Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Q3 meets expectations. The company reported Q3 revenue of $66.9 million, in line with our estimate of $66.6 million. Adj. EBITDA of $6.1 million was slightly better than our forecast of $5.5 million, illustrated in Figure #1 Q3 Variance. Notably, we are adjusting EBITDA for a one-time legal settlement fee paid by the company during the quarter.

Weak Q4 pacing. Management guided Q4 revenue down 3-5% year-over-year compared with our expectation of 7% growth. Management cited a weak Publishing outlook as well as an ongoing pullback in the company’s #1 broadcast advertising category (mortgage companies) as primary factors in the challenged outlook.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

Entravision Communications Corporation is a diversified Spanish-language media company utilizing a combination of television and radio operations to reach Hispanic consumers across the United States, as well as the border markets of Mexico. Entravision owns and/or operates 53 primary television stations and is the largest affiliate group of both the top-ranked Univision television network and Univision’s TeleFutura network, with television stations in 20 of the nation’s top 50 Hispanic markets. The Company also operates one of the nation’s largest groups of primarily Spanish-language radio stations, consisting of 48 owned and operated radio stations.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Refer to the full report for the price target, fundamental analysis, and rating.

Solid Q3 results. Q3 revenue of $241 million increased 21% versus the prior year period, better than our $234.1 million estimate. Digital revenues accounted for much of the upside variance while stronger than expected Political advertising contributed as well. Adj. EBITDA was $25.9 million, up 12% year over year, slightly below our $27.3 million estimate, which was impacted by currency exchange rates.

Digital continues its impressive growth. Digital revenues increased 29%, driven by strong performance of the company’s digital ad agency business in Latin America. Additionally, the recent acquisitions of 365 Digital and MediaDonuts were not fully accounted for in in Q3 of 2021, leading to further upside in the quarter.

This Company Sponsored Research is provided by Noble Capital Markets, Inc., a FINRA and S.E.C. registered broker-dealer (B/D).

*Analyst certification and important disclosures included in the full report. NOTE: investment decisions should not be based upon the content of this research summary. Proper due diligence is required before making any investment decision.

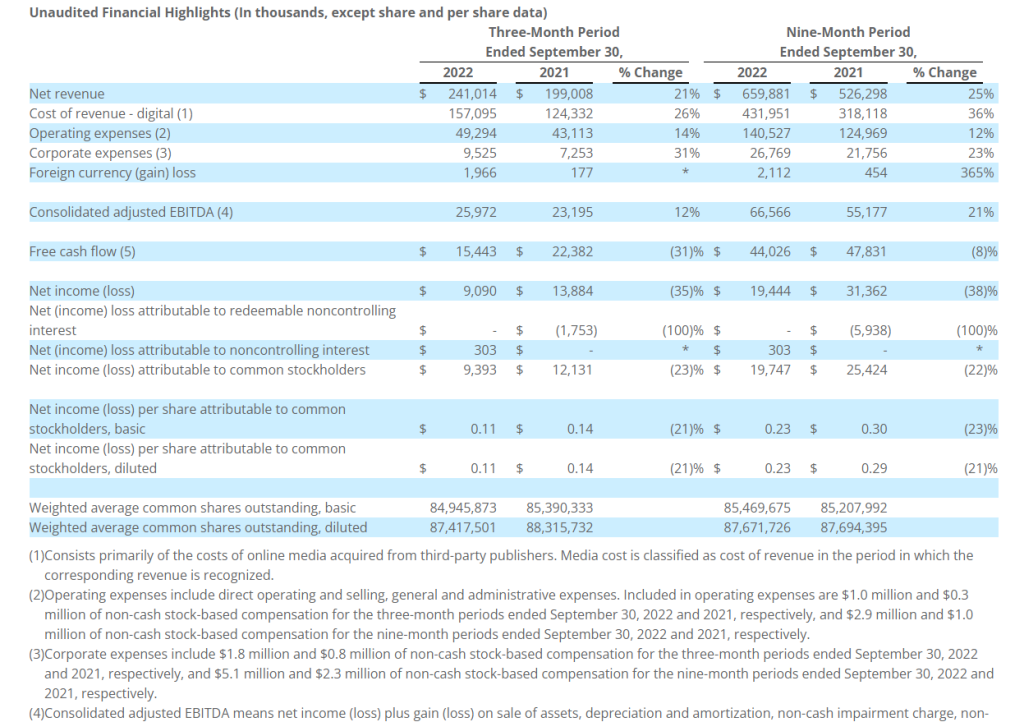

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision Communications Corporation (NYSE: EVC), a leading global advertising solutions, media and technology company, today announced financial results for the three- and nine-month periods ended September 30, 2022.

Third Quarter 2022 Highlights

Record third quarter advertising revenue

Net revenue up 21% over the prior-year quarter

Net income attributable to common stockholders down 23% over the prior-year quarter

Consolidated adjusted EBITDA up 12% over the prior-year quarter

Operating cash flow up 62% over the prior-year quarter

Free cash flow down 31% over the prior-year quarter

Quarterly cash dividend of $0.025 per share

“Entravision continued to see progress in the third quarter of 2022, with revenue up 21% versus the prior-year period. Adjusted EBITDA also improved double-digits, increasing 12% year-over-year,” said Walter Ulloa, Chairman and Chief Executive Officer. “Entravision’s strength throughout the quarter was again driven by our digital segment, where revenue improved 29% versus the third quarter of 2021. In our television and audio businesses, political ad spend, in particular, continued to perform strongly.”

Mr. Ulloa continued, “Entravision’s solid performance in the third quarter, together with our progress year-to-date, demonstrates the resiliency and growth of our business in a tough macro environment. We continue to strategically expand across the globe and now have operations in 40 countries across five continents in service of more than 7,000 clients. We are thoughtfully positioning our digital teams in emerging economies where Entravision’s unique offerings have a key first-mover advantage and where a critical mass of connected consumers exists alongside a growing advertising industry. We remain optimistic in finding multiple growth opportunities around the world for our digital business and look forward to sharing our progress as we continue to grow and expand globally.”

Quarterly Cash Dividend

The Company announced today that its Board of Directors approved a quarterly cash dividend to shareholders of $0.025 per share on the Company’s Class A, Class B and Class U common stock, in an aggregate amount of approximately $2.1 million. The quarterly dividend will be payable on December 30, 2022 to shareholders of record as of the close of business on December 15, 2022, and the common stock will trade ex-dividend on December 14, 2022. The Company currently anticipates that future cash dividends will be paid on a quarterly basis; however, any decision to pay future cash dividends will be subject to approval by the Board.

Non-GAAP Financial Measures

This press release contains certain non-GAAP financial measures as defined by SEC Regulation G. The GAAP financial measure most directly comparable to each of these non-GAAP financial measures, and a table reconciling each of these non-GAAP financial measures to its most directly comparable GAAP financial measure is included beginning on page 10.

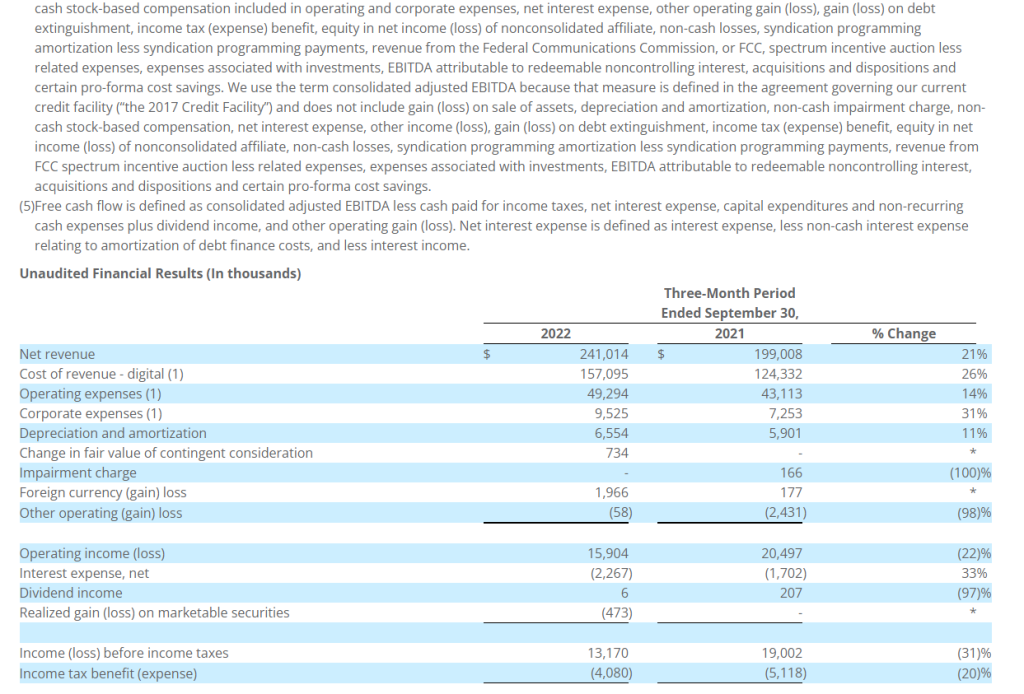

Net revenue in the third quarter of 2022 totaled $241.0 million, up 21% from $199.0 million in the prior-year period. Of the overall increase, approximately $42.8 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business, and due to our investment in a variable interest entity during the third quarter of 2022 and our acquisition of 365 Digital during the fourth quarter of 2021, neither of which contributed to net revenue in the comparable period ended September 30, 2021. In addition, of the overall increase, approximately $0.1 million was attributable to our audio segment, primarily due to increases in political advertising revenue and local advertising revenue, partially offset by a decrease in national advertising revenue. The overall increase was partially offset by a decrease of approximately $0.8 million attributable to our television segment, primarily due to decreases in local and national advertising revenue, and a decrease in retransmission consent revenue. These decreases were mainly attributed to the expiration of our Univision and UniMás network affiliation agreements in Orlando, Tampa and Washington, D.C. on December 31, 2021. The decrease in our television segment revenue was partially offset by increases in political advertising revenue and spectrum usage rights revenue.

Cost of revenue in the third quarter of 2022 totaled $157.1 million, up 26% from $124.3 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to our investment in a variable interest entity during the third quarter of 2022 and our acquisition of 365 Digital during the fourth quarter of 2021, neither of which incurred cost of revenue for us in the comparable period ended September 30, 2021.

Operating expenses in the third quarter of 2022 totaled $49.3 million, up 14% from $43.1 million in the prior-year period. Of the overall increase, approximately $5.9 million was attributable to our digital segment and was primarily due to an increase in expenses associated with the increase in digital advertising revenue, an increase in salary expense and our investment in a variable interest entity during the third quarter of 2022 and our acquisition of 365 Digital during the fourth quarter of 2021, which did not incur operating expenses for us in the comparable period. Additionally, of the overall increase in operating expenses, approximately $0.4 million was attributable to our audio segment primarily due to an increase in expenses associated with the increase in local advertising revenue. The overall increase in operating expenses was partially offset by a decrease of approximately $0.1 million that was attributable to our television segment primarily due to a decrease in expenses associated with the decrease in local and national advertising revenue, partially offset by an increase in rent expense and an increase in bad debt expense.

Corporate expenses in the third quarter of 2022 totaled $9.5 million, up 31% from $7.3 million in the prior-year period. The increase was primarily due to increases in non-cash stock-based compensation and an increase in salaries.

