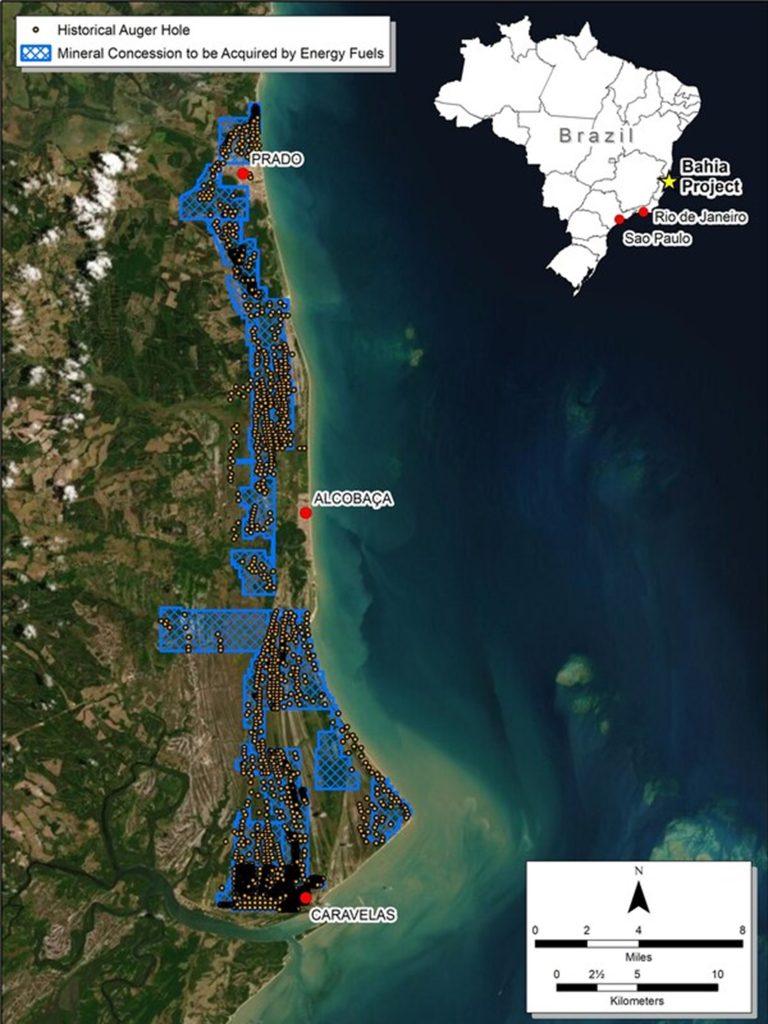

VANCOUVER, BC, Feb. 14, 2023 /CNW/ – Defense Metals Corp. (“Defense Metals” or the “Company“) (TSXV: DEFN) (OTCQB: DFMTF) (FSE:35D) announces the completion of flotation tests on variability samples and a master composite (“Master Composite” or “MC”) prepared from drill core obtained from its 100% owned Wicheeda Rare Earth Element (REE) deposit located in British Columbia, Canada.

John Goode, Defense Metals’ metallurgical advisor, stated:

“Flotation tests on variability samples from the dominant lithological unit of the Wicheeda REE deposit gave an average of 81% recovery to a concentrate assaying 45% rare earth oxide. Wicheeda is one of the few rare earth deposits under development from which a high-grade mineral flotation concentrate can be produced at recovery rates similar to those obtained by current rare earth producers. High-grade concentrates at high recoveries are a critical requirement for positive production economics. These successful flotation results help to position Defense Metals’ Wicheeda deposit as one of the best in North America.”

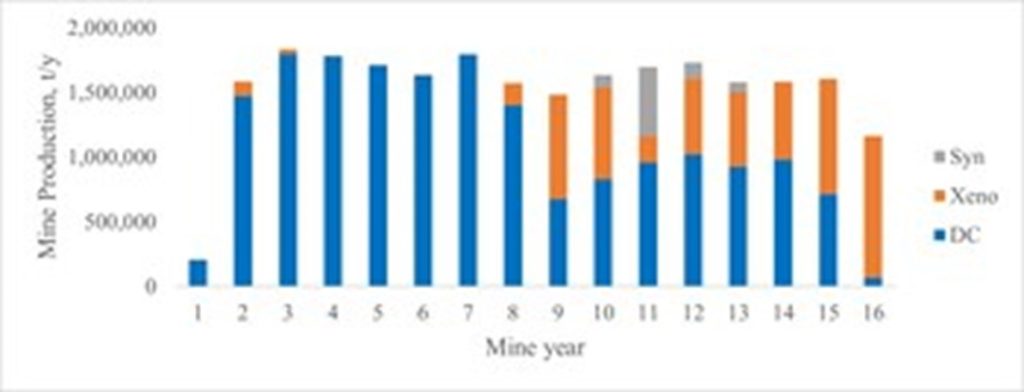

Defense Metals completed flotation tests on variability samples that are representative of the three key REE-bearing lithologies in the Wicheeda deposit: 1) the higher-grade dolomite carbonatite (“DC”) which makes up 73% of the deposit, 2) the xenolithic carbonatite (“XE”) that represents 24%; and 3) the syenite (“SYN”). The primary rare earths minerals are monazite, bastnäsite and synchysite/parisite. Figure 1 shows the mine plan as presented in the Independent Preliminary Economic Assessment issued in 20221.

Figure 1. Wicheeda REE Deposit Lithologies During Mine Life

Key Highlights:

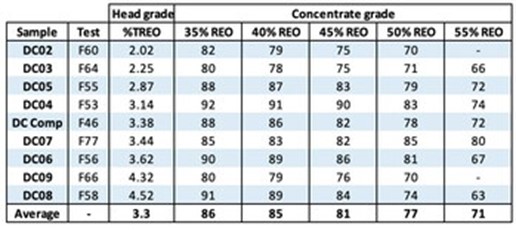

Table 1 results show that if the flotation plant is fed DC material at an average grade of 3.3% Total Rare Earth Oxide (“TREO”) and is operated to produce a flotation concentrate containing 45% TREO, an average 81% recovery will be observed. If 50% TREO were targeted, recovery would be expected to be 77%. The DC mineralized material will be essentially the only lithology fed to the flotation plant in the first eight years as shown in Figure 1.

Table 1:Recovery rates at concentrates of specified grades – DC samples

Note to Table 1: DC Comp is a blend of all DC variability samples.

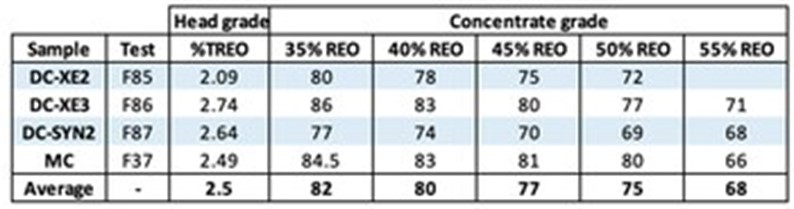

If the flotation plant is fed DC material mixed with other lithological types, as planned for later in the mine life, recoveries at different target concentrate grades will be as shown in Table 2. Of the four blends tested, when producing a 40% TREO flotation concentrate the recovery rate averaged 80% with higher recoveries when the DC content was higher.

Table 2: Recovery rates at concentrates of specified grades – DC blends

Notes to Table 2: DC-XE2 and DC-XE3 are 1:2 and 2:1 blends of DC and XE Comp, respectively. DC-SYN2 is 2:1 blend of DC Comp and SYN2. MC is a blend of DC (73.4%), XE (22.5%), and SYN (3.8%).

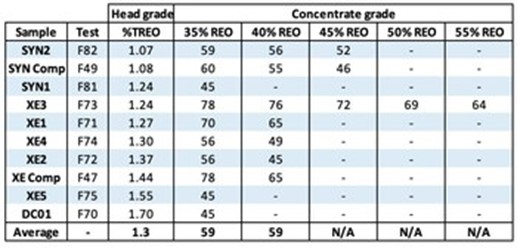

Table 3 shows the testwork results for the variability samples comprising pure XE and SYN lithologies. The flotation plant is expected to only see such lithologies when they are blended with DC. However, the data show that if the lower grade XE and SYN material are processed alone, at a target flotation concentrate grade of 40% TREO, the average recovery rate will be 59%.

Table 3: Recovery rates at concentrates of specified grades – SYN and XE samples

Notes to Table 3: SYN Comp and XE Comp are composites of respective variability samples. DC01 was mis-identified as being DC, but assays and mineralogy showed it to be XE and it was treated as such. N/A indicates insufficient data for meaningful average.

As noted above, in the first 8 years of the mine life, over 90% of the flotation plant feed will be DC material, with higher rare earth grade, with the later years being mostly DC and XE material at relatively lower grades (see Figure 1).

The grade-recovery-concentrate data provided above will support the upcoming preliminary feasibility study (PFS) and allow the development of an updated and enhanced mine plan incorporating drilling completed following the PEA that identifies lithology and feed grades to arrive at estimates of the concentrate and REO production rates in each year.

