Research News and Market Data on CDRO

05/07/2026

The Company delivered record quarterly net gaming revenue of €64.4 million and Adj. EBITDA of €6.0 million

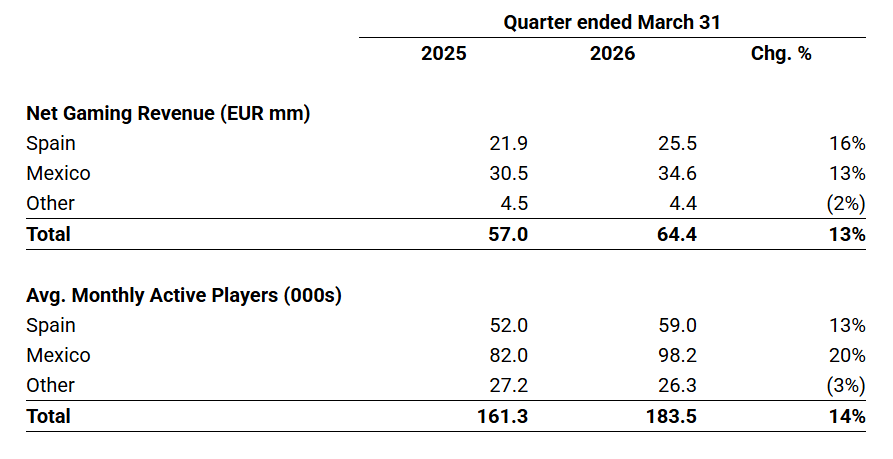

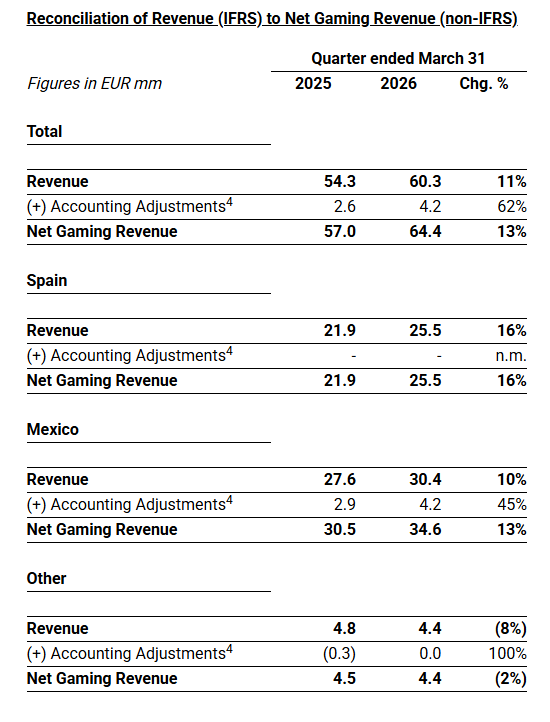

- Total revenue was €60.3 mm in Q1 2026, while net gaming revenue1 was €64.4 mm, 13% above Q1 2025.

- Spain revenue and net gaming revenue were €25.5 mm in Q1 2026, 16% above Q1 2025.

- Mexico revenue was €30.4 mm in Q1 2026, while net gaming revenue was €34.6 mm, 13% above Q1 2025.

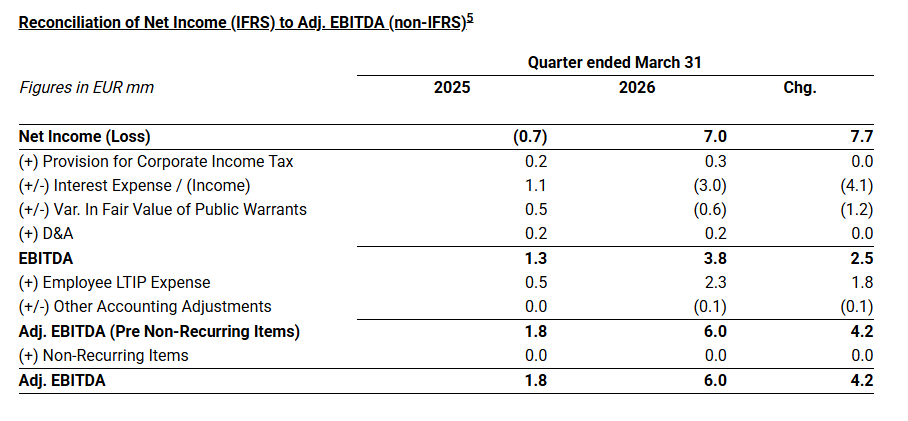

- Adj. EBITDA reached €6.0 mm in Q1 2026, €4.2 mm above Q1 2025.

- Net income was €7.0 mm in Q1 2026 versus a net loss of €0.7 mm in Q1 2025.

- Total cash position of €56.2 mm and no financial debt as of March 31, 2026.

- Unchanged outlook for FY 2026: Net gaming revenue of €235-245 mm and Adj. EBITDA2 of €15-20 mm.

