Nvidia’s stock tumbled nearly 8% on Tuesday, leading a broad decline in semiconductor stocks and contributing to a rough start for the market this month. The S&P 500 experienced a drop of over 1% amid a broader market slump, exacerbated by disappointing data from the ISM manufacturing index. This data raised concerns about the strength of the economy and the potential for the Federal Reserve to cut interest rates, which in turn impacted investor sentiment across various sectors.

The semiconductor sector, which has been a high-flyer over the past year thanks to the AI boom, saw significant losses. Nvidia, a dominant player in AI data center chips, saw its stock fall dramatically. Other major chipmakers also experienced declines, with Intel and Marvell down 8%, Broadcom falling around 6%, and AMD and Qualcomm each dropping 6%. The SMH, an index tracking semiconductor stocks, was down 6%, marking its biggest one-day loss in a month.

The optimism driving chip stocks had been fueled by the belief that the artificial intelligence revolution would lead to increased demand for semiconductors and memory. Nvidia, in particular, has seen its stock rise nearly 129% so far in 2024, bolstered by its leading position in AI data center chips. However, some investors were unsettled by Nvidia’s recent forecast, which suggested a potential slowdown in growth despite reporting impressive quarterly earnings of $30 billion and a 154% year-on-year increase in data center revenue.

Meanwhile, other chipmakers are striving to capture investor attention with their AI products. Intel unveiled new laptop processors capable of running AI programs on-device, and Broadcom, which collaborates with major companies to develop custom AI chips, is set to report its third-quarter earnings on Thursday. Qualcomm continues to promote its chips as optimal for AI applications on Android phones.

Despite the challenges faced by Nvidia and other chipmakers, Wall Street remains largely optimistic about the sector’s long-term prospects. Analysts from Stifel reiterated their Buy rating on Nvidia, maintaining a $165 price target. They remain confident in Nvidia’s role as a primary beneficiary of the ongoing modernization of data center computing.

As Nvidia prepares to ramp up production of its next-generation Blackwell chip later this year, analysts expect the stock to potentially recover and continue its upward trajectory, provided the new products meet market expectations.

Key Points: – U.S. consumer spending increased 0.5% in July, showing economic strength – Inflation remains moderate, with PCE price index rising 2.5% year-on-year – Robust spending challenges expectations for aggressive Fed rate cuts

In a surprising turn of events, U.S. consumer spending showed remarkable strength in July, potentially altering the Federal Reserve’s monetary policy trajectory. This robust economic indicator may put a damper on expectations for aggressive interest rate cuts, particularly the anticipated half-percentage-point reduction in September.

Consumer spending, which accounts for over two-thirds of U.S. economic activity, rose by 0.5% in July, following a 0.3% increase in June. This uptick, aligning with economists’ forecasts, suggests the economy is on firmer ground than previously thought. After adjusting for inflation, real consumer spending gained 0.4%, maintaining momentum from the second quarter. Conrad DeQuadros, senior economic advisor at Brean Capital, notes, “There is nothing here to push the Fed to a half-point cut. This is not the kind of spending growth associated with recession.”

While spending surged, inflation remained relatively contained. The Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, rose 0.2% for the month and 2.5% year-on-year. Core PCE inflation, which excludes volatile food and energy prices, increased by 0.2% monthly and 2.6% annually. These figures, while showing progress towards the Fed’s 2% target, indicate that inflationary pressures persist, potentially complicating the central bank’s decision-making process.

Despite a jump in the unemployment rate to a near three-year high of 4.3% in July, which initially stoked recession fears, the labor market continues to generate decent wage growth. Personal income rose 0.3% in July, with wages climbing at the same rate. This suggests that the slowdown in the labor market is primarily due to reduced hiring rather than increased layoffs.

Fed Chair Jerome Powell recently signaled that a rate cut was imminent, acknowledging concerns over the labor market. However, the strong consumer spending data may force the Fed to reconsider the pace and magnitude of potential rate cuts. David Alcaly, lead macroeconomic strategist at Lazard Asset Management, offers a longer-term perspective: “There’s a lot of focus right now on the pace of rate cuts in the short term, but we believe it ultimately will matter more how deep the rate-cutting cycle goes over time.”

The Atlanta Fed has raised its third-quarter GDP growth estimate to a 2.5% annualized rate, up from 2.0%. This revision, coupled with the strong consumer spending data, paints a picture of an economy that’s more resilient than many had anticipated. The increase in spending was broad-based, covering both goods and services. Consumers spent more on motor vehicles, housing and utilities, food and beverages, recreation services, and financial services. They also boosted spending on healthcare, visited restaurants and bars, and stayed at hotels.

As the Fed navigates this complex economic landscape, investors and policymakers alike will be closely watching for signs of whether the central bank will prioritize fighting inflation or supporting economic growth in its upcoming decisions. The robust consumer spending data suggests that the economy may not need as much support as previously thought, potentially leading to a more cautious approach to rate cuts.

For investors, this economic resilience presents both opportunities and challenges. While strong consumer spending bodes well for many sectors, it may also lead to a less accommodative monetary policy than some had hoped for. As always, a diversified approach and close attention to economic indicators will be crucial for navigating these uncertain waters.

HOUSTON, Aug. 29, 2024 (GLOBE NEWSWIRE) — Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) (NASDAQ: GLDD), the largest provider of dredging services in the United States, announced today that the Company’s issuer credit rating has been upgraded to “B-” from “CCC+” by S&P Global Ratings (“S&P”).

S&P based its ratings upgrade in part due to the Company’s improved revenue and profitability in the first half of 2024. S&P also cited that the Company’s strong backlog and recent awards gives visibility into improved cash flows through 2025. The stable rating reflects S&P’s expectation that the Company will continue to expand revenue and improve profitability throughout the remainder of 2024 and into 2025.

Great Lakes’ Senior Vice President and CFO Scott Kornblau commented, “We are pleased with the recent credit rating upgrade from S&P, which further demonstrates the improvements we have made this year to our balance sheet, cash flows and overall performance. This upgrade not only validates our efforts but also positions us for future growth and success.”

The Company Great Lakes Dredge & Dock Corporation (“Great Lakes” or the “Company”) is the largest provider of dredging services in the United States. In addition, Great Lakes is fully engaged in expanding its core business into the rapidly developing offshore wind energy industry. The Company has a long history of performing significant international projects. The Company employs experienced civil, ocean and mechanical engineering staff in its estimating, production and project management functions. In its over 134-year history, the Company has never failed to complete a marine project. Great Lakes owns and operates the largest and most diverse fleet in the U.S. dredging industry, comprised of approximately 200 specialized vessels. Great Lakes has a disciplined training program for engineers that ensures experienced-based performance as they advance through Company operations. The Company’s Incident-and Injury-Free® (IIF®) safety management program is integrated into all aspects of the Company’s culture. The Company’s commitment to the IIF® culture promotes a work environment where employee safety is paramount.

Cautionary Note Regarding Forward-Looking Statements Certain statements in this press release may constitute “forward-looking” statements as defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), the Private Securities Litigation Reform Act of 1995 (the “PSLRA”) or in releases made by the Securities and Exchange Commission (the “SEC”), all as may be amended from time to time. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Great Lakes and its subsidiaries, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Statements that are not historical fact are forward-looking statements. These cautionary statements are being made pursuant to the Exchange Act and the PSLRA with the intention of obtaining the benefits of the “safe harbor” provisions of such laws. Great Lakes cautions investors that any forward-looking statements made by Great Lakes are not guarantees or indicative of future events.

Although Great Lakes believes that its plans, intentions and expectations reflected in this press release are reasonable, actual events could differ materially. The forward-looking statements contained in this press release are made only as of the date hereof and Great Lakes does not have or undertake any obligation to update or revise any forward-looking statements whether as a result of new information, subsequent events or otherwise, unless otherwise required by law.

For further information contact: Tina Baginskis Director, Investor Relations 630-574-3024

For more than 45 years, 1-800-Flowers.com has offered truly original floral arrangements, plants and unique gifts to celebrate birthdays, anniversaries, everyday occasions, and seasonal holidays, and to deliver comfort during times of grief. Backed by a caring team obsessed with service, 1-800-Flowers.com provides customers thoughtful ways to express themselves and connect with the most important people in their lives. 1-800-Flowers.com is part of the 1-800-FLOWERS.COM, Inc. family of brands. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q4 results. The company reported Q4 revenue of $360.9 million, which was modestly below our estimate of $373.5 million by 3.4%. Additionally, Adj. EBITDA loss in the quarter of $8.8 million was below our estimate of negative $5.8 million. Illustrated in Figure #1 Q4 Results. While the results were softer than expected, there were some bright spots. Notably, Q4 gross profit margin increased 130 basis points from the prior year period, which was largely attributed to lower freight and commodity costs, as well as cost saving initiatives.