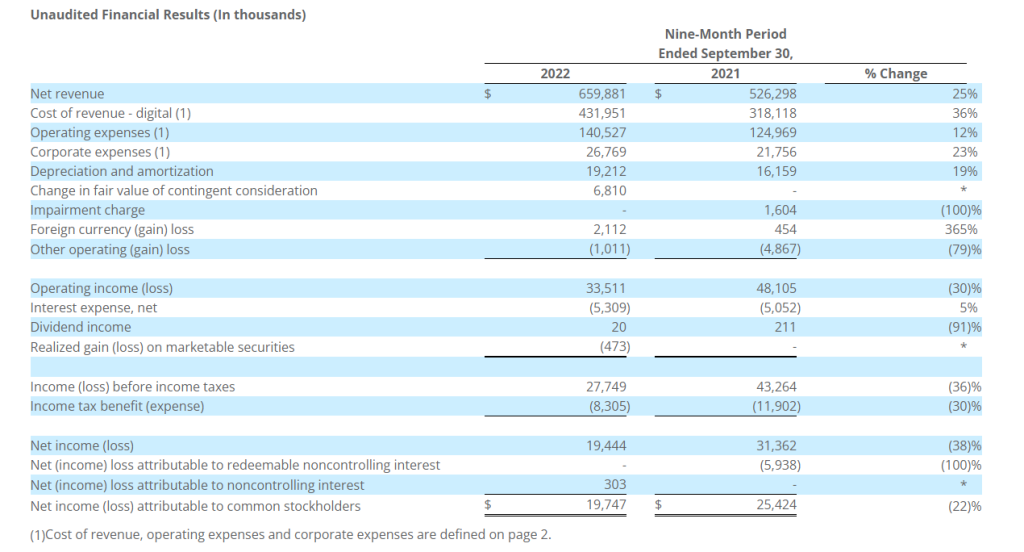

Net revenue for the nine-month period of 2022 totaled $659.9 million, up 25% from $526.3 million in the prior-year period. Of the overall increase, approximately $139.1 million was attributable to our digital segment and was primarily due to advertising revenue growth from our digital commercial partnerships business. In addition, the increase in net revenue in our digital segment was due to our investment in a variable interest entity and our acquisition of 365 Digital during the third quarter of 2022 and fourth quarter of 2021, respectively, neither of which contributed to net revenue in the comparable period ended September 30, 2021, and due to our acquisition of MediaDonuts during the third of 2021, which only partially contributed to net revenue in the comparable period ended September 30, 2021. Additionally, of the overall increase, approximately $2.1 million was attributable to our audio segment, primarily due to increases in political advertising revenue and local advertising revenue, partially offset by a decrease in national advertising revenue. The overall increase was partially offset by a decrease of approximately $7.7 million attributable to our television segment, primarily due to decreases in local and national advertising revenue, and a decrease in retransmission consent revenue. These decreases were mainly attributed to the expiration of our Univision and UniMás network affiliation agreements in Orlando, Tampa and Washington, D.C. on December 31, 2021. The decrease in our television segment revenue was partially offset by increases in political advertising revenue and spectrum usage rights revenue.

Cost of revenue for the nine-month period of 2022 totaled $432.0 million, up 36% from $318.1 million in the prior-year period. The increase was primarily due to increased cost of revenue related to advertising revenue growth from our digital commercial partnerships business, and due to our investment in a variable interest entity and our acquisition of 365 Digital during the third quarter of 2022 and fourth quarter of 2021, respectively, neither of which incurred cost of revenue for us in the comparable period ended September 30, 2021, and due to our acquisition of MediaDonuts during the third of 2021, which only partially incurred cost of revenue for us in the comparable period ended September 30, 2021.

Operating expenses for the nine-month period of 2022 totaled $140.5 million, up 12% from $125.0 million in the prior-year period. Of the overall increase, approximately $15.5 million was attributable to our digital segment and was primarily due to an increase in expenses associated with the increase in digital advertising revenue and an increase in salary expense. In addition, the increase in operating expenses in our digital segment was due to our investment in a variable interest entity and our acquisition of 365 Digital during the third quarter of 2022 and fourth quarter of 2021, respectively, neither of which incurred operating expenses for us in the comparable period ended September 30, 2021, and due to our acquisition of MediaDonuts during the third of 2021, which only partially incurred operating expenses for us in the comparable period ended September 30, 2021. Additionally, of the overall increase in operating expenses, approximately $0.6 million was attributable to our audio segment primarily due to an increase in expenses associated with the increase in local advertising revenue. The overall increase in operating expenses was partially offset by a decrease of approximately $0.6 million that was attributable to our television segment primarily due to a decrease in expenses associated with the decrease in local and national advertising revenue, partially offset by an increase in rent expense and bad debt expense.

Corporate expenses for the nine-month period of 2022 totaled $26.8 million, up 23% from $21.8 million in the prior-year period. The increase was primarily due to increases in non-cash stock-based compensation and an increase in salaries.

Balance Sheet and Related Metrics

Cash and marketable securities as of September 30, 2022 totaled approximately $164.8 million. Total debt under the Company’s credit agreement was $210.0 million. Net of $75 million of cash and marketable securities, total leverage as defined in the Company’s credit agreement was 1.4 times as of September 30, 2022. Net of total cash and marketable securities, total leverage was 0.5 times.

Notice of Conference Call

Entravision Communications Corporation will hold a conference call to discuss its third quarter 2022 results on Thursday, November 3, 2022 at 4:30 p.m. Eastern Time. To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (Int’l) ten minutes prior to the start time and reference Conference ID number 10171311. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

About Entravision Communications Corporation

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Forward-Looking Statements

This press release contains certain forward-looking statements. These forward-looking statements, which are included in accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, may involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results and performance in future periods to be materially different from any future results or performance suggested by the forward-looking statements in this press release. Although the Company believes the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that actual results will not differ materially from these expectations, and the Company disclaims any duty to update any forward-looking statements made by the Company. From time to time, these risks, uncertainties and other factors are discussed in the Company’s filings with the Securities and Exchange Commission.

IRVING, Texas–(BUSINESS WIRE)– Salem Media Group, Inc. (Nasdaq: SALM) released its results for the three and nine months ended September 30, 2022.

Third Quarter 2022 Results

For the quarter ended September 30, 2022 compared to the quarter ended September 30, 2021:

Consolidated

Total revenue increased 1.3% to $66.9 million from $66.0 million;

Total operating expenses increased 50.7% to $75.6 million from $50.2 million;

Operating expenses, excluding stock-based compensation expense, debt modification costs, gains and losses on the sale or disposition of assets, legal settlement, impairments, depreciation expense and amortization expense (1) increased 10.3% to $60.8 million from $55.2 million;

The company had an operating loss of $8.8 million compared to operating income of $15.8 million;

The company recognized $0.1 million in film distribution income from an unconsolidated equity investment;

The company had a net loss of $11.9 million, or $0.44 net loss per share compared to net income of $22.1 million, or $0.81 net income per diluted share;

EBITDA (1) decreased to $(5.7) million from $30.2 million; and

Adjusted EBITDA (1) decreased 78.8% to $2.3 million from $10.8 million.

Broadcast

Net broadcast revenue increased 3.1% to $51.1 million from $49.6 million;

Station Operating Income (“SOI”) (1) decreased 17.9% to $10.0 million from $12.1 million;

Same Station (1) net broadcast revenue increased 3.2% to $51.1 million from $49.5 million; and

Same Station SOI (1) decreased 16.7% to $10.1 million from $12.1 million.

Digital Media

Digital media revenue decreased 4.3% to $10.2 million from $10.6 million; and

Digital Media Operating Income (1) decreased 21.9% to $1.9 million from $2.4 million.

Publishing

Publishing revenue decreased 3.7% to $5.5 million from $5.7 million; and

Publishing Operating Loss (1) was $1.0 million as compared to publishing operating income of $0.5 million.

Included in the results for the quarter ended September 30, 2022 are:

A $7.7 million ($5.7 million, net of tax, or $0.21 per share) impairment charge to the value of broadcast licenses in Boston, Chicago, Columbus, Dallas, Greenville, Honolulu, Little Rock, Orlando, Philadelphia, Portland, Sacramento, and San Francisco;

A $0.1 million loss on the disposal of assets;

A $3.8 million ($2.8 million, net of tax, or $0.10 per share) legal settlement expense; and

A $0.1 million non-cash compensation charge related to the expensing of stock options.

Included in the results for the quarter ended September 30, 2021 are:

A $2.3 million ($1.7 million, net of tax, or $0.06 per share) charge for debt modification costs. On September 10, 2021, the company refinanced $112.8 million of the 2024 Notes by exchanging into $114.7 million (reflecting a call premium of 1.688%) of 2028 Notes. The transaction was assessed on a lender-specific level and was accounted for as a debt modification in accordance with ASC 470 with $2.3 million of fees paid to third parties included in operating expenses for the period;

A $11.2 million ($8.3 million, net of tax, or $0.30 per diluted share) gain on the forgiveness of PPP loans;

A $0.1 million loss from the early retirement of long-term debt associated with the 2024 Notes;

A $10.6 million ($7.8 million, net of tax, or $0.29 per diluted share) net gain on the disposition of assets relates to a $10.5 million pre-tax gain on the sale of land in Lewisville, Texas, and $0.1 million pre-tax gain on the sale of the Hilary Kramer Financial Newsletter and related assets as well as various other fixed asset disposals; and

A $0.1 million non-cash compensation charge ($0.1 million, net of tax) related to the expensing of stock options.

Per share numbers are calculated based on 27,216,787 diluted weighted average shares for the quarter ended September 30, 2022, and 27,280,949 diluted weighted average shares for the quarter ended September 30, 2021.

Year to Date 2022 Results

For the nine months ended September 30, 2022 compared to the nine months ended September 30, 2021:

Consolidated

Total revenue increased 4.8% to $198.2 million from $189.1 million;

Total operating expenses increased 19.2% to $194.6 million from $163.3 million;

Operating expenses, excluding stock-based compensation expense, debt modification costs, gains and losses on the sale or disposition of assets, legal settlement, impairments, depreciation expense and amortization expense (1) increased 9.2% to $176.6 million from $161.6 million;

The company’s operating income decreased 86.4% to $3.5 million from $25.8 million;

The company recognized $4.0 million in film distribution income from an unconsolidated equity investment;

The company had a net loss of $1.0 million, or $0.04 net loss per share compared to net income of $24.7 million, or $0.91 net income per diluted share;

EBITDA (1) decreased 63.6% to $17.0 million from $46.7 million; and

Adjusted EBITDA (1) decreased 24.3% to $20.8 million from $27.5 million.

Broadcast

Net broadcast revenue increased 8.3% to $152.0 million from $140.4 million;

SOI (1) decreased 6.8% to $31.2 million from $33.5 million;

Same station (1) net broadcast revenue increased 8.1% to $151.6 million from $140.2 million; and

Same station SOI (1) decreased 6.7% to $31.3 million from $33.6 million.

Digital media

Digital media revenue increased 2.3% to $31.3 million from $30.6 million; and

Digital media operating income (1) increased 16.7% to $6.2 million from $5.3 million.

Publishing

Publishing revenue decreased 18.0% to $14.8 million from $18.1 million; and

Publishing Operating Loss (1) was $1.6 million compared to publishing operating income of $1.2 million.

