National Cancer Institute (NCI)-led research of PDS0301, a novel investigational tumor-targeting IL-12 fusion protein, shows dose-dependent, immune responses and association with improved clinical outcomes

FLORHAM PARK, N.J., March 01, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, announced that clinical research conducted by the NCI, one of the Institutes of the National Institutes of Health, was published in the peer-reviewed journal, International Immunopharmacology. The clinical study assessed immune changes in relation to the dose level and dosing schedule of PDS0301 (NHS-IL12), a novel investigational fusion protein consisting of a tumor-targeting antibody conjugated to Interleukin 12 (IL-12). The study also evaluated the correlation of several treatment-related immunological changes with clinical responses.

As described in the paper, titled, “Immune correlates with response in patients with metastatic solid tumors treated with a tumor-targeting immunocytokine NHS-IL12,” the researchers at the NCI evaluated a subset of 23 patients with advanced cancers who participated in a Phase 1 clinical trial of PDS0301. Patients were dosed every 2 weeks with PDS0301 at one of two levels – 12.0 mcg/kg and 16.8 mcg/kg – or every 4 weeks at 16.8 mcg/kg to identify dosing amounts and regimens of PDS0301 that correlate with higher levels of immune activation, including quantities of CD8 T cells, immune suppressive T regulatory cells, natural killer cells (NK) and natural killer T cells (NKT).

Patients receiving the higher dose of PDS0301 generated “a more robust immune activation compared to a lower dose,” including a greater expansion of NK, NKT, and CD8 T cells. Additionally, patients treated with the higher dose at two-week intervals had a greater response than patients receiving treatment every four weeks in the study. Importantly, greater increases were seen at the higher dose level in the serum pro-inflammatory cytokines IFNγ and TNFα, and soluble PD-1 (sPD-1). Studies found that increases in sPD-1 post-therapy have been associated with improved survival in various cancers and may indicate re-activation of CD8 T cells.

The ability to limit exposure of IL-12 in the circulating blood, and to increase its presence within the tumors constitutes a significant advancement in the development of cytokine-based immunotherapy. “The research published by the NCI demonstrates the potential of PDS0301 as a tumor-targeting IL-12 and its ability to stimulate immune activation and increase the frequency of CD8 T cells and certain NK cell subsets to potentially overcome the immunosuppressive tumor microenvironment,” stated Dr. Lauren V. Wood, Chief Medical Officer of PDS Biotech. “Importantly, this study appears to demonstrate the safety and tolerability of biologically active doses of PDS0301 and reports increases in specific immune cells that were associated with PDS0301 administration and improved clinical outcomes.”

The publication also summarizes clinical results from a study combining PDS0301, with a checkpoint inhibitor and PDS0101, PDS Biotech’s HPV-targeted immunotherapy that has been shown to promote induction of multifunctional, tumor-infiltrating killer T-cells. In this study in advanced HPV-positive anal, cervical, head and neck, vaginal, and vulvar cancers patients with checkpoint inhibitor refractory disease, 63% of patients who received the 16.8 mcg/kg dose had an objective response.

About PDS0301

PDS0301 is a novel investigational tumor-targeting Interleukin 12 (IL-12) that enhances the proliferation, potency and longevity of T cells in the tumor microenvironment. Together with Versamune® based immunotherapies PDS0301 works synergistically to promote a targeted T cell attack against cancers. PDS0301 is given by a simple subcutaneous injection. Clinical data suggest the addition of PDS0301 to Versamune® based immunotherapies may demonstrate significant disease control by shrinking tumors and/or prolonging survival in recurrent/metastatic cancers with poor survival prognosis.

About PDS Biotechnology

PDS Biotech is a clinical-stage immunotherapy company developing a growing pipeline of targeted cancer and infectious disease immunotherapies based on our proprietary Versamune®, PDS0301, and Infectimune™ T cell-activating platforms. We believe our targeted Versamune® and PDS0301 based candidates have the potential to overcome the limitations of current immunotherapy approaches through the activation of the right type, quantity and potency of T cells. To date, our lead Versamune® clinical candidate, PDS0101, has demonstrated the ability to reduce tumors and stabilize disease in combination with approved and investigational therapeutics in patients with a broad range of HPV16-associated cancers in multiple Phase 2 clinical trials. Our Infectimune™ based vaccines have also demonstrated the potential to induce not only robust and durable neutralizing antibody responses, but also powerful T cell responses, including long-lasting memory T cell responses in pre-clinical studies to date. To learn more, please visit www.pdsbiotech.com or follow us on Twitter at @PDSBiotech.

Forward Looking Statements

This communication contains forward-looking statements (including within the meaning of Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended) concerning PDS Biotechnology Corporation (the “Company”) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management, as well as assumptions made by, and information currently available to, management. Forward-looking statements generally include statements that are predictive in nature and depend upon or refer to future events or conditions, and include words such as “may,” “will,” “should,” “would,” “expect,” “anticipate,” “plan,” “likely,” “believe,” “estimate,” “project,” “intend,” “forecast,” “guidance”, “outlook” and other similar expressions among others. Forward-looking statements are based on current beliefs and assumptions that are subject to risks and uncertainties and are not guarantees of future performance. Actual results could differ materially from those contained in any forward-looking statement as a result of various factors, including, without limitation: the Company’s ability to protect its intellectual property rights; the Company’s anticipated capital requirements, including the Company’s anticipated cash runway and the Company’s current expectations regarding its plans for future equity financings; the Company’s dependence on additional financing to fund its operations and complete the development and commercialization of its product candidates, and the risks that raising such additional capital may restrict the Company’s operations or require the Company to relinquish rights to the Company’s technologies or product candidates; the Company’s limited operating history in the Company’s current line of business, which makes it difficult to evaluate the Company’s prospects, the Company’s business plan or the likelihood of the Company’s successful implementation of such business plan; the timing for the Company or its partners to initiate the planned clinical trials for PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates; the future success of such trials; the successful implementation of the Company’s research and development programs and collaborations, including any collaboration studies concerning PDS0101, PDS0203 and other Versamune® and Infectimune™ based product candidates and the Company’s interpretation of the results and findings of such programs and collaborations and whether such results are sufficient to support the future success of the Company’s product candidates; the success, timing and cost of the Company’s ongoing clinical trials and anticipated clinical trials for the Company’s current product candidates, including statements regarding the timing of initiation, pace of enrollment and completion of the trials (including the Company’s ability to fully fund its disclosed clinical trials, which assumes no material changes to our currently projected expenses), futility analyses, presentations at conferences and data reported in an abstract, and receipt of interim or preliminary results (including, without limitation, any preclinical results or data), which are not necessarily indicative of the final results of the Company’s ongoing clinical trials; any Company statements about its understanding of product candidates mechanisms of action and interpretation of preclinical and early clinical results from its clinical development programs and any collaboration studies; the success of the Company’s license agreements, including the potential for the clinical and nonclinical data available under the Company’s exclusive license agreement with Merck KGaA to aid in the development of the Versamune® platform; and other factors, including legislative, regulatory, political and economic developments not within the Company’s control, including unforeseen circumstances or other disruptions to normal business operations arising from or related to COVID-19. The foregoing review of important factors that could cause actual events to differ from expectations should not be construed as exhaustive and should be read in conjunction with statements that are included herein and elsewhere, including the risk factors included in the Company’s annual and periodic reports filed with the SEC. The forward-looking statements are made only as of the date of this press release and, except as required by applicable law, the Company undertakes no obligation to revise or update any forward-looking statement, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

MELVILLE, N.Y. – March 1, 2023– Comtech (NASDAQ: CMTL) today announced that it plans to release its second quarter fiscal 2023 results after the market closes on Thursday, March 9, 2023.

At 5:00 p.m. ET that day, Ken Peterman, Comtech’s Chief Executive Officer and President, will hold a conference call to discuss the Company’s second quarter fiscal 2023 results, operations, and business trends. A real-time webcast of the call will be available to the public at the investor relations section of the Comtech web site at www.comtech.com. Alternatively, investors can access the conference call by dialing (800) 225-9448 (domestic) or (203) 518-9708 (international) and using the conference I.D. of “Comtech.” A replay of the call will also be available by dialing (800) 839-3516 or (402) 220-7238 through Friday, March 24, 2023.

About Comtech

Comtech Telecommunications Corp. is a leading global technology company providing terrestrial and wireless network solutions, next-generation 9-1-1 emergency services, satellite and space communications technologies, and cloud native capabilities to commercial and government customers around the world. Our unique culture of innovation and employee empowerment unleashes a relentless passion for customer success. With multiple facilities located in technology corridors throughout the United States and around the world, Comtech leverages our global presence, technology leadership, and decades of experience to create the world’s most innovative communications solutions.For more information, please visit www.comtech.com.

Forward-Looking Statements

Certain information in this press release contains statements that are forward-looking in nature and involve certain significant risks and uncertainties. Actual results could differ materially from such forward-looking information. The Company’s Securities and Exchange Commission filings identify many such risks and uncertainties. Any forward-looking information in this press release is qualified in its entirety by the risks and uncertainties described in such Securities and Exchange Commission filings.

