The U.S. oil industry is facing a sharp slowdown, with layoffs and spending cuts rippling across the sector as lower crude prices and industry consolidation squeeze margins. The wave of belt-tightening could mark the end of the rapid production growth that helped the United States overtake other producers to become the world’s top oil supplier in recent years.

International crude prices have fallen roughly 12% this year, dragged lower in part by rising output from OPEC and its allies, who have been steadily ramping up supply to reclaim market share lost to U.S. shale producers. Prices are now hovering just above $62 a barrel, uncomfortably close to breakeven levels for many U.S. operators. For companies already grappling with higher costs and trade-related tariffs, the weaker pricing environment is forcing tough decisions.

ConocoPhillips, the nation’s third-largest oil producer, recently announced plans to cut up to a quarter of its workforce. The move follows Chevron’s decision earlier this year to trim about 20% of its staff, amounting to roughly 8,000 jobs. Oilfield service providers such as SLB and Halliburton have also been cutting jobs, underscoring how the slowdown is spreading beyond producers to the broader energy ecosystem.

The cuts aren’t limited to people. According to a Reuters review of second-quarter results, 22 publicly traded U.S. producers—including ConocoPhillips, Diamondback Energy, and Occidental Petroleum—have reduced their combined capital spending by about $2 billion. Industry insiders say those pullbacks, along with falling rig counts, are early warning signs that production growth is set to level off. Baker Hughes data shows that the U.S. oil rig count has dropped by nearly 70 so far this year, down to just over 400.

In the Permian Basin, the heart of America’s shale boom, the tone has shifted from aggressive expansion to cautious retrenchment. “We’ve gone from ‘drill, baby, drill’ to ‘wait, baby, wait,’” said one Texas producer, pointing out that prices need to stabilize closer to $70–$75 a barrel before rig activity rebounds. Without that, analysts warn that U.S. output will plateau and could even begin to decline, with OPEC quickly stepping in to fill the gap.

Research firms are already forecasting slower momentum. Energy Aspects expects U.S. onshore production to drop by 300,000 barrels per day in 2025, while Wood Mackenzie projects only modest growth of 200,000 barrels per day—far below the record-setting pace of recent years.

Adding to the pressure are rising costs, much of it tied to tariffs on steel and other inputs. Diamondback Energy expects the price of steel casing for wells to climb by nearly 25% this year, inflating breakeven costs across the industry. For ConocoPhillips, controllable costs have already risen by $2 per barrel since 2021, making profitability harder to sustain.

The impact on employment is significant. Texas labor data shows U.S. oil and gas production jobs fell by nearly 5,000 in the first half of 2025, while energy services jobs have dropped by about 23,000 since January. Even with gains in drilling efficiency, industry analysts caution that technology alone won’t be enough to offset the slowdown.

For now, the U.S. oil industry remains a global leader. But with lower prices, higher costs, and fewer rigs in action, the sector’s once-rapid growth story appears to be entering a more uncertain chapter.

CALGARY, AB, September 2, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company”) is pleased to confirm that its Board of Directors has declared a monthly cash dividend of $0.09 per common share payable on September 30, 2025, to shareholders of record at the close of business on September 15, 2025. The monthly cash dividend is expected to be designated as an “eligible dividend” for Canadian federal and provincial income tax purposes.

About InPlay Oil Corp.

InPlay is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Darren Dittmer, Chief Financial Officer, InPlay Oil Corp., Telephone: (587) 955-0634

Oil prices advanced on Thursday, August 28, 2025, as geopolitical tensions once again overshadowed fundamentals in the energy market. West Texas Intermediate (WTI) crude rose 0.7% to above $64 per barrel, while Brent crude gained 0.4%. The move reversed earlier declines and reflected renewed concerns about Russian supply disruptions.

The rebound followed comments from German Chancellor Friedrich Merz, who said that a potential meeting between Ukrainian President Volodymyr Zelenskiy and Russian President Vladimir Putin would not take place. Markets had viewed such talks as a possible first step toward easing restrictions on Russian crude exports. With negotiations shelved, traders adjusted expectations for any near-term increase in Moscow’s oil shipments.

Attention also turned to Washington, where President Donald Trump is preparing a statement on Russia and Ukraine. Investors are weighing the possibility that new sanctions could target Moscow’s energy exports more aggressively, raising the risk of further supply constraints.

Meanwhile, Ukraine has escalated military pressure on Russia’s oil sector, ramping up drone strikes against key infrastructure. Over the past month, two refineries were targeted, and tanker-tracking data compiled by Bloomberg showed Russian crude exports slipping last week. These developments highlight the vulnerability of Russia’s energy flows, which remain a critical part of the global supply chain despite sanctions already in place.

The U.S. administration has also taken steps to discourage purchases of Russian crude abroad. White House trade adviser Peter Navarro recently urged India to halt imports, following Washington’s decision to double tariffs on Russian oil shipments to 50%. Any reduction in Indian demand could force Moscow to discount barrels more deeply or find alternative buyers, further complicating the supply picture.