Included in the results for the nine months ended September 30, 2022 are:

A $11.7 million ($8.6 million, net of tax, or $0.32 per share) impairment charge to the value of broadcast licenses in Boston, Chicago, Columbus, Dallas, Greenville, Honolulu, Little Rock, Orlando, Philadelphia, Portland, Sacramento and San Francisco;

A $8.5 million ($6.3 million, net of tax, or $0.23 per diluted share) net gain on the disposition of assets relates primarily to the $6.5 million pre-tax gain on the sale of land used in the company’s Denver, Colorado broadcast operations, the $1.8 million pre-tax gain on sale of land used in the company’s Phoenix, Arizona broadcast operations, and $0.5 million pre-tax gain on the sale of the company’s radio stations in Louisville, Kentucky offset by various fixed asset disposals;

A $18,000 loss on the early retirement of long-term debt associated with the 2024 Notes;

A $4.8 million ($3.5 million, net of tax, or $0.13 per share) legal settlement expense;

A $0.1 million ($0.1 million, net of tax) goodwill impairment charge;

A $0.2 million ($0.2 million, net of tax, or $0.01 per share) charge for debt modification costs; and

A $0.2 million non-cash compensation charge ($0.2 million, net of tax, or $0.01 per share) related to the expensing of stock options.

Included in the results for the nine months ended September 30, 2021 are:

A $2.3 million ($1.7 million, net of tax, or $0.06 per share) charge for debt modification costs. On September 10, 2021, the company refinanced $112.8 million of the 2024 Notes by exchanging into $114.7 million (reflecting a call premium of 1.688%) of 2028 Notes. The transaction was assessed on a lender-specific level and was accounted for as a debt modification in accordance with ASC 470 with $2.3 million of fees paid to third parties included in operating expenses for the period;

A $11.2 million ($8.3 million, net of tax, or $0.30 per diluted share) gain on the forgiveness of PPP loans;

A $0.1 million loss from the early retirement of long-term debt associated with the 2024 Notes;

A $10.6 million ($7.8 million, net of tax, or $0.29 per diluted share) net gain on the disposition of assets relating to a $10.5 million pre-tax gain on the sale of land in Lewisville, Texas, a $0.5 million pre-tax gain on the sale of Singing News Magazine and Singing News Radio and a $0.1 million pre-tax gain on the sale of the Hilary Kramer Financial Newsletter and related assets offset by $0.4 million additional loss recorded at closing on the sale of radio station WKAT-AM and FM translator in Miami, Florida and various fixed asset disposals; and

A $0.2 million non-cash compensation charge ($0.2 million, net of tax, or $0.01 per share) related to the expensing of stock options.

Per share numbers are calculated based on 27,202,983 diluted weighted average shares for the nine months ended September 30, 2022, and 27,217,382 diluted weighted average shares for the nine months ended September 30, 2021.

Balance Sheet

As of September 30, 2022, the company had $114.7 million outstanding on the 7.125% senior secured notes due 2028 (“2028 Notes”) and $44.7 million outstanding on 6.75% senior secured notes due 2024 (“2024 Notes”).

Acquisitions and Divestitures

The following transactions were completed since July 1, 2022:

On October 1, 2022, the company acquired websites and the related assets of DayTradeSPY for $0.6 million in cash. As part of the purchase agreement, the company may pay up to an additional $1.0 million of cash in contingent earn-out consideration within one-year of the closing date based on the achievement of certain revenue benchmarks.

Pending Transactions

On September 29, 2022, the company entered into an Asset Purchase Agreement (“APA”) to acquire radio station WMYM-AM and an FM translator in Miami, Florida for $5.0 million. The company paid $0.3 million of cash into an escrow account and plans to operate the radio stations under a Time Brokerage Agreement beginning on November 16, 2022.

On September 22, 2022, the company entered into an APA to acquire radio stations WWFE-AM, WRHC-AM and two FM translators in Miami, Florida for $5.0 million.

On June 2, 2021, the company entered into an APA to acquire radio station KKOL-AM in Seattle, Washington for $0.5 million. The company paid $0.1 million of cash into an escrow account and began operating the station under a Local Marketing Agreement on June 7, 2021.

Conference Call Information

Salem will host a teleconference to discuss its results on November 3, 2022 at 4:00 p.m. Central Time. To access the teleconference, please dial (888) 770-7291, and then ask to be joined into the Salem Media Group Third Quarter 2022 call or listen via the investor relations portion of the company’s website, located at investor.salemmedia.com. A replay of the teleconference will be available through November 17, 2022 and can be heard by dialing (800) 770-2030, passcode 2413416 or on the investor relations portion of the company’s website, located at investor.salemmedia.com.

Follow us on Twitter @SalemMediaGrp.

Fourth Quarter 2022 Outlook

For the fourth quarter of 2022, the company is projecting total revenue to decrease between 3% and 5% from fourth quarter 2021 total revenue of $69.1 million. This decrease is due largely to the fact that Regnery had an extremely strong fourth quarter in book sales last year. The company is also projecting operating expenses before gains or losses on the sale or disposal of assets, stock-based compensation expense, legal settlement, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation expense and amortization expense (“Recurring Operating Expenses”) to increase between 4% and 7% compared to the fourth quarter of 2021 Recurring Operating Expenses of $58.3 million.

A reconciliation of Recurring Operating Expenses to the most directly comparable GAAP measure is not available without unreasonable efforts on a forward-looking basis due to the potential high variability, complexity and low visibility with respect to the charges excluded from this non-GAAP financial measure, in particular, the change in the estimated fair value of earn-out consideration, impairments and gains or losses from the disposition of fixed assets. The company expects the variability of the above charges may have a significant, and potentially unpredictable, impact on its future GAAP financial results.

About Salem Media Group, Inc.

Salem Media Group is America’s leading multimedia company specializing in Christian and conservative content, with media properties comprising radio, digital media and book and newsletter publishing. Each day Salem serves a loyal and dedicated audience of listeners and readers numbering in the millions nationally. With its unique programming focus, Salem provides compelling content, fresh commentary and relevant information from some of the most respected figures across the Christian and conservative media landscape. Learn more about Salem Media Group, Inc. at www.salemmedia.com, Facebook and Twitter.

Forward-Looking Statements

Statements used in this press release that relate to future plans, events, financial results, prospects or performance are forward-looking statements as defined under the Private Securities Litigation Reform Act of 1995. Actual results may differ materially from those anticipated as a result of certain risks and uncertainties, including but not limited to the ability of Salem to close and integrate announced transactions, market acceptance of Salem’s radio station formats, competition from new technologies, inflation and other adverse economic conditions, and other risks and uncertainties detailed from time to time in Salem’s reports on Forms 10-K, 10-Q, 8-K and other filings filed with or furnished to the Securities and Exchange Commission. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Salem undertakes no obligation to update or revise any forward-looking statements to reflect new information, changed circumstances or unanticipated events.

(1) Regulation G

Management uses certain non-GAAP financial measures defined below in communications with investors, analysts, rating agencies, banks and others to assist such parties in understanding the impact of various items on its financial statements. The company uses these non-GAAP financial measures to evaluate financial results, develop budgets, manage expenditures and as a measure of performance under compensation programs.

The company’s presentation of these non-GAAP financial measures should not be considered as a substitute for or superior to the most directly comparable financial measures as reported in accordance with GAAP.

Regulation G defines and prescribes the conditions under which certain non-GAAP financial information may be presented in this earnings release. The company closely monitors EBITDA, Adjusted EBITDA, Station Operating Income (“SOI”), Same Station net broadcast revenue, Same Station broadcast operating expenses, Same Station Operating Income, Digital Media Operating Income, Publishing Operating Income (Loss), and operating expenses excluding gains or losses on the disposition of assets, stock-based compensation, changes in the estimated fair value of contingent earn-out consideration, impairments, depreciation and amortization, all of which are non-GAAP financial measures. The company believes that these non-GAAP financial measures provide useful information about its core operating results, and thus, are appropriate to enhance the overall understanding of its financial performance. These non-GAAP financial measures are intended to provide management and investors a more complete understanding of its underlying operational results, trends and performance.

The company defines Station Operating Income (“SOI”) as net broadcast revenue minus broadcast operating expenses. The company defines Digital Media Operating Income as net Digital Media Revenue minus Digital Media Operating Expenses. The company defines Publishing Operating Income (Loss) as net Publishing Revenue minus Publishing Operating Expenses. The company defines EBITDA as net income before interest, taxes, depreciation, and amortization. The company defines Adjusted EBITDA as EBITDA before gains or losses on the disposition of assets, before debt modification costs, before changes in the estimated fair value of contingent earn-out consideration, before impairments, before net miscellaneous income and expenses, before (gain) loss on early retirement of long-term debt and before non-cash compensation expense. SOI, Digital Media Operating Income, Publishing Operating Income (Loss), EBITDA and Adjusted EBITDA are commonly used by the broadcast and media industry as important measures of performance and are used by investors and analysts who report on the industry to provide meaningful comparisons between broadcasters. SOI, Digital Media Operating Income, Publishing Operating Income (Loss), EBITDA and Adjusted EBITDA are not measures of liquidity or of performance in accordance with GAAP and should be viewed as a supplement to and not a substitute for or superior to its results of operations and financial condition presented in accordance with GAAP. The company’s definitions of SOI, Digital Media Operating Income, Publishing Operating Income (Loss), EBITDA and Adjusted EBITDA are not necessarily comparable to similarly titled measures reported by other companies.

The company defines Same Station net broadcast revenue as broadcast revenue from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station broadcast operating expenses as broadcast operating expenses from its radio stations and networks that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. The company defines Same Station SOI as Same Station net broadcast revenue less Same Station broadcast operating expenses. Same Station operating results include those stations that the company owns or operates in the same format on the first and last day of each quarter, as well as the corresponding quarter of the prior year. Same Station operating results for a full calendar year are calculated as the sum of the Same Station-results for each of the four quarters of that year. The company uses Same Station operating results, a non-GAAP financial measure, both in presenting its results to stockholders and the investment community, and in its internal evaluations and management of the business. The company believes that Same Station operating results provide a meaningful comparison of period over period performance of its core broadcast operations as this measure excludes the impact of new stations, the impact of stations the company no longer owns or operates, and the impact of stations operating under a new programming format. The company’s presentation of Same Station operating results are not intended to be considered in isolation or as a substitute for the financial information prepared and presented in accordance with GAAP. The company’s definition of Same Station operating results is not necessarily comparable to similarly titled measures reported by other companies.

For all non-GAAP financial measures, investors should consider the limitations associated with these metrics, including the potential lack of comparability of these measures from one company to another.

The Supplemental Information tables that follow the condensed consolidated financial statements provide reconciliations of the non-GAAP financial measures that the company uses in this earnings release to the most directly comparable measures calculated in accordance with GAAP. The company uses non-GAAP financial measures to evaluate financial performance, develop budgets, manage expenditures, and determine employee compensation. The company’s presentation of this additional information is not to be considered as a substitute for or superior to the directly comparable measures as reported in accordance with GAAP.

SANTA MONICA, Calif.–(BUSINESS WIRE)– Entravision (NYSE: EVC), a leading global advertising solutions, media and technology company, announced that it will release its third quarter 2022 financial results after market close on Thursday, November 3, 2022. The Company will host a conference call that day at 4:30 p.m. Eastern Time to discuss the third quarter 2022 results.

To access the conference call, please dial (844) 836-8739 (U.S.) or (412) 317-5440 (International) ten minutes prior to the start time. The call will also be available via live webcast on the investor relations portion of the Company’s website located at www.entravision.com.

