Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

1Q 2026 financial results. Summit’s first quarter 2026 financial and operational results reflected continued strength in its Rockies and Permian segments, offset by weaker natural gas pricing, lower Mid-Con volumes, and higher interest expense. The company generated revenue of $139.1 million, adjusted EBITDA of $54.2 million, and free cash flow of $11.4 million. Net loss attributable to Summit Midstream Corporation amounted to $5.3 million, or $(0.43) per share, compared to a net loss of $1.9 million, or $(0.16) per share, in the first quarter of 2025, and our loss estimate of $6.1 million, or $(0.49) per share.

Updating estimates. We now forecast 2026 revenue of $584.8 million and adj. EBITDA of $241.4 million, compared to our prior estimates of $579.2 million and $245.2 million, respectively. First-quarter operational and financial results suggest that Summit’s earnings profile could strengthen progressively through the remainder of the year, with the second quarter expected to mark the beginning of a noticeable operational recovery, with the third and fourth quarters likely benefiting from accelerating volumes and improved commodity fundamentals. Management reiterated full-year 2026 adj. EBITDA guidance of $225 million to $265 million.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

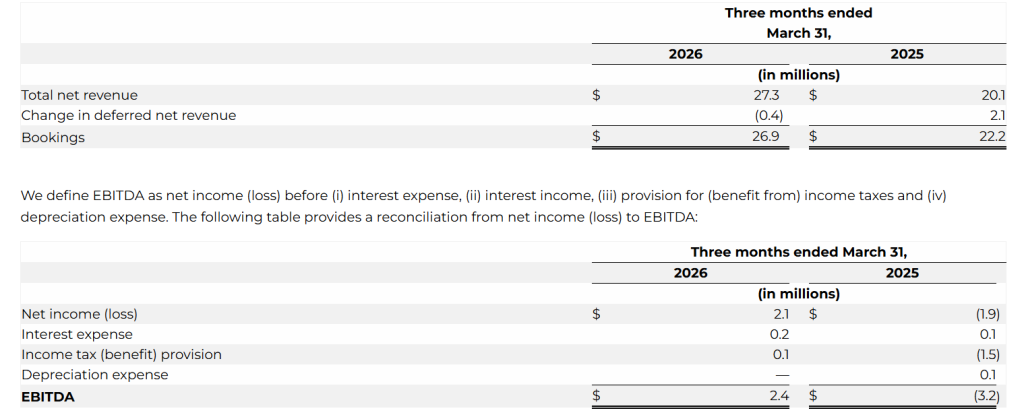

Strong Q1 results. The company reported Q1 revenue of $27.2 million and adj. EBITDA of $2.4 million, both of which surpassed our estimates of $18.0 million and a loss of $4.6 million, respectively. Notably, the favorable print was supported by increased ASA and Bellwright sales, as well as continued conversion of deferred revenue.

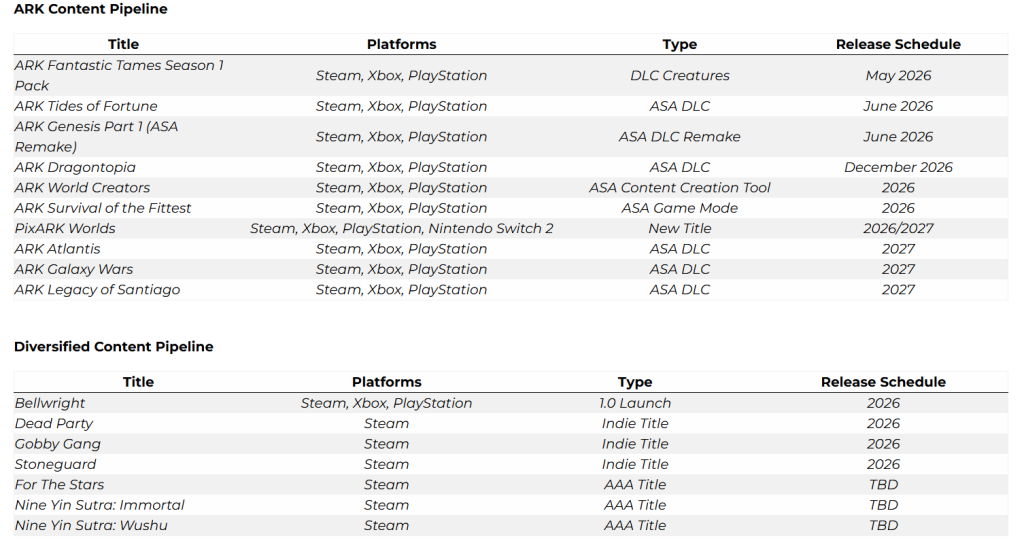

Busy release pipeline. The company has a busy release pipeline, with eleven internally developed projects and six licensed IP titles expected in the next 12-18 months. Notably, the pipeline includes multiple ASA content releases, the expansion of Bellwright to PlayStation and Xbox, and internally developed titles such as Gobby Game. Additionally, the company continues to advance its three AAA projects, For The Stars, Nine Yin Sutra: Immortal, and Nine Yin Sutra: Wushu, as part of its portfolio expansion strategy.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Mark Reichman, Managing Director, Equity Research Analyst, Natural Resources, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Thinking outside the box. Power Metallic has partnered with Ideon Technologies to deploy borehole muon tomography at the Lion Zone discovery within its Nisk polymetallic project in Quebec. The company intends to create a high-resolution three-dimensional model of the deposit by analyzing the behavior of naturally occurring cosmic ray particles. The technology is designed to validate results against more than 100 existing drill holes before expanding to district-scale exploration, potentially reducing the need for extensive drilling while reducing cost, time, and environmental impact.

Understanding the purpose. Muon tomography may be especially effective at Lion because the dense sulfide minerals within the deposit contrast sharply with surrounding host rocks, making the mineralization highly detectable. The six-month imaging program will map more than 55 million cubic meters of rock and establish a calibrated density signature that can be used to identify similar deposits hidden deeper underground beyond the reach of conventional geophysical methods.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before maki

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results largely in line with expectations. The company reported Q1 revenue of $517 million, down 1.4% year-over-year, while reporting a loss attributable to shareholders of $(18) million, or $(0.20) per share. Importantly, Local Media trends remained among the strongest in the industry, driven by sports advertising demand tied to the Winter Olympics, Super Bowl, and expanding NHL partnerships.