Stepping up revenue investments. Management indicated that it plans to step up marketing, post the upcoming elections, and will introduce new products at price points that may help to offset the lackluster sales particularly for its everyday gifting products. There has been a bifurcation of sales for its products that target its high end consumer and that for consumers that are price sensitive.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Key Points: – Nvidia’s stellar earnings fail to impress investors as AI excitement wanes – Big Tech struggles to show concrete returns on massive AI investments – Nvidia’s diverse applications provide stability amid AI uncertainty

The artificial intelligence gold rush that has captivated Wall Street for the past 18 months is showing signs of cooling, as investors begin to demand more tangible results from the technology sector’s massive AI investments. This shift in sentiment was starkly illustrated by the market’s lukewarm response to Nvidia’s recent earnings report, which, despite showcasing impressive growth, failed to ignite the enthusiasm that has become characteristic of the AI narrative.

Nvidia, the world’s leading AI chip producer, delivered a quarterly report that would be the envy of most businesses. Sales surged 122% in the second quarter, profits doubled, and the outlook for the current quarter remained strong. Yet, Nvidia’s shares slumped 7% following the announcement, a telling indicator of changing investor expectations in the AI space.

The muted reaction to Nvidia’s stellar performance speaks volumes about the evolving psychology of Wall Street. For months, investors have been throwing money at any company with potential AI profits, creating a hype train that has carried Nvidia to a staggering 3,000% stock price increase over the past five years. The company’s quarterly earnings reports had taken on an almost mythical quality, consistently beating expectations and training Wall Street to anticipate the extraordinary.

However, the initial thrill of AI breakthroughs is beginning to fade, and investors are adopting a more discerning approach. The key question now is no longer about the potential of AI, but about its ability to generate concrete revenue for the companies heavily invested in its development. Big Tech firms have poured billions into AI research and development, yet have relatively little to show for it in terms of transformative products or services.

While chatbots like ChatGPT and Google Gemini have impressed, they haven’t quite lived up to the game-changing potential touted by their creators. The current consumer demand for AI seems centered on making mundane tasks less onerous, rather than the grand visions of AI revolutionizing creative processes or complex problem-solving that tech companies have been promoting.

For Nvidia, this reality check presents both challenges and opportunities. Unlike many AI startups built on promises and potential, Nvidia has a solid foundation in producing essential hardware for the tech industry. CEO Jensen Huang emphasized that Nvidia’s chips power not just AI chatbots, but also ad-targeting systems, search engines, robotics, and recommendation algorithms. The company’s data center business continues to drive nearly 90% of its total revenue, providing a stable base even as the AI hype cycle fluctuates.

However, Nvidia isn’t without its vulnerabilities. The company’s current dominance in AI chip production is partly due to the complexity and difficulty of replicating its products. But this advantage may not be permanent. Tech giants like Google and Amazon, currently reliant on Nvidia’s chips, are racing to develop their own AI hardware. The potential emergence of these customers as competitors could pose a significant threat to Nvidia’s market position in the long term.

As the AI landscape continues to evolve, investors are likely to become increasingly discriminating, focusing on companies that can demonstrate practical applications and revenue generation from their AI investments. For the tech industry as a whole, this shift may necessitate a recalibration of expectations and a more grounded approach to AI development and marketing.

The cooling of AI fever doesn’t signal the end of the technology’s potential. Rather, it marks a transition from unbridled enthusiasm to a more measured evaluation of AI’s place in the business world. As this reality check unfolds, companies that can bridge the gap between AI’s promise and its practical, revenue-generating applications will likely emerge as the true winners in this next phase of technological evolution.

Investigator-initiated Phase 2 trial to evaluate TNX-102 SL’s potential to reduce severity of acute stress reaction (ASR) and frequency of acute stress disorder (ASD) and posttraumatic stress disorder (PTSD) expected to begin third quarter 2024

Currently, no medication approved at or near point-of-care to treat patients suffering from traumatic events and support their long-term health

CHATHAM, N.J., Aug. 29, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a fully-integrated biopharmaceutical company with marketed products and a pipeline of development candidates, presented clinical data on? acute stress reaction and prevention of PTSD data of TNX-102 SL in two poster presentations and presented preclinical data demonstrating automated high-throughput assay enabling screening for therapeutics to accelerate wound healing in a third poster presentation at the 2024 Military Health System Research Symposium (MHSRS), held August 26-29, 2024, in Kissimmee, Fla. Copies of the Company’s posters, titled:

“Two Clinical Trials of Bedtime Sublingual Cyclobenzaprine (TNX-102 SL) in Military-Related Posttraumatic Stress Disorder (PTSD) Provide Rationale to Study TNX-102 SL in the Aftermath of Trauma to Reduce Acute Stress Disorder (ASD) and Prevent PTSD”;

“Development of the AURORA Platform Trial Network to Test Interventions to Reduce Acute Stress Reaction Symptoms, and Illustration of Use Testing Sublingual Cyclobenzaprine TNX-102 SL”;

“Integrating Automated High-Throughput Scratch Assay and Cell Painting for Comprehensive Analysis of Cell Migration and Wound Healing”, are available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com.

TNX-102 SL is being evaluated for the reduction in severity of acute stress reaction (ASR) and the frequency of acute stress disorder (ASD) and posttraumatic stress disorder (PTSD) when administered within 24 hours of trauma event. In two double-blind, randomized clinical trials of military-related PTSD, TNX-102 SL showed effects on sleep and PTSD symptoms in two and four weeks of treatment1. Supportive data on the effects of TNX-102 SL on reducing PTSD symptoms suggest early intervention immediately after trauma using TNX-102 SL has the potential to reduce ASR/ASD symptoms which are similar to those of PTSD2,3. TNX-102 SL has been well-tolerated with no recognized liability for tolerance or abuse. Data from these trials support testing of TNX-102 SL within 24 hours of index trauma for effects on acute stress reaction (ASR) symptoms and the incidence of PTSD. In the U.S. Department of Defense-funded Optimizing Acute Stress Reaction Interventions (OASIS) trial conducted by the University of North Carolina under an investigator-initiated investigational new drug (IND) application, 14 days of bedtime TNX-102 SL will be dosed and tested in the immediate aftermath of motor vehicle collision. The study will test the potential for TNX-102 SL to target trauma-related sleep disturbance and its ability to facilitate recovery from ASR and to prevent PTSD. The results may ultimately provide military personnel with a new treatment option that, when administered in the early aftermath of a traumatic event to individuals with ASR symptoms, improves warfighter function.

“In previous trials, TNX-102 SL has been shown to improve sleep quality in PTSD and increased activity on sleep and stress-related symptoms in the first several weeks of treatment after a trauma event”, said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Since sleep disturbance plays a critical role in the development and maintenance of PTSD, sleep improvements may reorient the trajectory of posttraumatic pathology from acute trauma towards early recovery. The OASIS study is driven by the observation that the symptoms of ASR and PTSD are similar and by the hypothesis that TNX-102 SL’s effect on sleep quality may reduce ASR symptoms, potentially providing military personnel, veterans, and civilians with a new treatment option that, when administered in the early aftermath of a traumatic event, improves recovery, job performance, and quality of life.”

The investigator-initiated OASIS trial will examine the safety and efficacy of TNX-102 SL to reduce adverse posttraumatic neuropsychiatric sequelae among patients presenting to the emergency department (ED) after a motor vehicle collision. The trial plans to enroll approximately 180 trauma survivors at ED study sites around the U.S. Participants will be randomized in the ED to receive a two-week course of either TNX-102 SL 5.6 mg or placebo. The first participant for the OASIS trial is expected to enroll in the third quarter of 2024.

The OASIS trial will build upon a foundation of knowledge and infrastructure developed through the UNC-led, $40 million AURORA initiative. AURORA is a major national research initiative to improve the understanding, prevention and recovery of individuals who experience a traumatic event. AURORA is supported by funding from the National Institutes of Health (NIH), leading brain health nonprofit One Mind, private foundations, and partnerships with leading tech companies, such as Mindstrong Health and Verily Life Sciences, the healthcare arm of Alphabet, the parent company of Google.