Despite short-term concerns about Russian output, broader fundamentals continue to point toward a weaker market in the months ahead. Analysts expect crude balances to shift into surplus by the end of 2025, as production increases from the OPEC+ alliance and non-OPEC producers outweigh global demand growth.

OPEC+ is scheduled to meet on September 7, though officials have not indicated any immediate plans to cut or adjust production targets. With supply growth already underway, the group faces a delicate balancing act between maintaining market share and stabilizing prices.

Adding to subdued activity, U.S. markets are entering a quiet period ahead of the Labor Day holiday. Thin liquidity has amplified volatility, with relatively small shifts in sentiment causing outsized price moves. Traders appear cautious about taking on new risk until there is clarity from both geopolitical developments and OPEC’s next steps.

For investors, the current environment offers a mixed picture. On one hand, geopolitical risks related to Russia and Ukraine may support periodic rallies in crude prices. On the other, rising global output and surplus forecasts suggest a ceiling on sustained gains.

Small- and mid-cap energy producers with efficient cost structures may remain more resilient if prices soften later in the year, while refiners could benefit from volatile spreads driven by supply disruptions. Commodity-focused investors may find opportunities in short-term volatility, but longer-term positioning will likely depend on how OPEC+ manages supply and whether sanctions meaningfully reduce Russian exports.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

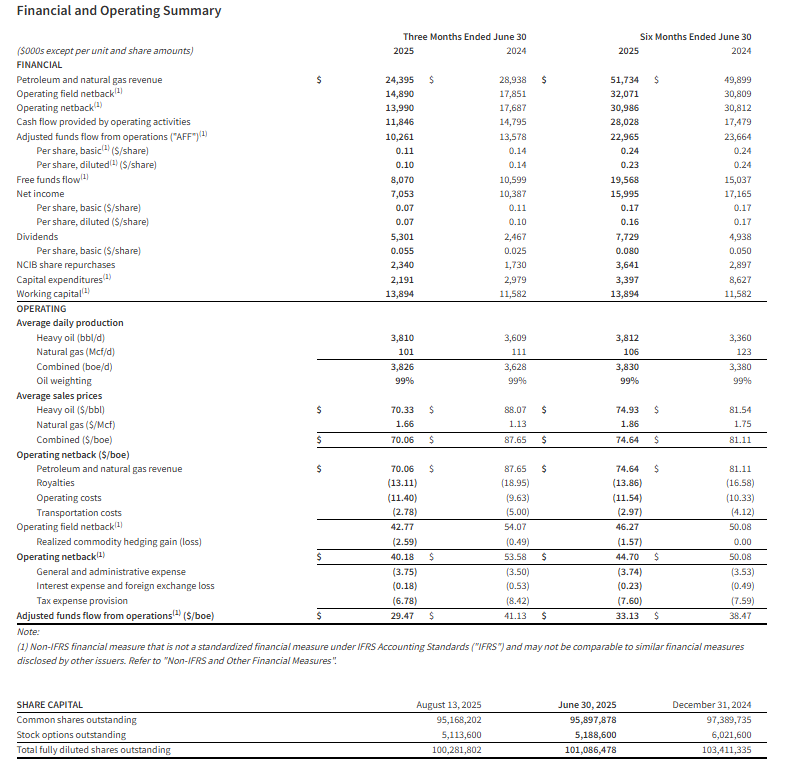

Second quarter financial results. Hemisphere reported oil and gas revenue of C$24.4 million in the second quarter, down 15.7% from the prior year period but ahead of our estimate of C$20.9 million. Net income was C$7.1 million, or C$0.07 per share, compared to C$10.4 million, or C$0.10 per share, last year, and above our forecast of C$5.8 million, or C$0.06 per share. Average daily production rose to 3,826 boe/d, up from 3,628 in Q2 2024 and modestly ahead of our estimate of 3,800 boe/d. The company realized an average sales price of C$70.06/boe, compared to C$87.65/boe in the prior year quarter. Adjusted funds flow totaled C$10.3 million, or C$0.10 per diluted share, versus C$13.6 million, or C$0.14 per diluted share, a year ago. This result exceeded our estimate of C$8.9 million, or C$0.09 per diluted share.

Updating estimates. Given the stronger-than-expected second quarter, we are raising our 2025 revenue forecast to C$97.7 million from C$95.0 million. Our operating expense assumption has been modestly increased to C$38.8 million from C$38.4 million. We now project net income of C$29.6 million, or C$0.30 per share, up from our prior forecast of C$28.7 million, or C$0.28 per share. Adjusted funds flow is expected to reach C$43.3 million, compared to our earlier estimate of C$42.2 million. For 2026, we forecast revenue of C$93.7 million, net income of C$27.5 million, or C$0.28 per share, and AFF of C$39.6 million, reflecting our expectation of a softer commodity price environment relative to 2025.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Aug. 13, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces its financial and operating results for the three and six months ended June 30, 2025 which is our first quarter following the April 7, 2025 closing date of the strategic acquisition of Cardium focused light oil assets in the Pembina area of Alberta (the “Acquisition“). InPlay’s condensed unaudited interim financial statements and notes, as well as its Management’s Discussion and Analysis (“MD&A”) for the three and six months ended June 30, 2025 will be available at “www.sedarplus.ca” and on our website at “www.inplayoil.com“. An updated corporate presentation is available on our website.

