smallpox viruses which was difficult to achieve before. Furthermore, our data suggest that applying this technology has the potential to increase the throughput of screening novel antivirals to shorten the discovery time for antivirals.”

About TNX-3400

TNX-3400 is the term for series of monoclonal antibodies which bind to key components of pox viruses such as monkeypox and smallpox and protect cells and tissues from infection with these pandemic causing viruses. These antibodies are being developed as broad-spectrum antipox virus and to potentially prevent or treat monkeypox and smallpox infection.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022 and expects interim data in the third quarter of 2023. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the first quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is expected to enter the clinic with a Phase 2 study in the first quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the first half of 2023. Tonix’s infectious disease pipeline includes a vaccine in development to prevent smallpox and monkeypox, TNX-801, a next-generation vaccine to prevent COVID-19, TNX-1850, a platform to make fully human monoclonal antibodies to treat COVID-19, TNX-3600, and humanized anti-SARS-CoV-2 monoclonal antibodies, TNX-3800, recently licensed from Curia. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in Kenya in the second half of 2023.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; delays and uncertainties caused by the global COVID-19 pandemic; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2021, as filed with the Securities and Exchange Commission (the “SEC”) on March 14, 2022, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

BRENTWOOD, Tenn., Jan. 24, 2023 (GLOBE NEWSWIRE) — CoreCivic, Inc. (NYSE: CXW) (the Company) announced today that it will release its 2022 fourth quarter financial results after the market closes on Wednesday, February 8, 2023. A live broadcast of CoreCivic’s conference call will begin at 10:00 a.m. central time (11:00 a.m. eastern time) on Thursday, February 9, 2023.

To participate via telephone and join the call live, please register in advance here https://register.vevent.com/register/BId87fe936f05a41fa8057f46bf4310550. Upon registration, telephone participants will receive a confirmation email detailing how to join the conference call, including the dial-in number and a unique passcode.

Participants may access the audio-only webcast of the conference call from the Company’s website at www.corecivic.com under the “Events & Presentations” section of the “Investors” page. A replay of the webcast will be available for seven days.

About CoreCivic

CoreCivic is a diversified, government-solutions company with the scale and experience needed to solve tough government challenges in flexible, cost-effective ways. We provide a broad range of solutions to government partners that serve the public good through high-quality corrections and detention management, a network of residential and non-residential alternatives to incarceration to help address America’s recidivism crisis, and government real estate solutions. We are the nation’s largest owner of partnership correctional, detention and residential reentry facilities, and believe we are the largest private owner of real estate used by government agencies in the United States. We have been a flexible and dependable partner for government for 40 years. Our employees are driven by a deep sense of service, high standards of professionalism and a responsibility to help government better the public good. Learn more at www.corecivic.com.

Harte Hanks (NASDAQ: HHS) is a leading global customer experience company whose mission is to partner with clients to provide them with CX strategy, data-driven analytics and actionable insights combined with seamless program execution to better understand, attract, and engage their customers. Using its unparalleled resources and award-winning talent in the areas of Customer Care, Fulfillment and Logistics, and Marketing Services, Harte Hanks has a proven track record of driving results for some of the world’s premier brands including Bank of America, GlaxoSmithKline, Unilever, Pfizer, HBOMax, Volvo, Ford, FedEx, Midea, Sony, and IBM among others. Headquartered in Chelmsford, Massachusetts , Harte Hanks has over 2,500 employees in offices across the Americas, Europe and Asia Pacific .

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 Preview. Fundamentals at the company appear favorable and Q4 revenue and adj. EBITDA estimates appear to be on target. We are adjusting our EPS estimate to reflect the repurchase of its convertible preferred shares with Wipro. The agreement was for liquidation value at $9.9 million, plus 100,000 HHS shares. Due to an accounting treatment, the company is expected to report a non cash $1.6 million loss on the repurchase. We are adjusting our Q4 EPS from $0.34 to $0.12 to reflect this charge.