Acute and chronic stress disorders can affect both civilian and military populations. According to the National Center for PTSD, in the U.S. about 60% of men and 50% of women experience at least one trauma in their lives.4 In the U.S. alone, one-third of ED visits (40-50 million patients per year) involve evaluation after trauma exposures, and in a 2014 study involving 3,157 US veterans, 87% reported exposure to at least one potentially traumatic event during their service.5 Moreover, as many as 500,000 U.S. troops who served in wars between 2001 and 2015 were diagnosed with PTSD.6

The third poster, titled “Integrating Automated High-Throughput Scratch Assay and Cell Painting for Comprehensive Analysis of Cell Migration and Wound Healing”, demonstrated optimization of a highly efficient scratch-wound assay development method. The scratch-wound assay, commonly used to study wound healing, has limitations that the study addresses by introducing an automated miniaturized high-throughput wound healing assay, enabling mass screening and identification of novel therapies for wound-healing. The screening technology was merged with cell-painting to allow discovery of morphological characteristics to identify mechanism of action of drugs for wound healing.

Tonix Pharmaceuticals Holding Corp.* Tonix is a fully-integrated biopharmaceutical company focused on developing, licensing and commercializing therapeutics to treat and prevent human disease and alleviate suffering. Tonix recently announced the U.S. Department of Defense (DoD), Defense Threat Reduction Agency (DTRA) awarded it a contract for up to $34 million over five years in an Other Transaction Agreement (OTA) to develop TNX-4200 small molecule broad-spectrum antiviral agents targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, MD. The company’s Good Manufacutring Practice (GMP)-capable advanced manufacturing facility in Dartmouth, MA was purpose-built to manufacture TNX-801 and the GMP suites are ready to be reactivated in case of a national or international emergency. Tonix’s development portfolio is focused on central nervous system (CNS) disorders. Tonix’s priority is to submit a New Drug Application (NDA) to the FDA in the second half of 2024 for TNX-102 SL, a product candidate for which two statistically significant Phase 3 studies have been completed for the management of fibromyalgia. The FDA has granted Fast Track designation to TNX-102 SL for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction. Tonix’s CNS portfolio includes TNX-1300 (cocaine esterase), a biologic designed to treat cocaine intoxication that has Breakthrough Therapy designation. Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix also has product candidates in development in the areas of rare disease and infectious disease. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

TNX-102 SL (cyclobenzaprine HCl sublingual tablets) has not been approved for any indication; (Tonmya™ is conditionally approved by FDA for the management of fibromyalgia)

Sullivan GM, et al. Randomized clinical trial of bedtime sublingual cyclobenzaprine (TNX-102 SL) in military-related PTSD and the role of sleep quality in treatment response. Psychiatry Res. 2021 Jul;301:113974.

Parmenter ME, et al. A phase 3, randomized, placebo-controlled, trial to evaluate the efficacy and safety of bedtime sublingual cyclobenzaprine (TNX-102 SL) in military-related posttraumatic stress disorder. Psychiatry Res. 2024 (In Press). https://doi.org/10.1016/j.psychres.2024.115764

Goldstein RB, et al. Soc Psychiatry Psychiatr Epidemiol. 2016. 51(8):1137-48

Wisco BE, et al. J Clin Psychiatry. 2014. 75(12):1338-46

Thompson M. Time. 2015;185(12):40-3

Forward Looking Statements Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 1, 2024, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today announced that Bill Shea has confirmed his intention to retire as Chief Financial Officer, effective December 29, 2024. The Board of Directors has appointed James Langrock as Chief Financial Officer, effective December 29, 2024.

“I want to take this opportunity to congratulate Bill on his upcoming retirement and to thank him for his three decades of tireless commitment to our company,” said Jim McCann, Chairman and Chief Executive Officer of 1-800-FLOWERS.COM, Inc. “Bill has been a terrific partner to me and a tremendous asset to our company during a period of tremendous growth and transformation. We wish Bill all the best upon his retirement.”

“I also want to congratulate James on his appointment to Chief Financial Officer upon Bill’s retirement,” Mr. McCann continued. “James has been a great addition to our leadership team since joining the Company and brings a great wealth of financial expertise to our company.”

Mr. Langrock joined 1-800-FLOWERS.COM, Inc. in April as Chief Administrative Officer, bringing a broad range of finance experience to the Company. Prior to joining the Company, Mr. Langrock held the position of Chief Financial Officer at several public and privately held companies, including Charcuterie Artisans, The Hain Celestial Group, and Monster Worldwide, Inc.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge on eligible products across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among America’s Most Trustworthy Companies by Newsweek. 1-800-FLOWERS.COM, Inc. was also recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com.

FLWS–COMP FLWS-FN

Special Note Regarding Forward Looking Statements:

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements represent the Company’s current expectations or beliefs concerning future events and can generally be identified using statements that include words such as “estimate,” “expects,” “project,” “believe,” “anticipate,” “intend,” “plan,” “foresee,” “forecast,” “likely,” “should,” “will,” “target” or similar words or phrases. These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of the Company’s control, which could cause actual results to differ materially from the results expressed or implied in the forward-looking statements, including, but not limited to, statements regarding the Company’s ability to achieve its guidance for the full Fiscal year; the Company’s ability to leverage its operating platform and reduce its operating expense ratio; its ability to successfully integrate acquired businesses and assets; its ability to successfully execute its strategic initiatives; its ability to cost effectively acquire and retain customers; the outcome of contingencies, including legal proceedings in the normal course of business; its ability to compete against existing and new competitors; its ability to manage expenses associated with sales and marketing and necessary general and administrative and technology investments; its ability to reduce promotional activities and achieve more efficient marketing programs; and general consumer sentiment and industry and economic conditions that may affect levels of discretionary customer purchases of the Company’s products. The Company undertakes no obligation to publicly update any of the forward-looking statements, whether because of new information, future events or otherwise, made in this release or in any of its SEC filings. Consequently, you should not consider any such list to be a complete set of all potential risks and uncertainties. For a more detailed description of these and other risk factors, refer to the Company’s SEC filings, including the Company’s Annual Reports on Form 10-K and its Quarterly Reports on Form 10-Q.

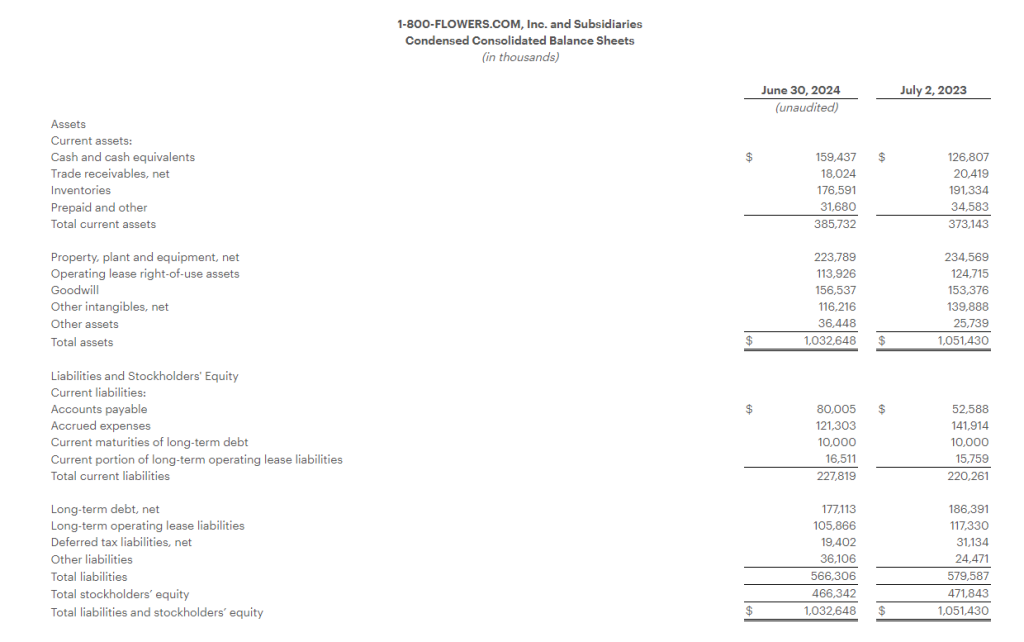

Reports Fiscal Year 2024 Revenue of $1.83 Billion and a Net Loss of $6.1 Million, which Includes a Non-Cash Impairment Charge of $19.8 million Recorded in the Second Quarter

Fiscal Year 2024 Gross Profit Margin Increased 260 Basis Points to 40.1%

Fiscal Year 2024 Adjusted EBITDA1 Increased to $93.1 million

Issues Fiscal Year 2025 Outlook

(1) Refer to “Definitions of Non-GAAP Financial Measures” and the tables attached at the end of this press release for reconciliation of non-GAAP results to applicable GAAP results.)