Local Media continues to outperform peers. Adjusted combined Local Media revenue increased 5.8% to $331 million, while core advertising revenue increased a healthy 7% to $137 million. Segment profit improved to $43.7 million from $32.3 million in the prior-year period despite modest expense growth, reflecting favorable operating leverage and strong advertiser demand.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

CULVER CITY, Calif., May 13, 2026 (GLOBE NEWSWIRE) — Snail, Inc. (Nasdaq: SNAL) (“Snail Games” or the “Company”), a leading global independent developer and publisher of interactive digital entertainment, today announced financial results for the first quarter ended March 31, 2026.

First Quarter 2026 and Recent Operational Highlights

ARK Franchise Updates:

ARK: Survival Evolved (“ASE”):

Units sold were approximately 573,000 for the first quarter of 2026

During the first quarter of 2026, average daily active users (“DAU”) was 117,000 and peak DAU was 143,000

ARK: Survival Ascended (“ASA”):

Units sold were approximately 1.4 million for the first quarter of 2026

During the first quarter of 2026, average DAU was 127,000 and peak DAU was 188,000

ARK: Ultimate Mobile Edition (“ARK Mobile”):

11.9 million downloads as of March 31, 2026

During the first quarter of 2026, average DAU was 141,000

Game Portfolio and Business Updates:

For The Stars

Released new developer diary, offering an in-depth look at the upcoming AAA title’s current development progress, including new pre-alpha footage and previously unreleased concept art

Revealed event-exclusive trailer during 2026 Games Developers Conference (“GDC”)

Introduced PixARK Worlds, a new title in development that features revolutionary user-generated content designed to further expand the ARK universe on Steam, Xbox, PlayStation, and the Nintendo Switch 2

Bellwright

Surpassed 1 million downloads on Steam Early Access, announced console port plans to Xbox and PlayStation, and launched the Maiden Voyage update.

Launched Echoes of Elysium on Steam Early Access in partnership with Loric Games

Launched Survivor Merc’s 1.0 version across Steam, Xbox, and PlayStation

Launched Above the Snow on Steam

Announced publishing agreement for co-op party action title Dead Party

Unveiled new upcoming indie title, Gobby Gang, at 2026 GDC

As of March 31, 2026, SaltyTV released 250+ short film dramas

ARK Content Pipeline

Management Commentary

“We exited 2025 with tailwinds that positioned Snail for stronger and more stable growth and results,” said Company CEO Hai Shi. “Momentum from the ASA pipeline we announced in December, the launch of ARK Lost Colony DLC, and the subsequent Steam Winter Sale event supported net revenue growth and a return to net income positive. Looking ahead, we aim to deliver year-over-year growth in Q2, driven by several upcoming ARK content releases. We have a Fantastic Tames Season 1 Expansion Pack coming in May 2026, and ARK Tides of Fortune to launch alongside the remake of Genesis Part 1 coming to ASA in June 2026 to provide a foundation for the quarter to build on. Approximately $11 million from our deferred revenue backlog is expected to be recognized upon the release of Genesis Part 1.

“Beyond ARK, Snail Games continues to execute on its strategy to eventually become a fully integrated game developer and publisher. Our upcoming AAA titles represent an important step toward building new franchises with the potential for multi-year to multi-decade game lifespans that can complement the scale of ASE and ASA. As previously disclosed, these projects have entered their final phases of development, and the eventual launch of these games position us to meaningfully diversify our revenue mix beyond ARK. With multiple gaming events and planned updates throughout the year, we look forward to sharing additional information on For the Stars, Nine Yin Sutra: Immortal, and Nine Yin Sutra: Wushu.

“The next 12-18 months will serve as an inflection period for Snail Games as we work to advance our ARK pipeline and deliver on the investments we have made across our broader pipeline. Over time, our ambition is for Snail Games to be recognized not only for ARK, but as a developer and publisher of multiple renown IPs and titles. We remain focused on unlocking the value of our pipeline and delivering results.”

First Quarter 2026 Financial Highlights

Net revenues increased 35.7% to $27.3 million compared to $20.1 million in the same period last year. The increase was primarily due to an increase of $4.2 million and $2.1 million in revenue related to ASA and Bellwright, respectively, and a $2.5 million increase in deferred revenue recognized during the period, offset by a decrease in revenue from ARK Mobile and ASE of $1.6 million.

Total units sold increased 42.6% to 2.2 million units compared to 1.5 million units in the same period last year, primarily driven by an increase in sales of ARK franchise IPs of 0.5 million units and Bellwright of 0.2 million units.

Net income increased 210% to $2.1 million compared to a net loss of $1.9 million in the same period last year. The increase was primarily due to an increase in net revenue of $7.2 million and a decrease in total operating expenses of $0.3 million partially offset by an increase in provision for income taxes of $1.6 million, an increase in cost of revenues of $1.4 million and a decrease in total other income, net of $0.5 million.

Bookings increased 21.1% to $26.9 million compared to $22.2 million in the same period last year. The increase was primarily due to better sales promotions in 2026 compared to 2025, tailwind momentum from the December 2025 ARK: Lost Colony DLC release, and Bellwright’s highly regarded content update in late 2025.

EBITDA increased 173.3% to $2.4 million compared to $(3.2) million in the same period last year. The increase was primarily due to an increase in net income of $4.1 million and a decrease in the benefit from income taxes of $1.6 million.

As of December 31, 2025, unrestricted cash was $14.3 million compared to $8.6 million as of December 31, 2025.

Use of Non-GAAP Financial Measures

In addition to the financial results determined in accordance with U.S. generally accepted accounting principles, or GAAP, Snail believes Bookings and EBITDA, as non-GAAP measures, are useful in evaluating its operating performance. Bookings and EBITDA are non-GAAP financial measures that are presented as supplemental disclosures and should not be construed as alternatives to net income (loss) or revenue as indicators of operating performance, nor as alternatives to cash flow provided by operating activities as measures of liquidity, both as determined in accordance with GAAP. Snail supplementally presents Bookings and EBITDA because they are key operating measures used by management to assess financial performance. Bookings adjusts for the impact of deferrals and, Snail believes, provides a useful indicator of sales in a given period. Management believes Bookings and EBITDA are useful to investors and analysts in highlighting trends in Snail’s operating performance, while other measures can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which Snail operates and capital investments.