Q1 Outlook. The company’s first quarter revenue mix is expected to skew toward lower margin revenue business, plus the company is expected to spend more heavily on technology investments and for the integration of a recent acquisition, InsideOut. Q1 revenues are expected to increase year over year, but Adj. EBITDA is expected to be lower.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Tokens.com Corp is a publicly traded company that invests in Web3 assets and businesses focused on the Metaverse, NFTs, DeFi, and gaming based digital assets. Tokens.com is the majority owner of Metaverse Group, one of the world’s first virtual real estate companies. Hulk Labs, a wholly-owned Tokens.com subsidiary, focuses on investing in play-to-earn revenue generating gaming tokens and NFTs. Additionally, Tokens.com owns and stakes crypto assets to earn additional tokens. Through its growing digital assets and NFTs, Tokens.com provides public market investors with a simple and secure way to gain exposure to Web3.

Joe Gomes, Managing Director – Generalist Analyst, Noble Capital Markets, Inc.

Joshua Zoepfel, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Genesis Global. In a recurring theme in the crypto space lately, last week Genesis Global Holdco LLC, the holding company of troubled cryptocurrency lender Genesis Global Capital, filed for Chapter 11 bankruptcy protection. Notably, in its filing, Genesis Global Capital said it expects that through the restructuring process, there will be money left over to pay unsecured creditors.

Tokens.com Impact. Tokens.com has an open loan facility with Genesis, for which the Company is required to post collateral in token assets. Based on the closing price on January 19, 2023, this collateral was worth US$749,000. Tokens.com has a loan outstanding against this collateral of US$138,000. The difference between the collateral and the loan value represents approximately 3.1% of Tokens.com’s total assets of US$20.0 million as at September 30, 2022. Tokens.com has requested to have its collateral returned and repay the loan outstanding in full.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Production from first drilled well is coming. The Eoff PPC #3 well in the Breedlove Field was completed in October and is going through a Flowback Recovery Period (removal of liquids). It was shut down due to freezing temperatures. Management expects full production by the end of February and will disclose flow rates then. The company hinted that it will probably go forward with converting the well to a horizontal well at an additional $1.1 million cost.

Cash is tight. Permex’s cash position is down to $2.5 million, not enough to drill another well. The company is opposed to taking on debt (which we agree with) because debt is the Achilles heel of start-up energy companies should energy prices decline. The company discussed selling acreage but indicated that it neither has a large contiguous field to sell (outside of its Breedlove Field position) nor does it have small, producing property that might be of interest to energy companies. Management would like to issue stock but not at the current stock price of 4% of net asset value.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Functional magnetic resonance imaging (fMRI), which measures changes in blood flow throughout the brain, has been used over the past couple of decades for a variety of applications, including “functional anatomy” — a way of determining which brain areas are switched on when a person carries out a particular task. fMRI has been used to look at people’s brains while they’re doing all sorts of things — working out math problems, learning foreign languages, playing chess, improvising on the piano, doing crossword puzzles, and even watching TV shows like “Curb Your Enthusiasm.”

One pursuit that’s received little attention is computer programming — both the chore of writing code and the equally confounding task of trying to understand a piece of already-written code. “Given the importance that computer programs have assumed in our everyday lives,” says Shashank Srikant, a PhD student in MIT’s Computer Science and Artificial Intelligence Laboratory (CSAIL), “that’s surely worth looking into. So many people are dealing with code these days — reading, writing, designing, debugging — but no one really knows what’s going on in their heads when that happens.” Fortunately, he has made some “headway” in that direction in a paper — written with MIT colleagues Benjamin Lipkin (the paper’s other lead author, along with Srikant), Anna Ivanova, Evelina Fedorenko, and Una-May O’Reilly — that was presented earlier this month at the Neural Information Processing Systems Conference held in New Orleans.

The new paper built on a 2020 study, written by many of the same authors, which used fMRI to monitor the brains of programmers as they “comprehended” small pieces, or snippets, of code. (Comprehension, in this case, means looking at a snippet and correctly determining the result of the computation performed by the snippet.) The 2020 work showed that code comprehension did not consistently activate the language system, brain regions that handle language processing, explains Fedorenko, a brain and cognitive sciences (BCS) professor and a coauthor of the earlier study. “Instead, the multiple demand network — a brain system that is linked to general reasoning and supports domains like mathematical and logical thinking — was strongly active.” The current work, which also utilizes MRI scans of programmers, takes “a deeper dive,” she says, seeking to obtain more fine-grained information.