If you cannot listen to the conference call at its scheduled time, there will be a replay available through Thursday, November 17, 2022 which can be accessed by dialing (844) 512-2921 (U.S.) or (412) 317-6671 (International) and entering the passcode 10171311. The webcast will also be archived on the Company’s website.

About Entravision

Entravision is a leading global advertising, media and ad-tech solutions company connecting brands to consumers by representing top platforms and publishers. Our dynamic portfolio includes digital, television and audio offerings. Digital, our largest revenue segment, is comprised of four business units: our digital sales representation business; Smadex, our programmatic ad purchasing platform; our branding and mobile performance solutions business; and our digital audio business. Through our digital sales representation business, we connect global media companies such as Meta, Twitter, TikTok and Spotify with advertisers in primarily emerging growth markets worldwide. Smadex is our mobile-first demand side platform, enabling advertisers to execute performance campaigns using machine learning. We also offer a branding and mobile performance solutions business, which provides managed services to advertisers looking to connect with global consumers, primarily on mobile devices, and our digital audio business provides digital audio advertising solutions for advertisers in the Americas. In addition to digital, Entravision has 49 television stations and is the largest affiliate group of the Univision and UniMás television networks. Entravision also manages 45 primarily Spanish-language radio stations that feature nationally recognized, Emmy award-winning talent. Shares of Entravision Class A Common Stock trade on the NYSE under ticker: EVC. Learn more about our offerings at entravision.com or connect with us on LinkedIn and Facebook.

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview. Develop a shopping list.This report focuses on the looming economic recession and how investors should position portfolios for the prospect of an economic recovery. But, a more important theme of this report is for investors not to look for the past leaders in the industry as the best way to play a rebound. In this report, we look beyond a rebound play and focus on our favorite growth plays.

Digital Media: The smaller beat the goliaths.Two of our current favorites in the AdTech and MarTech industries performed better than most of its respective peers in the quarter. Can the momentum continue?

Television Broadcasting: Will political carry the quarter? With signs of weakening National advertising, broadcasters are looking forward toward Q4 Political as an offset. Political advertising, however, is not usually evenly spent across all markets. There may be winners and some losers.

Radio Broadcasting: Polishing its tarnished image.One of the epic fails of the radio industry has been Audacy, once one of the leadership companies of the industry. The AUD shares are down a staggering 95% from highs in March 2021. New industry leaders are emerging and they are not focused on radio. We highlight a few of our current favorites.

Publishing: Once a leader, now a loser.It is hard to believe that Gannett was once a $90 stock and held a record for one of the longest strings of quarterly earnings gains in the S&P 500 Index. The shares are down 80% from year earlier highs to near $1.37. We believe that investors should take a look at a company that has developed into an impressive Digital Media publisher.

Overview

Develop A Shopping List

The best time to buy stocks is typically in the midst of an economic recession. Investors begin to look beyond the economic weakness and begin positioning portfolios for an economic rebound. The hard part is determining when the economy is in the middle of the downturn. It appears by all standard definitions of an economic downturn that the U.S. is in an economic recession. But, how long will a downturn last? Should investors try to be cute to predict the midpoint of the downturn?

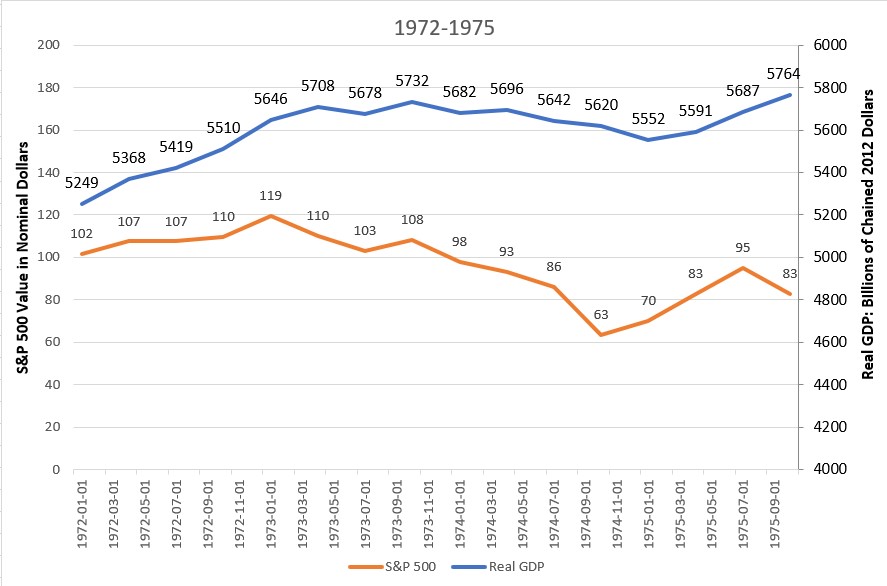

Many economic pundits paint the current state of the economy against the canvas of the 1970s, a period of high inflation and low economic growth. There are many similarities. The Federal Reserve in the early 70s was willing to provide cheap money to fuel the economy, without much concern about inflation. In the second half of the 70s, the economy was rocked by fuel supply shortages and high inflation. During the Covid pandemic, both fiscal and monetary policy was designed to provide liquidity and to make sure that people were able to pay their bills during the economic lockdowns. This had the affect of increasing personal income, even though GDP declined 31.4% in 2020. As the economy reopened, there was significant demand for goods and services, some of which were in short supply because of the previous and recurring economic lock downs. Simplistically, this fueled inflation, high demand with a consumer that had disposable income and limited supply.

As Figure #1 Early 1970s chart illustrates, the US economy grew 9.8%, as measured by real GDP, from January 1972 to September 1975. Notably, the stock market, as measured by the S&P 500 Index, declined a significant 18.6%. This was a period marked by rising inflation due to government spending. The inflation rate, as measured by the US Bureau of Labor Statistics, was a reasonable 3.3% in 1972, but increased to 11.1% in 1974 and then moderated slightly to 9.1% in 1975. The inflation rate remained above 5% for the following 3 years.

Figure #1 Early 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

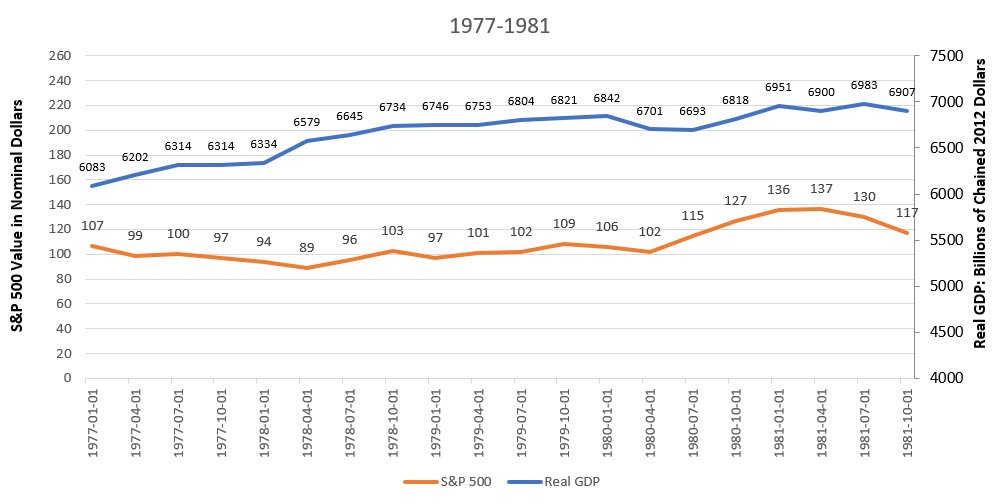

Given the current state of rising energy prices, many pundits paint the current US economic plight similar to the period of fuel shortages of the late 1970s. As Figure #2 Late 1970s illustrates, the US economy, as measured by real GDP, grew 13.5% from January 1977 to October 1981, an average of slightly more than 3% per year. Notably, inflation increased significantly, from 6.5% in 1977 to 11.3% in 1979, followed by 13.5% in 1980, and 10.3% in 1981. The stock market, as measured by the S&P 500 Index, did not react well, up 9.3% from January 1977 to October 1981, an average of 2.3% growth.

Figure #2 Late 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

So, where are we now? In the present, the Covid induced government spending and stimulus related fiscal policy, large spending on the Ukraine war, and a Fed unwilling to rein in early signs of inflation has put the US in a dire economic position. Certainly, supply chain shortages contributed to the current rise in inflation, as well. The Fed now appears to have religion on inflation and is aggressively raising interest rates. The Fed indicated that it is willing to create economic pain to arrest inflationary pressures. Most certainly this will cause additional economic weakness. The stock market in the near to intermediate term will need to digest the likelihood of weakening corporate profits, as well. Furthermore, as it relates to the equity markets, other investment classes, such as bonds, may become more appealing, taking demand from the stock market.

We believe that arresting inflation would set a favorable trajectory for the stock market, as investors position for the prospect of an economic recovery. To some degree, the 24.4% drop in the stock market, as measured by the S&P 500 index, from January 2022 to near current levels, anticipate some of the headwinds for investors described earlier in this report, including weakening corporate profits, the prospect of a further weakened US, and, even global economy, a move toward other investment classes, and stubborn inflation. What is different this time is that the Fed now appears to be aggressively tackling inflation. As such, the 47% drop in the stock market from highs in 1973 to the low in 1974 may not be a prelude to the current environment. It was a different Fed and it took different actions.

We encourage a different approach than trying to time the market. Our advice is for investors to develop a shopping list and begin accumulating. But, be selective.

We believe that the leadership companies of the past economic downturns are not likely to be the best positioned for the looming economic downturn or the recovery. Many of the larger cap names in each sector have fallen on hard times. This is discussed more fully in the following sector reports. Those that appear to be well positioned are companies that have diversified revenue streams, transitioned to faster growth digital businesses, and pared down debt. We encourage investors to focus on these companies given the prospect of faster revenue and cash flow growth coming out of the possible recession. Some of our current favorites include Entravision, Townsquare Media, Salem Media, Harte Hanks, Direct Digital, and Lee Enterprises. These companies are discussed in the following sector summaries.