Bookings is defined as the net amount of products and services sold digitally or physically in the period. Bookings is equal to revenues, excluding the impact from deferrals. Below is a reconciliation of total net revenue to Bookings, the closest GAAP financial measure.

Webcast Details

The Company will host a webcast at 4:30 PM ET today to discuss its first quarter 2026 financial and operational results. Participants may access the live webcast and replay via the link here or on the Company’s investor relations website at https://investor.snail.com/.

About Snail, Inc.

Snail, Inc. (Nasdaq: SNAL) is a leading, global independent developer and publisher of interactive digital entertainment for consumers around the world, with a premier portfolio of premium games designed for use on a variety of platforms, including consoles, PCs, and mobile devices. For more information, please visit: https://snail.com/.

Forward-Looking Statements

This press release contains statements that constitute forward-looking statements. Many of the forward-looking statements contained in this press release can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “may,” “predict,” “continue,” “estimate” and “potential,” or the negative of these terms or other similar expressions. Forward-looking statements appear in a number of places in this press release and include, but are not limited to, statements regarding Snail’s intent, belief or current expectations. These forward-looking statements include information about possible or assumed future results of Snail’s business, financial condition, results of operations, liquidity, plans and objectives. The statements Snail makes regarding the following matters are forward-looking by their nature: exiting 2025 with tailwinds that position the Company for stronger and more stable growth and results; delivering year-over-year growth in Q2 driven by several upcoming ARK content releases; releasing Fantastic Tames Season 1 Expansion Pack in May 2026 and ARK Tides of Fortune alongside the remake of Genesis Part 1 coming to ASA in June 2026 providing a foundation for the quarter to build on; recognizing approximately $11 million of deferred revenue backlog upon the release of Genesis Part 1; continuing to execute on the Company’s strategy to become a fully integrated game developer and publisher; the upcoming AAA titles representing an important step toward building new franchises with the potential for multi-year to multi-decade game lifespans that can complement the scale of ASE and ASA; the eventual launch of the upcoming games positioning the Company to meaningfully diversify our revenue mix beyond ARK; sharing additional information on For the Stars, Nine Yin Sutra: Immortal, and Nine Yin Sutra: Wushu; the next 12-18 months being an inflection period for the Company as it advances its ARK pipeline and delivers on the investments it has have made across its broader pipeline; the Company being recognized not only for ARK, but as a developer and publisher of multiple renown IPs and titles; and remaining focused on unlocking the value of the Company pipeline and delivering results.

Any forward-looking statements included herein reflect our current views, and they involve certain risks and uncertainties, including, among others, acceptance of our titles in the marketplace and the successful development, marketing or sale of our titles and our ability to retain our key employees or maintain our Nasdaq listing. These risks should not be construed as exhaustive and should be read together with the other cautionary statement included in our Annual Report on Form 10-K for the year ended December 31, 2025, subsequent Quarterly Reports on Form 10-Q and current reports on Form 8-K filed with the Securities and Exchange Commission. Any forward-looking statement speaks only as of the date on which it was initially made. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances or otherwise, unless required by law.

Investor Contact:

John Yi and Steven Shinmachi Gateway Group, Inc. 949-574-3860 [email protected]

100% insulin independence achieved in 10 patients with type 1 diabetes treated with tegoprubart following islet transplantation in UChicago Medicine-led study

FDA Orphan Drug designation granted to tegoprubart for the prevention of allograft rejection in liver transplantation

Cash, cash equivalents and short-term investments totaled $111.1 million as of March 31, 2026

IRVINE, Calif., May 13, 2026 (GLOBE NEWSWIRE) — Eledon Pharmaceuticals, Inc. (“Eledon”) (Nasdaq: ELDN) today reported its first quarter 2026 operating and financial results and provided recent business highlights.

“In the first quarter of 2026, we achieved significant milestones in our tegoprubart program, including important data updates in kidney and islet cell transplantation and FDA Orphan Drug designation for tegoprubart in liver transplantation,” said David-Alexandre C. Gros, M.D., Chief Executive Officer of Eledon. “Looking ahead, we expect multiple catalysts in 2026, including regulatory engagements supporting the advancement of tegoprubart into Phase 3 development in kidney transplantation and discussions regarding a potential path to market in islet cell transplantation. We also plan to initiate several new clinical trials, including an investigator sponsored study in liver transplantation, and share new kidney transplant data from our Phase 2 BESTOW long-term extension study, building on encouraging 24-month Phase 1b results that demonstrated a durable safety profile and improved graft function.”

First Quarter 2026 Business Highlights

In March 2026, announced updated results from an ongoing investigator-led trial at the University of Chicago Medicine Transplant Institute evaluating tegoprubart in 12 adults with high-risk type 1 diabetes undergoing allogenic islet transplantation. All 10 patients who are more than four weeks post-transplant achieved 100% insulin independence. There were no signs of graft rejection or de novo donor-specific HLA antibodies and no evidence of nephrotoxicity, hypertension, or neurotoxicity, which are commonly associated with tacrolimus-based immunosuppression regimens, the current standard of care.

The U.S. Food and Drug Administration (FDA) granted Orphan Drug designation to tegoprubart for the prevention of allograft rejection in liver transplantation.

Presented 24-month follow-up data from eight patients enrolled in the Phase 1b trial long-term extension trial evaluating tegoprubart in kidney transplantation at the American Society of Transplant Surgeons Winter Symposium in January 2026. Results showed there were no episodes of biopsy-proven acute rejection, graft loss, death, new-onset diabetes mellitus, or de novo donor-specific antibody formation during the study period. Mean estimated glomerular filtration rate (eGFR) increased over the measurement period, from 67.0 mL/min/1.73 m2 at 12 months to 74.2 mL/min/1.73 m2 at 24 months.

2026 Anticipated Upcoming Milestones

Receive FDA guidance on the Phase 3 trial design assessing tegoprubart in kidney transplantation, followed by initiation of the Phase 3 trial pending regulatory alignment.

Report long-term data from Phase 1b and Phase 2 BESTOW studies evaluating tegoprubart in kidney transplantation.

Receive FDA regulatory guidance on the path to market for tegoprubart in islet cell transplantation and xenotransplantation.