Whereas the previous study looked at 20 to 30 people to determine which brain systems, on average, are relied upon to comprehend code, the new research looks at the brain activity of individual programmers as they process specific elements of a computer program. Suppose, for instance, that there’s a one-line piece of code that involves word manipulation and a separate piece of code that entails a mathematical operation. “Can I go from the activity we see in the brains, the actual brain signals, to try to reverse-engineer and figure out what, specifically, the programmer was looking at?” Srikant asks. “This would reveal what information pertaining to programs is uniquely encoded in our brains.” To neuroscientists, he notes, a physical property is considered “encoded” if they can infer that property by looking at someone’s brain signals.

Take, for instance, a loop — an instruction within a program to repeat a specific operation until the desired result is achieved — or a branch, a different type of programming instruction than can cause the computer to switch from one operation to another. Based on the patterns of brain activity that were observed, the group could tell whether someone was evaluating a piece of code involving a loop or a branch. The researchers could also tell whether the code related to words or mathematical symbols, and whether someone was reading actual code or merely a written description of that code.

That addressed a first question that an investigator might ask as to whether something is, in fact, encoded. If the answer is yes, the next question might be: where is it encoded? In the above-cited cases — loops or branches, words or math, code or a description thereof — brain activation levels were found to be comparable in both the language system and the multiple demand network.

A noticeable difference was observed, however, when it came to code properties related to what’s called dynamic analysis.

Programs can have “static” properties — such as the number of numerals in a sequence — that do not change over time. “But programs can also have a dynamic aspect, such as the number of times a loop runs,” Srikant says. “I can’t always read a piece of code and know, in advance, what the run time of that program will be.” The MIT researchers found that for dynamic analysis, information is encoded much better in the multiple demand network than it is in the language processing center. That finding was one clue in their quest to see how code comprehension is distributed throughout the brain — which parts are involved and which ones assume a bigger role in certain aspects of that task.

The team carried out a second set of experiments, which incorporated machine learning models called neural networks that were specifically trained on computer programs. These models have been successful, in recent years, in helping programmers complete pieces of code. What the group wanted to find out was whether the brain signals seen in their study when participants were examining pieces of code resembled the patterns of activation observed when neural networks analyzed the same piece of code. And the answer they arrived at was a qualified yes.

“If you put a piece of code into the neural network, it produces a list of numbers that tells you, in some way, what the program is all about,” Srikant says. Brain scans of people studying computer programs similarly produce a list of numbers. When a program is dominated by branching, for example, “you see a distinct pattern of brain activity,” he adds, “and you see a similar pattern when the machine learning model tries to understand that same snippet.”

Mariya Toneva of the Max Planck Institute for Software Systems considers findings like this “particularly exciting. They raise the possibility of using computational models of code to better understand what happens in our brains as we read programs,” she says.

The MIT scientists are definitely intrigued by the connections they’ve uncovered, which shed light on how discrete pieces of computer programs are encoded in the brain. But they don’t yet know what these recently-gleaned insights can tell us about how people carry out more elaborate plans in the real world. Completing tasks of this sort — such as going to the movies, which requires checking showtimes, arranging for transportation, purchasing tickets, and so forth — could not be handled by a single unit of code and just a single algorithm. Successful execution of such a plan would instead require “composition” — stringing together various snippets and algorithms into a sensible sequence that leads to something new, just like assembling individual bars of music in order to make a song or even a symphony. Creating models of code composition, says O’Reilly, a principal research scientist at CSAIL, “is beyond our grasp at the moment.”

Lipkin, a BCS PhD student, considers this the next logical step — figuring out how to “combine simple operations to build complex programs and use those strategies to effectively address general reasoning tasks.” He further believes that some of the progress toward that goal achieved by the team so far owes to its interdisciplinary makeup. “We were able to draw from individual experiences with program analysis and neural signal processing, as well as combined work on machine learning and natural language processing,” Lipkin says. “These types of collaborations are becoming increasingly common as neuro- and computer scientists join forces on the quest towards understanding and building general intelligence.”

")

(CNW Group/Defense Metals Corp.)")