JERICHO, N.Y.–(BUSINESS WIRE)– 1-800-FLOWERS.COM, Inc. (NASDAQ: FLWS), a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships, today reported results for its Fiscal 2024 fourth quarter and year ended June 30, 2024.

“In a dynamic consumer environment that impacted discretionary consumer spending, especially amongst lower income households, our organization was able to grow year-over-year adjusted EBITDA, which benefitted from our significant gross margin recovery and our expense optimization efforts that more than offset the top line decline,” said Jim McCann, Chairman and Chief Executive Officer of 1-800-FLOWERS.COM, Inc. “During Fiscal 2024, through our Relationship Innovation initiatives, we significantly enhanced our gifting platform, including category expansion, broadening our price points, increasing our assortment of gifts available for same-day delivery, and enhancing the user experience. We also experienced a significant recovery in our gross profit margin, which benefitted from a reversion to the mean on a number of commodity costs combined with our Work Smarter initiatives to operate more efficiently.”

“As we turn to Fiscal 2025, with our gross margin recovery well underway, our organization continues to be keenly focused on improving our sales trends by leveraging our Relationship Innovation initiatives. Acknowledging the uncertain consumer environment, we anticipate revenue trends improving as the fiscal year progresses as consumers respond to our newer offerings and services. We are confident in our strategic direction to be the gifting destination of choice for thoughtful and expressive gift-giving occasions and remain focused on delivering long-term value to our shareholders,” Mr. McCann continued.

Fiscal 2024 Fourth Quarter Highlights

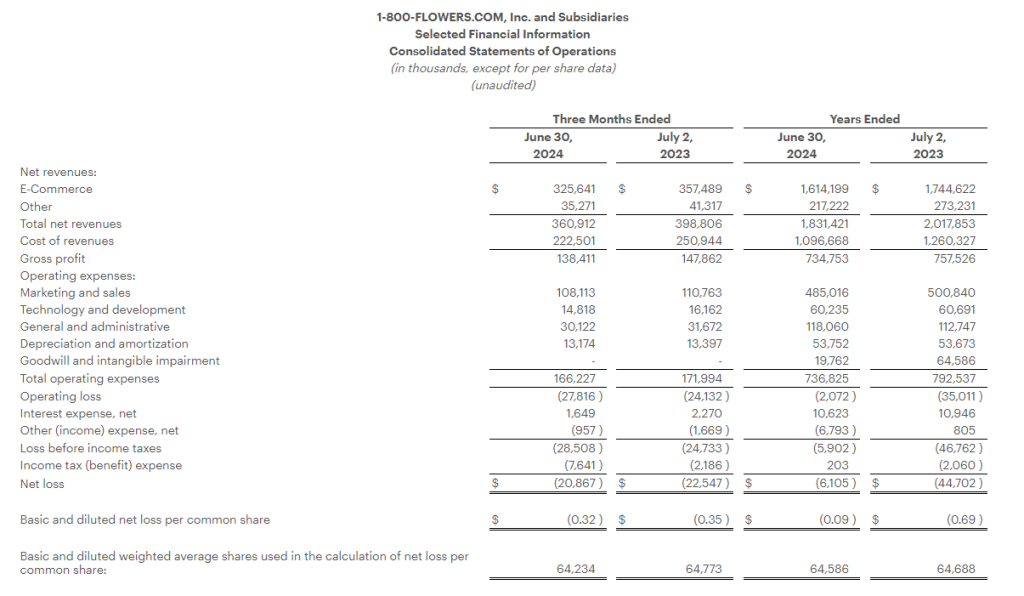

Total consolidated revenues decreased 9.5% to $360.9 million, compared with total consolidated revenues of $398.8 million in the prior year period.

Gross profit margin increased 130 basis points to 38.4%, compared with 37.1% in the prior year period. The gross profit margin improved on lower freight costs, a decline in certain commodity costs, and the Company’s logistics optimization efforts.

Operating expenses declined $5.8 million to $166.2 million, as compared with the prior year period.

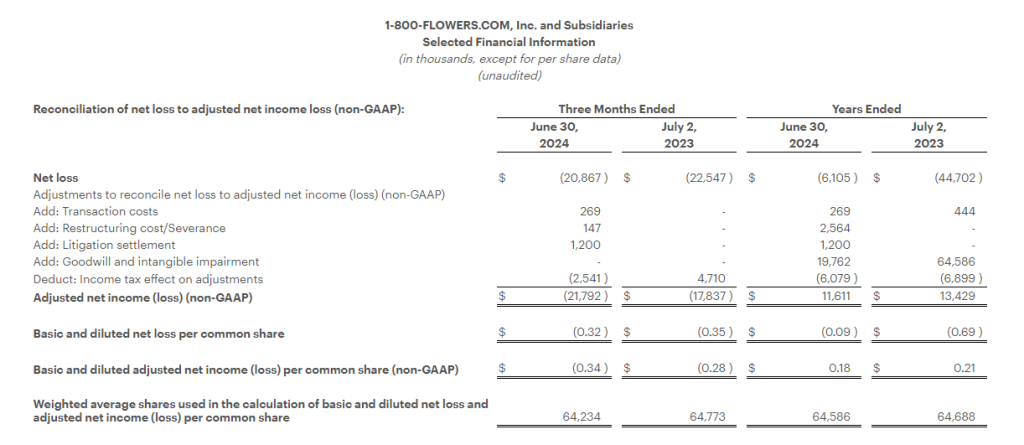

Net loss for the quarter was $20.9 million, or ($0.32) per share, as compared to a net loss of $22.5 million, or ($0.35) per share in the prior year period.

Adjusted Net Loss1 was $21.8 million, or ($0.34) per share, compared with an Adjusted Net Loss1 of $17.8 million, or ($0.28) per share, in the prior year period.

Adjusted EBITDA1 loss for the quarter was $8.8 million, as compared with an Adjusted EBITDA1 loss of $6.6 million in the prior year period.

Acquired Scharffen Berger Chocolate Maker, a high-end producer of extraordinary craft chocolates, that enhances and expands the Company’s chocolate offerings within its gourmet food and gift basket business. The acquisition closed after the fourth quarter ended.

Fiscal Year 2024 Highlights

Total consolidated revenues decreased 9.2% to $1.83 billion, compared with total consolidated revenues of $2.02 billion in the prior year period.

Gross profit margin increased 260 basis points to 40.1%, compared with 37.5% in the prior year period. The gross profit margin improved on lower freight costs, improved commodity costs, and the Company’s logistics optimization efforts.

Operating expenses declined $55.7 million to $736.8 million, as compared with the prior year period. Excluding impairment and other non-recurring charges in both periods, as well as the impact of the Company’s non-qualified deferred compensation plan in both periods, operating expenses declined by $22.2 million to $706.1 million, as compared with the prior year.

Net loss for the fiscal year was $6.1 million, or ($0.09) per share, compared with $44.7 million, or ($0.69) per share, in the prior year period. Both periods include impairment charges as outlined in the financial tables.

Adjusted Net Income1 was $11.6 million, or $0.18 per share, compared with Adjusted Net Income1 of $13.4 million, or $0.21 per share, in the prior year period.

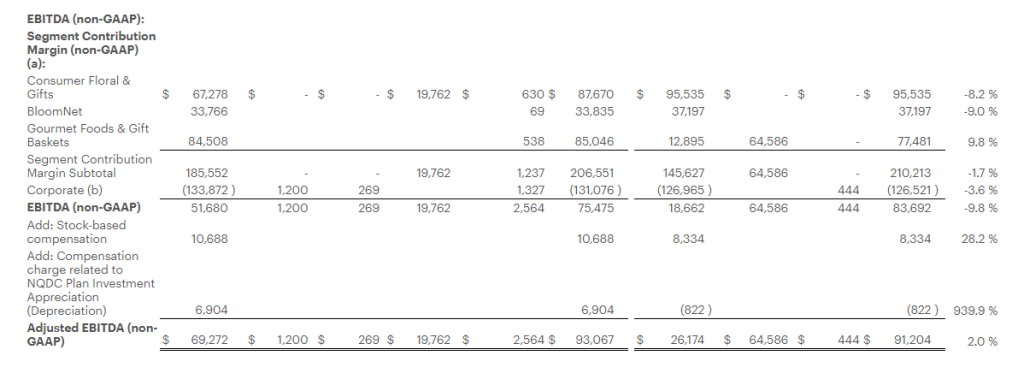

Adjusted EBITDA1 for the fiscal year was $93.1 million, as compared with $91.2 million in the prior year period.