Internet & Digital Media

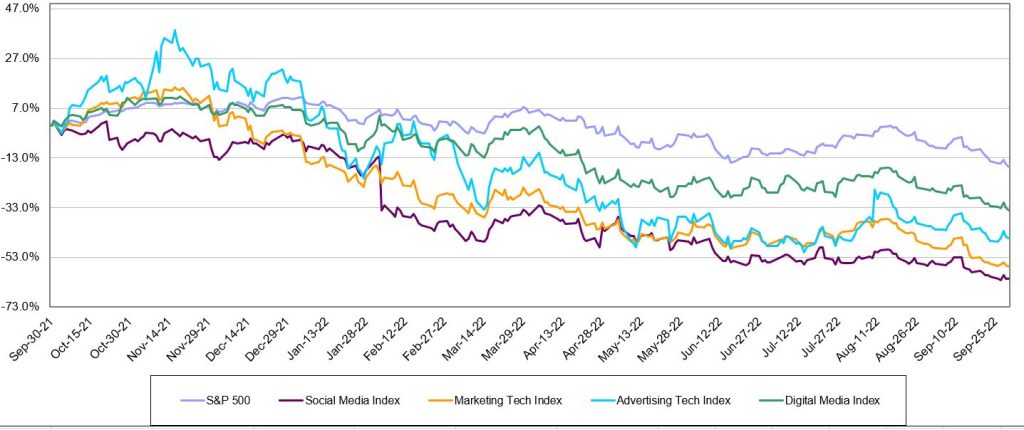

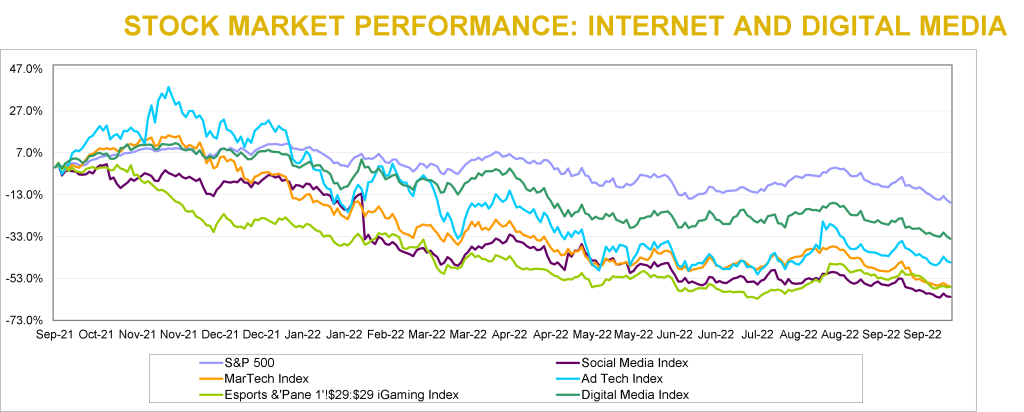

Internet and Digital Media stocks declined for the fourth consecutive quarter in a row, as Figure #3 Internet & Digital Media Stock Performance illustrates. It wasn’t all bad, as Noble’s Ad Tech Index outperformed the general market, as measured by the S&P 500 Index, up +7%. Comparatively, the S&P 500 Index decreased by 5%. Figure #4 Internet & Digital Media Q3 Performance reflects the outperformance of the AdTech sector. AdTech also materially outperformed Noble’s other Internet & Digital Media subsectors, including Noble’s Digital Media Index (-10%); Social Media Index (-15%) and MarTech Index (-16%). Notably, some of our closely followed companies significantly outperformed the respective peer group and outperformed the general market, discussed later in this report.

Figure #3 Internet & Digital Media LTM Stock Performance

Source: Capital IQ

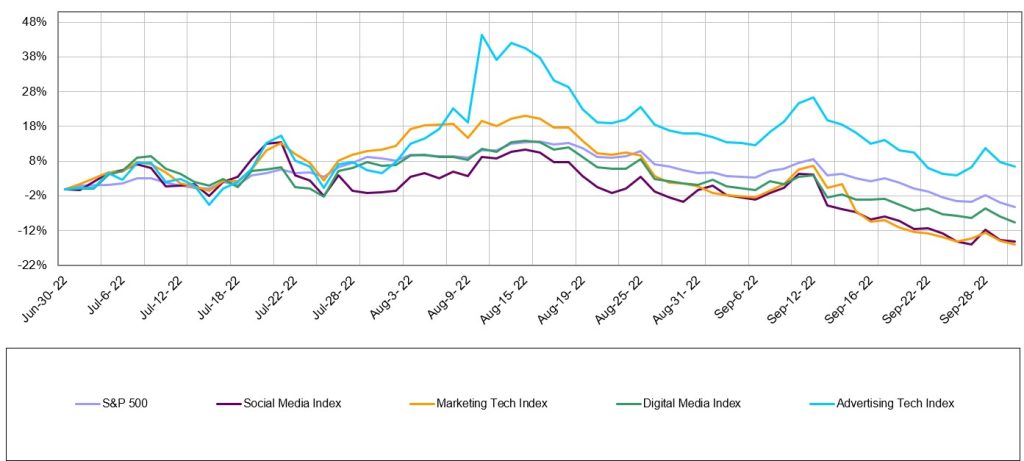

Figure #4 Internet & Digital Media Q3 Stock Performance

Source: Capital IQ

Marketing Technology

Harte Hanks shines in MarTech

The worst performing sector was the MarTech sector, which is also the least profitable sector. This likely explains the sector’s underperformance. Only 4 of the 24 companies we monitor in this sector generate positive EBITDA, and investors migrated away from unprofitable growth stocks towards more profitable companies or defensive sectors that might withstand a recession better. Investors would clearly like to see companies in this sector accelerate their path to profitability, and most companies in the sector are responding accordingly. To be fair, some of the companies that aren’t EBITDA positive do generate positive cash flow from operations, which is a quirk of SaaS software accounting. Of the two dozen companies in this sector, the only stock that was up during the quarter was Harte-Hanks (HHS), whose shares increased by 68%. HHS continues to generate improved operating results while lowering its debt and pension obligations.

MarTech stocks have also been victims of their own success. Earlier this year the group traded at average revenue and EBITDA multiples of 8.5x and 70.8x, respectively. Today the same group trades at average revenue and EBITDA multiples of 4.5x and 30.1x, respectively. Stocks like Shopify (SHOP), and Hubspot (HUBS) entered the year trading at 22.2x and 14.7x 2022E revenues, respectively, and now trade at 5.3x, and 7.7x, respectively. Some of this appears to be a Covid-related hangover: when Covid hit, retail companies needed to emphasize their online channels, and companies like Shopify benefited. As consumers return to stores, growth has moderated. Shopify aside, the broader message investors seem to be sending is that recurring revenues are great, but not if they are paired with EBITDA losses at a time when economy appears to be heading into a potential recession.

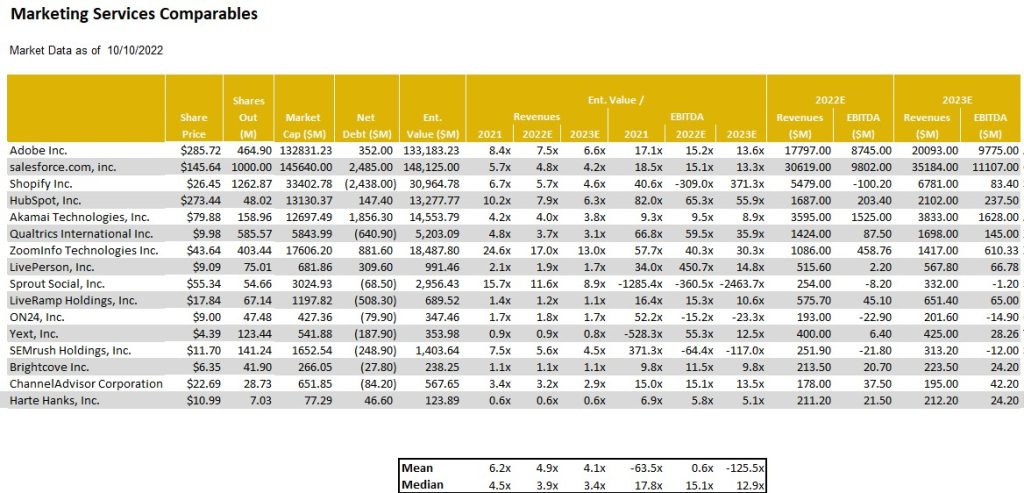

As Figure #5 Marketing Tech Comparables illustrate, the shares of Harte Hanks is among the cheapest in the sector, currently trading at 5.1 times Enterprise Value to our 2023 adj. EBITDA estimate. We believe that the modest stock valuation relative to peers, currently trading on average at 12.9 times, illustrates the head room for the stock in spite of the 68% move in the latest quarter. The shares of HHS continue to be among our favorites in the sector.

Figure #5 Marketing Tech Comparables

Source: Eikon, Company filings and Nobles estimates

Advertising Technology

Direct Digital exceeds peers

Noble’s AdTech Index was the worst performing Index of the group in the second quarter when it was down 39%. As such, it was nice to see a better performance in the third quarter. In addition, Noble Indices are market cap weighted, and we attribute the relative strength of the Ad Tech Index to the performance of The Trade Desk (TTD), the Ad Tech sectors largest market cap company, whose shares were up 42% during the quarter. Other notable performers were Digital Media Solutions (DMS; +73%) which announced a deal to be taken private, and Zeta Global (ZETA; +46%), whose 2Q results significantly exceeded guidance. Despite the relative strength of the sector, returns were not broad-based: only 9 of the 23 stocks in the Ad Tech sector were up during the quarter.

One of our closely followed companies, Direct Digital (DRCT) had a strong performance, up 75% in the quarter. The company’s second quarter exceeded expectations and the company raised full year 2022 revenue and cash flow guidance by a significant 40%. The company appears to be bucking the downward trend in National advertising, which is reflected in its peer group quarterly performance.

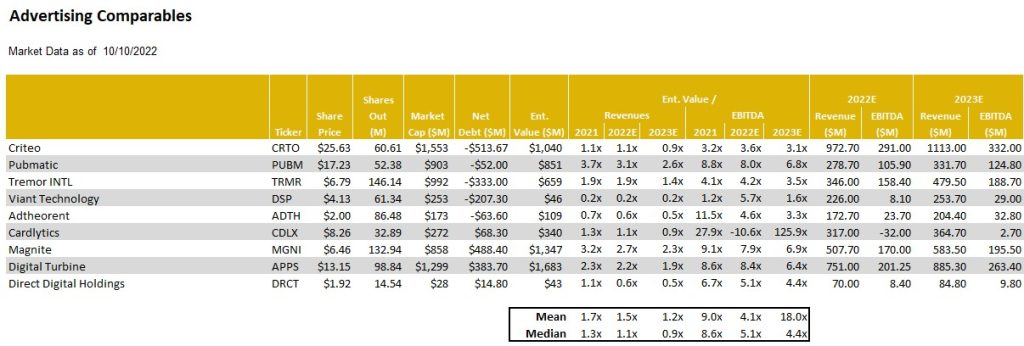

As Figure #6 Advertising Tech Comparables illustrate, Direct Digital Holdings is trading near the averages in terms of Enterprise Value to the 2023 adj. EBITDA estimate. We would note that this valuation is low considering that the company is outperforming its peers. As such, we believe that there is a valuation gap and we continue to view DRCT shares as among our favorites.