Methodology and QA/QC

Defense Metals prepared 17 variability samples covering different lithologies, areas of the deposit, and head grades using drill core material. The average mass of each sample was 31 kg, with the Total Rare Earth Oxide (“TREO”) assays ranging from 1.07% to 4.52% with an average of 2.34% TREO. Drill core material was also used to make a 260 kg Master Composite sample containing each of the three lithologies in their respective life-of-mine proportions. The MC sample had a head grade assay of 2.49% TREO.

All variability samples and the MC sample were shipped to SGS, Lakefield, Ontario where they were checked, crushed, and composited. A total of 87 flotation tests were completed to investigate the impact of collector type and dosage, depressant type and dosage, pulp temperature, pulp density, pulp pH, and flotation feed size.

Bulk flotation and other operations continue at SGS in order to prepare concentrate samples for continuing hydrometallurgical test work and planned hydrometallurgical pilot plant testing.

Feed samples were analyzed by Inductively coupled plasma mass spectrometry (ICP-MS) and flotation products were analyzed by SGS using wavelength dispersive X-ray fluorescence (WD-XRF) following lithium borate fusion of the sample. The SGS analyses included a quality assurance / quality control (QA/QC) program including the insertion of rare earth element standard and blank samples.

Defense Metals detected no significant QA/QC issues during review of the data. Defense Metals is not aware of any sampling, recovery or other factors that could materially affect the accuracy or reliability of the data referred to herein. SGS Lakefield is an ISO/IEC 17025 and ISO9001:2015 accredited laboratory. SGS is independent of Defense Metals Corp.

Qualified Person

The scientific and technical information contained in this news release, as it relates to the Wicheeda Rare Earth Element Project, has been reviewed and approved by John Goode, P. Eng., who is a Qualified Person as defined by National Instrument 43-101 and has provided the technical information relating to metallurgy in this news release. Kristopher J. Raffle, P.Geo. (BC), a director of the Company, is the Qualified Person as defined in National Instrument 43-101 for the information relating to resources in this news release.

About the Wicheeda REE Project

Defense Metals 100% owned, 4,262-hectare (~10,532-acre) Wicheeda REE property is located approximately 80 km northeast of the city of Prince George, British Columbia; population 77,000. The Wicheeda REE Project is readily accessible by all-weather gravel roads and is near infrastructure, including hydro power transmission lines and gas pipelines. The nearby Canadian National Railway and major highways allow easy access to the port facilities at Prince Rupert, the closest major North American port to Asia.

The 2021 Wicheeda REE Project Preliminary Economic Assessment technical report (“PEA”) outlined a robust after-tax net present value (NPV@8%) of $517 million and an 18% IRR1. This PEA contemplated an open pit mining operation with a 1.75:1 (waste:mill feed) strip ratio providing a 1.8 Mtpa (“million tonnes per year”) mill throughput producing an average of 25,423 tonnes REO annually over a 16 year mine life. A Phase 1 initial pit strip ratio of 0.63:1 (waste:mill feed) would yield rapid access to higher grade surface mineralization in year 1 and payback of $440 million initial capital within 5 years.

About Defense Metals Corp.

Defense Metals Corp. is a company focused on the development of its 100% owned Wicheeda Rare Earth Element mineral deposit, located near Prince George, British Columbia, Canada, that contains metals and elements commonly used in in green energy, aerospace, automotive and defense technologies. Rare earth elements are especially important in the production of magnets used in wind turbines and in permanent magnet motors for electric vehicles. Defense Metals Corp. trades in Canada under the symbol “DEFN” on the TSX Venture Exchange, in the United States, under “DFMTF” on the OTCQB and in Germany on the Frankfurt Exchange under “35D”.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Cautionary Statement Regarding “Forward-Looking” Information

This news release contains “forward–looking information or statements” within the meaning of applicable securities laws, which may include, without limitation, statements relating to advancing the Wicheeda REE Project, the continuing hydrometallurgical test work and planned hydrometallurgical pilot plant testing, completing the planned PFS, the Company’s plans for its Wicheeda REE Project, the expected results and outcomes, the technical, financial and business prospects of the Company, its project and other matters. All statements in this news release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Such statements and information are based on numerous assumptions regarding present and future business strategies and the environment in which the Company will operate in the future, including the price of rare earth elements, the anticipated costs and expenditures, the ability to achieve its goals, that general business and economic conditions will not change in a material adverse manner, that financing will be available if and when needed and on reasonable terms. Such forward-looking information reflects the Company’s views with respect to future events and is subject to risks, uncertainties and assumptions, including the risks and uncertainties relating to the interpretation of exploration and metallurgy results, risks related to the inherent uncertainty of exploration and cost estimates, the potential for unexpected costs and expenses and those other risks filed under the Company’s profile on SEDAR at www.sedar.com. While such estimates and assumptions are considered reasonable by the management of the Company, they are inherently subject to significant business, economic, competitive and regulatory uncertainties and risks. Factors that could cause actual results to differ materially from those in forward looking statements include, but are not limited to, continued availability of capital and financing and general economic, market or business conditions, adverse weather and climate conditions, failure to maintain or obtain all necessary government permits, approvals and authorizations, failure to maintain community acceptance (including First Nations), risks relating to unanticipated operational difficulties (including failure of equipment or processes to operate in accordance with specifications or expectations, cost escalation, unavailability of personnel, materials and equipment, government action or delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters), risks relating to inaccurate geological, metallurgical and engineering assumptions, decrease in the price of rare earth elements, the impact of Covid-19 or other viruses and diseases on the Company’s ability to operate, an inability to predict and counteract the effects of COVID-19 on the business of the Company, including but not limited to, the effects of COVID-19 on the price of commodities, capital market conditions, restriction on labour and international travel and supply chains, loss of key employees, consultants, or directors, increase in costs, delayed drilling results, litigation, and failure of counterparties to perform their contractual obligations. The Company does not undertake to update forward–looking statements or forward–looking information, except as required by law.

Nearly 90% of Diverse / Multicultural Consumers Report Taking Positive Action as a Result of a Marketer Purposefully Investing in Their Communities, Including Switching Brands

Majority Cite More Favorable Feelings About Brands That Advertise in Diverse / Multicultural Media; 4 in 10 More Likely to Notice Ads on Those Properties Compared with Mainstream Media

HOUSTON, Feb. 14, 2023 /PRNewswire/ — Direct Digital Holdings, Inc. (Nasdaq: DRCT) (“Direct Digital Holdings” or the “Company”), a leading advertising and marketing technology platform operating through its companies Colossus Media, LLC (“Colossus SSP”), Huddled Masses LLC (“Huddled Masses”) and Orange142, LLC (“Orange142”), today released a new whitepaper, Dollars & DEI: Multicultural Consumers’ Insights on Brands’ Media Buying and Marketing Practices. The findings reveal that brands, at a time of economic uncertainty, are currently missing out on significant revenue and market share growth opportunities – and jeopardizing future growth – due to a lack of appropriate and purposeful focus on the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities.

The whitepaper centers on exclusive research, commissioned by Direct Digital Holdings and conducted by Horowitz Research. An in-depth survey, the results spotlight the perspectives of diverse / multicultural consumers, a group that comprises two-fifths of the American consumer market, yet has not had proportionate attention from the advertising business.

The research tapped 1,342 U.S. adults 18+ from the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities to share their attitudes and behaviors in light of the marketing world’s scattershot diversity efforts.

According to the findings, almost 90 percent of diverse / multicultural consumers report taking action because of a company investing in their community, including telling others about the brand, sharing their support on social media – or even switching to a brand, away from a competitor that does not invest in their community.

Other takeaways have major implications and offer guidance to brands, including:

8 out of 10 diverse consumers said they feel more positively about brands that live up to promises to make a concerted effort of support to their communities, and alternatively, 8 in 10 say they feel negatively about brands that don’t live up to their promises.

The large majority of diverse consumers, about 8 in 10, feel more positively about brands that advertise in targeted diverse/multicultural media.

Nearly 7 out of 10 said that purposely investing ad dollars with media that is owned or focused on their respective communities strongly demonstrates support.

4 out of 10 of respondents said they notice ads more when they appear on targeted diverse / multicultural media channels versus mainstream media.

In addition, while ad spending was found to be one of the most impactful ways for marketers to demonstrate a commitment to these audiences, creating ads and content that are inclusive of diverse communities was cited as another strong demonstration of support. To put the findings into sharper focus, both came out ahead of simply sharing social posts.

“Given this compelling data for a growing U.S. economic market segment, there should be no more reason for brands to move slowly in diversifying their media allocations,” said Mark D. Walker, CEO and Co-Founder of Direct Digital Holdings, who penned the introduction to the whitepaper. “If we put aside all the rhetoric and platitudes, this is an industry that has always been and should still be about reaching customers and driving revenue.”

Alongside the survey findings, the paper includes insights from brand leaders from HP, McDonald’s and Visa; media and marketing agency executives from Mediahub Worldwide and One50One; publishers of diverse properties such as Black Enterprise, Glitter Magazine, ODK Media, NGL Collective and Pink Media; the architect behind the new DEI trade group BRIDGE; the chairman and CEO of MediaLink; and the head of Colossus SSP.