We are excited about InPlay’s future following the highly accretive acquisition completed in the second quarter. This transformative transaction has significantly enhanced the Company’s scale, market capitalization, and long-term sustainability. With a longer reserve life and an expanded inventory of high quality drilling locations, the combined Company is well positioned to generate strong free adjusted funds flow (“FAFF”)(3) for many years to come.

InPlay is off to a very strong start with second quarter production exceeding expectations by approximately 1,000 boe/d. This outperformance was driven by base production performing above expectations and seven (7.0 net) wells brought onstream in March significantly outperforming our type curves by ~135% on average based on the first 120 days of initial production (“IP”). Notably, three wells brought onstream in March ranked among the top ten Cardium producers in April with two of them holding the number one and two spots in April and May, and ranking second and third in June. These wells achieved payout in under 90 days in a US$60 WTI pricing environment. As a result of this outperformance, current production based on field estimates remains at 19,400 boe/d even though no new wells have been brought on since March. We now expect 2025 average production to be at the upper end of our guidance range. In addition, strong capital efficiencies are expected to result in capital spending landing in the lower half of our previously announced capital budget of $53 – $60 million. The Company continues to prioritize free cash flow generation to be used for debt reduction and the continued return of capital to shareholders through our monthly dividend.

Another exciting development is the recent announcement that Delek Group Ltd. (“Delek”) has become a 32.7% strategically aligned shareholder of InPlay. Delek brings a proven track record of value creation in the energy sector. They hold a 45% working interest in the largest natural gas field in the Mediterranean, with an estimated 23 TCF of recoverable natural gas. Additionally, Delek has been instrumental in the growth of Ithaca Energy plc, where they hold a 52% equity stake and have overseen production growth from 30,000 boe/d to over 120,000 boe/d since 2019.

For the remainder of 2025, InPlay plans to drill 5.0 – 5.5 net Cardium wells in Pembina. InPlay’s second half drilling campaign recently commenced in August, with the spudding of a three well pad which are in close proximity to the Company’s top producing Cardium wells and are expected to be on production near the beginning of October. The application of InPlay’s drilling and completion techniques to the acquired assets is expected to drive continued strong performance from new wells with additional capital directed to facility upgrades, optimization and required infrastructure projects.

InPlay will continue to be disciplined and timely in capital spending in the current commodity price environment, maintaining a focus on strong FAFF, debt reduction, per share growth and continuation of our return to shareholder strategy. To further enhance stability and mitigate risk, the Company has secured commodity hedges extending through 2025 and into 2026. InPlay has hedged over 70% of natural gas production and approximately 60% of light crude oil production for the second half of 2025.

Second Quarter 2025 Highlights

Successfully closed the strategic acquisition of Cardium focused light oil assets at highly accretive metrics, enhancing FAFF by 65% on a per share basis, expanding our drilling inventory to over 400 locations, lowering our corporate base decline rate to 24% and strengthening dividend sustainability (2025 forecasted FAFF equal to 2.5 times base dividend).

Achieved average quarterly production of 20,401 boe/d(1) (62% light crude oil and NGLs), a 125% increase from Q1 2025, including a 13% increase to light crude oil and liquids weighting to 62% from 55% and a 35% increase in light oil weighting to 51% from 38% in the first quarter of 2025 with oil being the main driver behind our netbacks.

Generated strong quarterly Adjusted Funds Flow (“AFF”)(2) of $40.1 million ($1.49 per basic share(3)).

Achieved significant FAFF of $35.5 million ($1.32 per basic share(3)) allowing the Company to reduce net debt by approximately $26 million, more than originally forecasted, resulting in a quarterly annualized net debt to earnings before interest, taxes and depreciation (“EBITDA”)(3) ratio of 1.2 times.

Realized operating income of $50.5 million(3), an increase of 140% compared to Q1 2025 leading to a strong operating income profit margin(3) of 55%, up from 54% in Q1 2025.

Improved field operating netbacks(3) to $27.20/boe, a 6% increase compared to Q1 2025 despite an 11% decrease to WTI pricing (13% decrease to realized crude oil pricing) and a 22% decrease in AECO natural gas pricing compared to Q1 2025.

Returned $7.9 million to shareholders via monthly dividends, representing a 10% yield relative to the current share price. Since November 2022, InPlay has distributed $52 million in dividends (including dividends declared to date in the third quarter).