Figure #6 Advertising Tech Comparables

Source: Eikon, Company filings and Nobles estimates

Traditional Media

Downward trends, but some bright spots

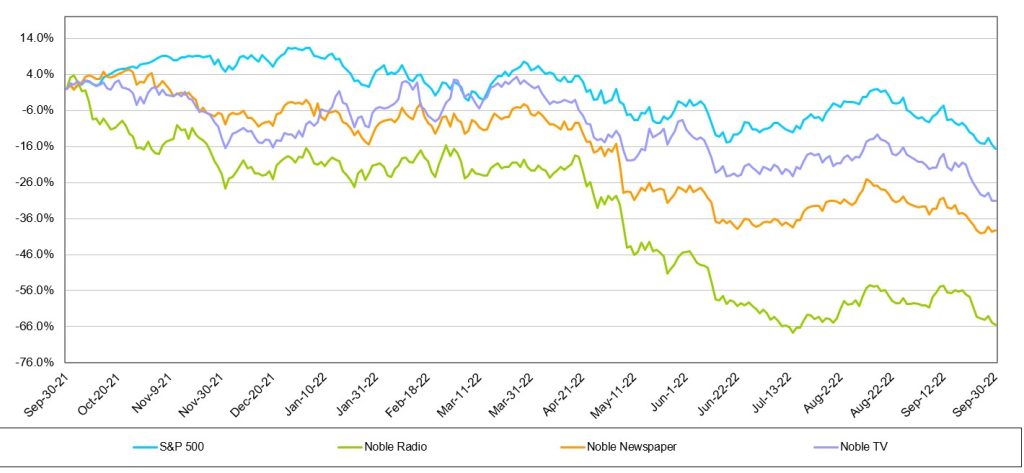

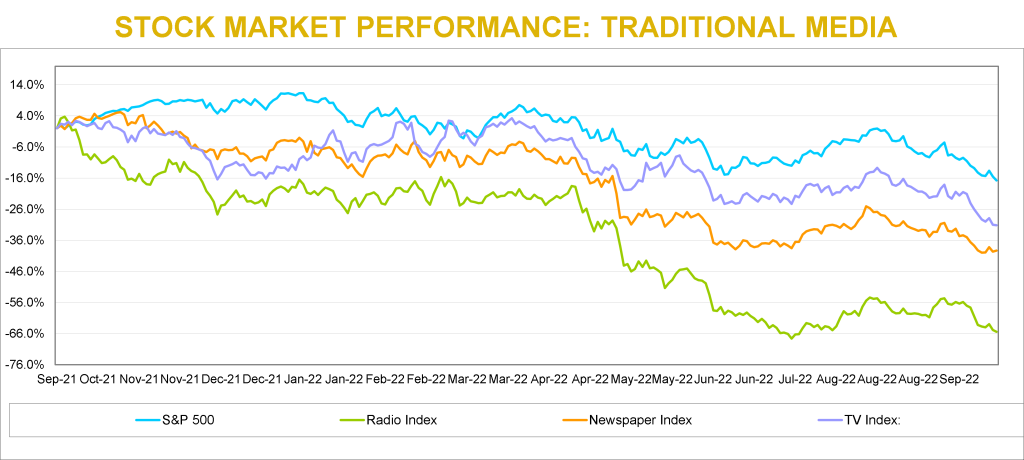

The Traditional Media stocks have had tough sledding this year. As Figure #7 Traditional Media LTM Stock Performance illustrates, all of Noble’s Traditional Media Indices have declined over the past 12 months and each have underperformed the general market. The downward spiral seemed to have moderated somewhat in the third quarter.

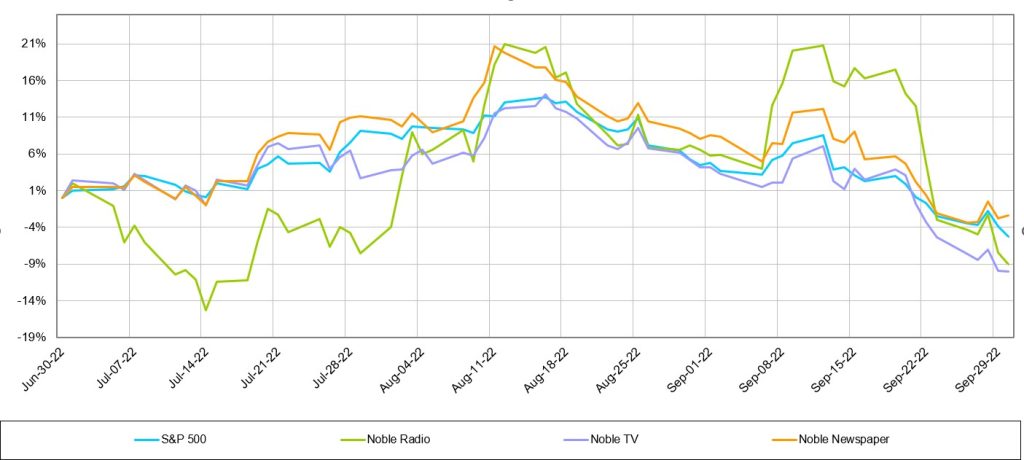

Notably, during the third quarter, many of the stocks had a very nice bounce before resuming a downward trend, as Figure #8 Traditional Media Q3 Stock Performance illustrates. At one point in the latest quarter, stocks were up as high as 30% from the second quarter end. It is important to note that only the Publishing stocks outperformed the general market in the latest quarter. A description of the traditional media sectors follow with our favorite picks for the upcoming quarter and year.

Figure #7 Traditional Media LTM Stock Performance

Source: Capital IQ

Figure #8 Traditional Media Q3 Stock Performance

Source: Capital IQ

Television Broadcasting

Noble’s TV Index dropped 10.1% in the third quarter, underperforming the broader market (-5.3%), illustrated in Figure #8 Traditional Media Q3 Stock Performance. As we indicated in our previous quarterly report, we believe that there would be a trading opportunity in the media stocks. The latest quarter stock performance indicated that. Many of the TV stocks had a strong performance from the end of the second quarter (June 30) to highs achieved in August. Many of the TV stocks increased a strong 25% on average. It is instructive to know that E.W. Scripps had the largest advance from June 30 lows, up 31% to highs achieved August 16. When the industry is in favor, the shares of E.W. Scripps tends to outperform its industry peers. The shares of Entravision (EVC) were the next best performing within the quarter, up 30%, before trading lower and ending down 12%.

The TV stocks were challenged by macro economic pressures such as inflation, rising cost of borrowing, and a Fed determined to curb inflation by slowing the economy. In the end, interest rate increases by the Fed curbed enthusiasm for TV stocks and the Noble TV Index ended the third quarter down.

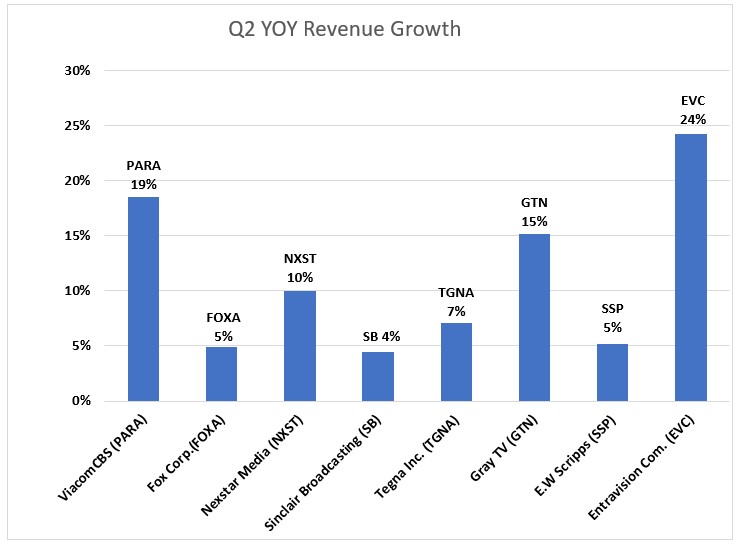

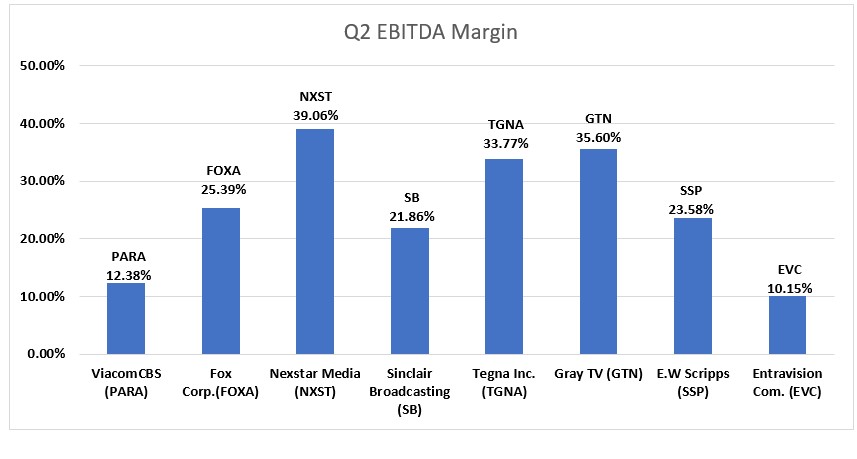

As Figure #9 Q2 YOY Revenue Growth illustrates, the average television company reported 11.1% revenue growth in the latest quarter. Most broadcasters were very optimistic about Political advertising, with some raising forecasts to be near the levels of the Presidential election, a highwater mark. We would note that Entravision had the highest revenue performance in the quarter, up 24%, as the company continues to benefit from its transition toward faster growth Digital, which now accounts for over 80% of its total company revenues.

Industry adj. EBITDA margins were healthy, as Figure #10 Q2 EBITDA margins illustrate, with the average margin for the industry at 25.5%. It is notable to mention that Entravision margins appear to be significantly below that of the industry at 10.1%. Its Digital business is a rep business, and, as such, the company reports revenues on a net basis and not gross revenues. While a rep business tends to be a lower margin business, the reporting of rep revenues gives the appearance of very low margins. The company is in a strong cash flow and free cash flow position.

Most companies will be reporting third quarter financial results in the first two weeks in November. We believe that the third quarter will reflect an influx of Political advertising, even though the lion’s share of the Political advertising likely will fall in the fourth quarter. Consequently, we believe that the third quarter revenue growth will be better than the second quarter, showing some acceleration. With signs of weakening National advertising, and a likely weakening Local advertising environment in some larger markets, broadcasters are looking forward toward Q4 Political as an offset. Many broadcasters indicated that Political advertising may be at record levels in 2022, even higher than the Presidential election year of 2020. Political advertising, however, is not usually evenly spent across all markets. As such, there may be winners and some disappointment.

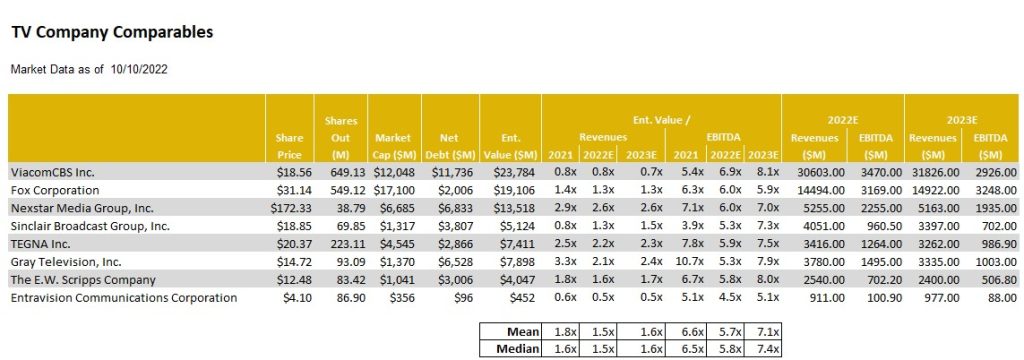

Investors are not encouraged to buy a Television broadcaster on the basis of the upcoming fourth quarter Political advertising influx. There are broader issues at play, like cord cutting, slowing Retransmission revenue growth, and the prospect for a weakening economy. We believe broadcasters with minimal emphasis on National advertising, a larger focus on small to medium size markets and local advertising, are best positioned to weather an economic downturn. We also like companies that do not have high debt leverage. In addition, we like diversified companies that can benefit from cord cutting, like E.W. Scripps, or have diversified revenue streams and large fast growing digital businesses, like Entravision. As Figure #11 TV Industry Comparables illustrate, the shares of Entravision are among the cheapest in the industry and the EVC shares leads our favorites in the industry.