“Siloing multicultural and diverse audiences into a separate line item in marketing plans needs to be a thing of the past,” added Alejandro Clabiorne, EVP, Executive Director, New York, Mediahub Worldwide. “This whitepaper not only makes clear that these groups are critical to marketers’ bottom lines, but also provides the types of insights that will show brands how to effectively reach and resonate with these prospective customers, building traction and brand loyalty that can fuel growth.”

“The research demonstrates that across the board, diverse and multicultural consumers recognize, appreciate and have the disposable income to spend on brands that target their communities either through authentic ad messages or media,” said Lashawnda Goffin, CEO, Colossus SSP, the sell-side technology company within Direct Digital Holdings. “Brands that have intentionally and sincerely engaged with these audiences have seen the benefit – and those looking to grow their customer base need to follow suit.”

“Making the right consumer connections is about to take on factorial proportions and while values and outlook may hold groups of targets together, beliefs and aspirations will splinter them, requiring, as the research confirms, much deeper considerations for message tone, creative and of course media placement,” said Sheryl Daija, Founder and CEO, BRIDGE. “It’s time for our industry to move from DEI as a philosophy to inclusion as a core business practice and growth driver.”

To download the whitepaper: Dollars & DEI: Multicultural Consumers’ Insights on Brands’ Media Buying and Marketing Practices, go to https://directdigitalholdings.com/whitepaper.

Methodology This study included qualitative and quantitative research conducted by Horowitz Research (www.horowitzresearch.com). The online surveys were conducted September – December 2022 among 1,342 U.S. adults 18+, including over 300 respondents each from the Black, Hispanic / Latin, AAPI and LGBTQIA+ communities.

About Direct Digital Holdings Direct Digital Holdings (Nasdaq: DRCT), owner of operating companies Colossus SSP, Huddled Masses and Orange 142, brings state-of-the-art sell- and buy-side advertising platforms together under one umbrella company. Direct Digital Holdings’ sell-side platform, Colossus SSP, offers advertisers of all sizes extensive reach within general market and multicultural media properties. The company’s subsidiaries Huddled Masses and Orange142 deliver significant ROI for middle market advertisers by providing data-optimized programmatic solutions at scale for businesses in sectors that range from energy to healthcare to travel to financial services. Direct Digital Holdings’ sell- and buy-side solutions manage approximately 90,000 clients monthly, generating over 100 billion impressions per month across display, CTV, in-app, and other media channels. Direct Digital Holdings is the ninth Black-owned company to go public in the U.S and was named a top minority-owned business by The Houston Business Journal.

Forward-Looking Statements This press release may contain forward-looking statements within the meaning of federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and which are subject to certain risks, trends and uncertainties.

As used below, “we,” “us,” and “our” refer to Direct Digital Holdings. We use words such as “could,” “would,” “may,” “might,” “will,” “expect,” “likely,” “believe,” “continue,” “anticipate,” “estimate,” “intend,” “plan,” “project” and other similar expressions to identify forward-looking statements, but not all forward-looking statements include these words. All statements contained in this release that do not relate to matters of historical fact should be considered forward-looking statements.

All of our forward-looking statements involve estimates and uncertainties that could cause actual results to differ materially from those expressed in or implied by the forward-looking statements. Our forward-looking statements are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. Although we believe that these forward-looking statements are based on reasonable assumptions, many factors could affect our actual operating and financial performance and cause our performance to differ materially from the performance expressed in or implied by the forward-looking statements, including, but not limited to: our dependence on the overall demand for advertising, which could be influenced by economic downturns; any slow-down or unanticipated development in the market for programmatic advertising campaigns; the effects of health epidemics, such as the ongoing global COVID-19 pandemic; operational and performance issues with our platform, whether real or perceived, including a failure to respond to technological changes or to upgrade our technology systems; any significant inadvertent disclosure or breach of confidential and/or personal information we hold, or of the security of our or our customers’, suppliers’ or other partners’ computer systems; any unavailability or non-performance of the non-proprietary technology, software, products and services that we use; unfavorable publicity and negative public perception about our industry, particularly concerns regarding data privacy and security relating to our industry’s technology and practices, and any perceived failure to comply with laws and industry self-regulation; restrictions on the use of third-party “cookies,” mobile device IDs or other tracking technologies, which could diminish our platform’s effectiveness; any inability to compete in our intensely competitive market; any significant fluctuations caused by our high customer concentration; any violation of legal and regulatory requirements or any misconduct by our employees, subcontractors, agents or business partners; any strain on our resources, diversion of our management’s attention or impact on our ability to attract and retain qualified board members as a result of being a public company; our dependence, as a holding company, of receiving distributions from Direct Digital Holdings, LLC to pay our taxes, expenses and dividends; and other factors and assumptions discussed in the “Risk Factors,” “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” and other sections of our filings with the SEC that we make from time to time. Should one or more of these risks or uncertainties materialize or should any of these assumptions prove to be incorrect, our actual operating and financial performance may vary in material respects from the performance projected in these forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and except as required by law, we undertake no obligation to update any forward-looking statement contained in this release to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances, and we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

SAN DIEGO, Feb. 14, 2023 (GLOBE NEWSWIRE) — Kratos Defense & Security Solutions, Inc. (NASDAQ: KTOS), a leading National Security Solutions provider, announced today that it will publish financial results for the fourth quarter and Fiscal Year End of 2022 after the close of market on Thursday, February 23rd. Management will discuss the Company’s operations and financial results in a conference call beginning at 2:00 p.m. Pacific (5:00 p.m. Eastern).

The call will be available at www.kratosdefense.com. Participants may register for the call using this Online Form. Upon registration, all telephone participants will receive the dial-in number along with a unique PIN that can be used to access the call. For those who cannot access the live broadcast, a replay will be available on Kratos’ website.

About Kratos Defense & Security Solutions Kratos Defense & Security Solutions, Inc. (NASDAQ:KTOS) develops and fields transformative, affordable technology, platforms and systems for United States National Security related customers, allies and commercial enterprises. Kratos is changing the way breakthrough technology for these industries are rapidly brought to market through proven commercial and venture capital backed approaches, including proactive research and streamlined development processes. At Kratos, affordability is a technology, and we specialize in unmanned systems, satellite communications, cyber security/warfare, microwave electronics, missile defense, hypersonic systems, training, combat systems and next generation turbo jet and turbo fan engine development. For more information go to www.KratosDefense.com.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Entertainment and Leisure stocks have had a good start to the New Year, but the better performance has not erased the disaster that was 2022. We believe that stocks appear to be baking in a mild economic downturn, a soft landing, so to speak. Given that we are skeptic of the conventional thought, we take a cautious stance regarding the recent lift in valuations and encourage investors to take an accumulation approach.

Entertainment:Bowlero on a roll. The Noble Entertainment Index performed well, up 1.5% in the last 12 months, compared with negative returns for the S&P 500 (-7.1%). Although there were broad economic challenges over the past year, entertainment companies benefited from the general public’s return to “normal” following the COVID pandemic. We believe that in-person experiential entertainment recovery is still in its early stage and should continue into 2024.

Gaming: Looking for value in the rubble.The Noble Gaming Index is down 53.1% in the past year, well below the S&P 500, down 7.1%. But, recently, the Noble Gaming Index increased 12.9% in the last quarter, outperforming the 3.2% increase in the general market, as measured by the S&P 500 Index. A reflex bounce? Short squeeze? Or, were the shares oversold? We encourage investors to play it safe.

Esports: Motorsport Games revs its engine. The company was full steam ahead in investing in its new product launches in 2023, but it was running out of cash. Fortunately, a couple of favorable moves to add liquidity set the stock soaring, up 1,600% in one day, creating further opportunities to raise cash. Now, flush with cash, investors look toward the product rollouts.

Leisure: Travel to new heights. The U.S. Travel Association updated its 2023 outlook, projecting a resilient domestic leisure travel market. Consumers appear eager to splurge on travel, in spite of the economic headwinds. We focus on one of our favorite internet media plays, Travelzoo. The company recently updated Fourth Quarter 2022 guidance with revenues expected to be roughly $18.5 million, a strong 31% increase year over year.

Overview

Have economic prospects improved?

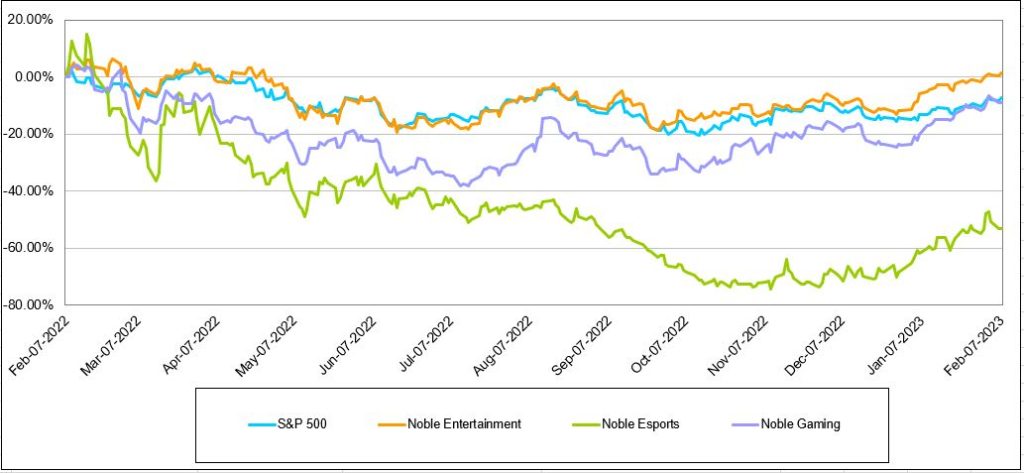

The Entertainment & Leisure industries performed better since the beginning of the year, providing some relief to the downturn that investors suffered in 2022. As Figure #1 Entertainment 12 Month Trailing Stock Performance highlights, the Entertainment and Leisure Indices are still recovering and many have yet to offset the 2022 declines, except for the Entertainment stocks. The Entertainment stocks not only have performed well in the first quarter, but have beat the general market as measured by the S&P 500 Index over the past year. The Noble Entertainment Index is up a modest 1.5% in the past year, better than the general market’s 7.1% decline. It is important to note that the Noble Indices are market cap weighted. As such, not all stocks reflected the favorable relative performance.