Second Quarter 2025 Financial & Operations Overview:

InPlay’s second quarter results exceeded expectations and marked the first reporting period incorporating the recently acquired assets, with pro forma operations effective April 8, 2025. Due to the outstanding efforts of our team and InPlay’s strong knowledge and focus in the area, the acquired assets were seamlessly integrated with no disruption to the Company’s ongoing operations.

Quarterly production averaged 20,401 boe/d(1) (62% light crude oil and NGLs) which was approximately 1,000 boe/d above internal forecasts. Base production exceeded expectations, and the seven (7.0 net) wells drilled on the combined assets in the first quarter significantly outperformed internal forecasts by approximately 135% (based on IP 120) as highlighted in the table below.

02-25 Pad (per well average)

14-33 Pad (per well average)

08-01 Pad (per well average)

boe/d

Oil and NGLs %

boe/d

Oil and NGLs %

boe/d

Oil and NGLs %

IP 30

887

88 %

680

75 %

265

89 %

IP 60

937

87 %

493

66 %

290

87 %

IP 90

922

85 %

569

63 %

288

86 %

IP 120

892

85 %

430

60 %

285

83 %

IP 150

N/A

N/A

487

58 %

275

82 %

Current

791

82 %

299

44 %

217

77 %

>300% above type curve

>75% above type curve

>25% above type curve

InPlay generated AFF of $40.1 million ($1.49 per basic share) a 138% increase from the first quarter of 2025. Limited capital spending in the second quarter of $4.6 million, resulted in $35.5 million of FAFF ($1.32 per basic share), highlighting the strong FAFF generation of the combined Company. These strong results were achieved despite an 11% decrease to WTI pricing (13% decrease to realized crude oil pricing) and a 22% decrease in AECO natural gas pricing compared to Q1 2025. The Company paid $7.9 million ($12.0 million in the first half of 2025) in dividends during the quarter.

During the quarter InPlay generated a net loss of $3.2 million. After excluding one-time transaction costs and the impact of unrealized mark-to-market hedging gains/losses, InPlay generated adjusted net income(3) of $2.0 million ($0.08 per basic share) in the quarter.

Strong results had net debt levels at the end of the quarter at $223 million, $5 million lower than originally anticipated. The quarterly annualized net debt to EBITDA ratio for the second quarter of 1.2x is evidence that our post-Acquisition accelerated debt reduction goals are well on track.

Operating synergies and stronger production allowed InPlay to maintain operating costs per boe in the second quarter in line with pre-acquisition levels and synergies have started to show a reduction in G&A cost per boe.

On behalf of the entire InPlay team and our Board of Directors, we thank our shareholders for their ongoing support as we execute our strategy of disciplined growth, reliable returns, and long-term value creation. We would like to send a special thanks to our employees for their significant effort in enabling a smooth integration of the new assets. We are very optimistic about building on the momentum from our strategic Acquisition that has transformed the future of the Company.

Notes:

1.

See “Production Breakdown by Product Type” at the end of this press release.

2.

Capital management measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

3.

Non-GAAP financial measure or ratio that does not have a standardized meaning under International Financial Reporting Standards (IFRS) and GAAP and therefore may not be comparable with the calculations of similar measures for other companies. Please refer to “Non-GAAP and Other Financial Measures” contained within this press release and in our most recently filed MD&A.

4.

Supplementary measure. See “Non-GAAP and Other Financial Measures” contained within this press release.

5.

Common share and per common share amounts have been updated to reflect the six for one (6:1) common share consolidation effective April 14, 2025.

For further information please contact:

Doug Bartole President and Chief Executive Officer InPlay Oil Corp. Telephone: (587) 955-0632

Vancouver, British Columbia–(Newsfile Corp. – August 14, 2025) – Hemisphere Energy Corporation (TSXV: HME) (OTCQX: HMENF) (“Hemisphere” or the “Company”) provides its financial and operating results for the second quarter ended June 30, 2025, declares a quarterly dividend payment to shareholders, and provides operations update.

Q2 2025 Highlights

Attained quarterly production of 3,826 boe/d (99% heavy oil).

Generated $24.4 million, or $70.06/boe, in revenue.

Achieved total operating and transportation costs of $14.18/boe.

Delivered an operating field netback1 of $14.9 million, or $42.77/boe.

Realized quarterly adjusted funds flow from operations (“AFF”)1 of $10.3 million, or $29.47/boe.

Executed a $2.2 million capital expenditure1 program, including preparatory spending for Hemisphere’s upcoming drilling program.

Generated free funds flow1 of $8.1 million, or $0.07/share.

Distributed $2.4 million, or $0.025/share, in base dividends to shareholders during the quarter.

Distributed $2.9 million, or $0.03/share, in special dividends to shareholders during the quarter.

Purchased and cancelled 1.3 million shares for $2.3 million under the Company’s Normal Course Issuer Bid (“NCIB”).

Renewed the Company’s $35 million two-year extendible credit facility.

Exited the first quarter with positive working capital1 of $13.9 million.