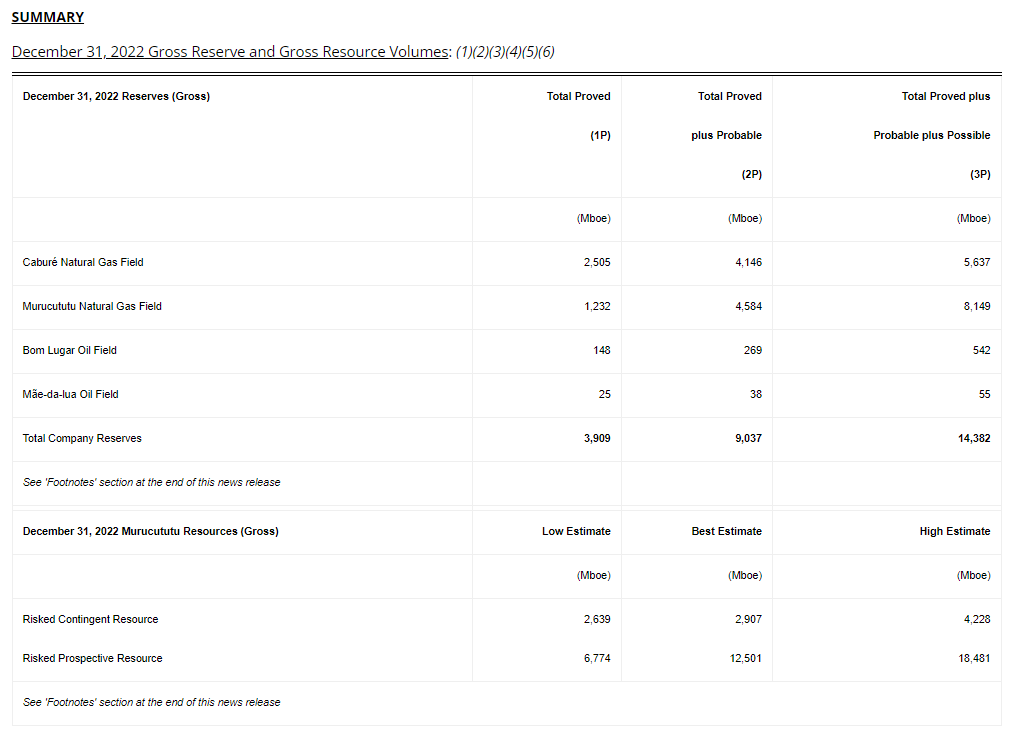

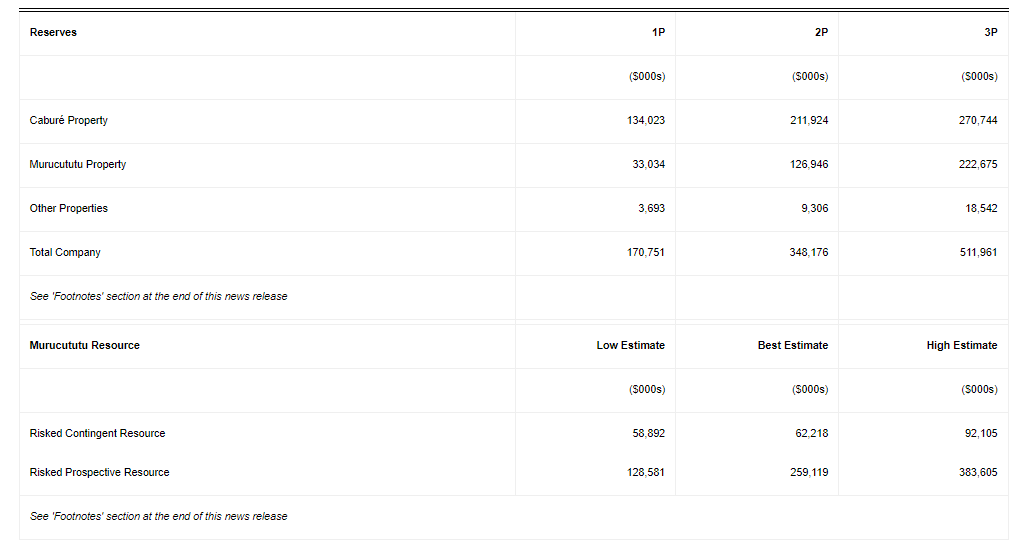

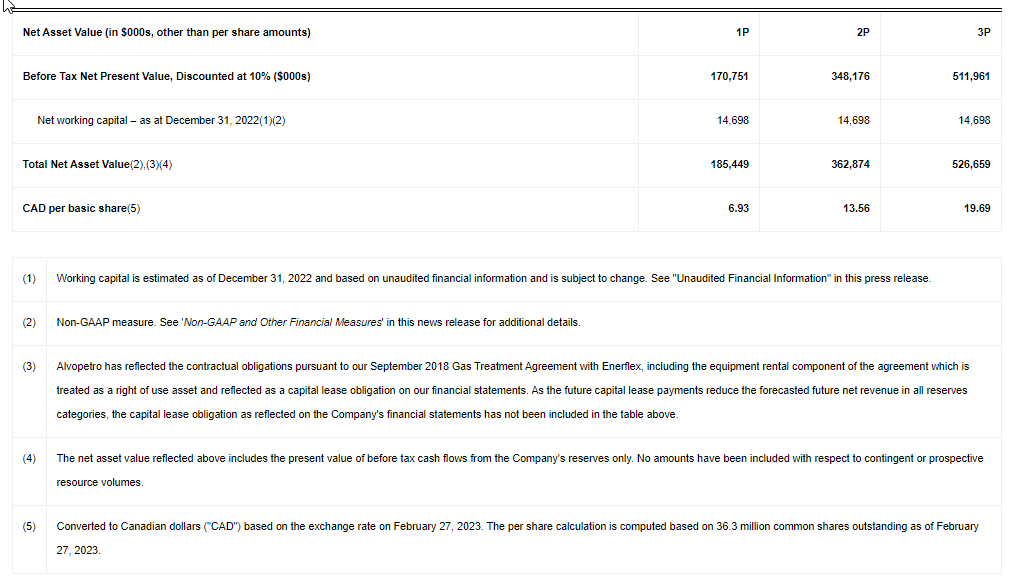

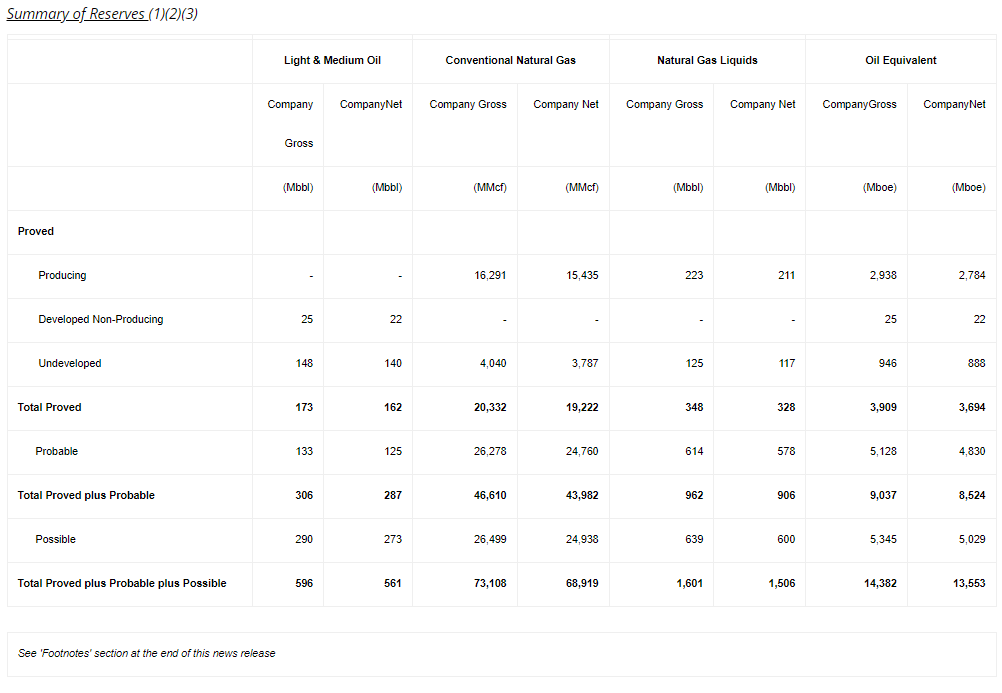

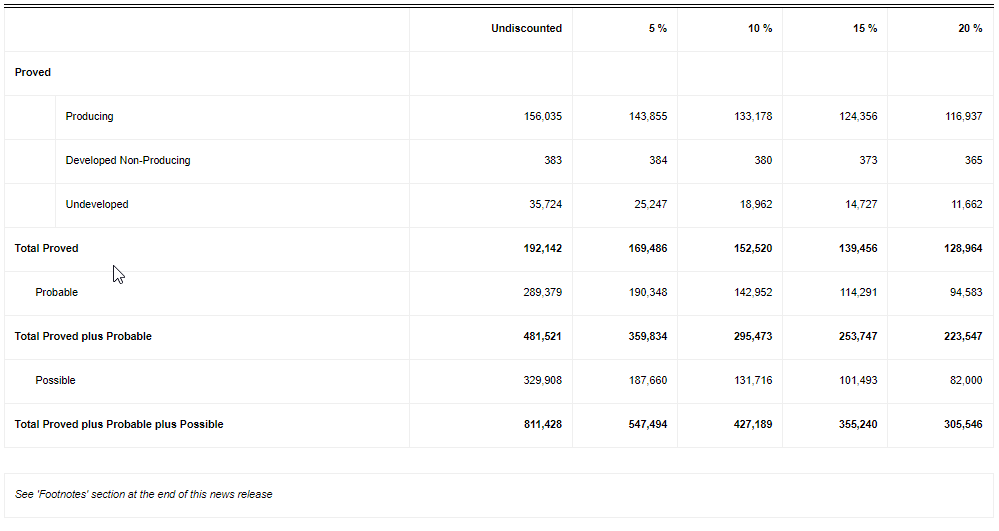

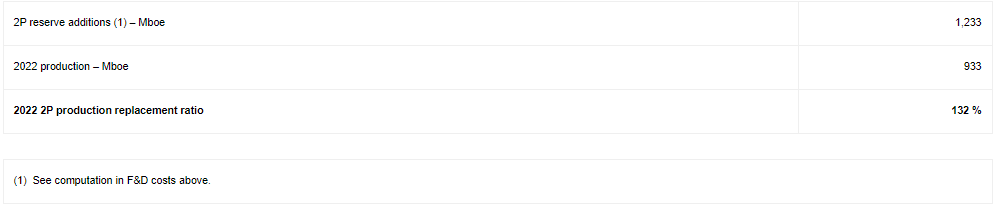

CALGARY, AB, Feb. 28, 2023 /CNW/ – Alvopetro Energy Ltd. (TSXV: ALV) (OTCQX: ALVOF) announces our reserves as at December 31, 2022 with total proved plus probable (“2P”) reserves of 9.0 MMboe and a before tax net present value discounted at 10% of $348.2 million. 2P reserve additions replaced 132% of 2022 production. 2P reserve volumes increased by 3%, despite 0.9 MMboe of production in 2022, due to reserve additions associated mainly with two additional Murucututu development locations (previously included in contingent resources). The before tax net present value of our 2P reserves (discounted at 10%) increased by 17% from December 31, 2021, due to reserve additions and increases in forecasted natural gas prices. Alvopetro also announces the December 31, 2022 assessment of the Company’s Murucututu natural gas resource with risked best estimate contingent resource of 2.9 MMboe and risked best estimate prospective resource of 12.5 MMboe. The Murucututu natural gas contingent and prospective resource values (risked best estimate net present value before tax, discounted at 10%) are $62.2 million and $259.1 million, respectively. The reserves and resources data set forth herein is based on an independent reserves and resources assessment and evaluation prepared by GLJ Ltd. (“GLJ”) dated February 27, 2023 with an effective date of December 31, 2022 (the “GLJ Reserves and Resources Report”).