Madrid, Spain and Tel Aviv, Israel, May 7, 2026 – (GLOBE NEWSWIRE) Codere Online (Nasdaq: CDRO / CDROW, the “Company”), a leading online gaming operator in Spain and Latin America, has released its preliminary unaudited3 financial results for the quarter ended March 31, 2026.

Below are the main financial and operating metrics of the period.

Aviv Sher, Chief Executive Officer of Codere Online, commented, “We delivered a very strong start to 2026, achieving record quarterly net gaming revenue of €64.4 million, up 13% year‑on‑year. In Spain, performance accelerated meaningfully, with net gaming revenue growing 16%, reflecting a clear continuation and acceleration of the positive trends we began to see in the second half of 2025, particularly in the fourth quarter. Mexico also continued to deliver double‑digit growth on the back of a 20% increase in the number of active customers”.

Marcus Arildsson, CFO of Codere Online, commented, “Q1 2026 marked a clear step forward in profitability, with Adjusted EBITDA reaching €6.0 million, €4.2 million above the same period last year and a net profit of €7.0 million. We closed the quarter with a solid total cash position of €56.2 million and no financial debt, providing a strong balance sheet. Based on this performance, we reiterate our outlook for full year 2026, with expected net gaming revenue of €235–245 million and Adjusted EBITDA of €15–20 million”.

Recent Events

Filings with the U.S. Securities and Exchange Commission

- On April 28, 2026, the Company filed its 2025 annual report on Form 20-F;

- On May 5, 2026, the Company filed its forms S-8 relating to the Company’s long term incentive plans.

Conference Call Information

Codere Online’s management will host a conference call to discuss the results and provide a business update at 8:30 am US Eastern Time today, May 7, 2026. Access links to the audio webcast and presentation will be accessible on Codere Online’s website at www.codereonline.com. A recording of the webcast will also be available following the conference call.

About Codere Online

Codere Online refers, collectively, to Codere Online Luxembourg, S.A. and its subsidiaries. Codere Online, launched in 2014 as part of the renowned casino operator Codere Group, offers online sports betting and online casino through its state-of-the art website and mobile applications. Codere Online currently operates in its core markets of Spain, Mexico, Colombia, Panama and Argentina; this online business is complemented by Codere Group’s physical presence in Spain and throughout Latin America, forming the foundation of the leading omnichannel gaming and casino presence.

About Codere Group

Codere Group is a multinational group dedicated to entertainment and leisure. It is a leading player in the private gaming industry, with four decades of experience and with presence in seven countries in Europe (Spain and Italy) and Latin America (Argentina, Colombia, Mexico, Panama, and Uruguay).

Note on Rounding. Due to decimal rounding, numbers presented throughout this report may not add up precisely to the totals and subtotals provided, and percentages may not precisely reflect the absolute figures.

Forward-Looking Statements

Certain statements in this document may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements include, but are not limited to, statements regarding Codere Online Luxembourg, S.A. and its subsidiaries (collectively, “Codere Online”) or Codere Online’s or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this document may include, for example, statements about Codere Online’s financial performance and, in particular, the potential evolution and distribution of its net gaming revenue; any prospective and illustrative financial information; and changes in Codere Online’s strategy, future operations and target addressable market, financial position, estimated revenues and losses, projected costs, prospects and plans.

These forward-looking statements are based on information available as of the date of this document and current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied upon as representing Codere Online’s or its management team’s views as of any subsequent date, and Codere Online does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, Codere Online’s actual results or performance may be materially different from those expressed or implied by these forward-looking statements. There may be additional risks that Codere Online does not presently know or that Codere Online currently believes are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. Some factors that could cause actual results to differ include (i) changes in applicable laws or regulations, including online gaming, privacy, data use and data protection rules and regulations as well as consumers’ heightened expectations regarding proper safeguarding of their personal information, (ii) the impacts and ongoing uncertainties created by regulatory restrictions, changes in perceptions of the gaming industry, changes in policies and increased competition, and geopolitical events such as war, (iii) the ability to implement business plans, forecasts, and other expectations and identify and realize additional opportunities, (iv) the risk of downturns and the possibility of rapid change in the highly competitive industry in which Codere Online operates, (v) the risk that Codere Online and its current and future collaborators are unable to successfully develop and commercialize Codere Online’s services, or experience significant delays in doing so, (vi) the risk that Codere Online may never achieve or sustain profitability, (vii) the risk that Codere Online will need to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all, (viii) the risk that Codere Online experiences difficulties in managing its growth and expanding operations, (ix) the risk that third-party providers, including the Codere Group, are not able to fully and timely meet their obligations, (x) the risk that the online gaming operations will not provide the expected benefits due to, among other things, the inability to obtain or maintain online gaming licenses in the anticipated time frame or at all, (xi) the risk that Codere Online is unable to secure or protect its intellectual property, (xii) the risk that Codere Online’s securities may be delisted from Nasdaq and (xiii) the possibility that Codere Online may be adversely affected by other political, economic, business, and/or competitive factors. Additional information concerning certain of these and other risk factors is contained in Codere Online’s filings with the U.S. Securities and Exchange Commission (the “SEC”). All subsequent written and oral forward-looking statements concerning Codere Online or other matters and attributable to Codere Online or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements above.