What is driving the improved stock performance in the latest quarter? We believe that investors have become more positive about the economic outlook, with conventional wisdom now anticipating a soft economic landing or a mild economic recession. This is a shift toward an optimistic tone from one that anticipated a severe economic recession. The Federal Reserve caused the dire outlook. The Fed signaled that it will continue to raise interest rates until inflation is arrested, in spite of the adverse impact on the economy and jobs. But, since then, conventional wisdom on the economy has brightened as inflation seems to have subsided. The more favorable economic outlook is exemplified by a Wall Street firm that decreased the risk of an economic recession in 2023 by a sizable 25%.

We tend to be skeptics and conservative. As such, we tend not to buy into strength. Our view is that the stocks were oversold and reflected recessionary type valuations. But, have the economic prospects really improved that much? We encourage investors to take an accumulation approach, focusing on some of our favorite stocks highlighted in this report, including Bowlero, Codere Online Luxembourg, Engine Gaming and Media, and Travelzoo.

Figure #1 Entertainment 12 Month Trailing Stock Performance

Source: Capital IQ

Entertainment

Bowlero on a roll

The Noble Entertainment Index performed well, up 1.5% in the last 12 months, compared with negative returns for the S&P 500 down 7.1%. Although there were broad economic challenges over the past year, entertainment companies benefited from the general public’s return to “normal” following the COVID pandemic. We believe that the trend toward social gathering and in-person activities are helping to offset broader macroeconomic headwinds. While some industries received a boost during late 2020 and 2021 when consumers were spending stimulus checks on online shopping, the recovery for in-person entertainment has been more recent. In our view, the recovery in experiential, in-person entertainment appears to be gaining traction and the recovery could continue into 2024.

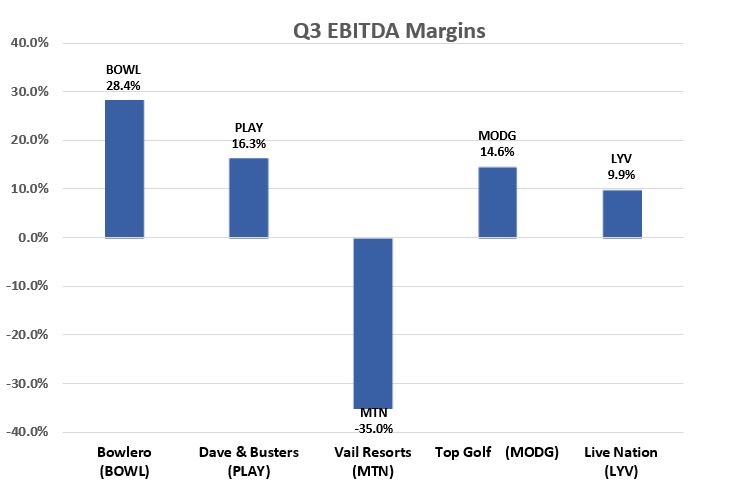

As Figure #2 Entertainment Revenue Growth illustrates, virtually all of the experiential entertainment companies reported strong revenue growth in the latest reported quarter, (the calendar third quarter end September 2022). One of the examples of the in-person recovery is in bowling centers, in general, and Bowlero, specifically. The company recently announced that it eclipsed $1 billion in Trailing Twelve Month (TTM) revenue as of December 31, 2022, which included 48% same store sales growth over the prior year. Additionally, Bowlero added 40 bowling centers over the past 18 months as it continues to successfully execute on its roll-up strategy. As revenues have improved, so too have margins. As Figure #3 Entertainment EBITDA Marginsillustrates, Bowlero delivered industry leading margins in the latest reported quarter at 24.8%.

Bowlero is on a roll. With the BOWL shares up roughly 50% in the past 12 months, the shares have outperformed both the Noble Entertainment Index up 1.5%, as well as the broader market, as measured by the S&P 500, which decreased -7.1%. In spite of the favorable fundamental tailwind, the shares trade in line with its experiential entertainment peers. Figure #4 Entertainment Comparables illustrates that the BOWL shares trade at 9.7 times Enterprise Value to our estimated 2023 adj. EBITDA, below the peer average of 10.7 times, despite the company’s industry leading fundamentals. Given its favorable fundamental outlook, prospects for enhanced revenue and cash flow growth through acquisitions and favorable internal growth, and compelling stock valuation, the BOWL shares lead our list for favorites in the Entertainment industry.

Figure #2 Entertainment Revenue Growth

Source: Company 10Qs

Figure #3 Entertainment EBITDA Margins

Source: Company 10Qs

Figure #4 Entertainment Comparables

Source: Company filings and Noble estimates

Gaming

Looking for value in the rubble

The Noble Gaming Index is down 53.1% in the past year, well below the S&P 500, down 7.1%. In our view, the poor performance of Gaming stocks was the result of investors trying to take risk off the table. Many Gaming companies are still in developmental stages, with high marketing and customer acquisition costs. As such, many in the industry are unprofitable and rely on the balance sheets to fund operations. Before Covid, these companies benefited from the easy money policies and favorable capital markets, which many relied on for funding. But, with the recent sharp rise in interest rates and difficult general market conditions to raise capital, the music has stopped. Gaming stock valuations are now more scrutinized, in an environment of increasing cost of capital. As such, we believe industry players that are already profitable, and those with little to no debt and ample cash on the balance sheet are best positioned for to lead the industry.

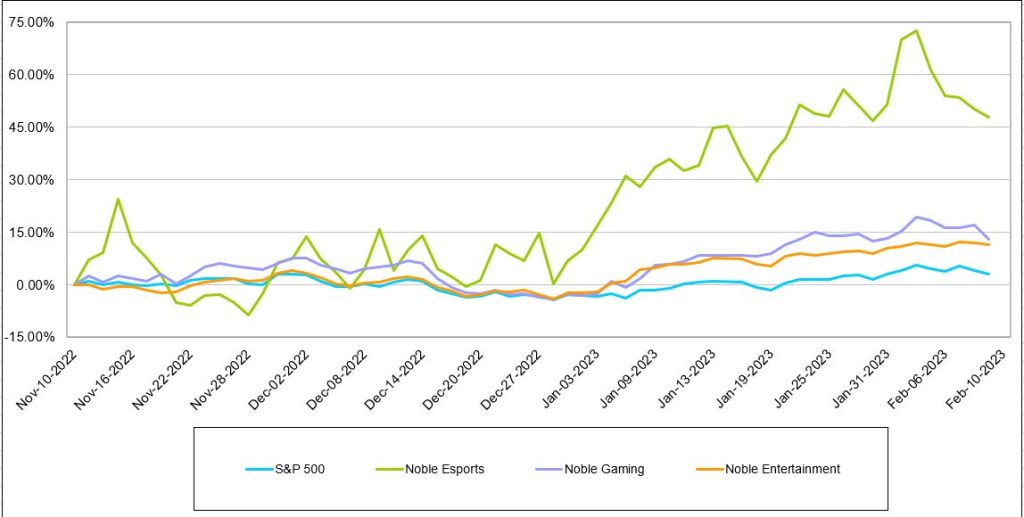

Our focus is on the shares of Codere Online Luxembourg, CDRO. The CDRO shares are down 42.4% in the last year, underperforming the S&P 500’s -7.1% return. However, despite a tough 12-month period, the CDRO shares outperformed the Noble Gaming Index, which dropped 53.1%. We believe that the relative outperformance of the CDRO shares over the past year reflects its better financial position than most of its peers. Most recently, the Noble Gaming Index improved, as illustrated in Figure #5 Three Month Stock Performance. The Noble Gaming Index increased 12.9%, outperforming the 3.2% increase in the general market, as measured by the S&P 500 Index. A reflex bounce? Short squeeze? Or, were the shares oversold? It appears to be all the above for many of the stocks in the index. The largest gains were from companies that appeared to be struggling and had favorable news. We believe that investing in struggling companies with limited access to capital is a dangerous place to be.

In terms of Codere Online Luxembourg, the fundamentals of the company appear favorable. Codere Online’s cash burn has been within expectations and the company had a strong cash balance of €72 million and virtually no long-term debt as of September 30, 2022. As such, the company appears positioned to continue executing its growth strategy in Latin America, which for the time being consists of broadening its presence in key markets such as Mexico and Columbia, and aggressively expanding in Argentina.