All references herein to $ refer to United States dollars, unless otherwise stated.

December 31, 2022 GLJ Reserves and Resource Report Highlights

2P net present value before tax discounted at 10% increased 17% to $348.2 million.

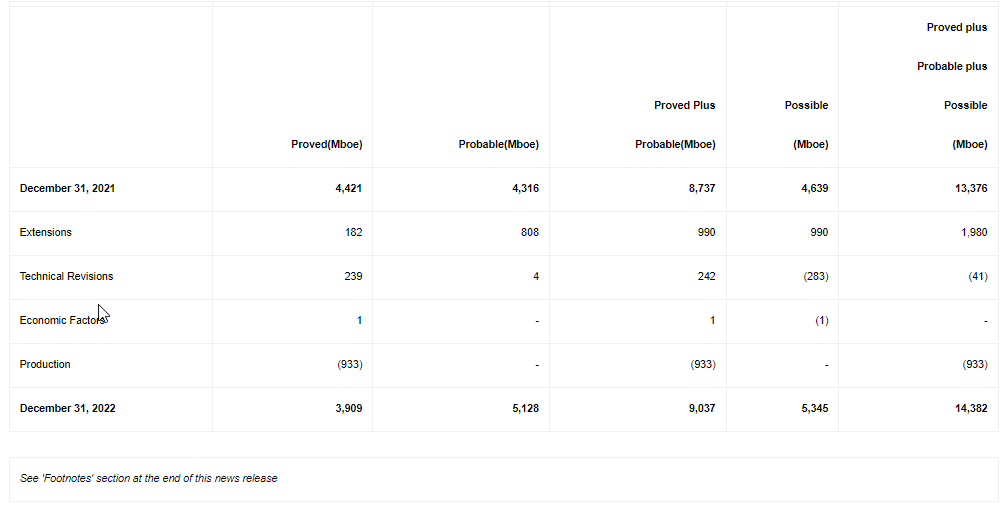

Proved reserves (“1P”) decreased 12% to 3.9 MMboe and 2P reserves increased 3% to 9.0 MMboe after 0.9 MMboe of production in 2022.

2P production replacement ratio(1) of 132%.

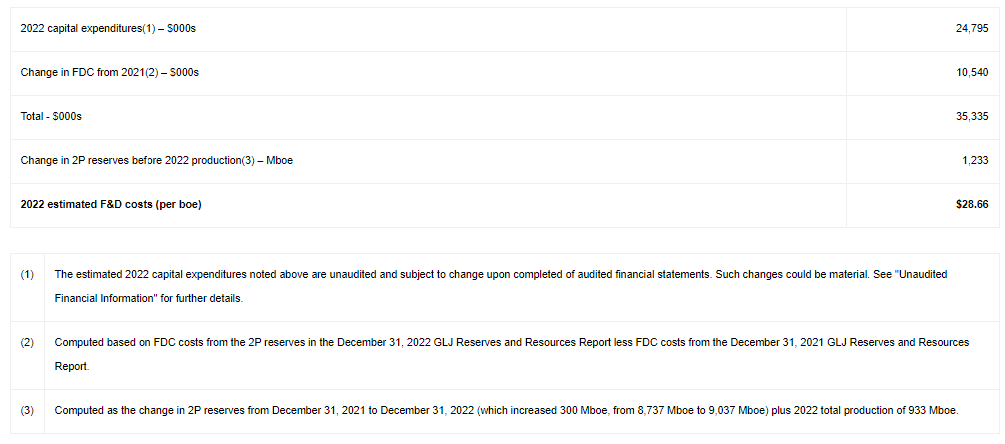

2P F&D costs(1) estimated at $28.66/boe.

2P recycle ratio(1) estimated at 2.1 times.

2P Net Asset Value(1) of CAD$13.56/share ($9.99/share) before any potential from contingent or prospective resources.

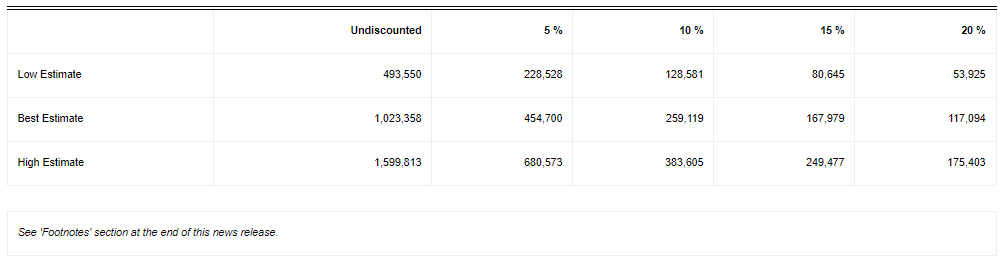

Risked best estimate contingent resource of 2.9 MMboe (NPV10 $62.2 million) and risked best estimate prospective resource of 12.5 MMboe (NPV10 $259.1 million).

Corey Ruttan, President and Chief Executive Officer, commented:

“Our 2022 year-end reserves and resource evaluations highlight the continued strong profitability from our Caburé natural gas field and the long-term potential of our Murucututu project. The increase in forecasted cash flows reflects the impact of reserve additions associated with our near-term development plans on our Murucututu asset and increases in forecasted natural gas prices under our long-term gas sales agreement. Our 2023 capital program is focused on lower risk development opportunities including accelerated activity on our Murucututu asset targeting the long-term natural gas potential of this field.”

(1)

Refer to the sections entitled “Oil and Natural Gas Advisories – Other Metrics” and “Non-GAAP and Other Financial Measures” for additional disclosures and assumptions used in calculating production replacement ratio, F&D costs, recycle ratio, net asset value and net asset value per share.

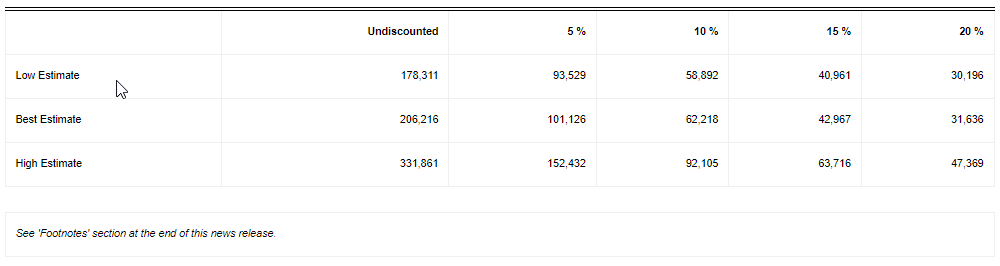

Net Present Value Before Tax Discounted at 10%:(1)(2)(3)(4)(5)(6)(7)(8)

NET ASSET VALUE

Following the December 31, 2022 reserves evaluation, based on the before tax net present value of Alvopetro’s 2P reserves (discounted at 10%), our total 2P net asset value is $362.9 million; CAD$13.56 per common share outstanding. Our 2P net asset value of $362.9 million is before including the before tax net present value (discounted at 10%) of our risked best estimate risked contingent resource of $62.2 million and our risked prospective resource of $259.1 million from the Murucututu natural gas field.

PRICING ASSUMPTIONS – FORECAST PRICES AND COSTS

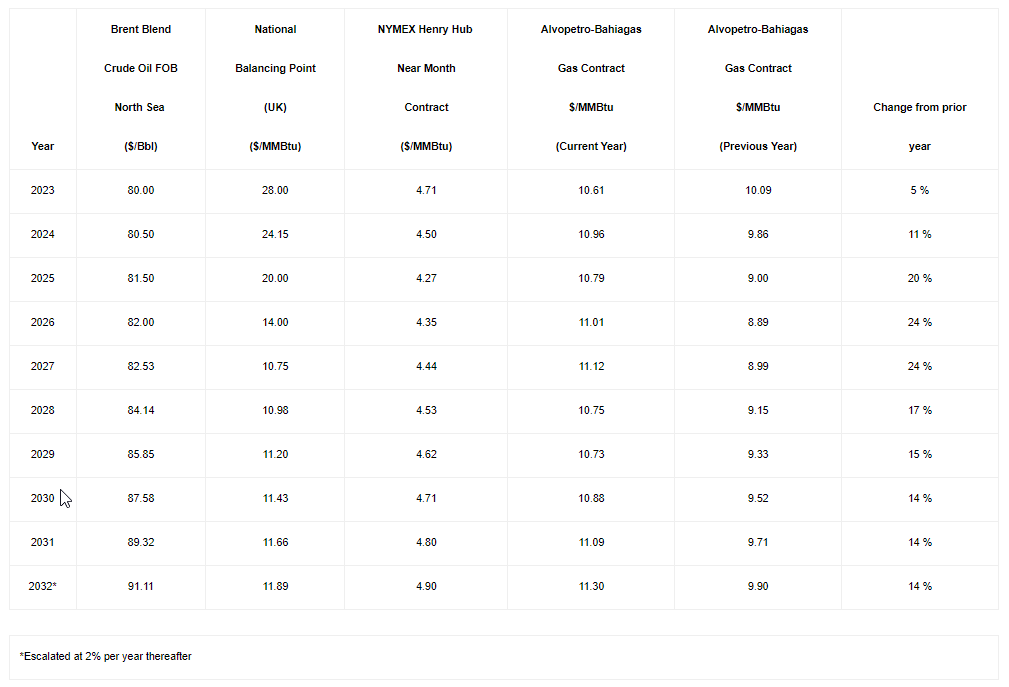

GLJ employed the following pricing and inflation rate assumptions as of January 1, 2023 in the GLJ Reserves and Resources Report in estimating reserves and resources data using forecast prices and costs.