(1) Operating field netback, adjusted funds flow from operations (AFF), free funds flow, capital expenditure, and working capital are non-IFRS measures, or when expressed on a per share or boe basis, non-IFRS ratio, that do not have any standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other entities. Non-IFRS financial measures and ratios are not standardized financial measures under IFRS and may not be comparable to similar financial measures disclosed by other issuers. Refer to the section “Non-IFRS and Other Specified Financial Measures”.

Selected financial and operational highlights should be read in conjunction with Hemisphere’s unaudited condensed interim consolidated financial statements and related notes, and the Management’s Discussion and Analysis for the three months ended June 30, 2025 which are available on SEDAR+ at www.sedarplus.ca and on Hemisphere’s website at www.hemisphereenergy.ca. All amounts are expressed in Canadian dollars unless otherwise noted.

Quarterly Dividend

Hemisphere is pleased to announce that its Board of Directors has approved a quarterly base cash dividend of $0.025 per common share in accordance with the Company’s dividend policy. The dividend will be paid on September 12, 2025 to shareholders of record as of the close of business on August 29, 2025. The dividend is designated as an eligible dividend for income tax purposes.

Operations Update

With significant volatility in the economy and oil markets earlier this year, Hemisphere elected to defer the majority of its capital spending into the latter third of the year. With relatively flat base production, the Company has focused on balance sheet strength and shareholder returns through its share buyback program, base quarterly dividends, and the announcements of two special dividends year-to-date.

The Company’s drilling program is now scheduled to commence late in the third quarter. It will include several development wells in Atlee Buffalo in addition to at least one new well in Marsden, which will test a second oil-bearing zone on Hemisphere’s lands adjacent to its oil treating facilities and active polymer pilot project.

Management will continue to closely monitor oil market volatility and adjust capital spending accordingly. With almost $14 million in working capital, an undrawn credit line, and stable cash flow from its production base, Hemisphere is in a unique position to act on potential acquisition opportunities and continued shareholder returns in addition to executing its drilling program.

EnerCom Denver Conference

Ms. Ashley Ramsden-Wood, Chief Development Officer of Hemisphere, will be presenting at the EnerCom Denver Conference on Tuesday, August 19 at 2:45 pm Mountain Daylight Time (1:45 pm Pacific Daylight Time). The presentation will be livestreamed on EnerCom’s website at www.enercomdenver.com/webcast (Confluence C) and archived on Hemisphere’s website at www.hemisphereenergy.ca.

About Hemisphere Energy Corporation

Hemisphere is a dividend-paying Canadian oil company focused on maximizing value-per-share growth with the sustainable development of its high netback, ultra-low decline conventional heavy oil assets through polymer flood enhanced oil recovery methods. Hemisphere trades on the TSX Venture Exchange as a Tier 1 issuer under the symbol “HME” and on the OTCQX Venture Marketplace under the symbol “HMENF”.

For further information, please visit the Company’s website at www.hemisphereenergy.ca to view its corporate presentation or contact:

Don Simmons, President & Chief Executive Officer Telephone: (604) 685-9255 Email: info@hemisphereenergy.ca

Certain statements included in this news release constitute forward-looking statements or forward-looking information (collectively, “forward-looking statements”) within the meaning of applicable securities legislation. Forward-looking statements are typically identified by words such as “anticipate”, “continue”, “estimate”, “expect”, “forecast”, “may”, “will”, “project”, “could”, “plan”, “intend”, “should”, “believe”, “outlook”, “potential”, “target” and similar words suggesting future events or future performance. In particular, but without limiting the generality of the foregoing, this news release includes forward-looking statements including that Hemisphere’s drilling program is now scheduled to commence late in the third quarter and will include several development wells in Atlee Buffalo in addition to at least one new well in Marsden, which will test a second oil-bearing zone on Hemisphere’s lands; that Hemisphere may adjust capital spending depending on oil market volatility; that Hemisphere is in a unique position to act on potential acquisition opportunities and continued shareholder returns; and that a dividend will be paid September 12, 2025 to shareholders of record as of the close of business on August 29, 2025.

Forward‐looking statements are based on a number of material factors, expectations or assumptions of Hemisphere which have been used to develop such statements and information but which may prove to be incorrect. Although Hemisphere believes that the expectations reflected in such forward‐looking statements or information are reasonable, undue reliance should not be placed on forward‐looking statements because Hemisphere can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified herein, assumptions have been made regarding, among other things: the current and go-forward oil price environment; that Hemisphere will continue to conduct its operations in a manner consistent with past operations; that results from drilling and development activities are consistent with past operations; the quality of the reservoirs in which Hemisphere operates and continued performance from existing wells; the continued and timely development of infrastructure in areas of new production; the accuracy of the estimates of Hemisphere’s reserve volumes; certain commodity price and other cost assumptions; continued availability of debt and equity financing and cash flow to fund Hemisphere’s current and future plans and expenditures; the impact of increasing competition; the general stability of the economic and political environment in which Hemisphere operates; the general continuance of current industry conditions; the timely receipt of any required regulatory approvals; the ability of Hemisphere to obtain qualified staff, equipment and services in a timely and cost efficient manner; drilling results; the ability of the operator of the projects in which Hemisphere has an interest in to operate the field in a safe, efficient and effective manner; the ability of Hemisphere to obtain financing on acceptable terms; field production rates and decline rates; the ability to replace and expand oil and natural gas reserves through acquisition, development and exploration; the timing and cost of pipeline, storage and facility construction and expansion and the ability of Hemisphere to secure adequate product transportation; future commodity prices; currency, exchange and interest rates; regulatory framework regarding royalties, taxes and environmental matters in the jurisdictions in which Hemisphere operates; and the ability of Hemisphere to successfully market its oil and natural gas products.