Initiate an investigator-led study evaluating tegoprubart for the prevention of organ rejection in patients with renal dysfunction receiving an islet cell transplant.

Initiate an investigator-led study evaluating tegoprubart for the prevention of organ rejection in patients receiving a de novo liver transplant.

Initiate an investigator-led study evaluating tegoprubart for kidney transplant tolerance induction.

First Quarter 2026 Financial Results

Cash, cash equivalents and short-term investments totaled $111.1 million as of March 31, 2026, compared to $133.3 million as of December 31, 2025. The company expects current cash, cash equivalents and short-term investments to fund operations into 2Q 2027.

Research and development (R&D) expenses for the first quarter of 2026 were $17.2 million, including $1.1 million of non-cash stock-based compensation expense, compared to $13.5 million, including $1.0 million of non-cash stock-based compensation expense, for the comparable period in 2025.

General and administrative (G&A) expenses for the first quarter of 2026 were $4.0 million, including $1.1 million of non-cash stock-based compensation expense, compared to $4.4 million, including $1.8 million of non-cash stock-based compensation expense, for the comparable period in 2025.

Net loss for the first quarter of 2026 was $39.0 million, or $0.33 per basic common share, compared to a net loss of $6.5 million, or $0.08 per basic common share, for the comparable period in 2025. Net loss in the first quarter of 2026 included a non-cash loss of $19.0 million from changes in the fair value of warrant liabilities, while the 2025 net loss included a non-cash gain of $10.1 million from such changes. Excluding the non-cash items related to changes in the fair value of warrant liabilities, Eledon would have recorded a net loss of $20.1 million for the three months ended March 31, 2026, and $16.6 million for the three months ended March 31, 2025.

About Eledon Pharmaceuticals and tegoprubart

Eledon Pharmaceuticals, Inc. is a clinical stage biotechnology company that is developing immune-modulating therapies for the management and treatment of life-threatening conditions. The Company’s lead investigational product is tegoprubart, an anti-CD40L antibody with high affinity for the CD40 Ligand, a well-validated biological target that has broad therapeutic potential. The central role of CD40L signaling in both adaptive and innate immune cell activation and function positions it as an attractive target for non-lymphocyte depleting, immunomodulatory therapeutic intervention. The Company is building upon a deep historical knowledge of anti-CD40 Ligand biology to conduct preclinical and clinical studies in kidney allograft transplantation, xenotransplantation, islet cell transplantation, liver transplantation and amyotrophic lateral sclerosis (ALS). Eledon is headquartered in Irvine, California. For more information, please visit the Company’s website at www.eledon.com.

Follow Eledon Pharmaceuticals on social media: LinkedIn; X

Forward-Looking Statements

This press release contains forward-looking statements that involve substantial risks and uncertainties. Any statements about the company’s future expectations, plans and prospects, including statements about planned clinical trials, the development of product candidates, expected timing for initiation of future clinical trials, expected timing for receipt of data from clinical trials, the company’s capital resources and ability to finance planned clinical trials, as well as other statements containing the words “believes,” “anticipates,” “plans,” “expects,” “estimates,” “intends,” “predicts,” “projects,” “targets,” “looks forward,” “could,” “may,” and similar expressions, constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are inherently uncertain and are subject to numerous risks and uncertainties, including: our short operating history and shifts in our business strategy; our operating losses since inception; our need for additional funding to develop our lead drug candidate and our ability to secure additional funding on acceptable terms or at all; the impact of issuances of our common stock, including in the possibility of dilution or a decline in our stock price; our ability to successfully develop our product candidates; unfavorable global economic and financial market conditions; the regulatory environment of our business and our ability to obtain required regulatory approvals; results of non-clinical studies and clinical trials, and risks that non-clinical studies or early clinical trials may not be predictive of results of later-stage clinical trials; delays or difficulties in enrollment of patients in clinical trials; our ability to attract and retain our executives and key employees; legislation of the pharmaceutical and healthcare industries; cybersecurity and data privacy risks; the ability of our products to achieve marketing approval; competition in our industry; our ability to obtain

insurance coverage; our dependence on contract research organizations; our ability to protect our intellectual property; public health crises; our ability to maintain proper and effective internal control over financial reporting and other risks disclosed in our Annual Report on Form 10-K for the year ended December 31, 2025, filed with the Securities and Exchange Commission on March 19, 2026. Actual results may differ materially from those indicated by such forward-looking statements as a result of various factors. These risks and uncertainties, as well as other risks and uncertainties that could cause the company’s actual results to differ materially from the forward-looking statements contained herein, are discussed in our Annual 10-K, and other filings with the U.S. Securities and Exchange Commission, which can be found at www.sec.gov. Any forward-looking statements contained in this press release speak only as of the date hereof and not of any future date, and the company expressly disclaims any intent to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Company Expands Strategic Immuno-Oncology Positioning Around Tumor Microenvironment Modulation, Checkpoint Enhancement, and Multi-Tumor Development Potential

ATLANTA, GA – May 13, 2026 – GeoVax Labs, Inc. (Nasdaq: GOVX), a clinical-stage biotechnology company developing immunotherapies and vaccines for solid tumors and infectious diseases, today highlighted the expanding strategic relevance of its Gedeptin® immuno-oncology program within the rapidly evolving landscape of combination immunotherapy and checkpoint inhibitor enhancement strategies.

GeoVax believes Gedeptin’s unique mechanism of localized tumor destruction combined with immune activation positions the program within a growing area of oncology focus: therapies designed to overcome immune resistance and enhance responsiveness to checkpoint inhibitors in immunologically “cold” tumors.

Checkpoint inhibitors targeting PD-1 and PD-L1 have transformed cancer treatment across multiple tumor types; however, many solid tumors remain insufficiently responsive due to immune-suppressive tumor microenvironments, inadequate immune-cell infiltration, and incomplete tumor antigen recognition. As a result, oncologists are increasingly focused on combination approaches capable of improving checkpoint inhibitor response rates and extending durability of benefit.

“Modern immuno-oncology is increasingly shifting toward combination strategies designed to improve the effectiveness of checkpoint inhibitors across broader patient populations,” said David Dodd, Chairman and Chief Executive Officer of GeoVax. “We believe Gedeptin aligns directly with this trend by functioning not simply as a localized tumor therapy, but as a potential immune-sensitization platform capable of enhancing anti-tumor immune responses in tumors where checkpoint inhibitors alone may be insufficient.”