The company’s growth could be bolstered if Brazil begins regulating sports betting in 2023. Importantly, Entain CEO Jette Nygaard-Anderson, recently stated that she expects Brazil to complete process of regulating sports betting in 2023, citing new administration of President Lula. In summary, Codere Online is distinguished from many of its peers, with an established foothold in key Latin American markets, flush with cash to penetrate existing markets and enter new ones. It has the ability to become the industry leader in many of its markets.

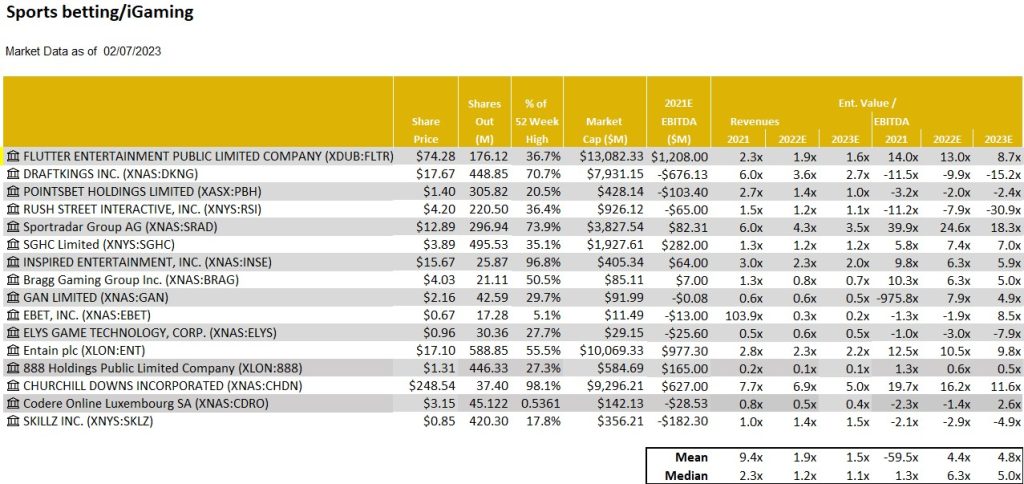

Near current levels, the iGaming industry peer group is trading at 5.0 times Enterprise Value to 2023 revenues, illustrated in Figure #6 Gaming Comparables. Codere Online Luxemburg (CDRO) is one of our favorite plays in the iGaming industry due to several factors. As mentioned above, the company has virtually no long-term debt and €72 million in cash, as of September 30, 2022. We believe that the company has a favorable runway to reach cash flow breakeven while continuing to fund its expansion in the meantime. Furthermore, in our view, given its ability to invest in its developing markets, the company appears to have the ability to become the preeminent online gambling leader in many Latin American markets. Finally, the CDRO shares appear compelling, trading near 2.6 times expected 2023 revenue, well below peers. As a result, we view the CDRO shares as among our favorite online gambling plays, with the shares rated Outperform with $9 price target.

Figure #5 Three Month Stock Performance

Source: Capital IQ

Figure #6 Gaming Comparables

Source: Company filings and Noble estimates

Esports

Motorsport revs its engine

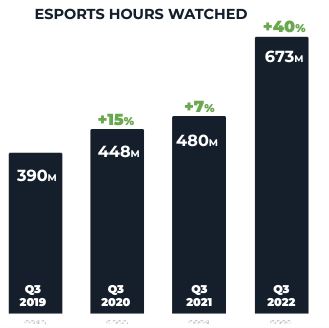

The Noble Esports Index was down 53% over the past year, underperforming the broader market, which was down 7%, as as measured by the S&P 500 Index. Not unlike many other emerging industries, Esports has been battered by macroeconomic headwinds over the past year. Investors are placing more importance on companies that are generating positive cash flow, rather than speculating on future profitability, given recessionary concerns and elevated interest rates. While the Esports industry has shown favorable trends in the number of viewers and hours watched, many companies are still burning cash and may need to raise additional capital. Total hours watched of esports content was up 40% in Q3 of 2022, illustrated in Figure #7 Esports Viewership.

The best performing stock in the Esports index was HUYA, which only declined by 9.7% on a TTM basis. Huya is the largest Esports live streaming platform in China and recently expanded into a variety of real-time events. Huya benefits from the favorable growth trends of the Esports and live streaming industries, as it does not rely on the popularity of a single game or tournament. The worst performing stock in the Esports index is Esports Entertainment Group (GMBL), which declined 97.2% on a TTM basis. The company burned through its cash and had limited access to additional capital.

In the latest quarter, however, the Noble Esports Index rebounded, up a strong 47.9%, as depicted in the earlier in Figure #5 Three Month Stock Performance. The strength in the quarter was due to a relatively few number of stocks, including HUYA (up 135.8%) and two of our favorite plays, Motorsport Games (MSGM) and Engine Gaming and Media (GAME), which increased 68.9% and 149.8%, respectively. In fact, Motorsport Games increased a stunning 1,618.8% with a trading day following news of a debt for equity swap.

Motorsport Games revs its engine

Motorsport Games is a publisher of motorsport video games, with the rights to iconic racing franchises such as NASCAR and 24 Hour of LeMans. The company recently completed a debt for equity swap which led to a surprisingly strong increase in the stock valuation. This allowed the company to complete several direct offerings, eliminating all company debt and raising over $11 million in cash. The capital raise alleviated liquidity concerns, allowing the company to continue developing games. In our view, the launch of several games in 2023 should allow the company to swing toward cash flow break even. We have moved our rating to Market Perform given that the shares blew through our $9 price target. Our rating is under review as the company updates investors on its product rollout roadmap and the level of cash burn until it launches its upcoming products.

Engine Gaming & Media

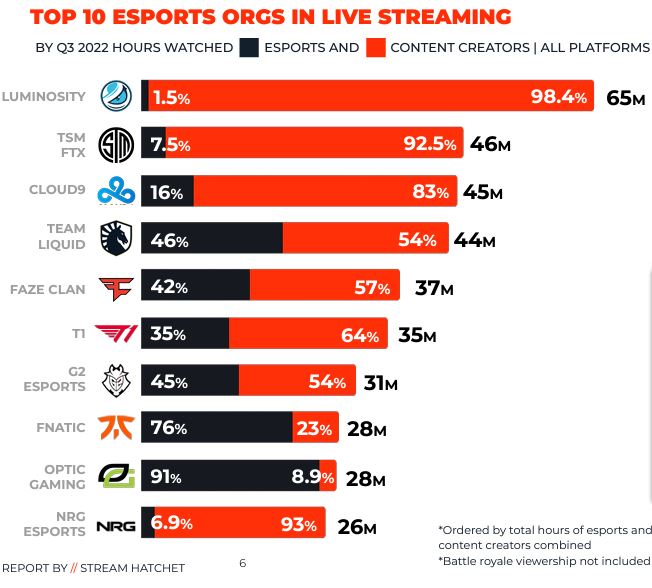

Another one of our favorites is Engine Gaming & Media (GAME). Engine Gaming & Media is a multi-platform media company engaged in most aspects of the Esports industry. The company’s media division coordinates video access and advertising, data analytics, and connects advertisers to social influencers in the gaming industry. Figure #7 Esports Viewership and Figure #8 Esports Live Streaming are from Stream Hatchet, the company’s live streaming data and Esports analytics business.

The company reported its fiscal first quarter results on January 17, 2023, which beat our expectations. Notably, the company’s influencer and gaming analytics software as a service revenue, a key growth vehicle, grew revenue by a strong 34.6% on a year over year basis. In addition, the company plans to merge with GameSquare Esports, which it expects will provide scale and provide cost synergies. Management indicated that the combination should accelerate the new company’s path toward profitability. We plan to update our models as more details emerge regarding the upcoming merger.

Figure #9 Esports Comparables highlight the stock valuations in the Esports industry. The valuations of many of the stocks, including Motorsport Games and Engine Gaming and Media are in flux. As mentioned, Motorsport Games significantly improved its financial position with recent equity raises and debt for equity swaps. Engine Gaming and Media’s fundamentals likely will change with a planned merger. In our view, the latest quarter has been a watershed moment for these companies. We look forward toward reevaluating our models, ratings and price targets upon more details on the developments from the respective companies.