The forward‐looking statements included in this news release are not guarantees of future performance and should not be unduly relied upon. Such information and statements, including the assumptions made in respect thereof, involve known and unknown risks, uncertainties and other factors that may cause actual results or events to defer materially from those anticipated in such forward‐looking statements including, without limitation: changes in commodity prices; changes in the demand for or supply of Hemisphere’s products, the early stage of development of some of the evaluated areas and zones; unanticipated operating results or production declines; changes in tax or environmental laws, royalty rates or other regulatory matters; changes in development plans of Hemisphere or by third party operators of Hemisphere’s properties, increased debt levels or debt service requirements; inaccurate estimation of Hemisphere’s oil and gas reserve volumes; limited, unfavourable or a lack of access to capital markets; increased costs; a lack of adequate insurance coverage; the impact of competitors; and certain other risks detailed from time‐to‐time in Hemisphere’s public disclosure documents, (including, without limitation, those risks identified in this news release and in Hemisphere’s Annual Information Form).

The forward‐looking statements contained in this news release speak only as of the date of this news release, and Hemisphere does not assume any obligation to publicly update or revise any of the included forward‐looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities laws.

CALGARY, AB, Aug. 7, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces that Delek Group Ltd. (“Delek“) has closed the previously announced acquisition of all 9,139,784 common shares in the capital of InPlay previously held by Obsidian Energy Ltd. (“Obsidian“) (the “Transaction“). Further details regarding the Transaction can be found in InPlay’s press release dated August 4, 2025.

In connection with closing of the Transaction, InPlay has appointed Ehud (Udi) Erez and Tamir Polikar to the Board of Directors of InPlay (the “Board“). Mr. Erez has served as the Chairman of the board of Delek since 2020 and has over 30 years of experience in the energy and real estate sectors. Mr. Polikar has served as the Chief Financial Officer of Delek since 2020 and has over 30 years of experience in the energy and real estate sectors.

InPlay also announces that with in connection with closing of the Transaction, Stephen Loukas and Peter Scott have stepped down from the Board. InPlay management and Board would like to thank Mr. Loukas and Mr. Scott for their contribution to InPlay’s Board and wish them, and Obsidian, continued success.

About InPlay Oil Corp.

InPlay Oil Corp. is a growth-oriented, sustainable oil and gas producer focused on long-term value creation for its shareholders. The Company’s operations are centered in the Western Canadian Sedimentary Basin, where InPlay holds a diverse portfolio of oil and natural gas assets. InPlay is committed to delivering strong per-share growth, maintaining a disciplined approach to capital investment, and providing consistent returns to shareholders.

About Delek Group

Delek is an independent E&P and the pioneering visionary behind the development of the East Med. With major finds in the Levant Basin, including Leviathan (21.4 TCF) and Tamar (11.2 TCF no longer owned by Delek) and others, Delek is leading the region’s development into a major natural gas export hub. In addition, Delek has significant presence s in the North Sea, with its subsidiary, Ithaca Energy (LSE: ITH). Delek is one of Israel’s largest and most prominent companies with a consistent track record of growth. Its shares are traded on the Tel Aviv Stock Exchange (TASE: DLEKG) and are part of the TA 35 Index.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President, Business & Corporate Development, InPlay Oil Corp., Telephone: (587) 893-6804

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Delek Group to acquire major stake in InPlay. Delek Group Ltd. (TASE: DLEKG) executed a definitive agreement to acquire Obsidian Energy’s (TSX: OBE, NYSE American: OBE) common share position in InPlay Oil, consisting of 9,139,784 common shares representing approximately 32.7% of InPlay’s issued and outstanding shares. Subject to certain adjustments, the purchase price is C$10.00 per InPlay share, representing an aggregate transaction value of C$91,397,840. Recall that Obsidian received the shares as partial consideration for its April sale of Pembina Cardium assets to InPlay Oil. The transaction with Delek is expected to close in the first half of August 2025 and remains subject to satisfaction or waiver of certain closing conditions.