Key characteristics of the Gedeptin platform include:

Tumor-agnostic mechanism of action independent of tumor histology or proliferation rate;

Strong bystander effect, allowing destruction of neighboring tumor cells even when only a fraction are directly transduced;

Tumor microenvironment remodeling and immune activation, potentially enhancing tumor recognition by the immune system;

Potential checkpoint sensitization, supporting combination strategies with PD-1 and PD-L1 inhibitors;

Compatibility with image-guided and intratumoral delivery approaches across multiple solid tumor settings.

GeoVax’s lead development focus for Gedeptin is a planned neoadjuvant combination study in recurrent head and neck squamous cell carcinoma (HNSCC), evaluating intratumoral Gedeptin together with PD-1 targeting immunotherapy in patients eligible for curative-intent surgery. The study is expected to evaluate pathologic response, immune biomarker modulation, and early event-free survival signals.

“The oncology field is increasingly recognizing that durable checkpoint inhibitor responses may require direct modulation of the tumor microenvironment in addition to checkpoint blockade alone,” continued Mr. Dodd. “We believe Gedeptin’s ability to induce localized tumor destruction while simultaneously promoting immune activation creates a compelling rationale for combination development approaches designed to broaden and deepen immunotherapy responses. Importantly, we believe this mechanism may ultimately extend beyond localized disease settings and support broader applicability across metastatic solid tumors where immune resistance remains a major therapeutic challenge.”

Beyond head and neck cancer, GeoVax believes Gedeptin may have broader applicability across solid tumors characterized by:

established checkpoint inhibitor treatment paradigms,

and at least one lesion amenable to intratumoral or image-guided delivery.

Potential future tumor targets under evaluation include melanoma, triple-negative breast cancer, cutaneous malignancies, and additional metastatic solid tumor settings.

“As the oncology landscape evolves beyond single-agent checkpoint inhibition toward increasingly sophisticated combination approaches, we believe therapies capable of enhancing immune recognition and overcoming tumor resistance mechanisms may become increasingly important,” added Mr. Dodd. “Our objective is to position Gedeptin within that emerging therapeutic landscape as a differentiated immune-enabling platform with potential applicability across multiple solid tumor indications.”

About Gedeptin®

Gedeptin® is GeoVax’s proprietary gene-directed enzyme prodrug therapy (GDEPT) platform under development for the treatment of solid tumors. The therapy is designed for intratumoral administration and utilizes a non-replicating adenoviral vector to deliver purine nucleoside phosphorylase (PNP) directly into tumor tissue. Following administration of fludarabine, the PNP enzyme converts the prodrug into a potent localized cytotoxic agent that destroys tumor cells while simultaneously generating immune-activating signals within the tumor microenvironment.

GeoVax is advancing development plans to evaluate Gedeptin in combination with immune checkpoint inhibitors, including pembrolizumab, with the goal of amplifying anti-tumor immune activation and broadening therapeutic applicability across multiple solid tumor indications.

About GeoVax

GeoVax Labs, Inc. is a clinical-stage biotechnology company focused on the development of vaccines and immunotherapies addressing high-consequence infectious diseases and solid tumor cancers. GeoVax’s priority program is GEO-MVA, a Modified Vaccinia Ankara (MVA)-based vaccine targeting mpox and smallpox. The program is advancing under an expedited regulatory pathway, with plans to initiate a pivotal Phase 3 clinical trial in the second half of 2026, to address critical global needs for expanded orthopoxvirus vaccine supply and biodefense preparedness. In oncology, GeoVax is developing Gedeptin®, a gene-directed enzyme prodrug therapy (GDEPT) designed to enhance immune checkpoint inhibitor activity. Gedeptin has completed a multicenter Phase 1/2 clinical trial in advanced head and neck cancer and is being advanced into combination strategies, including planned neoadjuvant and first-line settings. GeoVax’s broader pipeline includes the development of GEO-CM04S1, a next-generation COVID-19 vaccine candidate being evaluated in immunocompromised and other patient populations. GeoVax maintains a global intellectual property portfolio supporting its infectious disease and oncology programs and continues to evaluate strategic partnerships and funding opportunities aligned with its development priorities. For more information, visit www.geovax.com.

Forward-Looking Statements

This release contains forward-looking statements regarding GeoVax’s business plans. The words “believe,” “look forward to,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “could,” “target,” “potential,” “is likely,” “will,” “expect” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Actual results may differ materially from those included in these statements due to a variety of factors, including whether: GeoVax is able to obtain acceptable results from ongoing or future clinical trials of its investigational products, GeoVax’s immuno-oncology products and preventative vaccines can provoke the desired responses, and those products or vaccines can be used effectively, GeoVax’s viral vector technology adequately amplifies immune responses to cancer antigens, GeoVax can develop and manufacture its immuno-oncology products and preventative vaccines with the desired characteristics in a timely manner, GeoVax’s immuno-oncology products and preventative vaccines will be safe for human use, GeoVax’s vaccines will effectively prevent targeted infections in humans, GeoVax’s immuno-oncology products and preventative vaccines will receive regulatory approvals necessary to be licensed and marketed, GeoVax raises required capital to complete development, there is development of competitive products that may be more effective or easier to use than GeoVax’s products, GeoVax will be able to enter into favorable manufacturing and distribution agreements, and other factors, over which GeoVax has no control.

Further information on our risk factors is contained in our periodic reports on Form 10-Q and Form 10-K that we have filed and will file with the SEC. Any forward-looking statement made by us herein speaks only as of the date on which it is made. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

TORONTO, May 13, 2026 /CNW/ – Power Metallic Mines Inc. (the “Company” or “Power Metallic”) (TSXV: PNPN) (OTCBB: PNPNF) (Frankfurt: IVV1) is pleased to announce an engagement with Vancouver-based Ideon Technologies (“Ideon”) to activate a borehole muon tomography imaging program at the Lion Zone discovery within the Nisk Polymetallic project area in Quebec, Canada. A global leader in subsurface intelligence, the Ideon REVEAL™ solution will generate a high-resolution, three-dimensional density model of the rock composition in and around the Lion deposit.