Financial Information and Non-GAAP Financial Measures

Codere Online’s financial statements are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”), which can differ in certain significant respects from generally accepted accounting principles in the United States of America (“U.S. GAAP”).

This document includes certain financial measures not presented in accordance with U.S. GAAP or IFRS (“non-GAAP”), such as, without limitation, net gaming revenue, Adjusted EBITDA and constant currency information. These non-GAAP financial measures are not measures of financial performance in accordance with U.S. GAAP or IFRS and may exclude items that are significant in understanding and assessing Codere Online’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to revenue, net income, cash flows from operations or other measures of profitability, liquidity or performance under U.S. GAAP or IFRS. You should be aware that Codere Online’s presentation of these measures may not be comparable to similarly-titled measures used by other companies. In addition, the audit of Codere Online’s financial statements in accordance with PCAOB standards, may impact how Codere Online currently calculates its non-GAAP financial measures, and we cannot assure you that there would not be differences, and such differences could be material.

Codere Online believes that the use of these non-GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends in comparing Codere Online’s financial measures with other similar companies, many of which present similar non-GAAP financial measures to investors. These non-GAAP financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non-GAAP financial measures. Reconciliations of non-GAAP financial measures to their most directly comparable measure under IFRS are included herein.

This document may include certain projections of non-GAAP financial measures. Codere Online is unable to quantify certain amounts that would be required to be included in the most directly comparable U.S. GAAP or IFRS financial measures without unreasonable effort, due to the inherent difficulty and variability of accurately forecasting the occurrence and financial impact of the various adjusting items necessary for such comparable measures or such reconciliation that have not yet occurred, are out of our control, or cannot be reasonably predicted, ascertained or assessed, which could have a material impact on its future IFRS financial results. Consequently, no disclosure of estimated comparable U.S. GAAP or IFRS measures is included and no reconciliation of the forward-looking non-GAAP financial measures is included.

Use of Projections

This document contains financial forecasts with respect to Codere Online’s business and projected financial results, including net gaming revenue and adjusted EBITDA. Codere Online’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this document, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this document. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. See “Forward-Looking Statements” above. Accordingly, there can be no assurance that the prospective results are indicative of the future performance of Codere Online or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this document should not be regarded as a representation by any person that the results contained in the prospective financial information will be achieved.

For further information on the limitations and assumptions underlying these projections, please refer to Codere Online’s filings with the SEC.

Preliminary Information

This document contains figures, financial metrics, statistics and other information that is preliminary and subject to change (the “Preliminary Information”). The Preliminary Information has not been audited, reviewed, or compiled by any independent registered public accounting firm. This Preliminary Information is subject to ongoing review including, where applicable, by Codere Online’s independent auditors. Accordingly, no independent registered public accounting firm has expressed an opinion or any other form of assurance with respect to the Preliminary Information. During the course of finalizing such Preliminary Information, adjustments to such Preliminary Information presented herein may be identified, which may be material. Codere Online undertakes no obligation to update or revise the Preliminary Information set forth in this document as a result of new information, future events or otherwise, except as otherwise required by law. The Preliminary Information may differ from actual results. Therefore, you should not place undue reliance upon this Preliminary Information. The Preliminary Information is not a comprehensive statement of financial results, and should not be viewed as a substitute for full financial statements prepared in accordance with IFRS. In addition, the Preliminary Information is not necessarily indicative of the results to be achieved in any future period.

No Offer or Solicitation

This document does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor will there be any sale of securities in any states or jurisdictions in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities will be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act of 1933, as amended, or an exemption therefrom.

Trademarks

This document may contain trademarks, service marks, trade names and copyrights of Codere Online or other companies, which are the property of their respective owners. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referred to in this document may be listed without the TM, SM, © or ® symbols, but Codere Online will assert, to the fullest extent under applicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights.

Industry and Market Data

In this document, Codere Online relies on and refers to certain information and statistics obtained from publicly available information and third-party sources, which it believes to be reliable. Codere Online has not independently verified the accuracy or completeness of any such publicly-available and third-party information, does not make any representation as to the accuracy or completeness of such data and does not undertake any obligation to update such data after the date of this document. You are cautioned not to give undue weight to such industry and market data.

Contacts:

Investors and Media

Guillermo Lancha

Director, Investor Relations and Communications

[email protected]

(+34) 628.928.152

1 Net Gaming Revenue is a non-IFRS measure; please see reconciliation of Net Gaming Revenue to Revenue at the end of the report.

2 Adjusted EBITDA is a non-IFRS measure; please see reconciliation of Adjusted EBITDA to Net Income at the end of the report. Net gaming revenue and Adjusted EBITDA outlooks are forward-looking non-IFRS measures; please see important disclaimers at the end of the report.

3 See “Preliminary Information” below.

4 Figures primarily reflect differences in recognition of revenue related to certain partner and affiliate agreements in place in Colombia, VAT impact from entry fees in Mexico and the impact from the application of inflation accounting (IAS 29) in Argentina.

5 Please refer to page 24 of our Q1 2026 Earnings Presentation for further details regarding this reconciliation.

Source: Codere Online Luxembourg, S.A.