Figure #7 Esports Viewership

Source: Stream Hatchet

Figure #8 Esports Live Streaming

Source: Stream Hatchet

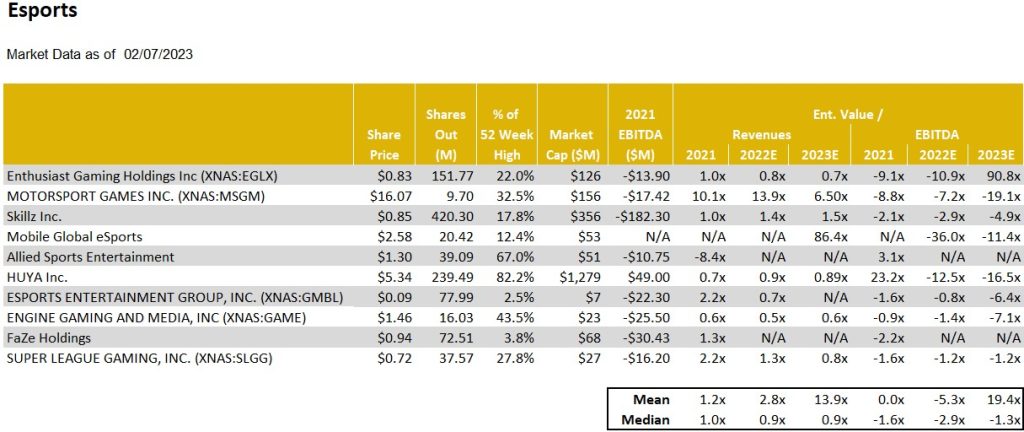

Figure #9 Esports Comparables

Source: Company filings and Noble estimates

Leisure

Travel to new heights

Once again, we focus on the travel industry in our Leisure section due to some favorable developments and outlook. Notably, the U.S. Travel Foundation forecasts an increase in travel spending in 2023 above both 2022 and 2019 levels. This would indicate that the travel industry has fully recovered from the depressed Covid impacted levels. Airline flights are full and there is high demand for hotels, even though pricing for those rooms are significantly higher. What is driving the demand and will it continue?

For the U.S., there are three factors influencing the relatively favorable outlook for the U.S. travel industry. The domestic leisure travel has been resilient in spite of higher gas prices, hotel rooms and airline tickets. A recent article from Forbes suggests that U.S. leisure travel is rebounding despite inflation as it is one area where people are willing to splurge. A second contributing factor to the favorable outlook is Business travel. Business travel is expected to be somewhat weaker in 2023 given the prospect of a mild economic recession in 2023. But, the business travel outlook is improved as a severe economic downturn appears less likely. The weak area has been international inbound travel to the U.S. We believe that this is a function of the strong U.S. dollar relative to other major currencies. On the flip side, international travel from the U.S. appears to be favorable given the U.S. dollar strength.

We believe that the inflationary trends, higher airline fares and hotel rates, as well as sluggish international travel, all have prompted travelers to seek travel deals. Consequently, one of our favorite plays on the travel industry, Travelzoo, has seen fundamental improvement. As an internet media company, its business is derived from its advertisers and travel partners to offer travel deals to its customers. This is different from travel suppliers and online travel agencies that rely on travel demand. Notably, Travelzoo recently updated its fourth quarter revenue guidance to be roughly $18.5 million, an increase of a strong 31% year over year, in line with our forecast.

Travelzoo is one of our favorite plays for the recovering travel industry. The shares are down roughly 46% in the past year, which we believe could present an attractive entry point for investors. Since reaching lows in December near $4.11 per share, the TZOO shares have rallied, up roughly 25% since that time. In our view, the shares may have reacted to a recent merger involving its founder, Ralph Bartel. The merger brought with it an influx of cash, but increased Mr. Bartels ownership of the company from slightly over 50% to over 60%. We view the move favorably as it provides increase liquidity for the company. Given the prospect for a favorable environment for travel deals, we view Travelzoo as among our favored ways to play the travel industry and the subsequent improved advertising from its travel partners. We rate the shares Outperform with a $9 price target.

Research reports on companies mentioned in this report are available by clicking below:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

EuroDry Ltd. was formed on January 8, 2018 under the laws of the Republic of the Marshall Islands to consolidate the drybulk fleet of Euroseas Ltd. into a separate listed public company. EuroDry was spun-off from Euroseas Ltd. on May 30, 2018; it trades on the NASDAQ Capital Market under the ticker EDRY. EuroDry operates in the dry cargo, drybulk shipping market. EuroDry’s operations are managed by Eurobulk Ltd., an ISO 9001:2008 and ISO 14001:2004 certified affiliated ship management company and Eurobulk (Far East) Ltd. Inc., which are responsible for the day- to-day commercial and technical management and operations of the vessels. EuroDry employs its vessels on spot and period charters and under pool agreements.

Michael Heim, CFA, Senior Research Analyst, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Lower shipping rates hurting results. Eurodry reported 2022-4Q revenues, net, of $15.1 million versus $22.3 million and below our projection of $19.9 million. Average TCE rates for the quarter were $16,689 versus $29,157 and our $18,982 estimate. Lower shipping rates led to a a 54% decline in adj. ebitda and a 78% decrease in adjusted net income. The sharp declines demonstrate Eurodry’s extreme sensitivity to shipping rates.

Shipping rate sensitivity will only increase in upcoming months. Fleet rate coverage drops off dramatically after the 2023-1Q. In fact, all 11 ships will be exposed to spot or indexed prices. This, combined with a further drop in shipping rates in February, could result in a difficult upcoming quarter for the company. Management estimates it would need rates above $12,700 to be cash flow breakeven while noting current prices in the $6,000-$7,000 range.

Equity Research is available at no cost to Registered users of Channelchek. Not a Member? Click ‘Join’ to join the Channelchek Community. There is no cost to register, and we never collect credit card information.

This Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

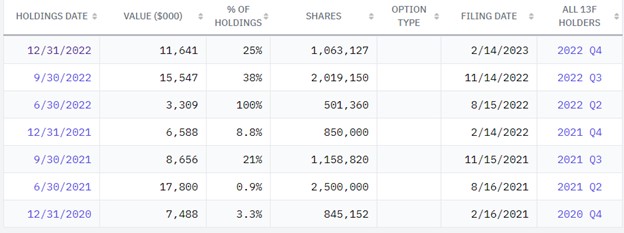

Scion’s Michael Burry Owns Online Retailers, Tech Firms, a Mortgage Servicer, and a Detention Provider

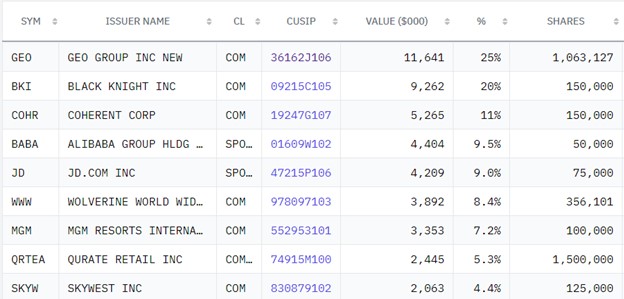

GEO Group (GEO), the publicly held prison company organized as a REIT, again tops Michael Burry’s public market holdings as of the end of last year. This is one of nine holdings; a few are on-again, off-again favorites of the revered hedge fund manager. If there is one theme in his positions, it is that of select online retail merchants. While the overall size of the positions as of quarter-end is known, these positions may not represent all investments, just those that are public and reportable to the SEC on form 13F. Burry famous for his portrayal in the movie “The Big Short” was not short any publicly traded securities as 2022 drew to a close.

Below are the nine holdings, in size order, copied directy from the 13F-HR filing. GEO, Alibaba, and JD.com are familiar to followers of Dr. Burry’s holdings as this is not the first time they have appeared in his portfolio.

Geo Group (GEO) runs private detention systems. As shown below, at the end of the second quarter of 2022, it represented 100% of Scion Asset Management’s public market positions. The current holding is roughly half the dollar amount of what it was three months prior.

Black Knight (BKI) is making its first appearance in the Scion portfolio. The mid-cap company provides mortgage and loan servicing products.

Coherent Corporation (COHR) has not been in the hedge fund manager’s portfolio prior to the last quarter. The small-cap technology company is involved in communications networks for aerospace, automotive, life sciences, and various other electronics and systems.

Alibaba (BABA) is often described as the “Chinese Amazon.com”. The only other time Scion held this well-known online retailer was during the second quarter of 2019.

JD.com (JD) is China’s largest online retailer and largest internet company by revenue. Burry owned shares once before during the first quarter of 2019.

Wolverine Worldwide (WWW) makes active footwear and apparel. Brands include Sperry, Saucony, and Hush Puppies. The small-cap company has not been in the Scion portfolio previously.

MGM Resorts (MGM) is a mid-cap company that owns and manages hotels and casinos worldwide. This is the first time Michael Burry has owned this name.

Qurante (QRTEA), formerly Liberty Interactive Corporation, is yet another direct marketer through the internet and video. The small-cap company is headquartered in Colorado.

Skywest Inc. (SKYW) is Burry’s smallest holding but still represents 4.4%. The airline has scheduled flights, including international, and also leases equipment for non-commercial flights. This is the first time the small-cap company has made an appearance in the Scion portfolio.

Take Away

Four times each year the SEC requires asset managers above a certain size to make a public filling of its portfolio.

Scion Asset Management is not exempt, but may, in addition to transacting in public securities, be creating positions in assets that are not required to be reported here. The reputation of Michael Burry has at times caused a lot of interest around less followed stocks.

Investors Receiving a 5% Yield are Losing to Inflation

The CPI inflation report and the Fed’s relentless increases in Fed funds levels have pushed the six-month US Treasury Bill (T-Bill) above 5%. This is the first time since 2007 that this low-risk investment has topped 5%. Last year on this date, the six-month T-Bill was 0.76%. While the stock market is concerned that higher borrowing costs will have the Fed’s intended effect of slowing demand, rates are reaching a point where another concern creeps in. The concern is will traditional stock investors lay back and be satisfied getting paid interest.