As of February 1, 2023, Alvopetro’s contracted natural gas price under the terms of our long-term gas sales agreement is based on the ceiling price within the contract and is forecasted to remain at the ceiling price until 2027. The ceiling price incorporates assumed US inflation of 3% in 2023 and 2% thereafter.

GLJ RESERVES AND RESOURCES REPORT

The GLJ Reserves and Resources Report has been prepared in accordance with the standards contained in the Canadian Oil and Gas Evaluation Handbook (“COGEH”) that are consistent with the standards of National Instrument 51-101 (“NI 51-101”). GLJ is a qualified reserves evaluator as defined in NI 51-101. The GLJ Reserves and Resources Report was an evaluation of all reserves of Alvopetro including our Caburé and Caburé Leste natural gas fields (collectively referred to as our Caburé natural gas field), our Murucututu natural gas project (previously referred to as Gomo), as well as our Bom Lugar and Mãe-da-lua oil fields. The GLJ Reserves and Resources Report also includes an evaluation of the gas resources of our Murucututu natural gas. In addition to the reserves assigned to our two existing Murucututu wells (197-1 and 183-1) and four additional development locations, contingent resource was assigned to the area in proximity to our existing Murucututu reserves, deemed to be discovered. The area mapped by 3D seismic west and north of the area defined as contingent was assigned prospective resource. Additional reserves and resources information as required under NI 51-101 will be included in the Company’s Annual Information Form for the 2022 fiscal year which will be filed on SEDAR by April 30, 2023.

December 31, 2022 Reserves Information:

Summary of Reserves (1)(2)(3)

Summary of Before Tax Net Present Value of Future Net Revenue – $000s(1)(2)(3)(7)(8)

Summary of After Tax Net Present Value of Future Net Revenue – $000s(1)(2)(3)(7)(8)

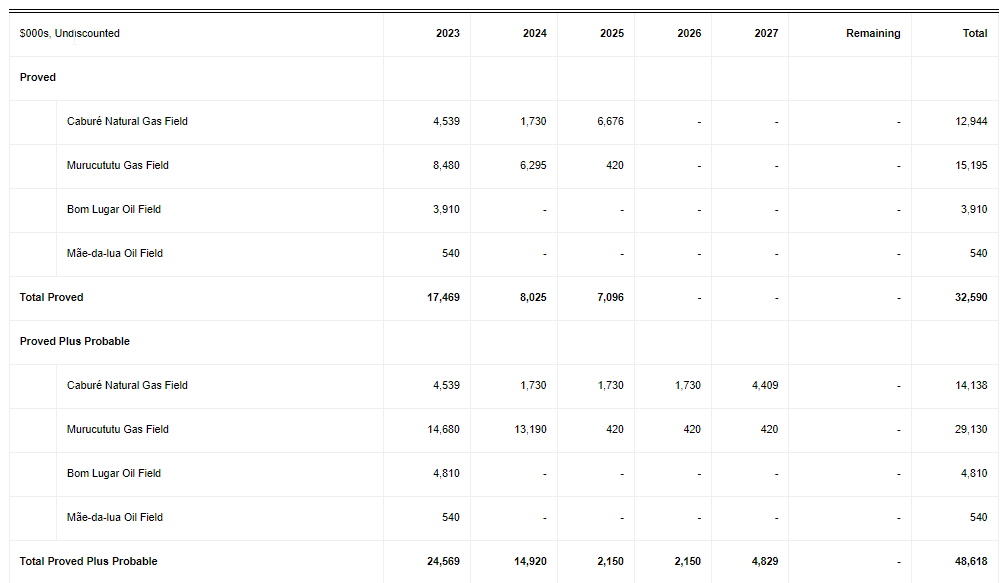

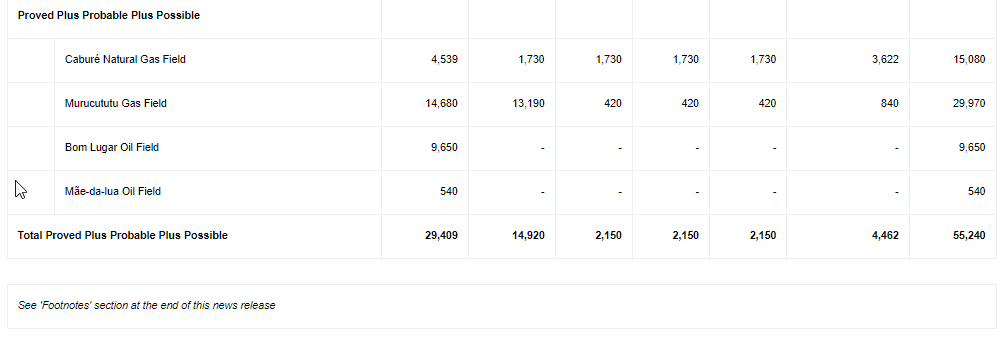

Future Development Costs (1)(2)(3)(7)(8)

The table below sets out the total development costs deducted in the estimation of future net revenue attributable to proved reserves, proved plus probable reserves and proved plus probable plus possible reserves (using forecast prices and costs), by field, in the GLJ Reserves and Resources Report. Total development costs include capital costs for drilling and facility and pipeline expenditures but excludes abandonment and reclamation costs.

Under each reserve category, Alvopetro has elected to reflect 100% of the contractual obligations pursuant to our Gas Treatment Agreement with Enerflex, including all operating, capital, and related financing costs for the full duration of the agreement. These costs are mainly attributable to the Caburé field and also represent the majority of the future development costs for the Caburé field in the table below. The future costs associated with equipment rental are also reflected as a capital lease obligation on our financial statements. Also included in future development costs for the Caburé field are two step-out wells and expansion of the unit facilities.

The future development costs for the Murucututu field in the proved category are for two development locations in the field and the stimulation of the 197(1) well. In the probable and possible categories, there are future development costs for two additional development locations. Also included in the Murucututu future development costs for all reserve categories are a portion of the anticipated contractual obligations associated with the expansion of the gas treatment facility. The future development costs for Bom Lugar in the proved category include costs for one development well and facilities upgrade. A second development well is included in the future development costs for the possible category for Bom Lugar. Future development costs at the Mãe-da-lua field relate to a stimulation of the existing producing well.

Reconciliation of Alvopetro’s Gross Reserves (Before Royalty) (1)(2)(3)(8)

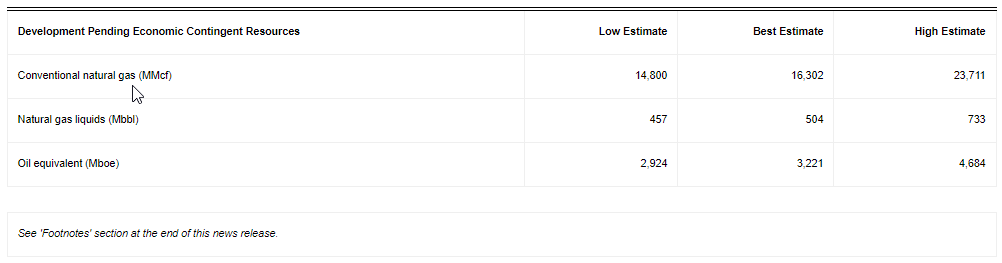

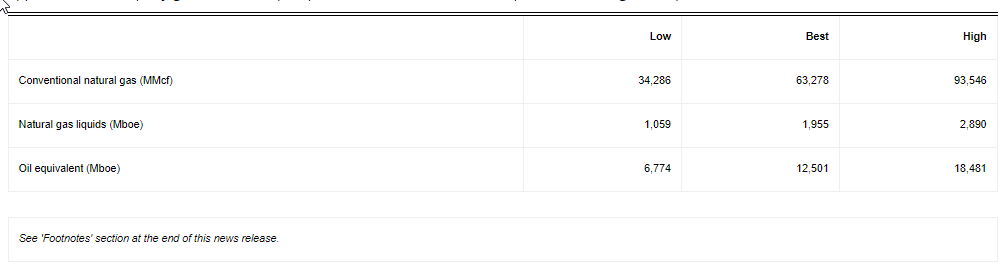

December 31, 2022 Murucututu Contingent Resources Information:

Summary of Unrisked Company Gross Contingent Resources (1)(2)(5)(6)

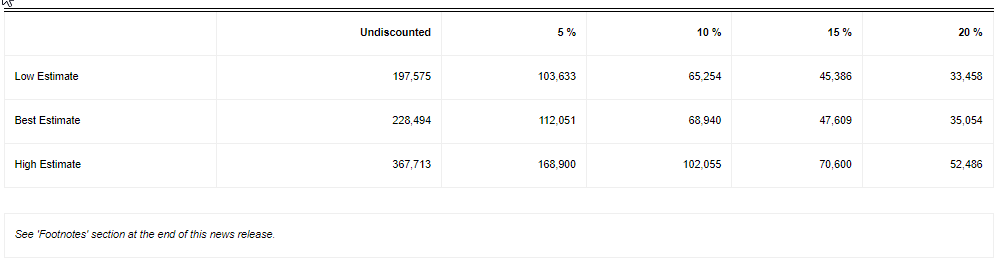

Summary of Before Tax Net Present Value of Future Net Revenue of Unrisked Contingent Resources- $000s (1)(2)(5)(6)(7)(8)

The GLJ Contingent Resource Report for Murucututu assumes capital deployment starting in 2024 for the drilling of wells with total project costs of $19.1 million and first commercial production in 2024. The information presented herein is based on company net project development costs. The recovery technology assumed for purposes of the estimate is based on established technologies utilized repeatedly in the industry.

There can be no certainty that the project will be developed on the timelines discussed herein. The project is based on a pre-development study. Development of the project is dependent on several contingencies as further described in this news release. Significant positive factors relevant to the estimate include existing production in close proximity, proximity to infrastructure, existing long-term gas sales agreement and corporate commitment to the project. Significant negative factors relevant to the estimate include reservoir performance and the economic viability of the project (with sensitivity to low commodity prices), access to and amount of capital required to develop resources at an acceptable cost, and regulatory approvals for planned activities including stimulations and new infrastructure developments.