Rationale. Delek is an independent exploration and production company based in Israel that has embarked on an international expansion with a focus on high-potential opportunities in the North Sea and North America. Delek views Canada as a strong and stable jurisdiction for oil and gas investment and identified InPlay as an attractive partner in the Canadian energy sector due to its strong record of operational performance and successful acquisitions. Delek holds a 52% equity interest in Ithaca Energy plc and has played a key role in supporting Ithaca’s production growth since the time of its initial investment.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CALGARY, AB, Aug. 3, 2025 /CNW/ – InPlay Oil Corp. (TSX: IPO) (OTCQX: IPOOF) (“InPlay” or the “Company“) announces that Obsidian Energy Ltd. (“Obsidian“) has entered into a definitive agreement with Delek Group Ltd. (“Delek“) in respect of the sale of all 9,139,784 common shares (“Common Shares“) in the capital of InPlay currently held by Obsidian (the “Transaction“).

“We are thrilled to welcome the Delek Group to our organization as part of their impressive oil and gas portfolio,” said Doug Bartole, President and CEO of InPlay Oil Corp. “Delek holds a 45% working interest in the largest natural gas field in the Mediterranean, with an estimated 23 TCF of recoverable natural gas. They have also played a key role in the growth of Ithaca Energy plc, where they hold a 52% equity stake, increasing production from 30,000 boe/d to over 120,000 boe/d since their initial investment. We look forward to partnering with Delek to continue building InPlay into a long-term, sustainable, growth-oriented Canadian oil and gas producer, with a strong focus on per-share growth and consistent returns to shareholders.”

“Delek is excited to partner with InPlay as our investment in the Canadian energy sector,” said Ehud (Udi) Erez, Chairman of the Board of the Delek Group. “We identified Canada as a strong and stable jurisdiction for our oil and gas investment, and InPlay stood out with its dynamic team and deep expertise in the Canadian market. InPlay has built a formidable track record through strong operational performance and strategic, accretive acquisitions. We look forward to seeing InPlay’s continued growth and continued success.”

The Transaction is expected to occur in the first half of August 2025 and remains subject to customary conditions to closing.

In connection with the Transaction, InPlay has entered into a registration rights agreement with Delek (the “Registration Rights Agreement“) and an investor rights agreement (the “Investor Rights Agreement“) substantially in the forms entered into between InPlay and Obsidian. The Registration Rights Agreement and Investor Rights Agreement are conditional upon closing of the Transaction.

The Investor Rights Agreement provides that, conditional upon closing of the Transaction, InPlay will appoint two nominees of Delek to the Board of Directors of InPlay (the “Board“) immediately following closing of the Transaction. For so long as Delek holds 20% or more of the issued and outstanding Common Shares and the Board is comprised of eight (8) members, Delek will be entitled to maintain two (2) board nominees. Delek has agreed that, subject to certain conditions, in respect of the election of directors and the appointment of the auditor’s at InPlay’s annual general meeting to be held in 2026 and the appointment of the auditor’s at InPlay’s annual general meeting to be held in 2027, Delek will vote (or, at Delek’s discretion, abstain or cause to be abstained from voting) all Common Shares held by it in accordance with the recommendations of the Board or management of InPlay. Additionally, the Investor Rights Agreement provides Delek with certain pre-emptive and participation rights with respect to certain equity offerings undertaken by InPlay.

The Registration Rights Agreement and the Investor Rights Agreement will be filed on InPlay’s SEDAR+ profile at www.sedarplus.com in due course.

About InPlay Oil Corp.

InPlay is a growth-oriented, sustainable oil and gas producer focused on long-term value creation for its shareholders. The Company’s operations are centered in the Western Canadian Sedimentary Basin, where InPlay holds a diverse portfolio of oil and natural gas assets. InPlay is committed to delivering strong per-share growth, maintaining a disciplined approach to capital investment, and providing consistent returns to shareholders.

About Delek Group

Delek is an independent E&P and the pioneering visionary behind the development of the East Med. With major finds in the Levant Basin, including Leviathan (21.4 TCF) and Tamar (11.2 TCF no longer owned by Delek) and others, Delek is leading the region’s development into a major natural gas export hub. In addition, Delek has invested in the North Sea, with its subsidiary, Ithaca Energy. Delek is one of Israel’s largest and most prominent companies with a consistent track record of growth. Its shares are traded on the Tel Aviv Stock Exchange (TASE:DLEKG) and are part of the TA 35 Index.

SOURCE InPlay Oil Corp.

For further information please contact: Doug Bartole, President and Chief Executive Officer, InPlay Oil Corp., Telephone: (587) 955-0632; Kevin Leonard, Vice President, Business & Corporate Development, InPlay Oil Corp., Telephone: (587) 893-6804

Graham Corporation designs, manufactures and sells critical equipment for the energy, defense and chemical/petrochemical industries. The Company designs and manufactures custom-engineered ejectors, vacuum pumping systems, surface condensers and vacuum systems. It is a nuclear code accredited fabrication and specialty machining company. It supplies components used inside reactor vessels and outside containment vessels of nuclear power facilities. Its equipment is found in applications, such as metal refining, pulp and paper processing, water heating, refrigeration, desalination, food processing, pharmaceutical, heating, ventilating and air conditioning. For the defense industry, its equipment is used in nuclear propulsion power systems for the United States Navy. The Company’s products are used in a range of industrial process applications in energy markets, including petroleum refining, defense, chemical and petrochemical processing, power generation/alternative energy and other.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Follow-on Order. Yesterday, Graham Corporation announced the Company was awarded a follow-on order to produce critical hardware for the MK48 Mod 7 Heavyweight torpedo program. This was a sole sourced award. Graham typically receives an annual order for this program once funding is approved for the current year’s supply.