Figure 1 – Plan view of muon survey overlain Lion (CNW Group/Power Metallic Mines Inc.)Figure 2: Long section of muon survey overlain Lion (CNW Group/Power Metallic Mines Inc.)Figure 3 – An example of a density model showing alignment with historic drilling and illumination of new exploration targets, from a muon program conducted at Fireweed Metals’ Macmillan Pass District, Yukon Territory. https://ideon.ai/results/fireweed-metals-macpass/ (CNW Group/Power Metallic Mines Inc.)Figure 4: High-density iso-surfaces of BHP’s Nickel West from muon tomography data (blue) are identified within the survey region of interest. The joint inversion of airborne, ground gravity and muon tomography (green) is also shown. The main N-S trending structure is clearly aligned with a mafic intrusion, as described earlier. The massive sulphide structure to the East is seen in the muon tomography inversion, but is not apparent in the gravity inversions – though there is some slight density variation seen in the airborne data. The joint inversion is very compatible with the presence of the massive sulphide. https://ideon.ai/results/bhp-leinster-mine/ (CNW Group/Power Metallic Mines Inc.)

The program is structured in two stages: first, validating the Ideon density model against Power Metallic’s existing 100-plus hole drill dataset at Lion; then applying the calibrated mineralization fingerprint to rank and test deep targets across the 330 km² Nisk district scale property that are below the detection limit of conventional surface-based geophysical methods (i.e., below 200 m).

About the Technology: Seeing Deep into the Earth using Energy from Space

The Ideon REVEAL™ Platform detects cosmic-ray muons — naturally occurring subatomic particles created by supernova explosions in deep space. Muons lose energy progressively in direct proportion to the density of the material they pass through. By positioning arrays of muon detectors in boreholes at varying depths, Ideon can construct 3D tomographic models of subsurface density over millions of cubic metres of earth, potentially replacing hundreds of drillholes while providing greater subsurface visibility at a fraction of the cost and time, and with significantly less environmental impact.

The Ideon REVEAL™ Platform and is designed for the most demanding of exploration and mining environments. It uses proprietary hardware, software and imaging systems with advanced AI-powered analysis and data fusion capabilities. It has been field-proven at some of the world’s most demanding mine sites, including at Rio Tinto’s Kennecott Utah Copper operation at Bingham Canyon, BHP’s Nickel West and Olympic Dam mines in Australia, Vale Base Metals’ Creighton and Totten mines in Sudbury, Ontario, and Fireweed Metals’ remote Macmillan Pass District in the Yukon Territory.

Why Lion Is an Exceptional Muon Target

The mineralogy of the Lion Zone is ideally suited to muon tomography. The deposit’s high-grade core is dominated by massive to brecciated chalcopyrite, cubanite, pyrrhotite, pentlandite, and pyrite — minerals with bulk densities of 4.0 to 5.0+ g/cc. These contrast sharply with the surrounding felsic, mafic and ultramafic host rocks, which carry background densities of approximately 2.8 to 3.0 g/cc. The Ideon solution will be used to produce 3D density models of individual dipping stratigraphic horizons and potential extensions of the deposit at multi-metre scale resolution.

The initial phase of the program will deploy borehole muon detectors into dedicated drill holes at the Lion Zone. The imaging program will run autonomously, passively and continuously collecting data over several months and delivering to Power Metallic a three-dimensional density model of the deposit. This phase will be conducted blindly, meaning that no constraining data (other than surface topography) will be provided.

In total the survey will map the density of over 55,000,000 m3 of rock volume. The imaging program is planned to run for 6 months in duration, with the option to extend to 8 months if needed to optimize resolution and establish the Lion Zone ore signature.

The Lion imaging program is designed as a validation exercise. Power Metallic holds an extensive drill dataset at Lion built from more than 100 holes across multiple campaigns. By producing an unconstrained muon inversion and then comparing it directly against the known resource model, the Company will establish the geophysical fingerprint of a Lion-style polymetallic massive sulfide system. Once the density signature of Lion mineralization is confirmed to match the tomographic model, that calibrated signature will become the search template for the broader Nisk project district.

District Scale: Opening a New Search Space

The most transformative potential of this program lies beyond Lion itself.

Power Metallic’s Nisk project encompasses ~330 km² of land including approximately 20 km of strike on the northern basin margin and 30 km on the southern basin margin — a contiguous belt hosting the Nisk Main deposit, the Lion discovery, and numerous additional untested geophysical anomalies. To date, surface and near-surface exploration methods including airborne magnetics, ground gravity, and Airborne EM have provided effective screening tools for targets shallower than approximately 200 m depth. Below that threshold, surface-based techniques are unable to detect deposit-scale targets.

“One of the challenges in exploring any deposit is false positives. Borehole EM continues to be the gold standard, but increasingly we are looking to combine it with other techniques that can image thicker mineralization. We are excited to integrate our current best practice workflow with muon tomography, a technique that’s demonstrated it can discover thicker intersections of sulfides. By incorporating an additional physical property beyond BHEM, we aim to improve our probability of target success and better discriminate high-quality conductors. We are always striving to discover better ore, not just more ore.” commented Steve Beresford, Director.

Muon tomography will be used to target a search space below 200 meters. Ideon muon sensors can image key geological features in the deep subsurface extending the effective targeting depth range where the next Lion-scale discovery may be hiding.

The geological rationale for deep exploration at Nisk is compelling. The Tiger Zone, located approximately 700 m east of Lion, has already returned Lion-style polymetallic mineralization, confirming the mineralizing system is not confined to Lion alone. The 5.5-km corridor between Lion and Nisk Main remains largely untested at depth. Company geologists have interpreted an easterly plunging structural control on high-grade Lion mineralization that acts as a vector toward a potential source body at greater depth. Regional structural analysis has identified a fold-hinge zone on newly acquired ground that covers an extension of the Lion mineralizing system previously outside the property boundary.

Once a validated muon signature of Lion mineralization is in hand, Power Metallic intends to conduct phased muon surveys across priority targets within this district, applying the calibrated density fingerprint of its known deposit type to rank and test anomalies that otherwise would have to be evaluated with blind drilling.

Learn more about how muon tomography works at this link.