Summary of Development Pending Risked Company Gross Contingent Resources(1)(2)(5)(6)

The GLJ Reserves and Resources Report estimates the Chance of Development as the product of two main contingencies associated with the project development, which are: 1) the probability of corporate sanctioning, which GLJ estimates at 95%; 2) the probability of finalization of a development plan, which GLJ estimates at 95%. The product of these two contingencies is 90%. As there is no risk related to discovery, the Chance of Commerciality for the contingent resource is therefore 90% which is the risk factor that has been applied to the Development Risked company gross contingent resources and the net present value figures reported below.

Summary of Development Pending Risked Before Tax Net Present Value of Future Net Revenue of Contingent Resources- $000s(1)(5)(6)(7)(8)

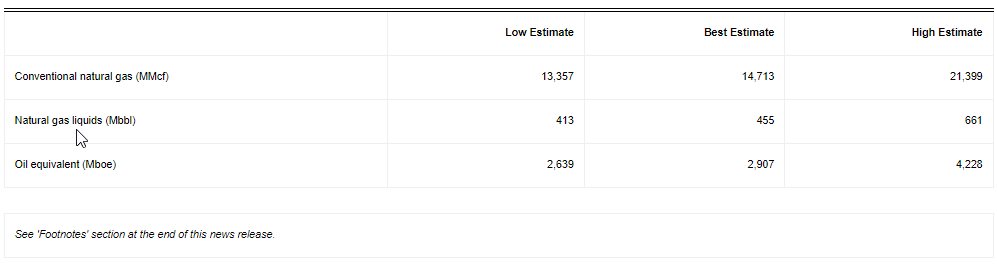

December 31, 2022 Murucututu Prospective Resources Information:

Summary of Unrisked Company Gross Prospective Resources (1)(2)(4)(6)

Summary of Before Tax Net Present Value of Future Net Revenue of Unrisked Prospective Resources – $000s (1)(4)(6)(7)(8)

The GLJ Reserves and Resources Report for Murucututu prospective resources assumes capital deployment starting in 2025 for the drilling of wells, expansion of field facilities, and additional pipeline capacity, with total project costs of $70.0 million and first commercial production in 2025. The information presented herein is based on company project development costs. The recovery technology assumed for purposes of the estimate is based on established technologies utilized repeatedly in the industry.

There can be no certainty that the project will be developed on the timelines discussed herein. Development of the project is dependent on several contingencies as further described in this news release. The project is based on a conceptual study. Significant positive factors relevant to the estimate include existing production in close proximity, proximity to infrastructure, existing long-term gas sales agreement and corporate commitment to the project. Significant negative factors relevant to the estimate include reservoir performance and the economic viability of the project (with sensitivity to low commodity prices), access to and amount of capital required to develop resources at an acceptable cost, and regulatory approvals for planned activities including stimulations and new infrastructure developments.

Summary of Development Risked Company Gross Prospective Resources(1)(2)(4)(6)

The GLJ Reserves and Resources Report estimates the Chance of Commerciality as the product between the Chance of Discovery and the Chance of Development. The Chance of Discovery of the prospective resources has been assessed at 90%, while the Chance of Development has been assessed as the same as for the Contingent Resources described above at 90%. The resulting Chance of Commerciality is 81%, which has been applied to the company gross unrisked prospective resources and the net present value figures reported below.

Summary of Development Risked Before Tax Net Present Value of Future Net Revenue of Prospective Resources- $000s(1)(4)(6)(7)(8)

UPCOMING 2022 RESULTS AND LIVE WEBCAST

Alvopetro anticipates announcing its 2022 fourth quarter and year-end results on March 21, 2023 after markets close and will host a live webcast to discuss the results at 9:00 am Mountain time, on March 22, 2023. Details for joining the event are as follows:

The webcast will include a question and answer period. Online participants will be able to ask questions through the Zoom portal. Dial-in participants can email questions directly to [email protected].

CORPORATE PRESENTATION

Alvopetro’s updated corporate presentation is available on our website at:

References to Company Gross reserves or Company Gross Resources means the total working interest share of remaining recoverable reserves or resources held by Alvopetro before deductions of royalties payable to others and without including any royalty interests held by Alvopetro.

(2)

The tables above are a summary of the reserves of Alvopetro and the net present value of future net revenue attributable to such reserves as evaluated in the GLJ Reserves and Resources Report based on forecast price and cost assumptions. The tables summarize the data contained in the GLJ Reserves and Resources Report and as a result may contain slightly different numbers than such report due to rounding. Also due to rounding, certain columns may not add exactly.

(3)

Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

(4)

Prospective Resources are defined in the COGE Handbook as those quantities of petroleum estimated, as of a given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. Prospective resources have both an associated chance of discovery and a chance of development. There is no certainty that any portion of the prospective resources will be discovered and even if discovered, there is no certainty that it will be commercially viable to produce any portion. Prospective Resources are further subdivided in accordance with the level of certainty associated with recoverable estimates assuming their discovery as described in footnote 11.

(5)

Contingent Resources are defined in the COGE Handbook as those quantities of petroleum estimated, as of a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but are not currently considered to be commercially recoverable due to one or more contingencies. Contingencies may include factors such as economic, legal, environmental, political and regulatory matters or a lack of markets. It is also appropriate to classify as contingent resources the estimated discovered recoverable quantities associated with a project in the early evaluation stage. Contingent Resources are further classified in accordance with the level of certainty associated with the estimates as described in footnote 11 and may be subclassified based on project maturity and/or characterized by their economic status. The Contingent Resources estimated in the GLJ Reserves and Resources Report are classified as “economic contingent resources”, which are those contingent resources that are currently economically recoverable. All such resources are further sub-classified with a project status of “development pending”, meaning that resolution of the final conditions for development are being actively pursued. The recovery estimates of the Company’s contingent resources provided herein are estimates only and there is no guarantee that the estimated resources will be recovered. There is uncertainty that it will be commercially viable to produce any portion of the resources. Actual recovered resource may be greater than or less than the estimates provided herein.

(6)

Low Estimate: This is considered to be a conservative estimate of the quantity that will actually be recovered. It is likely that the actual remaining quantities recovered will exceed the low estimate. If probabilistic methods are used, there should be at least a 90 percent probability (P90) that the quantities actually recovered will equal or exceed the low estimate.Best Estimate: This is considered to be the best estimate of the quantity that will actually be recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate. If probabilistic methods are used, there should be at least a 50 percent probability (P50) that the quantities actually recovered will equal or exceed the best estimate.High Estimate: This is considered to be an optimistic estimate of the quantity that will actually be recovered. It is unlikely that the actual remaining quantities recovered will exceed the high estimate. If probabilistic methods are used, there should be at least a 10 percent probability (P10) that the quantities actually recovered will equal or exceed the high estimate.

(7)

The net present value of future net revenue attributable to Alvopetro’s reserves and resources are stated without provision for interest costs and general and administrative costs, but after providing for estimated royalties, production costs, development costs, other income, future capital expenditures, well abandonment and reclamation costs for only those wells assigned reserves and material dedicated gathering systems and facilities. The net present values of future net revenue attributable to Alvopetro’s reserves and resources estimated by GLJ do not represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve and resource estimates of the Company’s reserves and resources provided herein are estimates only and there is no guarantee that the estimated reserves and resources will be recovered. Actual reserves and resources may be greater than or less than the estimates provided herein.

(8)

GLJ’s January 1, 2023 escalated price forecast is used in the determination of future gas sales prices under Alvopetro’s long-term gas sales agreement and for all forecasted oil sales and natural gas liquids sales. See https://www.gljpc.com/sites/default/files/pricing/Jan23.pdf for GLJ’s price forecast.

Alvopetro Energy Ltd.’svision is to become a leading independent upstream and midstream operator in Brazil. Our strategy is to unlock the on-shore natural gas potential in the state of Bahia in Brazil, building off the development of our Caburé natural gas field and our strategic midstream infrastructure.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All amounts contained in this news release are in United States dollars, except as otherwise noted.

Abbreviations:

1P = proved reserves2P = proved plus probable reserves3P = proved plus probable plus possible reservesCAD = Canadian dollarsF&D = finding and development costsFDC = future development costs;Mbbl = thousands of barrelsMboe = thousand barrels of oil equivalentMMbtu = million British Thermal UnitsMMcf = million cubic feetMMcf/d = million cubic feet per dayMMboe = million barrels of oil equivalent$000s = thousands of U.S. dollars

Oil and Natural Gas Advisories

Oil and Natural Gas Reserves

The disclosure in this news release summarizes certain information contained in the GLJ Reserves and Resources Report but represents only a portion of the disclosure required under NI 51-101. Full disclosure with respect to the Company’s reserves as at December 31, 2022 will be included in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023. All net present values in this press release are based on estimates of future operating and capital costs and GLJ’s forecast prices as of December 31, 2022. The reserves definitions used in this evaluation are the standards defined by COGEH reserve definitions and are consistent with NI 51-101 and used by GLJ. The net present values of future net revenue attributable to the Alvopetro’s reserves estimated by GLJ do not represent the fair market value of those reserves. Other assumptions and qualifications relating to costs, prices for future production and other matters are summarized herein. The recovery and reserve estimates of the Company’s reserves provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual reserves may be greater than or less than the estimates provided herein. Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. There is a 10% probability that the quantities actually recovered will equal or exceed the sum of proved plus probable plus possible reserves.

Contingent Resources

This news release discloses estimates of Alvopetro’s contingent resources and the net present value associated with net revenues associated with the production of such contingent resources as included in the GLJ Reserves and Resources Report. There is no certainty that it will be commercially viable to produce any portion of such contingent resources and the estimated future net revenues do not necessarily represent the fair market value of such contingent resources. Estimates of contingent resources involve additional risks over estimates of reserves. Full disclosure with respect to the Company’s contingent resources as at December 31, 2022 will be contained in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023.

Prospective Resources

This news release discloses estimates of Alvopetro’s prospective resources included in the GLJ Reserves and Resources Report. There is no certainty that any portion of the prospective resources will be discovered and even if discovered, there is no certainty that it will be commercially viable to produce any portion. Estimates of prospective resources involve additional risks over estimates of reserves. The accuracy of any resources estimate is a function of the quality and quantity of available data and of engineering interpretation and judgment. While resources presented herein are considered reasonable, the estimates should be accepted with the understanding that reservoir performance subsequent to the date of the estimate may justify revision, either upward or downward. Full disclosure with respect to the Company’s prospective resources as at December 31, 2022 will be contained in the Company’s annual information form for the year ended December 31, 2022 which will be filed on SEDAR (www.sedar.com) on or before April 30, 2023.