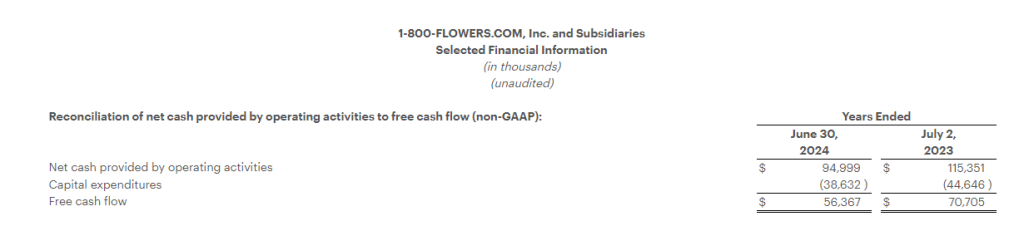

Net cash provided by operating activities was $95.0 million.

Generated Free Cash Flow1 of $56.4 million.

Segment Results

The Company provides Fiscal 2024 fourth quarter and full year selected financial results for its Gourmet Foods and Gift Baskets, Consumer Floral and Gifts, and BloomNet segments in the tables attached to this release and as follows:

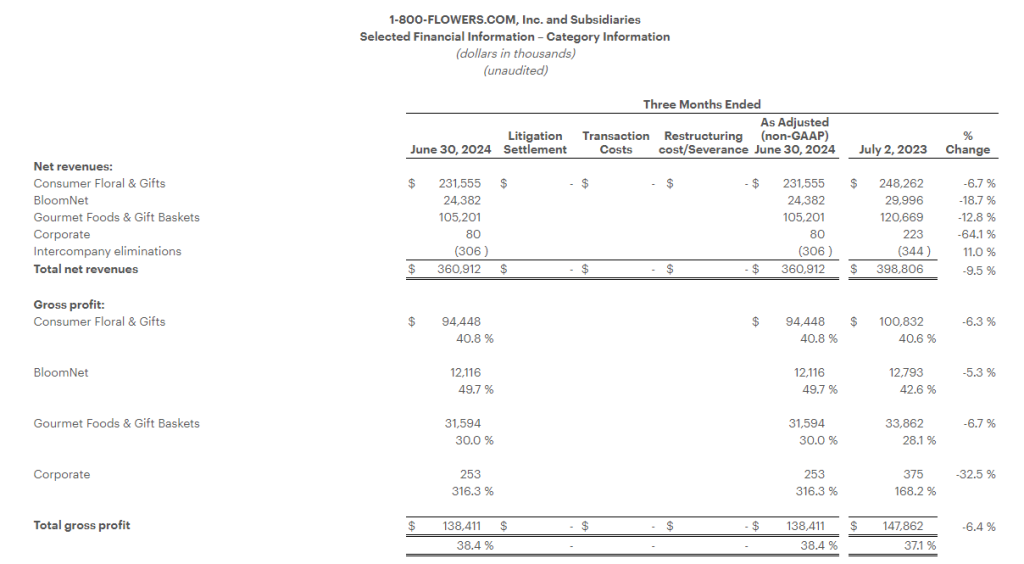

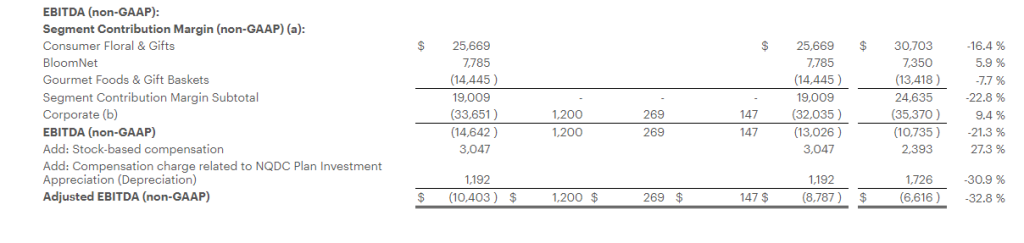

Gourmet Foods and Gift Baskets: Revenues for the quarter declined 12.8% to $105.2 million, as compared with the prior year period. Gross profit margin increased 190 basis points from the prior year period to 30.0%, benefiting from lower freight costs, the Company’s inventory and labor optimization efforts, as well as a decline in certain commodity costs. Segment contribution margin1 loss was $14.4 million, compared with a loss of $13.4 million in the prior year period.

For the full fiscal year, revenue decreased 9.4% to $874.3 million. Gross profit margin increased 340 basis points to 38.3%, benefiting from lower freight costs, the Company’s inventory and labor optimization efforts, as well as a decline in certain commodity costs. Excluding the impact of the severance charge in the current year and the impairment charge a year ago, segment contribution margin1 for the year was $85.0 million, compared with $77.5 million in the prior year.

Consumer Floral & Gifts: Revenues for the quarter declined 6.7% to $231.6 million, as compared with the prior year period. Gross profit margin increased 20 basis points from the prior year period to 40.8%. Segment contribution margin1 was $25.7 million, compared with $30.7 million in the prior year period.

For the full fiscal year, revenues decreased 7.7% to $849.8 million, as compared with the prior year period. Gross profit margin increased 130 basis points from the prior year period to 40.8%, improving on lower fulfillment costs and the Company’s logistics optimization efforts. Excluding the impact of the severance and impairment charges in the current year, segment contribution margin1 was $87.7 million, compared with $95.5 million in the prior year.

BloomNet: Revenues for the quarter declined 18.7% to $24.4 million, as compared with the prior year period. Revenue and gross margin were impacted by the lower volume of lower margin orders processed by BloomNet. Gross profit margin increased 710 basis points from the prior year period to 49.7%, also benefitting from lower ocean freight costs as well as product mix. Segment contribution margin1 was $7.8 million, compared with $7.4 million in the prior year period.

For the year, revenues decreased 19.1% to $107.8 million, as compared with the prior year period. Gross profit margin increased 550 basis points from the prior year period to 48.2% due to lower volume of lower margin orders, lower ocean freight costs, as well as product mix. Excluding the impact of the severance charge in the current year, segment contribution margin1 for the year was $33.8 million, compared with $37.2 million in the prior year.

Company Guidance

For Fiscal 2025, with a sustained challenging consumer environment, the Company expects revenue trends to improve as the fiscal year progresses benefitting from the company’s Relationship Innovation initiatives that have expanded the Company’s product offerings, broadened price points, and enhanced the user experience, combined with increased marketing spend. Additionally, the guidance assumes increased incentive compensation expense.

As a result, for Fiscal Year 2025 the Company expects:

total revenues on a percentage basis to be in a range of flat to a decrease in the low-single digits, as compared with the prior year;

Adjusted EBITDA1 to be in a range of $85 million to $95 million; and

Free Cash Flow1 to be in a range of $45 million to $55 million.

Conference Call

The Company will conduct a conference call to discuss the above details and attached financial results today, August 29, 2024, at 8:00 a.m. (ET). The conference call will be webcast from the Investors section of the Company’s website at www.1800flowersinc.com. A recording of the call will be posted on the Investors section of the Company’s website within two hours of the call’s completion. A telephonic replay of the call can be accessed beginning at 2:00 p.m. (ET) today through September 5, 2024, at: (US) 1-877-344-7529; (Canada) 855-669-9658; (International) 1-412-317-0088; enter conference ID #: 5141252.

Definitions of non-GAAP Financial Measures:

We sometimes use financial measures derived from consolidated financial information, but not presented in our financial statements prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). Certain of these are considered “non-GAAP financial measures” under the U.S. Securities and Exchange Commission rules. Non-GAAP financial measures referred to in this document are either labeled as “non-GAAP” or designated as such with a “1”. See below for definitions and the reasons why we use these non-GAAP financial measures. Where applicable, see the Selected Financial Information below for reconciliations of these non-GAAP measures to their most directly comparable GAAP financial measures. Reconciliations for forward-looking figures would require unreasonable efforts at this time because of the uncertainty and variability of the nature and amount of certain components of various necessary GAAP components, including, for example, those related to compensation, tax items, amortization or others that may arise during the year, and the Company’s management believes such reconciliations would imply a degree of precision that would be confusing or misleading to investors. For the same reasons, the Company is unable to address the probable significance of the unavailable information. The lack of such reconciling information should be considered when assessing the impact of such disclosures.