More likely, the high cash position represents “dry powder” waiting for an opportunity.

Short Term Rates

Money Market fund assets were $4.81 trillion for the week ended Wednesday, February 8, according to the Investment Company Institute. Just shy of the record MF balances reported in January. Higher than average cash levels have often been thought of as a bullish sign as it represents potential to drive stock prices up when flows toward equities increase.

This may be part of the situation as we come off a dismal 2022 for equities, but there is likely something else incentivizing the retreat to safety. The higher interest rates are in the short end of the curve, investors are getting paid to retreat. High-yielding cash equivalents with six-month T-Bills now at 5% (10-year Treasuries are only 3.75%) may be more than a parking place. It may represent an alternative investment with a much more assured return.

With inflation at 6.4%, the answer is no. But it is definitely preferable to seven of the periods on the 10-year chart above. And with January’s consumer price index (CPI) report revealing signs of sticky to reaccelerating inflation, the Federal Reserve is more likely to be hiking rates for longer than expected.

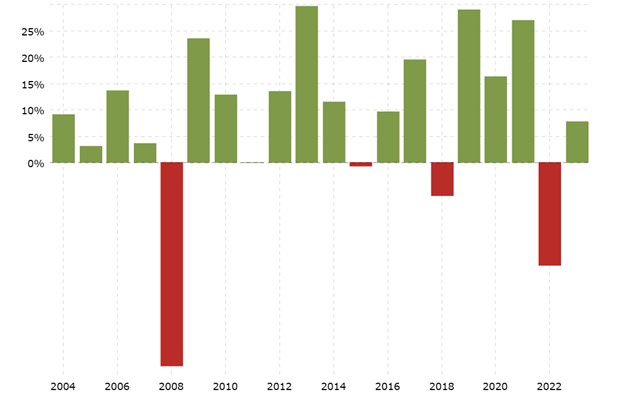

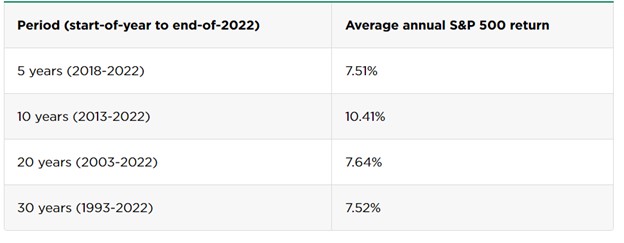

For investors looking to invest for longer periods, the stock market handily beats inflation. In other words, for the various time frames below, S&P 500 investors did not see their assets erode due to inflation.

Beating inflation is foundational to investing. Far exceeding it is the goal of many. Investors are not doing this choosing cash, in fact they are choosing to lose buying power rather than risk that the market doesn’t perform as it has historically.

Data released on Tuesday February 14 showed the inflation rate (CPI) slowed to 6.4% in January. The cost of goods and services rose 0.5% during the month. The half percentage is the largest one month erosion of purchasing power in three months.

Investors content with 4%-5% returns should consider that they are losing ground to persistent inflation.

Investors with a five-year time horizon or longer should weigh the risks of earning yields below the inflation rate to the ups and downs of stocks. In fact, as more do, the 4-5 trillion in cash can make or quite a bull market.

Traditional TV and OTT Meet to Maximize Local Hispanic Reach

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced today the launch of Entravision Plus, the newest way for companies to effectively connect and engage with Hispanic consumers through over-the-top (OTT) media and Connected TV (CTV). Entravision Plus helps optimize digital advertising results by leveraging performance-based data insights to connect with consumers as they consume content from premium Spanish-language publishers.

Entravision Plus is the latest addition in the full suite of digital solutions offered by Entravision. Along with OTT/CTV, this suite of digital services now includes: Digital Audio Ads, Display Ads, Digital Out of Home, Facebook / Instagram, TikTok, SEM, YouTube Ads, Email Marketing and Branded Content that complement the Company’s television and radio properties.

Currently, 90% of Hispanic consumers stream video on smart devices, which is 10% more than non-Hispanic consumers. In addition, the average Hispanic consumer spends over 26 hours per month watching video online, or seven more hours than the U.S average. With these statistics in mind, it is clear that a growing number of Latino households can now be reached via television and Entravision Plus online video products.

“Advertisers need to reach their consumers,” said Jessica Martinez, General Manager of Entravision US Digital. “We can now offer our clients the ability to reach consumers not only through our television and radio assets, but also through an array of digital products.”

Martinez continued, “Entravision Plus – our newest offering – provides advertisers with unique targeting, competitive ad separation and insightful analytics to reach all segments of the Latino consumers. We are excited to provide this premium solution, along with television and radio, to meet the needs of an evolving market. By leveraging Entravision Plus, we anticipate that our customers’ businesses will stand out and grow faster than ever before.”

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, comprises four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

For more information please contact: Kimberly Esterkin Addo Investor Relations evc@addo.com 310-829-5400

The ultimate sports lodgecontinues toperformat a high level, opening ninenew restaurantsand landingfive major development agreements

DALLAS, Feb. 13, 2023 (GLOBE NEWSWIRE) — FAT (Fresh. Authentic. Tasty.) Brands Inc., parent company of Twin Peaks Restaurant and 16 other restaurant concepts, is pleased to announce another strong year for Twin Peaks. The leading sports lodge concept generated strong growth throughout 2022 in addition to landing top spots on several prestigious awards lists.

In total, the banner year saw Twin Peaks open nine new lodges, while also signing four new area development agreements (ADAs) to add 26 future lodges in the United States and one ADA in Mexico for an additional 32 lodges. These agreements are expected to allow the brand to surpass the monumental 100-restaurant milestone by spring of 2023.

“We’re proud of the work our teams put in to ensure that Twin Peaks stays at the forefront of the sports bar segment and the restaurant industry as a whole,” said CEO Joe Hummel, who was named one of the most influential restaurant CEOs by Nation’s Restaurant News in 2022.

Twin Peaks began 2022 with the opening of its third lodge in Mexico City and now has four locations south of the border. The brand enters 2023 with 95 locations across the United States and Mexico with an anticipated 18-20 additional restaurants opening in 2023 in Chattanooga, Tennessee; Greenwood, Indiana; Deer Valley, Arizona; Columbus, Ohio; Springfield, Missouri; as well as Daytona Beach and Jacksonville, Florida to begin the year.

The brand signed several domestic ADAs to expand its footprint, including eight locations across North Carolina with Music City Consulting, four locations in the Ohio River Valley with JEB Food Group and three restaurants in the Pittsburgh area with the Falcons Group. Twin Peaks also secured an agreement with Dos Montes Corp. to add seven locations in Chicago and its largest international ADA to date with its subsidiary, Operadora 2 Montes, for 32 lodges in Mexico.

Twin Peaks also scored a number of industry honors. It placed seventh in Nation’s Restaurant News’ “Top 10 Biggest Sports Bars” and ranked 107th among the publication’s “Top 500 Restaurant Chains.” Twin Peaks also earned additional recognition by being named to Entrepreneur’s “Top 500” list, Black Box’s “Top 5 Restaurant Brands,” and Restaurant Business’ “Top 500” list for 2022.

In addition to these accolades, Twin Peaks continues to level up the sports bar’s menu. Twin Peaks amplified its scratch-made kitchen in 2022 with new artisan Flatbreads, Crispy Mini Beef Tacos, a variety of Street Tacos made with in-house smoked meats, a hand-cut choice New York Strip Steak, and specially crafted dessert and shot pairings.

Twin Peaks wrapped up its banner year by joining several partners in local fundraising initiatives. From serving meals to those affected by Hurricane Ian in Florida to fundraising efforts to raise $10,000 for Warriors for Freedom in Oklahoma to various local toy drives and gifting Christmas trees to military families throughout the holidays, Twin Peaks staff gave its time and effort to help support those in need throughout the communities in which it operates.

Capping off the year was Twin Peaks’ partnership with two national nonprofit organizations. Twin Peaks supported the ALS Foundation with a systemwide campaign to raise $15,000 for the organization and hosted the Twin Peaks Annual Hero’s Golf Tournament that raised $100,000 for its military foundation, Tunnel to Towers.

As Twin Peaks looks forward to surpassing the 100-restaurant milestone, the award-winning brand also has more big things in store for 2023 with continued unit growth, exciting marketing promotions for Super Bowl Sunday and March Madness, and a focus on the continued evolution of its sports bar fare with the launch of its new craft cocktails and spirits menu. Guests can also expect an expansion of its premium barrel selects that include refined choices like Angel’s Envy and Stagg Jr. bourbon and Corazon Resposado Buffalo Trace tequila to go along with reimagined cocktails and a fresh batch of quality spirits.

FAT Brands (NASDAQ: FAT) is a leading global franchising company that strategically acquires, markets, and develops fast casual, quick-service, casual dining, and polished casual dining concepts around the world. The Company currently owns 17 restaurant brands: Round Table Pizza, Fatburger, Marble Slab Creamery, Johnny Rockets, Fazoli’s, Twin Peaks, Great American Cookies, Hot Dog on a Stick, Buffalo’s Cafe & Express, Hurricane Grill & Wings, Pretzelmaker, Elevation Burger, Native Grill & Wings, Yalla Mediterranean and Ponderosa and Bonanza Steakhouses, and franchises and owns over 2,300 units worldwide.