“We have been excited about Nisk’s geological potential for many years and of course with the amazing success of the Lion Zone Discovery we entered a new frontier. With the guidance of our technical director Steve Beresford and the Geovector team led by our VP of Exploration Joe Campbell we have continuously pushed the targeting envelope to discover thicker massive Cu-PGE sulfides. Historically we know the polymetallic discoveries around the world are some of the largest and most profitable mines ever discovered. These discoveries are an order of magnitude bigger than what we have currently discovered. Even the smallest polymetallic discovery is more than 50% larger. What that means in practical terms is we have probably only scratched the surface at Nisk. Even as we are planning to publish our inaugural MRE (Mineral Resource Estinate) this summer to demonstrate that the current discoveries have exciting commercial potential, we remain focused on uncovering Nisk’s full potential. Our team believes that muon tomography is the next tool that can accelerate our discovery process and everything I have seen makes me confident that they have once again chosen wisely.” commented Terry Lynch, CEO & Director.

Qualified Person

Joseph Campbell, P. Geo, VP Exploration at Power Metallic, is the qualified person who has reviewed and approved the technical disclosure contained in this news release.

About Power Metallic Mines Inc.

Power Metallic is a Canadian exploration company focused on advancing the Nisk Project Area (Nisk–Lion–Tiger)–a high–grade Copper–PGE, Nickel, gold and silver system–toward Canada’s next polymetallic mine.

On 1 February 2021, Power Metallic (then Chilean Metals) secured an option to earn up to 80% of the Nisk project from Critical Elements Lithium Corp. (TSX–V: CRE). Following the June 2025 purchase of 313 adjoining claims (~167 km²) from Li–FT Power, the Company now controls ~330 km² and roughly 50 km of prospective basin margins.

Power Metallic is expanding mineralization at the Nisk and Lion discovery zones, evaluating the Tiger target, and exploring the enlarged land package through successive drill programs. Beyond the Nisk Project Area, Power Metallic indirectly has an interest in significant land packages in British Columbia and Chile, by its 50% share ownership position in Chilean Metals Inc., which were spun out from Power Metallic via a plan of arrangement on February 3, 2025.

It also owns 100% of Power Metallic Arabia which owns 100% interest in the Jabul Baudan exploration license in The Kingdon of Saudi Arabia’s Jabal Said Belt. The property encompasses over 200 square kilometres in an area recognized for its high prospectivity for copper gold and zinc mineralization. The region is known for its massive volcanic sulfide (VMS) deposits, including the world-class Jabal Sayid mine and the promising Umm and Damad deposit.

For further information, readers are encouraged to contact: Power Metallic Mines Inc. The Canadian Venture Building 82 Richmond St East, Suite 202 Toronto, ON

Neither the TSX Venture Exchange nor its Regulation Services Provider accepts responsibility for the adequacy or accuracy of this release.

QAQC and Sampling GeoVector Management Inc (“GeoVector”) is the Consulting company retained to perform the actual drilling program, which includes core logging and sampling of the drill core.

All core in this news release is either HQ or NQ sized core. Drill core is re-fitted and measured. Geotech on core includes photographs (wet & dry), rock quality index, magnetic susceptibility, conductivity, and recovery estimates. Core is logged for lithology, mineralogy, and structural features, and sample intervals are delineated and tagged.

Sampled core is mechanically sawn, and half-core is retained for future reference. GeoVector’s QAQC program includes regular insertion of CRM standards, duplicates, and blanks into the sample stream with a stringent review of all results. QAQC and data validation was performed, and no material errors were observed.

All samples were submitted to and analyzed at Activation Laboratories Ltd (“Actlabs”), a commercial laboratory independent of Power Metallic with no interest in the Project. Actlabs is an ISO 9001 and 17025 certified and accredited laboratories. Samples submitted through Actlabs are run through standard preparation methods and analysed using RX-1 (Dry, crush (< 7 kg) up to 80% passing 2 mm, riffle split (250 g) and pulverize (mild steel) to 95% passing 105 μm) preparation methods, and using 1F2 (ICP-OES) and 1C-OES – 4-Acid near total digestion + Gold-Platinum-Palladium analysis and 8-Peroxide ICP-OES, for regular and over detection limit analysis. Pegmatite samples are analyzed using UT7 – Li up to 5%, Rb up to 2% method. Actlabs also undertake their own internal coarse and pulp duplicate analysis to ensure proper sample preparation and equipment calibration.

This message contains certain statements that may be deemed “forward-looking statements” concerning the Company within the meaning of applicable securities laws. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects,” “plans,” “anticipates,” “believes,” “intends,” “estimates,” “projects,” “potential,” “indicates,” “opportunity,” “possible” and similar expressions, or that events or conditions “will,” “would,” “may,” “could” or “should” occur. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance, are subject to risks and uncertainties, and actual results or realities may differ materially from those in the forward-looking statements. Such material risks and uncertainties include, but are not limited to, among others; the timing for various drilling plans; the ability to raise sufficient capital to fund its obligations under its property agreements going forward and conduct drilling and exploration; to maintain its mineral tenures and concessions in good standing; to explore and develop its projects; changes in economic conditions or financial markets; the inherent hazards associates with mineral exploration and mining operations; future prices of nickel and other metals; changes in general economic conditions; accuracy of mineral resource and reserve estimates; the potential for new discoveries; the ability of the Company to obtain the necessary permits and consents required to explore, drill and develop the projects and if accepted, to obtain such licenses and approvals in a timely fashion relative to the Company’s plans and business objectives for the applicable project; the general ability of the Company to monetize its mineral resources; and changes in environmental and other laws or regulations that could have an impact on the Company’s operations, compliance with environmental laws and regulations, dependence on key management personnel and general competition in the mining industry.

SOURCE Power Metallic Mines Inc.

For further information on Power Metallic Mines Inc., please contact: Duncan Roy, VP Investor Relations, 416-580-3862, [email protected]

The North American gold mining sector just got a major reshuffling. Equinox Gold Corp. (TSX/NYSE American: EQX) and Orla Mining Ltd. (TSX/NYSE American: ORLA) announced Tuesday a definitive all-share merger agreement that will create one of the continent’s largest gold producers, carrying an implied market capitalization of $18.5 billion and a combined annual production target of 1.1 million ounces of gold.