EBITDA and Adjusted EBITDA:

We define EBITDA as net income (loss) before interest, taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA adjusted for the impact of stock-based compensation, Non-Qualified Plan Investment appreciation/depreciation, and for certain items affecting period-to-period comparability. See Selected Financial Information for details on how EBITDA and Adjusted EBITDA were calculated for each period presented. The Company presents EBITDA and Adjusted EBITDA because it considers such information meaningful supplemental measures of its performance and believes such information is frequently used by the investment community in the evaluation of similarly situated companies. The Company uses EBITDA and Adjusted EBITDA as factors to determine the total amount of incentive compensation available to be awarded to executive officers and other employees. The Company’s credit agreement uses EBITDA and Adjusted EBITDA to determine its interest rate and to measure compliance with certain covenants. EBITDA and Adjusted EBITDA are also used by the Company to evaluate and price potential acquisition candidates. EBITDA and Adjusted EBITDA have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. Some of the limitations are: (a) EBITDA and Adjusted EBITDA do not reflect changes in, or cash requirements for, the Company’s working capital needs; (b) EBITDA and Adjusted EBITDA do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on the Company’s debts; and (c) although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future and EBITDA does not reflect any cash requirements for such capital expenditures. EBITDA and Adjusted EBITDA should only be used on a supplemental basis combined with GAAP results when evaluating the Company’s performance.

Segment Contribution Margin and Adjusted Segment Contribution Margin

We define Segment Contribution Margin as earnings before interest, taxes, depreciation, and amortization, before the allocation of corporate overhead expenses. Adjusted Segment Contribution Margin is defined as Segment Contribution Margin adjusted for certain items affecting period-to-period comparability. See Selected Financial Information for details on how Segment Contribution Margin and Adjusted Segment Contribution Margin were calculated for each period presented. When viewed together with our GAAP results, we believe Segment Contribution Margin and Adjusted Segment Contribution Margin provide management and users of the financial statements meaningful information about the performance of our business segments. Segment Contribution Margin and Adjusted Segment Contribution Margin are used in addition to and in conjunction with results presented in accordance with GAAP and should not be relied upon to the exclusion of GAAP financial measures. The material limitation associated with the use of Segment Contribution Margin and Adjusted Segment Contribution Margin is that they are an incomplete measure of profitability as they do not include all operating expenses or non-operating income and expenses. Management compensates for this limitation when using these measures by looking at other GAAP measures, such as Operating Income and Net Income.

Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share:

We define Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share as Net Income (Loss) and Net Income (Loss) Per Common Share adjusted for certain items affecting period-to-period comparability. See Selected Financial Information below for details on how Adjusted Net Income (Loss) Per Common Share and Adjusted or Comparable Net Income (Loss) Per Common Share were calculated for each period presented. We believe that Adjusted Net Income (Loss) and Adjusted or Comparable Net Income (Loss) Per Common Share are meaningful measures because they increase the comparability of period-to-period results. Since these are not measures of performance calculated in accordance with GAAP, they should not be considered in isolation of, or as a substitute for, GAAP Net Income (Loss) and Net Income (Loss) Per Common share, as indicators of operating performance and they may not be comparable to similarly titled measures employed by other companies.

Free Cash Flow:

We define Free Cash Flow as net cash provided by operating activities less capital expenditures. The Company considers Free Cash Flow to be a liquidity measure that provides useful information to management and investors about the amount of cash generated by the business after the purchases of fixed assets, which can then be used to, among other things, invest in the Company’s business, make strategic acquisitions, strengthen the balance sheet, and repurchase stock or retire debt. Free Cash Flow is a liquidity measure that is frequently used by the investment community in the evaluation of similarly situated companies. Since Free Cash Flow is not a measure of performance calculated in accordance with GAAP, it should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. A limitation of the utility of Free Cash Flow as a measure of financial performance is that it does not represent the total increase or decrease in the Company’s cash balance for the period.

About 1-800-FLOWERS.COM, Inc.

1-800-FLOWERS.COM, Inc. is a leading provider of gifts designed to help inspire customers to give more, connect more, and build more and better relationships. The Company’s e-commerce business platform features an all-star family of brands, including: 1-800-Flowers.com®, 1-800-Baskets.com®, Cheryl’s Cookies®, Harry & David®, PersonalizationMall.com®, Shari’s Berries®, FruitBouquets.com®, Things Remembered®, Moose Munch®, The Popcorn Factory®, Wolferman’s Bakery®, Vital Choice®, and Simply Chocolate®. Through the Celebrations Passport® loyalty program, which provides members with free standard shipping and no service charge on eligible products across our portfolio of brands, 1-800-FLOWERS.COM, Inc. strives to deepen relationships with customers. The Company also operates BloomNet®, an international floral and gift industry service provider offering a broad-range of products and services designed to help members grow their businesses profitably; Napco℠, a resource for floral gifts and seasonal décor; DesignPac Gifts, LLC, a manufacturer of gift baskets and towers; and Alice’s Table®, a lifestyle business offering fully digital livestreaming and on demand floral, culinary and other experiences to guests across the country. 1-800-FLOWERS.COM, Inc. was recognized among America’s Most Trustworthy Companies by Newsweek. 1-800-FLOWERS.COM, Inc. was also recognized among the top 5 on the National Retail Federation’s 2021 Hot 25 Retailers list, which ranks the nation’s fastest-growing retail companies, and was named to the Fortune 1000 list in 2022. Shares in 1-800-FLOWERS.COM, Inc. are traded on the NASDAQ Global Select Market, ticker symbol: FLWS. For more information, visit 1800flowersinc.com or follow @1800FLOWERSInc on Twitter.

FLWS–COMP FLWS-FN

Special Note Regarding Forward Looking Statements:

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements represent the Company’s current expectations or beliefs concerning future events and can generally be identified using statements that include words such as “estimate,” “expects,” “project,” “believe,” “anticipate,” “intend,” “plan,” “foresee,” “forecast,” “likely,” “should,” “will,” “target” or similar words or phrases. These forward-looking statements are subject to risks, uncertainties, and other factors, many of which are outside of the Company’s control, which could cause actual results to differ materially from the results expressed or implied in the forward-looking statements, including, but not limited to, statements regarding the Company’s ability to achieve its guidance for the full Fiscal year; the Company’s ability to leverage its operating platform and reduce its operating expense ratio; its ability to successfully integrate acquired businesses and assets; its ability to successfully execute its strategic initiatives; its ability to cost effectively acquire and retain customers; the outcome of contingencies, including legal proceedings in the normal course of business; its ability to compete against existing and new competitors; its ability to manage expenses associated with sales and marketing and necessary general and administrative and technology investments; its ability to reduce promotional activities and achieve more efficient marketing programs; and general consumer sentiment and industry and economic conditions that may affect levels of discretionary customer purchases of the Company’s products. The Company undertakes no obligation to publicly update any of the forward-looking statements, whether because of new information, future events or otherwise, made in this release or in any of its SEC filings. Consequently, you should not consider any such list to be a complete set of all potential risks and uncertainties. For a more detailed description of these and other risk factors, refer to the Company’s SEC filings, including the Company’s Annual Reports on Form 10-K and its Quarterly Reports on Form 10-Q.

Note: The following tables are an integral part of this press release without which the information presented in this press release should be considered incomplete.

Key Points: – US weekly jobless claims decreased slightly, signaling a resilient labor market – The unemployment rate is expected to remain elevated in August – Federal Reserve considers interest rate cuts amid labor market changes

In the ever-changing landscape of the US economy, recent data on jobless claims has caught the attention of investors and policymakers alike. The slight dip in weekly unemployment benefit applications offers a glimmer of hope amidst concerns of a cooling labor market. But what does this mean for your investment strategy?

Decoding the Numbers

The latest report from the Labor Department reveals that initial claims for state unemployment benefits decreased by 2,000 to a seasonally adjusted 231,000 for the week ending August 24. While this drop may seem modest, it’s a positive sign in a market that has been showing signs of strain.

However, it’s crucial to look beyond the headlines. The unemployment rate is expected to remain elevated in August, potentially hovering around 4.2% to 4.3%. This persistence in higher unemployment levels suggests that while the job market isn’t collapsing, it’s not booming either.

The Federal Reserve’s Balancing Act

These labor market dynamics haven’t gone unnoticed by the Federal Reserve. Fed Chair Jerome Powell has hinted at potential interest rate cuts, acknowledging the delicate balance between controlling inflation and supporting employment. For investors, this signals a potential shift in monetary policy that could have far-reaching effects on various asset classes.

Investment Implications

Bond Market Opportunities: With interest rate cuts on the horizon, bond prices could see an uptick. Consider adjusting your fixed-income portfolio to capitalize on this potential trend.

Sector Rotation: As the job market evolves, certain sectors may outperform others. Keep an eye on industries that typically benefit from a resilient job market, such as consumer discretionary and technology.