Boe Disclosure

The term barrels of oil equivalent (“boe”) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet per barrel (6Mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. All boe conversions in this news release are derived from converting gas to oil in the ratio mix of six thousand cubic feet of gas to one barrel of oil.

Other Metrics

This press release contains metrics commonly used in the oil and natural gas industry, which have been prepared by management, including “F&D costs”, “net asset value”, “net asset value per share”, “operating netback per boe”, “production replacement ratio” and “recycle ratio”. These terms do not have a standardized meaning and may not be comparable to similar measures presented by other companies, and therefore should not be used to make such comparisons.

“F&D costs” are reflected on a per barrel of oil equivalent and are calculated as the sum of capital expenditures in the current year plus the change in FDC for the period, divided by the change in reserves in the period, before current year production. The estimated 2022 F&D costs are computed as follows:

“Net asset value” is based on the before tax net present value of the Company’s reserves as at December 31, 2022, discounted at 10% plus the Company’s net working capital balance estimated as of December 31, 2022. Net working capital is a capital management measure. See “Non-GAAP and Other Financial Measures” below for further details. The estimated net working capital as of December 31, 2022 is unaudited and subject to change upon completion of audited financial statements for the year-ended December 31, 2022. Such changes could be material. See “Unaudited Financial Information” for further details.

“Net asset value per share” is based on the computation of net asset value divided by basic shares outstanding of 36,311,579 adjusted to Canadian dollars based on the foreign exchange rate on February 27, 2023.

“Operating netback per boe” is a non-GAAP financial measure and operating netback per boe is a non-GAAP financial ratio. See “Non-GAAP and Other Financial Measures” below for further details. Alvopetro’s operating netback for the year ended December 31, 2022 is estimated at $59.43 per boe. This estimate is based on unaudited financial information and subject to change upon completion of audited financial statements for the year-ended December 31, 2022. Such changes could be material. See “Unaudited Financial Information” for further details.

“Production replacement ratio” is calculated as total reserve additions divided by current year production. Alvopetro’s 2P production replacement ratio in 2022 is calculated as:

“Recycle ratio” is calculated by dividing the estimated 2022 operating netback by estimated F&D costs per boe for the year. The Company’s estimated 2022 recycle ratio is calculated as follows:

Management uses these oil and gas metrics for its own performance measurements and to provide shareholders with measures to compare our operations over time. Readers are cautioned that the information provided by these metrics, or that can be derived from the metrics presented in this press release, should not be relied upon for investment or other purposes.

Forward-Looking Statements and Cautionary Language

This news release contains “forward-looking information” within the meaning of applicable securities laws. The use of any of the words “will”, “expect”, “intend” and other similar words or expressions are intended to identify forward-looking information. Forward-looking statements involve significant risks and uncertainties, should not be read as guarantees of future performance or results, and will not necessarily be accurate indications of whether or not such results will be achieved. A number of factors could cause actual results to vary significantly from the expectations discussed in the forward-looking statements. These forward-looking statements reflect current assumptions and expectations regarding future events. Accordingly, when relying on forward-looking statements to make decisions, Alvopetro cautions readers not to place undue reliance on these statements, as forward-looking statements involve significant risks and uncertainties. More particularly and without limitation, this news release contains forward-looking information concerning plans relating to the Company’s operational activities, proposed development activities and the timing for such activities, capital spending levels and future capital costs, the expected natural gas price, gas sales and gas deliveries under Alvopetro’s long-term gas sales agreement. The forward-looking statements are based on certain key expectations and assumptions made by Alvopetro, including but not limited to expectations and assumptions concerning the timing of regulatory licenses and approvals, equipment availability, the success of future drilling, completion, testing, recompletion and development activities, the performance of producing wells and reservoirs, well development and operating performance, expectations regarding Alvopetro’s working interest and the outcome of any redeterminations, environmental regulation, including regulation relating to hydraulic fracturing and stimulation, the ability to monetize hydrocarbons discovered, the outlook for commodity markets and ability to access capital markets, foreign exchange rates, general economic and business conditions, the impact of the COVID-19 pandemic, weather and access to drilling locations, the availability and cost of labour and services, the regulatory and legal environment and other risks associated with oil and gas operations. The reader is cautioned that assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be incorrect. Actual results achieved during the forecast period will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Although Alvopetro believes that the expectations and assumptions on which such forward-looking information is based are reasonable, undue reliance should not be placed on the forward-looking information because Alvopetro can give no assurance that it will prove to be correct. Readers are cautioned that the foregoing list of factors is not exhaustive. Additional information on factors that could affect the operations or financial results of Alvopetro are included in our annual information form which may be accessed on Alvopetro’s SEDAR profile at www.sedar.com. The forward-looking information contained in this news release is made as of the date hereof and Alvopetro undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

Unaudited Financial Information

Certain financial and operating information included in this news release for the year ended December 31, 2022 including, without limitation, 2022 capital expenditures and the impact on F&D costs, working capital, recycle ratio and operating netback, are based on estimated unaudited financial results for the year then ended, and are subject to the same limitations as discussed under Forward Looking Statements and Cautionary Language set out in this news release. These estimated amounts may change upon the completion of audited financial statements for the year ended December 31, 2022 and changes could be material.

Non-GAAP and Other Financial Measures

This news release contains references to various non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures as such terms are defined in National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. Such measures are not recognized measures under GAAP and do not have a standardized meaning prescribed by IFRS and might not be comparable to similar financial measures disclosed by other issuers. While these measures may be common in the oil and gas industry, the Company’s use of these terms may not be comparable to similarly defined measures presented by other companies. The non-GAAP and other financial measures referred to in this news release should not be considered an alternative to, or more meaningful than measures prescribed by IFRS and they are not meant to enhance the Company’s reported financial performance or position. These are complementary measures that are used by management in assessing the Company’s financial performance, efficiency and liquidity and they may be used by investors or other users of this document for the same purpose. Below is a description of the non-GAAP financial measures, non-GAAP ratios, capital management measures and supplementary financial measures used in this news release. For more information with respect to financial measures which have not been defined by GAAP, including reconciliations to the closest comparable GAAP measure, see the “Non-GAAP Measures and Other Financial Measures” section of the Company’s most recent MD&A which may be accessed through the SEDAR website at www.sedar.com .

Non-GAAP Financial Ratios

Operating netback per boe

Operating netback is calculated on a per unit basis, which is per barrel of oil equivalent (“boe”). It is a common non-GAAP measure used in the oil and gas industry and management believes this measurement assists in evaluating the operating performance of the Company. It is a measure of the economic quality of the Company’s producing assets and is useful for evaluating variable costs as it provides a reliable measure regardless of fluctuations in production. Alvopetro calculated operating netback per boe as operating netback (a non-GAAP financial measure calculated as natural gas, oil and condensate revenues less royalties and production expenses) divided by total sales volumes (barrels of oil equivalent). More details on the method of calculation is provided in the “Operating Netback per boe” section of the Company’s MD&A. The Company’s MD&A may be accessed through the SEDAR website at www.sedar.com. Operating netback is a common metric used in the oil and gas industry used to demonstrate profitability from operations on a per unit basis (boe). The Company’s operating netback per boe is estimated at $59.43 per boe for the year ended December 31, 2022. This amount is unaudited and subject to change as further discussed in the section “Unaudited Financial Information”.

Capital Management Measures

Net Working Capital

Net working capital is computed as current assets less current liabilities. Net working capital is a measure of liquidity, is used to evaluate financial resources. The Company’s net working capital as of December 31, 2022 is estimated at $14.7 million. This amount is unaudited and subject to change as further discussed in the section “Unaudited Financial Information”.

VANCOUVER, BC, Feb. 28, 2023 /PRNewswire/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE:35D) is pleased to report favourable comminution results on multiple samples extracted from the Wicheeda deposit. The data allows the design of the crushing and grinding plant that will be an integral part of the planned Wicheeda development. These data are essential inputs to the upcoming pre-feasibility study (PFS).

Comminution, i.e., crushing and grinding, will be the first step in the processing of material mined from the Wicheeda deposit. In the process, coarse, as-mined, rocks are reduced in size to sand-like particles, typically less than 1 mm in size, and suitable for upgrading by flotation or other means. Comminution usually accounts for a significant percentage of the energy demand, production cost and carbon footprint of a mineral processing plant.

John Goode, Metallurgy Advisor, stated: “Comminution tests on seventeen variability samples and a Master Composite show that the ore is soft, amenable to conventional grinding operations and has a low abrasion index. The recent results confirm, and expand on data obtained from a 30 t bulk sample taken in 2019. The data show that a conventional semi-autogenous grinding (SAG) mill-ball mill circuit will work well and that grinding energy and supply costs will be relatively low.”

Key Highlights:

The Wicheeda variability samples and Master Composite were studied using the industry-standard SMC test to determine amenability to, and sizing design parameters for, SAG processing. The A x b value averaged 97 and the SAG Circuit Specific Energy (SCSE) averaged 7 kWh/t indicating a very soft ore.

The Bond rod mill work index test was applied to the Master Composite and returned a value of 10 kWh/t – which again indicates a very soft feed material.

The Bond ball mill work index test was applied to all samples and resulted in an average of 10 kWh/t using a 65-mesh closing screen. This again indicates a very soft feed material.

A standard Bond abrasion test was performed on the Master Composite and returned a value of 0.059 g meaning a very low consumption of grinding balls and mill liners is anticipated.

The Bond ball mill work index and abrasion index data for these new samples are very similar to the values obtained on the 2019 bulk sample taken from the Wicheeda deposit giving additional confidence in the new data. Comminution data for the 2019 bulk sample were used during preparation of the 2021 Independent Preliminary Economic Assessment1.

Methodology

Seventeen variability samples and a Master Composite were made from drill core taken from the Wicheeda deposit. The variability samples covered different lithologies, depths, areas and grades of the deposit. The Master Composite had a mass of 260 kg and included all lithologies in the approximate ratios of their mass in the deposit.

SGS Lakefield performed all of the comminution tests. The SMC testing protocol is an industry-standard method of evaluating the amenability of material to grinding in a semi-autogenous grinding (SAG) mill. The Bond rod and ball mill indices and abrasion index are also industry-standard tests performed on crushed ore and are essential to the accurate sizing of a grinding circuit.