Figure #9 TV Industry Q2 YoY Revenue Growth

Source: Eikon and Company filings

Figure #10 TV Industry Q2 EBITDA Margins

Source: Eikon and Company filings

Figure #11 TV Industry Comparables

Source: Eikon, Company filings and Nobles estimates

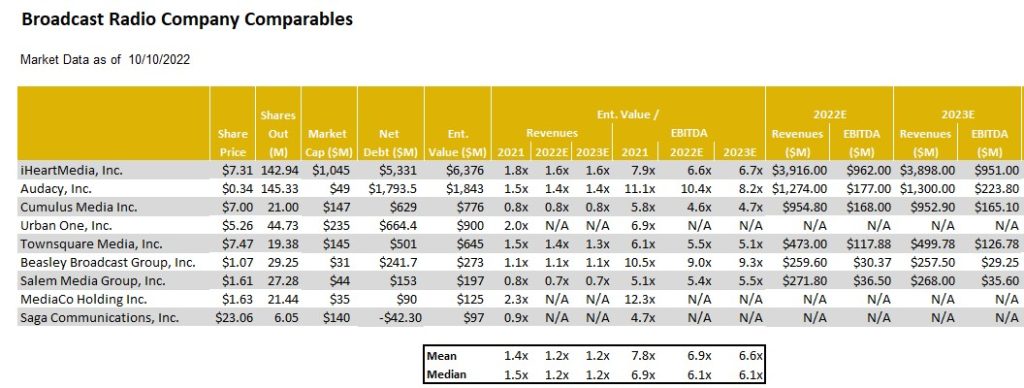

Radio Broadcasting

Polishing its tarnished image

One of the epic fails of the radio industry has been Audacy, once one of the leadership companies in the industry. The AUD shares are down a staggering 95% from highs in March 2021. The poor stock performance reflects the poor revenue and cash flow performance and high debt levels at the company. Recently, the company announced that it plans to sell some of its prized assets, including its podcasting business, Cadence 13, in an effort to more aggressively pare down debt. While Audacy struggles, there are emerging leaders in the industry, many that are not focused on its radio business, discussed later in this report.

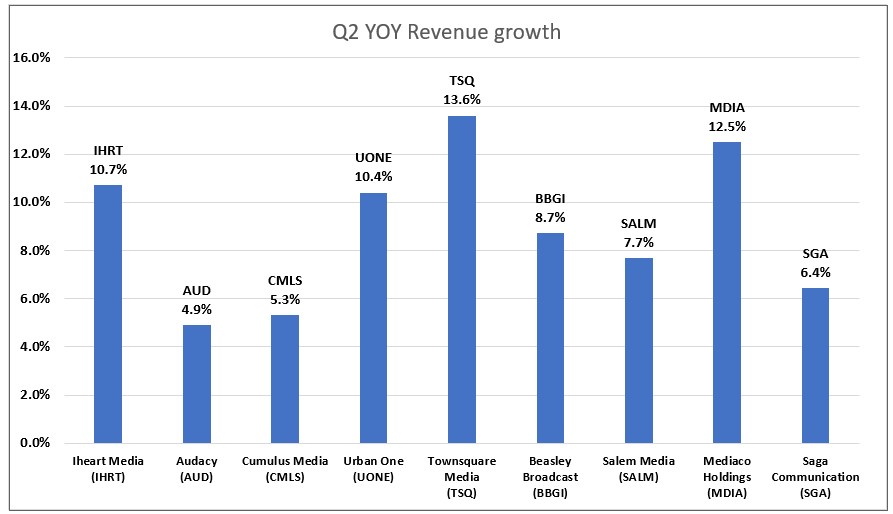

As Figure #12 Radio Industry Q2 YoY Revenue Growth chart illustrates, the average radio revenue grew 8.9%. Companies that were at the top of the list of revenue growth had diversified revenue streams. Townsquare Media was the best performer, with Q2 revenue growth of 13.6%. We believe that Townsquare also benefits from significantly lower National advertising and concentration on less cyclical larger markets. Other diversified companies that performed better than the lower growth companies in the group were Salem Media and Beasley Broadcasting. Salem Media has diversified into content creation and digital media and Beasley recently accelerated its push into Digital Media. Separately, Beasley recently announced a station swap with Audacy, which will enhance its position with its four existing stations in Las Vegas.

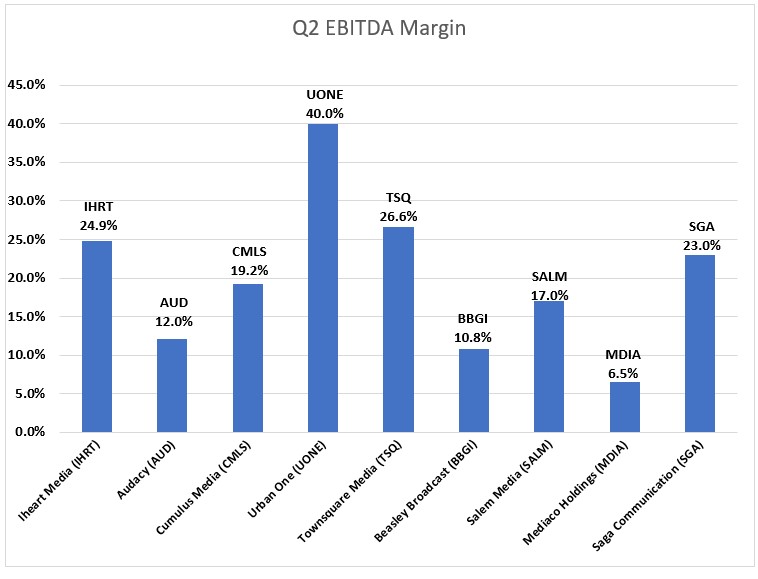

On the margin front, Townsquare Media also was among the leaders in the industry. Notably, Townsquare Media’s digital business carries margins similar to its Radio businesses, near 30%. As such, its investments in Digital Media are not depressing its total company margins. As Figure #13 Q2 Radio Industry EBITDA Margins illustrate, Townsquare’s Q2 adj. EBITDA margins were 26.6%, well above that of the larger industry peers like iHeart (24.9%), Cumulus Media (19.2%), and Audacy (12.0%).

In looking forward toward the upcoming third quarter results, which will be released in coming weeks, we believe that the effects of rising inflation and weakening economy will start to show. Many of the larger broadcasters which focus on larger markets, have national network business, may disappoint. In addition, we believe that there will be spotty Political advertising performances. In our view, the resulting potential weakness in the stocks may create an opportunity to more aggressively accumulate or establish positions.

Radio stocks largely mirrored the performance of the TV industry, falling 9% in the third quarter, illustrated above, in Figure #8 Traditional Media Q3 Stock Performance. Last quarter we pointed out that large industry players such as Audacy and iHeart had an outsized negative impact on the market cap-weighted index. This was due to the stocks being downgraded by a Wal Street firm on the basis of high leverage in a time of recession.

However, there are several broadcasters in the Radio industry with improving leverage profiles. Furthermore, we believe that in a time when traditional radio companies are making a transition to more digitally based revenue sources, investors would do well to differentiate among them on that basis as well. In our view, certain companies are ahead of peers in the digital transformation and are better shielded from certain fundamental headwinds that have traditionally plagued radio broadcasters in prior recessions. We encourage investors to focus on Townsquare Media (TSQ), Salem Media (SALM), and Beasley Broadcasting (BBGI). As Figure #14 Radio Industry Comparables highlights, Townsquare Media, Cumulus Media, and Salem Media are among the cheapest in the group.

Figure #12 Radio Industry Q2 YoY Revenue Growth

Source: Eikon and Company filings

Figure #13 Q2 Radio Industry EBITDA Margins

Source: Eikon and Company filings

Figure #14 Radio Industry Comparables

Source: Eikon, Company filings and Nobles estimates

Publishing

Once a leader, now a loser

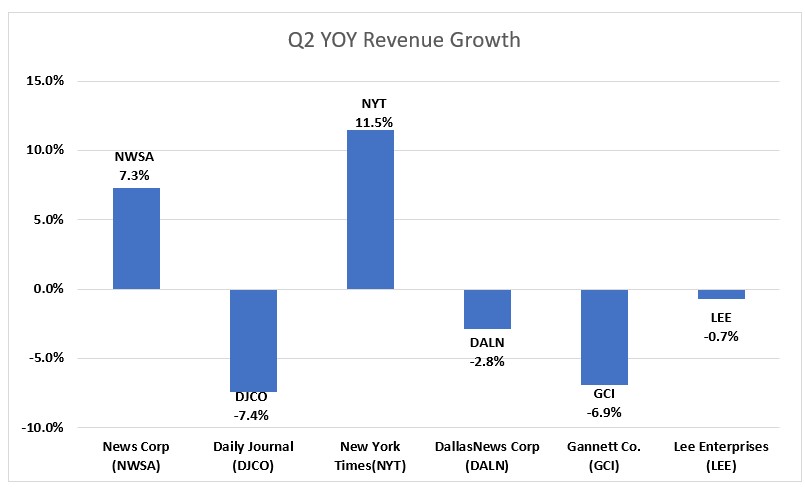

It is hard to believe that Gannett was once a $90 stock and held a record for one of the longest strings of quarterly earnings gains in the S&P 500 Index. The shares are down 80% from year earlier highs to near $1.37. For some anti newspaper investors, this is a “told you so” moment. But, this view missed notable exceptions, like the New York Times, which seemed to transition more quickly toward Digital revenues. There are publishers that are set apart from the weak trends at Gannett and are on a favorable trajectory toward a Digital future. As such, we believe that investors should not throw the baby out with the bathwater or avoid the industry. There are gems here, which is discussed later in this report.

There were sizable differences in the financial performance of the companies in the publishing group. As Figure #15 Publishing Industry Q2 YoY Revenue Performance chart illustrates, Q2 publishing revenue declined on average 1.5%. The notable exceptions to this performance was The New York Times, up 11.5%, News Corp, up 7.3%, and Lee Enterprises, down a modest 0.7%. The improved performance into the ranks of the leaders in the industry is quite notable. Lee’s digital subscriptions currently lead the industry. The company has exceeded all of its peers in terms of digital subscription growth in the past 11 consecutive quarters. Furthermore, over 50% of its advertising is derived from digital. Currently, roughly 30% of the company total revenues are derived from Digital, still short of the 55% at The New York Times, but closing the gap.

