U.S. Treasury yields rose on Wednesday as stronger-than-expected economic growth reinforced expectations that the Federal Reserve will maintain its current interest rate stance, even amid growing political pressure and global market sensitivities.

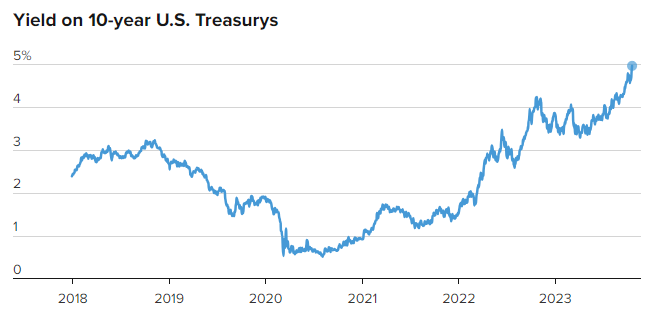

The benchmark 10-year Treasury yield climbed to 4.368%, reflecting rising investor confidence in the strength of the U.S. economy. The 2-year and 30-year yields also increased, closing at 3.904% and 4.904%, respectively. The moves followed a sharp rebound in second-quarter GDP, which showed the economy growing at an annualized rate of 3% — well above forecasts and reversing a 0.5% decline from the first quarter.

This robust data supports the case for keeping rates steady, at least in the near term, as the Federal Reserve continues to weigh inflation trends, labor market resilience, and long-term growth prospects. The Fed is widely expected to hold its benchmark interest rate between 4.25% and 4.5% during today’s announcement, but all eyes are on Chair Jerome Powell’s comments for insight into what comes next.

Adding complexity to the current environment is an ongoing effort by former President Donald Trump to pressure the Fed into lowering interest rates. Trump has criticized Powell’s leadership and floated the idea of replacing him in a potential second term. Despite this political noise, bond markets appear to be looking past the rhetoric, focusing instead on macroeconomic fundamentals. The continued rise in the 10-year yield suggests investors believe any leadership changes at the Fed would have little immediate impact on market direction.

Moreover, foreign holders of U.S. Treasuries could react to political instability or aggressive fiscal policy by offloading U.S. debt. This would push yields even higher, particularly if confidence in long-term economic or monetary policy erodes. The bond market’s sensitivity to global sentiment means that political pressure campaigns are unlikely to meaningfully influence interest rates without broader structural changes.

Adding further pressure is the threat of new tariffs, a cornerstone of Trump’s proposed economic agenda. Tariffs on imported goods would likely raise costs across the board, fueling inflation and reducing purchasing power domestically. As the U.S. imports many essential goods, any significant tariffs would shift costs onto consumers and businesses. This could complicate the Fed’s effort to keep core inflation within its 2% to 2.5% target range and delay any potential interest rate cuts.

For now, financial markets are signaling confidence in the Fed’s ability to manage the current environment, even if political rhetoric intensifies. Investors appear to be aligning their expectations with strong economic indicators and current inflation data rather than political speculation.

As the Federal Reserve’s decision looms, the upward movement in Treasury yields reflects not just optimism about U.S. growth, but also a more complex web of factors — from global capital flows and inflation expectations to political interference and international trade risks. The road ahead for monetary policy remains uncertain, but the market’s message is clear: economic fundamentals, not politics, will drive yields.