The comminution data will be used, along with other information, during the upcoming pre-feasibility study (PFS) to design the comminution circuit for the Wicheeda project.

PDAC Convention, Toronto, March 5 – 8, 2023

The Company is also pleased to announce that it will be attending this year’s Prospector’s and Developer’s Annual Convention (PDAC) in Toronto, Ontario, Canada from Sunday, March 5 to Wednesday, March 8, 2023.

The Company’s management team, members of the Board of Directors and technical advisors will be available during the convention (www.pdac.ca/convention) and invite you to drop by Booth #2500 in the Investors Exchange in the Metro Toronto Convention Centre from March 5 – 7, 2023, 10 a.m. to 5 p.m. and March 8, 2023, 9 a.m. to 12 p.m. to discuss the Company’s latest activities and plans for 2023 and onward.

In addition, we invite you to attend the following presentation at PDAC, which includes Kris Raffle, P.Geo, a director of the Company, presenting on behalf of Defense Metals at 2:14 p.m.: Electric materials / Rare earth elements (REE), Room 801B – MTCC Level 800.

Qualified Person

The scientific and technical information contained in this news release, as it relates to the Wicheeda Rare-Earth Project, has been reviewed and approved by John Goode, P. Eng., who is a Qualified Person as defined by National Instrument 43-101 and who has provided the technical information relating to metallurgy in this news release.

About the Wicheeda REE Property

Defense Metals 100% owned, 4,262-hectare (~10,532-acre) Wicheeda REE property is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda REE Project is readily accessible by all-weather gravel roads and is near infrastructure, including hydro power transmission lines and gas pipelines. The nearby Canadian National Railway and major highways allow easy access to the port facilities at Prince Rupert, the closest major North American port to Asia.

The 2021 Wicheeda REE Project Preliminary Economic Assessment technical report (“PEA”) outlined a robust after-tax net present value (NPV@8%) of $517 million and an 18% IRR1. This PEA contemplated an open pit mining operation with a 1.75:1 (waste:mill feed) strip ratio providing a 1.8 Mtpa (“million tonnes per year”) mill throughput producing an average of 25,423 tonnes REO annually over a 16 year mine life. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

About Defense Metals Corp.

Defense Metals Corp. is a mineral exploration and development company focused on the acquisition, exploration and development of mineral deposits containing metals and elements commonly used in the electric power markets, defense industry, national security sector and in the production of green energy technologies, such as, rare earths magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals owns 100% of the Wicheeda Rare Earth Element Deposit located near Prince George, British Columbia, Canada. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, completion of the PFS, attending PDAC, the Company’s plans for its Wicheeda REE Project, expected results and outcomes from the comminution data, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration and metallurgical results, risks related to the inherent uncertainty of exploration and development and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological, metallurgical and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

1 Independent Preliminary Economic Assessment for the Wicheeda Rare Earth Element Project, British Columbia, Canada, dated January 6, 2022, with an effective date of November 7, 2021, and prepared by SRK Consulting (Canada) Inc. is filed under Defense Metals Corp.’s Issuer Profile on SEDAR (www.sedar.com).

Continued progress for programs targeting eye diseases with the submission of an IND application for OCU200

Expanded portfolio now includes inhaled vaccines for COVID-19, seasonal flu, and a combination COVID-19+seasonal flu vaccine

MALVERN, Pa., Feb. 28, 2023 (GLOBE NEWSWIRE) — Ocugen, Inc. (Ocugen or the Company) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today reported fourth quarter and full year 2022 financial results along with a general business update.

“We continue to grow and advance as a diversified biotechnology organization as reflected in our accomplishments of 2022,” said Dr. Shankar Musunuri, Chairman, Chief Executive Officer, and Co-Founder of Ocugen. “Our pipeline has been expanded to appropriately address the current challenges and gaps in the fight against COVID-19, application of OCU410 to address Stargardt (a rare eye disease), and our novel approach to address dry age-related macular degeneration (dAMD)—a disease affecting vision in over 266 million people worldwide.

“Following FDA concurrence in the fourth quarter of 2022 on a confirmatory Phase 3 clinical trial design for NeoCart®, we are developing internal capabilities to move our regenerative medicine asset, NeoCart®, into the clinic next year.”

“The FDA has granted expanded orphan drug designations to OCU400 for the treatment of retinitis pigmentosa (RP) and Leber congenital amaurosis (LCA),” said Dr. Musunuri. “These broad, gene-agnostic designations are encouraging at this stage in the development of OCU400.”

“During our first decade, we have built a strong foundation for addressing the diseases and conditions we aim to treat. We delivered on our promise to file an OCU200 IND in the first quarter of 2023 and look forward to delivering on important milestones in 2023, especially regarding preliminary efficacy data for gene therapy product OCU400, as we progress toward realizing our long-term vision to address unmet medical needs through courageous innovation,” Dr. Musunuri concluded.

Business Updates

Ophthalmic Gene Therapies

OCU400 – Established the high dose as the maximum tolerable dose, completed retinitis pigmentosa patient enrollment, and continuing to enroll patients with LCA to receive the high dose. Ocugen intends to initiate a Phase 3 clinical trial near the end of 2023.

OCU410 and OCU410ST – Executing IND-enabling studies and intend to submit IND applications in the second quarter of 2023 to initiate Phase 1/2 clinical trials in dry AMD (geographic atrophy) and Stargardt disease.

Ophthalmic Biologic Product

OCU200 – Submitted an IND application on February 27, 2023 to initiate a Phase 1 clinical trial targeting diabetic macular edema.

Regenerative Cell Therapies

NeoCart® – Received concurrence from the FDA on the confirmatory Phase 3 clinical trial design. Ocugen intends to initiate the Phase 3 clinical trial in the first half of 2024. Ocugen is renovating its facility to accommodate cGMP manufacturing of NeoCart® for clinical trials and beyond.

Vaccines Portfolio

OCU500 Series – Developing a novel mucosal vaccine platform which includes OCU500, a bivalent COVID-19 inhaled vaccine; OCU510, a seasonal quadrivalent flu inhaled vaccine; and OCU520 a combination quadrivalent seasonal flu and bivalent COVID-19 inhaled vaccine.

COVAXIN™ (BBV152) – Completed enrollment in Phase 2/3 immuno-bridging and broadening clinical trial in fourth quarter 2022.

Financial Results

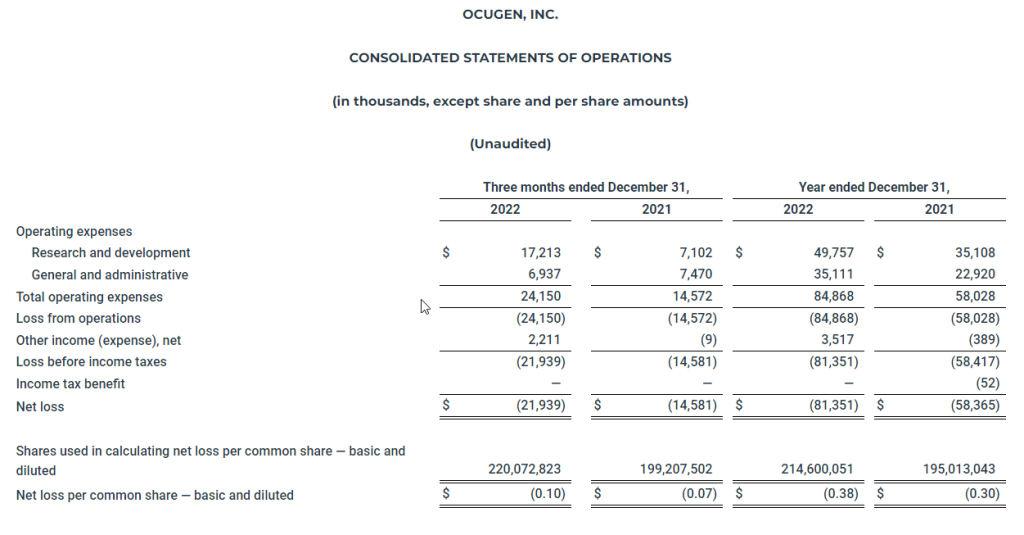

Fourth quarter — Research and development expenses for the three months ended December 31, 2022, were $17.2 million compared to $7.1 million for the three months ended December 31, 2021. General and administrative expenses for the three months ended December 31, 2022, were $6.9 million compared to $7.5 million for the three months ended December 31, 2021. Ocugen reported a $0.10 net loss per common share for the three months ended December 31, 2022, compared to a $0.07 net loss per common share for the three months ended December 31, 2021.

Full year — Research and development expenses for the year ended December 31, 2022, were $49.8 million compared to $35.1 million for the year ended December 31, 2021. General and administrative expenses for the year ended December 31, 2022, were $35.1 million compared to $22.9 million for the year ended December 31, 2021. Ocugen reported a $0.38 net loss per common share for the year ended December 31, 2022, compared to a $0.30 net loss per common share for the year ended December 31, 2021.

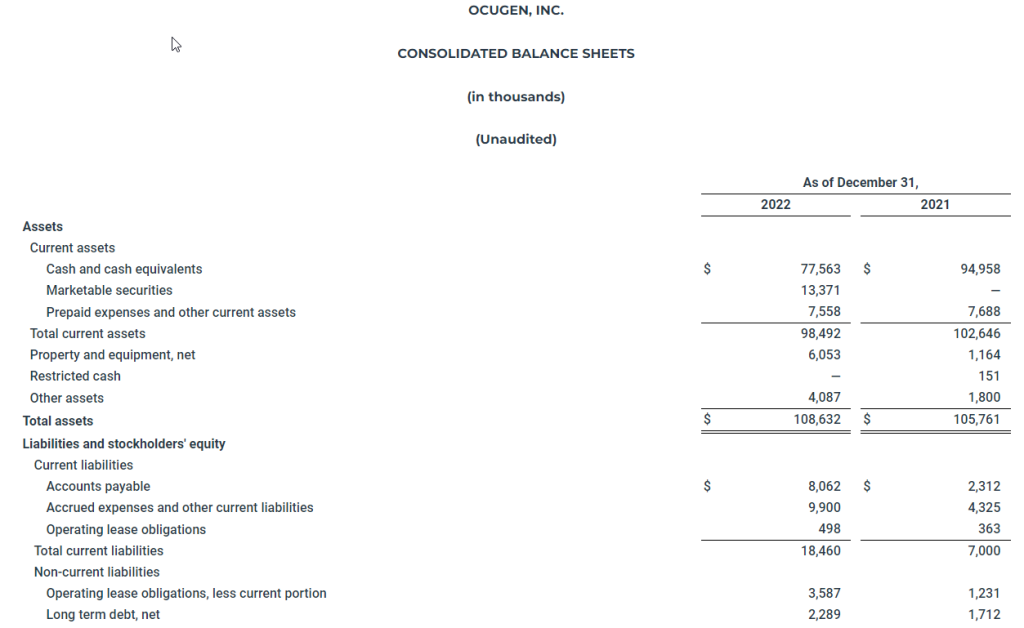

Ocugen’s cash, cash equivalents, restricted cash, and investments totaled $90.9 million as of December 31, 2022, compared to $95.1 million as of December 31, 2021. The Company estimates that its current cash, cash equivalents, and investments will enable it to fund its operations into the first quarter of 2024. The Company had 221.6 million shares of common stock outstanding as of December 31, 2022.