Long-term Perspective: While short-term fluctuations can be unnerving, remember that the job market’s resilience speaks to the underlying strength of the US economy. This could bode well for long-term equity investments.

The Immigration Wild Card

An interesting subplot in this economic narrative is the role of immigration. Some economists argue that increased jobs filled by undocumented workers may not be fully captured in official data. This “hidden” job growth could be masking even stronger economic fundamentals than the numbers suggest.

Looking Ahead

As we navigate these economic crosscurrents, it’s clear that the job market remains a crucial indicator for investors. While the slight drop in jobless claims is encouraging, it’s part of a larger picture that includes elevated unemployment rates and potential policy shifts.

For the savvy investor, this environment presents both challenges and opportunities. Diversification remains key, but so does staying informed about these labor market trends and their potential ripple effects across the economy.

Remember, in the world of investing, knowledge isn’t just power – it’s profit potential. Stay tuned to these job market indicators, as they may well be the tea leaves that help you read the future of your investment returns.

Key Points: – Trump announces plan to make the US the global crypto leader – Trump Organization rebrands crypto platform to “World Liberty Financial” – Crypto initiative intertwines with Trump’s political campaign and fundraising

In a bold move that blurs the lines between politics, business, and digital finance, former President Donald Trump has announced plans to position the United States as the global leader in cryptocurrency. This declaration comes as the Trump Organization rebrands its crypto platform, signaling a significant shift in the Republican presidential nominee’s stance on digital currencies.

Trump took to X (formerly Twitter) to share his vision with his 90 million followers. In a video message, he declared, “This afternoon, I’m laying out my plan to ensure that the United States will be the crypto capital of the planet.” This announcement marks a dramatic turnaround from his previous skepticism towards cryptocurrencies during his presidency.

The Trump Organization has rebranded its crypto platform from “The DeFiant Ones” to “World Liberty Financial.” This move appears to be a family affair, with Trump’s sons, Donald Jr. and Eric, actively promoting the initiative. Eric Trump announced the launch on X, hinting at “a new era in finance.”

While details about World Liberty Financial remain scarce, Donald Trump Jr. has suggested that the platform aims to rival traditional banking systems, emphasizing decentralized finance as a solution to perceived inequalities in access to financial services.

The timing of this crypto push, coinciding with Trump’s presidential campaign, raises questions about the interplay between his political ambitions and business interests. The campaign has reported raising $25 million in crypto-related donations, though this figure hasn’t been independently verified.

Trump’s embrace of crypto appears to be part of a broader strategy to court the crypto voting bloc and donors. By positioning himself as the pro-crypto candidate, Trump is tapping into a growing demographic of digital currency enthusiasts and investors.

The crypto platform launch follows Trump’s release of a new round of NFT trading cards, further cementing his foray into digital assets. Eric Trump has also hinted at the possibility of digital real estate offerings, potentially involving tokenized real-world assets or digital properties in the metaverse.

For investors, Trump’s crypto push could signal increased mainstream acceptance and potential regulatory changes favorable to the crypto industry. However, it also raises questions about the potential risks and rewards of politically aligned crypto ventures.

As the 2024 presidential race heats up, the intersection of politics and cryptocurrency is likely to become an increasingly important topic. Investors and voters alike will need to navigate this complex landscape carefully, considering both the potential opportunities and the inherent risks of this rapidly evolving sector.

LIMASSOL, Cyprus, Aug. 28, 2024 (GLOBE NEWSWIRE) — GDEV Inc. (NASDAQ: GDEV), an international gaming and entertainment company (“GDEV” or the “Company”), announces that its financial results for the second quarter ended June 30, 2024 will be released at 8:00 a.m. (Eastern Time) on Wednesday, September 4, 2024.

GDEV will host a conference call and webcast to discuss its results at 09:00 a.m. U.S. Eastern Time the same day.

The press release, as well as supplementary slides will be available at gdev.inc. To listen to the audio webcast please follow this link. To participate in the conference call, please use the following details:

US toll-free dial: +1 844-543-0451 US local: +1 864-991-4103 United Kingdom toll-free: +44 808 175 1536 United Kingdom local: +44 1400 220156 Conference ID: 886570

For additional dial-in options, please use this link.

ABOUT GDEV GDEV is a hub of gaming studios, focused on development and growth of its franchise portfolio across various genres and platforms. With a diverse range of subsidiaries including Nexters and Cubic Games among others, GDEV strives to create games that will inspire and engage millions of players for years to come. Its franchises, such as Hero Wars, Island Hoppers, Pixel Gun 3D and others have accumulated hundreds of millions of installs worldwide. For more information, please visit gdev.inc

CONTACTS: Investor Relations Roman Safiyulin | Chief Corporate Development Officer investor@gdev.inc

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS Certain statements in this press release may constitute “forward-looking statements” for purposes of the federal securities laws. Such statements are based on current expectations that are subject to risks and uncertainties. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements.

The forward-looking statements contained in this press release are based on the Company’s current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that the Company has anticipated. Forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Company’s control) or other assumptions. You should carefully consider the risks and uncertainties described in the “Risk Factors” section of the Company’s 2023 Annual Report on Form 20-F, filed by the Company on April 29, 2024, and other documents filed by the Company from time to time with the Securities and Exchange Commission. Should one or more of these risks or uncertainties materialize, or should any of the Company’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and the Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Oral presentation highlighted results from confirmatory Phase 3 RESILIENT study of TNX-102 SL (sublingual cyclobenzaprine HCl) treatment demonstrating statistically significant improvement in primary endpoint of fibromyalgia nociplastic pain and in all six key secondary endpoints, including sleep quality

NDA submission on track for second half 2024; Fast Track designation granted by FDA; FDA decision expected 2025

TNX-102 SL is a potential non-opiod analgesic targeting non-restorative sleep in fibromyalgia: Post hoc analyses highlight strong correlations between improvements in nociplastic pain and sleep quality

Nociplastic pain originates from altered pain perception in the brain and is the type of pain that manifests in fibromyalgia and other chronic overlapping pain conditions (COPCs)

CHATHAM, N.J., Aug. 28, 2024 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP) (Tonix or the Company), a fully-integrated biopharmaceutical company with marketed products and a pipeline of development candidates, presented data in an oral presentation at the 2024 Military Health System Research Symposium (MHSRS), held August 26-29, 2024, in Kissimmee, Fla. A copy of the Company’s presentation, titled “Assuaging Agony: Novel Pain Therapeutics”, is available under the Scientific Presentations tab of the Tonix website at www.tonixpharma.com.

In the Phase 3 RESILIENT study, TNX-102 SL met the pre-specified primary endpoint of significantly reducing daily pain compared to placebo (p-value=0.00005) in participants with fibromyalgia. TNX-102 SL demonstrated broad syndromal benefits with statistically significant improvement in all six pre-specified key secondary endpoints including those related to improving sleep quality, reducing fatigue, and improving patient global ratings and overall fibromyalgia symptoms and function. A post hoc analysis showed strong correlations between improvements in pain and sleep quality at Week 14, supporting the concept that targeting sleep quality has the potential to achieve syndromal improvement in fibromyalgia. TNX-102 SL was well tolerated with an adverse event profile comparable to prior studies and no new safety signals observed.

“Traditional analgesics like NSAIDs or opioids often prove ineffective, if not deleterious, as strategies for treating fibromyalgia,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “In contrast, TNX-102 SL provided broad-spectrum symptom relief in the Phase 3 RESILIENT study and was designed as a bedtime treatment to target non-restorative sleep and improve sleep quality. With the statistically significant results of two positive Phase 3 studies of TNX-102 SL in fibromyalgia we believe TNX-102 SL has the potential to be the first new treatment option for fibromyalgia patients in 15 years.”

Dr. Lederman continued, “Fibromyalgia is the prototypic nociplastic syndrome and chronic overlapping pain condition (COPC)3,4,5. Our results in fibromyalgia suggest potential for TNX-102 SL in treating other COPCs like post-concussive syndrome6, in which sleep disturbances correlate with persistence and severity. In addition, we expect to begin enrolling this quarter in a trial of TNX-102 SL for acute stress disorder/acute stress reaction in the immediate aftermath of motor vehicle collision in the U.S. Department of Defense (DoD)-funded Optimizing Acute Stress Reaction Interventions (OASIS) trial conducted by the University of North Carolina under an investigator-initiated investigational new drug (IND) application.

Tonix remains on track to submit a new drug application (NDA) to the FDA in the second half of 2024 for TNX-102 SL for the management of fibromyalgia. A decision on approval is expected in 2025.