MK48 Program. The follow-on order is valued at approximately $25.5 million. Graham manufactures and tests the alternators and regulators for the MK48 Mod 7 Heavyweight torpedo through its Barber-Nichols subsidiary. We believe there are two more option years remaining under the current program in which 50-120 MK 48s are produced annually.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lithium-metal anodes. Century Lithium announced that Alpha-En Corporation successfully converted Century’s lithium carbonate into battery-grade lithium-metal anodes for use in lithium-ion batteries. The lithium-metal anodes were produced using 99.8% pure lithium carbonate from Century’s Angel Island project and demonstration plant. The sample was converted by Alpha-En into lithium metal using Alpha-En’s patented conversion process.

LFP 18650 battery cells. Earlier in the month, Century announced that First Phosphate Corp. produced commercial-grade lithium iron phosphate (LFP) 18650 battery cells using North American critical minerals, including lithium carbonate sourced from Century’s Angel Island project and demonstration plant, along with high-purity phosphoric acid and iron powder from First Phosphate’s Begin-Lamarche property in Quebec. The LFP 18650 battery cells were assembled for First Phosphate by Ultion Technologies at their pilot facility in Nevada.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

InPlay Oil is a junior oil and gas exploration and production company with operations in Alberta focused on light oil production. The company operates long-lived, low-decline properties with drilling development and enhanced oil recovery potential as well as undeveloped lands with exploration possibilities. The common shares of InPlay trade on the Toronto Stock Exchange under the symbol IPO and the OTCQX Exchange under the symbol IPOOF.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Hans Baldau, Associate Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Company strategy. Despite the recent improvement in oil prices, InPlay is maintaining its 2025 production guidance at 16,000 to 16,800 boe/d. Management reiterated that the strategy remains centered on capital discipline, prioritizing debt reduction over production growth. The company’s approach is supported by fluctuating oil prices and the performance of assets acquired from Obsidian Energy, which have demonstrated low decline rates and continue to well-exceed type curve expectations. Recall that as part of the transaction, Obsidian Energy received InPlay shares as part of the consideration.

Non-binding offer. InPlay Oil announced that Obsidian Energy has entered into a non-binding agreement with a third party for the sale of its entire position in InPlay, totaling 9,139,784 common shares. The proposed transaction is expected to occur at a premium to InPlay’s share price as of July 15, 2025. While the parties remain in discussions, no binding agreement has been finalized at this time.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Oil prices held relatively steady on Wednesday, July 16, as competing forces in the global energy market kept prices from making strong moves in either direction. West Texas Intermediate (WTI) crude hovered near $66 per barrel after an earlier dip in the session.

The market saw downward pressure from an unexpected rise in crude inventories at Cushing, Oklahoma, a key storage and pricing hub. At the same time, distillate fuel demand, which includes diesel, showed signs of softening. These developments signaled a possible easing of near-term consumption, raising concerns about oversupply.

Despite those pressures, oil has shown strength over the past several weeks. Seasonal demand, particularly during summer months when travel activity peaks, has provided a degree of support. At the same time, the broader financial markets saw a boost after political tensions appeared to ease in Washington, improving investor sentiment across risk assets.

Globally, oil supply continues to rise as major producers ramp up output. The OPEC+ group has been reintroducing volumes that were previously held back, while production across North and South America has also grown. This increase in supply has raised the potential for a looser market in the months ahead, especially if demand growth slows.

Even so, signs of tightness remain in the short term. U.S. crude inventories fell by nearly 4 million barrels in the most recent report, and distillate stockpiles remain at their lowest seasonal level in decades. These conditions suggest that supply constraints are still present in certain segments of the market.

The structure of oil futures continues to indicate firm short-term demand. The price for immediate delivery remains higher than later-dated contracts, a pattern known as backwardation. This typically reflects a market that is undersupplied in the near term, even if concerns about oversupply persist further out.

Globally, oil stockpiles have been increasing in some regions, though the build-up has been concentrated in markets that do not heavily influence futures prices. This uneven distribution of supply has helped keep benchmark prices relatively supported, especially in Atlantic-based markets where Brent crude is priced.

As the oil market navigates seasonal trends, evolving supply dynamics, and shifts in global demand, prices are likely to remain rangebound in the near term. While inventory changes and geopolitical developments can trigger short-term fluctuations, the overall outlook continues to be shaped by a complex balance of economic and physical market factors.

")

")

")

")