Conference Call and Webcast Details

Ocugen has scheduled a conference call and webcast for 8:30 a.m. ET today to discuss the financial results and recent business highlights. Ocugen’s senior management team will host the call, which will be open to all listeners. There will also be a question-and-answer session following the prepared remarks.

Attendees are invited to participate on the call or webcast using the following details:

Dial-in Numbers: (800) 715-9871 for U.S. callers and (646) 307-1963 for international callers Conference ID: 8912239 Webcast: Available on Ocugen’s investor site

A replay of the call and archived webcast will be available for approximately 45 days following the event on the Ocugen investor site.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs.

Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

MALVERN, Pa., Feb. 27, 2023 (GLOBE NEWSWIRE) — Ocugen, Inc. (“Ocugen” or the “Company”) (NASDAQ: OCGN), a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, today announced that it has submitted an Investigational New Drug application (IND) with the U.S. Food and Drug Administration (FDA) to initiate a Phase 1 clinical trial of OCU200, a fusion protein with a distinct mechanism of action (MOA), for the treatment of diabetic macular edema (DME). This regulatory milestone fulfills the Company’s commitment to file the IND for OCU200 within the first quarter of 2023.

“Today’s achievement is an important step towards fulfilling our mission to bring novel therapeutics to address limitations of the current standard of care or unmet medical needs in hard-to-treat blindness diseases,” said Dr. Arun Upadhyay, Chief Scientific Officer at Ocugen. “We are encouraged by the potential for OCU200 to provide a new treatment option for the significant percentage of people living with DME, including non-responders to the current standard of care.”

The planned Phase 1 clinical study will assess the unilateral intravitreal administration of OCU200 alone or in combination with an approved anti-VEGF therapy in participants with DME. This is a multicenter, open-label, dose-ranging study with 3 cohorts in the dose-escalation portion of the study and 1 cohort in the combination therapy portion of the study.

DME is one of the most common vision-threatening diseases occurring in people with diabetes and includes blurriness in vision and progressive vision loss as the disease progresses. Approximately 745,000 people in the United States are affected with DME, and this number is expected to further increase as the number of people with diabetes increases.

The Company intends to pursue additional indications for OCU200 to potentially treat diabetic retinopathy and wet age-related macular degeneration, which combined affect nearly 9.0 million Americans.

About Ocugen, Inc. Ocugen, Inc. is a biotechnology company focused on discovering, developing, and commercializing novel gene and cell therapies, biologics, and vaccines, that improve health and offer hope for patients across the globe. We are making an impact on patient’s lives through courageous innovation—forging new scientific paths that harness our unique intellectual and human capital. Our breakthrough modifier gene therapy platform has the potential to treat multiple retinal diseases with a single product, and we are advancing research in infectious diseases to support public health and orthopedic diseases to address unmet medical needs. Discover more at www.ocugen.com and follow us on Twitter and LinkedIn.

About OCU200 OCU200 is a novel fusion protein consisting of human transferrin linked to human tumstatin. It exerts anti-proliferative, anti-inflammatory, and anti-oxidative effects by selective targeting to the retinal and choroidal tissues. OCU200 potentially showcases better bioavailability and tissue penetrance than tumstatin alone due to transferrin and provides distinct MOA binding through αVβ3 integrin pathways that can potentially reduce the number of injections for patients.

OCU200 can potentially be used for the treatment of diabetic macular edema, diabetic retinopathy, and wet age-related macular degeneration. These diseases, combined, account for approximately 10 million cases in the U.S.

Forward-Looking Statements This press release contains forward-looking statements within the meaning of The Private Securities Litigation Reform Act of 1995, which are subject to risks and uncertainties. We may, in some cases, use terms such as “predicts,” “believes,” “potential,” “proposed,” “continue,” “estimates,” “anticipates,” “expects,” “plans,” “intends,” “may,” “could,” “might,” “will,” “should,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. Such statements are subject to numerous important factors, risks, and uncertainties that may cause actual events or results to differ materially from our current expectations. These and other risks and uncertainties are more fully described in our periodic filings with the Securities and Exchange Commission (SEC), including the risk factors described in the section entitled “Risk Factors” in the quarterly and annual reports that we file with the SEC. Any forward-looking statements that we make in this press release speak only as of the date of this press release. Except as required by law, we assume no obligation to update forward-looking statements contained in this press release whether as a result of new information, future events, or otherwise, after the date of this press release.

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced today that its Asia-based digital business unit has become the Authorized Sales Partner in Mongolia of Meta, the company that owns Facebook, Instagram and WhatsApp.

“This partnership reinforces our commitment to advertisers and their agencies to connect brands to consumers through local strategic support, creative expertise and relevant in-market training,” said Pieter-Jan de Kroon, Chief Executive Officer of Entravision Asia. “As we continue to expand our presence throughout Asia, we are thrilled to partner with Meta as their Authorized Sales Partner in Mongolia to equip and empower local businesses with the most advanced and effective advertising solutions.”

As an Authorized Sales Partner of Meta, Entravision will provide a dedicated local team, strategic direction, support, training, lines of credit and local billing to advertisers in the Mongolian market to enable them to meet their business objectives.

“Mongolia is an important country for Meta, and it is a priority for us to invest in the market and to be closer to the people and businesses here,” said Jordi Fornies, Managing Director of Emerging Markets for APAC at Meta. “As such, we are excited to introduce Entravision as Meta’s Authorized Sales Partner in Mongolia. With robust local expertise and insights, we can provide better support for businesses and agencies to help them to emerge from this challenging time stronger and further unlock their potential growth.”

About Entravision

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

About Meta

Meta builds technologies that help people connect, find communities, and grow businesses. When Facebook launched in 2004, it changed the way people connect. Apps like Messenger, Instagram, and WhatsApp further empowered billions around the world. Now, Meta is moving beyond 2D screens toward immersive experiences like augmented and virtual reality to help build the next evolution in social technology.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

Investors: Christopher T. Young Interim Chief Executive Officer 310-447-3870

Received guidance on registrational path for combination in recurrent/metastatic, immune checkpoint inhibitor refractory head and neck cancer

FLORHAM PARK, N.J., Feb. 27, 2023 (GLOBE NEWSWIRE) — PDS Biotechnology Corporation (Nasdaq: PDSB), a clinical-stage immunotherapy company developing a growing pipeline of targeted immunotherapies for cancer and infectious disease, announced the successful completion of a Type B meeting with the U.S. Food and Drug Administration (FDA) for a combination therapy of PDS0101, PDS0301 and an FDA-approved immune checkpoint inhibitor (ICI) for the treatment of recurrent/metastatic human papilloma virus (HPV)-positive, ICI refractory head and neck cancer. Head and neck cancers are the most common of all HPV-positive cancers and the number of cases is growing rapidly, according to the National Cancer Institute (NCI), one of the National Institutes of Health (NIH). There remains a critical unmet medical need to develop new treatment options for patients who have failed treatment with ICIs.

In recent interactions with the FDA, PDS Biotech has confirmed the required contents of the study design for a potential registrational trial of the combination of PDS0101, PDS0301 and a commercial immune checkpoint inhibitor. PDS0101, PDS Biotech’s lead candidate, is a Versamune® based investigational immunotherapy designed to stimulate a potent targeted T cell attack against HPV16-positive cancers. PDS0301 is a novel, proprietary investigational tumor-targeting fusion protein of Interleukin 12 (IL-12) that enhances the proliferation, potency and longevity of T cells in the tumor microenvironment, and is designed to overcome tumor immune suppression utilizing a different mechanism from checkpoint inhibitors. The combination of Versamune® and IL-12 is patented by PDS Biotech. In a National Cancer Institute (NCI)-led clinical trial in advanced HPV-positive ICI refractory patients, the combination of PDS0101 and PDS0301 administered with an investigational bi-functional ICI resulted in a median overall survival of 21 months, which compares favorably to the historical median survival of 3-4 months.

“We are pleased with the guidance from the FDA on key elements of a study design to progress the development of our assets, PDS0101 and PDS0301, in combination with a commercial immune checkpoint inhibitor,” said Dr. Frank Bedu-Addo, Chief Executive Officer of PDS Biotech. “This concurrence to substitute an FDA-approved commercially available ICI for the investigational agent studied in the NCI trial simplifies the regulatory pathway for this triple combination.”

Dr. Bedu-Addo continued, “Versamune® based investigational immunotherapies in combination with PDS0301 represent a potentially transformative treatment approach for recurrent/metastatic, ICI refractory cancer patients with poor survival prognosis. We remain committed to addressing unmet needs in cancer with more effective immunotherapy.”

About PDS0101 PDS0101, PDS Biotech’s lead candidate, is a novel investigational human papilloma virus (HPV)-targeted immunotherapy that stimulates a potent targeted T cell attack against HPV-positive cancers. PDS

Refinancing Expected to Strengthen Company’s Balance Sheet

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (NASDAQ: SALM) (the “Company”), today announced that it has issued an irrevocable notice of redemption (the “Notice”) to the trustee of its outstanding 6.75% Senior Secured Notes due 2024 (the “2024 Notes”). The Notice calls for the redemption in full of the remaining $36.5 million in outstanding aggregate principal amount of 2024 Notes.