1Moldofsky H, et al. Psychosom Med. 1975;37:341-51

2Moldofsky H, Scarisbrick P. Psychosom Med. 1976;38:35-44

3Fitzcharles MA, et al. Lancet. 2021;397:2098-110

4Clauw DJ. Ann Rheum Dis. Published Online First: 2024

5Kaplan CM, et al. Nat Rev Neurol. 2024;20, 347–363

6Kureshi S et al. Healthcare (Basel) 2024 12(3): 289.

About Fibromyalgia

Fibromyalgia is a chronic pain disorder that is understood to result from amplified sensory and pain signaling within the central nervous system. Fibromyalgia afflicts more than 10 million adults in the U.S., the majority of whom are women. Symptoms of fibromyalgia include chronic widespread pain, non-restorative sleep, fatigue, and brain fog (or cognitive dysfunction). Other associated symptoms include mood disturbances, including anxiety and depression, headaches, and abdominal pain or cramps. Individuals suffering from fibromyalgia struggle with their daily activities, have impaired quality of life, and frequently are disabled. Physicians and patients report common dissatisfaction with currently marketed products. According to the recent report from the U.S. National Academies of Sciences, fibromyalgia is a diagnosable condition that may also occur in the context of Long COVID

About TNX-102 SL

TNX-102 SL is a centrally acting, non-opioid, non-addictive, bedtime investigational drug. The tablet is a patented sublingual formulation of cyclobenzaprine hydrochloride developed for the management of fibromyalgia. In December 2023, the company announced highly statistically significant and clinically meaningful topline results in RESILIENT, the second pivotal Phase 3 clinical trial of TNX-102 SL for the management of fibromyalgia. In the study, TNX-102 SL met its pre-specified primary endpoint, significantly reducing daily pain compared to placebo (p=0.00005) in participants with fibromyalgia. Statistically significant and clinically meaningful results were also seen in all six key secondary endpoints related to improving sleep quality, reducing fatigue and improving overall fibromyalgia symptoms and function. RELIEF, the first statistically significant Phase 3 trial of TNX-102 SL in fibromyalgia, was completed in December 2020. It met its pre-specified primary endpoint of daily pain reduction compared to placebo (p=0.010) and showed activity in key secondary endpoints. In both pivotal studies, the most common treatment-emergent adverse event was tongue or mouth numbness at the administration site, which was temporally related to dosing, self-limited, never rated as severe, and rarely led to study discontinuation (one participant in each study). TNX-102 SL was recently granted Fast Track Designation by the FDA for the management of fibromyalgia and remains on track to submit an NDA to FDA in the second half of 2024.

About Nociplastic Pain

Nociplastic pain is the third category of pain distinct from nociceptive pain and neuropathic pain. Nociplastic pain is characterized by pain arising from altered nociception despite no evidence of actual or threatened tissue damage causing activation of peripheral nociceptors or somatosensory system disease or lesion. Its underlying pathophysiology involves altered pain processing by the central nervous system (CNS). Nociplastic syndromes, officially recognized by the International Association for the Study of Pain (IASP) in 2017, also include several other chronic overlapping pain conditions: myalgic encephalomyelitis/chronic fatigue syndrome, irritable bowel syndrome, temporomandibular disorders, forms of chronic back pain and chronic headache. The pathophysiology of nociplastic pain involves central sensitization (CS), where neurons of the CNS become hyperexcitable, amplifying pain signals. CS can be triggered by peripheral pain stimuli, emotional stress, or other factors, leading to persistent pain despite no peripheral nociceptive input.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a fully-integrated biopharmaceutical company focused on developing, licensing and commercializing therapeutics to treat and prevent human disease and alleviate suffering. Tonix recently announced the U.S. DoD, Defense Threat Reduction Agency (DTRA) awarded it a contract for up to $34 million over five years to develop TNX-4200 small molecule broad-spectrum antiviral agents targeting CD45 for the prevention or treatment of infections to improve the medical readiness of military personnel in biological threat environments. Tonix owns and operates a state-of-the art infectious disease research facility in Frederick, MD. The company also owns a Good Manufacutring Practice (GMP)-capable advanced manufacturing facility in Dartmouth, MA, which was purpose-built to manufacture TNX-801, a potential mpox vaccine, and the GMP suites are ready to be reactivated in case of a national emergency. Tonix’s development portfolio is focused on CNS disorders. Tonix’s priority is to submit an NDA to the FDA in the second half of 2024 for TNX-102 SL, a product candidate for which two statistically significant Phase 3 studies have been completed for the management of fibromyalgia. The FDA has granted Fast Track designation to TNX-102 SL for the management of fibromyalgia. TNX-102 SL is also being developed to treat acute stress reaction. Tonix’s CNS portfolio includes TNX-1300 (cocaine esterase), a biologic designed to treat cocaine intoxication that has Breakthrough Therapy designation, which is enrolling in a potential pivotal Phase 2 trial. Tonix’s immunology development portfolio consists of biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft rejection and for the treatment of autoimmune diseases. Tonix also has product candidates in development in the areas of rare disease and infectious disease. Tonix Medicines, our commercial subsidiary, markets Zembrace® SymTouch® (sumatriptan injection) 3 mg and Tosymra® (sumatriptan nasal spray) 10 mg for the treatment of acute migraine with or without aura in adults.

*Tonix’s product development candidates are investigational new drugs or biologics and have not been approved for any indication.

Zembrace SymTouch and Tosymra are registered trademarks of Tonix Medicines. All other marks are property of their respective owners.

This press release and further information about Tonix can be found at www.tonixpharma.com.

Forward Looking Statements

Certain statements in this press release are forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These statements may be identified by the use of forward-looking words such as “anticipate,” “believe,” “forecast,” “estimate,” “expect,” and “intend,” among others. These forward-looking statements are based on Tonix’s current expectations and actual results could differ materially. There are a number of factors that could cause actual events to differ materially from those indicated by such forward-looking statements. These factors include, but are not limited to, risks related to the failure to obtain FDA clearances or approvals and noncompliance with FDA regulations; risks related to the failure to successfully market any of our products; risks related to the timing and progress of clinical development of our product candidates; our need for additional financing; uncertainties of patent protection and litigation; uncertainties of government or third party payor reimbursement; limited research and development efforts and dependence upon third parties; and substantial competition. As with any pharmaceutical under development, there are significant risks in the development, regulatory approval and commercialization of new products. Tonix does not undertake an obligation to update or revise any forward-looking statement. Investors should read the risk factors set forth in the Annual Report on Form 10-K for the year ended December 31, 2023, as filed with the Securities and Exchange Commission (the “SEC”) on April 1, 2024, and periodic reports filed with the SEC on or after the date thereof. All of Tonix’s forward-looking statements are expressly qualified by all such risk factors and other cautionary statements. The information set forth herein speaks only as of the date thereof.

MALVERN, Pa., Aug. 28, 2024 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies and vaccines, today announced that dosing is complete in the third cohort of its Phase 1/2 GARDian clinical trial for OCU410ST (AAV-hRORA)—a modifier gene therapy candidate being developed for Stargardt disease. Stargardt disease affects approximately 100,000 people in the United States (U.S.) and Europe.

“With all patients dosed in cohort 3 (high dose), Phase 1 of the dose-escalation portion of the trial is complete,” said Dr. Huma Qamar, Chief Medical Officer of Ocugen. “We will continue to advance the trial as efficiently as possible, and work toward fulfilling an unmet medical need for Stargardt patients.”

Three subjects received a single subretinal injection of the highest dose (2.25×1011 vg/mL) being tested. The GARDian clinical trial is being performed at six leading retinal surgery centers across the U.S.

“OCU410ST is a novel modifier gene therapy that has the potential to be a one-time treatment given by subretinal injection in the operating room,” said Charles Wykoff, MD, PhD, Director of Research, Retina Consultants of Texas, lead investigator in the study. “The safety and tolerability profile of OCU410ST remains encouraging as the clinical trial progresses and brings hope to patients with Stargardt disease, who have no FDA-approved treatment options.”

The GARDian clinical trial will assess the safety and efficacy of unilateral subretinal administration of OCU410ST in subjects with Stargardt disease and will be conducted in two phases. Phase 1 is a multicenter, open-label, dose-ranging study consisting of three dose levels [low dose (3.75×1010 vg/mL), medium dose (7.5×1010 vg/mL), and high dose (2.25×1011 vg/mL)].

Ocugen remains committed to advancing treatments for blindness, focusing on innovative gene therapy solutions that aim to provide lasting benefits to patients.

The Company will continue to provide clinical updates on a periodic basis.