The deal is structured as an at-market combination in which each Orla shareholder will receive one Equinox common share plus a nominal cash payment of $0.0001 per share. Upon closing, existing Equinox shareholders will hold approximately 67% of the combined entity, with former Orla shareholders retaining 33% on a fully diluted, in-the-money basis. The transaction is expected to close in Q3 2026, pending shareholder votes anticipated for July and standard regulatory approvals in both Canada and Mexico.

Scale Built on Canadian Bedrock

The strategic logic here is hard to argue with. The combined company will be anchored by three long-life Canadian gold mines — Equinox’s Greenstone (Ontario) and Valentine (Newfoundland & Labrador) assets, alongside Orla’s Musselwhite mine in Ontario. Together, those three Canadian operations alone are projected to produce approximately 685,000 ounces in 2026, positioning the new Equinox Gold as the second-largest producer of Canadian gold.

The remaining production is spread across the U.S. (75,000 oz), Mexico (115,000 oz), and Nicaragua (225,000 oz), rounding out a six-mine North American portfolio that offers both operational diversification and jurisdictional focus.

A Growth Pipeline With Teeth

What separates this deal from a simple consolidation play is the organic growth runway. Management has outlined a clear path to more than 1.9 million ounces of annual gold production — an approximately 70% increase from the 1.1 million ounce baseline — driven entirely by internally funded North American expansion projects. Key growth contributors include the Valentine Phase 2 expansion in Canada, South Railroad and Castle Mountain in the U.S., and Los Filos and Camino Rojo underground in Mexico. All four projects carry established Mineral Reserves, reducing the execution risk that typically plagues expansion-stage narratives.

Combined Proven & Probable Mineral Reserves stand at 22.7 million ounces, with an additional 25.1 million ounces of Measured & Indicated Resources, giving the new entity a reserve base that rivals many of its senior peers.

Financial Firepower

Based on current analyst consensus estimates, the combined company is projected to generate roughly $1.4 billion in free cash flow and approximately $3.4 billion in EBITDA in 2026. Combined available liquidity is also pegged at $1.4 billion, providing the financial flexibility to fund growth without dilutive equity raises — a critical distinction in a capital-intensive sector.

What It Means for the Market

This merger is the latest signal that gold sector consolidation is accelerating, driven by elevated gold prices, rising development costs, and the premium the market increasingly assigns to scale and reserve quality. For investors tracking mid-tier and senior producers, the creation of a new $18.5 billion North American-focused gold company sets a new benchmark for what a fully integrated, internally funded growth story looks like in this cycle.

The transaction includes break fees of $475 million payable by Equinox and $250 million by Orla in certain termination scenarios, underscoring the commitment both boards have made to seeing this through.

Robert LeBoyer, Senior Vice President, Equity Research Analyst, Biotechnology, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

First Quarter Operating Loss Was Lower Than Our Estimates. Unicycive reported a 1Q Loss From Operations of $8.0 million, compared with our estimate of $9.9 million. An increase of $8.3 million in the Fair Value of Warrant Liabilities resulted in a Net Comprehensive Loss attributable to common shareholders of $12.8 million, or $(0.54) per share. Importantly, the company confirmed that NDA approval for OLC is on track to meet the June 29 PDUFA date. Cash on March 31, 2026, was $57.1 million.

We Expect OLC Approval By The PDUFA Date. The NDA for OLC (oxylanthanum calcium) was submitted in December and accepted for review in January. We believe the preclinical and clinical sections have already passed FDA review, and previous manufacturing problems associated with a contract manufacturer have been corrected. We expect OLC to receive FDA approval on or before its June 29, 2026, approval date.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q1 results exceeded expectations despite continued legacy business runoff.Q1 revenue of $54.3 million exceeded the high end of management’s guidance range of $49 million to $54 million and was above our estimate of $50.0 million. Adjusted EBITDA of $8.0 million also exceeded management’s guidance range of $4 million to $7 million and our estimate of $4.4 million.

Management shifts focus toward nutrition-led growth and omnichannel expansion. During the quarter, management emphasized that the company is now deploying its significantly leaner operating model toward growth initiatives centered on nutrition, supplements, and retail expansion. Management highlighted that the global nutrition market is more than 12 times the size of the digital fitness market, positioning nutrition as the company’s largest long-term opportunity.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Joe Gomes, CFA, Managing Director, Equity Research Analyst, Generalist , Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Overview. First quarter 2026 results fell short of expectations. Startup delays for new projects and broader macroeconomic conditions caused the Building Solutions and Business Services divisions to perform worse than expected. The Energy Services division, however, maintained solid momentum. Star did see some significant new business wins and contract renewals in the quarter and realized merger synergies are running ahead of plan.

1Q26 Results. Revenue of $50.1 million was up 57.1% on a reported basis and up 7.7% on a pro forma basis. Top line, however, came in below our projection of $54 million, mostly due to the soft Business Services revenue. Adjusted EBITDA loss in 1Q26 increased to $1.6 million versus a loss of $0.7 million on a reported basis in 1Q25 and a loss of $1.2 million on a pro forma basis. We were at a positive adjusted EBITDA of $1.9 million. Net loss was $1.17 per share, and adjusted net loss was $0.99, compared to $0.59 and $0.38, respectively, in 1Q25.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Michael Kupinski, Director of Research, Equity Research Analyst, Digital, Media & Technology , Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Delayed filing and significant operating deterioration. Bitcoin Depot disclosed it is unable to timely file its Form 10-Q, citing unreasonable effort and expense, while preliminary fiscal Q1 2026 results reflected a sharp deterioration in operating performance driven by regulatory impacts and enhanced compliance controls.

Revenue and gross profit collapse. Revenue declined 49.2% year-over-year, falling by $80.7 million in the quarter, while gross profit declined 85.5% to $4.5 million from $31.2 million in the prior-year period, reflecting significantly lower transaction volumes and substantial margin compression.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

")

")

")

")

are identified within the survey region of interest. The joint inversion of airborne, ground gravity and muon tomography (green) is also shown. The main N-S trending structure is clearly aligned with a mafic intrusion, as described earlier. The massive sulphide structure to the East is seen in the muon tomography inversion, but is not apparent in the gravity inversions – though there is some slight density variation seen in the airborne data. The joint inversion is very compatible with the presence of the massive sulphide. https://ideon.ai/results/bhp-leinster-mine/ (CNW Group/Power Metallic Mines Inc.)")