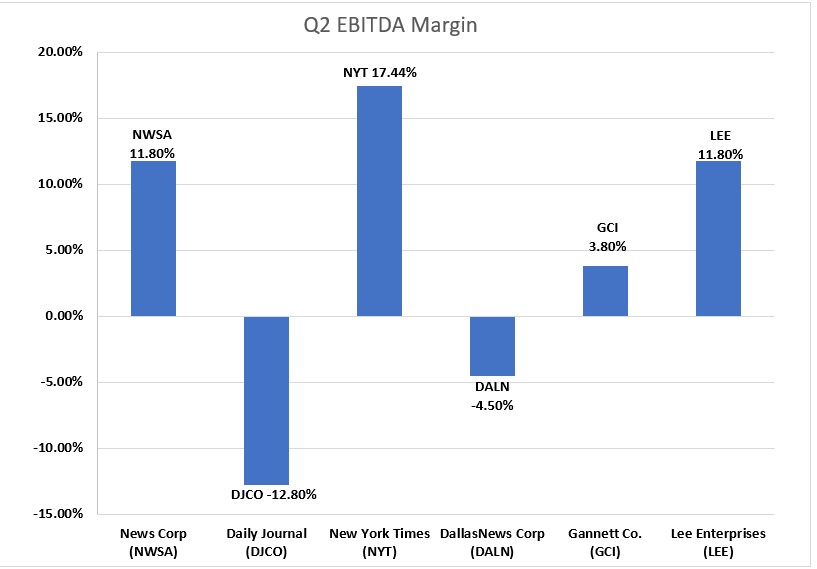

Not only is Lee performing well on the Digital revenue front, it has industry leading margins. As Figure #16 Q2 Publishing Industry EBITDA Margins illustrates, Lee’s Q2 EBITDA margins were 11.8%, in line with News Corp and second only to the New York Times at 17.4%. We believe that margins should improve over time as the company continues to migrate toward a higher digital margin business model.

Illustrated above in Figure #8 Traditional Media Q3 Stock Performance is Noble’s Publishing Index, which decreased a modest 2.4% in the quarter, outperforming the S&P (-5.3%). The relatively favorable performance of the index was primarily due to its largest constituents, News Corp. and The New York Times, which rebounded from -29.7% and -39.1%, respectively in Q2, to -3% and +3%, respectively, in Q3. The average percentage change of the stocks in the industry was -16.2%, more in line with Traditional Media as a whole. One of the poor performing stocks in the index for the quarter was Gannett (GCI) which declined 47%. It was recently reported that the company implemented austerity measures included unpaid leave and voluntary layoffs. In the case of Lee Enterprises, the shares were down a much more modest 7%, more in line with the general market. In our view, the company is expected to report favorable third quarter results and the shares are undervalued.

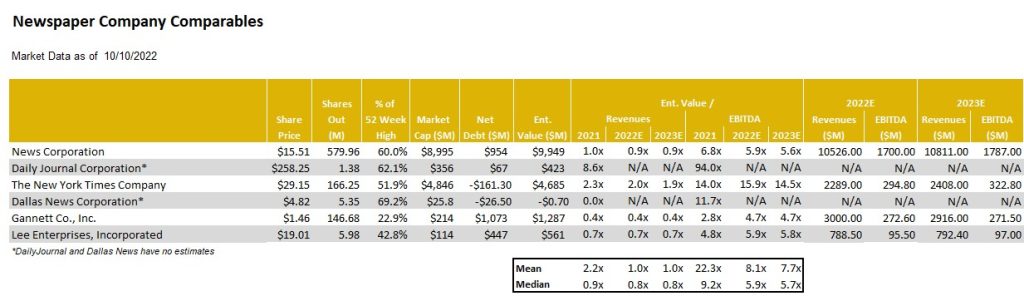

As Figure #17 Publishing Industry Comparables chart illustrates, the LEE shares trade at an average industry multiple of 5.8 times Enterprise Value to our 2023 adj. EBITDA estimate. Notably, the company is closing the gap with its Digital Media revenue contribution to that of New York Times, which is currently trading at an estimated 14.5 times EV to 2023 adj. EBITDA. We believe that the valuation gap with the New York Times should close as well. In recent Lee Enterprise news, a buyout specialist investor filed a 13D and indicated interest in taking the company private.While financial players continue to circle the wagons for Lee, we believe that investors should take note. In our view, the LEE shares are compelling and offer a favorable risk/reward relationship.

Figure #15 Publishing Industry Q2 YoY Revenue Growth

Source: Eikon and Company filings

Figure #16 Q2 Publishing Industry EBITDA Margins

Source: Eikon and Company filings

Figure #17 Publishing Industry Comparables

Source: Eikon, Company filings and Nobles estimates

Reports with important disclosure information of companies highlighted in this report may be found here:

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report. The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report. Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis. Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.” FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public appearance and/or research report.

Ownership and Material Conflicts of Interest Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.

Internet and Digital Media stocks declined for the fourth consecutive quarter in a row. It wasn’t all bad, as two of Noble’s Internet and Digital Media Indices outperformed the broader market (which we define as the S&P 500). Noble’s Ad Tech (+7%) and eSports & iGaming (+7%) Indices each finished up for the quarter, and significantly outperformed the S&P 500 Index in the process, which decreased by 5% in 3Q 2022. These two sectors also materially outperformed Noble’s other Internet & Digital Media subsectors, including Noble’s Digital Media Index (-10%); Social Media Index (-15%) and MarTech Index (-16%).

Noble Indices are market cap weighted, and we attribute the relative strength of the Ad Tech Index to The Trade Desk (TTD), the Ad Tech sector’s largest market cap company, whose shares were up 42% during the quarter. Other notable performers were Digital Media Solutions (DMS; +73%) which announced a deal to be taken private, and Zeta Global (ZETA; +46%), whose 2Q results significantly exceeded guidance. Despite the relative strength of the sector, returns were not broad-based: only 9 of the 23 stocks in the Ad Tech sector were up during the quarter.

The relative strength of Noble’s eSports and iGaming sector was also driven by the largest cap stocks in the sector. Shares of Draft Kings (DKNG) increased by 30% while shares of Flutter Entertainment (ISE:FLTR), the owner of FanDuel, increased by 17%. Shares of sports betting stocks have been battered this year as investors have become skeptical of the time it might take for these companies to reach profitability amidst a backdrop of a slowing economy and consumer propensity to spend.

Year-to-date, FLTR shares are down 19% while DKNG shares are down 45%. Shares are down even more relative to their highs reached in 4Q 2020. Like the Ad Tech sector, the eSports & iGaming sector’s relative strength was not broad-based: only 4 of the 16 stocks in this sector were up during the third quarter, and all of stocks in the sector are down year-to-date.

The worst performing sector was the MarTech sector, which is also the least profitable sector, which likely explains the sector’s underperformance. Only 4 of the 24 companies we monitor in this sector generate positive EBITDA, and investors migrated away from unprofitable growth stocks towards more profitable companies or defensive sectors that might withstand a recession better. Investors would clearly like to see companies in this sector accelerate their path to profitability, and most companies in the sector are responding accordingly. To be fair, some of the companies that aren’t EBITDA positive do generate positive cash flow from operations, which is a quirk of SaaS software accounting. Of the two dozen companies in this sector, the only stock that was up during the quarter was Harte-Hanks (HHS), whose shares increased by 68%. HHS continues to generate improved operating results while lowering its debt and pension obligations.

MarTech stocks have also been victims of their own success. Earlier this year the group traded at average revenue and EBITDA multiples of 8.5x and 70.8x, respectively. Today the same group trades at average revenue and EBITDA multiples of 4.5x and 30.1x, respectively. Stocks like Shopify (SHOP), and Hubspot (HUBS) entered the year trading at 22.2x and 14.7x 2022E revenues, respectively, and now trade at 5.3x, and 7.7x, respectively. Some of this appears to be a Covid-related hangover: when Covid hit, retail companies needed to emphasize their online channels, and companies like Shopify benefited. As consumers return to stores, growth has moderated. Shopify aside, the broader message investors seem to be sending is that recurring revenues are great, but not if they are paired with EBITDA losses at a time when economy appears to be heading into a potential recession.

M&A Continues to Hold Up Well Despite Macro Headwinds

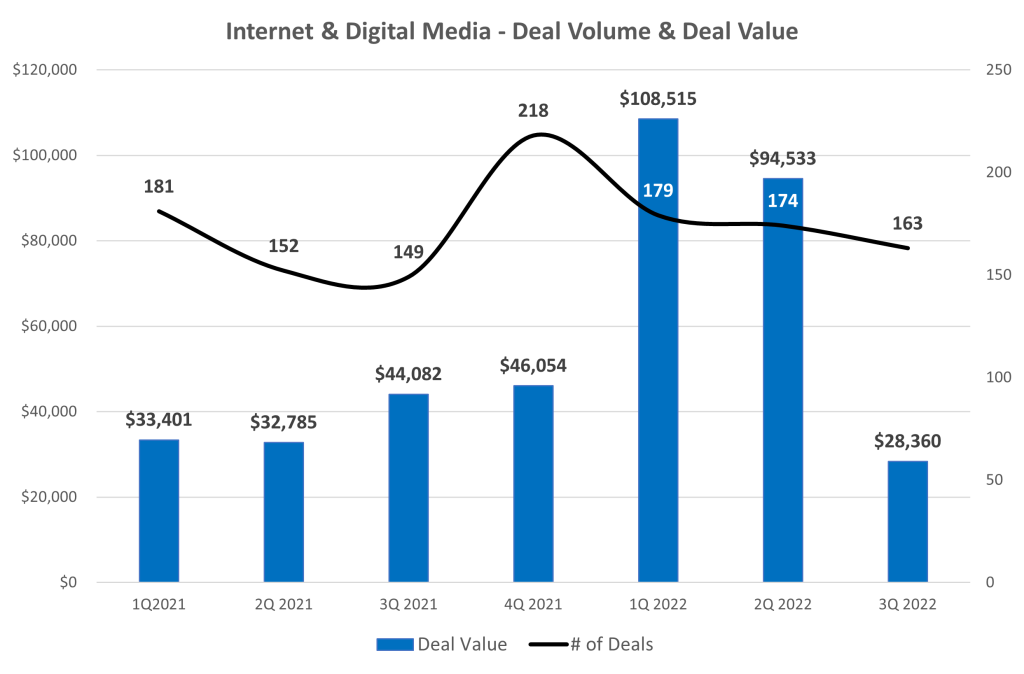

Overall, we are impressed with the resiliency of the M&A marketplace in the Internet & Digital Media sectors. Despite a background that includes public equity market volatility, Fed rate hikes, persistent inflation, contractionary monetary policy, and geopolitical conflict, the M&A marketplace has held up relatively well, all things considered. Noble tracked 163 transactions in the third quarter of 2022 in the TMT sectors we follow, a 9% increase compared to the third quarter of 2021, when we tracked 150 deals, and 6% sequential slowdown compared to 2Q 2022, when we tracked 174 transactions. Year-to-date, the number of M&A transactions is up 7% vs. the year ago period, with 516 announced transactions this year compared to 483 transactions announced through the end of last year’s third quarter.

The real difference between 2022 and 2021 is the dollar value of transactions. Total deal value in 3Q 2022 fell by 36% to $28.4 billion, down from $44.1 billion in 3Q 2021. On a sequential basis, the $28.4 billion in deal value represents a 70% decrease from 2Q 2022 levels of $94.5 billion, nearly half of which reflects Elon Musk’s $46 billion offer to acquire Twitter (TWTR).

In looking at the M&A trends in the chart on the previous page, the biggest change is not the number of deals, but primarily the number of mega-deals. There was only one transaction in 3Q 2022 that was greater than $10 billion dollars: Adobe’s $19.4 billion acquisition of Figma, a collaborative all-in-one design platform. This decline in larger deal activity suggests acquirers are becoming more cautious about making big bets in the current environment or it could also mean that arranging for financing to close on larger deals is becoming more challenging. No doubt the cost to incur debt to close on transactions today are higher than they were just a few months ago, which lowers the return on debt financed M&A transactions. Referencing the Twitter deal again, according to media reports, Apollo Global Management and Sixth Street Partners, which had agreed to provide financing for the Twitter deal when it was first announced in April, are no longer in talks with Elon Musk to provide financing.