About Twin Peaks

Founded in 2005 in the Dallas suburb of Lewisville, Twin Peaks now has nearly 100 locations in the US and Mexico. Twin Peaks is the ultimate sports lodge featuring made-from-scratch food and the coldest beer in the business surrounded by scenic views and the latest in high-definition TVs. At every Twin Peaks, guests are immediately welcomed by a friendly Twin Peaks Girl and served up a menu made for MVPs. From its smashed and seared to order burgers to its in-house smoked brisket, pork and wings, guests can expect menu items capable of satisfying every appetite. To learn more about franchise opportunities, visit twinpeaksfranchise.com. For more information, visit twinpeaksrestaurant.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements relating to the timing and performance of new store openings and growth in same-store sales. Forward-looking statements reflect expectations of management concerning the future and are subject to significant business, economic and competitive risks, uncertainties and contingencies, including but not limited to uncertainties surrounding the severity, duration and effects of the COVID-19 pandemic. These factors are difficult to predict and beyond our control, and could cause our actual results to differ materially from those expressed or implied in such forward-looking statements. We refer you to the documents that are filed from time to time by FAT Brands Inc. with the Securities and Exchange Commission, such as its reports on Form 10-K, Form 10-Q and Form 8-K, for a discussion of these and other factors. We undertake no obligation to update any forward-looking statement to reflect events or circumstances occurring after the date of this press release.

Immunocompromised Individuals, Including Organ Transplant Recipients, Are at Increased Risk of Severe COVID-19 and Poor Clinical Outcomes

SARS-CoV-2 has Mutated to Evade the Formerly EUA-Approved Monoclonal Antibody Therapies and Preventatives

CHATHAM, N.J., Feb. 13, 2023 (GLOBE NEWSWIRE) — Tonix Pharmaceuticals Holding Corp. (Nasdaq: TNXP), a clinical-stage biopharmaceutical company, today announced that it has exercised an option to obtain an exclusive license from Columbia University for the development of a portfolio of fully human (TNX-3600) and murine (TNX-4100) monoclonal antibodies (mAbs) for the treatment or prophylaxis of SARS-CoV-2 infection. SARS-CoV-2 is the cause of COVID-19. The licensed mAbs were developed as part of a research collaboration and option agreement between Tonix and Columbia University, originally announced in 2020.

“The licensing of these mAbs strengthens our expanding pipeline of next-generation therapeutics to treat and prevent COVID-19,” said Seth Lederman, M.D., Chief Executive Officer of Tonix Pharmaceuticals. “Immunocompromised individuals, including organ transplant recipients, are at increased risk of severe COVID-19 and poor clinical outcomes1. We believe there is a need for second-generation mAb treatments and prophylactics2,3 to protect this population.”

Although five mAb products containing seven distinct mAbs received emergency use authorization (EUA) from the U.S. Food and Drug Administration (FDA) for either treatment or prophylaxis of COVID-19, none remain useful or available since January 26, 2023, when the FDA announced that the last remaining mAb, Evusheld®, is no longer authorized4. Previously, either the National Institutes of Health COVID Treatment Guidelines Panel or FDA had removed recommendations or approvals for the other mAbs5,6.

Ilya Trakht, Ph.D., Associate Research Scientist at Columbia University Vagelos College of Physicians and Surgeons said, “We are excited to work with Tonix because of its commitment to developing therapeutics for COVID-19. Our antibody platform has proven robust and capable of rapidly making therapeutically relevant fully human mAbs to SARS-CoV-2. We have also generated murine mAbs, which represent a new approach. Murine mAbs have the potential for neutralizing a broader spectrum of SARS-CoV-2 variants and may be harder for SARS-CoV-2 to evade as we face a multitude of variants.”

To date, the formerly EUA-approved products were derived from the blood of COVID-convalescent patients or humanized mice7-9. The fully human mAbs generated by Columbia University, TNX-3600, have been isolated using a proprietary system involving a human hybridoma fusion partner.

The Company believes that murine mAbs, such as TNX-4100, have the potential to generate high affinity antibodies that recognize different epitopes on the SARS-CoV-2 spike protein. This is because mice have a different repertoire of antibodies than humans and the technology for generating antibodies optimizes the selection of appropriate B cells by the timing of immunization, harvesting approach and screening platform.

Dr. Lederman added, “The potential therapeutic antibodies licensed from Columbia University leverage our expanding internal development and manufacturing capabilities for biologics. These fully human and murine mAbs and their humanized counterparts build on a base of knowledge from a distinct murine mAb platform in development, TNX-3800, from which we have licensed three humanized mAbs from Curia Global.”

About TNX-3600

TNX-3600 are fully human mAbs generated from SARS-CoV-2+ asymptomatic individuals or COVID-19 convalescent patients, on which Tonix is collaborating with Columbia University. Given the unpredictable trajectory of the SARS-CoV-2 virus and new variants, we seek to contribute to a broad set of mAbs that can be scaled up quickly and potentially combined with other mAbs for the treatment or prophylaxis of SARS-CoV-2 infection.

About TNX-4100

TNX-4100 are murine mAbs and their humanized counterparts generated from mice immunized with SARS-CoV-2 spike protein, on which Tonix is collaborating with Columbia University. Since mice have a different repertoire of antibodies than humans, murine mAbs have the potential for neutralizing a broader spectrum of SARS-CoV-2 variants than fully human mAbs.

Tonix Pharmaceuticals Holding Corp.*

Tonix is a clinical-stage biopharmaceutical company focused on discovering, licensing, acquiring and developing therapeutics to treat and prevent human disease and alleviate suffering. Tonix’s portfolio is composed of central nervous system (CNS), rare disease, immunology and infectious disease product candidates. Tonix’s CNS portfolio includes both small molecules and biologics to treat pain, neurologic, psychiatric and addiction conditions. Tonix’s lead CNS candidate, TNX-102 SL (cyclobenzaprine HCl sublingual tablet), is in mid-Phase 3 development for the management of fibromyalgia with a new Phase 3 study launched in the second quarter of 2022 and interim data expected in the second quarter of 2023. TNX-102 SL is also being developed to treat Long COVID, a chronic post-acute COVID-19 condition. Tonix initiated a Phase 2 study in Long COVID in the third quarter of 2022. TNX-1300 (cocaine esterase) is a biologic designed to treat cocaine intoxication and has been granted Breakthrough Therapy designation by the FDA. A Phase 2 study of TNX-1300 is expected to be initiated in the second quarter of 2023. TNX-1900 (intranasal potentiated oxytocin), a small molecule in development for chronic migraine, is being studied in a potential pivotal Phase 2 study that initiated enrollment in the first quarter of 2023 and for which interim data is expected in the fourth quarter of 2023. TNX-601 ER (tianeptine hemioxalate extended-release tablets) is a once-daily formulation of tianeptine being developed as a potential treatment for major depressive disorder (MDD) with a Phase 2 study expected to be initiated in the first quarter of 2023. Tonix’s rare disease portfolio includes TNX-2900 (intranasal potentiated oxytocin) for the treatment of Prader-Willi syndrome. TNX-2900 has been granted Orphan Drug designation by the FDA. Tonix’s immunology portfolio includes biologics to address organ transplant rejection, autoimmunity and cancer, including TNX-1500, which is a humanized monoclonal antibody targeting CD40-ligand (CD40L or CD154) being developed for the prevention of allograft and xenograft rejection and for the treatment of autoimmune diseases. A Phase 1 study of TNX-1500 is expected to be initiated in the second quarter of 2023. Tonix’s infectious disease pipeline includes a vaccine in development to prevent smallpox and monkeypox, TNX-801; a next-generation vaccine to prevent COVID-19, TNX-1850; a platform to make fully human monoclonal antibodies to treat COVID-19, TNX-3600; and humanized anti-SARS-CoV-2 monoclonal antibodies, TNX-3800; and a class of broad-spectrum small molecule oral antivirals, TNX-3900. TNX-801, Tonix’s vaccine in development to prevent smallpox and monkeypox, also serves as the live virus vaccine platform or recombinant pox vaccine (RPV) platform for other infectious diseases. A Phase 1 study of TNX-801 is expected to be initiated in the second half of 2023.

*All of Tonix’s product candidates are investigational new drugs or biologics and have not been approved for any indication.

1Haidar G, Mellors JW. Improving the Outcomes of Immunocompromised Patients With Coronavirus Disease 2019. Clin Infect Dis. 2021;73(6):e1397-e1401. Doi:10.1093/cid/ciab397

3Callaway, E. Oct 28 2022. Nature (News). COVID ‘variant soup’ is making winter surges hard to predict: Descendants of Omicron are proliferating worldwide — and the same mutations are coming up again and again. www.nature.com/articles/d41586-022-03445-6

4https://www.fda.gov/drugs/drug-safety-and-availability/fda-announces-evusheld-not-currently-authorized-emergency-use-us – Accessed Feb 7, 2023

7Hansen J et al. Science. 2020 Aug 21;369(6506):1010-1014. Doi: 10.1126/science.abd0827